AASB and Australian Accounting Practices

VerifiedAdded on 2020/03/04

|18

|2804

|413

AI Summary

This assignment delves into the impact of Australian Accounting Standards Board (AASB) pronouncements on Australian businesses. It analyzes how AASB standards, such as AASB 6 and AASB 136, have affected accounting quality, asset impairments, and disclosure practices. The assignment also explores the broader context of IFRS adoption in Australia and its influence on accounting information usefulness.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in accounting

Name of the Student:

Name of the University:

Author’s Note:

Contemporary Issues in accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary:

The report is prepared to demonstrate the analysis of conceptual framework of the consumer

companies in Australia. It also relates to the discussion of the concepts of produce and their

drawbacks and revised framework. Two organizations selected for the analysis purpose is

Wesfarmers limited and Woolworths. Moreover, analysis is done by depiction of facts from their

respective annual reports for the financial year 2016.

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary:

The report is prepared to demonstrate the analysis of conceptual framework of the consumer

companies in Australia. It also relates to the discussion of the concepts of produce and their

drawbacks and revised framework. Two organizations selected for the analysis purpose is

Wesfarmers limited and Woolworths. Moreover, analysis is done by depiction of facts from their

respective annual reports for the financial year 2016.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................2

Discussion........................................................................................................................................3

Conceptual framework of accounting of Woolworths and Wesfarmers:........................................3

General purpose financial statements as per the framework of AASB:..........................................4

Director’s declaration:.....................................................................................................................7

Analysis of shareholders:.................................................................................................................9

Remuneration report:.....................................................................................................................10

Prudence and its impact on dealing with corporate disparity:.......................................................12

Comparison of the annual report of Wesfarmers and Woolworths Ltd:.......................................13

Recommendation:..........................................................................................................................14

Conclusion:....................................................................................................................................14

Reference:......................................................................................................................................16

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................2

Discussion........................................................................................................................................3

Conceptual framework of accounting of Woolworths and Wesfarmers:........................................3

General purpose financial statements as per the framework of AASB:..........................................4

Director’s declaration:.....................................................................................................................7

Analysis of shareholders:.................................................................................................................9

Remuneration report:.....................................................................................................................10

Prudence and its impact on dealing with corporate disparity:.......................................................12

Comparison of the annual report of Wesfarmers and Woolworths Ltd:.......................................13

Recommendation:..........................................................................................................................14

Conclusion:....................................................................................................................................14

Reference:......................................................................................................................................16

3

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction:

The report is prepared to emphasize on the overall comprehending operational procedures

of the conceptual framework related to Australian Listed companies. Two companies that have

been selected for analysing their conceptual framework by referring to their annual reports are

two consumer companies that are Wesfarmers and Woolworths Limited. Woolworths is the

largest supermarket retail chain operating in Australia and Wesfarmers limited has diverse

business operations and has diverse portfolio of business. The financial declaration of these two

organizations has been demonstrated in the current study with the intention of identifying various

measures taken by the corporations in order to support the directives laid down by Australian

accounting standard board (Barth et al. 2014). For analysing their framework, various extracts

has been taken for their annual report such as director’s declaration, remuneration report and

notes to financial statement.

Discussion

Conceptual framework of accounting of Woolworths and Wesfarmers:

Conceptual framework helps in rendering useful information and depicts the financial

declaration objectives. The framework deals with the enumeration and detection of several

financial statements components as indicated under the financial statements. Sometimes, the

organization fails to provide with the user of their financial statements with the relevant and

useful information.

The fact whether Woolworths and Wesfarmers adhere to the specific requirements of

conceptual framework is revealed by the analysis of their annual report. The overall financial

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction:

The report is prepared to emphasize on the overall comprehending operational procedures

of the conceptual framework related to Australian Listed companies. Two companies that have

been selected for analysing their conceptual framework by referring to their annual reports are

two consumer companies that are Wesfarmers and Woolworths Limited. Woolworths is the

largest supermarket retail chain operating in Australia and Wesfarmers limited has diverse

business operations and has diverse portfolio of business. The financial declaration of these two

organizations has been demonstrated in the current study with the intention of identifying various

measures taken by the corporations in order to support the directives laid down by Australian

accounting standard board (Barth et al. 2014). For analysing their framework, various extracts

has been taken for their annual report such as director’s declaration, remuneration report and

notes to financial statement.

Discussion

Conceptual framework of accounting of Woolworths and Wesfarmers:

Conceptual framework helps in rendering useful information and depicts the financial

declaration objectives. The framework deals with the enumeration and detection of several

financial statements components as indicated under the financial statements. Sometimes, the

organization fails to provide with the user of their financial statements with the relevant and

useful information.

The fact whether Woolworths and Wesfarmers adhere to the specific requirements of

conceptual framework is revealed by the analysis of their annual report. The overall financial

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

CONTEMPORARY ISSUES IN ACCOUNTING

position o organization is depicted by the balance sheet as they involve liabilities and assets as

the two main factors. Other aspects such as inventories, shareholders equity and tangible and

intangibles are also included. The development of conceptual framework is essential for

eliminating the diverse concept relating to prudence.

General purpose financial statements as per the framework of AASB:

The consolidated financial statements of Woolworths have been prepared according to

the ASIC class order 98/100. Furthermore, they are prepared in accordance with the International

financial reporting standard, Australian Accounting standard along with their interpretations and

all other requirements of law. Except for the financial assets sales derivates, all the component

are measured at the fair value and the financial statements have been prepared at historical cost.

AASB 107 of the cash flow statements forms the basis of the cash flow resulting from the

repayment of borrowings and proceeds from borrowing. The entire new and amended accounting

standard and their interpretations have been adopted by organization and they are effective for

the period beginning after June 30th, 2015. The amount recognized in the current period was not

materially affected by any of the amendments and new standards and it is not likely to affect

them in the future period (Camfferman and Zeff 2015).

CONTEMPORARY ISSUES IN ACCOUNTING

position o organization is depicted by the balance sheet as they involve liabilities and assets as

the two main factors. Other aspects such as inventories, shareholders equity and tangible and

intangibles are also included. The development of conceptual framework is essential for

eliminating the diverse concept relating to prudence.

