Corporate Accounting ; Sample Assignment

VerifiedAdded on 2021/06/14

|24

|5441

|54

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Corporate Accounting 1

CORPORATE ACCOUNTING 22754

Author

Course Title

Professor

City

Date

CORPORATE ACCOUNTING 22754

Author

Course Title

Professor

City

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting 2

Table of Contents

Executive Summary.........................................................................................................................1

Introduction.....................................................................................................................................3

Evaluate Whether The Takeover of OAMPS by Wesfarmers in 2006 Was Value Enhancing To

Shareholders....................................................................................................................................6

Rationales behind OAMPS acquisition by Wesfarmers.............................................................6

Acquisition Method Employed During the Takeover................................................................7

Acquisition Analysis Based on Its Offer Price, the Mode of Payment As Well As Amount of

the Goodwill................................................................................................................................8

Amount of Goodwill....................................................................................................................9

Reaction of the market towards the takeover during the announcement date...........................9

Analysis of post-acquisition......................................................................................................10

Whether the takeover was value enhancing to different shareholders.....................................14

Conclusion.................................................................................................................................15

Reference List................................................................................................................................17

Appendices....................................................................................................................................19

Appendix 1: Income Statement..................................................................................................19

Appendix 2: Balance Sheet........................................................................................................21

Table of Contents

Executive Summary.........................................................................................................................1

Introduction.....................................................................................................................................3

Evaluate Whether The Takeover of OAMPS by Wesfarmers in 2006 Was Value Enhancing To

Shareholders....................................................................................................................................6

Rationales behind OAMPS acquisition by Wesfarmers.............................................................6

Acquisition Method Employed During the Takeover................................................................7

Acquisition Analysis Based on Its Offer Price, the Mode of Payment As Well As Amount of

the Goodwill................................................................................................................................8

Amount of Goodwill....................................................................................................................9

Reaction of the market towards the takeover during the announcement date...........................9

Analysis of post-acquisition......................................................................................................10

Whether the takeover was value enhancing to different shareholders.....................................14

Conclusion.................................................................................................................................15

Reference List................................................................................................................................17

Appendices....................................................................................................................................19

Appendix 1: Income Statement..................................................................................................19

Appendix 2: Balance Sheet........................................................................................................21

Corporate Accounting 3

Executive Summary

The assignment was aimed to help students apply the knowledge and skills learnt in evaluating

whether takeover of OAMPS by Wesfarmers was value enhancing or not. As such, this report

presented analysis of OAMPS takeover by Wesfarmers in the year 2006.The report started

with a brief overview of the main rationale behind the takeover. It is then followed by

explanation of the chief method of takeover applied by Wesfarmers in acquiring OAMPS.

Further, the report presented detailed analysis of the takeover based on the offer price, the

method of payment as well as goodwill paid. It also presented analysis as to whether the

goodwill amount was justified and explanation of the market reaction toward the takeover. It

is then concluded by detailed explanation on whether the takeover was value enhancing or not

based on the post-acquisition analysis of the company’s financial performance by end of 2006.

From the analysis it is found out that the takeover enhanced value creation for the shareholders

since given that the Wesfarmers’ strength, this would accelerate competitiveness and growth of

this business. Hence, such coupled with numerous opportunities in the Wesfarmers would yield

tremendous result for the shareholders. Furthermore, given that Wesfarmers understand that the

OAMPS is people driven firm that preserve independence of the form broking activities while

creating a situation for both firms to leverage their combined strengths, the takeover would be

enhancing value creation to the shareholders. This is also based on the fact that the takeover

would deliver better outcomes for the clients and great opportunities for the employees. It was

also found out the takeover of OAMPS by Wesfarmers in 2006 can be said to be value

enhancing to the stakeholders. This is based on the fact that the takeover increases

shareholders wealth for both businesses and parties. Besides, given that earnings before

interest and tax increased three years after the acquisition, this is a clear signal that the

Executive Summary

The assignment was aimed to help students apply the knowledge and skills learnt in evaluating

whether takeover of OAMPS by Wesfarmers was value enhancing or not. As such, this report

presented analysis of OAMPS takeover by Wesfarmers in the year 2006.The report started

with a brief overview of the main rationale behind the takeover. It is then followed by

explanation of the chief method of takeover applied by Wesfarmers in acquiring OAMPS.

Further, the report presented detailed analysis of the takeover based on the offer price, the

method of payment as well as goodwill paid. It also presented analysis as to whether the

goodwill amount was justified and explanation of the market reaction toward the takeover. It

is then concluded by detailed explanation on whether the takeover was value enhancing or not

based on the post-acquisition analysis of the company’s financial performance by end of 2006.

From the analysis it is found out that the takeover enhanced value creation for the shareholders

since given that the Wesfarmers’ strength, this would accelerate competitiveness and growth of

this business. Hence, such coupled with numerous opportunities in the Wesfarmers would yield

tremendous result for the shareholders. Furthermore, given that Wesfarmers understand that the

OAMPS is people driven firm that preserve independence of the form broking activities while

creating a situation for both firms to leverage their combined strengths, the takeover would be

enhancing value creation to the shareholders. This is also based on the fact that the takeover

would deliver better outcomes for the clients and great opportunities for the employees. It was

also found out the takeover of OAMPS by Wesfarmers in 2006 can be said to be value

enhancing to the stakeholders. This is based on the fact that the takeover increases

shareholders wealth for both businesses and parties. Besides, given that earnings before

interest and tax increased three years after the acquisition, this is a clear signal that the

Corporate Accounting 4

takeover was essential and facilitated value creation to all shareholders of both the target

company which was OAMPS and Wesfarmers.

takeover was essential and facilitated value creation to all shareholders of both the target

company which was OAMPS and Wesfarmers.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting 5

Introduction

Takeover is one of the fastest means for organizations to up all the scale of their chief

operations, widen their product portfolio as well as enter to the new markets. Nonetheless, the

main question in relation to takeover is whether they destroy or enhance value creation to the

shareholders. It usually relies on how takeover is implemented and designed. Takeover that

starts with right vision or mission and implemented at right price is said to enhance the

shareholders’ value. Conversely, a takeover that starts with wrong vision or mission and

implemented at wrong price is said to destroy the shareholders’ values. The OAMPS is one of

the Australian largest public listed insurance brokers, with gross revenues of around $1 billion

in the year 2006. It is also the specialist underwriter as well as financial service provider. As

such this report presents analysis of OAMPS takeover by Wesfarmers in the year 2006.

Wesfarmers on the other hand is one of the Australian conglomerates running its operations in

New Zealand and Australia. The company engages in numerous operations like liquor,

convenience stores, supermarkets, home improvements, hotels industrial division and office

supplies. Having a net income of AU$65.98 billion in 2016, the company is considered as one

of the largest firm in Australia by revenue (Wesfarmers Ltd 2006). In addition, it is one of the

largest employers in Australia with over 220,000 personnel. This is aimed at evaluating

whether the takeover had any value enhancement to different shareholders involved. The

report starts with a brief overview of the main rationale behind the takeover. It is then

followed by explanation of the chief method of takeover applied by Wesfarmers in acquiring

OAMPS. Further, the report present detailed analysis of the takeover based on the offer price,

the method of payment as well as goodwill paid. It also presents analysis as to whether the

goodwill amount was justified and explanation of the market reaction toward the takeover. It

Introduction

Takeover is one of the fastest means for organizations to up all the scale of their chief

operations, widen their product portfolio as well as enter to the new markets. Nonetheless, the

main question in relation to takeover is whether they destroy or enhance value creation to the

shareholders. It usually relies on how takeover is implemented and designed. Takeover that

starts with right vision or mission and implemented at right price is said to enhance the

shareholders’ value. Conversely, a takeover that starts with wrong vision or mission and

implemented at wrong price is said to destroy the shareholders’ values. The OAMPS is one of

the Australian largest public listed insurance brokers, with gross revenues of around $1 billion

in the year 2006. It is also the specialist underwriter as well as financial service provider. As

such this report presents analysis of OAMPS takeover by Wesfarmers in the year 2006.

Wesfarmers on the other hand is one of the Australian conglomerates running its operations in

New Zealand and Australia. The company engages in numerous operations like liquor,

convenience stores, supermarkets, home improvements, hotels industrial division and office

supplies. Having a net income of AU$65.98 billion in 2016, the company is considered as one

of the largest firm in Australia by revenue (Wesfarmers Ltd 2006). In addition, it is one of the

largest employers in Australia with over 220,000 personnel. This is aimed at evaluating

whether the takeover had any value enhancement to different shareholders involved. The

report starts with a brief overview of the main rationale behind the takeover. It is then

followed by explanation of the chief method of takeover applied by Wesfarmers in acquiring

OAMPS. Further, the report present detailed analysis of the takeover based on the offer price,

the method of payment as well as goodwill paid. It also presents analysis as to whether the

goodwill amount was justified and explanation of the market reaction toward the takeover. It

Corporate Accounting 6

is then concluded by detailed explanation on whether the takeover was value enhancing or not

based on the post-acquisition analysis of the company’s financial performance by end of 2006.

