Corporate Accounting Report 2022

VerifiedAdded on 2022/10/11

|15

|2851

|12

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Accounts

0

Amcor Limited and Alumina Limited

Corporate accounting

9/23/2019

0

Amcor Limited and Alumina Limited

Corporate accounting

9/23/2019

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounts

1

Abstract

The report is based on the study of the financial statements

so that the terms which are used in the equities and the

liabilities can be ascertained. In this report sources of funds

used by both, the companies are explained which are equity

shares and retained earnings. The companies have raised

funds from these sources. In this report, it is evaluated that a

small proprietary company is the one who has the less than

the $25 million gross operating revenue for the consolidated

monetary year and the large company has more than the

$50 million (Kaya and Koch, 2015)

1

Abstract

The report is based on the study of the financial statements

so that the terms which are used in the equities and the

liabilities can be ascertained. In this report sources of funds

used by both, the companies are explained which are equity

shares and retained earnings. The companies have raised

funds from these sources. In this report, it is evaluated that a

small proprietary company is the one who has the less than

the $25 million gross operating revenue for the consolidated

monetary year and the large company has more than the

$50 million (Kaya and Koch, 2015)

Accounts

2

Contents

Introduction........................................................................................................................3

Part A.................................................................................................................................3

Items recorded in the owner’s equity section.................................................................3

The movements of the items recorded in the owner’s

equity section..................................................................................................................4

Items recorded under the liability section.......................................................................4

The movements of the items recorded in the liability

section............................................................................................................................5

The relative advantages or disadvantages of each sources

of fund.............................................................................................................................7

Part B.................................................................................................................................8

The concepts of small proprietary company, large

proprietary company and reporting entity and their

implications.....................................................................................................................8

Conclusion.........................................................................................................................9

References.......................................................................................................................10

2

Contents

Introduction........................................................................................................................3

Part A.................................................................................................................................3

Items recorded in the owner’s equity section.................................................................3

The movements of the items recorded in the owner’s

equity section..................................................................................................................4

Items recorded under the liability section.......................................................................4

The movements of the items recorded in the liability

section............................................................................................................................5

The relative advantages or disadvantages of each sources

of fund.............................................................................................................................7

Part B.................................................................................................................................8

The concepts of small proprietary company, large

proprietary company and reporting entity and their

implications.....................................................................................................................8

Conclusion.........................................................................................................................9

References.......................................................................................................................10

Accounts

3

Introduction

The report is made in regards to the corporate and the

financial accounting in the company Amcor limited and

Alumina Limited. The financial accounting of this two

companies will be studied for the last three years so that the

understanding in terms of the equity and liabilities in the

company can be developed (Demyanyk, et al., 2017). The

purpose of this assignment is to understand how to

companies raise their funds from different sources. The

movement in the funds which have risen will also be

identified in this report. The advantages and disadvantage of

each source of the fund will be elaborated so that

importance of these funds can be analyzed in the company.

The other part of this assignment will elaborate the concept if

the large proprietary, small proprietary and reporting entity

and their compliance requirements in the company.

Part A

Items recorded in the owner’s equity section

Amcor limited: The items recorded in the owner’s equity

section of the Amcor Limited are reserves, contributed equity

and retained earnings. Contributed equity can be defined as

the paid-up capital for the company. It is the amount of cash

given by the shareholders of the company in exchange for

the stock of the company (Amcor Limited, 2017). For taking

the ownership stake in the company, the amount is paid by

the shareholders is the contributed equity. The reserves are

the unrestricted cash of the company which has been kept

for the purpose of future use. This is the profits only which is

used by the company in the sense of the provision. Retained

earnings are the accumulated net earnings of the company

which is generally retained at the expiration of the reporting

year.

3

Introduction

The report is made in regards to the corporate and the

financial accounting in the company Amcor limited and

Alumina Limited. The financial accounting of this two

companies will be studied for the last three years so that the

understanding in terms of the equity and liabilities in the

company can be developed (Demyanyk, et al., 2017). The

purpose of this assignment is to understand how to

companies raise their funds from different sources. The

movement in the funds which have risen will also be

identified in this report. The advantages and disadvantage of

each source of the fund will be elaborated so that

importance of these funds can be analyzed in the company.

The other part of this assignment will elaborate the concept if

the large proprietary, small proprietary and reporting entity

and their compliance requirements in the company.

