Analyzing Impairment Loss in Cash Generating Units: A Case Study.

VerifiedAdded on 2023/03/31

|13

|2382

|153

Essay

AI Summary

This assignment provides an analysis of impairment loss for cash-generating units (CGUs), excluding goodwill, in accordance with AASB 136. It defines CGUs and explains the process of recognizing and measuring impairment losses, including the determination of recoverable amounts and the allocation of losses within a CGU. The assignment also discusses goodwill impairment and the conditions under which impairment reversals can occur. A practical component involves calculations and journal entries for a case study of Gali Ltd, demonstrating the application of these principles in a real-world scenario. Desklib offers a variety of resources, including past papers and solved assignments, to support students in their studies.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Part A:................................................................................................................................2

Part B:................................................................................................................................9

References:......................................................................................................................11

Table of Contents

Part A:................................................................................................................................2

Part B:................................................................................................................................9

References:......................................................................................................................11

2CORPORATE ACCOUNTING

Part A:

Introduction:

For an organisation to carry out its day-to-day operations, investments have to be

made in assets like property, plant and equipment, land, machinery, factory and others.

The intention is to generate revenue by using these assets. However, with the passage

of time, an asset becomes damaged or obsolete leading to change in value. Such

change in valuation is deemed as impairment (Beaudoin and Hughes 2014).

On the other hand, an asset could be rarely found generating cash flows

independent of other assets. For instance, an airline company would own planes and

their licenses that would be categorised as its assets. In case; these assets are invested

individually, there would be no generation of cash flows. More precisely, it is not

possible for an airline to own planes in the absence of licenses for operating the same.

In a similar manner, it is not possible for the airline to have licenses without owning

some planes. This asset combination is termed as a cash-generating unit (CGU) and it

could be impaired like individual assets (Detzen, Wersborg and Zülch 2015).

In 2008, ABC Learning witnessed a scandal related to overvaluation of assets

and more specifically, the wrong valuation of its childcare subsidiaries and goodwill. As

a result, considerable emphasis has been placed on the impairment practices of the

business organisations (Hassine and Jilani 2017). The current essay would shed light

on the recognition of impairment losses by an organisation and the measures to be

adopted for gauging the losses in relation to CGUs excluding goodwill.

Part A:

Introduction:

For an organisation to carry out its day-to-day operations, investments have to be

made in assets like property, plant and equipment, land, machinery, factory and others.

The intention is to generate revenue by using these assets. However, with the passage

of time, an asset becomes damaged or obsolete leading to change in value. Such

change in valuation is deemed as impairment (Beaudoin and Hughes 2014).

On the other hand, an asset could be rarely found generating cash flows

independent of other assets. For instance, an airline company would own planes and

their licenses that would be categorised as its assets. In case; these assets are invested

individually, there would be no generation of cash flows. More precisely, it is not

possible for an airline to own planes in the absence of licenses for operating the same.

In a similar manner, it is not possible for the airline to have licenses without owning

some planes. This asset combination is termed as a cash-generating unit (CGU) and it

could be impaired like individual assets (Detzen, Wersborg and Zülch 2015).

In 2008, ABC Learning witnessed a scandal related to overvaluation of assets

and more specifically, the wrong valuation of its childcare subsidiaries and goodwill. As

a result, considerable emphasis has been placed on the impairment practices of the

business organisations (Hassine and Jilani 2017). The current essay would shed light

on the recognition of impairment losses by an organisation and the measures to be

adopted for gauging the losses in relation to CGUs excluding goodwill.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Discussion:

The amendments on the way of treating impairment losses in CGUs are included

in AASB 136 that defines an impairment loss as the carrying amount of CGU minus

recoverable amount of that CGU (Avallone and Quagli 2015). Recoverable amount

could be defined as the amount, which is collected by selling or using an asset.

The application of AASB 136 could be made in different asset list like goodwill,

land, machinery, building, equipment, intangible assets, joint ventures, subsidiaries and

equipment. However, the guidelines of the standard are not applicable to certain assets

like inventory, contract assets, insurance contract and investment property (Boučková

2016). Cash-generating units could be described as assets or class of assets, which are

able to fetch cash flows independent of other group of assets.

According to “AASB 136, Paragraphs 9 and 10”, assets and CGUs have to be

tested for impairment at the end of the reporting period and annually for goodwill and

intangible assets. If indication is found regarding the impairment of CGU, it is necessary

for the organisation to compute the recoverable amount of CGU ad the same has to be

compared with the carrying amount of the CGU (Aasb.gov. au 2019). The carrying

amount includes the value of the asset as denoted in the financial statement minus

impairment losses and accumulated depreciation.