Evaluate Whether The Takeover of OAMPS by Wesfarmers in 2006 Was Value

Enhancing To Shareholders.

Rationales behind OAMPS acquisition by Wesfarmers

The rationale behind takeover of OAMPS by Wesfarmers in 2006 was mostly to help the firm

compete efficiently in the market. The takeover was also aimed to assist accelerate the

OAMPS growth as well as its competitiveness in the market through Wesfarmers’s strengths.

The takeover is also said to significantly help in lessening competition within the market for

the general insurance services and products as it would cause substantial consolidation in the

market (Theage.com 2007). The takeover was also aimed at providing Wesfarmers with more

differentiated operation base which would in turn enable it explore extra opportunities within

the financial sector. Besides, this takeover was to offer improved penetration and scale in the

specialist insurance levels with numerous platforms for the growth.

Basically, the takeover is considered as value-adding and logical proposal for its shareholders

and the OAMPS’ shareholders. The acquisition also builds on Wesfarmers 2003 takeover of

Lumley Insurance in New Zealand and Australia which was successfully integrated in

Wesfarmers’ insurance division. In fact the takeover is a strong business strategic fit for

Wesfarmers insurance division since both firms focus on developing employees, shareholders

returns as well as consumer services. Therefore, the takeover would create significant business

that would be strong rival within the insurance industry within Australia (Theage.com 2007).

is then concluded by detailed explanation on whether the takeover was value enhancing or not

based on the post-acquisition analysis of the company’s financial performance by end of 2006.

Evaluate Whether The Takeover of OAMPS by Wesfarmers in 2006 Was Value

Enhancing To Shareholders.

Rationales behind OAMPS acquisition by Wesfarmers

The rationale behind takeover of OAMPS by Wesfarmers in 2006 was mostly to help the firm

compete efficiently in the market. The takeover was also aimed to assist accelerate the

OAMPS growth as well as its competitiveness in the market through Wesfarmers’s strengths.

The takeover is also said to significantly help in lessening competition within the market for

the general insurance services and products as it would cause substantial consolidation in the

market (Theage.com 2007). The takeover was also aimed at providing Wesfarmers with more

differentiated operation base which would in turn enable it explore extra opportunities within

the financial sector. Besides, this takeover was to offer improved penetration and scale in the

specialist insurance levels with numerous platforms for the growth.

Basically, the takeover is considered as value-adding and logical proposal for its shareholders

and the OAMPS’ shareholders. The acquisition also builds on Wesfarmers 2003 takeover of

Lumley Insurance in New Zealand and Australia which was successfully integrated in

Wesfarmers’ insurance division. In fact the takeover is a strong business strategic fit for

Wesfarmers insurance division since both firms focus on developing employees, shareholders

returns as well as consumer services. Therefore, the takeover would create significant business

that would be strong rival within the insurance industry within Australia (Theage.com 2007).

Corporate Accounting 7

Besides, the takeover of OAMPS combined with Wesfarmers’ strong statement of the

financial position as well as superb credit rating creates a significant opportunity in accessing

the new underwriting niches and optimizing the reinsurance arrangements (Theage.com 2007).

The takeover is anticipated to be the EPS positive by year end and to meet the takeover’s

benchmarks. It was also anticipated to offer Wesfarmers with more differentiated business

base from which the company can explore extra opportunities within the financial industry.

Acquisition Method Employed During the Takeover

Wesfarmers applied the off-market takeover bid. This is based on the fact that its bid was

mainly subjected to regulatory approval as well as minimum acceptance of 90%. In fact,

OAMPS acceptance of the bid was subjected to absence of another higher bid or offer other

than the one offered by Wesfarmers (Akben-Selcuk & Altiok-Yilmaz 2011). In essence, off-

market bid was applied in this takeover since the takeover entails offer to all stakeholders of

OAMPS in purchase of their shares for specified amount. In essence, it is evident that an off-

market bid was applied evidenced by the fact that separate offers were given for different

classes of the shareholders. It is also evidenced by the fact that the takeover offer was

accompanied by bidder’s statement, which contained information that was designed in

enabling target stakeholders in assessing whether to accept the offer or not as well as

acceptance form (Theage.com 2007). It is also evident that this takeover employed off-market

bid since the bidder which in this case was Wesfarmers made individual offer directly to

OAMPS to acquire its securities. Here, the OAMPS management was free to make decision on

whether to accept the offer for the acquisition or not (Gregoriou & Neuhauser 2007). Given

that the bid entails setting out terms of the offer by Wesfarmers and committing the company

and the OAMPS to takeover bid agreement, it can be stated that the method of takeover

Besides, the takeover of OAMPS combined with Wesfarmers’ strong statement of the

financial position as well as superb credit rating creates a significant opportunity in accessing

the new underwriting niches and optimizing the reinsurance arrangements (Theage.com 2007).

The takeover is anticipated to be the EPS positive by year end and to meet the takeover’s

benchmarks. It was also anticipated to offer Wesfarmers with more differentiated business

base from which the company can explore extra opportunities within the financial industry.

Acquisition Method Employed During the Takeover

Wesfarmers applied the off-market takeover bid. This is based on the fact that its bid was

mainly subjected to regulatory approval as well as minimum acceptance of 90%. In fact,

OAMPS acceptance of the bid was subjected to absence of another higher bid or offer other

than the one offered by Wesfarmers (Akben-Selcuk & Altiok-Yilmaz 2011). In essence, off-

market bid was applied in this takeover since the takeover entails offer to all stakeholders of

OAMPS in purchase of their shares for specified amount. In essence, it is evident that an off-

market bid was applied evidenced by the fact that separate offers were given for different

classes of the shareholders. It is also evidenced by the fact that the takeover offer was

accompanied by bidder’s statement, which contained information that was designed in

enabling target stakeholders in assessing whether to accept the offer or not as well as

acceptance form (Theage.com 2007). It is also evident that this takeover employed off-market

bid since the bidder which in this case was Wesfarmers made individual offer directly to

OAMPS to acquire its securities. Here, the OAMPS management was free to make decision on

whether to accept the offer for the acquisition or not (Gregoriou & Neuhauser 2007). Given

that the bid entails setting out terms of the offer by Wesfarmers and committing the company

and the OAMPS to takeover bid agreement, it can be stated that the method of takeover

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 8

employed in this case was off-market bid. In addition, the method of takeover employed in

this case was off-market bid evidenced by the fact that the agreement obliges OAMPS in

supporting takeover bid and in ensuring that OAMPS management recommend that is

stakeholders accept the acquisition offer provided by Wesfarmers ( Theage.com 2007).

Additionally, given that the agreement entered during the takeover by Wesfarmers set out how

OAMPS and Wesfarmers would work closely together during the takeover bid, this is a clear

signal that the method employed was off-market bid. Besides given that the takeover only

required 90% of the relevant interest in OAMPS shares and 75% of the non-bidder-held

securities by the close of the bid, it can be indicated that the takeover utilized off-market bid

technique during the acquisition of OAMPS.

This method was applied since it is less complex and easier to understand. Furthermore, off-

market bid was applied since it is less flexible compared to scheme arrangement in a takeover

and the offer price could be varied in order to result in an increase in its offer price.

Additionally, the off-market bid was applied since it is mostly made subject to some

conditions that in case triggered could enable the bidder in letting its bid lapses and all the

acceptances would be voided (Al‐Sharkas, Hassan & Lawrence 2008).

Acquisition Analysis Based on Its Offer Price, the Mode of Payment As Well As Amount

of the Goodwill

Wesfarmers offered to purchase shares of OAMPS at $4.5 per each share. In total, the

company made a total offer of around $700 million to the OAMPS (Theage.com 2007). This

offer was recommended by OAMPS board that it would offer Wesfarmers chances to contact

employed in this case was off-market bid. In addition, the method of takeover employed in

this case was off-market bid evidenced by the fact that the agreement obliges OAMPS in

supporting takeover bid and in ensuring that OAMPS management recommend that is

stakeholders accept the acquisition offer provided by Wesfarmers ( Theage.com 2007).

Additionally, given that the agreement entered during the takeover by Wesfarmers set out how

OAMPS and Wesfarmers would work closely together during the takeover bid, this is a clear

signal that the method employed was off-market bid. Besides given that the takeover only

required 90% of the relevant interest in OAMPS shares and 75% of the non-bidder-held

securities by the close of the bid, it can be indicated that the takeover utilized off-market bid

technique during the acquisition of OAMPS.

This method was applied since it is less complex and easier to understand. Furthermore, off-

market bid was applied since it is less flexible compared to scheme arrangement in a takeover

and the offer price could be varied in order to result in an increase in its offer price.

