Corporate Accounting Assignment Solution for ACT305, Semester 2, 2018

VerifiedAdded on 2023/06/04

|9

|2098

|385

Homework Assignment

AI Summary

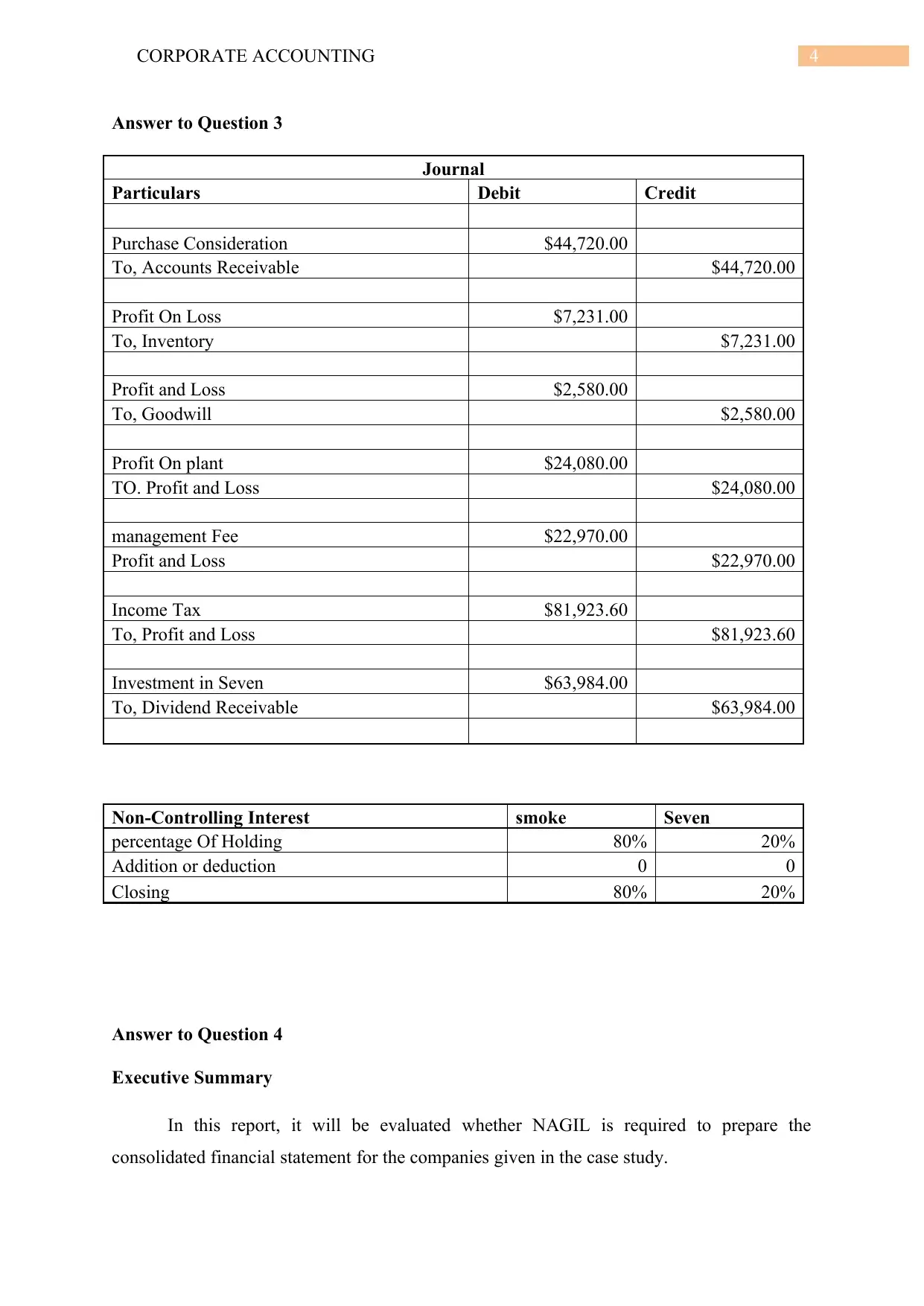

This document presents a comprehensive solution to a Corporate Accounting assignment (ACT305), addressing various aspects of financial accounting. The solution includes detailed journal entries for different scenarios, such as profit recognition and dividend investments. It also features a liquidator's final statement of accounts, demonstrating the allocation of assets and liabilities. Furthermore, the assignment delves into consolidation accounting, analyzing scenarios based on AASB 10 to determine whether consolidated financial statements are required for different investments. The analysis evaluates the level of control an investor has over investee companies, considering factors like loan arrangements, administrative power, and share ownership. The document concludes by summarizing the consolidation requirements for each case, providing a clear understanding of the application of accounting standards.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.