Corporate Accounting - Sample Assignment PDF

VerifiedAdded on 2021/06/15

|9

|2232

|42

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HI5020 Corporate Accounting

Assessment 2 – Retail Food Group

STUDENT ID:

[Pick the date]

Assessment 2 – Retail Food Group

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting

RFG (Retail Food Group) is the company that is chosen to complete the assessment.

Considering that the most recent annual report is to taken, hence annual report for FY2107

has been taken for extracting various relevant data required for this task.

CASH FLOWS STATEMENT

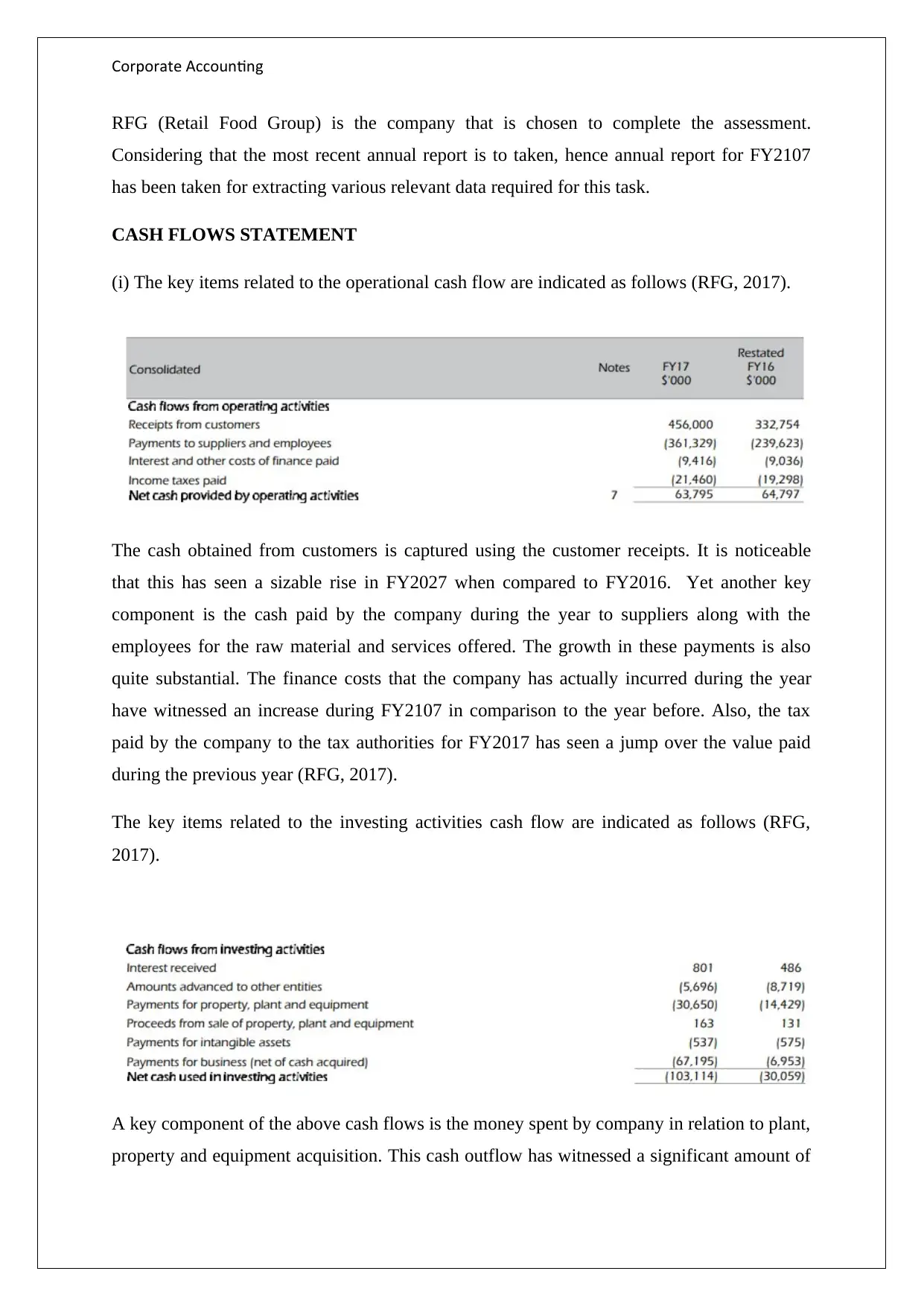

(i) The key items related to the operational cash flow are indicated as follows (RFG, 2017).

