Assignment On Corporate Accounting (Doc)

21 Pages3104 Words27 Views

Added on 2020-04-01

Assignment On Corporate Accounting (Doc)

Added on 2020-04-01

ShareRelated Documents

Running head: CORPORATE ACCOUNTINGCorporate accountingName of the UniversityName of the studentAuthors note

1CORPORATE ACCOUNTING

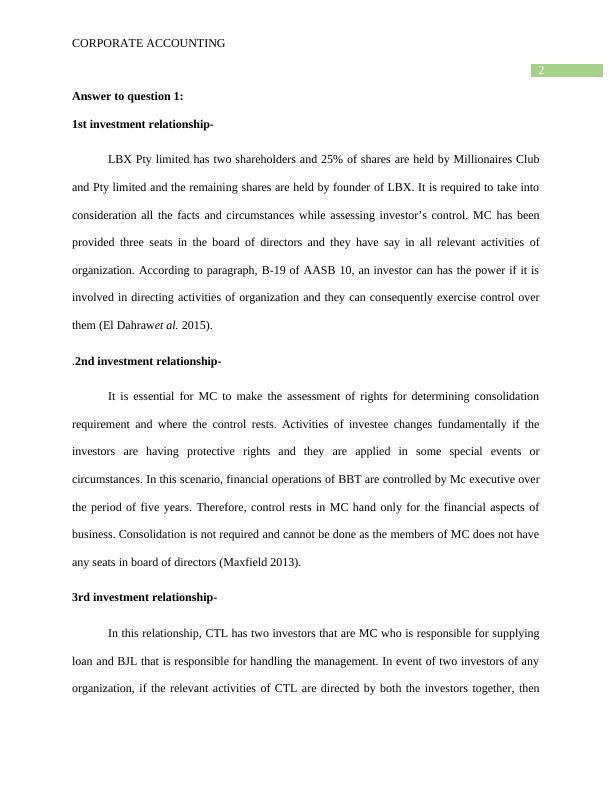

2CORPORATE ACCOUNTINGAnswer to question 1:1st investment relationship- LBX Pty limited has two shareholders and 25% of shares are held by Millionaires Cluband Pty limited and the remaining shares are held by founder of LBX. It is required to take intoconsideration all the facts and circumstances while assessing investor’s control. MC has beenprovided three seats in the board of directors and they have say in all relevant activities oforganization. According to paragraph, B-19 of AASB 10, an investor can has the power if it isinvolved in directing activities of organization and they can consequently exercise control overthem (El Dahrawet al. 2015). .2nd investment relationship- It is essential for MC to make the assessment of rights for determining consolidationrequirement and where the control rests. Activities of investee changes fundamentally if theinvestors are having protective rights and they are applied in some special events orcircumstances. In this scenario, financial operations of BBT are controlled by Mc executive overthe period of five years. Therefore, control rests in MC hand only for the financial aspects ofbusiness. Consolidation is not required and cannot be done as the members of MC does not haveany seats in board of directors (Maxfield 2013).3rd investment relationship- In this relationship, CTL has two investors that are MC who is responsible for supplyingloan and BJL that is responsible for handling the management. In event of two investors of anyorganization, if the relevant activities of CTL are directed by both the investors together, then

