Corporate Accounting Analysis of Cash Flow and Tax Implications

VerifiedAdded on 2021/06/14

|13

|3031

|72

Report

AI Summary

This report provides a detailed analysis of a corporate accounting assignment focused on Gazal Corporation Limited's financial statements. It begins with an analysis of the cash flow statement, segmenting cash flows into operating, investing, and financing activities, and highlights significant changes between 2016 and 2017. The report then compares these cash flow categories, noting trends in net cash flows. It explores the components of the comprehensive income statement, including reclassified and non-reclassified items. Further, it explains key concepts like revaluation of land and buildings, and exchange differences. The report also contrasts the profit and loss statement with the statement of comprehensive income. It examines income tax expense, corporate tax rates, and the relationship between accounting income and taxable profit. The balance sheet's deferred tax liabilities are discussed, including their recognition and measurement. The report also addresses income tax payable, its difference from income tax expense, and the treatment of tax in the financial statements, including the formation of a tax consolidated group and the allocation of tax liabilities among subsidiaries. Finally, the report concludes with a discussion of the treatment of hedging transactions and the implications of changes in legislation.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the Student

Name of the University

Author Note

Corporate accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Table of Contents

Requirement i)............................................................................................................................2

Requirement ii)...........................................................................................................................3

Requirement iii).........................................................................................................................3

Requirement iv)..........................................................................................................................4

Requirement v)...........................................................................................................................5

Requirement vi)..........................................................................................................................5

Requirement vii).........................................................................................................................5

Requirement viii).......................................................................................................................6

Requirement ix)..........................................................................................................................6

Requirement x)...........................................................................................................................7

Requirement xi)..........................................................................................................................8

References list:.........................................................................................................................10

Appendix:.................................................................................................................................12

Table of Contents

Requirement i)............................................................................................................................2

Requirement ii)...........................................................................................................................3

Requirement iii).........................................................................................................................3

Requirement iv)..........................................................................................................................4

Requirement v)...........................................................................................................................5

Requirement vi)..........................................................................................................................5

Requirement vii).........................................................................................................................5

Requirement viii).......................................................................................................................6

Requirement ix)..........................................................................................................................6

Requirement x)...........................................................................................................................7

Requirement xi)..........................................................................................................................8

References list:.........................................................................................................................10

Appendix:.................................................................................................................................12

CORPORATE ACCOUNTING

Requirement i)

Analysis of cash flow statement:

