Corporate Accounting: Evaluation of Income and Cash Flow Statements

VerifiedAdded on 2023/01/06

|33

|4723

|96

AI Summary

This study evaluates the usefulness of income and cash flow statements for investors and conducts a critical analysis of the consolidated cash flow statements of three companies. It also assesses the cash flow trends and compares them to net profit after tax and dividend payments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Corporate Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

The study-report summarizes thorough evaluation of relative information contents of income-

statement as well as cash-flow statement with aim to assess how these statements are useful for

investors. Moreover, study conducts critical analysis of consolidated cash-flow-statements of

three companies Santos Ltd, BHP Ltd and Funtastic Ltd to assess the actual comparative

performance of such corporations during period 2017 to 2019 with aim to explore different

financial aspects of each corporation, their strengths and identify which company is most

preferable for lending.

The study-report summarizes thorough evaluation of relative information contents of income-

statement as well as cash-flow statement with aim to assess how these statements are useful for

investors. Moreover, study conducts critical analysis of consolidated cash-flow-statements of

three companies Santos Ltd, BHP Ltd and Funtastic Ltd to assess the actual comparative

performance of such corporations during period 2017 to 2019 with aim to explore different

financial aspects of each corporation, their strengths and identify which company is most

preferable for lending.

Contents

EXECUTIVE SUMMARY.......................................................................................................................2

INTRODUCTION.....................................................................................................................................4

MAIN BODY.............................................................................................................................................4

Part A......................................................................................................................................................4

Part B.......................................................................................................................................................7

CONCLUSION........................................................................................................................................30

REFERENCES........................................................................................................................................32

EXECUTIVE SUMMARY.......................................................................................................................2

INTRODUCTION.....................................................................................................................................4

MAIN BODY.............................................................................................................................................4

Part A......................................................................................................................................................4

Part B.......................................................................................................................................................7

CONCLUSION........................................................................................................................................30

REFERENCES........................................................................................................................................32

INTRODUCTION

Each organization needs to do some sort of accounting. This is essential for assess the financial

state of the company. Accounting, also regarded as bookkeeping, encompasses the selection,

examination, assessment, evaluation, presentation and distribution of financial details

(Schaltegger, Etxeberria and Ortas, 2017). There are several forms of accounting. Corporate

accounting is also one of them. It's better suited for corporations. Corporate accounting copes

with procedures like compiling cash-flows statements, tax returns, income statements and much

more. It may be employed to control specific business operations like acquisition, amalgamation

as well as the development of consolidated reports. The study-report covers different aspects of

corporate accounting in two distinct parts. The first part evaluates basic contents of cash-flow

statement & income-statement as to assess why these contents are useful for

stakeholders/investors. While other part evaluates consolidated-cash flow statement of

mentioned companies as to assess their real performance and identify other relevant aspects.

MAIN BODY

Part A

Reviewing information stated in income statements and cash-flows statements.

Financial statements of a company are compiled records which reflect the corporation 's

corporate practices and finance reports. Financial statements are audited by government bodies,

auditors, agencies, etc. as to ensure compliance and for accounting, finance or investment

objectives. The financial statements therefore mainly involve: balance-sheet, income statement

(P&L a/c) and Cash-flow statement. Financial statements of corporation provide investors with a

portrayal of all activities which go into the firm, where each transaction leads to its performance.

A cash-flow statement considered to be most insightful among financial statements since it

reflects cash created by the company in three major ways — via operations, investments and

financing (Liu, Zeng and An, 2017). The amount of such three segments is considered net cash

flows. Here is thorough review of contents and information of income and cash-flows statement:

Each organization needs to do some sort of accounting. This is essential for assess the financial

state of the company. Accounting, also regarded as bookkeeping, encompasses the selection,

examination, assessment, evaluation, presentation and distribution of financial details

(Schaltegger, Etxeberria and Ortas, 2017). There are several forms of accounting. Corporate

accounting is also one of them. It's better suited for corporations. Corporate accounting copes

with procedures like compiling cash-flows statements, tax returns, income statements and much

more. It may be employed to control specific business operations like acquisition, amalgamation

as well as the development of consolidated reports. The study-report covers different aspects of

corporate accounting in two distinct parts. The first part evaluates basic contents of cash-flow

statement & income-statement as to assess why these contents are useful for

stakeholders/investors. While other part evaluates consolidated-cash flow statement of

mentioned companies as to assess their real performance and identify other relevant aspects.

MAIN BODY

Part A

Reviewing information stated in income statements and cash-flows statements.

Financial statements of a company are compiled records which reflect the corporation 's

corporate practices and finance reports. Financial statements are audited by government bodies,

auditors, agencies, etc. as to ensure compliance and for accounting, finance or investment

objectives. The financial statements therefore mainly involve: balance-sheet, income statement

(P&L a/c) and Cash-flow statement. Financial statements of corporation provide investors with a

portrayal of all activities which go into the firm, where each transaction leads to its performance.

A cash-flow statement considered to be most insightful among financial statements since it

reflects cash created by the company in three major ways — via operations, investments and

financing (Liu, Zeng and An, 2017). The amount of such three segments is considered net cash

flows. Here is thorough review of contents and information of income and cash-flows statement:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Income statement- The income statement is accounting statement which displays how profitable

the company has been over the fiscal period. This indicates company's profits, minus

company's expenses and other losses. Here is review of information-content of income-

statement, as follows:

Sales/turnover: Sales turnover is the money earned by the corporation from the selling of

products. In finance, the words "selling" and "revenues" are sometimes used interchangeable

terms to describe same thing. this is necessary to remember that income does not always equal

cash earned. A proportion of sales may be charged in cash as well as a part may be charged out

on credits by means like trade receivables accounts. Sales revenue is displayed on income

statement both as gross sales figure or net-revenues.

Cost-of-goods sold: Usually referred to "COGS," which shows how much it takes to create all

the products/services company has provided to customers. COGS only include direct costs such

as materials, wage costs and transport costs (Hoang and Joseph, 2019).

Gross Profit: This is amount of what business get after deducting overall COGS from

turnover/sales. Gross profit demonstrates how profitable the company is, considering direct

costs, but prior considering overhead costs. This is a basic indicator of how effective a company

is.

General expenses: also refers to as operating expenses which include leases, banking & Internet

banking fees, machinery expenses, advertisement & promotional expenses, promotions, and all

other spending will require to keep running.

Operating earnings: This shows how profitable the company is after considering internal costs,

which company have more influence over, but prior to considering external costs, such as

mortgage interest rates and taxation, which company have little control over.

Net Profit: this figure which shows actual profitability status and net profit sum remain after

considering all business expenses.

Cash-flow Statement: A cash balance statement lays down the multiple kinds of cash-inflows

and cash-outflows (as well as cash-equivalents) which a corporation experiences which is

perhaps one most significant financial statements corporation can produce. understanding how to

the company has been over the fiscal period. This indicates company's profits, minus

company's expenses and other losses. Here is review of information-content of income-

statement, as follows:

Sales/turnover: Sales turnover is the money earned by the corporation from the selling of

products. In finance, the words "selling" and "revenues" are sometimes used interchangeable

terms to describe same thing. this is necessary to remember that income does not always equal

cash earned. A proportion of sales may be charged in cash as well as a part may be charged out

on credits by means like trade receivables accounts. Sales revenue is displayed on income

statement both as gross sales figure or net-revenues.

Cost-of-goods sold: Usually referred to "COGS," which shows how much it takes to create all

the products/services company has provided to customers. COGS only include direct costs such

as materials, wage costs and transport costs (Hoang and Joseph, 2019).

Gross Profit: This is amount of what business get after deducting overall COGS from

turnover/sales. Gross profit demonstrates how profitable the company is, considering direct

costs, but prior considering overhead costs. This is a basic indicator of how effective a company

is.

General expenses: also refers to as operating expenses which include leases, banking & Internet

banking fees, machinery expenses, advertisement & promotional expenses, promotions, and all

other spending will require to keep running.

Operating earnings: This shows how profitable the company is after considering internal costs,

which company have more influence over, but prior to considering external costs, such as

mortgage interest rates and taxation, which company have little control over.

Net Profit: this figure which shows actual profitability status and net profit sum remain after

considering all business expenses.

Cash-flow Statement: A cash balance statement lays down the multiple kinds of cash-inflows

and cash-outflows (as well as cash-equivalents) which a corporation experiences which is

perhaps one most significant financial statements corporation can produce. understanding how to

compose and analyze cash flows statement is fast and efficient. this can let manager and other

stakeholders better see how corporation generates or expenses cash, how much cash is expended

or raised, which can give useful insights into the corporation 's finances. Here below is

evaluation of information-content of cash-flow statement, as follows:

Cash-flows through Operating Activities: The net sum of funds in or out of a corporation's day-

to-day operating activities is considered Cash Flow through Operations. There are operating

revenues and non-cash items like depreciation incurred (Harring, Jagers and Matti, 2019).

Because operating results are diminished through non-cash items like depreciation and

amortization) they have to be applied back to operating income in order to determine cash flows.

cash flow through operations is essential indicator since it shows the investor about the

profitability of the existing business strategy and activities. In long term, cash generation from

operations would be revenue inflows in return for the company to be sustainable and account for

usual outflows through investment and financing activities.

Cash through Investing Activities: Investment operations involve both forms and applications of

cash through investments made by a corporation. Buy or disposal of an assets, loans provided to

or obtained, or other payouts relating to mergers or acquisitions shall be specified in this section.

In brief, shifts in infrastructure, assets, investments are related to cash through investing.

Generally, cash changes through investment are "cash out" object, since cash is utilized to

purchase new machinery, buildings, or shorter-term assets like sellable securities. Conversely,

whenever a corporation relinquishes an asset, deal is perceived to be a cash in as to

determine cash from investments.

Cash through Financing Activities: Cash through financing operations requires channels of funds

from customers or financial institutions, and also the usage of cash provided to stakeholders.

Collection of dividends, buyback payments including redemption of the primary debt

(mortgages) are specified in this section (Warren and Jones, 2018). Adjustments of cash through

financing are regarded as cash in" if money is collected and cash-out if dividends are taken out.

Therefore, when a corporation sells bonds to public, the corporation collects cash financing; but,

when interests is accrued to bondholders, corporation reduces its capital.

Significance of income statement for investors:

stakeholders better see how corporation generates or expenses cash, how much cash is expended

or raised, which can give useful insights into the corporation 's finances. Here below is

evaluation of information-content of cash-flow statement, as follows:

Cash-flows through Operating Activities: The net sum of funds in or out of a corporation's day-

to-day operating activities is considered Cash Flow through Operations. There are operating

revenues and non-cash items like depreciation incurred (Harring, Jagers and Matti, 2019).

Because operating results are diminished through non-cash items like depreciation and

amortization) they have to be applied back to operating income in order to determine cash flows.

cash flow through operations is essential indicator since it shows the investor about the

profitability of the existing business strategy and activities. In long term, cash generation from

operations would be revenue inflows in return for the company to be sustainable and account for

usual outflows through investment and financing activities.

Cash through Investing Activities: Investment operations involve both forms and applications of

cash through investments made by a corporation. Buy or disposal of an assets, loans provided to

or obtained, or other payouts relating to mergers or acquisitions shall be specified in this section.

In brief, shifts in infrastructure, assets, investments are related to cash through investing.

Generally, cash changes through investment are "cash out" object, since cash is utilized to

purchase new machinery, buildings, or shorter-term assets like sellable securities. Conversely,

whenever a corporation relinquishes an asset, deal is perceived to be a cash in as to

determine cash from investments.

Cash through Financing Activities: Cash through financing operations requires channels of funds

from customers or financial institutions, and also the usage of cash provided to stakeholders.

Collection of dividends, buyback payments including redemption of the primary debt

(mortgages) are specified in this section (Warren and Jones, 2018). Adjustments of cash through

financing are regarded as cash in" if money is collected and cash-out if dividends are taken out.

Therefore, when a corporation sells bonds to public, the corporation collects cash financing; but,

when interests is accrued to bondholders, corporation reduces its capital.

Significance of income statement for investors:

Investors consider company's income statement to assess the performance of a business over

period. Investors watch at patterns in business expenditures and profits when the document

breaks down employee sales and expenditures. If a corporation is not prosperous or if the

earnings transition year over year, income statement allows them to know where sum is flowing.

The details regarding earnings per share is another crucial aspect for investors. That sum that a

corporation will pay to its shareholders on every share, if company paid out most of net profits as

dividends. Companies should not have to render such payments, however, and they generally

reinvest the cash back into company rather than paying this to shareholders. When a corporation

pays dividends to investors, the income statement would indicate how much corporation has paid

out.

Significance of cash flow statement for investors:

This allows investors to utilize information about company’s past cash-flows to forecast potential

cash-flows on that to based their investment choices (Ioannidis, 2019). It demonstrates

improvements in balance sheet and assists in the review of operations, acquisition and financing

operations. This gives insights into the liquidity including solvency of company and is crucial to

the sustainability and success of every company. This indicates the financial condition of the

organization over a span of time. This allows to provide information on cash-generating

capacities of the key operations of the organization. Stockholders and investors prefer to

contrast Cash-Flow Statements of several firms as they allow them to disclose the consistency of

their revenues. This helps to make the appropriate decision for them. Given that the corporation

has certain longer-term financial commitments, Cash Flow Statement helps investors and lenders

to assess the probability of redemption. It could be utilized to forecast accurately the pace,

quantities and volatility of potential cash flows.