Part A

Items recorded in the owner’s equity section

Amcor limited: The items recorded in the owner’s equity

section of the Amcor Limited are reserves, contributed equity

and retained earnings. Contributed equity can be defined as

the paid-up capital for the company. It is the amount of cash

given by the shareholders of the company in exchange for

the stock of the company (Amcor Limited, 2017). For taking

the ownership stake in the company, the amount is paid by

the shareholders is the contributed equity. The reserves are

the unrestricted cash of the company which has been kept

for the purpose of future use. This is the profits only which is

used by the company in the sense of the provision. Retained

earnings are the accumulated net earnings of the company

which is generally retained at the expiration of the reporting

year.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounts

4

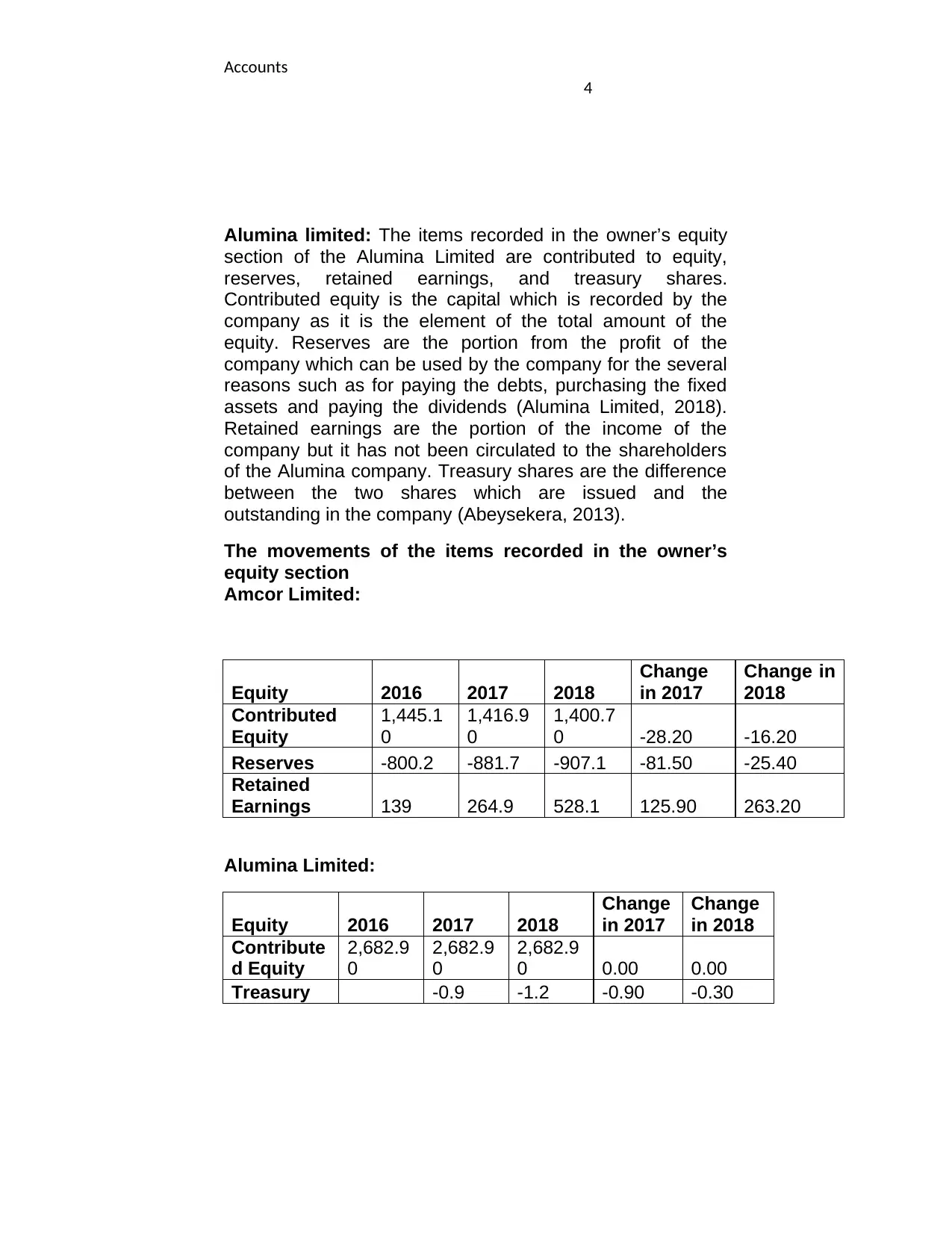

Alumina limited: The items recorded in the owner’s equity

section of the Alumina Limited are contributed to equity,

reserves, retained earnings, and treasury shares.

Contributed equity is the capital which is recorded by the

company as it is the element of the total amount of the

equity. Reserves are the portion from the profit of the

company which can be used by the company for the several

reasons such as for paying the debts, purchasing the fixed

assets and paying the dividends (Alumina Limited, 2018).

Retained earnings are the portion of the income of the

company but it has not been circulated to the shareholders

of the Alumina company. Treasury shares are the difference

between the two shares which are issued and the

outstanding in the company (Abeysekera, 2013).

The movements of the items recorded in the owner’s

equity section

Amcor Limited:

Equity 2016 2017 2018

Change

in 2017

Change in

2018

Contributed

Equity

1,445.1

0

1,416.9

0

1,400.7

0 -28.20 -16.20

Reserves -800.2 -881.7 -907.1 -81.50 -25.40

Retained

Earnings 139 264.9 528.1 125.90 263.20

Alumina Limited:

Equity 2016 2017 2018

Change

in 2017

Change

in 2018

Contribute

d Equity

2,682.9

0

2,682.9

0

2,682.9

0 0.00 0.00

Treasury -0.9 -1.2 -0.90 -0.30

4

Alumina limited: The items recorded in the owner’s equity

section of the Alumina Limited are contributed to equity,

reserves, retained earnings, and treasury shares.

Contributed equity is the capital which is recorded by the

company as it is the element of the total amount of the

equity. Reserves are the portion from the profit of the

company which can be used by the company for the several

reasons such as for paying the debts, purchasing the fixed

assets and paying the dividends (Alumina Limited, 2018).

Retained earnings are the portion of the income of the

company but it has not been circulated to the shareholders

of the Alumina company. Treasury shares are the difference

between the two shares which are issued and the

outstanding in the company (Abeysekera, 2013).

The movements of the items recorded in the owner’s

equity section

Amcor Limited:

Equity 2016 2017 2018

Change

in 2017

Change in

2018

Contributed

Equity

1,445.1

0

1,416.9

0

1,400.7

0 -28.20 -16.20

Reserves -800.2 -881.7 -907.1 -81.50 -25.40

Retained

Earnings 139 264.9 528.1 125.90 263.20

Alumina Limited:

Equity 2016 2017 2018

Change

in 2017

Change

in 2018

Contribute

d Equity

2,682.9

0

2,682.9

0

2,682.9

0 0.00 0.00

Treasury -0.9 -1.2 -0.90 -0.30

Accounts

5

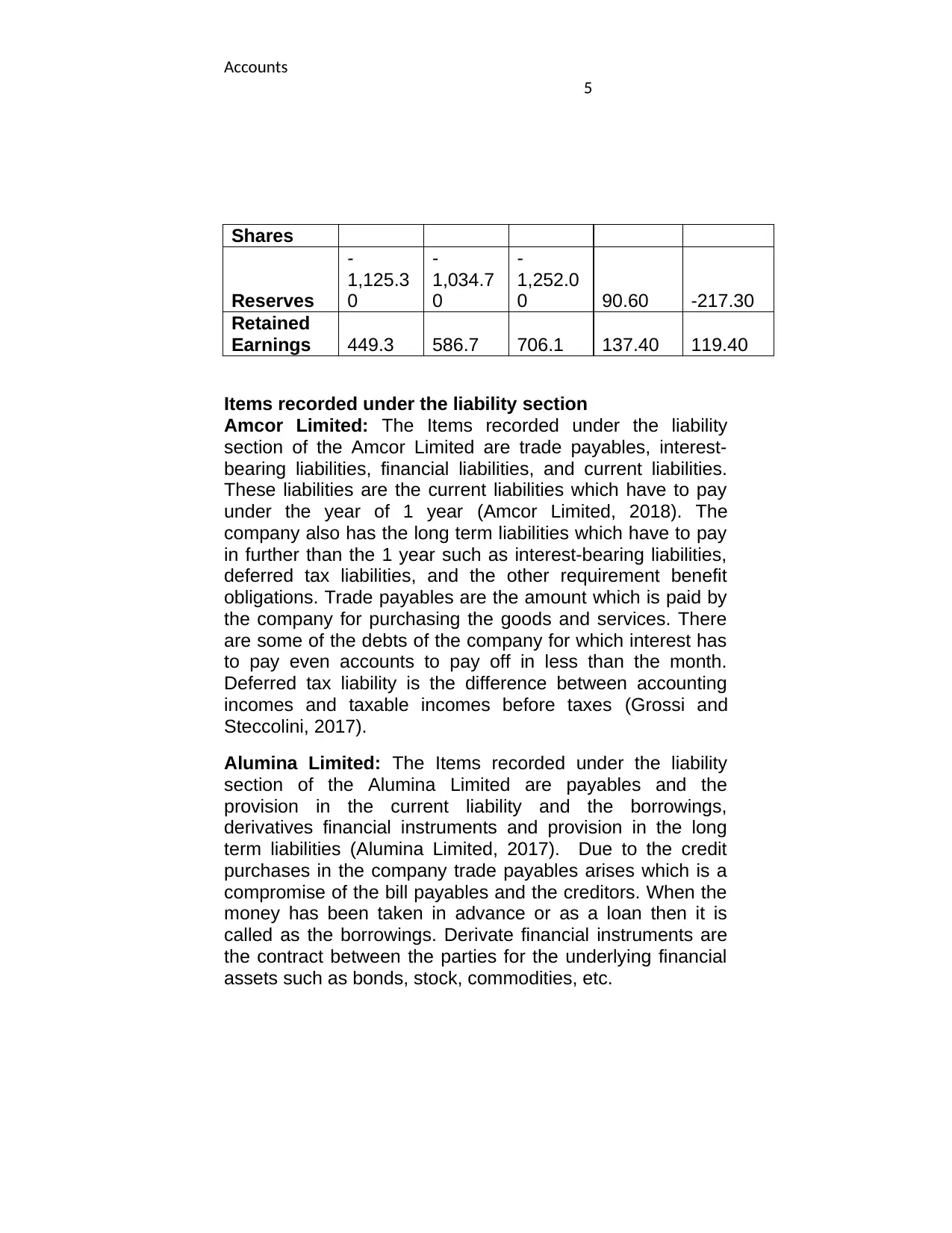

Shares

Reserves

-

1,125.3

0

-

1,034.7

0

-

1,252.0

0 90.60 -217.30

Retained

Earnings 449.3 586.7 706.1 137.40 119.40

Items recorded under the liability section

Amcor Limited: The Items recorded under the liability

section of the Amcor Limited are trade payables, interest-

bearing liabilities, financial liabilities, and current liabilities.

These liabilities are the current liabilities which have to pay

under the year of 1 year (Amcor Limited, 2018). The

company also has the long term liabilities which have to pay

in further than the 1 year such as interest-bearing liabilities,

deferred tax liabilities, and the other requirement benefit

obligations. Trade payables are the amount which is paid by

the company for purchasing the goods and services. There

are some of the debts of the company for which interest has

to pay even accounts to pay off in less than the month.

Deferred tax liability is the difference between accounting

incomes and taxable incomes before taxes (Grossi and

Steccolini, 2017).

Alumina Limited: The Items recorded under the liability

section of the Alumina Limited are payables and the

provision in the current liability and the borrowings,

derivatives financial instruments and provision in the long

term liabilities (Alumina Limited, 2017). Due to the credit

purchases in the company trade payables arises which is a

compromise of the bill payables and the creditors. When the

money has been taken in advance or as a loan then it is

called as the borrowings. Derivate financial instruments are

the contract between the parties for the underlying financial

assets such as bonds, stock, commodities, etc.

5

Shares

Reserves

-

1,125.3

0

-

1,034.7

0

-

1,252.0

0 90.60 -217.30

Retained

Earnings 449.3 586.7 706.1 137.40 119.40

Items recorded under the liability section

Amcor Limited: The Items recorded under the liability

section of the Amcor Limited are trade payables, interest-

bearing liabilities, financial liabilities, and current liabilities.

These liabilities are the current liabilities which have to pay

under the year of 1 year (Amcor Limited, 2018). The

company also has the long term liabilities which have to pay

in further than the 1 year such as interest-bearing liabilities,

deferred tax liabilities, and the other requirement benefit

obligations. Trade payables are the amount which is paid by

the company for purchasing the goods and services. There

are some of the debts of the company for which interest has

to pay even accounts to pay off in less than the month.

Deferred tax liability is the difference between accounting

incomes and taxable incomes before taxes (Grossi and

Steccolini, 2017).