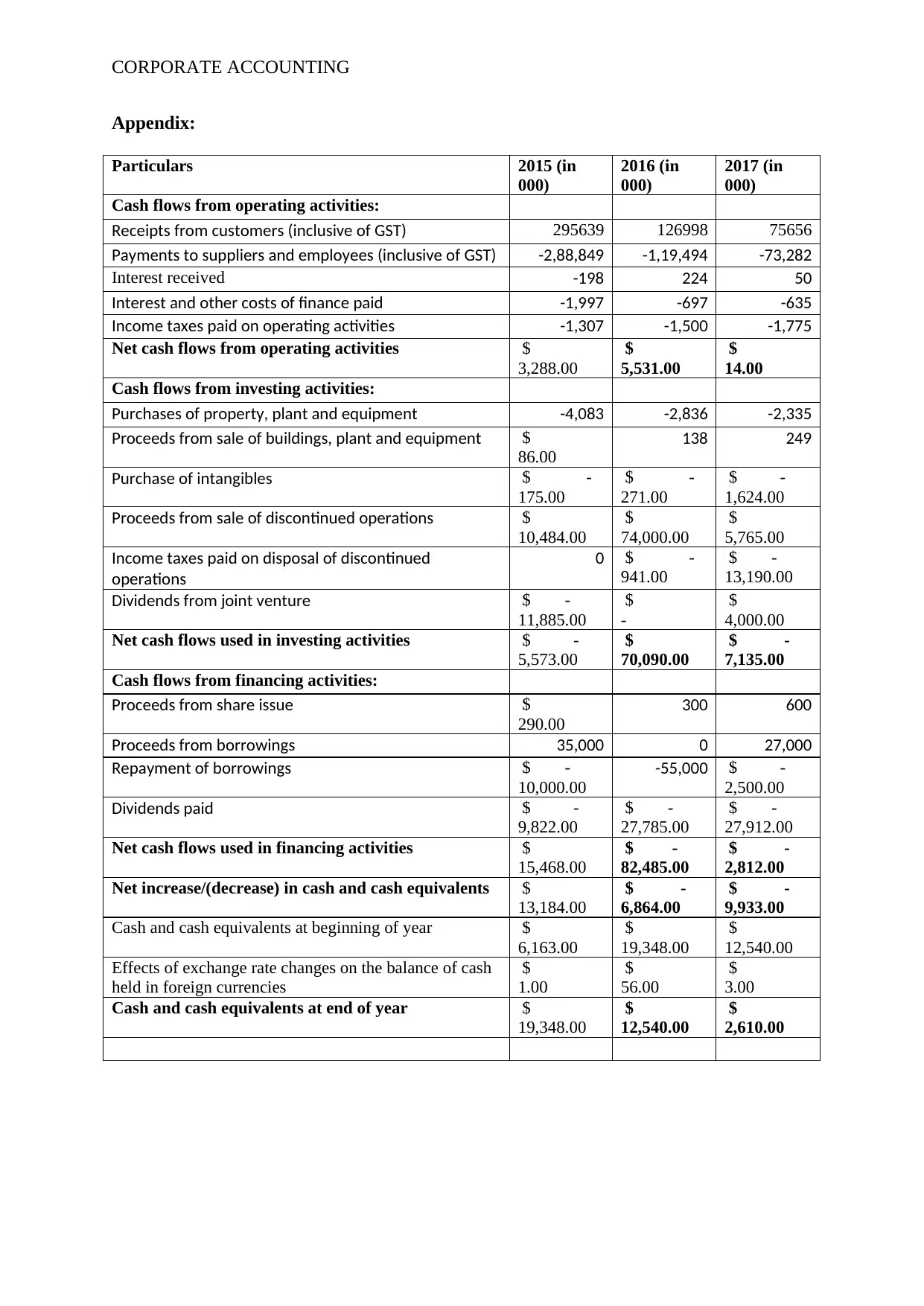

The cash flow of Gazal Corporation limited has been segmented into three parts that

is cash flow from operating activities, cash flow from financing activities sand cash flow

from investing activities. Items reported under cash flow from operating activities include

payment from customers, payment to suppliers, interest received, income tax paid and

interest and other cost of finances paid. It can be seen that net cash flow from operating

activities has reduced significantly from $ 5531000 in year 2016 compared to $ 14000 in year

2017. The reason attributable to this fall is that payment from customers has reduced

drastically and there has been increment in income tax paid.

Items under cash flow from financing activities include proceed from share issue,

proceed from borrowing, dividend paid and repayment from borrowing. The net cash used in

financing activities reduced from $ 82485000 in year 2016 as against 2812 in year 2017. This

is so because there has been reduction in amount that is repaid on borrowing in the current

year.

Items reported under cash flow from investing activities include purchase of property,

equipment and plant, purchase of intangibles, proceeds from sale of building, equipment and

plant, proceeds from sale of discontinued operations, income tax paid non discontinued

operations and dividend from joint ventures. Net cash flow generated from investing

activities in year 2016 stood at $ 70090000 to ($7135000) in year 2017 indicating net cash

used in investing activities. Total amount of cash and cash equivalent in year 2017 is

recorded at $ 2610 compared to $ 12540 in year 2016 depicting a considerable decline.

Requirement i)

Analysis of cash flow statement:

The cash flow of Gazal Corporation limited has been segmented into three parts that

is cash flow from operating activities, cash flow from financing activities sand cash flow

from investing activities. Items reported under cash flow from operating activities include

payment from customers, payment to suppliers, interest received, income tax paid and

interest and other cost of finances paid. It can be seen that net cash flow from operating

activities has reduced significantly from $ 5531000 in year 2016 compared to $ 14000 in year

2017. The reason attributable to this fall is that payment from customers has reduced

drastically and there has been increment in income tax paid.

Items under cash flow from financing activities include proceed from share issue,

proceed from borrowing, dividend paid and repayment from borrowing. The net cash used in

financing activities reduced from $ 82485000 in year 2016 as against 2812 in year 2017. This

is so because there has been reduction in amount that is repaid on borrowing in the current

year.

Items reported under cash flow from investing activities include purchase of property,

equipment and plant, purchase of intangibles, proceeds from sale of building, equipment and

plant, proceeds from sale of discontinued operations, income tax paid non discontinued

operations and dividend from joint ventures. Net cash flow generated from investing

activities in year 2016 stood at $ 70090000 to ($7135000) in year 2017 indicating net cash

used in investing activities. Total amount of cash and cash equivalent in year 2017 is

recorded at $ 2610 compared to $ 12540 in year 2016 depicting a considerable decline.

You're viewing a preview

Unlock full access by subscribing today!

