Corporate Accounting: Detailed Analysis of Cash Flow, Income Tax, OCI

VerifiedAdded on 2024/06/03

|10

|2517

|356

Report

AI Summary

This report provides a detailed analysis of corporate accounting principles, focusing on cash flow statements, corporate income tax, and other comprehensive income (OCI). It examines the components of the cash flow statement, including operating, investing, and financing activities, using AMA Group Limited as a case study. The report offers a comparative evaluation of these cash flow categories over three years. Furthermore, it explores the items reported in the other comprehensive income statement and explains why these items are not included in the traditional income statement. The analysis extends to the firm's tax expense, deferred tax assets and liabilities, and the discrepancies between income tax expense and income tax payable. The report concludes by addressing the differences between the income tax expense shown in the income statement and the income tax paid as reflected in the cash flow statement, highlighting the timing differences and accounting standards that contribute to these variations. Desklib provides access to this and other solved assignments to support students.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Cash flows statement.......................................................................................................................3

Other comprehensive income statement..........................................................................................5

Accounting for corporate income tax..............................................................................................6

Reference List..................................................................................................................................9

2

Cash flows statement.......................................................................................................................3

Other comprehensive income statement..........................................................................................5

Accounting for corporate income tax..............................................................................................6

Reference List..................................................................................................................................9

2

Cash flows statement

(i) From your firm’s financial statement, list each item of reported in the CASH FLOWS

STATEMENT and write your understanding of each item. Discuss any changes in each

item of CASH FLOWS STATEMENT for your firm over the past year articulating the

reasons for the change.

Cash flow statement can be considered as a procedure that helps to depict about the amount of

cash generation in a specific time duration. This can be considered as one of the most important

financial statement that the experts are applied in order to create three-statement model. Cash

flow statement can be categorized into three different subparts such as (1) operating actions, (2)

investing actions and finally (3) financing actions of an organization (Bhasin, 2015). The sum of

total cash, which are provided by these three different activities that will arrive in the end of this

system can be considered as cash flow statement. In addition, in the bottom line, the cash flow

statement can be called as “closing cash balance”. In case of AMA group limited (the chosen

company of Australian Securities Exchange), cash flow statement plays a crucial role in order to

maintain and keep the record of every earnings of the company along with the debts.

Figure: Cash flow statement

(Source: Tahat et al., 2017)

3

(i) From your firm’s financial statement, list each item of reported in the CASH FLOWS

STATEMENT and write your understanding of each item. Discuss any changes in each

item of CASH FLOWS STATEMENT for your firm over the past year articulating the

reasons for the change.

Cash flow statement can be considered as a procedure that helps to depict about the amount of

cash generation in a specific time duration. This can be considered as one of the most important

financial statement that the experts are applied in order to create three-statement model. Cash

flow statement can be categorized into three different subparts such as (1) operating actions, (2)

investing actions and finally (3) financing actions of an organization (Bhasin, 2015). The sum of

total cash, which are provided by these three different activities that will arrive in the end of this

system can be considered as cash flow statement. In addition, in the bottom line, the cash flow

statement can be called as “closing cash balance”. In case of AMA group limited (the chosen

company of Australian Securities Exchange), cash flow statement plays a crucial role in order to

maintain and keep the record of every earnings of the company along with the debts.

Figure: Cash flow statement

(Source: Tahat et al., 2017)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