General purpose financial statements as per the framework of AASB:

The consolidated financial statements of Woolworths have been prepared according to

the ASIC class order 98/100. Furthermore, they are prepared in accordance with the International

financial reporting standard, Australian Accounting standard along with their interpretations and

all other requirements of law. Except for the financial assets sales derivates, all the component

are measured at the fair value and the financial statements have been prepared at historical cost.

AASB 107 of the cash flow statements forms the basis of the cash flow resulting from the

repayment of borrowings and proceeds from borrowing. The entire new and amended accounting

standard and their interpretations have been adopted by organization and they are effective for

the period beginning after June 30th, 2015. The amount recognized in the current period was not

materially affected by any of the amendments and new standards and it is not likely to affect

them in the future period (Camfferman and Zeff 2015).

5

CONTEMPORARY ISSUES IN ACCOUNTING

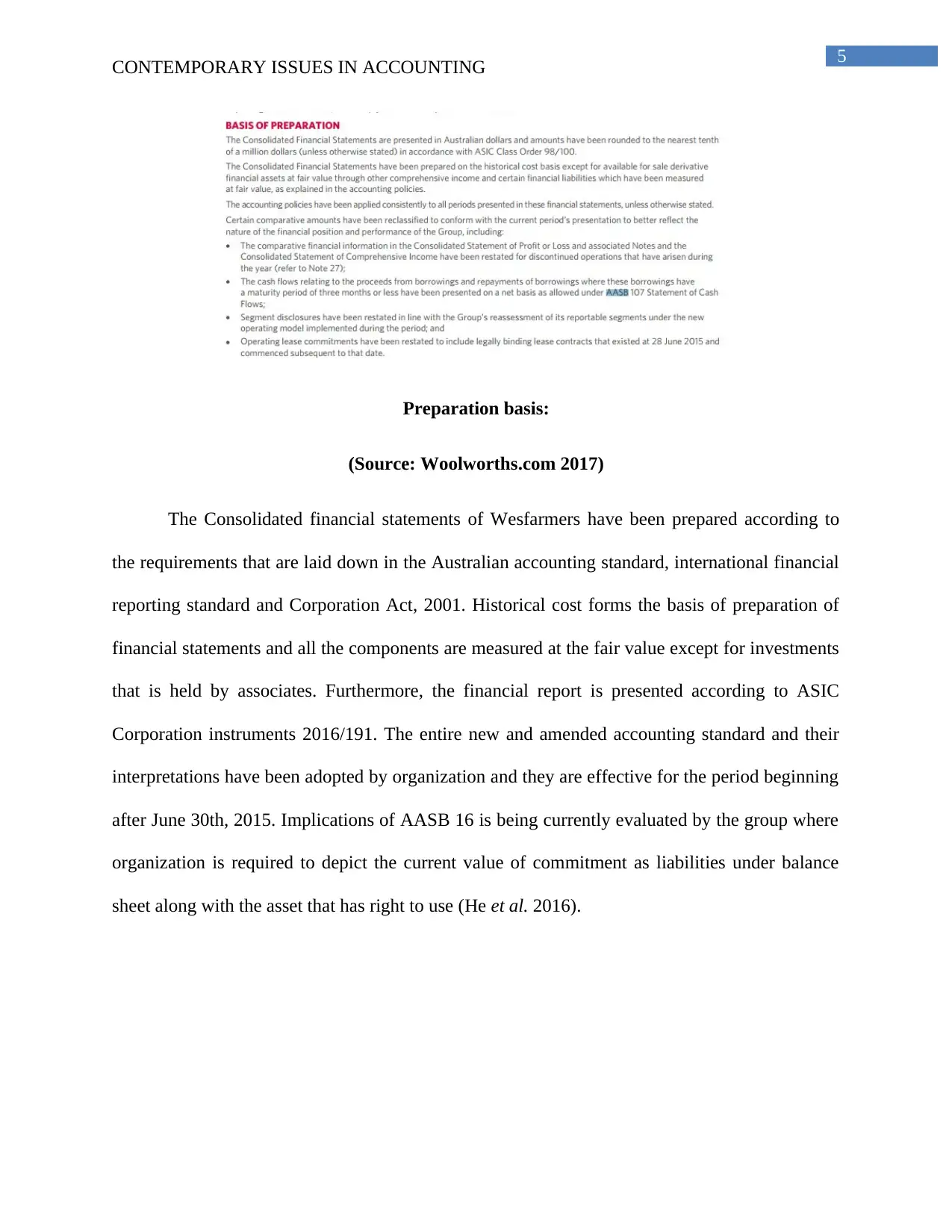

Preparation basis:

(Source: Woolworths.com 2017)