The cash obtained from customers is captured using the customer receipts. It is noticeable

that this has seen a sizable rise in FY2027 when compared to FY2016. Yet another key

component is the cash paid by the company during the year to suppliers along with the

employees for the raw material and services offered. The growth in these payments is also

quite substantial. The finance costs that the company has actually incurred during the year

have witnessed an increase during FY2107 in comparison to the year before. Also, the tax

paid by the company to the tax authorities for FY2017 has seen a jump over the value paid

during the previous year (RFG, 2017).

The key items related to the investing activities cash flow are indicated as follows (RFG,

2017).

A key component of the above cash flows is the money spent by company in relation to plant,

property and equipment acquisition. This cash outflow has witnessed a significant amount of

RFG (Retail Food Group) is the company that is chosen to complete the assessment.

Considering that the most recent annual report is to taken, hence annual report for FY2107

has been taken for extracting various relevant data required for this task.

CASH FLOWS STATEMENT

(i) The key items related to the operational cash flow are indicated as follows (RFG, 2017).

The cash obtained from customers is captured using the customer receipts. It is noticeable

that this has seen a sizable rise in FY2027 when compared to FY2016. Yet another key

component is the cash paid by the company during the year to suppliers along with the

employees for the raw material and services offered. The growth in these payments is also

quite substantial. The finance costs that the company has actually incurred during the year

have witnessed an increase during FY2107 in comparison to the year before. Also, the tax

paid by the company to the tax authorities for FY2017 has seen a jump over the value paid

during the previous year (RFG, 2017).

The key items related to the investing activities cash flow are indicated as follows (RFG,

2017).

A key component of the above cash flows is the money spent by company in relation to plant,

property and equipment acquisition. This cash outflow has witnessed a significant amount of

Corporate Accounting

increase in the year ending on June 30, 2017 in comparison to the year ending on June 30,

2016. Further, the company also tends to liquidate some of the plant, property and equipment

holdings which it considers as redundant and cash inflows are realised from the same.

Besides, a sizable chunk of cash is used by the company to purchase various businesses along

with acquiring intangible assets particularly brands. There is a huge jump in cash outflow on

account of investing activities in FY2017 (RFG, 2017).