Additionally, the off-market bid was applied since it is mostly made subject to some

conditions that in case triggered could enable the bidder in letting its bid lapses and all the

acceptances would be voided (Al‐Sharkas, Hassan & Lawrence 2008).

Acquisition Analysis Based on Its Offer Price, the Mode of Payment As Well As Amount

of the Goodwill

Wesfarmers offered to purchase shares of OAMPS at $4.5 per each share. In total, the

company made a total offer of around $700 million to the OAMPS (Theage.com 2007). This

offer was recommended by OAMPS board that it would offer Wesfarmers chances to contact

Corporate Accounting 9

the new underwriting slots as well as augment the reinsurance provisions within the market.

Wesfarmers helps 9.8% of the OAMPS shares; hence, the offer represented 29% premium to

the OAMPS’s average stock prices for 90 trading days (Insurance Journal 2006). In other

words, the takeover entailed an offer price of $4.50 for every share to all outstanding shares of

the OAMPS, which was valued at around $700 million. In this case, amount of dividend paid

to the OAMPS stakeholders from that date the announcement was made including final

dividend of around 11 cent for every share by 12th October 2006 would be subtracted from

offer price of around $4.50 every share (Smh.com 2007). The $4.5 per share offer price was

representing 26% premium to OAMPS volume weighted average share for 30 trading days

following the announcement (ACCC 2007). It also represented 29% premium to OAMPS

volume of the weighted average share prices for 90 trading days following the announcement.

It also represented 17% premium to OAMPS closing share prices by 4th September 2006 as

well as 2006 fiscal year price per earnings multiple of around 16.4 times (Theage.com 2007).

The takeover comprises of break-free of approximate 1% of bid value payables to the

Wesfarmers in specific situations (Wesfarmers Ltd 2006).

Goodwill which is considered as intangible assets recorded whenever an organization acquires

another firm. It comprises of prices that is paid for acquired firm minus the fair value of the

company net assets. In essence, to get identifiable assets one should subtract liabilities on

attained firm’s balance sheet from its fair value of the identifiable assets. Therefore, the

amount of goodwill paid by Wesfarmers for acquiring OAMPS was as follows;

Total amount paid to the OAMPS shareholders = $646,368

OAMPS assets before acquisition = 234,061

the new underwriting slots as well as augment the reinsurance provisions within the market.

Wesfarmers helps 9.8% of the OAMPS shares; hence, the offer represented 29% premium to

the OAMPS’s average stock prices for 90 trading days (Insurance Journal 2006). In other

words, the takeover entailed an offer price of $4.50 for every share to all outstanding shares of

the OAMPS, which was valued at around $700 million. In this case, amount of dividend paid

to the OAMPS stakeholders from that date the announcement was made including final

dividend of around 11 cent for every share by 12th October 2006 would be subtracted from

offer price of around $4.50 every share (Smh.com 2007). The $4.5 per share offer price was

representing 26% premium to OAMPS volume weighted average share for 30 trading days

following the announcement (ACCC 2007). It also represented 29% premium to OAMPS

volume of the weighted average share prices for 90 trading days following the announcement.

It also represented 17% premium to OAMPS closing share prices by 4th September 2006 as

well as 2006 fiscal year price per earnings multiple of around 16.4 times (Theage.com 2007).

The takeover comprises of break-free of approximate 1% of bid value payables to the

Wesfarmers in specific situations (Wesfarmers Ltd 2006).

Goodwill which is considered as intangible assets recorded whenever an organization acquires

another firm. It comprises of prices that is paid for acquired firm minus the fair value of the

company net assets. In essence, to get identifiable assets one should subtract liabilities on

attained firm’s balance sheet from its fair value of the identifiable assets. Therefore, the

amount of goodwill paid by Wesfarmers for acquiring OAMPS was as follows;

Total amount paid to the OAMPS shareholders = $646,368

OAMPS assets before acquisition = 234,061

Corporate Accounting 10

Liabilities = 195,252

The fair value of the identifiable assets for the takeover = 234,061 – 195,252 = 38,809

With these it is evident that the amount of goodwill arising on the acquisition was as follows;

Cost of the takeover = cash paid to the shareholders + the costs associated with the acquisition

= 646,368 + 23,726 = 670,094

Goodwill = net cost of the takeover – fair value of the identifiable net assets

= 670,094– 38,809 = 631,285

Amount of Goodwill

The amount of goodwill is usually the variance between costs of the investment in the firm’s

acquiring the other firm financial report and value attributable to numerous liabilities and

assets subjected to acquisition in consolidated financial report. The amount of goodwill

offered; that is $557,370 was justified since it represented appropriate premium and was the

fair and full value for the OAMPS as whole. This is based on the fact that the value was far

higher than the net cash outflow on the takeover;

The net cash flow on the takeover was as follows;

Net cash acquired on the operating account 7,485

The net cash acquired on the broking trust 85,580

Liabilities = 195,252

The fair value of the identifiable assets for the takeover = 234,061 – 195,252 = 38,809

With these it is evident that the amount of goodwill arising on the acquisition was as follows;

Cost of the takeover = cash paid to the shareholders + the costs associated with the acquisition

= 646,368 + 23,726 = 670,094

Goodwill = net cost of the takeover – fair value of the identifiable net assets

= 670,094– 38,809 = 631,285

Amount of Goodwill

The amount of goodwill is usually the variance between costs of the investment in the firm’s

acquiring the other firm financial report and value attributable to numerous liabilities and

assets subjected to acquisition in consolidated financial report. The amount of goodwill

offered; that is $557,370 was justified since it represented appropriate premium and was the

fair and full value for the OAMPS as whole. This is based on the fact that the value was far

higher than the net cash outflow on the takeover;

The net cash flow on the takeover was as follows;

Net cash acquired on the operating account 7,485

The net cash acquired on the broking trust 85,580

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting 11

Cash paid 670,094

The net cash outflow 577,029

In essence, the goodwill amount computed above was justifiable since it is based on the fair

value of the identifiable assets as well as liabilities of the OAMPS which was known at the

date of the acquisition. This amount is fair since it is arising from numerous aspects including

the synergistic savings which was arising from combination of the administrative and

underwriting activities with the current Group operations, inseparable intangible assets like

employees’ experience and skills as well as savings from delisting of the OAMPS.

Reaction of the market towards the takeover during the announcement date

Any time entity takeover another, different individuals within the market have different

reactions towards the takeover. In this case, after the announcement of OAMPS takeover bid,

its stock price is said to move upwards. This was based on the fact that OAMPS shareholders

expected the acquiring company to pay a specified amount of premium for the takeover. These

premiums are usually implausible for approvals by shareholders of OAMPS unless the stock

prices of are viewed to be a above or higher than the prevailing market prices. Under the

OAMPS acquisition, Wesfarmers equates its bid to higher stock price compared to the present

or existing price of the acquired firm; hence, there was increased incentive for different

shareholders in OAMPS in selling the shares to Wesfarmers. Hence, with announcement of

OAMPS takeover by Wesfarmers, market price of OAMPS increased on daily basis. This was

based on the notion that a good number of investors were rushing to purchase OAMPS shares

in order to enjoy higher price per share purchased once Wesfarmers acquire the company. In

Cash paid 670,094

The net cash outflow 577,029

In essence, the goodwill amount computed above was justifiable since it is based on the fair

value of the identifiable assets as well as liabilities of the OAMPS which was known at the

date of the acquisition. This amount is fair since it is arising from numerous aspects including

the synergistic savings which was arising from combination of the administrative and

underwriting activities with the current Group operations, inseparable intangible assets like

employees’ experience and skills as well as savings from delisting of the OAMPS.

Reaction of the market towards the takeover during the announcement date

Any time entity takeover another, different individuals within the market have different

reactions towards the takeover. In this case, after the announcement of OAMPS takeover bid,

its stock price is said to move upwards. This was based on the fact that OAMPS shareholders

expected the acquiring company to pay a specified amount of premium for the takeover. These

premiums are usually implausible for approvals by shareholders of OAMPS unless the stock

prices of are viewed to be a above or higher than the prevailing market prices. Under the

OAMPS acquisition, Wesfarmers equates its bid to higher stock price compared to the present

or existing price of the acquired firm; hence, there was increased incentive for different

shareholders in OAMPS in selling the shares to Wesfarmers. Hence, with announcement of

OAMPS takeover by Wesfarmers, market price of OAMPS increased on daily basis. This was

based on the notion that a good number of investors were rushing to purchase OAMPS shares

in order to enjoy higher price per share purchased once Wesfarmers acquire the company. In

Corporate Accounting 12

other words, after announcement of OAMPS takeover, potential investors and existing

shareholders were trying to purchase as many shares as possible in anticipation that once the

takeover is approved, they would be in a position to sell the shares at higher price enabling

them to make significant amount of return. In addition, the takeover was aimed at helping

Wesfarmers achieve significant rank within the insurance and financial industry. The takeover

aimed to assist Wesfarmers accomplishes its chief commitment to offer the leading insurance

services to its clients.