The recoverable amount of the CGU is computed as the higher between fair

value less selling cost and value-in-use. The fair value less selling cost could be defined

as the value to be realised by an organisation from sale of the CGU. On the other hand,

Discussion:

The amendments on the way of treating impairment losses in CGUs are included

in AASB 136 that defines an impairment loss as the carrying amount of CGU minus

recoverable amount of that CGU (Avallone and Quagli 2015). Recoverable amount

could be defined as the amount, which is collected by selling or using an asset.

The application of AASB 136 could be made in different asset list like goodwill,

land, machinery, building, equipment, intangible assets, joint ventures, subsidiaries and

equipment. However, the guidelines of the standard are not applicable to certain assets

like inventory, contract assets, insurance contract and investment property (Boučková

2016). Cash-generating units could be described as assets or class of assets, which are

able to fetch cash flows independent of other group of assets.

According to “AASB 136, Paragraphs 9 and 10”, assets and CGUs have to be

tested for impairment at the end of the reporting period and annually for goodwill and

intangible assets. If indication is found regarding the impairment of CGU, it is necessary

for the organisation to compute the recoverable amount of CGU ad the same has to be

compared with the carrying amount of the CGU (Aasb.gov. au 2019). The carrying

amount includes the value of the asset as denoted in the financial statement minus

impairment losses and accumulated depreciation.

The recoverable amount of the CGU is computed as the higher between fair

value less selling cost and value-in-use. The fair value less selling cost could be defined

as the value to be realised by an organisation from sale of the CGU. On the other hand,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

value-in-use could be defined as the present value of discounted future cash flows,

which is attached to use the asset combination (Komissarov, Kastantin and Rick 2014).

When the recoverable amount of a CGU is below the carrying amount,

impairment of CGU is evident (Vogt et al. 2016). In opposition, when the recoverable

amount of the CGU is more compared to its carrying amount with no past impairments,

the CGU is not impaired. Hence, the organisation is not needed to conduct any

measure. There is recognition of impairment loss in relation to a CGU by minimisation of

the carrying amount (Linnenluecke et al. 2015). Firstly, the allocation of loss would be

made to goodwill after which other assets would be assigned within the CGU in relation

to their carrying amounts.

It is necessary to assure that the carrying amount of each asset within a CGU

does not fall below zero, value-in-use or fair value less selling cost. By subjecting to

limits, the unallocated amounts would then be assigned back to the other assets within

a CGU.

It is possible to reverse impairments when the conditions resulting in impairment

in the initial stage has been lifted. “AASB 136, Para 10” needs the conditions to be

assessed per year (Aasb.gov.au 2019).

In case; there is lift of conditions, the organisation needs to compute the

recoverable amount. When the carrying amount is lower than the recoverable amount of

CGU, reversal of impairment could occur subject to a limit of not beyond the ceiling.

“AASB 136, Para 117” describes ceiling as the carrying amount of the asset by

assuming that no impairments have taken place (Aasb.gov.au 2019).

value-in-use could be defined as the present value of discounted future cash flows,

which is attached to use the asset combination (Komissarov, Kastantin and Rick 2014).

When the recoverable amount of a CGU is below the carrying amount,

impairment of CGU is evident (Vogt et al. 2016). In opposition, when the recoverable

amount of the CGU is more compared to its carrying amount with no past impairments,

the CGU is not impaired. Hence, the organisation is not needed to conduct any

measure. There is recognition of impairment loss in relation to a CGU by minimisation of

the carrying amount (Linnenluecke et al. 2015). Firstly, the allocation of loss would be

made to goodwill after which other assets would be assigned within the CGU in relation

to their carrying amounts.

It is necessary to assure that the carrying amount of each asset within a CGU

does not fall below zero, value-in-use or fair value less selling cost. By subjecting to

limits, the unallocated amounts would then be assigned back to the other assets within

a CGU.

It is possible to reverse impairments when the conditions resulting in impairment

in the initial stage has been lifted. “AASB 136, Para 10” needs the conditions to be

assessed per year (Aasb.gov.au 2019).

In case; there is lift of conditions, the organisation needs to compute the

recoverable amount. When the carrying amount is lower than the recoverable amount of

CGU, reversal of impairment could occur subject to a limit of not beyond the ceiling.