Part B

1.Examination of cash flow of each company.

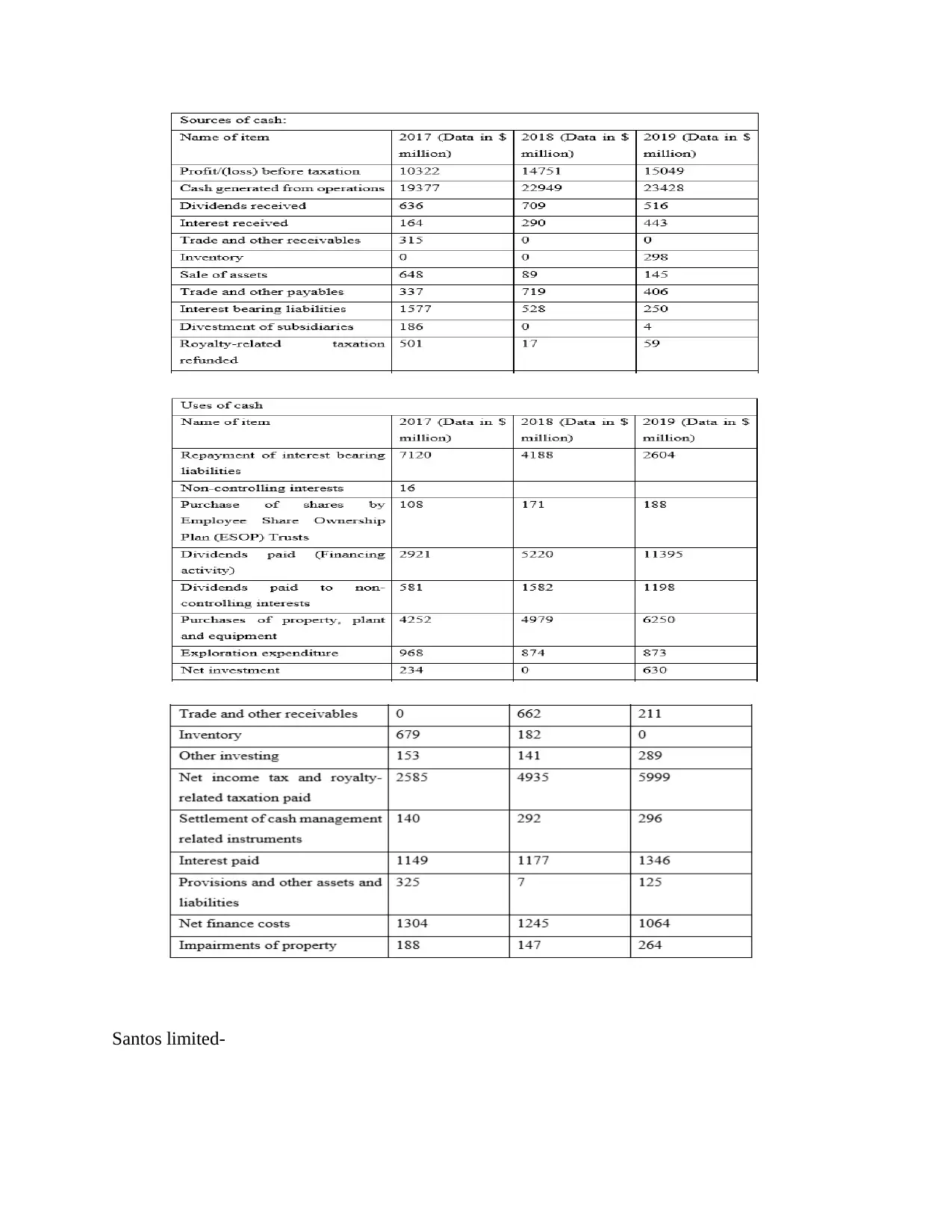

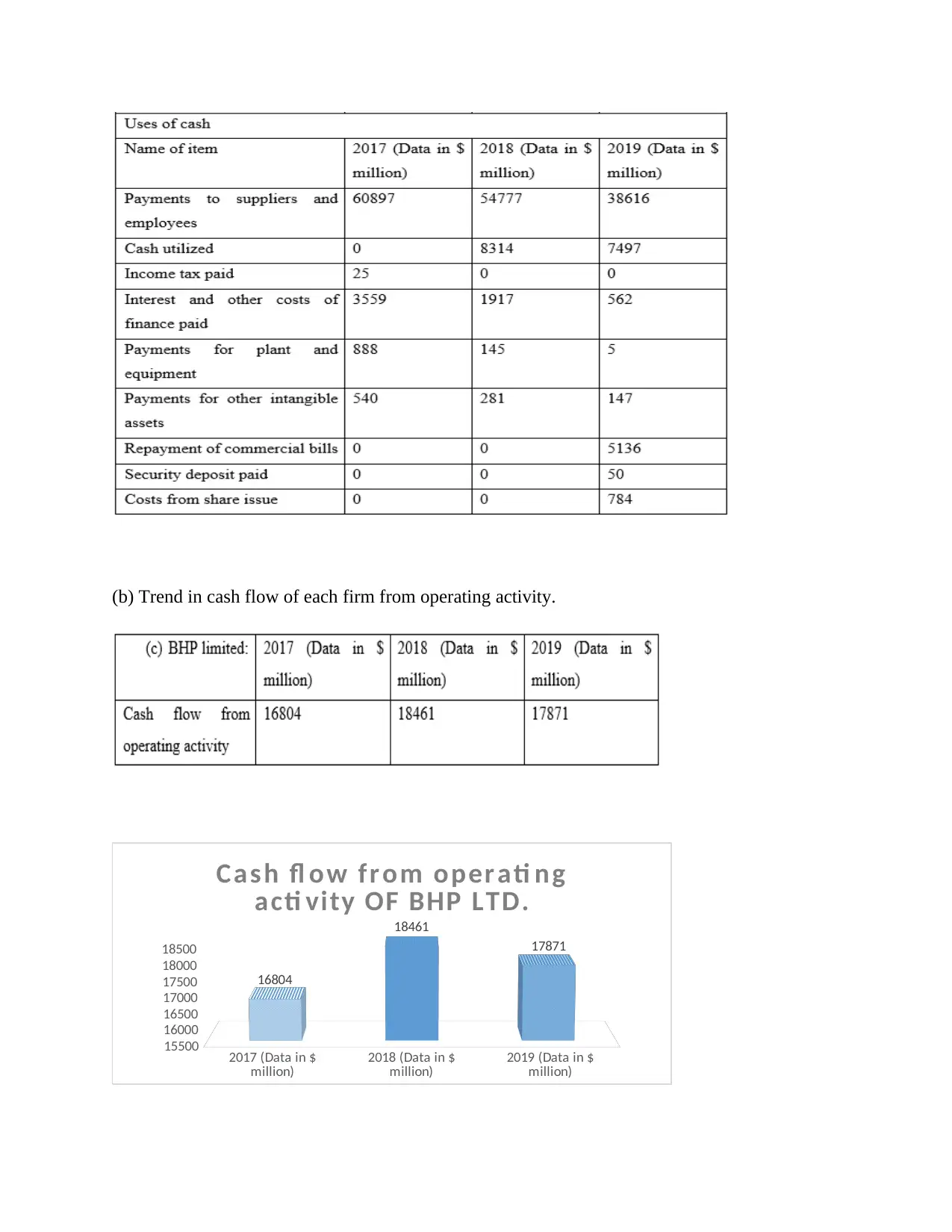

(a) Major source and uses of cash of each firm.

BHP limited:

period. Investors watch at patterns in business expenditures and profits when the document

breaks down employee sales and expenditures. If a corporation is not prosperous or if the

earnings transition year over year, income statement allows them to know where sum is flowing.

The details regarding earnings per share is another crucial aspect for investors. That sum that a

corporation will pay to its shareholders on every share, if company paid out most of net profits as

dividends. Companies should not have to render such payments, however, and they generally

reinvest the cash back into company rather than paying this to shareholders. When a corporation

pays dividends to investors, the income statement would indicate how much corporation has paid

out.

Significance of cash flow statement for investors:

This allows investors to utilize information about company’s past cash-flows to forecast potential

cash-flows on that to based their investment choices (Ioannidis, 2019). It demonstrates

improvements in balance sheet and assists in the review of operations, acquisition and financing

operations. This gives insights into the liquidity including solvency of company and is crucial to

the sustainability and success of every company. This indicates the financial condition of the

organization over a span of time. This allows to provide information on cash-generating

capacities of the key operations of the organization. Stockholders and investors prefer to

contrast Cash-Flow Statements of several firms as they allow them to disclose the consistency of

their revenues. This helps to make the appropriate decision for them. Given that the corporation

has certain longer-term financial commitments, Cash Flow Statement helps investors and lenders

to assess the probability of redemption. It could be utilized to forecast accurately the pace,

quantities and volatility of potential cash flows.

Part B

1.Examination of cash flow of each company.

(a) Major source and uses of cash of each firm.