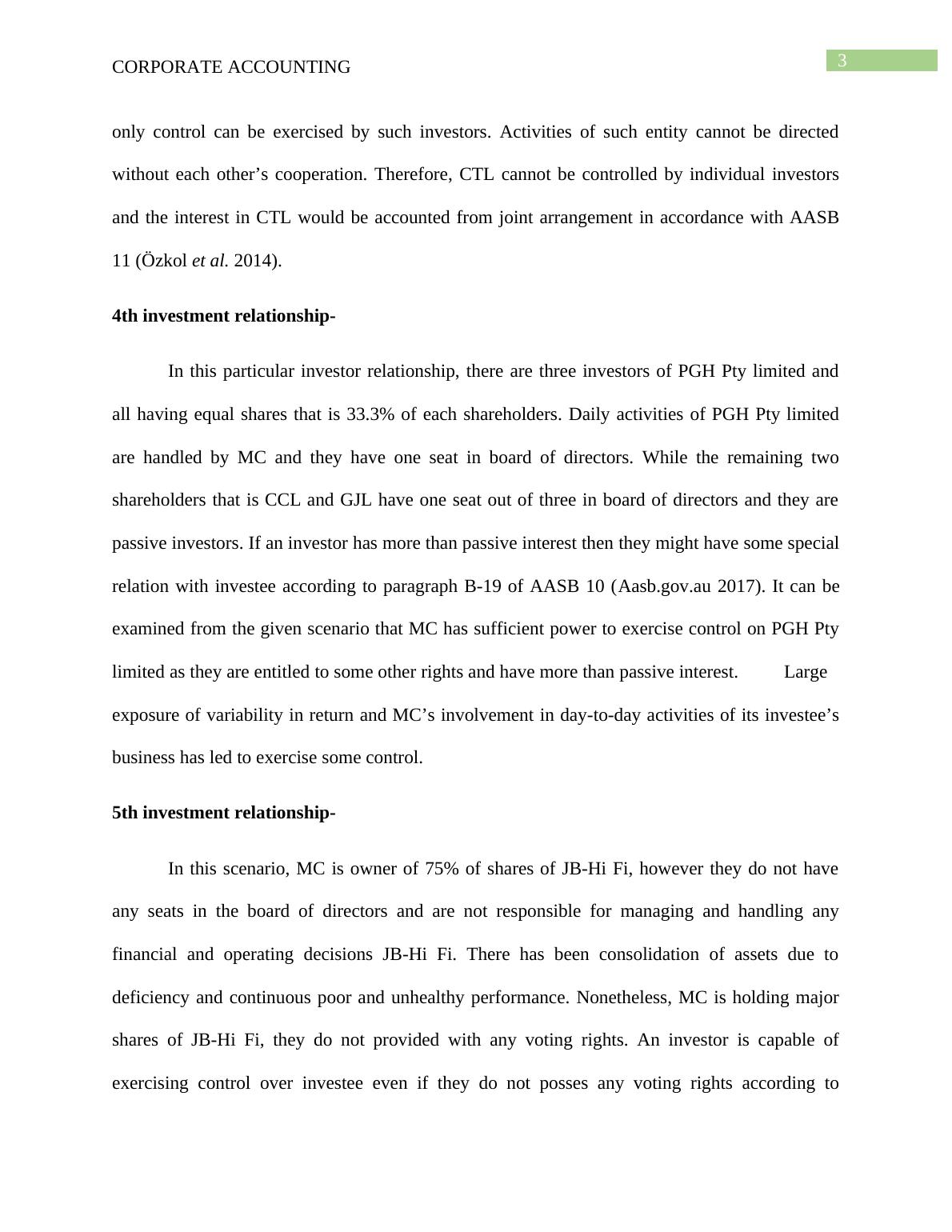

3CORPORATE ACCOUNTINGonly control can be exercised by such investors. Activities of such entity cannot be directedwithout each other’s cooperation. Therefore, CTL cannot be controlled by individual investorsand the interest in CTL would be accounted from joint arrangement in accordance with AASB11 (Özkol et al. 2014). 4th investment relationship- In this particular investor relationship, there are three investors of PGH Pty limited andall having equal shares that is 33.3% of each shareholders. Daily activities of PGH Pty limitedare handled by MC and they have one seat in board of directors. While the remaining twoshareholders that is CCL and GJL have one seat out of three in board of directors and they arepassive investors. If an investor has more than passive interest then they might have some specialrelation with investee according to paragraph B-19 of AASB 10 (Aasb.gov.au 2017). It can beexamined from the given scenario that MC has sufficient power to exercise control on PGH Ptylimited as they are entitled to some other rights and have more than passive interest.Largeexposure of variability in return and MC’s involvement in day-to-day activities of its investee’sbusiness has led to exercise some control.5th investment relationship- In this scenario, MC is owner of 75% of shares of JB-Hi Fi, however they do not haveany seats in the board of directors and are not responsible for managing and handling anyfinancial and operating decisions JB-Hi Fi. There has been consolidation of assets due todeficiency and continuous poor and unhealthy performance. Nonetheless, MC is holding majorshares of JB-Hi Fi, they do not provided with any voting rights. An investor is capable ofexercising control over investee even if they do not posses any voting rights according to