“AASB 136, Para 117” describes ceiling as the carrying amount of the asset by

assuming that no impairments have taken place (Aasb.gov.au 2019).

5CORPORATE ACCOUNTING

The term Goodwill impairment is an earnings charge which is kept recorded in

the income statement of thecompany when the carrying value of goodwill exceeds the

fair value in the financial statements of the company (Sun 2016).The reason behind that

is many companies acquire other firms and bears a price that exceeds the fair value of

the assets and liabilities acquired by the firm. Hence the difference between the

purchase price and the fair value of acquired assets of the firm which is further recorded

as a goodwill.

A particular asset is impaired when the value of the asset exceeds the

recoverable amount of the company and the individual asset is termed as the cash

generating unit. The indication when the intangible asset is impaired is that the asset

market value has significantly reduced more than the expected result of the normal

usage. The significant changes will create an adverse effect on the enterprise due to the

certain factors which take place in the near futureoperates within the technological,

economic market (Sedkiet al. 2018).

The main principle of impairment is that an asset might not be carried on the

balance sheet of the financial statement beyond its recoverable amount. Such value

arising is greater as it is the difference between fair value of the asset and cost to sell

and value-in-use. The carrying value of an asset is compared with its recoverable

amount. Further the asset is impaired at the time when the positive outcome takes place

in such difference. Such impairment which is distributed to the asset at that particular

point of time when the impairment loss is further realisedin profit or loss (Huikku,

Mouritsen and Silvola 2017).

The term Goodwill impairment is an earnings charge which is kept recorded in

the income statement of thecompany when the carrying value of goodwill exceeds the

fair value in the financial statements of the company (Sun 2016).The reason behind that

is many companies acquire other firms and bears a price that exceeds the fair value of

the assets and liabilities acquired by the firm. Hence the difference between the

purchase price and the fair value of acquired assets of the firm which is further recorded

as a goodwill.

A particular asset is impaired when the value of the asset exceeds the

recoverable amount of the company and the individual asset is termed as the cash

generating unit. The indication when the intangible asset is impaired is that the asset

market value has significantly reduced more than the expected result of the normal

usage. The significant changes will create an adverse effect on the enterprise due to the

certain factors which take place in the near futureoperates within the technological,

economic market (Sedkiet al. 2018).

The main principle of impairment is that an asset might not be carried on the

balance sheet of the financial statement beyond its recoverable amount. Such value

arising is greater as it is the difference between fair value of the asset and cost to sell

and value-in-use. The carrying value of an asset is compared with its recoverable

amount. Further the asset is impaired at the time when the positive outcome takes place

in such difference. Such impairment which is distributed to the asset at that particular

point of time when the impairment loss is further realisedin profit or loss (Huikku,

Mouritsen and Silvola 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

There lies and indication that the asset might be impaired when all the assets

subject to the review of impairment are verified for impairment. There are various

intangible assets of the firms which are the goodwill, patent, trademark and many more

are quite frequently tested for yearly impairment despite of any absence in the

impairment indicator. The evaluation of recoverable amount is prepared at an individual

level of asset. The assets of the firm leads to the independent cash flow in the system

and further some of the most valuable or the significant assets are tested for impairment

which are explained in the form of the cash generating unit. As per the “AASB 136 of

Para 104”, the cash generating unit of the impairment loss would be made only if the

recoverable amount of the unit is lower than the comparable unit of the company

(Aasb.gov.au, 2019). The significant purpose of the impairment loss is to minimize the

carrying amount of the assets in two separate sequential orders.The carrying amount of

the goodwill apportioned to the cash-generating unit which must be minimized and

secondly, the other asset units carrying amount is based on the pro-rata basis which

would also be minimized.The process ofminimizations in the carrying amounts is

needed to be treated in the form of loss of impairment on the individual assets.As per

“AASB 136 of Para 60” most of the asset impairment is based on the carrying amount.

According to “AASB 136 of Para 105” which further indicates that in order to distribute

impairment loss, it is significant for the organizationtominimize an the carrying amount

of an asset below the greater of three possible alternatives. The possible alternatives

includes the value-in-use, fair value minus disposal costs and zero (Kabir and Rahman

2016).