Alumina Limited: The Items recorded under the liability

section of the Alumina Limited are payables and the

provision in the current liability and the borrowings,

derivatives financial instruments and provision in the long

term liabilities (Alumina Limited, 2017). Due to the credit

purchases in the company trade payables arises which is a

compromise of the bill payables and the creditors. When the

money has been taken in advance or as a loan then it is

called as the borrowings. Derivate financial instruments are

the contract between the parties for the underlying financial

assets such as bonds, stock, commodities, etc.

Accounts

6

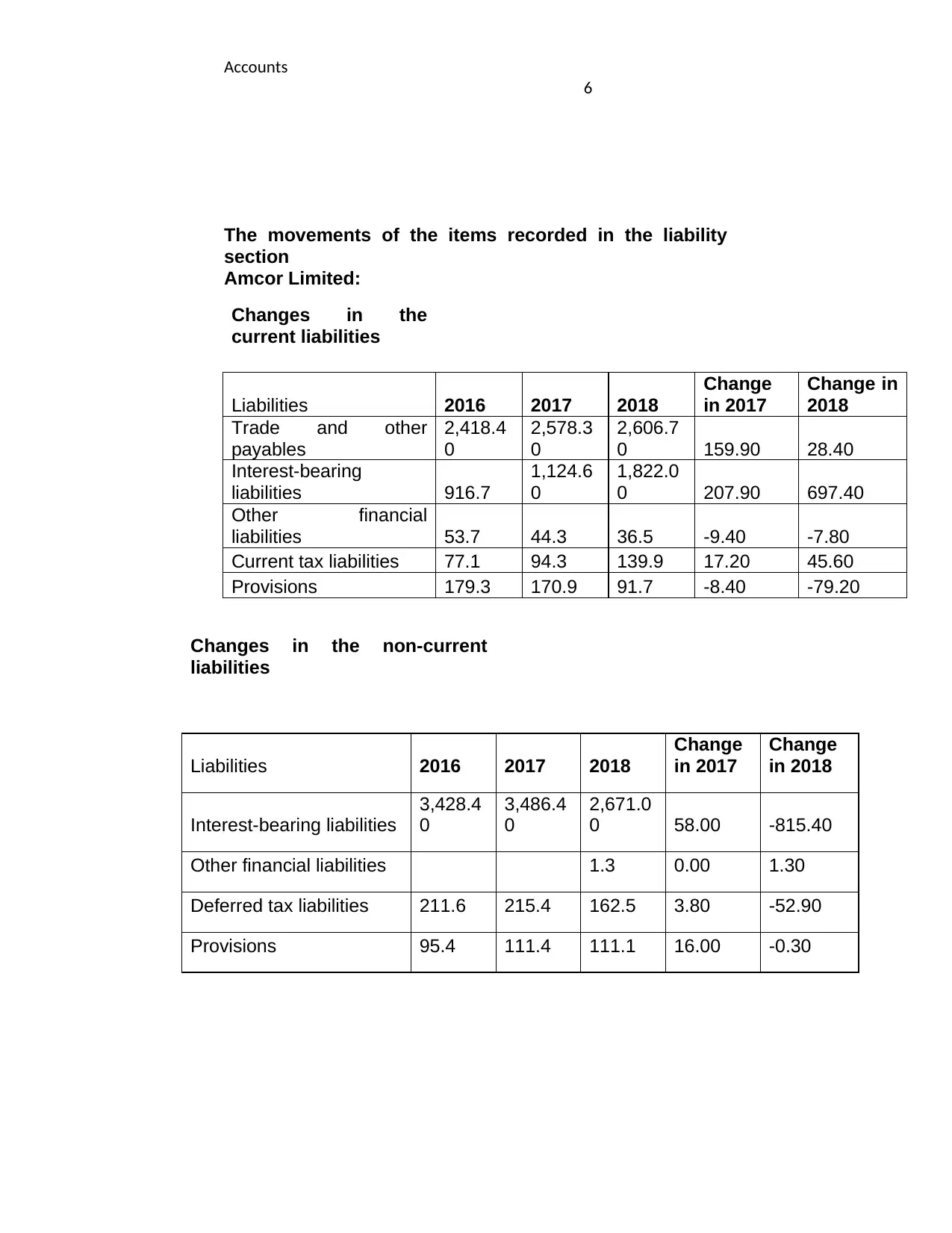

The movements of the items recorded in the liability

section

Amcor Limited:

Changes in the

current liabilities

Liabilities 2016 2017 2018

Change

in 2017

Change in

2018

Trade and other

payables

2,418.4

0

2,578.3

0

2,606.7

0 159.90 28.40

Interest-bearing

liabilities 916.7

1,124.6

0

1,822.0

0 207.90 697.40

Other financial

liabilities 53.7 44.3 36.5 -9.40 -7.80

Current tax liabilities 77.1 94.3 139.9 17.20 45.60

Provisions 179.3 170.9 91.7 -8.40 -79.20

Changes in the non-current

liabilities

Liabilities 2016 2017 2018

Change

in 2017

Change

in 2018

Interest-bearing liabilities

3,428.4

0

3,486.4

0

2,671.0

0 58.00 -815.40

Other financial liabilities 1.3 0.00 1.30

Deferred tax liabilities 211.6 215.4 162.5 3.80 -52.90

Provisions 95.4 111.4 111.1 16.00 -0.30

6

The movements of the items recorded in the liability

section

Amcor Limited:

Changes in the

current liabilities

Liabilities 2016 2017 2018

Change

in 2017

Change in

2018

Trade and other

payables

2,418.4

0

2,578.3

0

2,606.7

0 159.90 28.40

Interest-bearing

liabilities 916.7

1,124.6

0

1,822.0

0 207.90 697.40

Other financial

liabilities 53.7 44.3 36.5 -9.40 -7.80

Current tax liabilities 77.1 94.3 139.9 17.20 45.60

Provisions 179.3 170.9 91.7 -8.40 -79.20

Changes in the non-current

liabilities

Liabilities 2016 2017 2018

Change

in 2017

Change

in 2018

Interest-bearing liabilities

3,428.4

0

3,486.4

0

2,671.0

0 58.00 -815.40

Other financial liabilities 1.3 0.00 1.30

Deferred tax liabilities 211.6 215.4 162.5 3.80 -52.90

Provisions 95.4 111.4 111.1 16.00 -0.30

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts

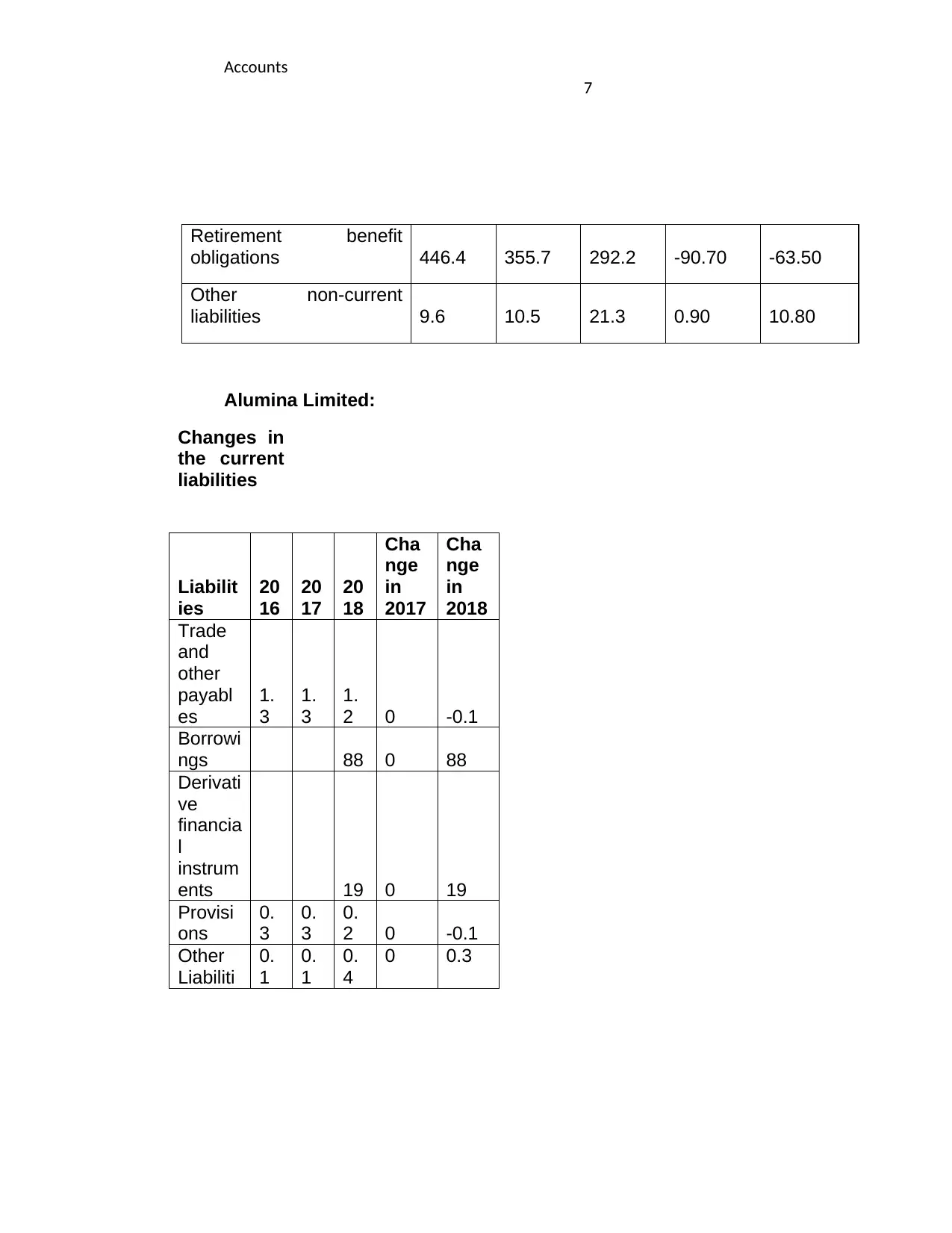

7

Retirement benefit

obligations 446.4 355.7 292.2 -90.70 -63.50

Other non-current

liabilities 9.6 10.5 21.3 0.90 10.80

Alumina Limited:

Changes in

the current

liabilities

Liabilit

ies

20

16

20

17

20

18

Cha

nge

in

2017

Cha

nge

in

2018

Trade

and

other

payabl

es

1.

3

1.

3

1.

2 0 -0.1

Borrowi

ngs 88 0 88

Derivati

ve

financia

l

instrum

ents 19 0 19

Provisi

ons

0.

3

0.

3

0.

2 0 -0.1

Other

Liabiliti

0.

1

0.

1

0.

4

0 0.3

7

Retirement benefit

obligations 446.4 355.7 292.2 -90.70 -63.50

Other non-current

liabilities 9.6 10.5 21.3 0.90 10.80

Alumina Limited:

Changes in

the current

liabilities

Liabilit

ies

20

16

20

17

20

18

Cha

nge

in

2017

Cha

nge

in

2018

Trade

and

other

payabl

es

1.

3

1.

3

1.

2 0 -0.1

Borrowi

ngs 88 0 88

Derivati

ve

financia

l

instrum

ents 19 0 19

Provisi

ons

0.

3

0.

3

0.

2 0 -0.1

Other

Liabiliti

0.

1

0.

1

0.