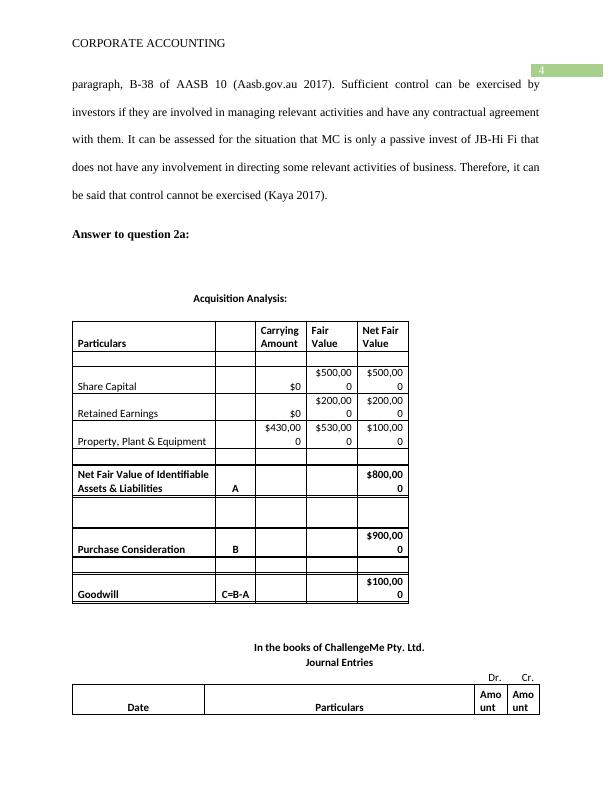

4CORPORATE ACCOUNTINGparagraph, B-38 of AASB 10 (Aasb.gov.au 2017). Sufficient control can be exercised byinvestors if they are involved in managing relevant activities and have any contractual agreementwith them. It can be assessed for the situation that MC is only a passive invest of JB-Hi Fi thatdoes not have any involvement in directing some relevant activities of business. Therefore, it canbe said that control cannot be exercised (Kaya 2017). Answer to question 2a:Acquisition Analysis:ParticularsCarryingAmountFair ValueNet Fair ValueShare Capital$0 $500,000 $500,000 Retained Earnings$0 $200,000 $200,000 Property, Plant & Equipment$430,000 $530,000 $100,000 Net Fair Value of IdentifiableAssets & LiabilitiesA$800,000 Purchase ConsiderationB$900,000 GoodwillC=B-A$100,000 In the books of ChallengeMe Pty. Ltd.Journal EntriesDr.Cr.DateParticularsAmountAmount