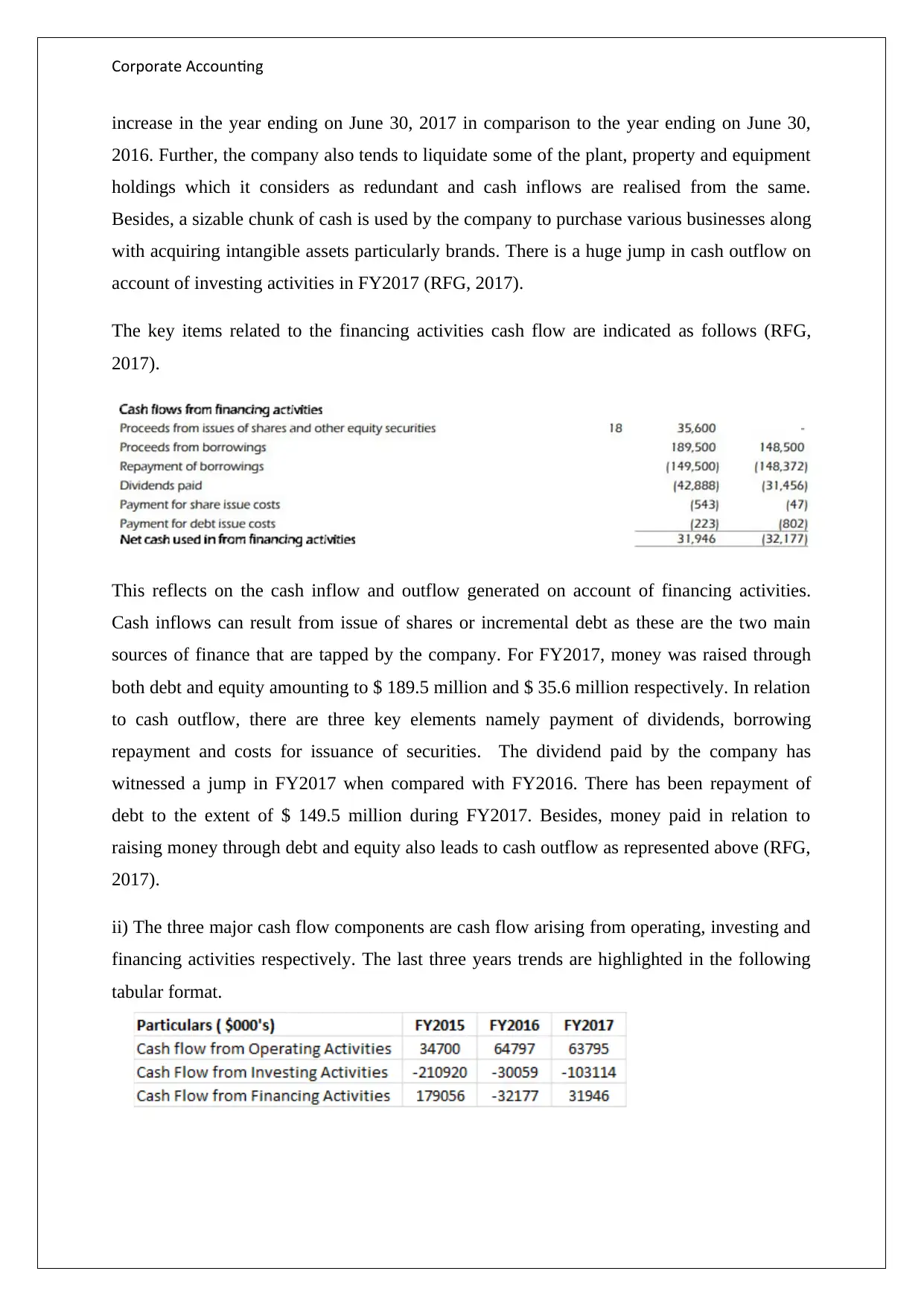

The key items related to the financing activities cash flow are indicated as follows (RFG,

2017).

This reflects on the cash inflow and outflow generated on account of financing activities.

Cash inflows can result from issue of shares or incremental debt as these are the two main

sources of finance that are tapped by the company. For FY2017, money was raised through

both debt and equity amounting to $ 189.5 million and $ 35.6 million respectively. In relation

to cash outflow, there are three key elements namely payment of dividends, borrowing

repayment and costs for issuance of securities. The dividend paid by the company has

witnessed a jump in FY2017 when compared with FY2016. There has been repayment of

debt to the extent of $ 149.5 million during FY2017. Besides, money paid in relation to

raising money through debt and equity also leads to cash outflow as represented above (RFG,

2017).

ii) The three major cash flow components are cash flow arising from operating, investing and

financing activities respectively. The last three years trends are highlighted in the following

tabular format.

increase in the year ending on June 30, 2017 in comparison to the year ending on June 30,

2016. Further, the company also tends to liquidate some of the plant, property and equipment

holdings which it considers as redundant and cash inflows are realised from the same.

Besides, a sizable chunk of cash is used by the company to purchase various businesses along

with acquiring intangible assets particularly brands. There is a huge jump in cash outflow on

account of investing activities in FY2017 (RFG, 2017).

The key items related to the financing activities cash flow are indicated as follows (RFG,

2017).

This reflects on the cash inflow and outflow generated on account of financing activities.

Cash inflows can result from issue of shares or incremental debt as these are the two main

sources of finance that are tapped by the company. For FY2017, money was raised through

both debt and equity amounting to $ 189.5 million and $ 35.6 million respectively. In relation

to cash outflow, there are three key elements namely payment of dividends, borrowing

repayment and costs for issuance of securities. The dividend paid by the company has

witnessed a jump in FY2017 when compared with FY2016. There has been repayment of

debt to the extent of $ 149.5 million during FY2017. Besides, money paid in relation to

raising money through debt and equity also leads to cash outflow as represented above (RFG,

2017).

ii) The three major cash flow components are cash flow arising from operating, investing and

financing activities respectively. The last three years trends are highlighted in the following

tabular format.