There lies and indication that the asset might be impaired when all the assets

subject to the review of impairment are verified for impairment. There are various

intangible assets of the firms which are the goodwill, patent, trademark and many more

are quite frequently tested for yearly impairment despite of any absence in the

impairment indicator. The evaluation of recoverable amount is prepared at an individual

level of asset. The assets of the firm leads to the independent cash flow in the system

and further some of the most valuable or the significant assets are tested for impairment

which are explained in the form of the cash generating unit. As per the “AASB 136 of

Para 104”, the cash generating unit of the impairment loss would be made only if the

recoverable amount of the unit is lower than the comparable unit of the company

(Aasb.gov.au, 2019). The significant purpose of the impairment loss is to minimize the

carrying amount of the assets in two separate sequential orders.The carrying amount of

the goodwill apportioned to the cash-generating unit which must be minimized and

secondly, the other asset units carrying amount is based on the pro-rata basis which

would also be minimized.The process ofminimizations in the carrying amounts is

needed to be treated in the form of loss of impairment on the individual assets.As per

“AASB 136 of Para 60” most of the asset impairment is based on the carrying amount.

According to “AASB 136 of Para 105” which further indicates that in order to distribute

impairment loss, it is significant for the organizationtominimize an the carrying amount

of an asset below the greater of three possible alternatives. The possible alternatives

includes the value-in-use, fair value minus disposal costs and zero (Kabir and Rahman

2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

The amount of impairment lossis further allocated in a different manner which would

have been allocated differently to the asset. This is further needed to be distributed in

the basis of pro-rata to the assets of the other unit. According to “AASB 136 of Para

106” it is impossible to expect the recoverable amount associated with the cash-

generating unit of the assets. Standard apportionment of impairment loss expect

goodwill because each asset of a cash-generating unit is involved in employed together.

“AASB 136 of Para 107”signifies that recoverable amount which is associated with

an individual asset is not determined as it might lead to two different circumstances. In

“AASB 136 of Para 104 and 105” (AASB 2015), an impairment loss is realisedwhen the

carrying amount is higher in respect to the difference between the fair value minus

disposal cost and the outcomes of the procedures of distribution. The realisation of

impairment loss of an asset is related to the cash-generating unit which is not impaired.

This situation is only applicable when there lies difference between fair value of the

asset and the disposal cost is lower in comparison of the carrying amount of the asset

(Caruso et al. 2016).

The performance of the machine is not effective as it was previously as the machine

has met some of the physical damage (Chen, Shroff and Zhang 2017). The difference

between the fair value and disposal cost of the machine is lower which is further

compared to the carrying cots of the machine. This does not imply the independent

cash flows in the business of the company. As per the norms, it is significant to identify

the class of theassets including the machine along with the independent cash inflows of

the other assets is further related to the line of production where the machine belongs.

The amount of impairment lossis further allocated in a different manner which would

have been allocated differently to the asset. This is further needed to be distributed in

the basis of pro-rata to the assets of the other unit. According to “AASB 136 of Para

106” it is impossible to expect the recoverable amount associated with the cash-

generating unit of the assets. Standard apportionment of impairment loss expect

goodwill because each asset of a cash-generating unit is involved in employed together.

“AASB 136 of Para 107”signifies that recoverable amount which is associated with

an individual asset is not determined as it might lead to two different circumstances. In

“AASB 136 of Para 104 and 105” (AASB 2015), an impairment loss is realisedwhen the

carrying amount is higher in respect to the difference between the fair value minus

disposal cost and the outcomes of the procedures of distribution. The realisation of

impairment loss of an asset is related to the cash-generating unit which is not impaired.

This situation is only applicable when there lies difference between fair value of the

asset and the disposal cost is lower in comparison of the carrying amount of the asset

(Caruso et al. 2016).

The performance of the machine is not effective as it was previously as the machine

has met some of the physical damage (Chen, Shroff and Zhang 2017). The difference

between the fair value and disposal cost of the machine is lower which is further

compared to the carrying cots of the machine. This does not imply the independent

cash flows in the business of the company. As per the norms, it is significant to identify

the class of theassets including the machine along with the independent cash inflows of

the other assets is further related to the line of production where the machine belongs.

8CORPORATE ACCOUNTING

The recoverable amount which is related to the line of production indicates that the lone

of production is not impaired to the machine.

In this case, two different assumptions are sortedwhen the forecasts or budgets

which is approved by the management seeks lack of commitment level of the assets.

The recoverable amount of the machine could not be expected, as there might be

deviation from the value-in-use of the machine to the fair value minus disposal costs.