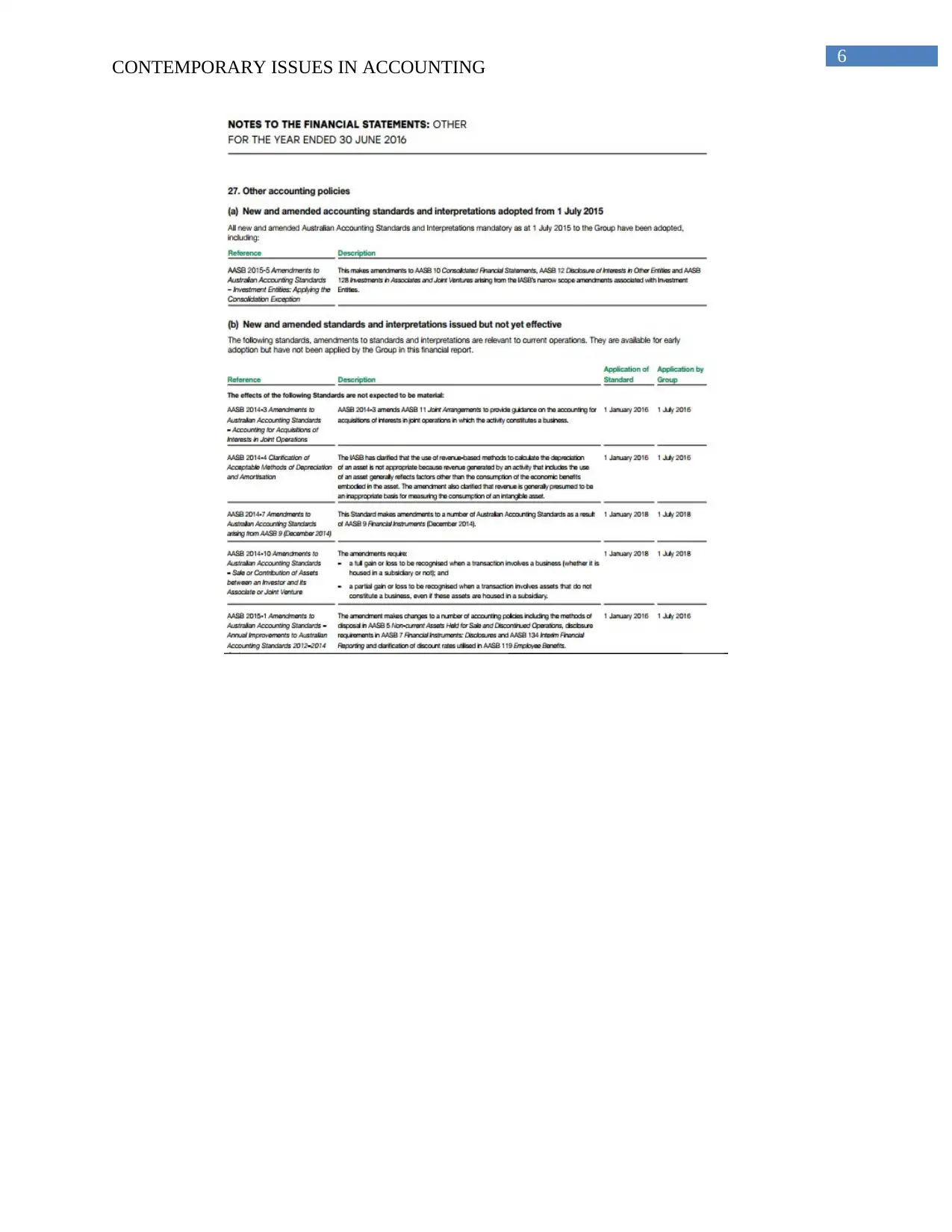

The Consolidated financial statements of Wesfarmers have been prepared according to

the requirements that are laid down in the Australian accounting standard, international financial

reporting standard and Corporation Act, 2001. Historical cost forms the basis of preparation of

financial statements and all the components are measured at the fair value except for investments

that is held by associates. Furthermore, the financial report is presented according to ASIC

Corporation instruments 2016/191. The entire new and amended accounting standard and their

interpretations have been adopted by organization and they are effective for the period beginning

after June 30th, 2015. Implications of AASB 16 is being currently evaluated by the group where

organization is required to depict the current value of commitment as liabilities under balance

sheet along with the asset that has right to use (He et al. 2016).

CONTEMPORARY ISSUES IN ACCOUNTING

Preparation basis:

(Source: Woolworths.com 2017)

The Consolidated financial statements of Wesfarmers have been prepared according to

the requirements that are laid down in the Australian accounting standard, international financial

reporting standard and Corporation Act, 2001. Historical cost forms the basis of preparation of

financial statements and all the components are measured at the fair value except for investments

that is held by associates. Furthermore, the financial report is presented according to ASIC

Corporation instruments 2016/191. The entire new and amended accounting standard and their

interpretations have been adopted by organization and they are effective for the period beginning

after June 30th, 2015. Implications of AASB 16 is being currently evaluated by the group where

organization is required to depict the current value of commitment as liabilities under balance

sheet along with the asset that has right to use (He et al. 2016).