BHP limited:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

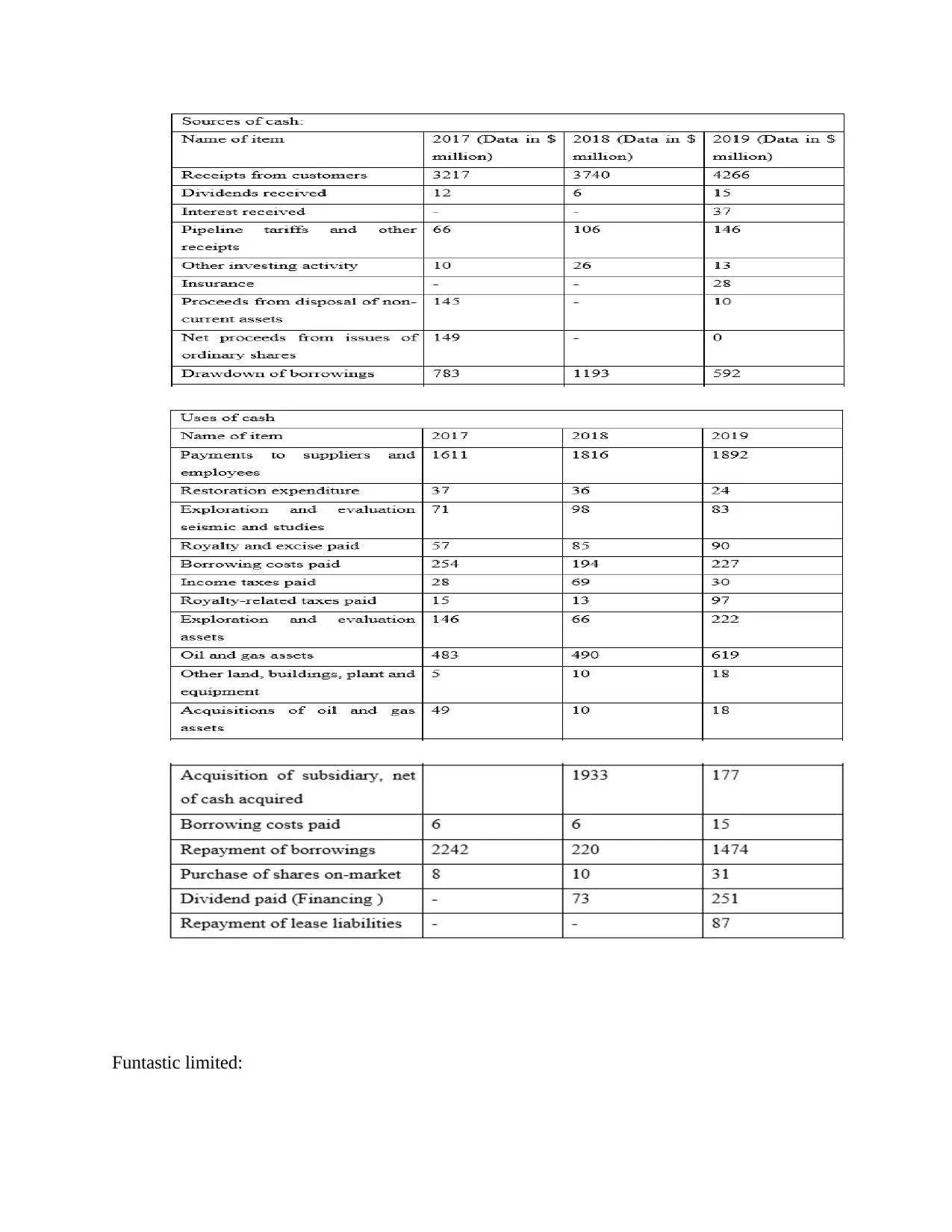

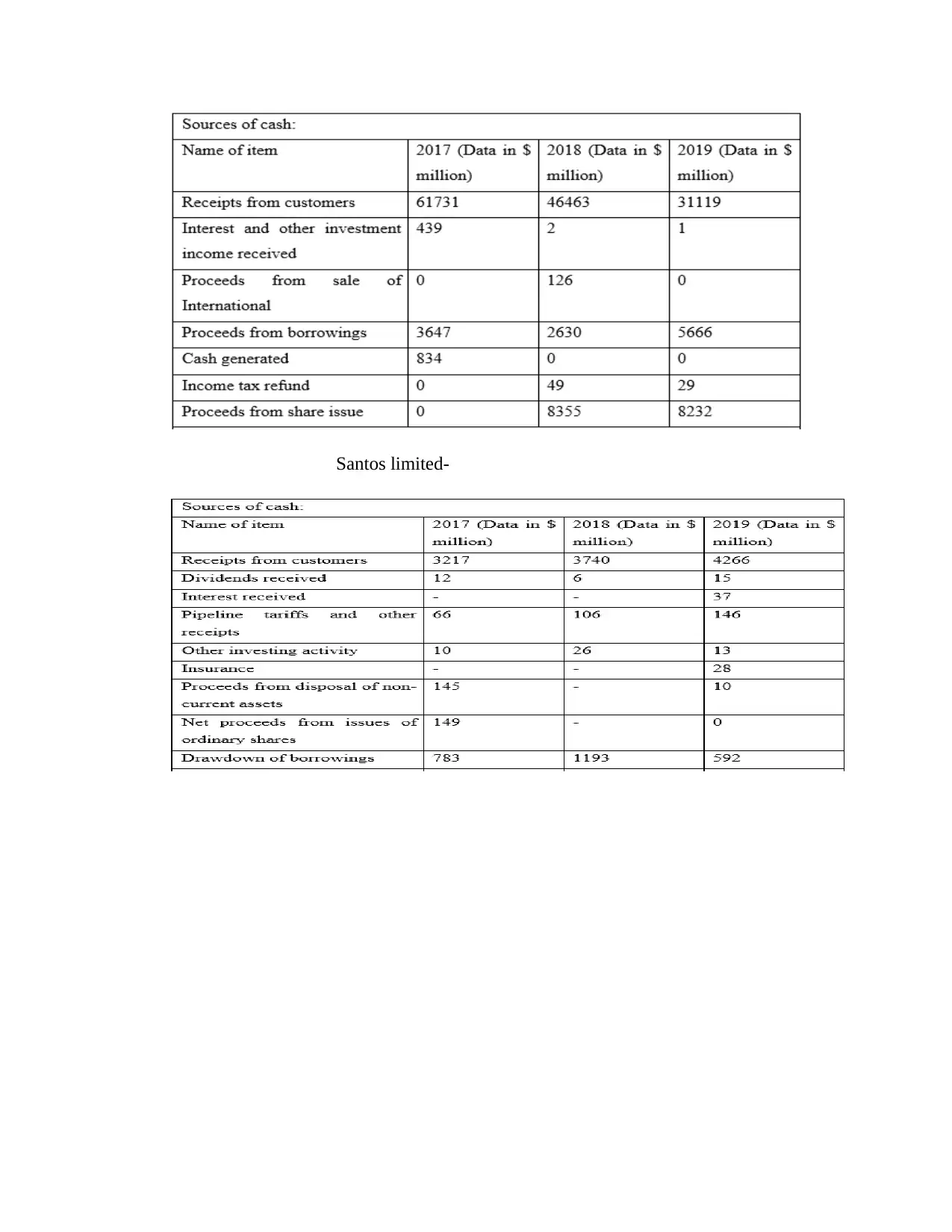

Santos limited-

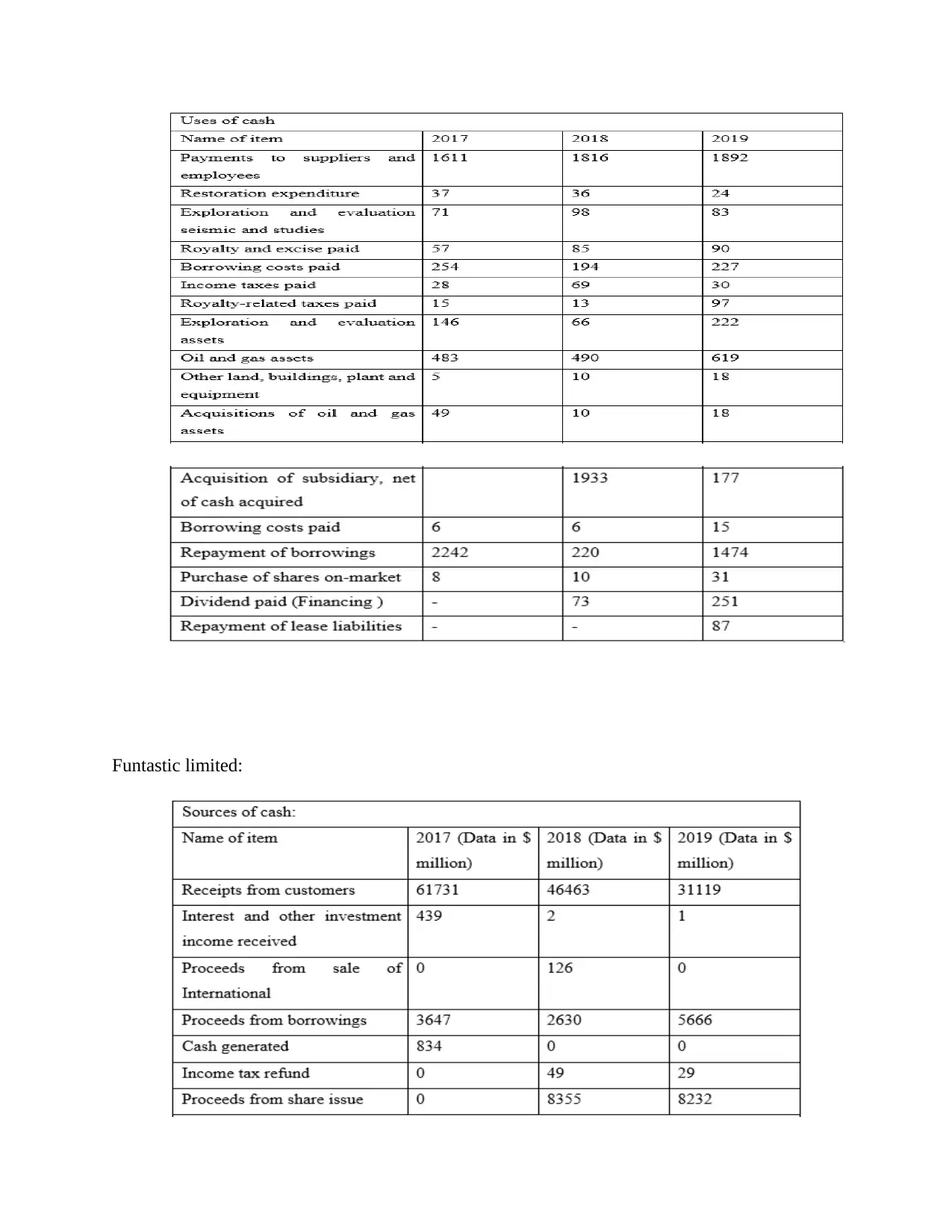

Funtastic limited:

Santos limited-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Funtastic limited:

(b) Trend in cash flow of each firm from operating activity.

2017 (Data in $

million) 2018 (Data in $

million) 2019 (Data in $

million)

15500

16000

16500

17000

17500

18000

18500

16804

18461

17871

Cash fl ow from operati ng

acti vity OF BHP LTD.

2017 (Data in $

million) 2018 (Data in $

million) 2019 (Data in $

million)

15500

16000

16500

17000

17500

18000

18500

16804

18461

17871

Cash fl ow from operati ng

acti vity OF BHP LTD.

Trend- In accordance of above chart this can be find out that cash flow from operating of BHP

limited is fluctuating in all three years. Though, there is cash inflow in these three years and

highest was in year 2018 with a value of $18461 million while lowest was in year 2017. The

rationale behind fluctuation in cash flow from operating activity is increase and decrease in

operating income and expenses during each accounting cycle.

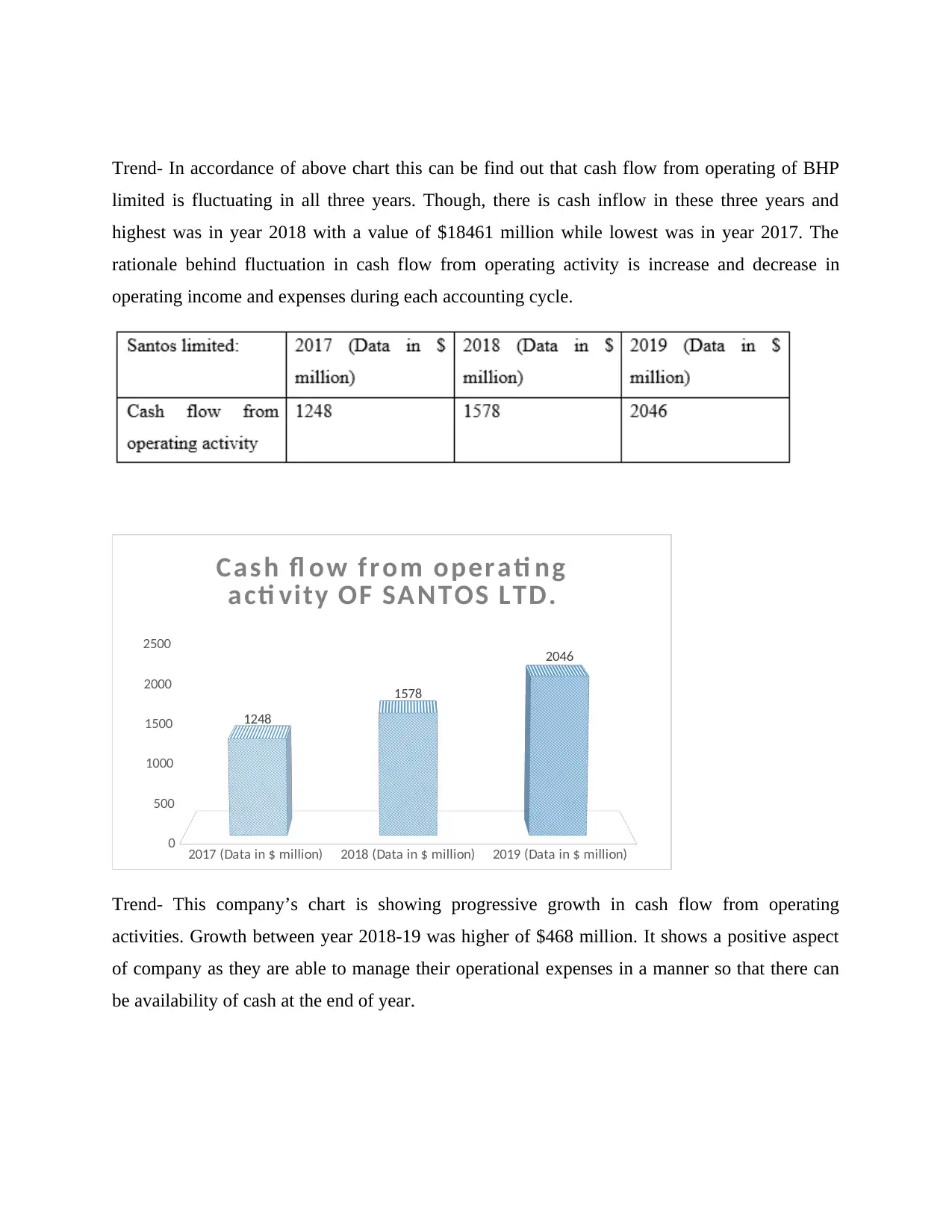

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

500

1000

1500

2000

2500

1248

1578

2046

Cash fl ow from operati ng

acti vity OF SANTOS LTD.

Trend- This company’s chart is showing progressive growth in cash flow from operating

activities. Growth between year 2018-19 was higher of $468 million. It shows a positive aspect

of company as they are able to manage their operational expenses in a manner so that there can

be availability of cash at the end of year.

limited is fluctuating in all three years. Though, there is cash inflow in these three years and

highest was in year 2018 with a value of $18461 million while lowest was in year 2017. The

rationale behind fluctuation in cash flow from operating activity is increase and decrease in

operating income and expenses during each accounting cycle.

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

500

1000

1500

2000

2500

1248

1578

2046

Cash fl ow from operati ng

acti vity OF SANTOS LTD.

Trend- This company’s chart is showing progressive growth in cash flow from operating

activities. Growth between year 2018-19 was higher of $468 million. It shows a positive aspect

of company as they are able to manage their operational expenses in a manner so that there can

be availability of cash at the end of year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 (Data in $

million) 2018 (Data in $

million) 2019 (Data in $

million)

-12000

-10000

-8000

-6000

-4000

-2000

0

Cas h outf low from oper ati ng

acti vity of funtas ti c ltd.