Corporate Accounting

The above figures clearly reflect a healthy trend as far as cash flow from operating

activities is concerned as it has enhanced especially in FY2016 which clearly indicates that

the underlying business model of the company is sound. Further, it is evident that the

company seems to be investing aggressively in acquisition of various business assets

which is why for all the years under consideration, the investing activities related cash

inflow indicates an outflow. Also, this investment in the business would lead to sizable

benefit for shareholders in the future as higher earnings may be delivered. Also, another

positive observation is that the company has ensured that over-leveraging of the balance

sheet does not happen which is why the company is raising money through equity dilution

and also aiming to keep the debt levels within limits (Damodaran, 2015).

OTHER COMPREHENSIVE INCOME STATEMENT

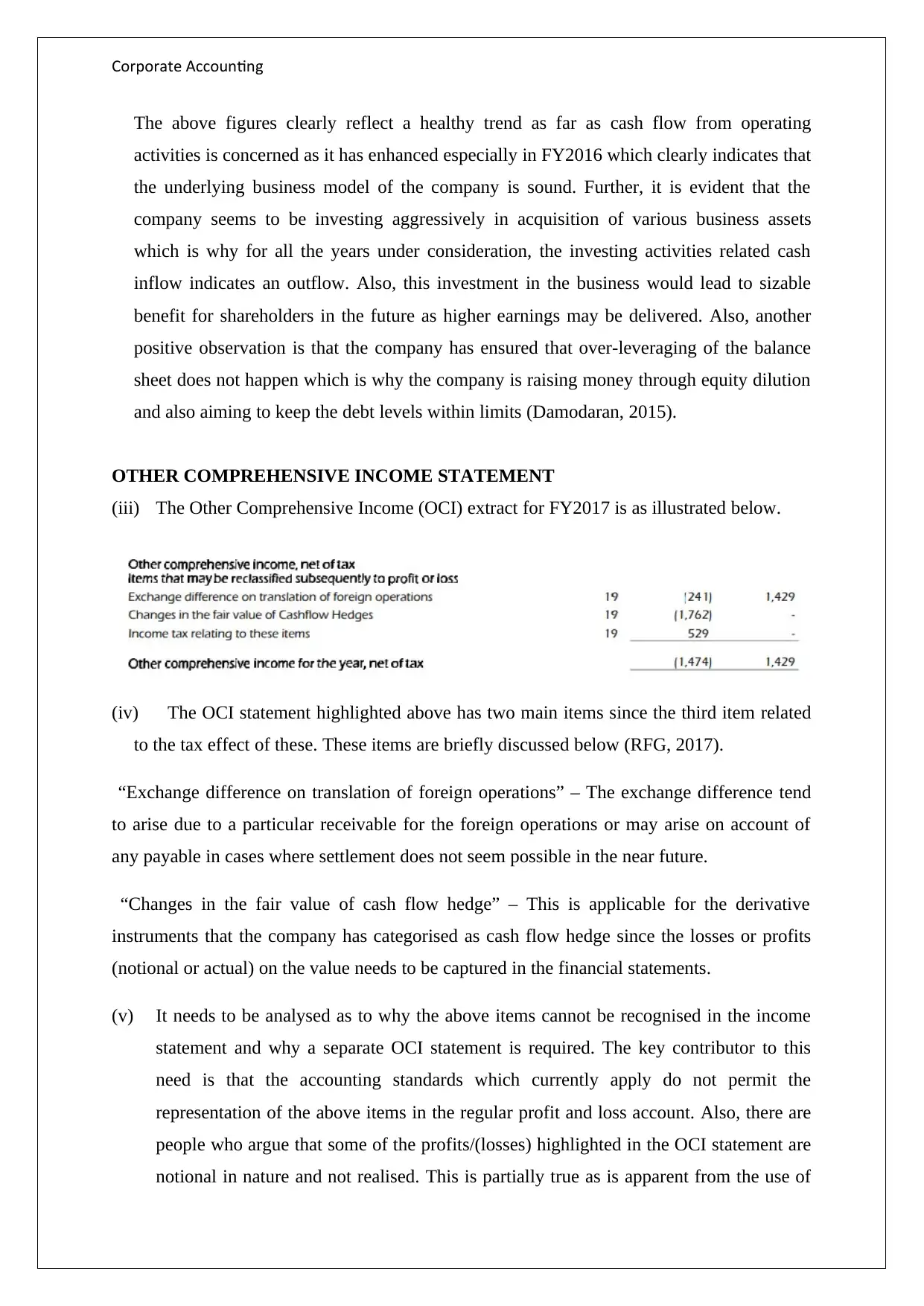

(iii) The Other Comprehensive Income (OCI) extract for FY2017 is as illustrated below.