6

CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

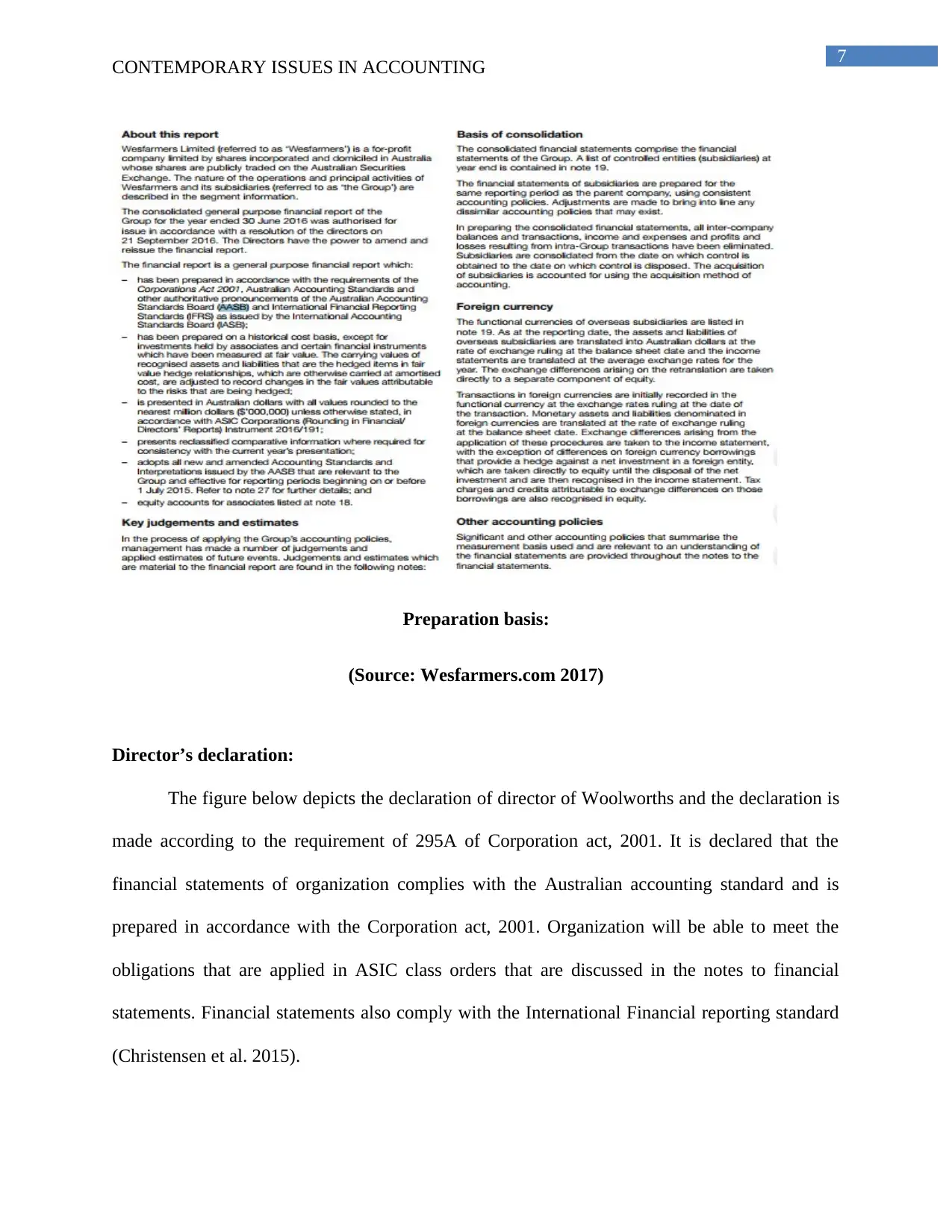

Preparation basis:

(Source: Wesfarmers.com 2017)

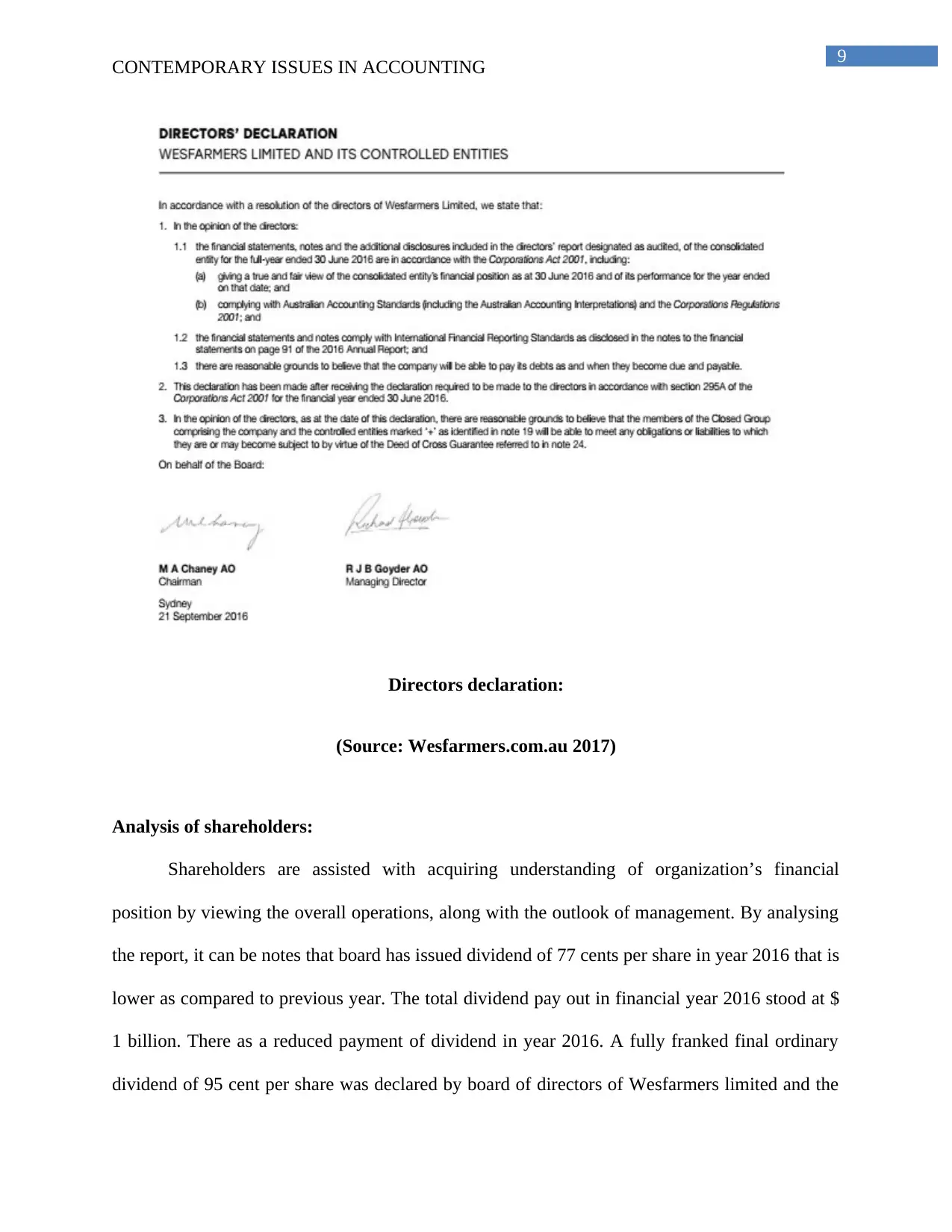

Director’s declaration:

The figure below depicts the declaration of director of Woolworths and the declaration is

made according to the requirement of 295A of Corporation act, 2001. It is declared that the

financial statements of organization complies with the Australian accounting standard and is

prepared in accordance with the Corporation act, 2001. Organization will be able to meet the

obligations that are applied in ASIC class orders that are discussed in the notes to financial

statements. Financial statements also comply with the International Financial reporting standard

(Christensen et al. 2015).

CONTEMPORARY ISSUES IN ACCOUNTING

Preparation basis:

(Source: Wesfarmers.com 2017)

Director’s declaration:

The figure below depicts the declaration of director of Woolworths and the declaration is

made according to the requirement of 295A of Corporation act, 2001. It is declared that the

financial statements of organization complies with the Australian accounting standard and is

prepared in accordance with the Corporation act, 2001. Organization will be able to meet the

obligations that are applied in ASIC class orders that are discussed in the notes to financial

statements. Financial statements also comply with the International Financial reporting standard

(Christensen et al. 2015).