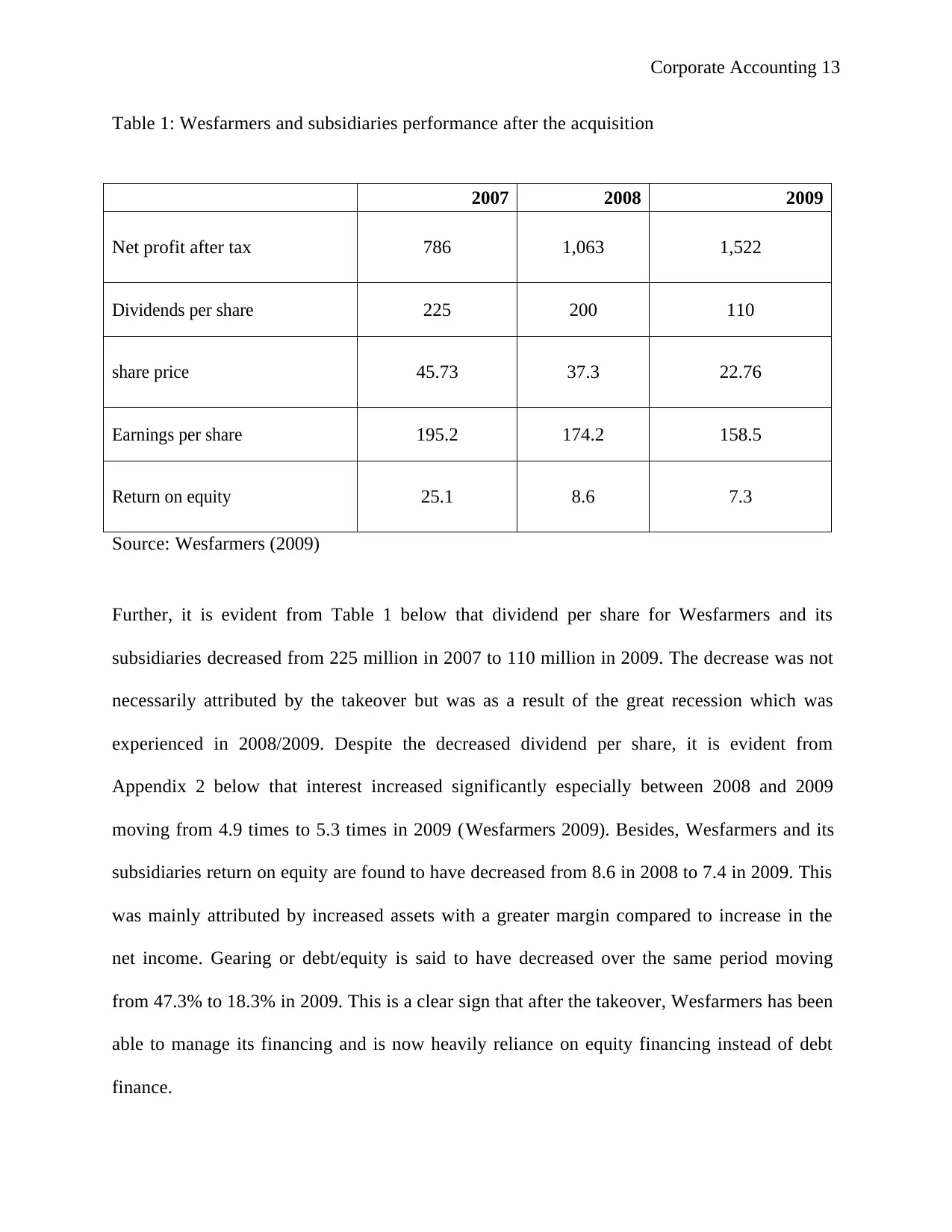

Analysis of post-acquisition

The post-acquisition resulted in doubled year insurance sales for Wesfarmers by year end

2006, adding around $1 billion shares to its current existing insurance segments gross sale of

around $1.1 billion in the previous year. Besides, with the takeover, Wesfarmers insurance

division had pro-forma gross revenue in 2006 of around A$2.1 billion ( Wesfarmers 2007).

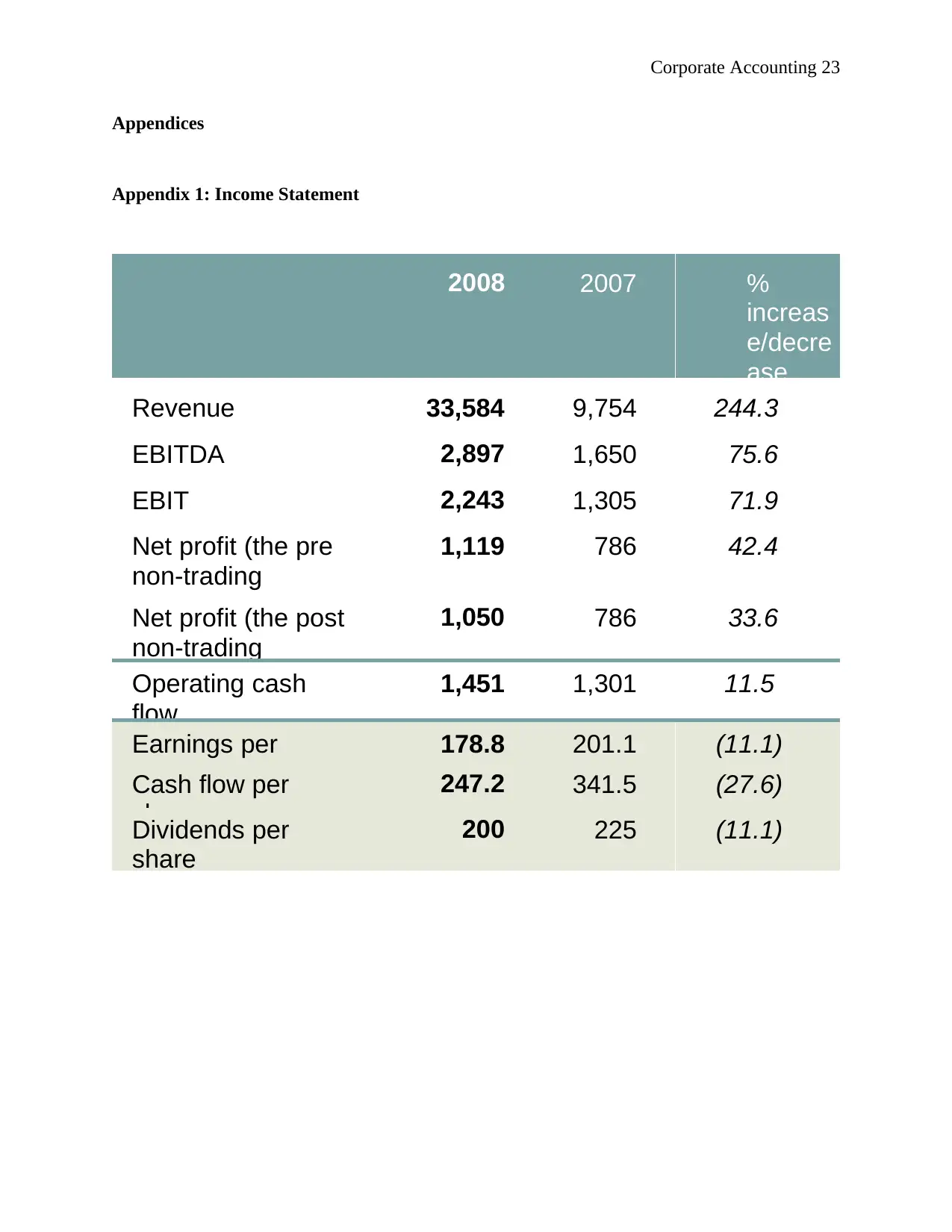

Furthermore, from Table 1 below, it is evident that after the acquisition, Wesfarmers and its

subsidiaries was able to achieve an increasing net income. This is evidenced by the fact that

the company net income increased from 786 million in 2007 to 1,063 million in the year 2008

and later to 1,522 million by 2009 (Wesfarmers 2009). Besides, after the acquisition,

Wesfarmers and its subsidiaries was able to accomplish operating revenue of approximate

$1.4 billion with some solid support from the targeted market industries. Besides, during this

period, earnings before interest and tax was around $130 million while its divisional insurance

margin during this period was 9.5% and its combined operating ratio was around 94.2%. This

trend is said to have changed with the company recording increase in the EBIT with the most