4

0 0.3

Accounts

8

es

Changes in the non-current liabilities

Liabilities

2016

20

17

20

18

Chan

ge in

2017

Chan

ge in

2018

Borrowings 92.4

98.

4 6 -98.4

Derivative financial

instruments 16.2 8.3 -7.9 -8.3

Provisions 0.6 0.5 0.5 -0.1 0

The relative advantages or disadvantages of each

source of fund

Amcor Limited: The major sources of fund for Amcor

Limited are the Retained Earnings and their advantages and

disadvantages are stated below:

Advantages: Retained earning are the cheaper sources of

the financing for the company which don”t involve any

acquisition cost. The company does not have to pay any

obligation in this funding (Stafievskaya, et al., 2015). The

financial position of the company gets stable by this source

of funding. Even if the Amcor limited don”t earns sufficient

money then also shareholders will get some constant

dividend. The market value of the shares also increases.

Disadvantages: This fund is utilized for careless spending.

Overcapitalization in the company happens when the huge

accumulation of the retained earning happens. The rate of

dividend is lower which creates the dissatisfaction among

the shareholders and the market value of the shares is also

getting affected adversely (Moskowitz, et al., 2012).

8

es

Changes in the non-current liabilities

Liabilities

2016

20

17

20

18

Chan

ge in

2017

Chan

ge in

2018

Borrowings 92.4

98.

4 6 -98.4

Derivative financial

instruments 16.2 8.3 -7.9 -8.3

Provisions 0.6 0.5 0.5 -0.1 0

The relative advantages or disadvantages of each

source of fund

Amcor Limited: The major sources of fund for Amcor

Limited are the Retained Earnings and their advantages and

disadvantages are stated below:

Advantages: Retained earning are the cheaper sources of

the financing for the company which don”t involve any

acquisition cost. The company does not have to pay any

obligation in this funding (Stafievskaya, et al., 2015). The

financial position of the company gets stable by this source

of funding. Even if the Amcor limited don”t earns sufficient

money then also shareholders will get some constant

dividend. The market value of the shares also increases.

Disadvantages: This fund is utilized for careless spending.

Overcapitalization in the company happens when the huge

accumulation of the retained earning happens. The rate of

dividend is lower which creates the dissatisfaction among

the shareholders and the market value of the shares is also

getting affected adversely (Moskowitz, et al., 2012).

Accounts

9

Alumina Limited: The major source of fund for the company

Alumina limited is the equity shares and their advantages

and disadvantages stated below:

Advantages: The Company can increase its funds by

issuing the shares in the market. It results in increasing the

market price of the share and due to this gain arises in the

company. The liability of this share is limited so the company

Alumina limited also gets benefited from this. Equity shares

have to pay the dividend at the fixed rate to the shareholders

of the company and they do not have any obligation (Patton,

et al., 2015). This share is the permanent source of capital

for the company and it also does not create any charge over

the assets of the company.

Disadvantages: These sources of the fund also have some

disadvantage such as the company cannot take the benefit

of the trading on equity if the shares are issued. The

chances of the overcapitalization happen in the company if

equity capital cannot be redeemed. Speculation increases in

the company as higher dividend has to be paid on these

shares.

Part B

The concepts of small proprietary company, large

proprietary company and reporting entity and their

implications

Small proprietary company: This Company is the one who

has less than the $25 million gross operating revenue for the

consolidated monetary year. The company should also be

considered as the small proprietary when they have the less

than the $12.5 million value in the consolidated uncivilized

assets of the company at the expiration of the monetary

years (ASIC, 2019). In this company the number of

9

Alumina Limited: The major source of fund for the company

Alumina limited is the equity shares and their advantages

and disadvantages stated below:

Advantages: The Company can increase its funds by

issuing the shares in the market. It results in increasing the

market price of the share and due to this gain arises in the

company. The liability of this share is limited so the company

Alumina limited also gets benefited from this. Equity shares

have to pay the dividend at the fixed rate to the shareholders

of the company and they do not have any obligation (Patton,

et al., 2015). This share is the permanent source of capital

for the company and it also does not create any charge over

the assets of the company.

Disadvantages: These sources of the fund also have some

disadvantage such as the company cannot take the benefit

of the trading on equity if the shares are issued. The

chances of the overcapitalization happen in the company if

equity capital cannot be redeemed. Speculation increases in

the company as higher dividend has to be paid on these

shares.

Part B

The concepts of small proprietary company, large

proprietary company and reporting entity and their

implications

Small proprietary company: This Company is the one who

has less than the $25 million gross operating revenue for the

consolidated monetary year. The company should also be

considered as the small proprietary when they have the less

than the $12.5 million value in the consolidated uncivilized

assets of the company at the expiration of the monetary

years (ASIC, 2019). In this company the number of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounts

10

employees should have less than the 50 at the end of the

financial year.

The monetary reports have to be prepared by the company

when it is directed under Section 293 or 294. The company

also has to keep the money and director report of the

company when the company registered under a foreign

company or the company is lodged with the disclosing entity.

If this company does not control by any foreign company or

they are not directed under the section 293 or 294 then they

do not have to prepare the monetary report and the manager

report (Patton, et al., 2015).

Large proprietary company: This company is the one has

additional than the $50 million gross operating revenue for

the consolidated monetary year (ASIC, 2019). If the value is

greater than the $25 million for the associated gross assets

of the company at the close of the monetary year then it is

considered as the large company. If the company has more

100 or more employees than it is also considered.

This company has to comply with the according to the

Australian Securities and Investment Commission and get

their financial report audited by the auditor. It is compulsory

for large companies to audit the financial reports of the

company to analyses whether the financial stamens

prepared by the company are accurate or not. They have to

lodge the financial and the director report every financial

year and must audit them for the grants relief.

Reporting entity: Reporting entity is the entity where all the

decisions taken by the entity is based on the monetary

performance of the company and the users are fully

dependent on the monetary situation of the company.