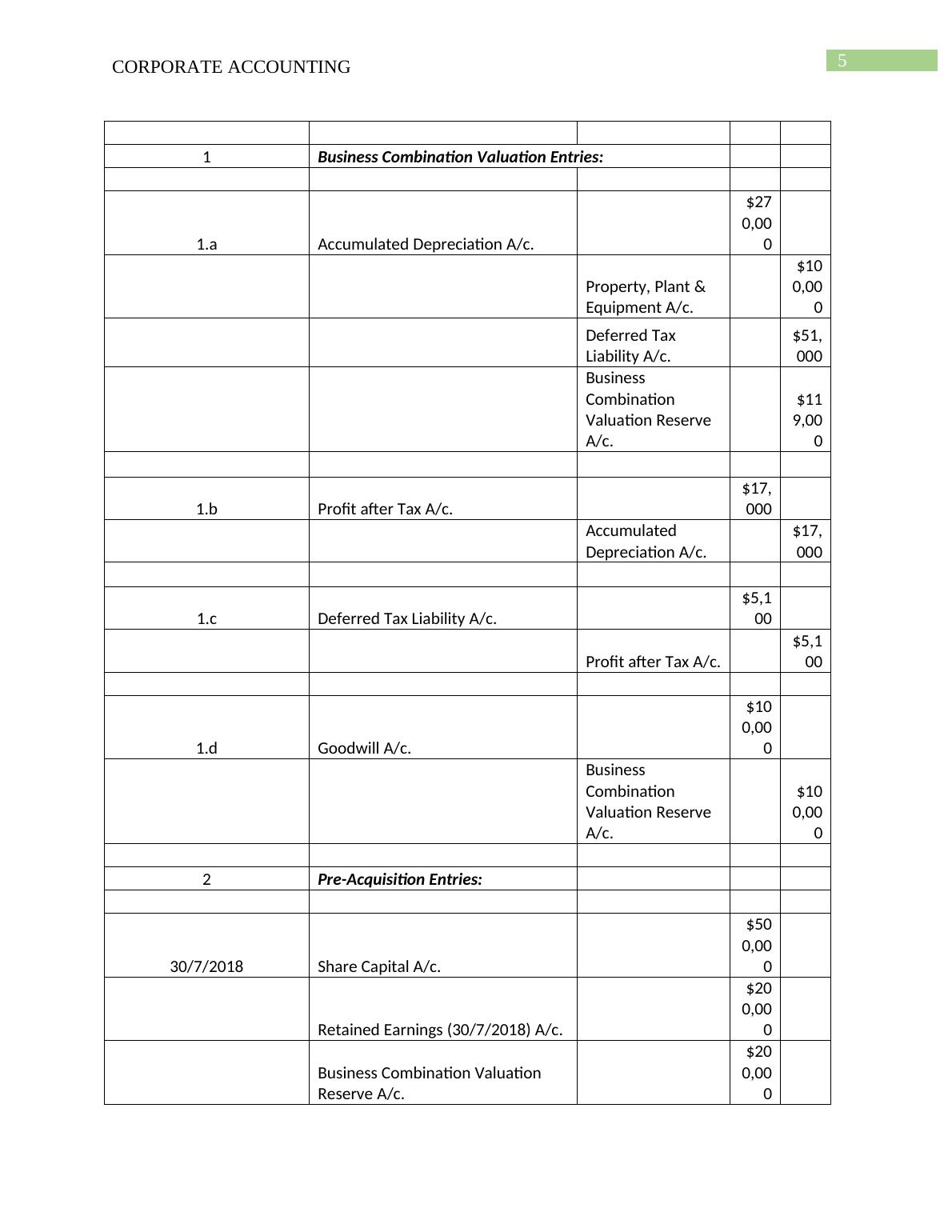

5CORPORATE ACCOUNTING1Business Combination Valuation Entries:1.aAccumulated Depreciation A/c.$270,000 Property, Plant & Equipment A/c.$100,000 Deferred Tax Liability A/c.$51,000 BusinessCombinationValuation ReserveA/c.$119,000 1.bProfit after Tax A/c.$17,000 AccumulatedDepreciation A/c.$17,000 1.cDeferred Tax Liability A/c.$5,100 Profit after Tax A/c.$5,100 1.dGoodwill A/c.$100,000 BusinessCombinationValuation ReserveA/c.$100,000 2Pre-Acquisition Entries:30/7/2018Share Capital A/c.$500,000 Retained Earnings (30/7/2018) A/c.$200,000 Business Combination ValuationReserve A/c.$200,000

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

ACT305 Corporate Accounting Assignment - LBX Pty limitedlg...

|6

|1089

|87

Corporate Accounting Assignment AASB 10lg...

|19

|2997

|38

Assignment Corporate Accounting Millionaires Club and Pty limitedlg...

|19

|2925

|73

Corporate Accounting Assignmentlg...

|22

|1789

|37

The Share Capital of LBX Pty Limited (LBX) | Assignmentlg...

|20

|4150

|37

AASB 10 Consolidation Financial Statements Assignmentlg...

|17

|4138

|69