(iv) The OCI statement highlighted above has two main items since the third item related

to the tax effect of these. These items are briefly discussed below (RFG, 2017).

“Exchange difference on translation of foreign operations” – The exchange difference tend

to arise due to a particular receivable for the foreign operations or may arise on account of

any payable in cases where settlement does not seem possible in the near future.

“Changes in the fair value of cash flow hedge” – This is applicable for the derivative

instruments that the company has categorised as cash flow hedge since the losses or profits

(notional or actual) on the value needs to be captured in the financial statements.

(v) It needs to be analysed as to why the above items cannot be recognised in the income

statement and why a separate OCI statement is required. The key contributor to this

need is that the accounting standards which currently apply do not permit the

representation of the above items in the regular profit and loss account. Also, there are

people who argue that some of the profits/(losses) highlighted in the OCI statement are

notional in nature and not realised. This is partially true as is apparent from the use of

The above figures clearly reflect a healthy trend as far as cash flow from operating

activities is concerned as it has enhanced especially in FY2016 which clearly indicates that

the underlying business model of the company is sound. Further, it is evident that the

company seems to be investing aggressively in acquisition of various business assets

which is why for all the years under consideration, the investing activities related cash

inflow indicates an outflow. Also, this investment in the business would lead to sizable

benefit for shareholders in the future as higher earnings may be delivered. Also, another

positive observation is that the company has ensured that over-leveraging of the balance

sheet does not happen which is why the company is raising money through equity dilution

and also aiming to keep the debt levels within limits (Damodaran, 2015).

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) The Other Comprehensive Income (OCI) extract for FY2017 is as illustrated below.

(iv) The OCI statement highlighted above has two main items since the third item related

to the tax effect of these. These items are briefly discussed below (RFG, 2017).

“Exchange difference on translation of foreign operations” – The exchange difference tend

to arise due to a particular receivable for the foreign operations or may arise on account of

any payable in cases where settlement does not seem possible in the near future.

“Changes in the fair value of cash flow hedge” – This is applicable for the derivative

instruments that the company has categorised as cash flow hedge since the losses or profits

(notional or actual) on the value needs to be captured in the financial statements.

(v) It needs to be analysed as to why the above items cannot be recognised in the income

statement and why a separate OCI statement is required. The key contributor to this

need is that the accounting standards which currently apply do not permit the

representation of the above items in the regular profit and loss account. Also, there are

people who argue that some of the profits/(losses) highlighted in the OCI statement are

notional in nature and not realised. This is partially true as is apparent from the use of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting

cash flow hedge in the given case whereby difference in fair value from the beginning

of the financial year and closing of the financial year would be recognised as either

profit or loss depending on which value is greater. However, OCI statement can also

reflect on actual losses and gains that have been realised by the company on the

assets/liabilities and therefore is vital for users (Deegan, 2014).

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) The income statement highlights the underlying tax expense which for RFG for

FY2107 stands at $ 25,686,000 (RFG, 2017).

(vii) In order to verify whether the tax expense can indeed be obtained by simply

multiplying the applicable corporate tax rate to the pre-tax income, the following

computations ought to be performed (RFG, 2017).

Tax expense (Pre-tax income*Corporate Tax Rate) = 0.3*87,613,000 = $26,283,900

Tax expense as reported in the financial statements = $25,686,000

Clearly, the two deviate and are not the same. To account for the underlying differences

between the two figures computed, it makes sense to consider the analyse the actual

computation of income tax expense by the company as indicated in the notes to account

(RFG, 2017).

cash flow hedge in the given case whereby difference in fair value from the beginning

of the financial year and closing of the financial year would be recognised as either

profit or loss depending on which value is greater. However, OCI statement can also

reflect on actual losses and gains that have been realised by the company on the

assets/liabilities and therefore is vital for users (Deegan, 2014).

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) The income statement highlights the underlying tax expense which for RFG for

FY2107 stands at $ 25,686,000 (RFG, 2017).

(vii) In order to verify whether the tax expense can indeed be obtained by simply

multiplying the applicable corporate tax rate to the pre-tax income, the following

computations ought to be performed (RFG, 2017).