Financial accountability is the primary notion of the reporting

entity (Jackowicz, et al., 2017). This entity is consists of the

three things which are primary government, the companies

10

employees should have less than the 50 at the end of the

financial year.

The monetary reports have to be prepared by the company

when it is directed under Section 293 or 294. The company

also has to keep the money and director report of the

company when the company registered under a foreign

company or the company is lodged with the disclosing entity.

If this company does not control by any foreign company or

they are not directed under the section 293 or 294 then they

do not have to prepare the monetary report and the manager

report (Patton, et al., 2015).

Large proprietary company: This company is the one has

additional than the $50 million gross operating revenue for

the consolidated monetary year (ASIC, 2019). If the value is

greater than the $25 million for the associated gross assets

of the company at the close of the monetary year then it is

considered as the large company. If the company has more

100 or more employees than it is also considered.

This company has to comply with the according to the

Australian Securities and Investment Commission and get

their financial report audited by the auditor. It is compulsory

for large companies to audit the financial reports of the

company to analyses whether the financial stamens

prepared by the company are accurate or not. They have to

lodge the financial and the director report every financial

year and must audit them for the grants relief.

Reporting entity: Reporting entity is the entity where all the

decisions taken by the entity is based on the monetary

performance of the company and the users are fully

dependent on the monetary situation of the company.

Financial accountability is the primary notion of the reporting

entity (Jackowicz, et al., 2017). This entity is consists of the

three things which are primary government, the companies

Accounts

11

for which the primary government is accountable and the

other company which has a relationship with the primary

government.

The reporting entity has to comply with the International

Accounting Standards so that the transparency can be

maintained in the company. The requirements of the

international accounting standards help the company in

achieving comparability and consistency in financial

reporting (Vernimmen, et al., 2014).

Conclusion

It has been analyzed from the above evaluation that

corporate accounting is the branch of the accounting which

deals with the financial accounts of the company. In this

report, two reputed companies are chosen which Amcor

Limited is and the Alumina Limited and their financial report

for the last three years have been studied thoroughly so that

the performance of the company can be analyzed. The

equity and the liability section of the report have been

studied properly and their terms have been analyzed. In this

report the sources of funds to raise the capital in the

company is also stated and their pros and cons in also

elaborated. In this report the concept of the small, large and

reporting entity has analyzed and their reporting

requirements are also stated. The debt of both companies

has increased in the last three years so the companies have

to reduce their expenses and make proper budget to reduce

their debt.

11

for which the primary government is accountable and the

other company which has a relationship with the primary

government.

The reporting entity has to comply with the International

Accounting Standards so that the transparency can be

maintained in the company. The requirements of the

international accounting standards help the company in

achieving comparability and consistency in financial

reporting (Vernimmen, et al., 2014).

Conclusion

It has been analyzed from the above evaluation that

corporate accounting is the branch of the accounting which

deals with the financial accounts of the company. In this

report, two reputed companies are chosen which Amcor

Limited is and the Alumina Limited and their financial report

for the last three years have been studied thoroughly so that

the performance of the company can be analyzed. The

equity and the liability section of the report have been

studied properly and their terms have been analyzed. In this

report the sources of funds to raise the capital in the

company is also stated and their pros and cons in also

elaborated. In this report the concept of the small, large and

reporting entity has analyzed and their reporting

requirements are also stated. The debt of both companies

has increased in the last three years so the companies have

to reduce their expenses and make proper budget to reduce

their debt.

Accounts

12

References

Abeysekera, I., 2013. Accounting for intellectual assets and

liabilities. Journal of Human Resource Costing &

Accounting, 7(3), pp.7-14.

Alumina Limited, 2016. Annual report. Alumina Limited.

Available at:

http://www.annualreports.com/HostedData/AnnualReportArc

hive/A/ASX_AWC_2016.pdf Accessed on: 23 September

2019.

Alumina Limited, 2017. Annual report. Alumina Limited.

Available at:

http://www.annualreports.com/HostedData/AnnualReportArc

hive/A/ASX_AWC_2017.pdf Accessed on: 23 September

2019.

Alumina Limited, 2018. Annual report. Alumina Limited.

Available at:

http://www.annualreports.com/HostedData/AnnualReports/P

DF/ASX_AWC_2018.pdf Accessed on: 23 September 2019.

Amcor Limited, 2016. Annual report. Amcor Limited.

Available at:

https://assets.ctfassets.net/f7tuyt85vtoa/V80juIB2yAye0kkoq

CcKG/aee38dec167b02c90bbd367a9a14b886/

Amcor_Annual_Report_2016.pdf Accessed on: 23

September 2019.

Amcor Limited, 2017. Annual report. Amcor Limited.

Available at:

https://assets.ctfassets.net/f7tuyt85vtoa/2ckiIO9GXymIqu6qi

8Oo4s/6a9b62ee553e2af1e354e042c6055d8a/

Amcor_Annual_Report_2017.pdf Accessed on: 23

September 2019.

12

References

Abeysekera, I., 2013. Accounting for intellectual assets and

liabilities. Journal of Human Resource Costing &

Accounting, 7(3), pp.7-14.

Alumina Limited, 2016. Annual report. Alumina Limited.

Available at:

http://www.annualreports.com/HostedData/AnnualReportArc

hive/A/ASX_AWC_2016.pdf Accessed on: 23 September

2019.

Alumina Limited, 2017. Annual report. Alumina Limited.

Available at:

http://www.annualreports.com/HostedData/AnnualReportArc

hive/A/ASX_AWC_2017.pdf Accessed on: 23 September

2019.

Alumina Limited, 2018. Annual report. Alumina Limited.

Available at:

http://www.annualreports.com/HostedData/AnnualReports/P

DF/ASX_AWC_2018.pdf Accessed on: 23 September 2019.

