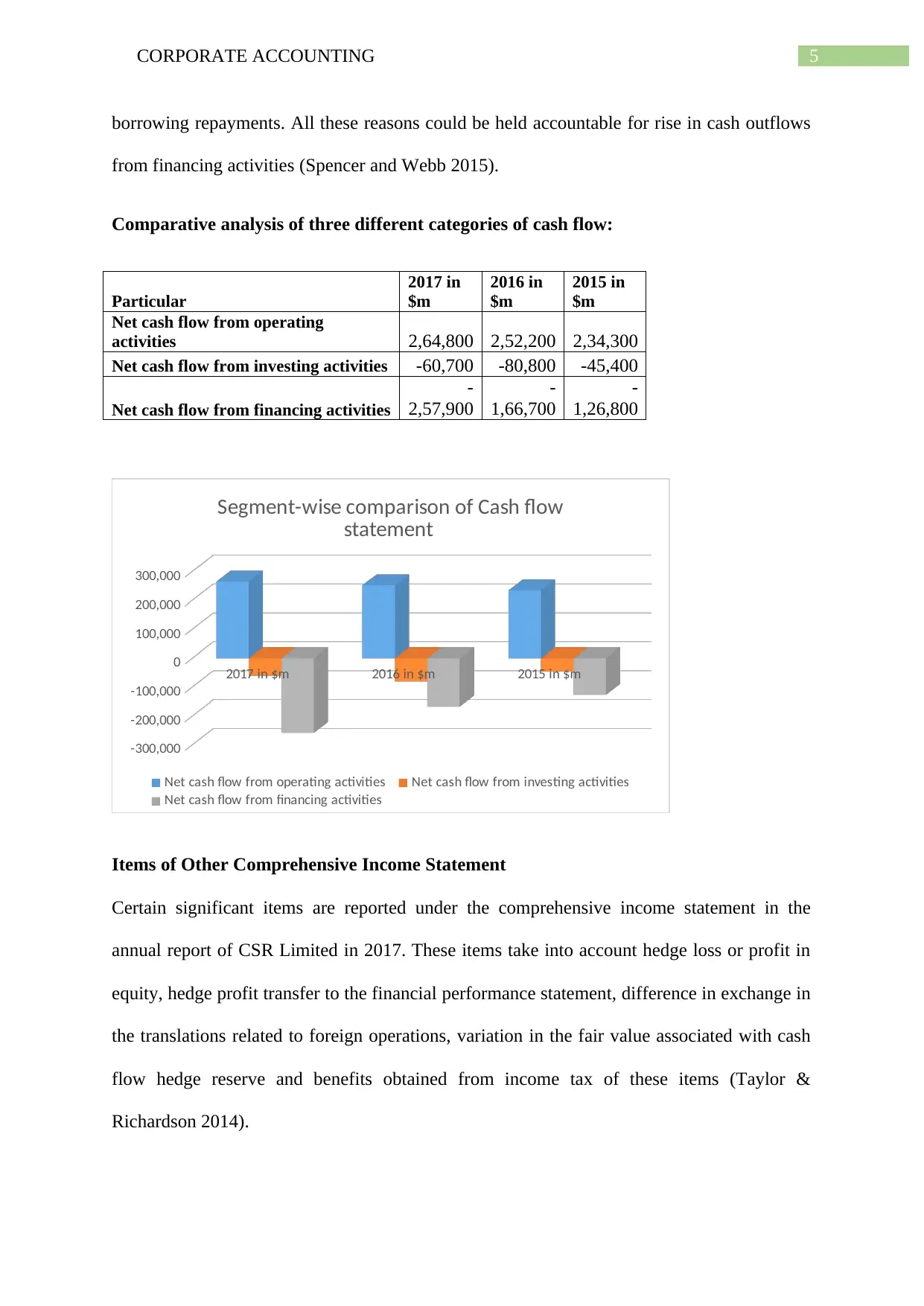

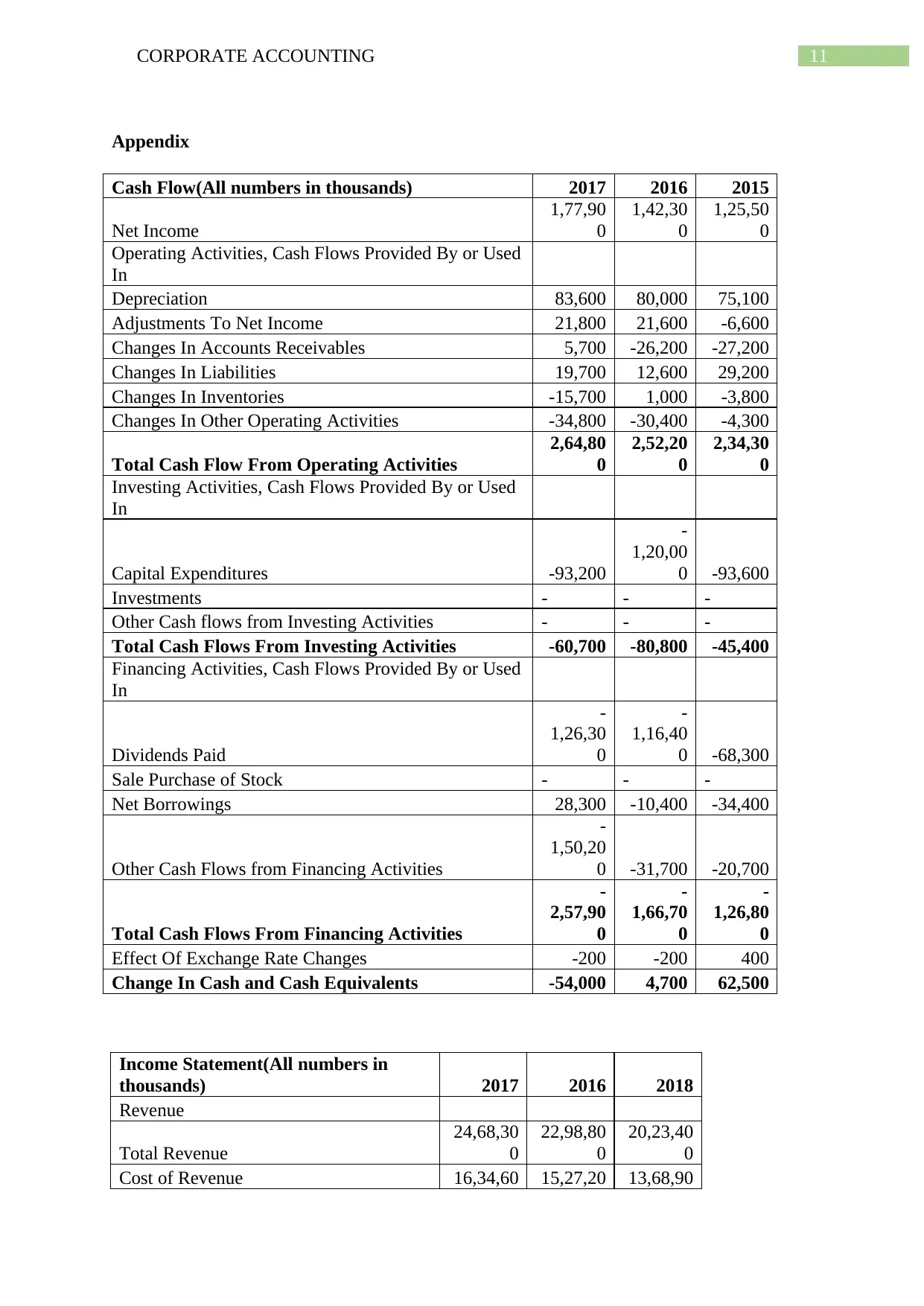

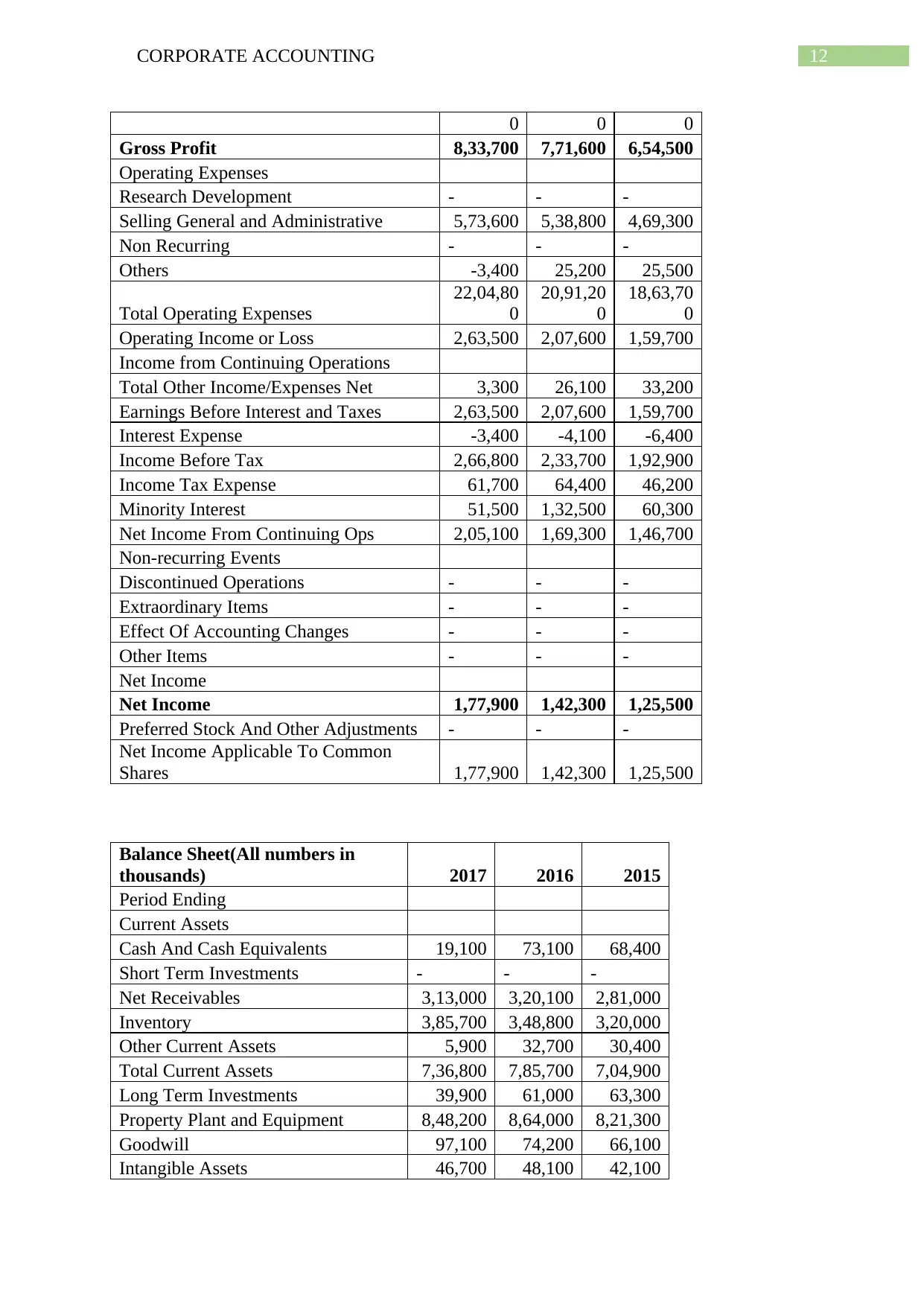

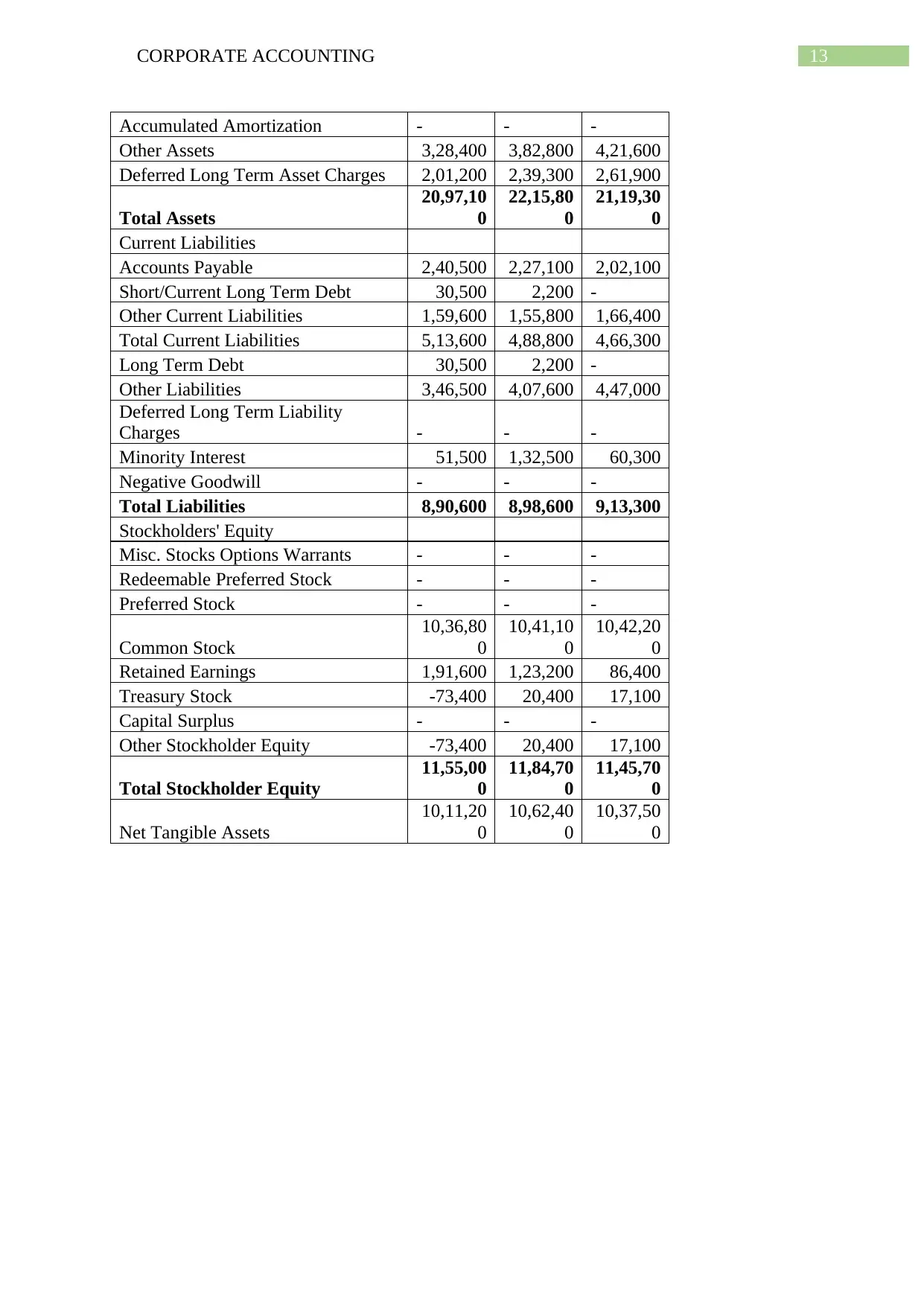

This paper analyses the cash flow statement and other financial statements of CSR Limited, including changes in each item of cash flows statement, comparative analysis of the company’s three broad categories of cash flows, items of other comprehensive income statement, clear description of the firm’s income tax expense, verification of the figure of tax being same as the company tax rate times the firm’s accounting income, deferred tax that is reported in the balance sheet, current tax assets or income tax payable recorded by the company, verification of the income tax expense shown in the income statement same as the income tax paid shown in the cash flow statement, and unique characteristics in the financial statements, new insights, and other information.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)