This could be determined for the CGU to which the machine particularly exists. However

there is no realisation of impairment loss for the machine as per the above discussion. It

is further significant for the organization to evaluate the period or the method of

depreciation related to the machine (Vogt et al. 2016). It is recommended to the

organization to adopt the faster method of depreciation for suggesting the remaining life

or rather the economic way in which the benefits are estimated which are further

consumed by the machine.

Conclusion:

It has been analysed from the above discussion that numerous assets generate

cash flows in a combination in opposition to individual assets. This class of assets is

denoted as a cash generating unit or in simple words, CGU. Like individual assets, a

CGU could change in value with the passage of time owing to the damage of separate

assets along with other factors. Therefore, it is crucial for the organisation to conduct

regular checks for the indicators of impairment for analysing if there are changes in

values. The objective of the check is to avoid the reporting of over-valued assets, which

could not alter the financial statements of an organisation or estimations and thus, it

does not represent its fair and true value.

The recoverable amount which is related to the line of production indicates that the lone

of production is not impaired to the machine.

In this case, two different assumptions are sortedwhen the forecasts or budgets

which is approved by the management seeks lack of commitment level of the assets.

The recoverable amount of the machine could not be expected, as there might be

deviation from the value-in-use of the machine to the fair value minus disposal costs.

This could be determined for the CGU to which the machine particularly exists. However

there is no realisation of impairment loss for the machine as per the above discussion. It

is further significant for the organization to evaluate the period or the method of

depreciation related to the machine (Vogt et al. 2016). It is recommended to the

organization to adopt the faster method of depreciation for suggesting the remaining life

or rather the economic way in which the benefits are estimated which are further

consumed by the machine.

Conclusion:

It has been analysed from the above discussion that numerous assets generate

cash flows in a combination in opposition to individual assets. This class of assets is

denoted as a cash generating unit or in simple words, CGU. Like individual assets, a

CGU could change in value with the passage of time owing to the damage of separate

assets along with other factors. Therefore, it is crucial for the organisation to conduct

regular checks for the indicators of impairment for analysing if there are changes in

values. The objective of the check is to avoid the reporting of over-valued assets, which

could not alter the financial statements of an organisation or estimations and thus, it

does not represent its fair and true value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

