Carbon Disclosure Determinants in Companies

Added on 2021-04-24

12 Pages2155 Words146 Views

Running head: CONTEMPORARY ISSUES OF MANAGEMENT ACCOUNTINGClimate Change and its Consequences for StakeholdersName of the University:Name of the Student:Authors Note:

1CONTEMPORARY ISSUES OF MANAGEMENT ACCOUNTINGTable of Contents1. Literature Review............................................................................................................21.1. Carbon or Voluntary Disclosure by Companies.......................................................21.2. Stakeholder Theory...................................................................................................21.3. Carbon Disclosure Determinants Within Corporate Real Estate Companies...........32. Conceptual Model............................................................................................................33. Hypothesis.......................................................................................................................44. Proxy Measures for Theoretical Constructs:...................................................................55. Research Method:............................................................................................................65.1 Research Approach:...................................................................................................65.2 Data Collection Technique:.......................................................................................65.3 Sampling and Sample Size:.......................................................................................75.4 Data Analysis Technique:..........................................................................................7References:..........................................................................................................................8Appendix:..........................................................................................................................11

2CONTEMPORARY ISSUES OF MANAGEMENT ACCOUNTING1. Literature Review1.1. Carbon or Voluntary Disclosure by CompaniesChiuand Wang (2015) indicated that CDP works for decreasing greenhouse gasemissions of the companies with reducing the risk of climate change. These researchers alsoindicated that in the year 2015, 822 investors have more than US$95 trillion within assets backedCDP’s climate change information request. Guenther et al. (2016) had a different opinionregarding greenhouse gas information gradually disclosed by the organizations of the countrythat is listed. This is also carried out by means of two different communication channels likecorporate report and the project of carbon disclosure. From the stakeholder theory perspective, itis indicated that the greenhouse gas amounts are gradually decreased within the corporate reportswithin the CDP (Hartmann, Perego and Young 2013). 1.2. Stakeholder TheoryAccording to Lee, Park and Klassen (2015) stakeholder theory is indicated as anorganizational management theory as well as voluntary carbon disclosures that is associated withmaintaining morals and values of managing all the company’s stakeholders. These researchersalso indicated that this theory makes sure that an organization’s intention is to developstakeholders’ value (Lovell 2010). Due to these causes, a company must take into account itsconsumers, suppliers, communities and shareholders. In accordance, Jaggi et al. (2017) statedthat stakeholder engagement is a two-way theory of communication which focuses onmaintaining information exchange concerning the issues related with domestic sustainability. Itis understood to be a dialogue which supports the council in deciding the choices that will beacceptable to the local community.

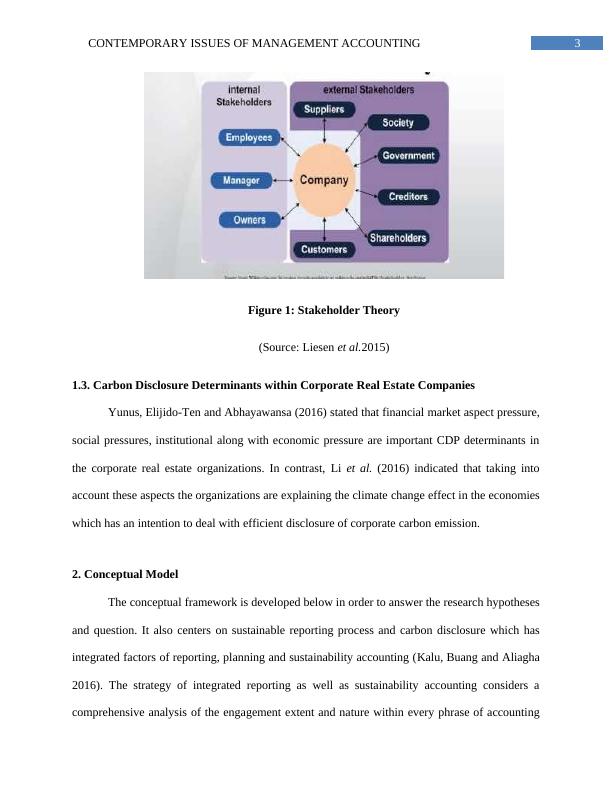

3CONTEMPORARY ISSUES OF MANAGEMENT ACCOUNTINGFigure 1: Stakeholder Theory(Source: Liesen et al.2015)1.3. Carbon Disclosure Determinants within Corporate Real Estate CompaniesYunus, Elijido-Ten and Abhayawansa (2016) stated that financial market aspect pressure,social pressures, institutional along with economic pressure are important CDP determinants inthe corporate real estate organizations. In contrast, Li et al. (2016) indicated that taking intoaccount these aspects the organizations are explaining the climate change effect in the economieswhich has an intention to deal with efficient disclosure of corporate carbon emission. 2. Conceptual ModelThe conceptual framework is developed below in order to answer the research hypothesesand question. It also centers on sustainable reporting process and carbon disclosure which hasintegrated factors of reporting, planning and sustainability accounting (Kalu, Buang and Aliagha2016). The strategy of integrated reporting as well as sustainability accounting considers acomprehensive analysis of the engagement extent and nature within every phrase of accounting

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Contemporary Issues of Management Accounting - Doclg...

|12

|2013

|95

Relationship between Green Gas Emission and Firm Disclosure Level - Agency Theorylg...

|10

|1644

|302

Assignment Contemporary Issues in Accountinglg...

|14

|2524

|53

MGT723 Integration of Climate Change in Businesslg...

|7

|1174

|67

Assessing the Effects of Carbon Disclosure Project on Minimizing Carbon Emissionslg...

|14

|4057

|52

Voluntary Sustainability and Environmental Reportinglg...

|8

|1424

|78