8

CONTEMPORARY ISSUES IN ACCOUNTING

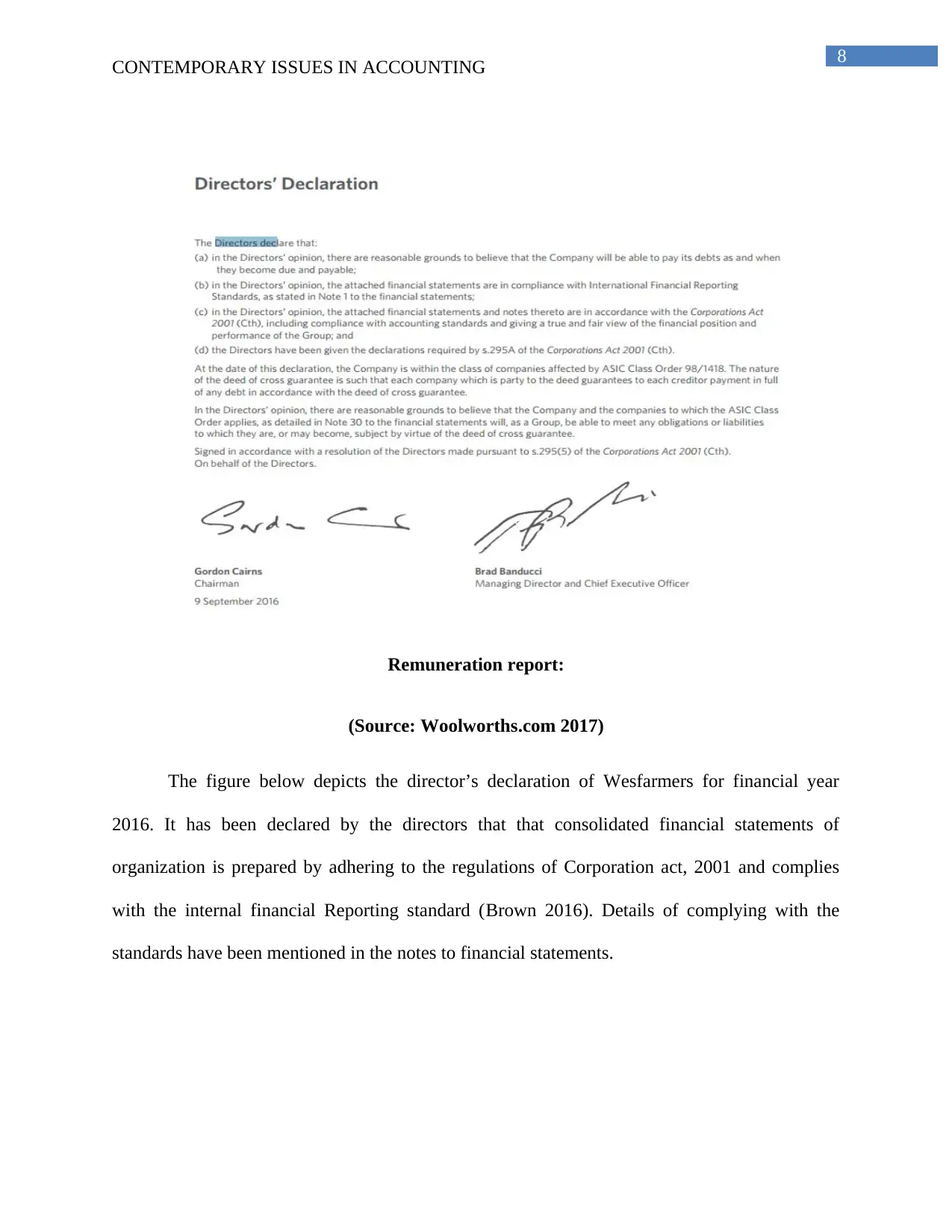

Remuneration report:

(Source: Woolworths.com 2017)

The figure below depicts the director’s declaration of Wesfarmers for financial year

2016. It has been declared by the directors that that consolidated financial statements of

organization is prepared by adhering to the regulations of Corporation act, 2001 and complies

with the internal financial Reporting standard (Brown 2016). Details of complying with the

standards have been mentioned in the notes to financial statements.

CONTEMPORARY ISSUES IN ACCOUNTING

Remuneration report:

(Source: Woolworths.com 2017)

The figure below depicts the director’s declaration of Wesfarmers for financial year

2016. It has been declared by the directors that that consolidated financial statements of

organization is prepared by adhering to the regulations of Corporation act, 2001 and complies

with the internal financial Reporting standard (Brown 2016). Details of complying with the

standards have been mentioned in the notes to financial statements.

9

CONTEMPORARY ISSUES IN ACCOUNTING

Directors declaration:

(Source: Wesfarmers.com.au 2017)

Analysis of shareholders:

Shareholders are assisted with acquiring understanding of organization’s financial

position by viewing the overall operations, along with the outlook of management. By analysing

the report, it can be notes that board has issued dividend of 77 cents per share in year 2016 that is

lower as compared to previous year. The total dividend pay out in financial year 2016 stood at $

1 billion. There as a reduced payment of dividend in year 2016. A fully franked final ordinary

dividend of 95 cent per share was declared by board of directors of Wesfarmers limited and the

CONTEMPORARY ISSUES IN ACCOUNTING

Directors declaration:

(Source: Wesfarmers.com.au 2017)

Analysis of shareholders:

Shareholders are assisted with acquiring understanding of organization’s financial

position by viewing the overall operations, along with the outlook of management. By analysing

the report, it can be notes that board has issued dividend of 77 cents per share in year 2016 that is

lower as compared to previous year. The total dividend pay out in financial year 2016 stood at $

1 billion. There as a reduced payment of dividend in year 2016. A fully franked final ordinary

dividend of 95 cent per share was declared by board of directors of Wesfarmers limited and the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

CONTEMPORARY ISSUES IN ACCOUNTING

dividend payment has reduced in the current year. Dividend per share for financial year stood at

$ 1.86. The total amount of dividend for the year 2016 that was paid to shareholders stood at $

1070 million (Wesfarmers.com.au 2017).