CORPORATE ACCOUNTING

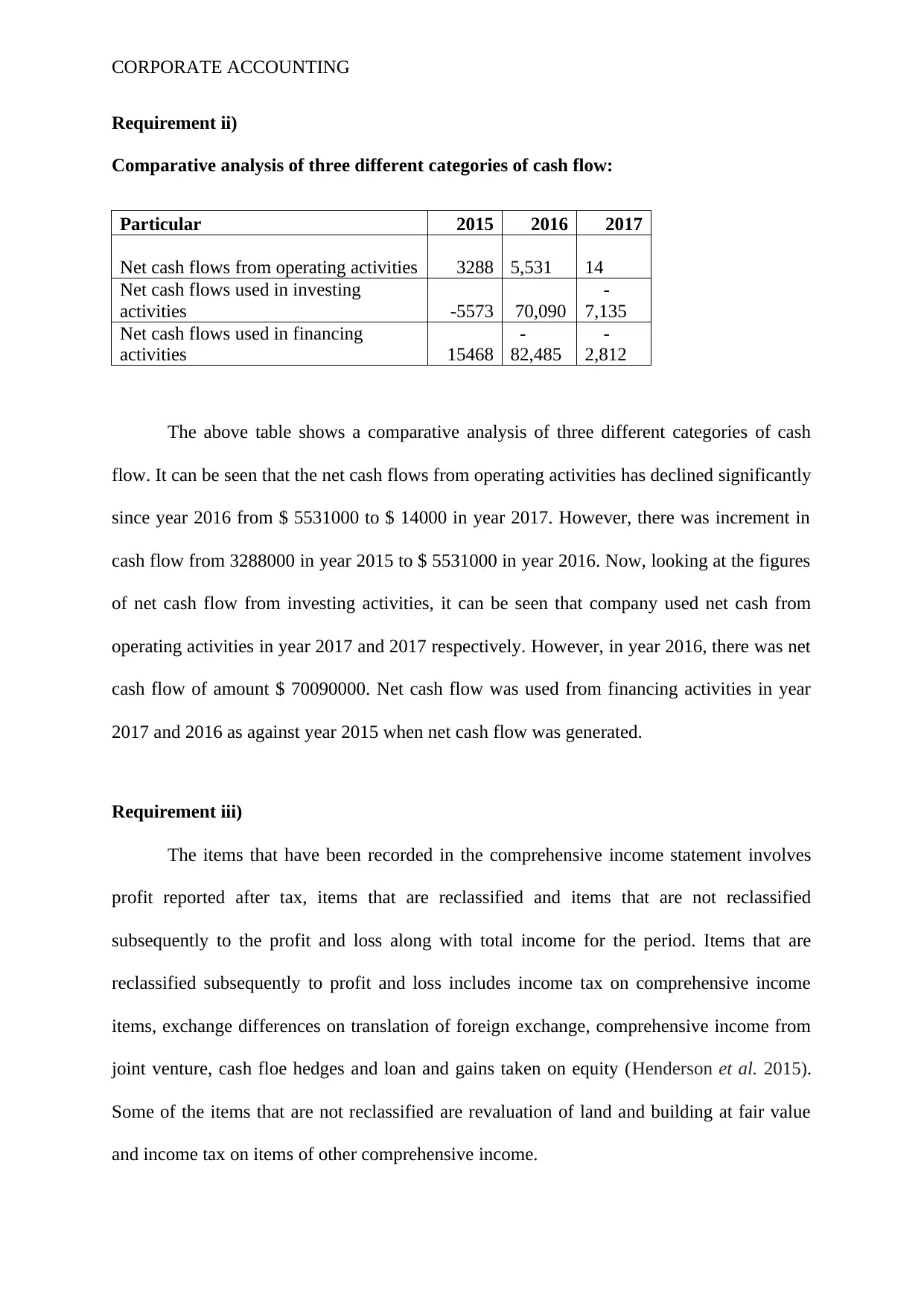

Requirement ii)

Comparative analysis of three different categories of cash flow:

Particular 2015 2016 2017

Net cash flows from operating activities 3288 5,531 14

Net cash flows used in investing

activities -5573 70,090

-

7,135

Net cash flows used in financing

activities 15468

-

82,485

-

2,812

The above table shows a comparative analysis of three different categories of cash

flow. It can be seen that the net cash flows from operating activities has declined significantly

since year 2016 from $ 5531000 to $ 14000 in year 2017. However, there was increment in

cash flow from 3288000 in year 2015 to $ 5531000 in year 2016. Now, looking at the figures

of net cash flow from investing activities, it can be seen that company used net cash from

operating activities in year 2017 and 2017 respectively. However, in year 2016, there was net

cash flow of amount $ 70090000. Net cash flow was used from financing activities in year

2017 and 2016 as against year 2015 when net cash flow was generated.

Requirement iii)

The items that have been recorded in the comprehensive income statement involves

profit reported after tax, items that are reclassified and items that are not reclassified

subsequently to the profit and loss along with total income for the period. Items that are

reclassified subsequently to profit and loss includes income tax on comprehensive income

items, exchange differences on translation of foreign exchange, comprehensive income from

joint venture, cash floe hedges and loan and gains taken on equity (Henderson et al. 2015).