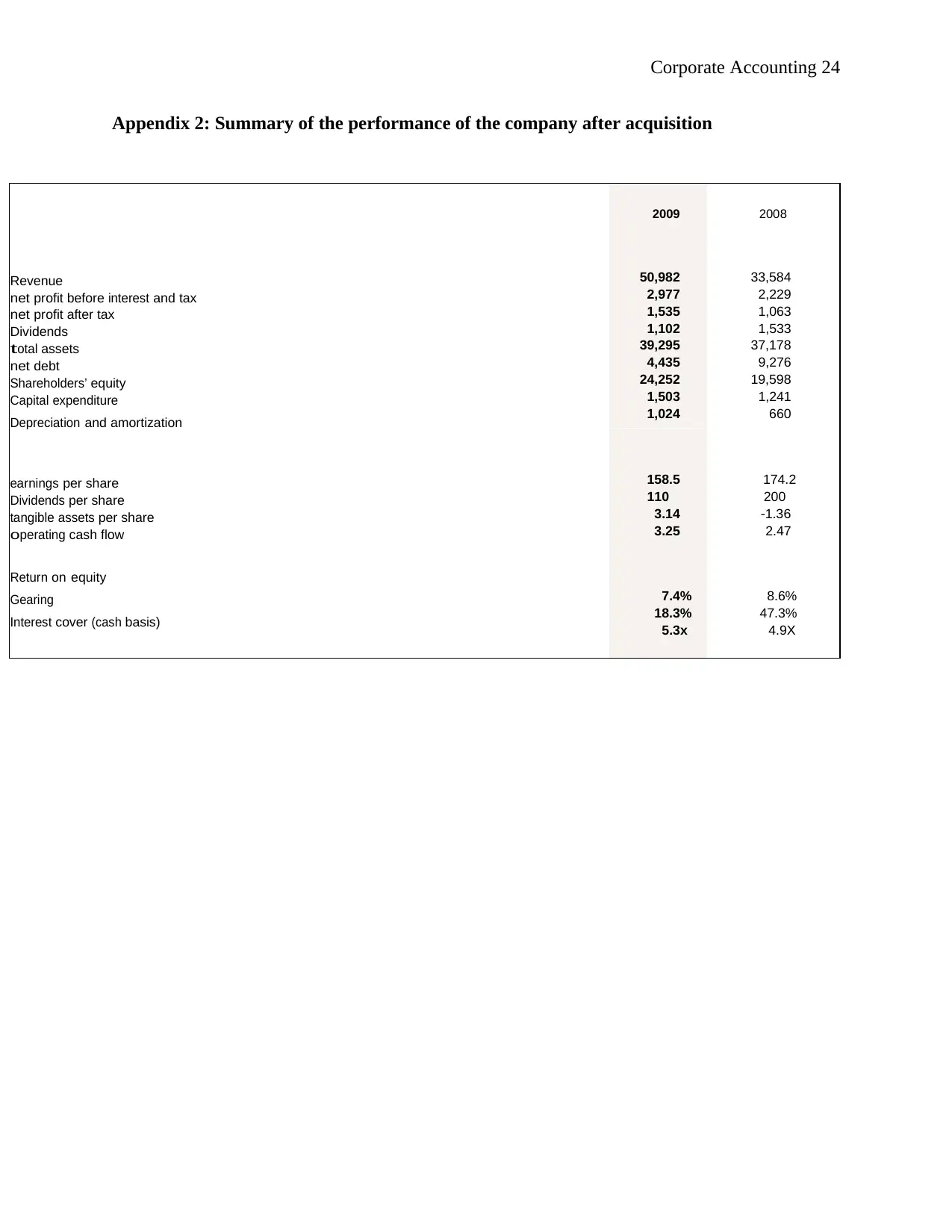

recent being 2,229 million in 2008 to 2,977 in 2009 as shown in Appendix 2 below.

other words, after announcement of OAMPS takeover, potential investors and existing

shareholders were trying to purchase as many shares as possible in anticipation that once the

takeover is approved, they would be in a position to sell the shares at higher price enabling

them to make significant amount of return. In addition, the takeover was aimed at helping

Wesfarmers achieve significant rank within the insurance and financial industry. The takeover

aimed to assist Wesfarmers accomplishes its chief commitment to offer the leading insurance

services to its clients.

Analysis of post-acquisition

The post-acquisition resulted in doubled year insurance sales for Wesfarmers by year end

2006, adding around $1 billion shares to its current existing insurance segments gross sale of

around $1.1 billion in the previous year. Besides, with the takeover, Wesfarmers insurance

division had pro-forma gross revenue in 2006 of around A$2.1 billion ( Wesfarmers 2007).

Furthermore, from Table 1 below, it is evident that after the acquisition, Wesfarmers and its

subsidiaries was able to achieve an increasing net income. This is evidenced by the fact that

the company net income increased from 786 million in 2007 to 1,063 million in the year 2008

and later to 1,522 million by 2009 (Wesfarmers 2009). Besides, after the acquisition,

Wesfarmers and its subsidiaries was able to accomplish operating revenue of approximate

$1.4 billion with some solid support from the targeted market industries. Besides, during this

period, earnings before interest and tax was around $130 million while its divisional insurance

margin during this period was 9.5% and its combined operating ratio was around 94.2%. This

trend is said to have changed with the company recording increase in the EBIT with the most

recent being 2,229 million in 2008 to 2,977 in 2009 as shown in Appendix 2 below.

Corporate Accounting 13

Table 1: Wesfarmers and subsidiaries performance after the acquisition

2007 2008 2009

Net profit after tax 786 1,063 1,522

Dividends per share 225 200 110

share price 45.73 37.3 22.76

Earnings per share 195.2 174.2 158.5

Return on equity 25.1 8.6 7.3

Source: Wesfarmers (2009)

Further, it is evident from Table 1 below that dividend per share for Wesfarmers and its

subsidiaries decreased from 225 million in 2007 to 110 million in 2009. The decrease was not

necessarily attributed by the takeover but was as a result of the great recession which was

experienced in 2008/2009. Despite the decreased dividend per share, it is evident from

Appendix 2 below that interest increased significantly especially between 2008 and 2009

moving from 4.9 times to 5.3 times in 2009 (Wesfarmers 2009). Besides, Wesfarmers and its

subsidiaries return on equity are found to have decreased from 8.6 in 2008 to 7.4 in 2009. This

was mainly attributed by increased assets with a greater margin compared to increase in the

net income. Gearing or debt/equity is said to have decreased over the same period moving

from 47.3% to 18.3% in 2009. This is a clear sign that after the takeover, Wesfarmers has been

able to manage its financing and is now heavily reliance on equity financing instead of debt

finance.

Table 1: Wesfarmers and subsidiaries performance after the acquisition

2007 2008 2009

Net profit after tax 786 1,063 1,522

Dividends per share 225 200 110

share price 45.73 37.3 22.76

Earnings per share 195.2 174.2 158.5

Return on equity 25.1 8.6 7.3

Source: Wesfarmers (2009)

Further, it is evident from Table 1 below that dividend per share for Wesfarmers and its

subsidiaries decreased from 225 million in 2007 to 110 million in 2009. The decrease was not

necessarily attributed by the takeover but was as a result of the great recession which was

experienced in 2008/2009. Despite the decreased dividend per share, it is evident from

Appendix 2 below that interest increased significantly especially between 2008 and 2009

moving from 4.9 times to 5.3 times in 2009 (Wesfarmers 2009). Besides, Wesfarmers and its

subsidiaries return on equity are found to have decreased from 8.6 in 2008 to 7.4 in 2009. This

was mainly attributed by increased assets with a greater margin compared to increase in the

net income. Gearing or debt/equity is said to have decreased over the same period moving

from 47.3% to 18.3% in 2009. This is a clear sign that after the takeover, Wesfarmers has been

able to manage its financing and is now heavily reliance on equity financing instead of debt