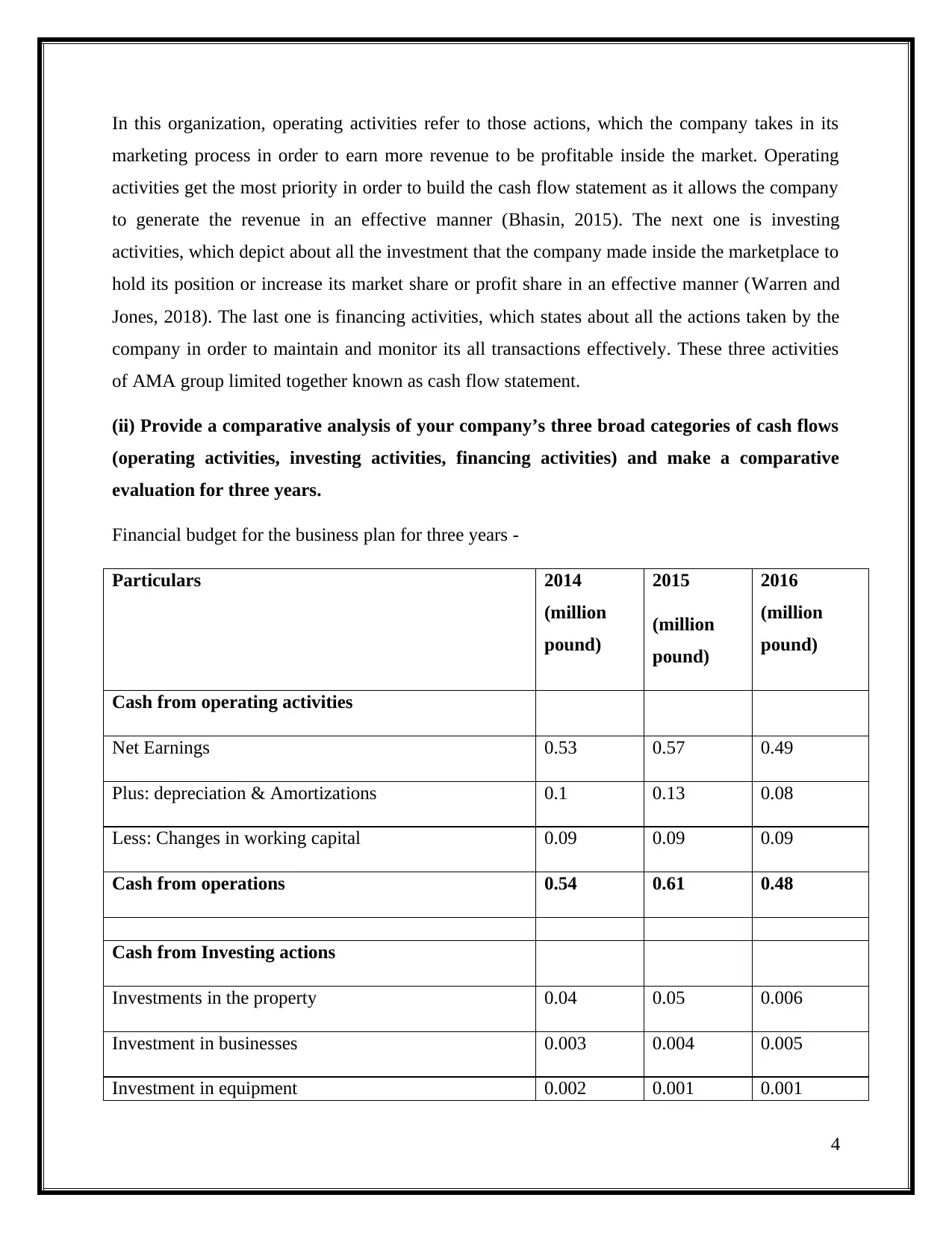

In this organization, operating activities refer to those actions, which the company takes in its

marketing process in order to earn more revenue to be profitable inside the market. Operating

activities get the most priority in order to build the cash flow statement as it allows the company

to generate the revenue in an effective manner (Bhasin, 2015). The next one is investing

activities, which depict about all the investment that the company made inside the marketplace to

hold its position or increase its market share or profit share in an effective manner (Warren and

Jones, 2018). The last one is financing activities, which states about all the actions taken by the

company in order to maintain and monitor its all transactions effectively. These three activities

of AMA group limited together known as cash flow statement.

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years.

Financial budget for the business plan for three years -

Particulars 2014

(million

pound)

2015

(million

pound)

2016

(million

pound)

Cash from operating activities

Net Earnings 0.53 0.57 0.49

Plus: depreciation & Amortizations 0.1 0.13 0.08

Less: Changes in working capital 0.09 0.09 0.09

Cash from operations 0.54 0.61 0.48

Cash from Investing actions

Investments in the property 0.04 0.05 0.006

Investment in businesses 0.003 0.004 0.005

Investment in equipment 0.002 0.001 0.001

4

marketing process in order to earn more revenue to be profitable inside the market. Operating

activities get the most priority in order to build the cash flow statement as it allows the company

to generate the revenue in an effective manner (Bhasin, 2015). The next one is investing

activities, which depict about all the investment that the company made inside the marketplace to

hold its position or increase its market share or profit share in an effective manner (Warren and

Jones, 2018). The last one is financing activities, which states about all the actions taken by the

company in order to maintain and monitor its all transactions effectively. These three activities

of AMA group limited together known as cash flow statement.