Remuneration report:

The figure below depicts the remuneration report of Woolworths and it provides with the

changes in the remuneration that is paid to the non-executive and executive directors of

company. The remuneration principle of Woolworths has been set by aligning it with the

refocused business strategy. It is as per the discretion of board of directors whether to increase

the salary of executives based on their performance. The fees of non executive directors are

approved by the shareholders and they are paid an annual fee of $ 4000000. Fees payable is

under the current aggregate annual feel pool.

CONTEMPORARY ISSUES IN ACCOUNTING

dividend payment has reduced in the current year. Dividend per share for financial year stood at

$ 1.86. The total amount of dividend for the year 2016 that was paid to shareholders stood at $

1070 million (Wesfarmers.com.au 2017).

Remuneration report:

The figure below depicts the remuneration report of Woolworths and it provides with the

changes in the remuneration that is paid to the non-executive and executive directors of

company. The remuneration principle of Woolworths has been set by aligning it with the

refocused business strategy. It is as per the discretion of board of directors whether to increase

the salary of executives based on their performance. The fees of non executive directors are

approved by the shareholders and they are paid an annual fee of $ 4000000. Fees payable is

under the current aggregate annual feel pool.

11

CONTEMPORARY ISSUES IN ACCOUNTING

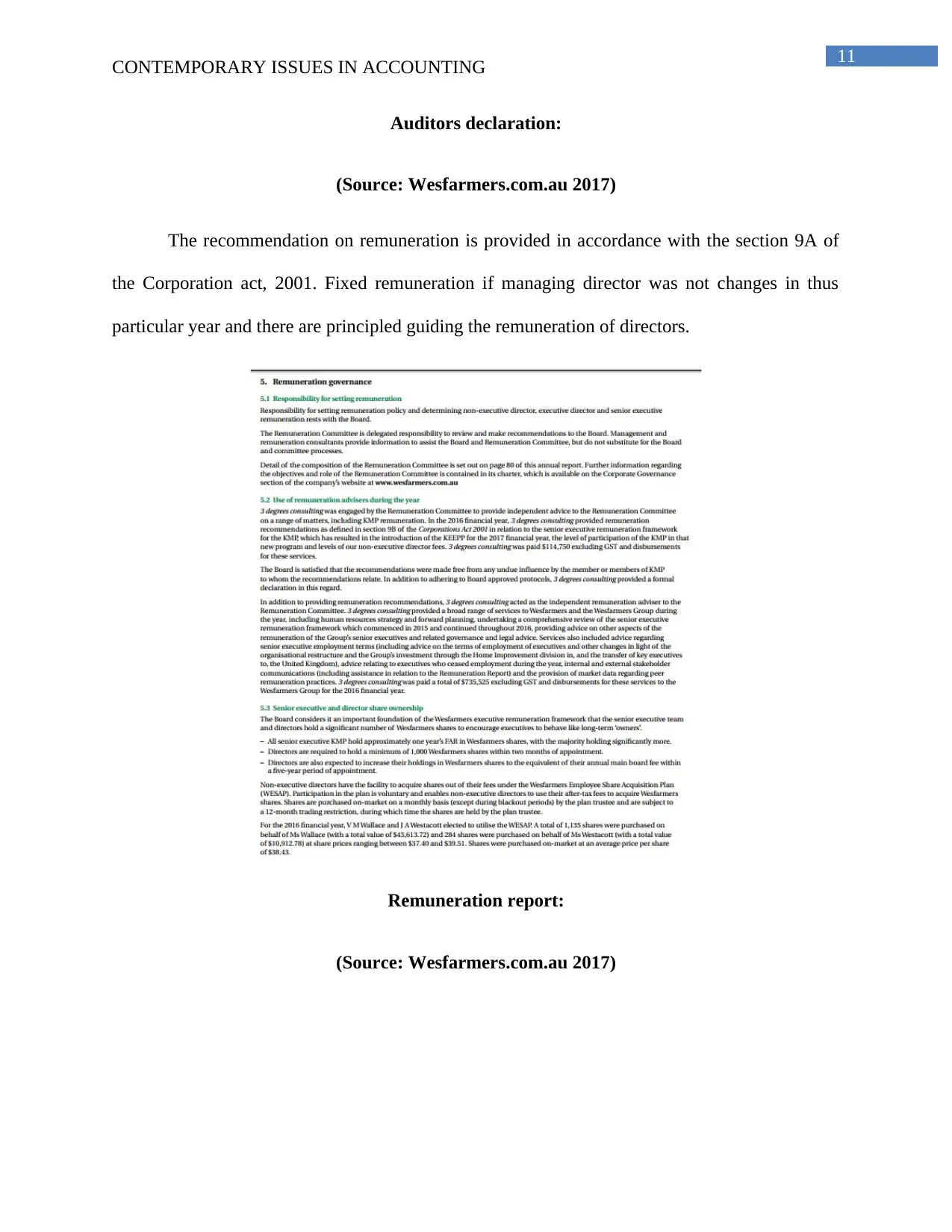

Auditors declaration:

(Source: Wesfarmers.com.au 2017)

The recommendation on remuneration is provided in accordance with the section 9A of

the Corporation act, 2001. Fixed remuneration if managing director was not changes in thus

particular year and there are principled guiding the remuneration of directors.

Remuneration report:

(Source: Wesfarmers.com.au 2017)

CONTEMPORARY ISSUES IN ACCOUNTING

Auditors declaration:

(Source: Wesfarmers.com.au 2017)

The recommendation on remuneration is provided in accordance with the section 9A of

the Corporation act, 2001. Fixed remuneration if managing director was not changes in thus

particular year and there are principled guiding the remuneration of directors.

Remuneration report:

(Source: Wesfarmers.com.au 2017)

12

CONTEMPORARY ISSUES IN ACCOUNTING

Prudence and its impact on dealing with corporate disparity:

Prudence is considered as important and vital concepts in the conceptual framework for

maintaining accounting principles. It is required in the event of realization concerning with the

registering if liabilities and expenses. Prudence helps in reducing the unethical evaluation of

liabilities and assets. It is required by organization following the conceptual framework to revise

particular explicit notion of reference according to the proposed changes. Organization will be

able to achieve neutrality in the preparation of financial statements by the inclusion of prudence

in their framework. It would bring in capability on part of preparers of financial statements to

understate assets and income and overstate their liabilities and expenses. Some of the prevailing

disparities in the financial report of organization will be able to address with the help of

measuring the issues related to the prudence inclusion in the conceptual framework. Earlier, due

to some of existing loopholes, organization took the undue advantage of the concept prudence

and inflated their assets and liabilities in order to depict a stable financial report to their users.