Some of the items that are not reclassified are revaluation of land and building at fair value

and income tax on items of other comprehensive income.

Requirement ii)

Comparative analysis of three different categories of cash flow:

Particular 2015 2016 2017

Net cash flows from operating activities 3288 5,531 14

Net cash flows used in investing

activities -5573 70,090

-

7,135

Net cash flows used in financing

activities 15468

-

82,485

-

2,812

The above table shows a comparative analysis of three different categories of cash

flow. It can be seen that the net cash flows from operating activities has declined significantly

since year 2016 from $ 5531000 to $ 14000 in year 2017. However, there was increment in

cash flow from 3288000 in year 2015 to $ 5531000 in year 2016. Now, looking at the figures

of net cash flow from investing activities, it can be seen that company used net cash from

operating activities in year 2017 and 2017 respectively. However, in year 2016, there was net

cash flow of amount $ 70090000. Net cash flow was used from financing activities in year

2017 and 2016 as against year 2015 when net cash flow was generated.

Requirement iii)

The items that have been recorded in the comprehensive income statement involves

profit reported after tax, items that are reclassified and items that are not reclassified

subsequently to the profit and loss along with total income for the period. Items that are

reclassified subsequently to profit and loss includes income tax on comprehensive income

items, exchange differences on translation of foreign exchange, comprehensive income from

joint venture, cash floe hedges and loan and gains taken on equity (Henderson et al. 2015).

Some of the items that are not reclassified are revaluation of land and building at fair value

and income tax on items of other comprehensive income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Requirement iv)

Revaluation of land and building at fair value means that such assets are reclassified

at the fair value where the date of revaluation is less subsequent to accumulated depreciation

impairment.

Exchange difference is the difference that occurs due to the translation of a given

number of currencies in one unit to another currency at different exchange rates.

Income tax on the items of comprehensive income is the amount of tax that is paid by

entity on items such as expenses, revenue, losses and gains that is mentioned after excluding

the net income reported on income statement.

Requirement v)

The profit and loss statement of company depicts the performance in terms of net loss

or gain realized at the end of any reporting period. However, the statement of comprehensive

income includes the loss and gains that are unrealized. All the items of income and expenses

are recorded in the profit and loss statement except those that are recognized in the statement

of comprehensive income.

Requirement vi)

The income tax expense is reported in the income statement of Gazal Corporation

limited and the amount of income tax expense recorded in the financial year 2017 and 2016

stood at $ 1501 and $ 1550. There is reduction in the income tax payment by reporting entity

in year 2017. Income tax expense recorded in year 2015 stood at $ 914. It is suggested by

figure that income tax expense has increased initially and it declined subsequently.

Requirement iv)

Revaluation of land and building at fair value means that such assets are reclassified

at the fair value where the date of revaluation is less subsequent to accumulated depreciation

impairment.

Exchange difference is the difference that occurs due to the translation of a given

number of currencies in one unit to another currency at different exchange rates.

Income tax on the items of comprehensive income is the amount of tax that is paid by

entity on items such as expenses, revenue, losses and gains that is mentioned after excluding

the net income reported on income statement.

Requirement v)

The profit and loss statement of company depicts the performance in terms of net loss

or gain realized at the end of any reporting period. However, the statement of comprehensive

income includes the loss and gains that are unrealized. All the items of income and expenses

are recorded in the profit and loss statement except those that are recognized in the statement

of comprehensive income.

Requirement vi)

The income tax expense is reported in the income statement of Gazal Corporation

limited and the amount of income tax expense recorded in the financial year 2017 and 2016

stood at $ 1501 and $ 1550. There is reduction in the income tax payment by reporting entity

in year 2017. Income tax expense recorded in year 2015 stood at $ 914. It is suggested by

figure that income tax expense has increased initially and it declined subsequently.

CORPORATE ACCOUNTING

Requirement vii)

The corporate tax rate that is applicable to company is at the rate of 30%. Total

amount of accounting income reported by company in year 2017 and 2016 stood at $

1223000 and $ 58789000 indicating a considerable decline in the amount of accounting profit

generated. The taxation rate when applicable to the accounting profit reported comes to $

3669 (30% of $ 1223000) and $ 17637 (30% of $ 58789000). It can be seen from the

computation that the total amount of income tax paid as reported in the income statement is

different from the accounting income times the applicable taxation rate of company. From the

figures, it can be inferred that the amount if corporate tax paid by reporting entity in both the

years is less than the accounting income times the tax rate. This is so because the amount of

accounting profits and taxable profits are significantly different.

Requirement viii)

The balance sheet of Gazal Corporation limited depicts the total amount of deferred

tax liabilities under the heading noncurrent liabilities. It can be seen that there is no deferred

assets recorded in the balance sheet at the reporting date. Total amount of deferred tax

liabilities recorded in year 2017 and 2016 stood at $ 10932 and $ 8525. It is indicated by the

figure that there is increase in amount of deferred tax liabilities in year 2017 (Gazal.com.au

2018).