Tax expense (Pre-tax income*Corporate Tax Rate) = 0.3*87,613,000 = $26,283,900

Tax expense as reported in the financial statements = $25,686,000

Clearly, the two deviate and are not the same. To account for the underlying differences

between the two figures computed, it makes sense to consider the analyse the actual

computation of income tax expense by the company as indicated in the notes to account

(RFG, 2017).

Corporate Accounting

It is evident that the computations of income tax expense begin with the 30% corporate tax

rate on the accounting income before profit. However, thereafter several adjustments are

made which tend to produce an income tax expense which deviates from the theoretical

understanding. In the above backdrop, it is crucial to consider that the adjustment is

required due to the different provisions for computation of income for accounting

purposes as against computing the same for tax purposes. The net result is that there are

differences created which tend to extend in the future years through the deferred tax assets

and liabilities (Petty et. al., 2012).

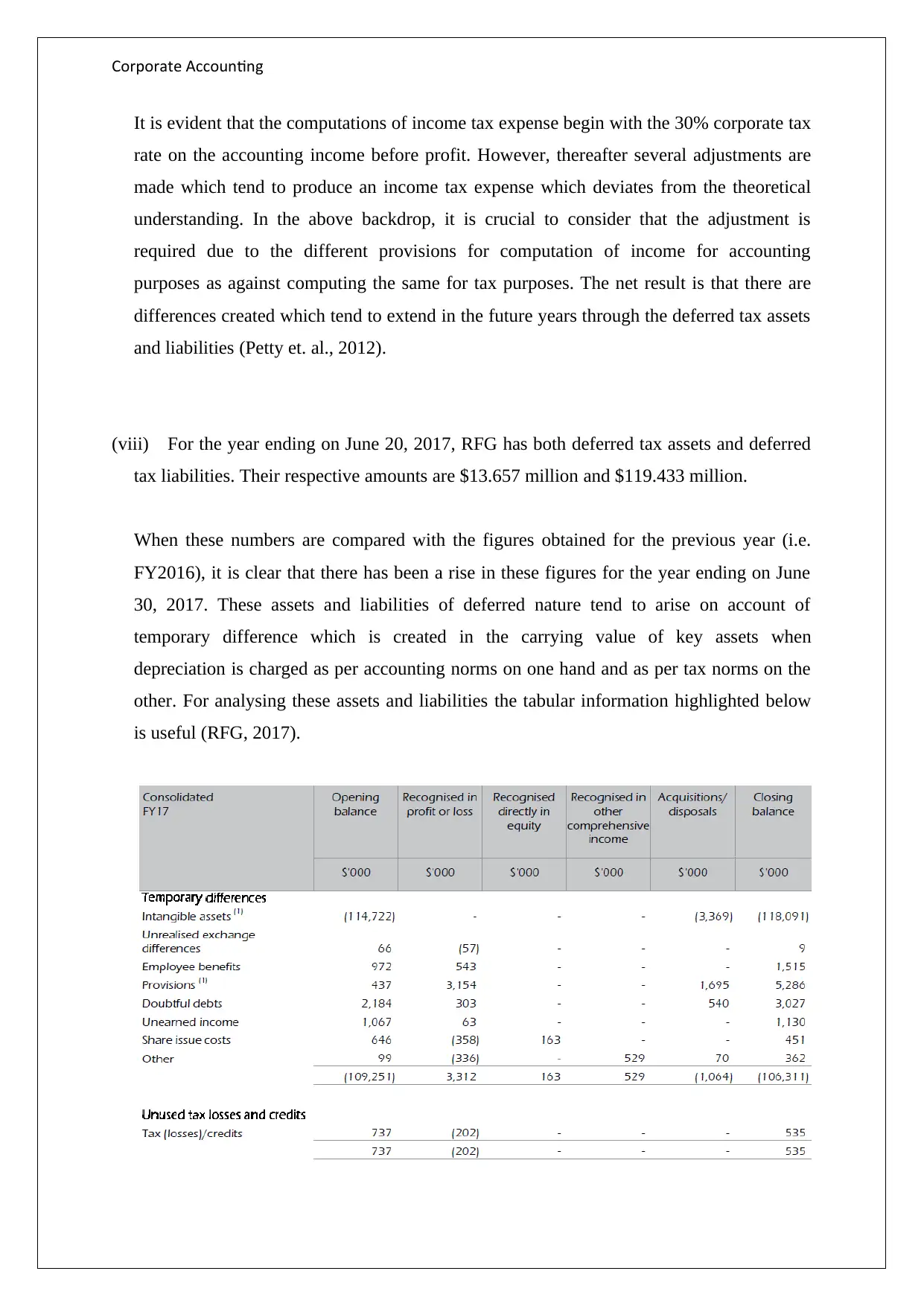

(viii) For the year ending on June 20, 2017, RFG has both deferred tax assets and deferred

tax liabilities. Their respective amounts are $13.657 million and $119.433 million.