Inclusion of prudence would significantly impact the rices of financial report of different

companies. Organization will be able to present genuine the components of financial reports and

thereby providing the users with relevant facts and figures that would assist tem in making

investment decisions. It has been mentioned that organizations are able to produce a more

reliable financial statement by including prudence in their conceptual framework. Due to the

existing loopholes in the produce, the conceptual framework used by organizations was violated.

Investors were mainly duped in terms of required investment capital and payment of dividends.

From the past evidence and record, it can be seen that the concept of prudence was basically used

by organizations as a way to reduce their financial liabilities (Palepu et al. 2013). Therefore, in

CONTEMPORARY ISSUES IN ACCOUNTING

Prudence and its impact on dealing with corporate disparity:

Prudence is considered as important and vital concepts in the conceptual framework for

maintaining accounting principles. It is required in the event of realization concerning with the

registering if liabilities and expenses. Prudence helps in reducing the unethical evaluation of

liabilities and assets. It is required by organization following the conceptual framework to revise

particular explicit notion of reference according to the proposed changes. Organization will be

able to achieve neutrality in the preparation of financial statements by the inclusion of prudence

in their framework. It would bring in capability on part of preparers of financial statements to

understate assets and income and overstate their liabilities and expenses. Some of the prevailing

disparities in the financial report of organization will be able to address with the help of

measuring the issues related to the prudence inclusion in the conceptual framework. Earlier, due

to some of existing loopholes, organization took the undue advantage of the concept prudence

and inflated their assets and liabilities in order to depict a stable financial report to their users.

Inclusion of prudence would significantly impact the rices of financial report of different

companies. Organization will be able to present genuine the components of financial reports and

thereby providing the users with relevant facts and figures that would assist tem in making

investment decisions. It has been mentioned that organizations are able to produce a more

reliable financial statement by including prudence in their conceptual framework. Due to the

existing loopholes in the produce, the conceptual framework used by organizations was violated.

Investors were mainly duped in terms of required investment capital and payment of dividends.

From the past evidence and record, it can be seen that the concept of prudence was basically used

by organizations as a way to reduce their financial liabilities (Palepu et al. 2013). Therefore, in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

CONTEMPORARY ISSUES IN ACCOUNTING

the present era, prudence in the conceptual framework cannot be applied if there are more

restrictive bindings that will prevent organizations to take any unethical advantage.

The neutrality in terms of the presentation of assets and liabilities in the financial

statements are affected in the reasonable manner as prudence leads to the asymmetric treatment

of the same. Exclusion of prudence from the financial reporting by Australian accounting

standard has resulted in substitution of one opportunity to other and their reduction. It is

presented by many critics that inclusion of prudence in the conceptual framework would be

redundant and it is the responsibility of investors for using the information presented in the

financial statements wisely while dealing with capital allocation. In the event of uncertainty,

organization will be able to prevent any optimist view about their financial statements by

including prudence in the preparation of financial statements (Bond et al. 2016). Therefore, both

the organizations cam includes the concept of prudence in their conceptual framework and while

preparing their financial statements as it is regarded as essential principal in corporate reporting.

Comparison of the annual report of Wesfarmers and Woolworths Ltd:

From the above discussion, it can be see that both the organization that is Woolworths

and Wesfarmers has the same basis or preparing their financial statements. Woolworths as well

as Wesfarmers complies with the Australian accounting standard and their interpretations, IFRS

and all the requirements of Corporation act, 2001. However, the presented of some of the factors

is different in both the organization. It can be deduced that the amended accounting treatments

have been effectively applied by the organizations and is effective from financial year 2015. The

remuneration report of both the organization set out the total amount of remuneration that is paid

to the executive, non-executive directors and senior executives and presents with their respective

CONTEMPORARY ISSUES IN ACCOUNTING

the present era, prudence in the conceptual framework cannot be applied if there are more

restrictive bindings that will prevent organizations to take any unethical advantage.

The neutrality in terms of the presentation of assets and liabilities in the financial

statements are affected in the reasonable manner as prudence leads to the asymmetric treatment

of the same. Exclusion of prudence from the financial reporting by Australian accounting

standard has resulted in substitution of one opportunity to other and their reduction. It is

presented by many critics that inclusion of prudence in the conceptual framework would be

redundant and it is the responsibility of investors for using the information presented in the

financial statements wisely while dealing with capital allocation. In the event of uncertainty,

organization will be able to prevent any optimist view about their financial statements by

including prudence in the preparation of financial statements (Bond et al. 2016). Therefore, both

the organizations cam includes the concept of prudence in their conceptual framework and while

preparing their financial statements as it is regarded as essential principal in corporate reporting.

Comparison of the annual report of Wesfarmers and Woolworths Ltd:

From the above discussion, it can be see that both the organization that is Woolworths

and Wesfarmers has the same basis or preparing their financial statements. Woolworths as well

as Wesfarmers complies with the Australian accounting standard and their interpretations, IFRS

and all the requirements of Corporation act, 2001. However, the presented of some of the factors

is different in both the organization. It can be deduced that the amended accounting treatments

have been effectively applied by the organizations and is effective from financial year 2015. The

remuneration report of both the organization set out the total amount of remuneration that is paid

to the executive, non-executive directors and senior executives and presents with their respective

14

CONTEMPORARY ISSUES IN ACCOUNTING

remuneration structure. It was observed that Woolworths did not meet the overall expectation

and for the finance year 2017, the organization has adopted new remuneration principles that will

guide its structure. Performance associated with remuneration helps in driving the leadership

performance (Rahman 2013).

Recommendation:

Ongoing concerns and entities are required to adapt to the amended and revised concept

of accounting framework in order to produce more reliable financial statements to their users. It

is required by organizations to include the concept of prudence in their financial reporting

framework for overcoming some of the unethical practices. For each class of claims of equity,

there is a need to update the several measures. The role of prudence needs to be recognized in the

conceptual framework as it is a relevant principle. It is expected that a solid foundation of

financial reporting can be created with the inclusion of prudence as it does nit have any

precautionary principles for creating revenue and retaining hidden reserves.