Recognition of deferred tax liabilities are done when such income tax liability arises

from goodwill recognition or from any liabilities and assets that are not affecting either the

taxable profit or accounting profit. Measurement of deferred tax liabilities are done at the tax

rate after the liability is settled or assets are realized. The reason why it is recorded under the

balance sheet is that it accounts for the temporary differences between tax that is paid today

and tax that will be paid in future and this forms a part of liability and hence recorded there.

Requirement vii)

The corporate tax rate that is applicable to company is at the rate of 30%. Total

amount of accounting income reported by company in year 2017 and 2016 stood at $

1223000 and $ 58789000 indicating a considerable decline in the amount of accounting profit

generated. The taxation rate when applicable to the accounting profit reported comes to $

3669 (30% of $ 1223000) and $ 17637 (30% of $ 58789000). It can be seen from the

computation that the total amount of income tax paid as reported in the income statement is

different from the accounting income times the applicable taxation rate of company. From the

figures, it can be inferred that the amount if corporate tax paid by reporting entity in both the

years is less than the accounting income times the tax rate. This is so because the amount of

accounting profits and taxable profits are significantly different.

Requirement viii)

The balance sheet of Gazal Corporation limited depicts the total amount of deferred

tax liabilities under the heading noncurrent liabilities. It can be seen that there is no deferred

assets recorded in the balance sheet at the reporting date. Total amount of deferred tax

liabilities recorded in year 2017 and 2016 stood at $ 10932 and $ 8525. It is indicated by the

figure that there is increase in amount of deferred tax liabilities in year 2017 (Gazal.com.au

2018).

Recognition of deferred tax liabilities are done when such income tax liability arises

from goodwill recognition or from any liabilities and assets that are not affecting either the

taxable profit or accounting profit. Measurement of deferred tax liabilities are done at the tax

rate after the liability is settled or assets are realized. The reason why it is recorded under the

balance sheet is that it accounts for the temporary differences between tax that is paid today

and tax that will be paid in future and this forms a part of liability and hence recorded there.

You're viewing a preview

Unlock full access by subscribing today!

CORPORATE ACCOUNTING

The amount of deferred tax liabilities and deferred tax assets recorded in the balance

sheet are subject to change with the change in the rate of income tax. Amount of deferred tax

assets and deferred tax liabilities are readjusted for reflecting the tax that is incurred when the

reversal occurs due to the change in tax rate. Such change in taxation rate helps in depicting

the timing differences and adjustments to previous balance are disclosed as reduction or

addition in the component of deferred tax of the income tax expenses.

Requirement ix)

Yes, there is an income tax payable recorded by Gazal Corporation limited in the

recent financial years. The amount of income tax payable recorded by company stood at $

835 in year 2017 compared to $ 13880 in year 2016 (Gazal.com.au 2018). It can be seen that

there is considerable fall in amount of income tax payable in recent year. There is difference

between the income tax payable and income tax expense reported.

The reason is attributable to the fact that income tax expense is calculated and treated

using the accounting rules and it is reported in the income statement. On other hand,

computation of income tax payable is based on rules and taxation standard and hence it

appears on the liability side of balance sheet until the amount of tax is paid (Meade and Li

2015).

Requirement x)

The total amount of income tax paid comprise of income tax paid on investing

activities and income tax paid on operating activities. Total amount of income tax paid in

year 2017 is recorded at $ 14965 compared to $ 2441 in year 2016. On other hand, the

amount of income tax expense in the financial year 2017 and 2016 stood at $ 1501 and $

1550 (Gazal.com.au 2018). From the figures, it is suggested that total amount of income tax

The amount of deferred tax liabilities and deferred tax assets recorded in the balance

sheet are subject to change with the change in the rate of income tax. Amount of deferred tax

assets and deferred tax liabilities are readjusted for reflecting the tax that is incurred when the

reversal occurs due to the change in tax rate. Such change in taxation rate helps in depicting

the timing differences and adjustments to previous balance are disclosed as reduction or

addition in the component of deferred tax of the income tax expenses.

Requirement ix)

Yes, there is an income tax payable recorded by Gazal Corporation limited in the

recent financial years. The amount of income tax payable recorded by company stood at $

835 in year 2017 compared to $ 13880 in year 2016 (Gazal.com.au 2018). It can be seen that

there is considerable fall in amount of income tax payable in recent year. There is difference

between the income tax payable and income tax expense reported.

The reason is attributable to the fact that income tax expense is calculated and treated

using the accounting rules and it is reported in the income statement. On other hand,

computation of income tax payable is based on rules and taxation standard and hence it

appears on the liability side of balance sheet until the amount of tax is paid (Meade and Li

2015).