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years.

Financial budget for the business plan for three years -

Particulars 2014

(million

pound)

2015

(million

pound)

2016

(million

pound)

Cash from operating activities

Net Earnings 0.53 0.57 0.49

Plus: depreciation & Amortizations 0.1 0.13 0.08

Less: Changes in working capital 0.09 0.09 0.09

Cash from operations 0.54 0.61 0.48

Cash from Investing actions

Investments in the property 0.04 0.05 0.006

Investment in businesses 0.003 0.004 0.005

Investment in equipment 0.002 0.001 0.001

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash from operations 0.045 0.055 0.012

Cash from financing activities

Issuance (repayment) of debt 0.29 0.32 0.29

Issuance (repayment) of equity 0.09 0.1 0.08

Payment of Dividends 0.03 0.04 0.01

Cash from Financing 0.23 0.26 0.22

Net increase (decrease) in cash 0.3 0.7 0.6

Opening cash balance 0.8 0.9 1.3

Closing cash balance 1.915 2.525 2.612

Other comprehensive income statement

(iii) What items have been reported in the other comprehensive income statement

In AMA group limited, there are several other comprehensive revenue refers to those incomes

that are expenses, losses and gains underneath of “general accounting principle” as well as

“international financial report standards”, which can be excluded through the net revenue over

the revenue statement (Heese et al., 2015). The incomes, gains, expenses along with losses can

be appeared in case of other comprehensive revenues while those cannot be identified or

realized. There are several other things, which can be identified while the underlying transactions

have been completed effectively. For example, it can be stated that while the investment is solid

or secure, that can be called as comprehensive revenue. It AMA group limited, bonds (in case of

gaining or loss) can be taken into consideration in this context (Agrawal and Cooper, 2017).

5

Cash from financing activities

Issuance (repayment) of debt 0.29 0.32 0.29

Issuance (repayment) of equity 0.09 0.1 0.08

Payment of Dividends 0.03 0.04 0.01

Cash from Financing 0.23 0.26 0.22

Net increase (decrease) in cash 0.3 0.7 0.6

Opening cash balance 0.8 0.9 1.3

Closing cash balance 1.915 2.525 2.612

Other comprehensive income statement

(iii) What items have been reported in the other comprehensive income statement

In AMA group limited, there are several other comprehensive revenue refers to those incomes

that are expenses, losses and gains underneath of “general accounting principle” as well as

“international financial report standards”, which can be excluded through the net revenue over

the revenue statement (Heese et al., 2015). The incomes, gains, expenses along with losses can

be appeared in case of other comprehensive revenues while those cannot be identified or

realized. There are several other things, which can be identified while the underlying transactions

have been completed effectively. For example, it can be stated that while the investment is solid

or secure, that can be called as comprehensive revenue. It AMA group limited, bonds (in case of

gaining or loss) can be taken into consideration in this context (Agrawal and Cooper, 2017).

5

(iv) Explain your understanding of each item reported in the other comprehensive income

statement

The term comprehensive revenue, in case of “Net actions in order to exchange the rate of reserve

after taxation” denotes to those differences, which occurs during the inequality of exchange rates

when the volume of units is converted from one currency to another. This position in the other

insurance Australia account statement in 2015 was $ 70 million that was reduced to $ 20 million

in 2017. The last term in the other income statement of Insurance Australia is the other

comprehensive result, representing the net profit generated in a company from sources other than

ordinary business. This position in the Company's other income statement in 2015 was $ 43

million, from $ 10 million in 2016 (Bhasin, 2015).

