Corporate Accounting: Tax, Goodwill, and Non-Controlling Interests

VerifiedAdded on 2023/01/06

|16

|1943

|94

Homework Assignment

AI Summary

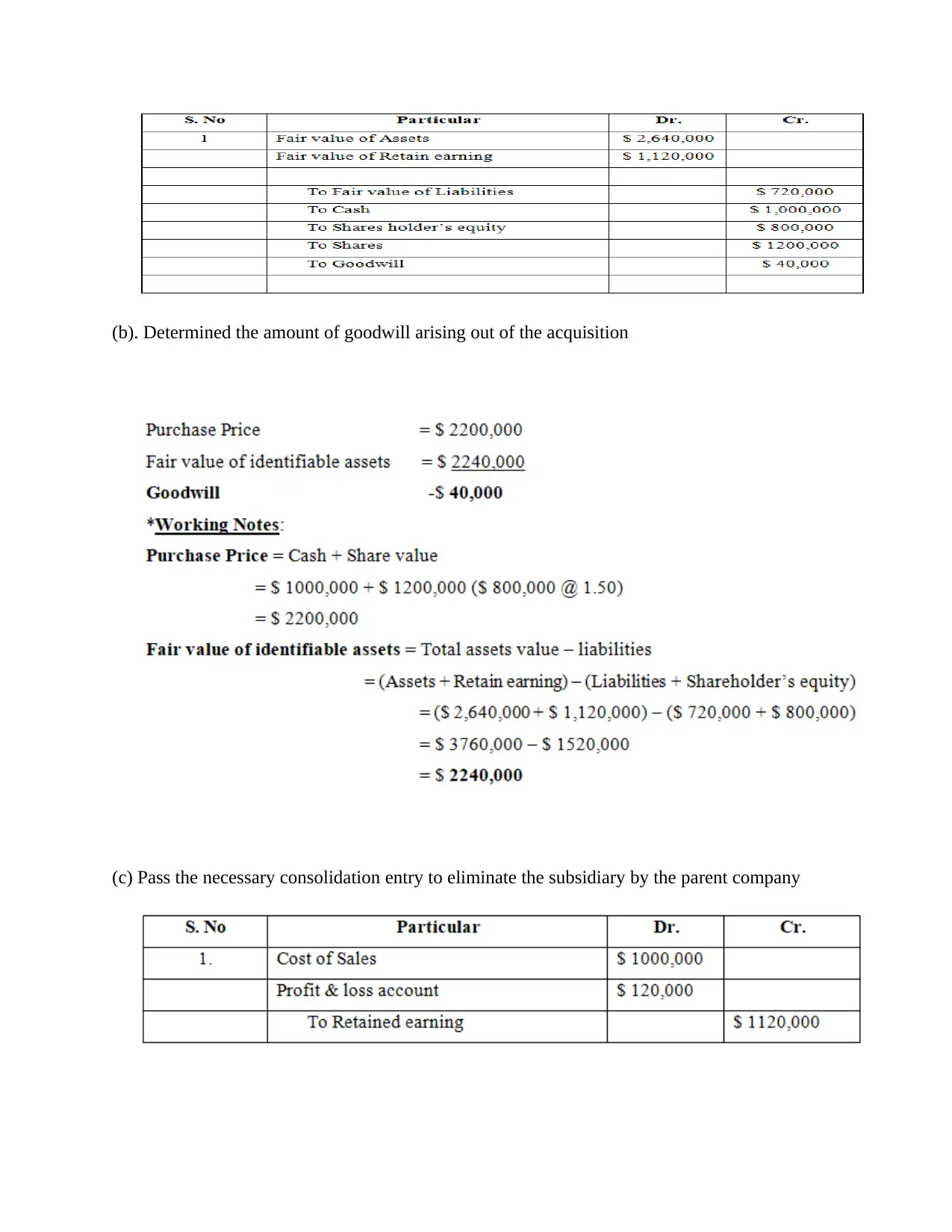

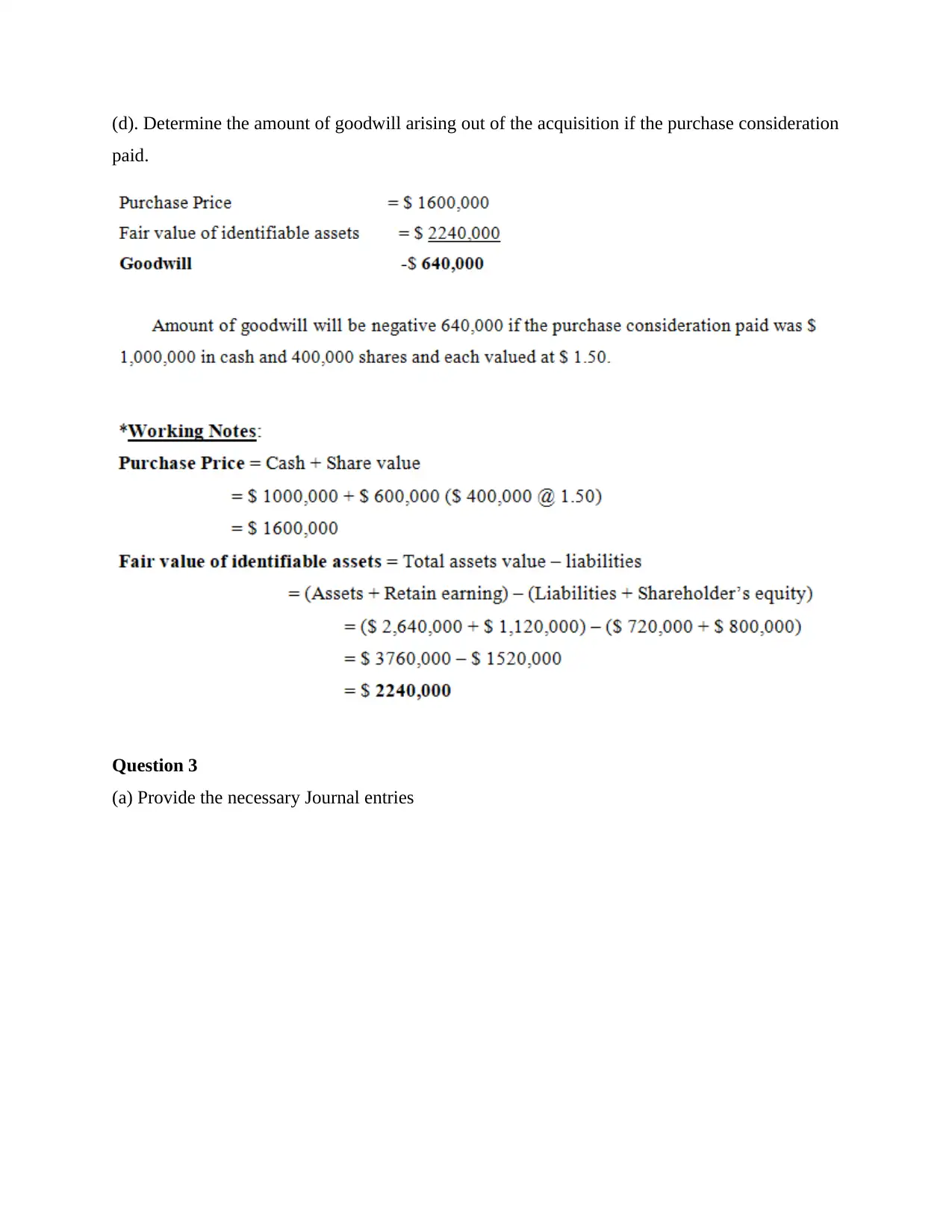

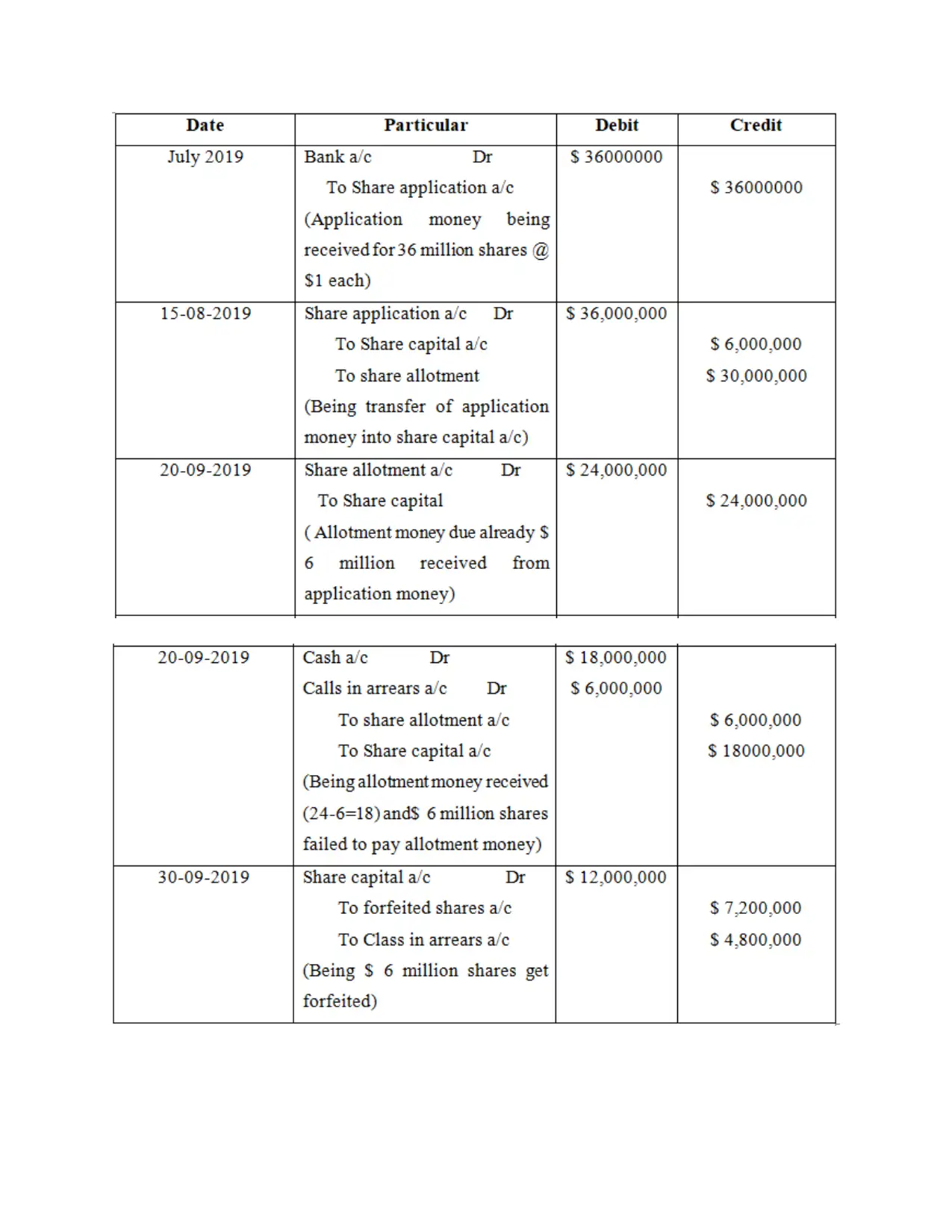

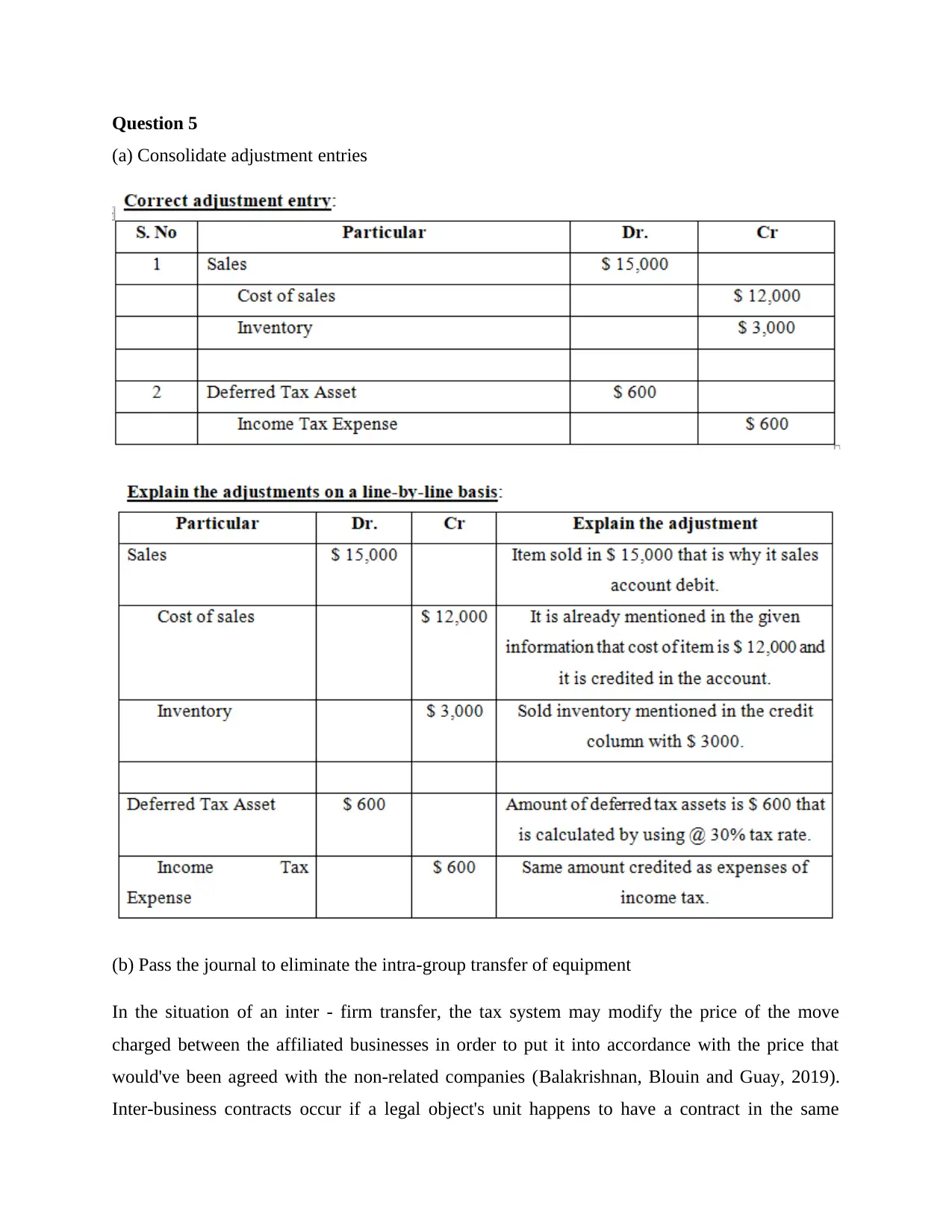

This homework assignment delves into various aspects of corporate accounting, providing detailed solutions to complex problems. It begins with the calculation of taxable profit and deferred tax liabilities, including the preparation of necessary journal entries. The assignment further explores topics such as recording acquisitions, determining goodwill, and preparing consolidation entries. It examines intra-group transactions, evaluating the portion needing elimination and the impact on non-controlling interests. The document outlines the steps to calculate total non-controlling interest and addresses inter-firm transfers, including adjustments for tax implications. The assignment concludes with calculations of goodwill and the preparation of journal entries for subsequent years, offering a comprehensive understanding of corporate accounting principles. The solution references key concepts like consolidation, non-controlling interests, and intra-group transactions, providing a thorough analysis of financial reporting and accounting practices.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.