finance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 14

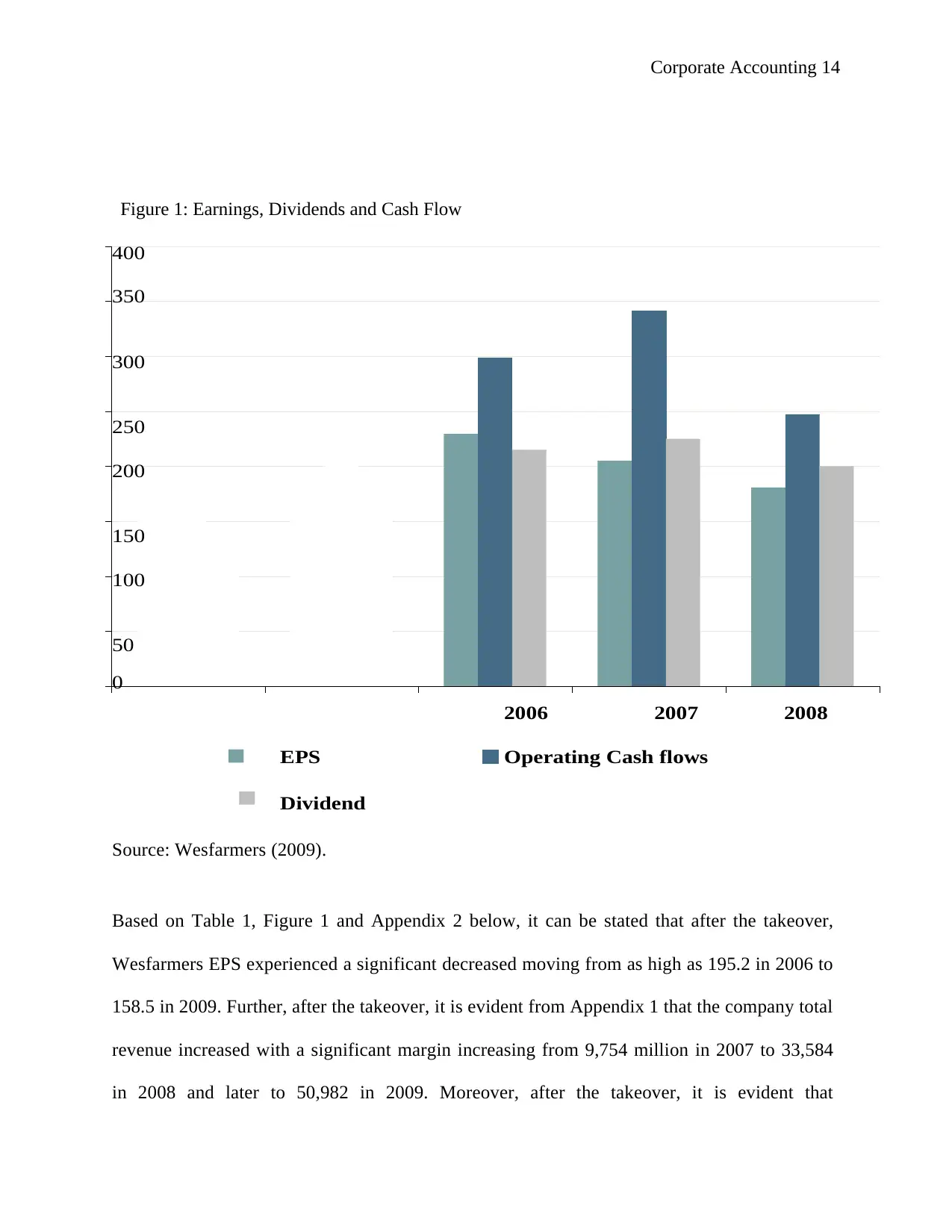

Figure 1: Earnings, Dividends and Cash Flow

400

350

300

250

200

150

100

50

0

2006 2007 2008

EPS Operating Cash flows

Dividend

Source: Wesfarmers (2009).

Based on Table 1, Figure 1 and Appendix 2 below, it can be stated that after the takeover,

Wesfarmers EPS experienced a significant decreased moving from as high as 195.2 in 2006 to

158.5 in 2009. Further, after the takeover, it is evident from Appendix 1 that the company total

revenue increased with a significant margin increasing from 9,754 million in 2007 to 33,584

in 2008 and later to 50,982 in 2009. Moreover, after the takeover, it is evident that

Figure 1: Earnings, Dividends and Cash Flow

400

350

300

250

200

150

100

50

0

2006 2007 2008

EPS Operating Cash flows

Dividend

Source: Wesfarmers (2009).

Based on Table 1, Figure 1 and Appendix 2 below, it can be stated that after the takeover,

Wesfarmers EPS experienced a significant decreased moving from as high as 195.2 in 2006 to

158.5 in 2009. Further, after the takeover, it is evident from Appendix 1 that the company total

revenue increased with a significant margin increasing from 9,754 million in 2007 to 33,584

in 2008 and later to 50,982 in 2009. Moreover, after the takeover, it is evident that

Corporate Accounting 15

Wesfarmers operating cash flows increased from around $2.47 per share in 2008 to around

$3.25 per share in the financial year 2009 (Wesfarmers 2009).

Furthermore, it is evident from Appendix 2 below that after the takeover; shareholder’s equity

of Wesfarmers increased with year 2008 recording 19,598 and year 2009 the company

recording shareholders’ equity of around 24,252 (Wesfarmers 2009). This means that the

takeover enhanced different shareholders to invest in the company; hence, the increase in

shareholder’s value. The depreciation and amortization of the company increased over three

years after the takeover with the company recording depreciation and amortization of around

660 million and in 2009 the company recorded depreciation and amortization of around 1,024

million. Furthermore, after the acquisition, it is evident that the company capital expenditure

on the PPE and the intangibles increased over the next three years after the acquisition. This is

evident by increase in capital expenditure from 1,241 million in 2008 to 1,503 million in 2009

(Appendix 2).

Whether the takeover was value enhancing to different shareholders

The takeover of OAMPS by Wesfarmers in 2006 can be said to be value enhancing to the

stakeholders. This is based on the fact that the takeover increases shareholders wealth for both

parties and companies. The takeover would be value enhancing since combination of the

Wesfarmers insurance division and the OAMPS would create significant business operations

which would be strong rival in insurance sector within the country. In addition, the takeover

was value enhancing since both firms were mostly focused on the customer service,

developing employees as well as on the shareholder’s returns; therefore, combining them

would enhance greater shareholder’s returns over time. In essence, the takeover would be

Wesfarmers operating cash flows increased from around $2.47 per share in 2008 to around

$3.25 per share in the financial year 2009 (Wesfarmers 2009).

Furthermore, it is evident from Appendix 2 below that after the takeover; shareholder’s equity

of Wesfarmers increased with year 2008 recording 19,598 and year 2009 the company

recording shareholders’ equity of around 24,252 (Wesfarmers 2009). This means that the

takeover enhanced different shareholders to invest in the company; hence, the increase in

shareholder’s value. The depreciation and amortization of the company increased over three

years after the takeover with the company recording depreciation and amortization of around

660 million and in 2009 the company recorded depreciation and amortization of around 1,024

million. Furthermore, after the acquisition, it is evident that the company capital expenditure

on the PPE and the intangibles increased over the next three years after the acquisition. This is

evident by increase in capital expenditure from 1,241 million in 2008 to 1,503 million in 2009

(Appendix 2).

Whether the takeover was value enhancing to different shareholders

The takeover of OAMPS by Wesfarmers in 2006 can be said to be value enhancing to the

stakeholders. This is based on the fact that the takeover increases shareholders wealth for both

parties and companies. The takeover would be value enhancing since combination of the

Wesfarmers insurance division and the OAMPS would create significant business operations

which would be strong rival in insurance sector within the country. In addition, the takeover

was value enhancing since both firms were mostly focused on the customer service,

developing employees as well as on the shareholder’s returns; therefore, combining them

would enhance greater shareholder’s returns over time. In essence, the takeover would be

Corporate Accounting 16

value enhancing since it combines the strong balance sheet as well as credit rating of the

Wesfarmers and OAMPS’ specialists or professional underwriting skills which would assist in

creating opportunities in accessing new underwriting slots and in optimizing the reinsurance

schedules. In addition, the takeover enhanced value creation since the offer represented best

outcome for the OAMPS stockholders both in certainty and price. Besides, given that earnings

before interest and tax increased in the year 2007, 2008 and 2009, this is a clear signal that the

takeover was essential and facilitated value creation to all shareholders of both the target

company which was OAMPS and Wesfarmers. In addition, given that the acquisition of

OAMPS contributed around $24.8 million in net income for Wesfarmers, this is a good

indication that the takeover was value creating or enhancing to different shareholders. Besides,

with Wesfarmers having recorded a net profit of around $1,063 million in 2008 and $1,535

million in 2009 which is a significant increase of about 20% excluding impact of sales of the

Australian Railroad Group, this is enough evidence that the takeover enhanced value creation

to all the shareholders. Moreover, given that Wesfarmers operating cash flows increased by

21% to around $2.47 per share in 2008 to $3.24 per share in the year 2009, it can be indicated

that the takeover was value enhancing to different shareholder.