(v) Why these items have not been reported in Income Statement/Profit and Loss

Statement

However, these items might not be included in a company's profit and loss account. They are

included in a AMA group limited 's other income statement because it affects the total results of

the company (Saeidi et al., 2015). The statement of other income accounts to cover this issue, as

well as the income of an organization, arising from any type of operation that differs from that of

general commercial operations.

The main cause for which the elements, like the net movement of currencies, the revaluation of

certain benefits, etc are create disadvantage for the company. Not listed in AMA group limited’s

results statement is that these items have no effect on net income after tax (Heese et al., 2015).

These items also do not affect the benefits accrued in the Company. As these two factors do not

affect, all of the remaining items must be excluded through the revenue statement.

Accounting for corporate income tax

(vi) What is your firm’s tax expense in its latest financial statements?

Tax expenditure can be described as thosee expenses or amounts that a company has to pay to

the government through which it can be operated as well as can be also recognized in case of the

profit plus loss account for every company. Insurance Australia's tax expense, as reported in the

Company's income statement, was $ 329 million for fiscal year ending 31 December 2017. The

6

statement

The term comprehensive revenue, in case of “Net actions in order to exchange the rate of reserve

after taxation” denotes to those differences, which occurs during the inequality of exchange rates

when the volume of units is converted from one currency to another. This position in the other

insurance Australia account statement in 2015 was $ 70 million that was reduced to $ 20 million

in 2017. The last term in the other income statement of Insurance Australia is the other

comprehensive result, representing the net profit generated in a company from sources other than

ordinary business. This position in the Company's other income statement in 2015 was $ 43

million, from $ 10 million in 2016 (Bhasin, 2015).

(v) Why these items have not been reported in Income Statement/Profit and Loss

Statement

However, these items might not be included in a company's profit and loss account. They are

included in a AMA group limited 's other income statement because it affects the total results of

the company (Saeidi et al., 2015). The statement of other income accounts to cover this issue, as

well as the income of an organization, arising from any type of operation that differs from that of

general commercial operations.

The main cause for which the elements, like the net movement of currencies, the revaluation of

certain benefits, etc are create disadvantage for the company. Not listed in AMA group limited’s

results statement is that these items have no effect on net income after tax (Heese et al., 2015).

These items also do not affect the benefits accrued in the Company. As these two factors do not

affect, all of the remaining items must be excluded through the revenue statement.

Accounting for corporate income tax

(vi) What is your firm’s tax expense in its latest financial statements?

Tax expenditure can be described as thosee expenses or amounts that a company has to pay to

the government through which it can be operated as well as can be also recognized in case of the

profit plus loss account for every company. Insurance Australia's tax expense, as reported in the

Company's income statement, was $ 329 million for fiscal year ending 31 December 2017. The

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

latest AMA group limited accounts also show that The Company's income tax expense was in

2016 $ 218 million (Atanasov and Black, 2016).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

The tax rate paid to the government by all publicly listed companies listed under ASX is 35%.

Insurance Australia Group Limited also has to pay a 30% tax on its accounting profits. However,

when analyzing the tax expense of the recent financial reports of the AMA group limited, it is

possible to verify that the tax expense recognized in the company's income statement is higher

than the taxable amount if the tax rate is 35%. This demonstrates that the tax expense of AMA

group limited does not match the tax rates of organizational accounting revenue (Killian and

O'Regan, 2016).

On the other hand, the examination of the explanations of the company's accounts shows why

and how the figure is different. The company's tax is calculated at a tax rate of 35%. Though, the

difference occurred because the company adjusted non-taxable amounts, such as the difference

between the tax rate, dividends, etc., which used the company's tax rates and insurance tax

expenditures. AMA group limited was different in the previous year of each other (Schneider,

2015). The following is an exposition of the tax expenditures of Insurance Australia Group

Limited during the past two years,

(viii) Comment on deferred tax assets/liabilities that is reported in the balance sheet

articulating the possible reasons why they have been recorded.

() stated that the delayed tax properties can be recognized in the company's balance sheet relate

to the prepaid expenses of the company which serve as an asset as they help the company to

reduce its taxable income. Besides that, Heese et al., (2015) argued that deferred tax liability is

the unpaid cost of a company regarded as a company's responsibility as it ultimately increases

the taxable profits of the business. The clarification of the financial statements of AMA group

limited, and especially its balance sheets, shows that there are no deferred tax liabilities in the

company.