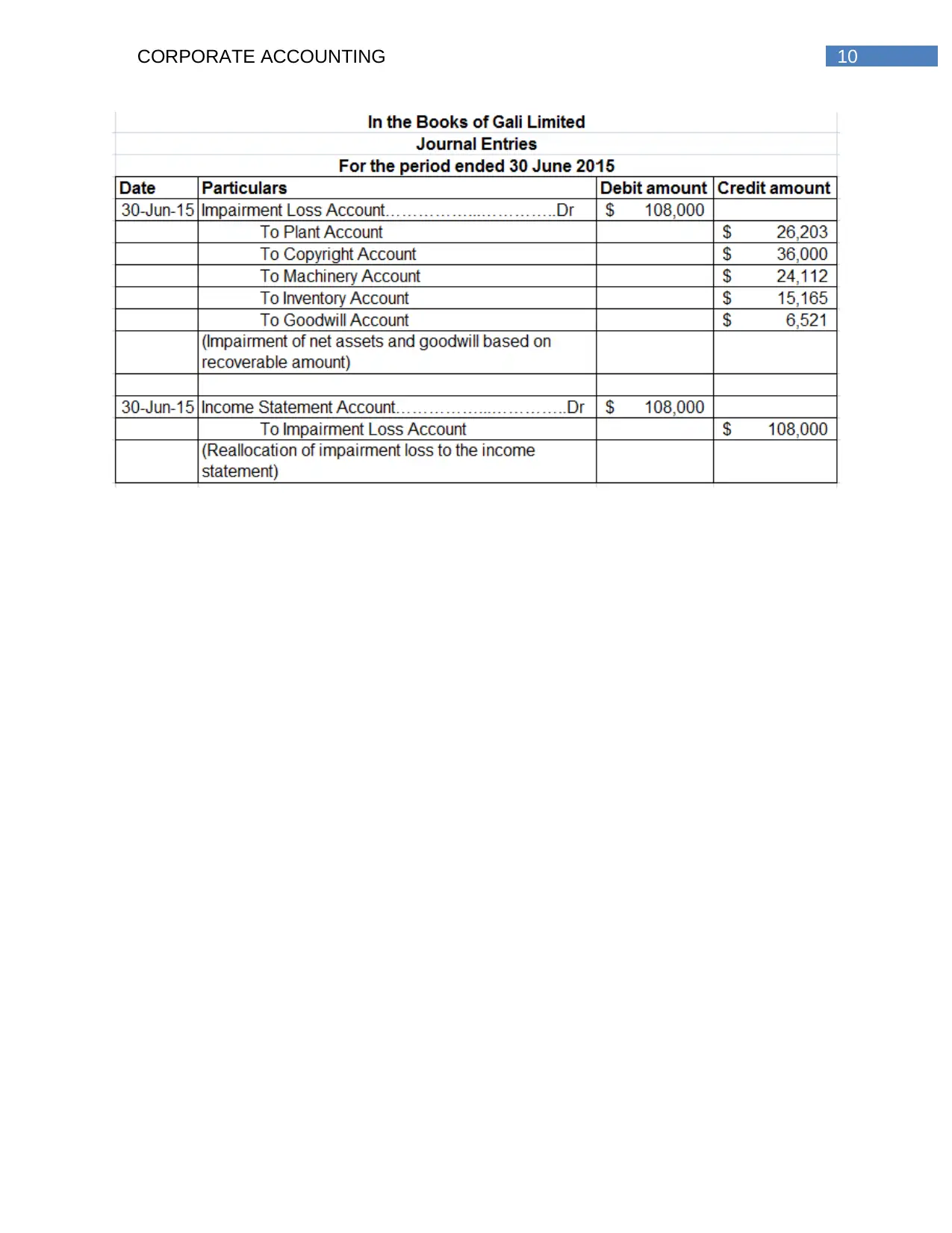

Part B:

Part B:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

11CORPORATE ACCOUNTING

References:

Aasb.gov.au, 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-

09.pdf [Accessed 10 Jun. 2019].

Avallone, F. and Quagli, A., 2015. Insight into the variables used to manage the

goodwill impairment test under IAS 36. Advances in accounting, 31(1), pp.107-114.

Beaudoin, C.A. and Hughes, S.B., 2014. APT, Inc.: An application of impairment testing

and fair value estimation using International Financial Reporting Standards. Issues in

Accounting Education Teaching Notes, 29(1), pp.1-17.

Boučková, M., 2016. Quality of disclosed information with emphasis on goodwill

impairment. European Financial and Accounting Journal, 11(2), pp.37-52.

Caruso, G.D., Ferrari, E.R. and Pisano, V., 2016. Earnings management and goodwill

impairment: An empirical analysis in the Italian M & A context. Journal of Intellectual

Capital, 17(1), pp.120-147.

Chen, W., Shroff, P.K. and Zhang, I., 2017. Fair value accounting: consequences of

booking market-driven goodwill impairment. Available at SSRN 2420528.

Detzen, D., Wersborg, T.S.G. and Zülch, H., 2015. Bleak weather for sun-shine AG: A

case study of impairment of assets. Issues in Accounting Education, 30(2), pp.18-39.

Hassine, N.M. and Jilani, F., 2017. Earnings Management Behavior with Respect to

Goodwill Impairment Losses under IAS 36: The French Case. International Journal of

References:

Aasb.gov.au, 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-

09.pdf [Accessed 10 Jun. 2019].

Avallone, F. and Quagli, A., 2015. Insight into the variables used to manage the

goodwill impairment test under IAS 36. Advances in accounting, 31(1), pp.107-114.

Beaudoin, C.A. and Hughes, S.B., 2014. APT, Inc.: An application of impairment testing

and fair value estimation using International Financial Reporting Standards. Issues in

Accounting Education Teaching Notes, 29(1), pp.1-17.

Boučková, M., 2016. Quality of disclosed information with emphasis on goodwill

impairment. European Financial and Accounting Journal, 11(2), pp.37-52.

Caruso, G.D., Ferrari, E.R. and Pisano, V., 2016. Earnings management and goodwill

impairment: An empirical analysis in the Italian M & A context. Journal of Intellectual

Capital, 17(1), pp.120-147.

Chen, W., Shroff, P.K. and Zhang, I., 2017. Fair value accounting: consequences of

booking market-driven goodwill impairment. Available at SSRN 2420528.

Detzen, D., Wersborg, T.S.G. and Zülch, H., 2015. Bleak weather for sun-shine AG: A

case study of impairment of assets. Issues in Accounting Education, 30(2), pp.18-39.

Hassine, N.M. and Jilani, F., 2017. Earnings Management Behavior with Respect to

Goodwill Impairment Losses under IAS 36: The French Case. International Journal of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.