Requirement x)

The total amount of income tax paid comprise of income tax paid on investing

activities and income tax paid on operating activities. Total amount of income tax paid in

year 2017 is recorded at $ 14965 compared to $ 2441 in year 2016. On other hand, the

amount of income tax expense in the financial year 2017 and 2016 stood at $ 1501 and $

1550 (Gazal.com.au 2018). From the figures, it is suggested that total amount of income tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

paid in both the years is less than the amount of income tax expense. The amount of income

tax expense is usually higher than the amount of income tax paid and this is attributable to the

fact that the two systems of accounting eventually depreciate the same value with only timing

factor creating such difference. The difference in amount of income tax paid and income tax

expenses are attributable to the difference in accounting treatment of accounting rules and

taxation rules (Powers et al. 2016).

Requirement xi)

The treatment of tax in the financial statements of Gazal Corporation limited seems to

be quite interesting as there is proper and segregated disclosure of the accounting treatment

relating to income tax. Treatment and adjustment of the income tax such as income tax

expense, income tax payable, deferred income tax liabilities and income tax payable on

comprehensive income are presented in different financial statements according to the rules

of accounting (Auerbach and Hassett 2015). It has been ascertained from the analysis of the

annual report of company that all the Australia capital gain tax losses have been utilized by

the group. The statement of comprehensive income depicts the amount of income tax that is

paid on items of other comprehensive income. Amount of income tax payable is presented

under the liability side of balance sheet. Cash flow statement on other hand depicts the

amount of income tax that is paid on operating and investing activities (Dyreng et al. 2017).

Therefore, it can be seen that there is proper segregation of all the items relating to income

tax that is quite an interesting fact.

Moreover, a tax consolidated group has been formed by Gazal Corporation limited

that was effective from 1st July, 2003 and the group is head entity of the tax consolidated

group. In order to allocate the income tax liabilities to the wholly owned subsidiaries,

members of the group have entered into an arrangement of tax sharing. The allocation of

paid in both the years is less than the amount of income tax expense. The amount of income

tax expense is usually higher than the amount of income tax paid and this is attributable to the

fact that the two systems of accounting eventually depreciate the same value with only timing

factor creating such difference. The difference in amount of income tax paid and income tax

expenses are attributable to the difference in accounting treatment of accounting rules and

taxation rules (Powers et al. 2016).

Requirement xi)

The treatment of tax in the financial statements of Gazal Corporation limited seems to

be quite interesting as there is proper and segregated disclosure of the accounting treatment

relating to income tax. Treatment and adjustment of the income tax such as income tax

expense, income tax payable, deferred income tax liabilities and income tax payable on

comprehensive income are presented in different financial statements according to the rules

of accounting (Auerbach and Hassett 2015). It has been ascertained from the analysis of the

annual report of company that all the Australia capital gain tax losses have been utilized by

the group. The statement of comprehensive income depicts the amount of income tax that is

paid on items of other comprehensive income. Amount of income tax payable is presented

under the liability side of balance sheet. Cash flow statement on other hand depicts the

amount of income tax that is paid on operating and investing activities (Dyreng et al. 2017).

Therefore, it can be seen that there is proper segregation of all the items relating to income

tax that is quite an interesting fact.

Moreover, a tax consolidated group has been formed by Gazal Corporation limited

that was effective from 1st July, 2003 and the group is head entity of the tax consolidated

group. In order to allocate the income tax liabilities to the wholly owned subsidiaries,

members of the group have entered into an arrangement of tax sharing. The allocation of

CORPORATE ACCOUNTING

income tax liabilities are done based on the formula that is set out in the agreement.

Agreements that is providing for the allocation of the liabilities pertaining to income tax

between entities should the entity default on its obligations of income tax payment

(Gazal.com.au 2018). The possibility of default is remote at the balance date. Furthermore,

the members of tax consolidated group accounts for the effect of tax. As per the agreement,

the current tax is allocated to the members of tax consolidated group along with allocating the

deferred tax to the members of tax consolidated group (Gazal.com.au 2018). Such allocations

are on done in accordance with the principles of AASB 112 Income taxes. Under the tax

funding agreement, allocation of taxes is recognized as a decrease or increase in the accounts

of inter company subsidiaries with the tax consolidated company of Gazal corporation

limited. In addition to this, the tax treatment of hedging transactions has been observed with

changes with the legislation in place.

income tax liabilities are done based on the formula that is set out in the agreement.