On the other hand, the examination of the “balance sheet” of the Company's balance shows that

AMA group limited has deferred tax assets. The analysis of the Company's balance sheet shows

7

2016 $ 218 million (Atanasov and Black, 2016).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

The tax rate paid to the government by all publicly listed companies listed under ASX is 35%.

Insurance Australia Group Limited also has to pay a 30% tax on its accounting profits. However,

when analyzing the tax expense of the recent financial reports of the AMA group limited, it is

possible to verify that the tax expense recognized in the company's income statement is higher

than the taxable amount if the tax rate is 35%. This demonstrates that the tax expense of AMA

group limited does not match the tax rates of organizational accounting revenue (Killian and

O'Regan, 2016).

On the other hand, the examination of the explanations of the company's accounts shows why

and how the figure is different. The company's tax is calculated at a tax rate of 35%. Though, the

difference occurred because the company adjusted non-taxable amounts, such as the difference

between the tax rate, dividends, etc., which used the company's tax rates and insurance tax

expenditures. AMA group limited was different in the previous year of each other (Schneider,

2015). The following is an exposition of the tax expenditures of Insurance Australia Group

Limited during the past two years,

(viii) Comment on deferred tax assets/liabilities that is reported in the balance sheet

articulating the possible reasons why they have been recorded.

() stated that the delayed tax properties can be recognized in the company's balance sheet relate

to the prepaid expenses of the company which serve as an asset as they help the company to

reduce its taxable income. Besides that, Heese et al., (2015) argued that deferred tax liability is

the unpaid cost of a company regarded as a company's responsibility as it ultimately increases

the taxable profits of the business. The clarification of the financial statements of AMA group

limited, and especially its balance sheets, shows that there are no deferred tax liabilities in the

company.

On the other hand, the examination of the “balance sheet” of the Company's balance shows that

AMA group limited has deferred tax assets. The analysis of the Company's balance sheet shows

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that the Company had deferred tax assets of $ 553 million in 2016, which changed by 2017 and

decreased to 550 million dollars. This reflects a decrease in deferred tax. of the company

indicates assets. However, there are several reasons why a company recognizes its “deferred tax

asset” into the balance sheet.

Subsequently the “deferred tax” possessions of AMA group limited are prepaid expenses and the

Company's taxable income may be reduced in future due to this prepaid cost, it can be argued

that the Company recognizes deferred tax assets in its balance sheet that may reduce the taxable

revenue.

(ix) Is there any current tax assets or income tax payable recorded by your company? Why

is the income tax payable not the same as income tax expense?

The instructions for economic accounting as well as tax accounting differ in several areas. The

most basic differences are how an organization devaluates its possessions (Atanasov and Black,

2016). According to generally accepted accounting principles, a company can cancel assets in

almost any chronicle, provided that this schedule is “systematic and rational”. However, the tax

act requires that assets should be recorded in accordance with very accurate guidelines. As the

business's depreciation directly affects the company and taxes your company tax on the profits,

the difference among the two accounting rules leads to two different calculations of the

business's tax liabilities.

“Expense on income tax” can be considered those that have calculated entity pays tax based on

the usual accounting standards. It should be declared that this type of expense in the income

statement. The “Income Tax” is the actual amount that the company pays in tax according to the

rules of the Tax Act. The payable income tax appears as a liability in the balance sheet until the

company pays the tax account (Schneider, 2015).

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?

Differences in financial and tax balances need to be balanced over time. With depreciation, to

use the previous example, the two systems eventually lose the same amount of value; the

difference is just in time. For example, the tax burden on the company may be higher this year

than the actual tax, but at a later date the tax account will be higher than the tax account.

8

decreased to 550 million dollars. This reflects a decrease in deferred tax. of the company

indicates assets. However, there are several reasons why a company recognizes its “deferred tax

asset” into the balance sheet.

Subsequently the “deferred tax” possessions of AMA group limited are prepaid expenses and the

Company's taxable income may be reduced in future due to this prepaid cost, it can be argued

that the Company recognizes deferred tax assets in its balance sheet that may reduce the taxable

revenue.