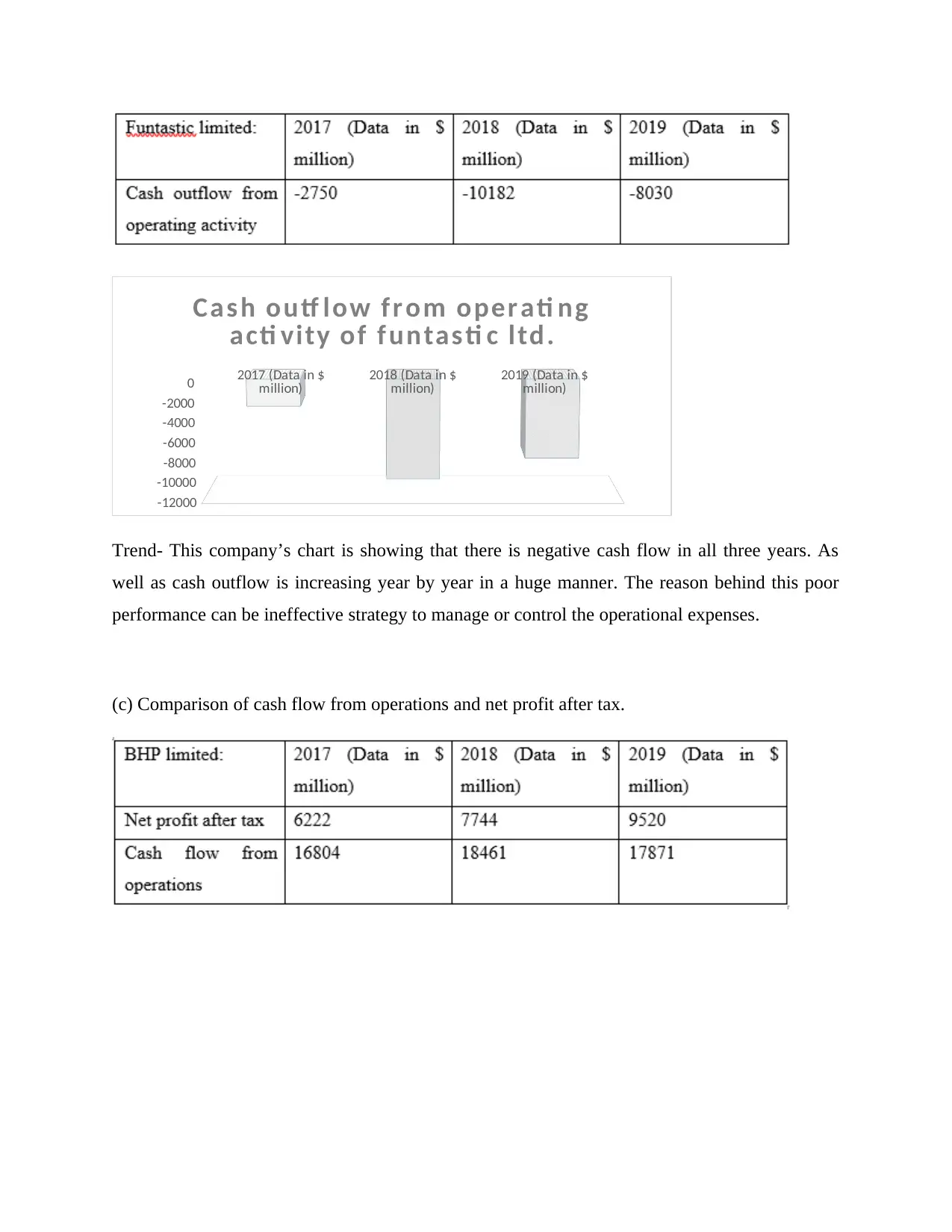

Trend- This company’s chart is showing that there is negative cash flow in all three years. As

well as cash outflow is increasing year by year in a huge manner. The reason behind this poor

performance can be ineffective strategy to manage or control the operational expenses.

(c) Comparison of cash flow from operations and net profit after tax.

million) 2018 (Data in $

million) 2019 (Data in $

million)

-12000

-10000

-8000

-6000

-4000

-2000

0

Cas h outf low from oper ati ng

acti vity of funtas ti c ltd.

Trend- This company’s chart is showing that there is negative cash flow in all three years. As

well as cash outflow is increasing year by year in a huge manner. The reason behind this poor

performance can be ineffective strategy to manage or control the operational expenses.

(c) Comparison of cash flow from operations and net profit after tax.

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

5000

10000

15000

20000

25000

30000

6222 7744 9520

16804

18461 17871

Difference between net profit

after tax and cash flow from

operations

Net profit after tax Cash flow from operations

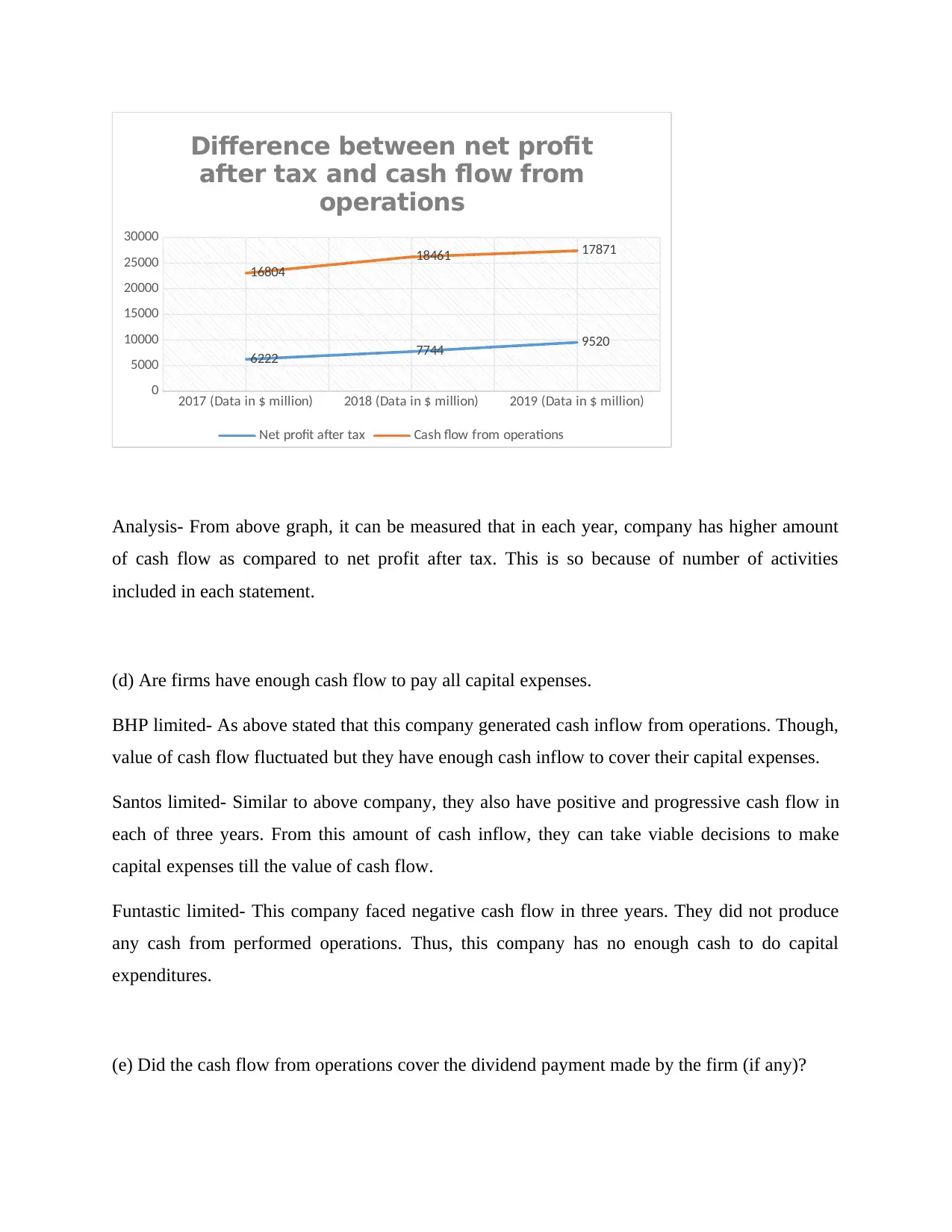

Analysis- From above graph, it can be measured that in each year, company has higher amount

of cash flow as compared to net profit after tax. This is so because of number of activities

included in each statement.

(d) Are firms have enough cash flow to pay all capital expenses.

BHP limited- As above stated that this company generated cash inflow from operations. Though,

value of cash flow fluctuated but they have enough cash inflow to cover their capital expenses.

Santos limited- Similar to above company, they also have positive and progressive cash flow in

each of three years. From this amount of cash inflow, they can take viable decisions to make

capital expenses till the value of cash flow.

Funtastic limited- This company faced negative cash flow in three years. They did not produce

any cash from performed operations. Thus, this company has no enough cash to do capital

expenditures.

(e) Did the cash flow from operations cover the dividend payment made by the firm (if any)?

0

5000

10000

15000

20000

25000

30000

6222 7744 9520

16804

18461 17871

Difference between net profit

after tax and cash flow from

operations

Net profit after tax Cash flow from operations

Analysis- From above graph, it can be measured that in each year, company has higher amount

of cash flow as compared to net profit after tax. This is so because of number of activities

included in each statement.

(d) Are firms have enough cash flow to pay all capital expenses.

BHP limited- As above stated that this company generated cash inflow from operations. Though,

value of cash flow fluctuated but they have enough cash inflow to cover their capital expenses.

Santos limited- Similar to above company, they also have positive and progressive cash flow in

each of three years. From this amount of cash inflow, they can take viable decisions to make

capital expenses till the value of cash flow.

Funtastic limited- This company faced negative cash flow in three years. They did not produce

any cash from performed operations. Thus, this company has no enough cash to do capital

expenditures.

(e) Did the cash flow from operations cover the dividend payment made by the firm (if any)?

2017 (Data in $ million)

2018 (Data in $ million)

2019 (Data in $ million)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2921

5220

11395

16804

18461

17871

BHP LIMITED

Dividend paid Cash flow from operations

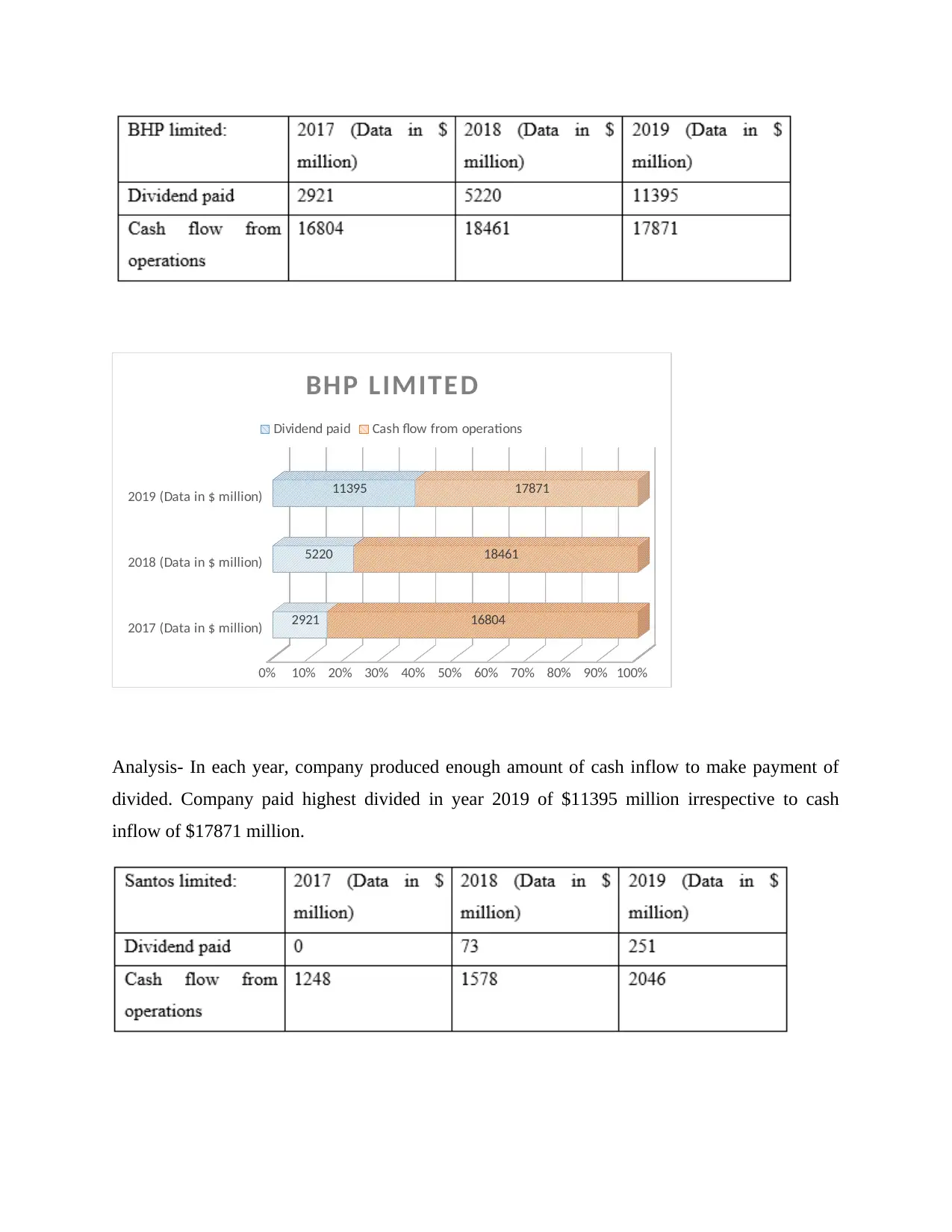

Analysis- In each year, company produced enough amount of cash inflow to make payment of

divided. Company paid highest divided in year 2019 of $11395 million irrespective to cash

inflow of $17871 million.