Conclusion:

The study depicts the overall evaluation of the conceptual framework of Woolworth and

Wesfarmers limited that are two consumer companies in Australia. Overall significance and the

existing loopholes of the concepts of prudence is discussed in the report. It can be ascertained

from the analysis of various extracts of annual report of both the organization that they comply

with the relevant accounting standards in the formulation of their accounting policies an

preparing the financial statements. Analysis of remuneration report and directors declaration

helped in coming out with the specifics facts and the respective structural framework.

Furthermore, the preparation of report includes the discussion of prudence and their significance

CONTEMPORARY ISSUES IN ACCOUNTING

remuneration structure. It was observed that Woolworths did not meet the overall expectation

and for the finance year 2017, the organization has adopted new remuneration principles that will

guide its structure. Performance associated with remuneration helps in driving the leadership

performance (Rahman 2013).

Recommendation:

Ongoing concerns and entities are required to adapt to the amended and revised concept

of accounting framework in order to produce more reliable financial statements to their users. It

is required by organizations to include the concept of prudence in their financial reporting

framework for overcoming some of the unethical practices. For each class of claims of equity,

there is a need to update the several measures. The role of prudence needs to be recognized in the

conceptual framework as it is a relevant principle. It is expected that a solid foundation of

financial reporting can be created with the inclusion of prudence as it does nit have any

precautionary principles for creating revenue and retaining hidden reserves.

Conclusion:

The study depicts the overall evaluation of the conceptual framework of Woolworth and

Wesfarmers limited that are two consumer companies in Australia. Overall significance and the

existing loopholes of the concepts of prudence is discussed in the report. It can be ascertained

from the analysis of various extracts of annual report of both the organization that they comply

with the relevant accounting standards in the formulation of their accounting policies an

preparing the financial statements. Analysis of remuneration report and directors declaration

helped in coming out with the specifics facts and the respective structural framework.

Furthermore, the preparation of report includes the discussion of prudence and their significance

15

CONTEMPORARY ISSUES IN ACCOUNTING

and relevance in preparing of the financial report of different companies. Analysis of the

conceptual framework will assist the user in their decision making by presenting the financial

position of companies.

CONTEMPORARY ISSUES IN ACCOUNTING

and relevance in preparing of the financial report of different companies. Analysis of the

conceptual framework will assist the user in their decision making by presenting the financial

position of companies.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

CONTEMPORARY ISSUES IN ACCOUNTING

Reference:

AASB, 2014. AASB 6: Exploration for and Evaluation of Mineral Resources.

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

Barth, M.E., Landsman, W.R. and Lang, M.H., 2014. International accounting standards and

accounting quality. Journal of accounting research, 46(3), pp.467-498.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Brown, A.M., 2016. The financial milieu of the IASB and AASB. Australian Accounting

Review, 16(38), pp.85-95.

Camfferman, K. and Zeff, S.A., 2015. Aiming for global accounting standards: the International

Accounting Standards Board, 2001-2011. Oxford University Press, USA.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting Review,

24(1), pp.31-61.

DeFond, M.L., Hung, M., Li, S. and Li, Y., 2014. Does mandatory IFRS adoption affect crash

risk?. The Accounting Review, 90(1), pp.265-299.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

CONTEMPORARY ISSUES IN ACCOUNTING

Reference:

AASB, 2014. AASB 6: Exploration for and Evaluation of Mineral Resources.

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

Barth, M.E., Landsman, W.R. and Lang, M.H., 2014. International accounting standards and

accounting quality. Journal of accounting research, 46(3), pp.467-498.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Brown, A.M., 2016. The financial milieu of the IASB and AASB. Australian Accounting

Review, 16(38), pp.85-95.

Camfferman, K. and Zeff, S.A., 2015. Aiming for global accounting standards: the International

Accounting Standards Board, 2001-2011. Oxford University Press, USA.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting Review,

24(1), pp.31-61.

DeFond, M.L., Hung, M., Li, S. and Li, Y., 2014. Does mandatory IFRS adoption affect crash

risk?. The Accounting Review, 90(1), pp.265-299.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

17

CONTEMPORARY ISSUES IN ACCOUNTING

He, L., Evans, E. and He, R., 2016. The Impact of AASB 8 Operating Segments on Analysts’

Earnings Forecasts: Australian Evidence. Australian Accounting Review, 26(4), pp.330-340.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Rahman, A.R., 2013. The Australian Accounting Standards Review Board (RLE Accounting):

The Establishment of Its Participative Review Process. Routledge.

Soderstrom, N.S. and Sun, K.J., 2013. IFRS adoption and accounting quality: a review. European

Accounting Review, 16(4), pp.675-702.

Wesfarmers.com.au (2017). Annual reports | Wesfarmers Group. [online] Available at:

https://www.wesfarmers.com.au/investor-centre/reporting/annual-reports [Accessed 15 Aug.

2017].

Woolworths.com. (2017). Annual reports | woolworths Group. [online] Available at:

https://www.woolworths.com/investor-centre/reporting/annual-reports [Accessed 15 Aug. 2017].

CONTEMPORARY ISSUES IN ACCOUNTING

He, L., Evans, E. and He, R., 2016. The Impact of AASB 8 Operating Segments on Analysts’

Earnings Forecasts: Australian Evidence. Australian Accounting Review, 26(4), pp.330-340.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Rahman, A.R., 2013. The Australian Accounting Standards Review Board (RLE Accounting):

The Establishment of Its Participative Review Process. Routledge.

Soderstrom, N.S. and Sun, K.J., 2013. IFRS adoption and accounting quality: a review. European

Accounting Review, 16(4), pp.675-702.

Wesfarmers.com.au (2017). Annual reports | Wesfarmers Group. [online] Available at:

https://www.wesfarmers.com.au/investor-centre/reporting/annual-reports [Accessed 15 Aug.

2017].

Woolworths.com. (2017). Annual reports | woolworths Group. [online] Available at:

https://www.woolworths.com/investor-centre/reporting/annual-reports [Accessed 15 Aug. 2017].

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.