Besides, with the takeover having contributed around $24.8 million in net income for

Wesfarmers, this is another clear sign that the takeover was significant to all the shareholders

since increase in net income means higher returns or EPS for the shareholders. Additionally,

given that after the takeover Wesfarmers was able to normalize its earnings per share by over

23% to approximate $195.2 in 2007 to around $174.2 in 2008 and later to $160 in 2009, this

means that the takeover added greater value to different shareholders. Another sign which

could be interpreted as a good signal to value creation for the shareholders was the fact that

value enhancing since it combines the strong balance sheet as well as credit rating of the

Wesfarmers and OAMPS’ specialists or professional underwriting skills which would assist in

creating opportunities in accessing new underwriting slots and in optimizing the reinsurance

schedules. In addition, the takeover enhanced value creation since the offer represented best

outcome for the OAMPS stockholders both in certainty and price. Besides, given that earnings

before interest and tax increased in the year 2007, 2008 and 2009, this is a clear signal that the

takeover was essential and facilitated value creation to all shareholders of both the target

company which was OAMPS and Wesfarmers. In addition, given that the acquisition of

OAMPS contributed around $24.8 million in net income for Wesfarmers, this is a good

indication that the takeover was value creating or enhancing to different shareholders. Besides,

with Wesfarmers having recorded a net profit of around $1,063 million in 2008 and $1,535

million in 2009 which is a significant increase of about 20% excluding impact of sales of the

Australian Railroad Group, this is enough evidence that the takeover enhanced value creation

to all the shareholders. Moreover, given that Wesfarmers operating cash flows increased by

21% to around $2.47 per share in 2008 to $3.24 per share in the year 2009, it can be indicated

that the takeover was value enhancing to different shareholder.

Besides, with the takeover having contributed around $24.8 million in net income for

Wesfarmers, this is another clear sign that the takeover was significant to all the shareholders

since increase in net income means higher returns or EPS for the shareholders. Additionally,

given that after the takeover Wesfarmers was able to normalize its earnings per share by over

23% to approximate $195.2 in 2007 to around $174.2 in 2008 and later to $160 in 2009, this

means that the takeover added greater value to different shareholders. Another sign which

could be interpreted as a good signal to value creation for the shareholders was the fact that

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting 17

debt decreased from 9,276 million in 2008 to 4,435 million in 2009. Such implies that all the

shareholders have been enjoying relatively low debt burden after the acquisition.

Given decreased interest coverage from 4.9 in 2008 to 5.3 in 2009, it can also be stated that

the deals enhanced value creation to the shareholders. The decrease was attributed by

decreased debts which are in turn resulted in decreased interest rates. Further, provided that

Wesfarmers shareholders’ equity increased three years after the acquisition, this is a sign that

the company was now effective enough in utilizing its shareholders’ equity to produce some

income. This is based on the fact that increased shareholder’s equity means increased

shareholders’ value in the company which they are likely to enjoy in terms of dividends at the

end of the year. Besides, with increased stock price after the takeover, it is evident that this

takeover was value enhancer to all shareholders since higher stock price means higher returns

for the company and in turn higher dividends would be offered to the shareholders.

With these, it is evident that the takeover enhanced value creation to all the shareholders.

Additionally, given that Gearing or debt/equity decreased after the takeover, this is a good

signal sign that the takeover, was value enhancer to different shareholders since decreased

debt/equity implies that Wesfarmers was able to manage all its financing and was currently

utilizing shareholders’ equity to finance its operations. This is a greater stride since with

decreased debt financing it means that the company is not volatile to being liquidated.

Conclusion

In conclusion, takeover is one of the fastest means for organizations to up all the scale of their

chief operations, widen their product portfolio as well as enter to the new markets.

debt decreased from 9,276 million in 2008 to 4,435 million in 2009. Such implies that all the

shareholders have been enjoying relatively low debt burden after the acquisition.

Given decreased interest coverage from 4.9 in 2008 to 5.3 in 2009, it can also be stated that

the deals enhanced value creation to the shareholders. The decrease was attributed by

decreased debts which are in turn resulted in decreased interest rates. Further, provided that

Wesfarmers shareholders’ equity increased three years after the acquisition, this is a sign that

the company was now effective enough in utilizing its shareholders’ equity to produce some

income. This is based on the fact that increased shareholder’s equity means increased

shareholders’ value in the company which they are likely to enjoy in terms of dividends at the

end of the year. Besides, with increased stock price after the takeover, it is evident that this

takeover was value enhancer to all shareholders since higher stock price means higher returns

for the company and in turn higher dividends would be offered to the shareholders.

With these, it is evident that the takeover enhanced value creation to all the shareholders.

Additionally, given that Gearing or debt/equity decreased after the takeover, this is a good

signal sign that the takeover, was value enhancer to different shareholders since decreased

debt/equity implies that Wesfarmers was able to manage all its financing and was currently

utilizing shareholders’ equity to finance its operations. This is a greater stride since with

decreased debt financing it means that the company is not volatile to being liquidated.

Conclusion

In conclusion, takeover is one of the fastest means for organizations to up all the scale of their

chief operations, widen their product portfolio as well as enter to the new markets.

Corporate Accounting 18

Nonetheless, the main question in relation to takeover is whether they destroy or enhance

value creation to the shareholders. The OAMPS was one of the Australian largest public listed

insurance broker, with a gross revenue of around $1 billion in the year 2006. It is also the

specialist underwriter as well as financial service provider. Wesfarmers on the other hand is

one of the Australian conglomerates running its operations in New Zealand and Australia.

Based on the above analysis it can be concluded that the takeover enhance value creation for the

shareholders since given that the Wesfarmers’ strength, this would accelerate competitiveness

and growth of this business. Hence, such coupled with numerous opportunities in the

Wesfarmers would yield tremendous result for the shareholders.

Furthermore, given that Wesfarmers understand that the OAMPS is people driven firm that

preserve independence of the form broking activities while creating a situation for both firms to

leverage their combined strengths, the takeover would be enhancing value creation to the

shareholders. This is also based on the fact that the takeover would deliver better outcomes for

the clients and great opportunities for the employees. It can also be concluded from the analysis

that the takeover of OAMPS by Wesfarmers in 2006 can be said to be value enhancing to the

stakeholders since it increases shareholders wealth for both business and parties. It can also be

stated that the takeover was value enhancing since combination of the Wesfarmers insurance

division and the OAMPS would create significant business operations which would be strong

rival in insurance sector within the country. Additionally, based on the financial analysis

during the post-acquisition, it is evident that the takeover was value enhancing since both

firms were mostly focused on the customer service, developing employees as well as on the

shareholder’s returns; therefore, combining them would enhance greater shareholder’s returns

over time.

Nonetheless, the main question in relation to takeover is whether they destroy or enhance

value creation to the shareholders. The OAMPS was one of the Australian largest public listed

insurance broker, with a gross revenue of around $1 billion in the year 2006. It is also the

specialist underwriter as well as financial service provider. Wesfarmers on the other hand is

one of the Australian conglomerates running its operations in New Zealand and Australia.

Based on the above analysis it can be concluded that the takeover enhance value creation for the

shareholders since given that the Wesfarmers’ strength, this would accelerate competitiveness

and growth of this business. Hence, such coupled with numerous opportunities in the

Wesfarmers would yield tremendous result for the shareholders.

Furthermore, given that Wesfarmers understand that the OAMPS is people driven firm that

preserve independence of the form broking activities while creating a situation for both firms to

leverage their combined strengths, the takeover would be enhancing value creation to the

shareholders. This is also based on the fact that the takeover would deliver better outcomes for

the clients and great opportunities for the employees. It can also be concluded from the analysis

that the takeover of OAMPS by Wesfarmers in 2006 can be said to be value enhancing to the

stakeholders since it increases shareholders wealth for both business and parties. It can also be

stated that the takeover was value enhancing since combination of the Wesfarmers insurance

division and the OAMPS would create significant business operations which would be strong

rival in insurance sector within the country. Additionally, based on the financial analysis

during the post-acquisition, it is evident that the takeover was value enhancing since both

firms were mostly focused on the customer service, developing employees as well as on the

shareholder’s returns; therefore, combining them would enhance greater shareholder’s returns

over time.

Corporate Accounting 19

In essence, the takeover would be value enhancing since it combines the strong balance sheet

as well as credit rating of the Wesfarmers and OAMPS’ specialists or professional

underwriting skills which would assist in creating opportunities in accessing new underwriting

slots and in optimizing the reinsurance schedules. In addition, the takeover enhanced value

creation since the offer represented best upshot for the OAMPS stockholders both in certainty

and price. Further, it can be stated that the takeover of OAMPS by Wesfarmers was value

enhancing to the shareholder since it was able to normalize Wesfarmers’ earnings per share by

over 23%, meaning that the takeover added some value to all the shareholders in terms of

EPS.

In essence, the takeover would be value enhancing since it combines the strong balance sheet

as well as credit rating of the Wesfarmers and OAMPS’ specialists or professional

underwriting skills which would assist in creating opportunities in accessing new underwriting

slots and in optimizing the reinsurance schedules. In addition, the takeover enhanced value

creation since the offer represented best upshot for the OAMPS stockholders both in certainty

and price. Further, it can be stated that the takeover of OAMPS by Wesfarmers was value

enhancing to the shareholder since it was able to normalize Wesfarmers’ earnings per share by

over 23%, meaning that the takeover added some value to all the shareholders in terms of

EPS.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 20

Reference List

ACCC 2007, Wesfarmers Limited - proposed acquisition of OAMPS Limited: Available from:

http://registers.accc.gov.au/content/index.phtml/itemId/764466/fromItemId/751043 [Access at

25th May 2018]

Akben-Selcuk, E & Altiok-Yilmaz, A 2011, ‘The impact of mergers and acquisitions on acquirer

performance: Evidence from Turkey,’ Business and Economics Journal, 22, 1-8.