2018 (Data in $ million)

2019 (Data in $ million)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2921

5220

11395

16804

18461

17871

BHP LIMITED

Dividend paid Cash flow from operations

Analysis- In each year, company produced enough amount of cash inflow to make payment of

divided. Company paid highest divided in year 2019 of $11395 million irrespective to cash

inflow of $17871 million.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2017 (Data in $ million)

2018 (Data in $ million)

2019 (Data in $ million)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

0

73

251

1248

1578

2046

Santos lim ited

Dividend paid Cash flow from operations

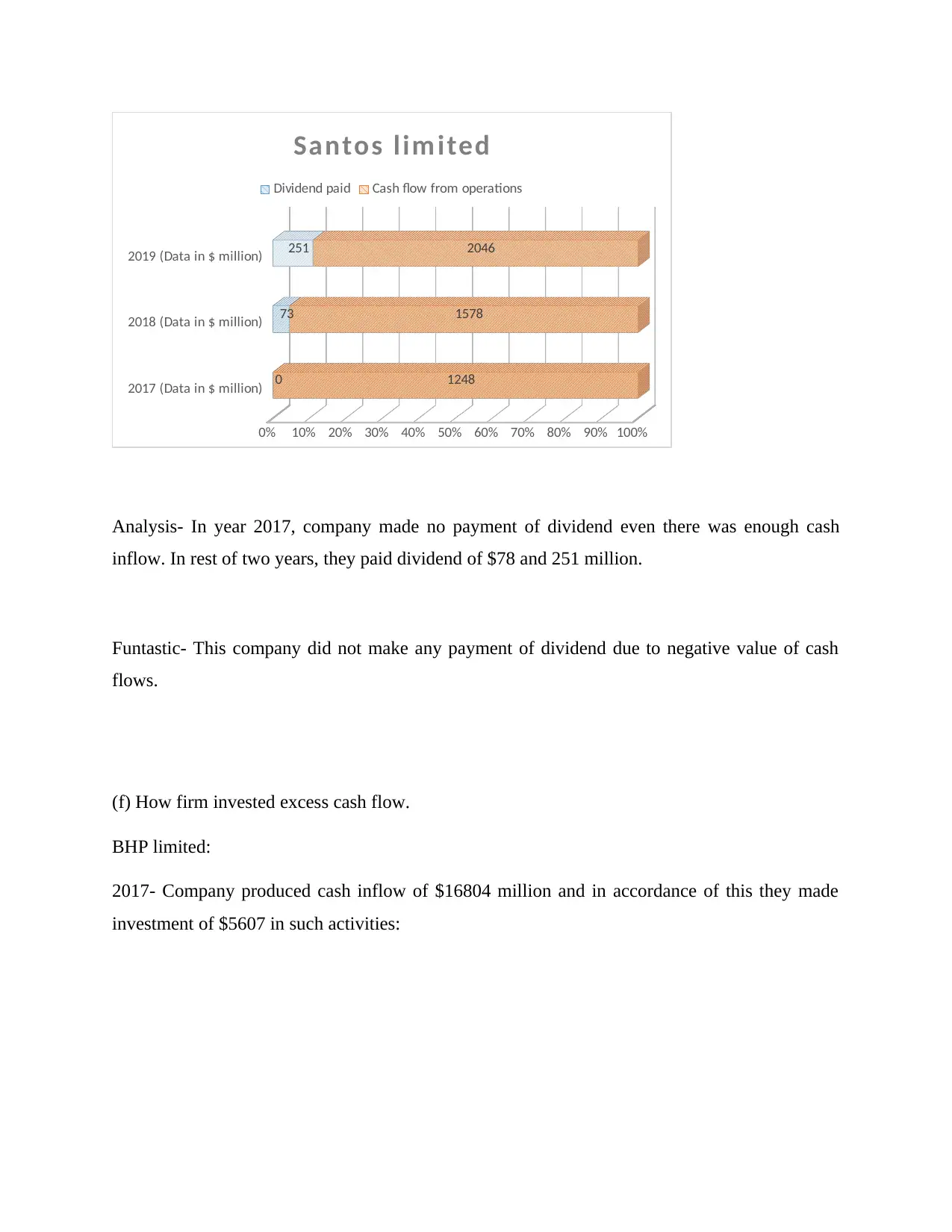

Analysis- In year 2017, company made no payment of dividend even there was enough cash

inflow. In rest of two years, they paid dividend of $78 and 251 million.

Funtastic- This company did not make any payment of dividend due to negative value of cash

flows.

(f) How firm invested excess cash flow.

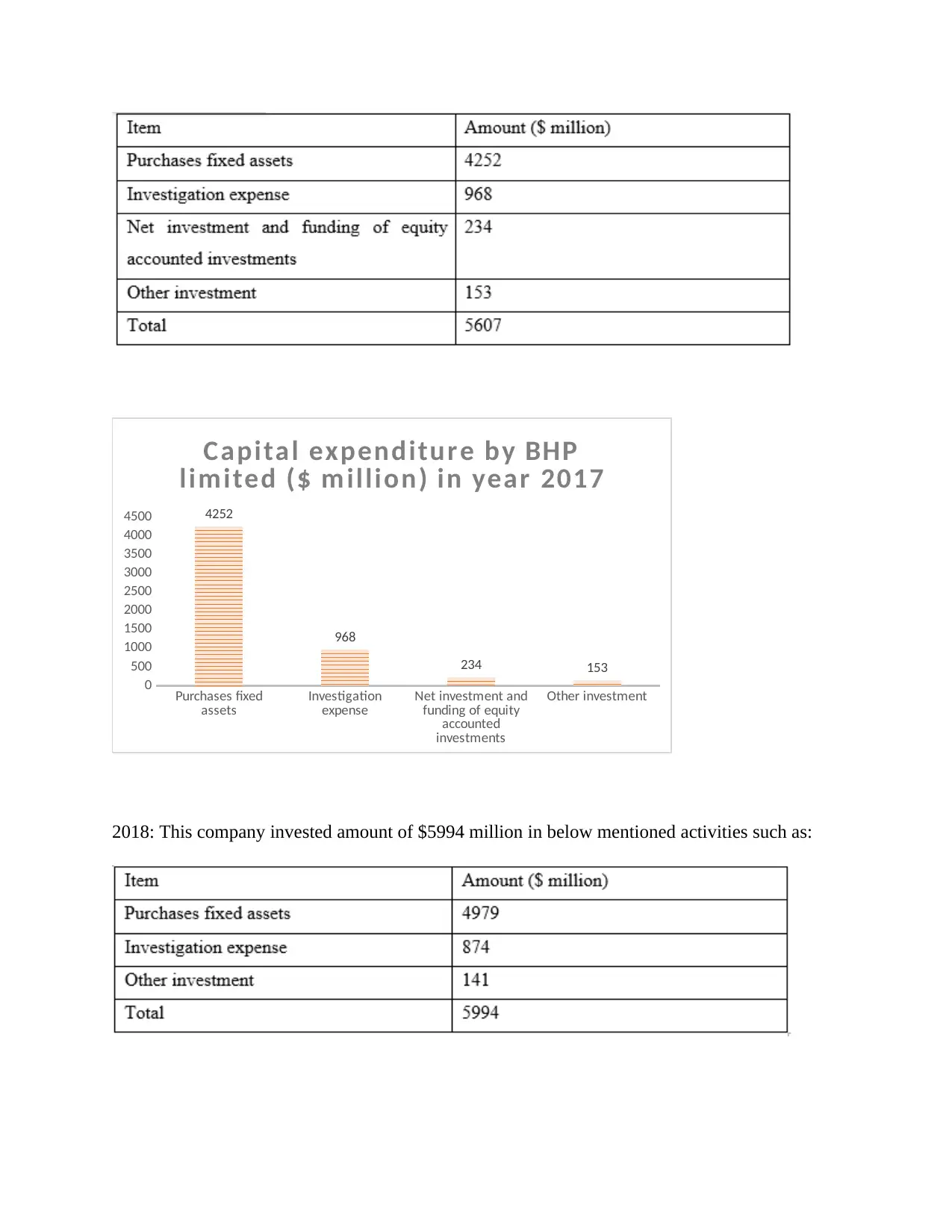

BHP limited:

2017- Company produced cash inflow of $16804 million and in accordance of this they made

investment of $5607 in such activities:

2018 (Data in $ million)

2019 (Data in $ million)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

0

73

251

1248

1578

2046

Santos lim ited

Dividend paid Cash flow from operations

Analysis- In year 2017, company made no payment of dividend even there was enough cash

inflow. In rest of two years, they paid dividend of $78 and 251 million.

Funtastic- This company did not make any payment of dividend due to negative value of cash

flows.

(f) How firm invested excess cash flow.

BHP limited:

2017- Company produced cash inflow of $16804 million and in accordance of this they made

investment of $5607 in such activities:

Purchases fixed

assets Investigation

expense Net investment and

funding of equity

accounted

investments

Other investment

0

500

1000

1500

2000

2500

3000

3500

4000

4500 4252

968

234 153

Capital expenditure by BHP

limited ($ m illion) in year 2017

2018: This company invested amount of $5994 million in below mentioned activities such as:

assets Investigation

expense Net investment and

funding of equity

accounted

investments

Other investment

0

500

1000

1500

2000

2500

3000

3500

4000

4500 4252

968

234 153

Capital expenditure by BHP

limited ($ m illion) in year 2017

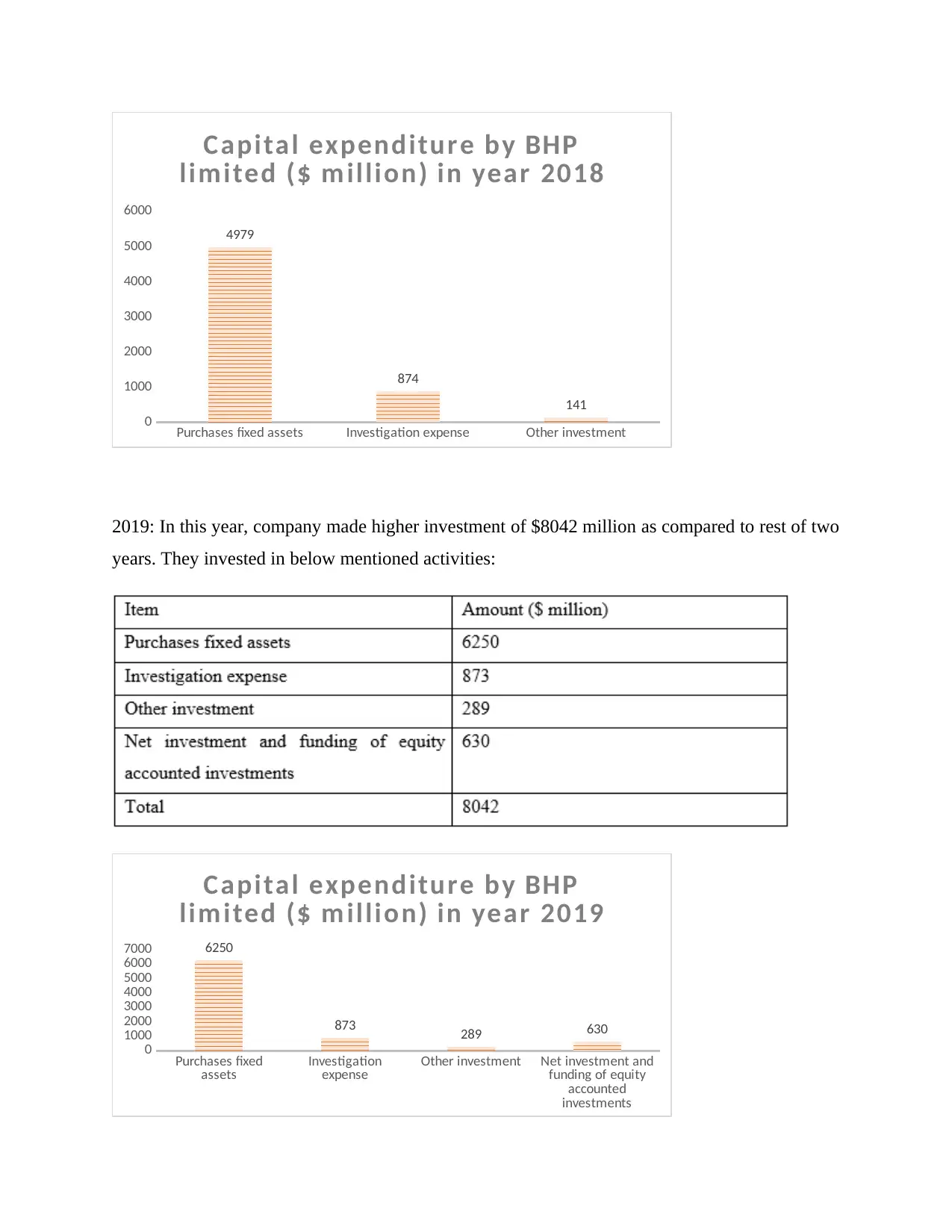

2018: This company invested amount of $5994 million in below mentioned activities such as:

Purchases fixed assets Investigation expense Other investment

0

1000

2000

3000

4000

5000

6000

4979

874

141

Capital expenditure by BHP

limited ($ m illion) in year 2018

2019: In this year, company made higher investment of $8042 million as compared to rest of two

years. They invested in below mentioned activities:

Purchases fixed

assets Investigation

expense Other investment Net investment and

funding of equity

accounted

investments

0

1000

2000

3000

4000

5000

6000

7000 6250

873 289 630

Capital expenditure by BHP

limited ($ m illion) in year 2019

0

1000

2000

3000

4000

5000

6000

4979

874

141

Capital expenditure by BHP

limited ($ m illion) in year 2018

2019: In this year, company made higher investment of $8042 million as compared to rest of two

years. They invested in below mentioned activities:

Purchases fixed

assets Investigation

expense Other investment Net investment and

funding of equity

accounted

investments

0

1000

2000

3000

4000

5000

6000

7000 6250

873 289 630

Capital expenditure by BHP

limited ($ m illion) in year 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

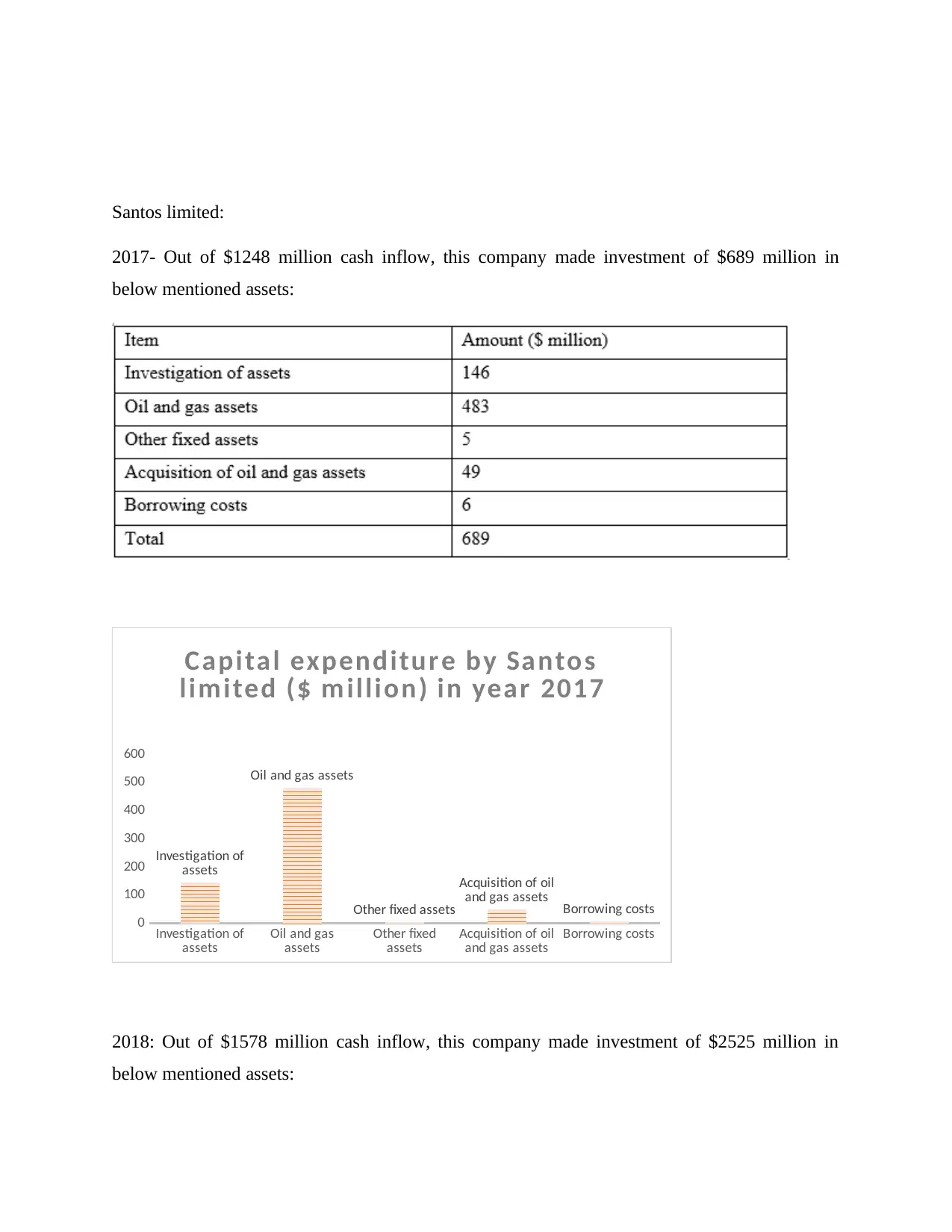

Santos limited:

2017- Out of $1248 million cash inflow, this company made investment of $689 million in

below mentioned assets:

Investigation of

assets Oil and gas

assets Other fixed

assets Acquisition of oil

and gas assets Borrowing costs

0

100

200

300

400

500

600

Investigation of

assets

Oil and gas assets

Other fixed assets

Acquisition of oil

and gas assets Borrowing costs

Capital expenditure by Santos

limited ($ m illion) in year 2017

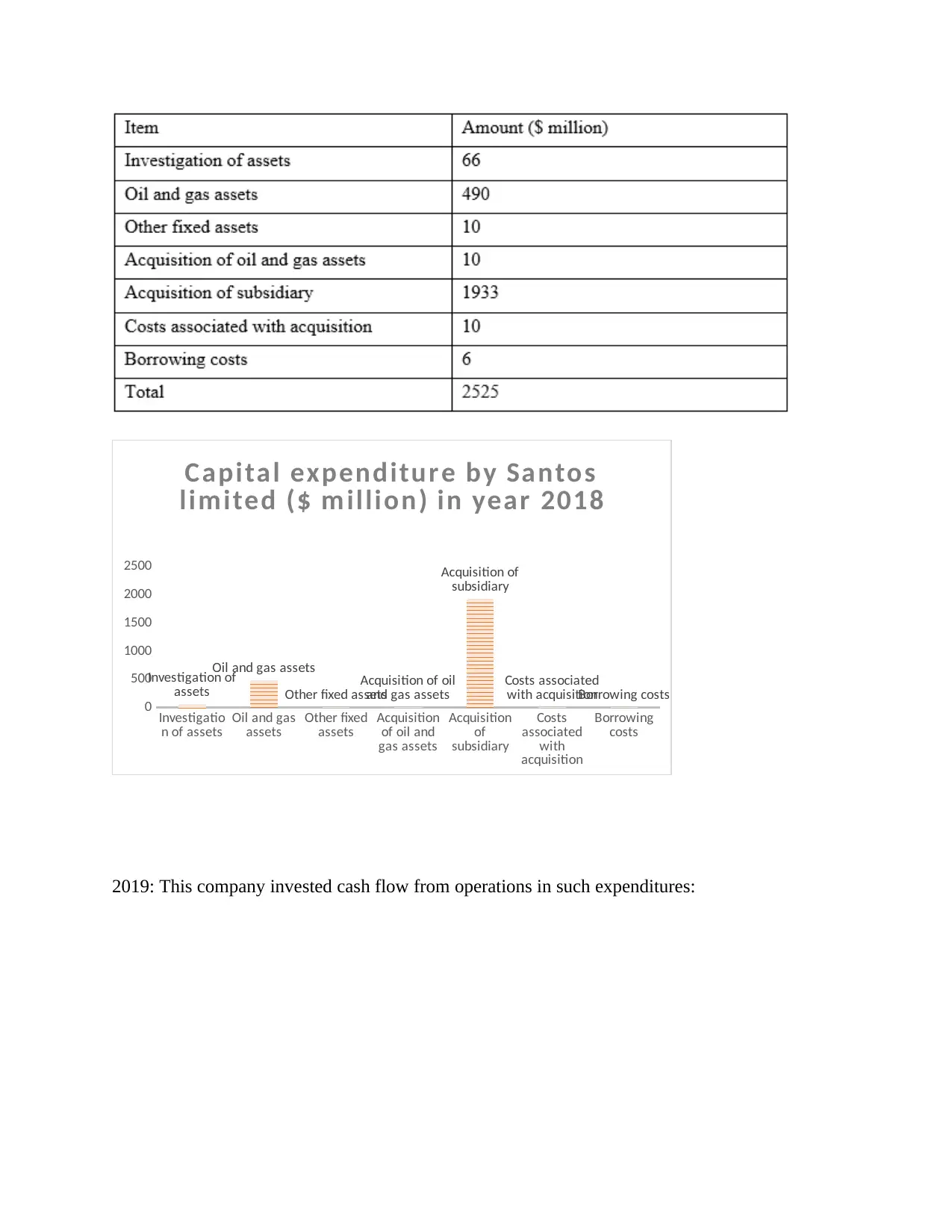

2018: Out of $1578 million cash inflow, this company made investment of $2525 million in

below mentioned assets:

2017- Out of $1248 million cash inflow, this company made investment of $689 million in

below mentioned assets:

Investigation of

assets Oil and gas

assets Other fixed

assets Acquisition of oil

and gas assets Borrowing costs

0

100

200

300

400

500

600

Investigation of

assets

Oil and gas assets

Other fixed assets

Acquisition of oil

and gas assets Borrowing costs

Capital expenditure by Santos

limited ($ m illion) in year 2017

2018: Out of $1578 million cash inflow, this company made investment of $2525 million in

below mentioned assets:

Investigatio

n of assets Oil and gas

assets Other fixed

assets Acquisition

of oil and

gas assets

Acquisition

of

subsidiary

Costs

associated

with

acquisition

Borrowing

costs

0

500

1000

1500

2000

2500

Investigation of

assets

Oil and gas assets

Other fixed assets

Acquisition of oil

and gas assets

Acquisition of

subsidiary

Costs associated

with acquisitionBorrowing costs

Capital expenditure by Santos

limited ($ m illion) in year 2018

2019: This company invested cash flow from operations in such expenditures:

n of assets Oil and gas

assets Other fixed

assets Acquisition

of oil and

gas assets

Acquisition

of

subsidiary

Costs

associated

with

acquisition

Borrowing

costs

0

500

1000

1500

2000

2500

Investigation of

assets

Oil and gas assets

Other fixed assets

Acquisition of oil

and gas assets

Acquisition of

subsidiary

Costs associated

with acquisitionBorrowing costs

Capital expenditure by Santos

limited ($ m illion) in year 2018

2019: This company invested cash flow from operations in such expenditures:

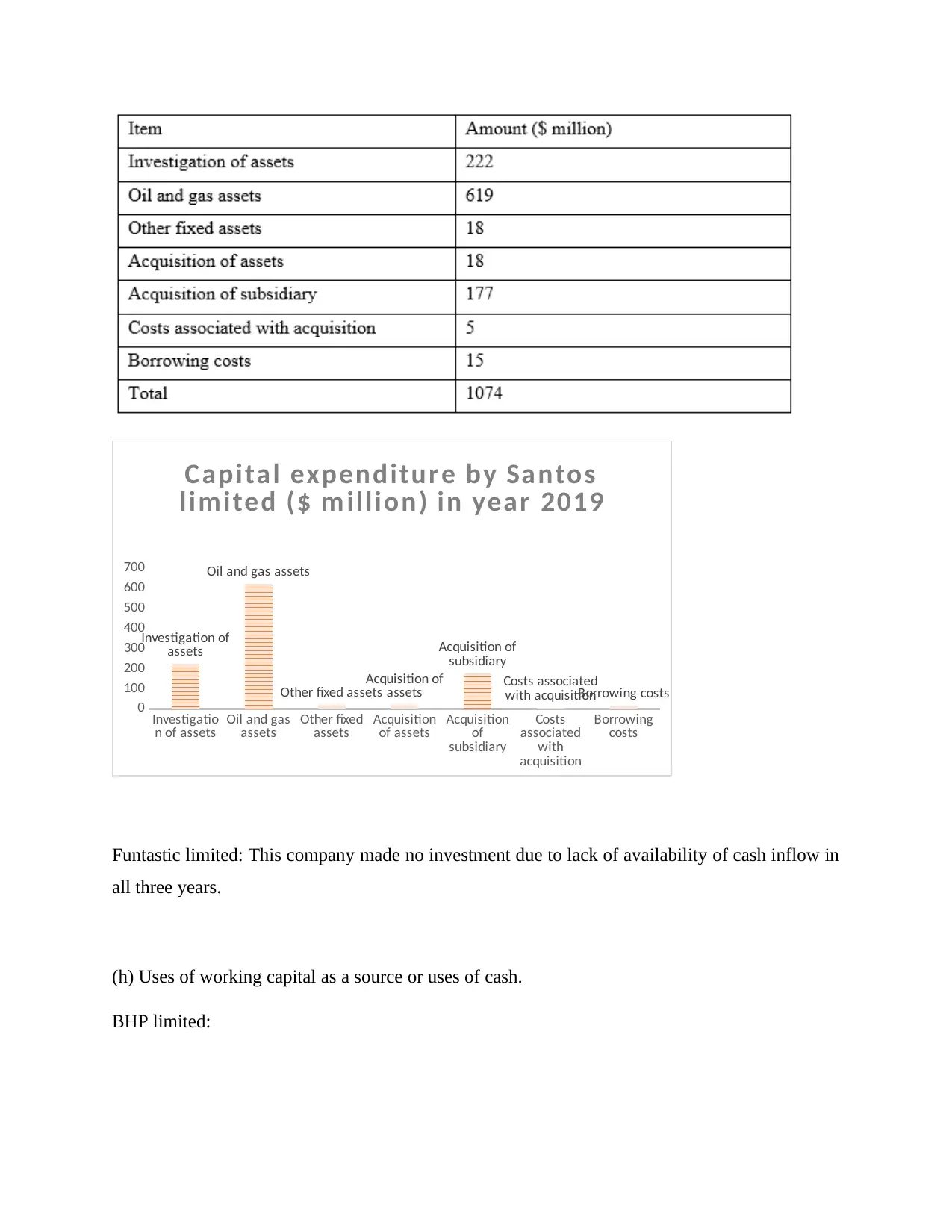

Investigatio

n of assets Oil and gas

assets Other fixed

assets Acquisition

of assets Acquisition

of

subsidiary

Costs

associated

with

acquisition

Borrowing

costs

0

100

200

300

400

500

600

700

Investigation of

assets

Oil and gas assets

Other fixed assets

Acquisition of

assets

Acquisition of

subsidiary

Costs associated

with acquisitionBorrowing costs

Capital expenditure by Santos

limited ($ m illion) in year 2019

Funtastic limited: This company made no investment due to lack of availability of cash inflow in

all three years.