Agreements that is providing for the allocation of the liabilities pertaining to income tax

between entities should the entity default on its obligations of income tax payment

(Gazal.com.au 2018). The possibility of default is remote at the balance date. Furthermore,

the members of tax consolidated group accounts for the effect of tax. As per the agreement,

the current tax is allocated to the members of tax consolidated group along with allocating the

deferred tax to the members of tax consolidated group (Gazal.com.au 2018). Such allocations

are on done in accordance with the principles of AASB 112 Income taxes. Under the tax

funding agreement, allocation of taxes is recognized as a decrease or increase in the accounts

of inter company subsidiaries with the tax consolidated company of Gazal corporation

limited. In addition to this, the tax treatment of hedging transactions has been observed with

changes with the legislation in place.

You're viewing a preview

Unlock full access by subscribing today!

CORPORATE ACCOUNTING

References list:

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Bergner, S.M. and Heckemeyer, J.H., 2017. Simplified tax accounting and the choice of legal

form. European accounting review, 26(3), pp.581-601.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Dagwell, R., Wines, G. and Lambert, C., 2015. Corporate accounting in Australia. Pearson

Higher Education AU.

De Simone, L., 2016. Does a common set of accounting standards affect tax-motivated

income shifting for multinational firms?. Journal of Accounting and Economics, 61(1),

pp.145-165.

Dyreng, S.D., Hanlon, M., Maydew, E.L. and Thornock, J.R., 2017. Changes in corporate

effective tax rates over the past 25 years. Journal of Financial Economics, 124(3), pp.441-

463.

Gazal.com.au. (2018). Gazal. [online] Available at:

http://www.gazal.com.au/asx_announcements.html [Accessed 23 May 2018].

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

References list:

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Bergner, S.M. and Heckemeyer, J.H., 2017. Simplified tax accounting and the choice of legal

form. European accounting review, 26(3), pp.581-601.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Dagwell, R., Wines, G. and Lambert, C., 2015. Corporate accounting in Australia. Pearson

Higher Education AU.

De Simone, L., 2016. Does a common set of accounting standards affect tax-motivated

income shifting for multinational firms?. Journal of Accounting and Economics, 61(1),

pp.145-165.

Dyreng, S.D., Hanlon, M., Maydew, E.L. and Thornock, J.R., 2017. Changes in corporate

effective tax rates over the past 25 years. Journal of Financial Economics, 124(3), pp.441-

463.

Gazal.com.au. (2018). Gazal. [online] Available at:

http://www.gazal.com.au/asx_announcements.html [Accessed 23 May 2018].

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Keightley, M.P. and Sherlock, M.F., 2014. The corporate income tax system: Overview and

options for reform.

Lee, T.A. and Parker, R.H. eds., 2014. Evolution of Corporate Financial Reporting (RLE

Accounting). Routledge.

Li, Z., Wang, L. and Wruck, K., 2017. Accounting-Based Compensation Contracts, the Cost

of Borrowing, and the Structure of Corporate Debt Contracts. Working Paper Chapman

University.

Meade, J.A. and Li, S., 2015. Strategic corporate tax lobbying. The Journal of the American

Taxation Association, 37(2), pp.23-48.

Oxner, K.M., Oxner, T.H. and Phillips, A.D., 2018. Impact of the Tax Cuts and Jobs Act on

Accounting for Deferred Income Taxes. Journal of Corporate Accounting & Finance, 29(2),

pp.12-21.

Powers, K., Robinson, J.R. and Stomberg, B., 2016. How do CEO incentives affect corporate

tax planning and financial reporting of income taxes?. Review of Accounting Studies, 21(2),

pp.672-710.

Stein, M.J., Salterio, S.E. and Shearer, T., 2017. “Transparency” in Accounting and

Corporate Governance: Making Sense of Multiple Meanings. Accounting and the Public

Interest, 17(1), pp.31-59.

Toder, E. and Viard, A.D., 2016. Replacing corporate tax revenues with a mark-to-market tax

on shareholder income. National Tax Journal, 69(3), p.701.

Wahab, N.S.A. and Holland, K., 2015. The persistence of book-tax differences. The British

Accounting Review, 47(4), pp.339-350.

Keightley, M.P. and Sherlock, M.F., 2014. The corporate income tax system: Overview and

options for reform.

Lee, T.A. and Parker, R.H. eds., 2014. Evolution of Corporate Financial Reporting (RLE

Accounting). Routledge.

Li, Z., Wang, L. and Wruck, K., 2017. Accounting-Based Compensation Contracts, the Cost

of Borrowing, and the Structure of Corporate Debt Contracts. Working Paper Chapman

University.

Meade, J.A. and Li, S., 2015. Strategic corporate tax lobbying. The Journal of the American

Taxation Association, 37(2), pp.23-48.

Oxner, K.M., Oxner, T.H. and Phillips, A.D., 2018. Impact of the Tax Cuts and Jobs Act on

Accounting for Deferred Income Taxes. Journal of Corporate Accounting & Finance, 29(2),

pp.12-21.

Powers, K., Robinson, J.R. and Stomberg, B., 2016. How do CEO incentives affect corporate

tax planning and financial reporting of income taxes?. Review of Accounting Studies, 21(2),

pp.672-710.