Al‐Sharkas, AA, Hassan, MK, & Lawrence, S 2008, ‘The impact of mergers and acquisitions on

the efficiency of the US banking industry: Further evidence,’ Journal of Business Finance &

Accounting, 35(1‐2), 50-70.

Gregoriou, G & Neuhauser, K 2007, Mergers and acquisitions: current issues. Springer.

Harford, J, Jenter, D & Li, K 2011, ‘Institutional cross-holdings and their effect on acquisition

decisions,’ Journal of Financial Economics, 99(1), 27-39.

Insurance Journal 2006, Wesfarmers Makes $534 Million Offer for Australian Broker OAMPS:

Available from: https://www.insurancejournal.com/news/international/2006/09/07/72142.htm

[Access at 25th May 2018]

Kumar, S & Bansal, LK 2008, ‘The impact of mergers and acquisitions on corporate

performance in India,’ Management Decision, 46(10), 1531-1543.

Reference List

ACCC 2007, Wesfarmers Limited - proposed acquisition of OAMPS Limited: Available from:

http://registers.accc.gov.au/content/index.phtml/itemId/764466/fromItemId/751043 [Access at

25th May 2018]

Akben-Selcuk, E & Altiok-Yilmaz, A 2011, ‘The impact of mergers and acquisitions on acquirer

performance: Evidence from Turkey,’ Business and Economics Journal, 22, 1-8.

Al‐Sharkas, AA, Hassan, MK, & Lawrence, S 2008, ‘The impact of mergers and acquisitions on

the efficiency of the US banking industry: Further evidence,’ Journal of Business Finance &

Accounting, 35(1‐2), 50-70.

Gregoriou, G & Neuhauser, K 2007, Mergers and acquisitions: current issues. Springer.

Harford, J, Jenter, D & Li, K 2011, ‘Institutional cross-holdings and their effect on acquisition

decisions,’ Journal of Financial Economics, 99(1), 27-39.

Insurance Journal 2006, Wesfarmers Makes $534 Million Offer for Australian Broker OAMPS:

Available from: https://www.insurancejournal.com/news/international/2006/09/07/72142.htm

[Access at 25th May 2018]

Kumar, S & Bansal, LK 2008, ‘The impact of mergers and acquisitions on corporate

performance in India,’ Management Decision, 46(10), 1531-1543.

Corporate Accounting 21

Liargovas, P & Repousis, S 2011, ‘The impact of mergers and acquisitions on the performance

of the Greek banking sector: An event study approach,’ International Journal of Economics and

Finance, 3(2), 89.

Marembo, J 2012, ‘The Impact of Mergers and Acquisitions on the financial performance of

Commercial Banks in Kenya,’ Unpublished MBA thesis. University of Nairobi.

Reiser, I & Nishikawa, RM 2010, ‘Task‐based assessment of breast tomosynthesis: Effect of

acquisition parameters and quantum noise,’ Medical physics, 37(4), 1591-1600.

Slobin, DI 2014, The crosslinguistic study of language acquisition (Vol. 4). Psychology Press.

Smh.com 2007, W'farmers triggers chase for OAMPS: Available from:

https://www.smh.com.au/news/business/wfarmers-triggers-chase-for-oamps/

2006/09/05/1157222131439.html [Access at 25th May 2018]

Theage.com (2007), Wesfarmers makes takeover offer for OAMPS: Available from:

https://www.theage.com.au/news/business/wesfarmers-makes-takeover-offer-for-oamps/

2006/09/05/1157222107331.html [Access at 25th May 2018]

Wesfarmers Ltd (2006), Wesfarmers Ltd 2006 annual report: Available from:

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/wesfarmers-2006-

annual-report.pdf?sfvrsn=0 [Access at 25th May 2018]

Liargovas, P & Repousis, S 2011, ‘The impact of mergers and acquisitions on the performance

of the Greek banking sector: An event study approach,’ International Journal of Economics and

Finance, 3(2), 89.

Marembo, J 2012, ‘The Impact of Mergers and Acquisitions on the financial performance of

Commercial Banks in Kenya,’ Unpublished MBA thesis. University of Nairobi.

Reiser, I & Nishikawa, RM 2010, ‘Task‐based assessment of breast tomosynthesis: Effect of

acquisition parameters and quantum noise,’ Medical physics, 37(4), 1591-1600.

Slobin, DI 2014, The crosslinguistic study of language acquisition (Vol. 4). Psychology Press.

Smh.com 2007, W'farmers triggers chase for OAMPS: Available from:

https://www.smh.com.au/news/business/wfarmers-triggers-chase-for-oamps/

2006/09/05/1157222131439.html [Access at 25th May 2018]

Theage.com (2007), Wesfarmers makes takeover offer for OAMPS: Available from:

https://www.theage.com.au/news/business/wesfarmers-makes-takeover-offer-for-oamps/

2006/09/05/1157222107331.html [Access at 25th May 2018]

Wesfarmers Ltd (2006), Wesfarmers Ltd 2006 annual report: Available from:

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/wesfarmers-2006-

annual-report.pdf?sfvrsn=0 [Access at 25th May 2018]

Corporate Accounting 22

Wesfarmers 2007, Wesfarmers Ltd 2007 annual report: Available from:

https://www.wesfarmers.com.au/docs/default-source/reports/2006-2007-annual-report.pdf?

sfvrsn=2 [Access at 25th May 2018]

Wesfarmers Ltd 2009, Wesfarmers Ltd 2009 annual report: Available from:

https://www.wesfarmers.com.au/docs/default-source/reports/2009-annual-report.pdf?sfvrsn=2

[Access at 25th May 2018]

Wesfarmers 2007, Wesfarmers Ltd 2007 annual report: Available from:

https://www.wesfarmers.com.au/docs/default-source/reports/2006-2007-annual-report.pdf?

sfvrsn=2 [Access at 25th May 2018]

Wesfarmers Ltd 2009, Wesfarmers Ltd 2009 annual report: Available from:

https://www.wesfarmers.com.au/docs/default-source/reports/2009-annual-report.pdf?sfvrsn=2

[Access at 25th May 2018]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting 23

Appendices

Appendix 1: Income Statement

2008 2007 %

increas

e/decre

ase

Revenue 33,584 9,754 244.3

EBITDA 2,897 1,650 75.6

EBIT 2,243 1,305 71.9

Net profit (the pre

non-trading

components)

1,119 786 42.4

Net profit (the post

non-trading

1,050 786 33.6

Operating cash

flow

1,451 1,301 11.5

Earnings per

share

178.8 201.1 (11.1)

Cash flow per

share

247.2 341.5 (27.6)

Dividends per

share

200 225 (11.1)

Appendices

Appendix 1: Income Statement

2008 2007 %

increas

e/decre

ase

Revenue 33,584 9,754 244.3

EBITDA 2,897 1,650 75.6

EBIT 2,243 1,305 71.9

Net profit (the pre

non-trading

components)

1,119 786 42.4

Net profit (the post

non-trading

1,050 786 33.6

Operating cash

flow

1,451 1,301 11.5

Earnings per

share

178.8 201.1 (11.1)

Cash flow per

share

247.2 341.5 (27.6)

Dividends per

share

200 225 (11.1)

Corporate Accounting 24

Appendix 2: Summary of the performance of the company after acquisition

2009 2008

Revenue

net profit before interest and tax

net profit after tax

Dividends

total assets

net debt

Shareholders’ equity

Capital expenditure

Depreciation and amortization

50,982

2,977

1,535

1,102

39,295

4,435

24,252

1,503

1,024

33,584

2,229

1,063

1,533

37,178

9,276

19,598

1,241

660

earnings per share

Dividends per share

tangible assets per share

o perating cash flow

158.5

110

3.14

3.25

174.2

200

-1.36

2.47

Return on equity

Gearing

Interest cover (cash basis)

7.4%

18.3%

5.3x

8.6%

47.3%

4.9X

Appendix 2: Summary of the performance of the company after acquisition

2009 2008

Revenue

net profit before interest and tax

net profit after tax

Dividends

total assets

net debt

Shareholders’ equity

Capital expenditure

Depreciation and amortization

50,982

2,977

1,535

1,102

39,295

4,435

24,252

1,503

1,024

33,584

2,229

1,063

1,533

37,178

9,276

19,598

1,241

660

earnings per share

Dividends per share

tangible assets per share

o perating cash flow

158.5

110

3.14

3.25

174.2

200

-1.36

2.47

Return on equity

Gearing

Interest cover (cash basis)

7.4%

18.3%

5.3x

8.6%

47.3%

4.9X

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.