(h) Uses of working capital as a source or uses of cash.

BHP limited:

n of assets Oil and gas

assets Other fixed

assets Acquisition

of assets Acquisition

of

subsidiary

Costs

associated

with

acquisition

Borrowing

costs

0

100

200

300

400

500

600

700

Investigation of

assets

Oil and gas assets

Other fixed assets

Acquisition of

assets

Acquisition of

subsidiary

Costs associated

with acquisitionBorrowing costs

Capital expenditure by Santos

limited ($ m illion) in year 2019

Funtastic limited: This company made no investment due to lack of availability of cash inflow in

all three years.

(h) Uses of working capital as a source or uses of cash.

BHP limited:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

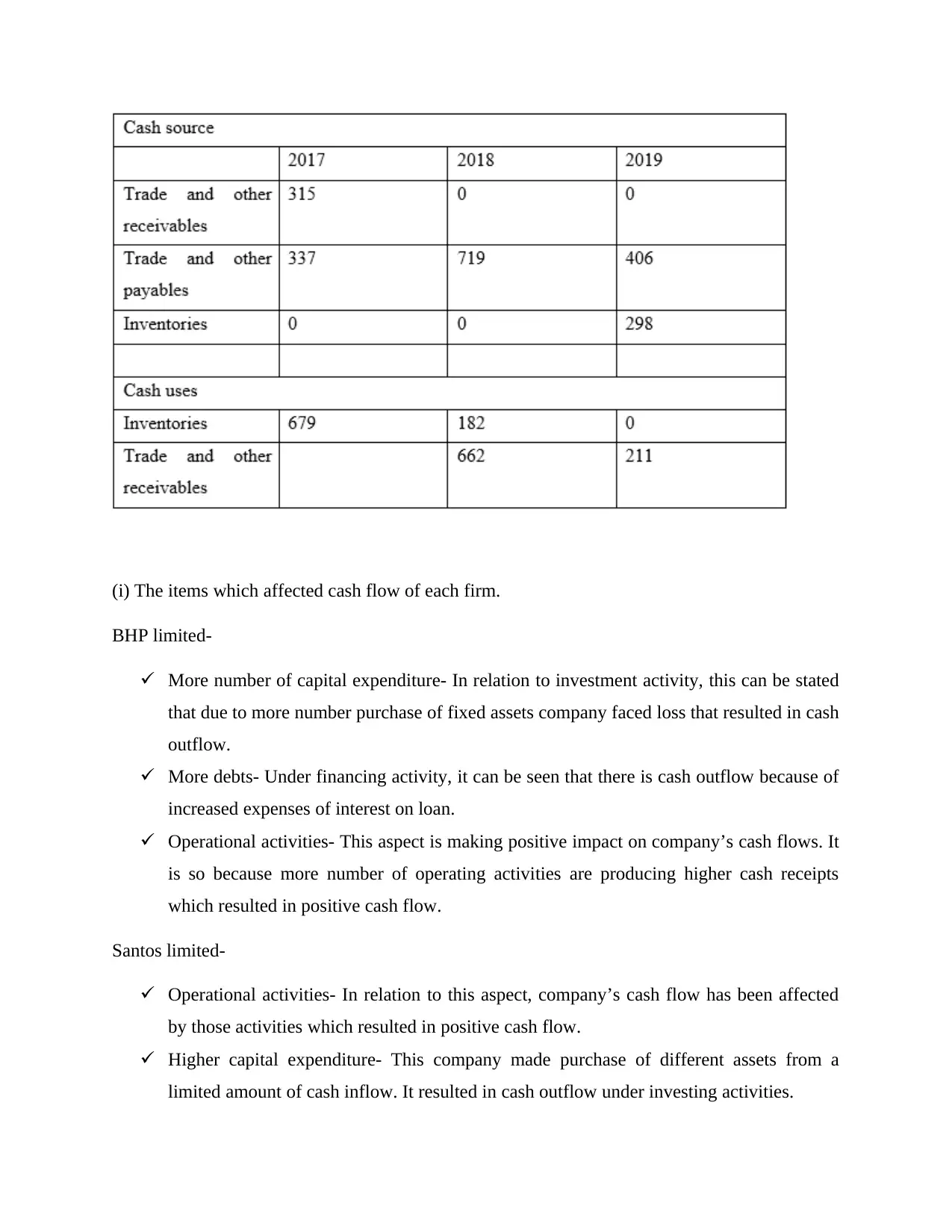

(i) The items which affected cash flow of each firm.

BHP limited-

More number of capital expenditure- In relation to investment activity, this can be stated

that due to more number purchase of fixed assets company faced loss that resulted in cash

outflow.

More debts- Under financing activity, it can be seen that there is cash outflow because of

increased expenses of interest on loan.

Operational activities- This aspect is making positive impact on company’s cash flows. It

is so because more number of operating activities are producing higher cash receipts

which resulted in positive cash flow.

Santos limited-

Operational activities- In relation to this aspect, company’s cash flow has been affected

by those activities which resulted in positive cash flow.

Higher capital expenditure- This company made purchase of different assets from a

limited amount of cash inflow. It resulted in cash outflow under investing activities.

BHP limited-

More number of capital expenditure- In relation to investment activity, this can be stated

that due to more number purchase of fixed assets company faced loss that resulted in cash

outflow.

More debts- Under financing activity, it can be seen that there is cash outflow because of

increased expenses of interest on loan.

Operational activities- This aspect is making positive impact on company’s cash flows. It

is so because more number of operating activities are producing higher cash receipts

which resulted in positive cash flow.

Santos limited-

Operational activities- In relation to this aspect, company’s cash flow has been affected

by those activities which resulted in positive cash flow.

Higher capital expenditure- This company made purchase of different assets from a

limited amount of cash inflow. It resulted in cash outflow under investing activities.

Higher payment of debts- In each year, company made payment of higher interest on loan

which became cause of cash outflow.

Funtastic limited-

Uncontrolled operational expenses- This company affected by those activities which

resulted in higher operating expenses.

Financing activities- Company’s cash flow from financing activities was affected in a

positive manner due to more number of gain over given loan.

Capital expenditures- Company’s cash flow from investing activities affected negatively

because of improper allocation of fund.

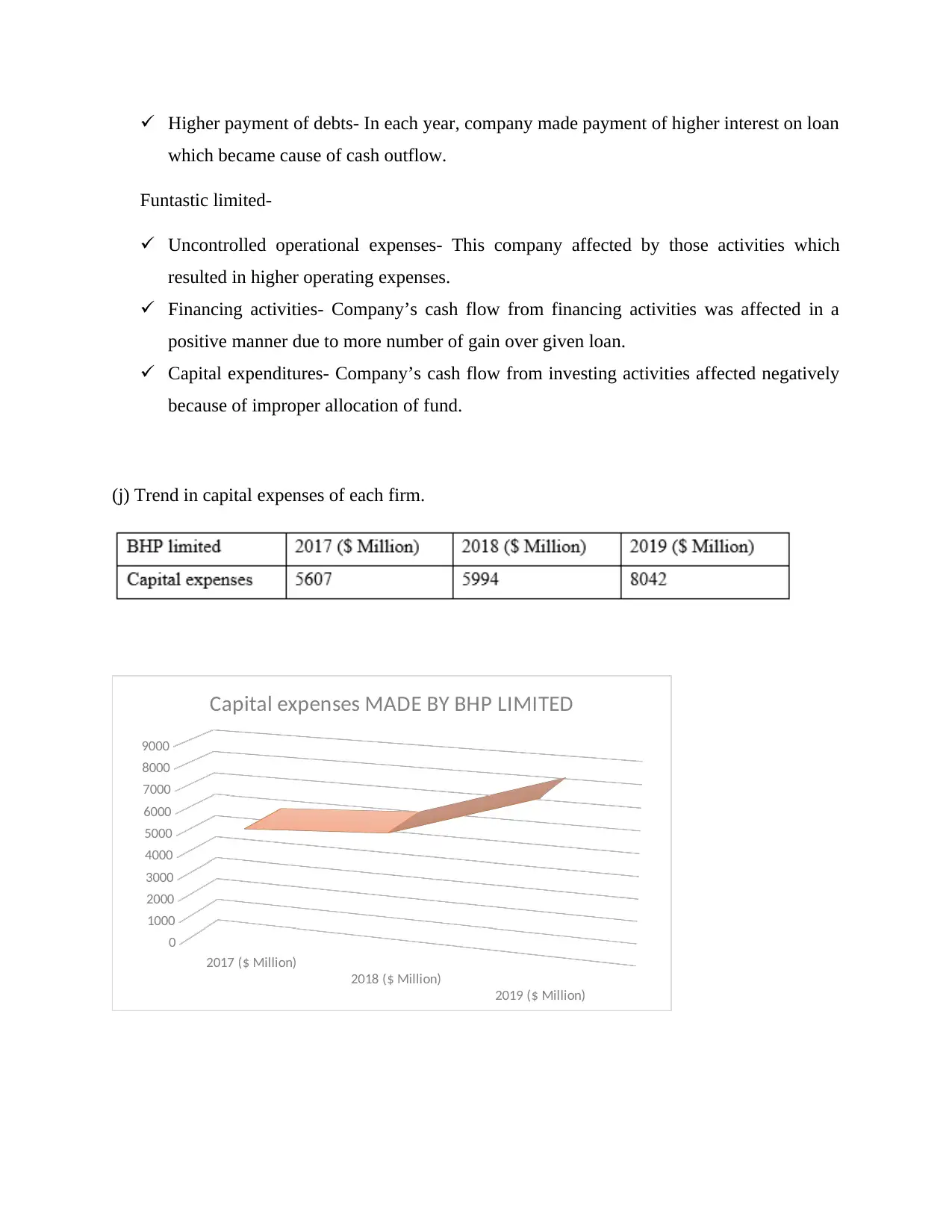

(j) Trend in capital expenses of each firm.

2017 ($ Million)

2018 ($ Million)

2019 ($ Million)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Capital expenses MADE BY BHP LIMITED

which became cause of cash outflow.

Funtastic limited-

Uncontrolled operational expenses- This company affected by those activities which

resulted in higher operating expenses.

Financing activities- Company’s cash flow from financing activities was affected in a

positive manner due to more number of gain over given loan.

Capital expenditures- Company’s cash flow from investing activities affected negatively

because of improper allocation of fund.

(j) Trend in capital expenses of each firm.

2017 ($ Million)

2018 ($ Million)

2019 ($ Million)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Capital expenses MADE BY BHP LIMITED

Trend- This graph is indicating that company’s capital expenditures increased year by year. It is

so because of positive cash flow from operations.

2017 ($ Million)

2018 ($ Million)

2019 ($ Million)

0

500

1000

1500

2000

2500

3000

689

2525

1074

Capital expenses made by santos limited

Trend- This company fluctuated their expenses in accordance of their need. After year 2018,

there was huge fell down in company’s expenses.

2017 ($ Million) 2018 ($ Million) 2019 ($ Million)

0

500

1000

1500 1428

426

152

Capital expenses made by funtastic limited

so because of positive cash flow from operations.

2017 ($ Million)

2018 ($ Million)

2019 ($ Million)

0

500

1000

1500

2000

2500

3000

689

2525

1074

Capital expenses made by santos limited

Trend- This company fluctuated their expenses in accordance of their need. After year 2018,

there was huge fell down in company’s expenses.

2017 ($ Million) 2018 ($ Million) 2019 ($ Million)

0

500

1000

1500 1428

426

152

Capital expenses made by funtastic limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trend- This company dropped their capital expenses year by year. It is so because of negative

cash flow from operations.