Amcor Limited, 2016. Annual report. Amcor Limited.

Available at:

https://assets.ctfassets.net/f7tuyt85vtoa/V80juIB2yAye0kkoq

CcKG/aee38dec167b02c90bbd367a9a14b886/

Amcor_Annual_Report_2016.pdf Accessed on: 23

September 2019.

Amcor Limited, 2017. Annual report. Amcor Limited.

Available at:

https://assets.ctfassets.net/f7tuyt85vtoa/2ckiIO9GXymIqu6qi

8Oo4s/6a9b62ee553e2af1e354e042c6055d8a/

Amcor_Annual_Report_2017.pdf Accessed on: 23

September 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts

13

Amcor Limited, 2018. Annual report. Amcor Limited.

Available at:

https://assets.ctfassets.net/f7tuyt85vtoa/Ry9ogH9cQemqGA

800oiGE/cbcc6bef0d76b79be2a227dfc13a7e87/

Amcor_Annual_Report_2018.PDF Accessed on: 23

September 2019.

ASIC, 2019. Are you a large or a small proprietary

company? Available at: https://asic.gov.au/regulatory-

resources/financial-reporting-and-audit/preparers-of-

financial-reports/are-you-a-large-or-small-proprietary-

company/ Accessed on: 23 September 2019.

Demyanyk, Y., Hryshko, D., Luengo-Prado, M.J. and

Sørensen, B.E., 2017. Moving to a job: The role of home

equity, debt, and access to credit. American Economic

Journal: Macroeconomics, 9(2), pp.149-81.

Gaver, J.J. and Pottier, S.W., 2005. The role of holding

company financial information in the insurer‐rating process:

Evidence from the property‐liability industry. Journal of Risk

and Insurance, 72(1), pp.77-103.

Grossi, G. and Steccolini, I., 2015. Pursuing private or public

accountability in the public sector? Applying IPSASs to

define the reporting entity in municipal

consolidation. International Journal of Public

Administration, 38(4), pp.325-334.

Jackowicz, K., Mielcarz, P. and Wnuczak, P., 2017. Fair

value, equity cash flow and project finance valuation:

ambiguities and a solution. Managerial Finance, 43(8),

pp.914-927.

Kaya, D. and Koch, M., 2015. Countries’ adoption of the

International Financial Reporting Standard for Small and

Medium-sized Entities (IFRS for SMEs)–early empirical

13

Amcor Limited, 2018. Annual report. Amcor Limited.

Available at:

https://assets.ctfassets.net/f7tuyt85vtoa/Ry9ogH9cQemqGA

800oiGE/cbcc6bef0d76b79be2a227dfc13a7e87/

Amcor_Annual_Report_2018.PDF Accessed on: 23

September 2019.

ASIC, 2019. Are you a large or a small proprietary

company? Available at: https://asic.gov.au/regulatory-

resources/financial-reporting-and-audit/preparers-of-

financial-reports/are-you-a-large-or-small-proprietary-

company/ Accessed on: 23 September 2019.

Demyanyk, Y., Hryshko, D., Luengo-Prado, M.J. and

Sørensen, B.E., 2017. Moving to a job: The role of home

equity, debt, and access to credit. American Economic

Journal: Macroeconomics, 9(2), pp.149-81.

Gaver, J.J. and Pottier, S.W., 2005. The role of holding

company financial information in the insurer‐rating process:

Evidence from the property‐liability industry. Journal of Risk

and Insurance, 72(1), pp.77-103.

Grossi, G. and Steccolini, I., 2015. Pursuing private or public

accountability in the public sector? Applying IPSASs to

define the reporting entity in municipal

consolidation. International Journal of Public

Administration, 38(4), pp.325-334.

Jackowicz, K., Mielcarz, P. and Wnuczak, P., 2017. Fair

value, equity cash flow and project finance valuation:

ambiguities and a solution. Managerial Finance, 43(8),

pp.914-927.

Kaya, D. and Koch, M., 2015. Countries’ adoption of the

International Financial Reporting Standard for Small and

Medium-sized Entities (IFRS for SMEs)–early empirical

Accounts

14

evidence. Accounting and Business Research, 45(1), pp.93-

120.

Moskowitz, T.J. and Vissing-Jørgensen, A., 2012. The

returns to entrepreneurial investment: A private equity

premium puzzle?. American Economic Review, 92(4),

pp.745-778.

Patton, A.J., Ramadorai, T. and Streatfield, M., 2015.

Change you can believe in? Hedge fund data revisions. The

Journal of Finance, 70(3), pp.963-999.

Stafievskaya, M.V., Sarycheva, Т.V., Nikolayeva, L.V.,

Vanyukovа, R.А., Danilova, O.A., Semenova, O.A. and

Sokolova, T.A., 2015. Risks in Сonditions of

Uncertainty. Mediterranean Journal of Social Sciences, 6(3

S7), p.107.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and

Salvi, A., 2014. Corporate finance: theory and practice. John

Wiley & Sons.

14

evidence. Accounting and Business Research, 45(1), pp.93-

120.

Moskowitz, T.J. and Vissing-Jørgensen, A., 2012. The

returns to entrepreneurial investment: A private equity

premium puzzle?. American Economic Review, 92(4),

pp.745-778.

Patton, A.J., Ramadorai, T. and Streatfield, M., 2015.

Change you can believe in? Hedge fund data revisions. The

Journal of Finance, 70(3), pp.963-999.

Stafievskaya, M.V., Sarycheva, Т.V., Nikolayeva, L.V.,

Vanyukovа, R.А., Danilova, O.A., Semenova, O.A. and

Sokolova, T.A., 2015. Risks in Сonditions of

Uncertainty. Mediterranean Journal of Social Sciences, 6(3

S7), p.107.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and

Salvi, A., 2014. Corporate finance: theory and practice. John

Wiley & Sons.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.