Stein, M.J., Salterio, S.E. and Shearer, T., 2017. “Transparency” in Accounting and

Corporate Governance: Making Sense of Multiple Meanings. Accounting and the Public

Interest, 17(1), pp.31-59.

Toder, E. and Viard, A.D., 2016. Replacing corporate tax revenues with a mark-to-market tax

on shareholder income. National Tax Journal, 69(3), p.701.

Wahab, N.S.A. and Holland, K., 2015. The persistence of book-tax differences. The British

Accounting Review, 47(4), pp.339-350.

CORPORATE ACCOUNTING

Appendix:

Particulars 2015 (in

000)

2016 (in

000)

2017 (in

000)

Cash flows from operating activities:

Receipts from customers (inclusive of GST) 295639 126998 75656

Payments to suppliers and employees (inclusive of GST) -2,88,849 -1,19,494 -73,282

Interest received -198 224 50

Interest and other costs of finance paid -1,997 -697 -635

Income taxes paid on operating activities -1,307 -1,500 -1,775

Net cash flows from operating activities $

3,288.00

$

5,531.00

$

14.00

Cash flows from investing activities:

Purchases of property, plant and equipment -4,083 -2,836 -2,335

Proceeds from sale of buildings, plant and equipment $

86.00

138 249

Purchase of intangibles $ -

175.00

$ -

271.00

$ -

1,624.00

Proceeds from sale of discontinued operations $

10,484.00

$

74,000.00

$

5,765.00

Income taxes paid on disposal of discontinued

operations

0 $ -

941.00

$ -

13,190.00

Dividends from joint venture $ -

11,885.00

$

-

$

4,000.00

Net cash flows used in investing activities $ -

5,573.00

$

70,090.00

$ -

7,135.00

Cash flows from financing activities:

Proceeds from share issue $

290.00

300 600

Proceeds from borrowings 35,000 0 27,000

Repayment of borrowings $ -

10,000.00

-55,000 $ -

2,500.00

Dividends paid $ -

9,822.00

$ -

27,785.00

$ -

27,912.00

Net cash flows used in financing activities $

15,468.00

$ -

82,485.00

$ -

2,812.00

Net increase/(decrease) in cash and cash equivalents $

13,184.00

$ -

6,864.00

$ -

9,933.00

Cash and cash equivalents at beginning of year $

6,163.00

$

19,348.00

$

12,540.00

Effects of exchange rate changes on the balance of cash

held in foreign currencies

$

1.00

$

56.00

$

3.00

Cash and cash equivalents at end of year $

19,348.00

$

12,540.00

$

2,610.00

Appendix:

Particulars 2015 (in

000)

2016 (in

000)

2017 (in

000)

Cash flows from operating activities:

Receipts from customers (inclusive of GST) 295639 126998 75656

Payments to suppliers and employees (inclusive of GST) -2,88,849 -1,19,494 -73,282

Interest received -198 224 50

Interest and other costs of finance paid -1,997 -697 -635

Income taxes paid on operating activities -1,307 -1,500 -1,775

Net cash flows from operating activities $

3,288.00

$

5,531.00

$

14.00

Cash flows from investing activities:

Purchases of property, plant and equipment -4,083 -2,836 -2,335

Proceeds from sale of buildings, plant and equipment $

86.00

138 249

Purchase of intangibles $ -

175.00

$ -

271.00

$ -

1,624.00

Proceeds from sale of discontinued operations $

10,484.00

$

74,000.00

$

5,765.00

Income taxes paid on disposal of discontinued

operations

0 $ -

941.00

$ -

13,190.00

Dividends from joint venture $ -

11,885.00

$

-

$

4,000.00

Net cash flows used in investing activities $ -

5,573.00

$

70,090.00

$ -

7,135.00

Cash flows from financing activities:

Proceeds from share issue $

290.00

300 600

Proceeds from borrowings 35,000 0 27,000

Repayment of borrowings $ -

10,000.00

-55,000 $ -

2,500.00

Dividends paid $ -

9,822.00

$ -

27,785.00

$ -

27,912.00

Net cash flows used in financing activities $

15,468.00

$ -

82,485.00

$ -

2,812.00

Net increase/(decrease) in cash and cash equivalents $

13,184.00

$ -

6,864.00

$ -

9,933.00

Cash and cash equivalents at beginning of year $

6,163.00

$

19,348.00

$

12,540.00

Effects of exchange rate changes on the balance of cash

held in foreign currencies

$

1.00

$

56.00

$

3.00

Cash and cash equivalents at end of year $

19,348.00

$

12,540.00

$

2,610.00

You're viewing a preview

Unlock full access by subscribing today!

CORPORATE ACCOUNTING

References list:

References list:

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.