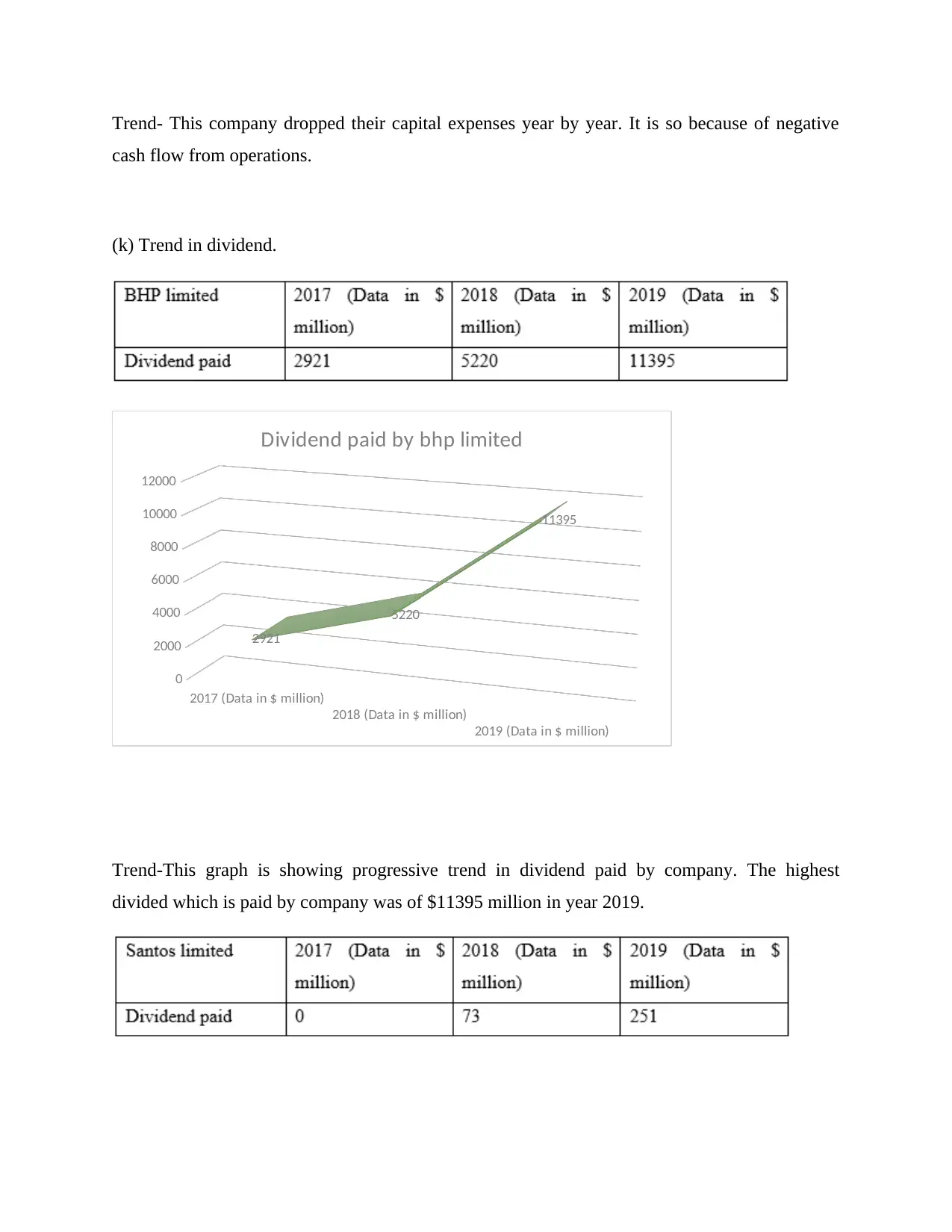

(k) Trend in dividend.

2017 (Data in $ million)

2018 (Data in $ million)

2019 (Data in $ million)

0

2000

4000

6000

8000

10000

12000

2921

5220

11395

Dividend paid by bhp limited

Trend-This graph is showing progressive trend in dividend paid by company. The highest

divided which is paid by company was of $11395 million in year 2019.

cash flow from operations.

(k) Trend in dividend.

2017 (Data in $ million)

2018 (Data in $ million)

2019 (Data in $ million)

0

2000

4000

6000

8000

10000

12000

2921

5220

11395

Dividend paid by bhp limited

Trend-This graph is showing progressive trend in dividend paid by company. The highest

divided which is paid by company was of $11395 million in year 2019.

2017 (Data in $ million)

2018 (Data in $ million)

2019 (Data in $ million)

0

50

100

150

200

250

300

0

73

251

Dividend paid by santos limited

Trend- Except year 2017, company paid dividend in a progressive manner because of more cash

inflows in these two years.

Trend in net borrowings.

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

1000

2000

3000

4000

5000

6000

7000

8000 7156

4406

2764

Net borrowings of bhp limited

Trend- This graph is showing fell down in net borrowings year by year. It shows that company’s

dependency has been reduced over debts.

2018 (Data in $ million)

2019 (Data in $ million)

0

50

100

150

200

250

300

0

73

251

Dividend paid by santos limited

Trend- Except year 2017, company paid dividend in a progressive manner because of more cash

inflows in these two years.

Trend in net borrowings.

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

1000

2000

3000

4000

5000

6000

7000

8000 7156

4406

2764

Net borrowings of bhp limited

Trend- This graph is showing fell down in net borrowings year by year. It shows that company’s

dependency has been reduced over debts.

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

200

400

600

800

1000

1200

1400

783

1193

592

Net borr owings of santos

limited

Trend-This company’s chart is showing fluctuation in net borrowings as per their need. The

highest net borrowing was in year 2018 of $1193 million.

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

1000

2000

3000

4000

5000

6000

3647

2630

5666

Net borr owings by funtas ti c

limited

0

200

400

600

800

1000

1200

1400

783

1193

592

Net borr owings of santos

limited

Trend-This company’s chart is showing fluctuation in net borrowings as per their need. The

highest net borrowing was in year 2018 of $1193 million.

2017 (Data in $ million) 2018 (Data in $ million) 2019 (Data in $ million)

0

1000

2000

3000

4000

5000

6000

3647

2630

5666

Net borr owings by funtas ti c

limited

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Trend- In last year 2019, company increased their borrowings with a value of $5666 million. It

shows the dependency of loan of this company.

(l) Trend in working capital accounts.

Trend: This table is showing that company’s working capital is higher in each year which shows

that they have enough current assets in order to make payment of current liabilities. In each year,

company’s working capital is increasing which indicates a positive trend in growth of liquidity.

2. Financial strength of each company.

In accordance of above done analysis regards to the cash condition of each business, it can be

observed that each company has some strengths and limitations. It relies on firms how they work

with vulnerability and leverage their assets effectively. Below the strengths of three companies

listed that is addressed in this way:

BHP limited-

The key positive point of this organization is that it has created massive sums of cash

inflows from business operations for all three years. This was made possible by the

efficient control of gross revenue and expenditures under each operation.

Excessive capital inflows from running activities is used by the company in an

appropriate manner to buy various forms of fixed assets.

Along with this corporation's emphasis on borrowing is too narrow which states the

productivity of funds.

Santos limited-

shows the dependency of loan of this company.

(l) Trend in working capital accounts.

Trend: This table is showing that company’s working capital is higher in each year which shows

that they have enough current assets in order to make payment of current liabilities. In each year,

company’s working capital is increasing which indicates a positive trend in growth of liquidity.

2. Financial strength of each company.

In accordance of above done analysis regards to the cash condition of each business, it can be

observed that each company has some strengths and limitations. It relies on firms how they work

with vulnerability and leverage their assets effectively. Below the strengths of three companies

listed that is addressed in this way:

BHP limited-

The key positive point of this organization is that it has created massive sums of cash

inflows from business operations for all three years. This was made possible by the

efficient control of gross revenue and expenditures under each operation.

Excessive capital inflows from running activities is used by the company in an

appropriate manner to buy various forms of fixed assets.

Along with this corporation's emphasis on borrowing is too narrow which states the

productivity of funds.

Santos limited-

The strength of this business is that the cash flow from different operations has grown in

a comprehensive way. It indicates that the organization has increased its financial

efficiency.

The corporation paid the dividends only because there was a substantial volume of cash

inflow, and did not bear any burden to fund the dividend.

Along with in 2018, the organization generated net cash inflows from all three

operations, demonstrating that they offset cash outflows from borrowing and acquisition

activities at the end of the year.

Funtastic limited:

In 2018, the organization created cash inflows from its overall operations. This indicates

that they were similarly concentrated on all three activities.

The business created positive cash inflows from financing activities that demonstrate that

they handled their debts and shares properly in all three years.

This organization has wisely acquired the investments by using a limited portion of the

loan without suffering any losses.

3. Selection of a company for lending purpose.

If I have an option to pick up one business for the purpose of lending, then I would prefer

Funtastic Limited. The reasoning for this is that, it is the only one whose cash flow from funding

operations is optimistic. It means that this organization will be able to recover the principal sum

in a successful way for given loan.

CONCLUSION

From above study-report this has been inferred that significance of cash Flow Statement

in company is that this ascertain cash inflows or outflows for a specified time-period. This

information of the liquidity condition of the firm will not only allow the business or investors to

intend for the shorter or longer term, however can also allow to analyze the appropriate amount

of cash required in the business. Cash flow as well as income statement is regarded to be

beneficial and important tool for management of the corporation for the purposes of shorter-term

a comprehensive way. It indicates that the organization has increased its financial

efficiency.

The corporation paid the dividends only because there was a substantial volume of cash

inflow, and did not bear any burden to fund the dividend.

Along with in 2018, the organization generated net cash inflows from all three

operations, demonstrating that they offset cash outflows from borrowing and acquisition

activities at the end of the year.

Funtastic limited:

In 2018, the organization created cash inflows from its overall operations. This indicates

that they were similarly concentrated on all three activities.

The business created positive cash inflows from financing activities that demonstrate that

they handled their debts and shares properly in all three years.

This organization has wisely acquired the investments by using a limited portion of the

loan without suffering any losses.

3. Selection of a company for lending purpose.

If I have an option to pick up one business for the purpose of lending, then I would prefer

Funtastic Limited. The reasoning for this is that, it is the only one whose cash flow from funding

operations is optimistic. It means that this organization will be able to recover the principal sum

in a successful way for given loan.

CONCLUSION

From above study-report this has been inferred that significance of cash Flow Statement

in company is that this ascertain cash inflows or outflows for a specified time-period. This

information of the liquidity condition of the firm will not only allow the business or investors to

intend for the shorter or longer term, however can also allow to analyze the appropriate amount

of cash required in the business. Cash flow as well as income statement is regarded to be

beneficial and important tool for management of the corporation for the purposes of shorter-term

planning, together with control of cash-fund. In order to fulfil the various obligations, each

business entity must maintain an adequate quantity of liquid cash reserves so that,

whenever requirement arises, company can pay same amount. Therefore, cash flow statement

allows the financial planner to estimate cash flows in near term by using previous cash

inflows and outflows info.

business entity must maintain an adequate quantity of liquid cash reserves so that,

whenever requirement arises, company can pay same amount. Therefore, cash flow statement

allows the financial planner to estimate cash flows in near term by using previous cash

inflows and outflows info.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal:

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2),

pp.113-122.

Liu, Y., Li, X., Zeng, H. and An, Y., 2017. Political connections, auditor choice and corporate

accounting transparency: evidence from private sector firms in China. Accounting &

Finance, 57(4), pp.1071-1099.

Hoang, T.C. and Joseph, D.M., 2019. The effect of new corporate accounting regime on earnings

management: Evidence from Vietnam. Journal of International Studies, 12(1).

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Ioannidis, J.P., 2019. The importance of predefined rules and prespecified statistical analyses: do

not abandon significance. Jama, 321(21), pp.2067-2068.

Harring, N., Jagers, S.C. and Matti, S., 2019. The significance of political culture, economic

context and instrument type for climate policy support: a cross-national study. Climate

policy, 19(5), pp.636-650.

Online:

Annual report of BHP limited for year 2017. [online] available through:<

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf>

Annual report of BHP limited for year 2018. [online] available through:<

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf>

Annual report of BHP limited for year 2019. [online] available through:<

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf>

Annual report of Santos limited for year 2017. [online] available through:<

https://www.santos.com/wp-content/uploads/2020/02/2017-annual-report.pdf>

Annual report of Santos limited for year 2018. [online] available through:<

https://www.santos.com/wp-content/uploads/2020/02/2018-annual-report.pdf>

Annual report of Santos limited for year 2019. [online] available through:<

https://www.santos.com/wp-content/uploads/2020/02/2019-annual-report.pdf>

Books and journal:

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2),

pp.113-122.

Liu, Y., Li, X., Zeng, H. and An, Y., 2017. Political connections, auditor choice and corporate

accounting transparency: evidence from private sector firms in China. Accounting &

Finance, 57(4), pp.1071-1099.

Hoang, T.C. and Joseph, D.M., 2019. The effect of new corporate accounting regime on earnings

management: Evidence from Vietnam. Journal of International Studies, 12(1).

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Ioannidis, J.P., 2019. The importance of predefined rules and prespecified statistical analyses: do

not abandon significance. Jama, 321(21), pp.2067-2068.

Harring, N., Jagers, S.C. and Matti, S., 2019. The significance of political culture, economic

context and instrument type for climate policy support: a cross-national study. Climate

policy, 19(5), pp.636-650.

Online:

Annual report of BHP limited for year 2017. [online] available through:<

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf>

Annual report of BHP limited for year 2018. [online] available through:<

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf>

Annual report of BHP limited for year 2019. [online] available through:<

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf>

Annual report of Santos limited for year 2017. [online] available through:<

https://www.santos.com/wp-content/uploads/2020/02/2017-annual-report.pdf>

Annual report of Santos limited for year 2018. [online] available through:<

https://www.santos.com/wp-content/uploads/2020/02/2018-annual-report.pdf>

Annual report of Santos limited for year 2019. [online] available through:<

https://www.santos.com/wp-content/uploads/2020/02/2019-annual-report.pdf>

Annual report of Funtastic limited for year 2017. [online] available through:<

https://www.annualreports.com/HostedData/AnnualReportArchive/f/ASX_FUN_2017.pd

f>

Annual report of Funtastic limited for year 2018 & 2019. [online] available through:<

https://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_FUN_2019.pdf>

https://www.annualreports.com/HostedData/AnnualReportArchive/f/ASX_FUN_2017.pd

f>

Annual report of Funtastic limited for year 2018 & 2019. [online] available through:<

https://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_FUN_2019.pdf>

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.