When these numbers are compared with the figures obtained for the previous year (i.e.

FY2016), it is clear that there has been a rise in these figures for the year ending on June

30, 2017. These assets and liabilities of deferred nature tend to arise on account of

temporary difference which is created in the carrying value of key assets when

depreciation is charged as per accounting norms on one hand and as per tax norms on the

other. For analysing these assets and liabilities the tabular information highlighted below

is useful (RFG, 2017).

It is evident that the computations of income tax expense begin with the 30% corporate tax

rate on the accounting income before profit. However, thereafter several adjustments are

made which tend to produce an income tax expense which deviates from the theoretical

understanding. In the above backdrop, it is crucial to consider that the adjustment is

required due to the different provisions for computation of income for accounting

purposes as against computing the same for tax purposes. The net result is that there are

differences created which tend to extend in the future years through the deferred tax assets

and liabilities (Petty et. al., 2012).

(viii) For the year ending on June 20, 2017, RFG has both deferred tax assets and deferred

tax liabilities. Their respective amounts are $13.657 million and $119.433 million.

When these numbers are compared with the figures obtained for the previous year (i.e.

FY2016), it is clear that there has been a rise in these figures for the year ending on June

30, 2017. These assets and liabilities of deferred nature tend to arise on account of

temporary difference which is created in the carrying value of key assets when

depreciation is charged as per accounting norms on one hand and as per tax norms on the

other. For analysing these assets and liabilities the tabular information highlighted below

is useful (RFG, 2017).

Corporate Accounting

Deferred tax assets are defined as the future effect of the transactions carried out in the

year which would result in tax savings for the company. On the contrary, deferred tax

liabiltiies are defined as the future effect of the transactions carried out in the year which

would result incremental tax outflow for the company (Gilders et. al., 2016).

(ix) The company did not have any current tax assets on the balance sheet as on the last

day of FY2017. However, there was presence of tax assets to the extent of $ 4.455 million

as indicated in FY2016 related balance sheet. The effect of this is highlighted from the

name whereby a tax benefit in the FY2018 would arise on account of current tax assets in

FY2017 (RFG, 2017).

Tax expense tends to deviate from the tax payable which may be attributed to primarily

one reason which is the difference in the rules related to accounting income computation

and taxable income computation. The prime concern of income tax expense is the

accounting income reported on pre-tax basis which then requires appropriate adjustments

based on deferred tax assets and liabilities. On the other hand, the taxable income is

computed through reconciliation to the accounting pre-tax income taking into

consideration suitable difference in the assessability and deductions (Damodaran, 2015).

(x) Income tax expense (FY2017 income statement) = $25.686 million

Income tax paid (FY2017 cash flow statement) = $ 21.46 million

The above difference may be related to the following two issues which are briefly

enumerated as follows.

Tax expense is obtained from income statement. This is prepared considering an

accrual basis which essentially leads to a creation of tax payable liability for the

expense. In contrast, tax paid is obtained from the cash flow statement. This is

prepared considering a cash basis and hence the tax paid in FY2017 would constitute

some tax paid for the previous year (i.e. FY2016) along with some tax outflow for

FY2017. Therefore, the difference arises (Petty et. al., 2012).

Deferred tax assets are defined as the future effect of the transactions carried out in the

year which would result in tax savings for the company. On the contrary, deferred tax

liabiltiies are defined as the future effect of the transactions carried out in the year which

would result incremental tax outflow for the company (Gilders et. al., 2016).

(ix) The company did not have any current tax assets on the balance sheet as on the last

day of FY2017. However, there was presence of tax assets to the extent of $ 4.455 million

as indicated in FY2016 related balance sheet. The effect of this is highlighted from the

name whereby a tax benefit in the FY2018 would arise on account of current tax assets in

FY2017 (RFG, 2017).