(ix) Is there any current tax assets or income tax payable recorded by your company? Why

is the income tax payable not the same as income tax expense?

The instructions for economic accounting as well as tax accounting differ in several areas. The

most basic differences are how an organization devaluates its possessions (Atanasov and Black,

2016). According to generally accepted accounting principles, a company can cancel assets in

almost any chronicle, provided that this schedule is “systematic and rational”. However, the tax

act requires that assets should be recorded in accordance with very accurate guidelines. As the

business's depreciation directly affects the company and taxes your company tax on the profits,

the difference among the two accounting rules leads to two different calculations of the

business's tax liabilities.

“Expense on income tax” can be considered those that have calculated entity pays tax based on

the usual accounting standards. It should be declared that this type of expense in the income

statement. The “Income Tax” is the actual amount that the company pays in tax according to the

rules of the Tax Act. The payable income tax appears as a liability in the balance sheet until the

company pays the tax account (Schneider, 2015).

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?

Differences in financial and tax balances need to be balanced over time. With depreciation, to

use the previous example, the two systems eventually lose the same amount of value; the

difference is just in time. For example, the tax burden on the company may be higher this year

than the actual tax, but at a later date the tax account will be higher than the tax account.

8

Conversely, if this year's tax expense is less than the actual fiscal bill, a future fiscal bill will be

greater than the cost (Atanasov and Black, 2016). If the company's income tax expense differs

from the actual tax account, the difference must appear on the balance sheet so that it can be

exhausted later.

9

greater than the cost (Atanasov and Black, 2016). If the company's income tax expense differs

from the actual tax account, the difference must appear on the balance sheet so that it can be

exhausted later.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference List

Bhasin, M.L., 2015. Corporate accounting fraud: A case study of Satyam Computers Limited.

Tahat, Y., Omran, M. and Dunne, T., 2017. Development of Accounting Regulations and

Practices in Kuwait: An Analytical Review. Journal of Corporate Accounting & Finance, 28(6),

pp.14-28.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Heese, J., Khan, M. and Ramanna, K., 2015. Political Standards: Corporate Interest, Ideology,

and Leadership in the Shaping of Accounting Rules for the Market Economy. Journal of

Accounting & Economics, 64(20), pp.2-3.

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of Finance, 7(01),

p.1650014.

Saeidi, S.P., Sofian, S., Saeidi, P., Saeidi, S.P. and Saaeidi, S.A., 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of Business Research, 68(2), pp.341-

350.

Atanasov, V. and Black, B., 2016. Shock-based causal inference in corporate finance and

accounting research.

Killian, S. and O'Regan, P., 2016. Social accounting and the co-creation of corporate

legitimacy. Accounting, Organizations and Society, 50, pp.1-12.

Schneider, A., 2015. Reflexivity in sustainability accounting and management: Transcending the

economic focus of corporate sustainability. Journal of Business Ethics, 127(3), pp.525-536.

10

Bhasin, M.L., 2015. Corporate accounting fraud: A case study of Satyam Computers Limited.

Tahat, Y., Omran, M. and Dunne, T., 2017. Development of Accounting Regulations and

Practices in Kuwait: An Analytical Review. Journal of Corporate Accounting & Finance, 28(6),

pp.14-28.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Heese, J., Khan, M. and Ramanna, K., 2015. Political Standards: Corporate Interest, Ideology,

and Leadership in the Shaping of Accounting Rules for the Market Economy. Journal of

Accounting & Economics, 64(20), pp.2-3.

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of Finance, 7(01),

p.1650014.

Saeidi, S.P., Sofian, S., Saeidi, P., Saeidi, S.P. and Saaeidi, S.A., 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of Business Research, 68(2), pp.341-

350.

Atanasov, V. and Black, B., 2016. Shock-based causal inference in corporate finance and

accounting research.

Killian, S. and O'Regan, P., 2016. Social accounting and the co-creation of corporate

legitimacy. Accounting, Organizations and Society, 50, pp.1-12.

Schneider, A., 2015. Reflexivity in sustainability accounting and management: Transcending the

economic focus of corporate sustainability. Journal of Business Ethics, 127(3), pp.525-536.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.