Tax expense tends to deviate from the tax payable which may be attributed to primarily

one reason which is the difference in the rules related to accounting income computation

and taxable income computation. The prime concern of income tax expense is the

accounting income reported on pre-tax basis which then requires appropriate adjustments

based on deferred tax assets and liabilities. On the other hand, the taxable income is

computed through reconciliation to the accounting pre-tax income taking into

consideration suitable difference in the assessability and deductions (Damodaran, 2015).

(x) Income tax expense (FY2017 income statement) = $25.686 million

Income tax paid (FY2017 cash flow statement) = $ 21.46 million

The above difference may be related to the following two issues which are briefly

enumerated as follows.

Tax expense is obtained from income statement. This is prepared considering an

accrual basis which essentially leads to a creation of tax payable liability for the

expense. In contrast, tax paid is obtained from the cash flow statement. This is

prepared considering a cash basis and hence the tax paid in FY2017 would constitute

some tax paid for the previous year (i.e. FY2016) along with some tax outflow for

FY2017. Therefore, the difference arises (Petty et. al., 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

Besides, the difference in the two amounts also arises due to tax norms being at odds

with accounting norms. The net result is that that tax paid is linked to the tax payable

and not essentially the income tax expense. This leads to some deviation between the

two figures (Deegan, 2014).

(xi) A particular aspect which attracted my maximum attentions was the topic of tax

liabilities/ assets of deferred nature and the manner of their creation and functioning. A

key takeaway from the given task is that the computation of tax liability in theory is quite

simple but practically it is a complex affair which is why there are dedicated professionals

whose services are sought after by companies. The underlying complexity is increased to

a higher level because of the differences in tax regime and accounting regime with regards

to certain deductions, income assessability and treatment of depreciation. Thus, the given

year income tax expense would also be impacted on account of transactions in the past

which would either lower or increase this tax expense amount. Also, considering the

complexity of the computation of tax as exhibited in the current company’s financial

statements, it is apparent that this requires high concept clarity and practice in dealing with

various transactions so as to ensure that financial statements are reflective of the financial

performance. Further, the given task by posing various questions and provided actual

financial statements provided valuable insight into the application of the concepts learnt in

the class in reality and thus has contributed to incremental learning having positive

implications for future professional life.

Besides, the difference in the two amounts also arises due to tax norms being at odds

with accounting norms. The net result is that that tax paid is linked to the tax payable

and not essentially the income tax expense. This leads to some deviation between the

two figures (Deegan, 2014).

(xi) A particular aspect which attracted my maximum attentions was the topic of tax

liabilities/ assets of deferred nature and the manner of their creation and functioning. A

key takeaway from the given task is that the computation of tax liability in theory is quite

simple but practically it is a complex affair which is why there are dedicated professionals

whose services are sought after by companies. The underlying complexity is increased to

a higher level because of the differences in tax regime and accounting regime with regards

to certain deductions, income assessability and treatment of depreciation. Thus, the given

year income tax expense would also be impacted on account of transactions in the past

which would either lower or increase this tax expense amount. Also, considering the

complexity of the computation of tax as exhibited in the current company’s financial

statements, it is apparent that this requires high concept clarity and practice in dealing with

various transactions so as to ensure that financial statements are reflective of the financial

performance. Further, the given task by posing various questions and provided actual

financial statements provided valuable insight into the application of the concepts learnt in

the class in reality and thus has contributed to incremental learning having positive

implications for future professional life.

Corporate Accounting

References

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Deegan, C. (2014). Financial Accounting Theory, 4th ed. Sydney: McGraw-Hill

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016, 9th ed. Sydney: LexisNexis/Butterworths.

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education,

French Forest Australia.

RFG (2017), Annual Report FY2017, Retrieved from http://www.rfg.com.au/index.php/110-

general-pages/investor-news/816-2017-annual-report (

References

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Deegan, C. (2014). Financial Accounting Theory, 4th ed. Sydney: McGraw-Hill

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016, 9th ed. Sydney: LexisNexis/Butterworths.

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education,

French Forest Australia.

RFG (2017), Annual Report FY2017, Retrieved from http://www.rfg.com.au/index.php/110-

general-pages/investor-news/816-2017-annual-report (

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.