CORPORATE ACCOUNTING CORPORATE ACCOUNTING CORPORATE ACCOUNTING Name of the university Student ID

VerifiedAdded on 2021/05/31

|12

|2326

|443

AI Summary

The reason of decrease was that the receipts from the customers in the year 2017 were significantly high if it is compared with the receipts of the year 2016. Answer (ii) Particulars 2017 ($'000) 2016 ($'000) 2015 ($'000) Net cash used in operating activities -4,401.00 34,770.00 -38,623.00 Net cash (used in) / provided by investing activities -66,430.00 -66,430.00 Net cash (used in) / provided

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 1

Table of Contents

Answer (i)...................................................................................................................................2

Answer (ii).................................................................................................................................3

Answer (iii)................................................................................................................................4

Answer (iv).................................................................................................................................4

Answer (v)..................................................................................................................................5

Answer (vi).................................................................................................................................5

Answer (vii)...............................................................................................................................5

Answer (viii)..............................................................................................................................6

Answer (ix).................................................................................................................................6

Answer (x)..................................................................................................................................6

Answer (xi).................................................................................................................................7

Reference....................................................................................................................................8

Table of Contents

Answer (i)...................................................................................................................................2

Answer (ii).................................................................................................................................3

Answer (iii)................................................................................................................................4

Answer (iv).................................................................................................................................4

Answer (v)..................................................................................................................................5

Answer (vi).................................................................................................................................5

Answer (vii)...............................................................................................................................5

Answer (viii)..............................................................................................................................6

Answer (ix).................................................................................................................................6

Answer (x)..................................................................................................................................6

Answer (xi).................................................................................................................................7

Reference....................................................................................................................................8

CORPORATE ACCOUNTING 2

The ASX listed company XERO Limited offers the platform for the online accounting

and the business services for the small scale business entities. The company provides XERO

software that is service software and it can be accessed from internet cloud through the

standard browser (Xero Accounting Software 2018.). The objective of this report is to

analyse the company’s cash flow statement, balance sheet and other comprehensive income

statement for last 3 years that covers 2015, 2016 and 2017.

Answer (i)

Looking into the annual report of XERO Limited it is recognised that the company’s

cash flow statement is divided into 3 parts – cash flows from operating activities, cash flow

from investing activities and cash flow from financing activities.

Net cash flow or cash used in operating activities – this includes all the cash flows or

the cash used in the operational activities of the company like payment of tax, receipt

of interest and payment made to suppliers. Generally the operating activities of the

company includes the non-cash expenses like depreciation, net income and changes in

the working capital (Chang et al. 2014). There is significant decrease in the cash

flows from operating activities of the company over the years from 2016 to 2017. The

reason of decrease was that the receipts from the customers in the year 2017 were

significantly high if it is compared with the receipts of the year 2016.

Net cash used in or provided by the investing activities – cash flow from investing

activities records the cash generated from or cash used in the investing activities of

the company (Sarfaty 2015). Financing activities of XERO Limited includes

capitalised cost for development, cost of rental bonds and amount spend for

purchasing plant, equipment and property.

Net cash provided by or used in the financing activities – cash flow from financing

activities records the cash generated from or cash used in the financing activities of

The ASX listed company XERO Limited offers the platform for the online accounting

and the business services for the small scale business entities. The company provides XERO

software that is service software and it can be accessed from internet cloud through the

standard browser (Xero Accounting Software 2018.). The objective of this report is to

analyse the company’s cash flow statement, balance sheet and other comprehensive income

statement for last 3 years that covers 2015, 2016 and 2017.

Answer (i)

Looking into the annual report of XERO Limited it is recognised that the company’s

cash flow statement is divided into 3 parts – cash flows from operating activities, cash flow

from investing activities and cash flow from financing activities.

Net cash flow or cash used in operating activities – this includes all the cash flows or

the cash used in the operational activities of the company like payment of tax, receipt

of interest and payment made to suppliers. Generally the operating activities of the

company includes the non-cash expenses like depreciation, net income and changes in

the working capital (Chang et al. 2014). There is significant decrease in the cash

flows from operating activities of the company over the years from 2016 to 2017. The

reason of decrease was that the receipts from the customers in the year 2017 were

significantly high if it is compared with the receipts of the year 2016.

Net cash used in or provided by the investing activities – cash flow from investing

activities records the cash generated from or cash used in the investing activities of

the company (Sarfaty 2015). Financing activities of XERO Limited includes

capitalised cost for development, cost of rental bonds and amount spend for

purchasing plant, equipment and property.

Net cash provided by or used in the financing activities – cash flow from financing

activities records the cash generated from or cash used in the financing activities of

CORPORATE ACCOUNTING 3

the company. Financing activities of XERO Limited includes proceeds from and

payments towards short-term deposits and repayment of the management loan.

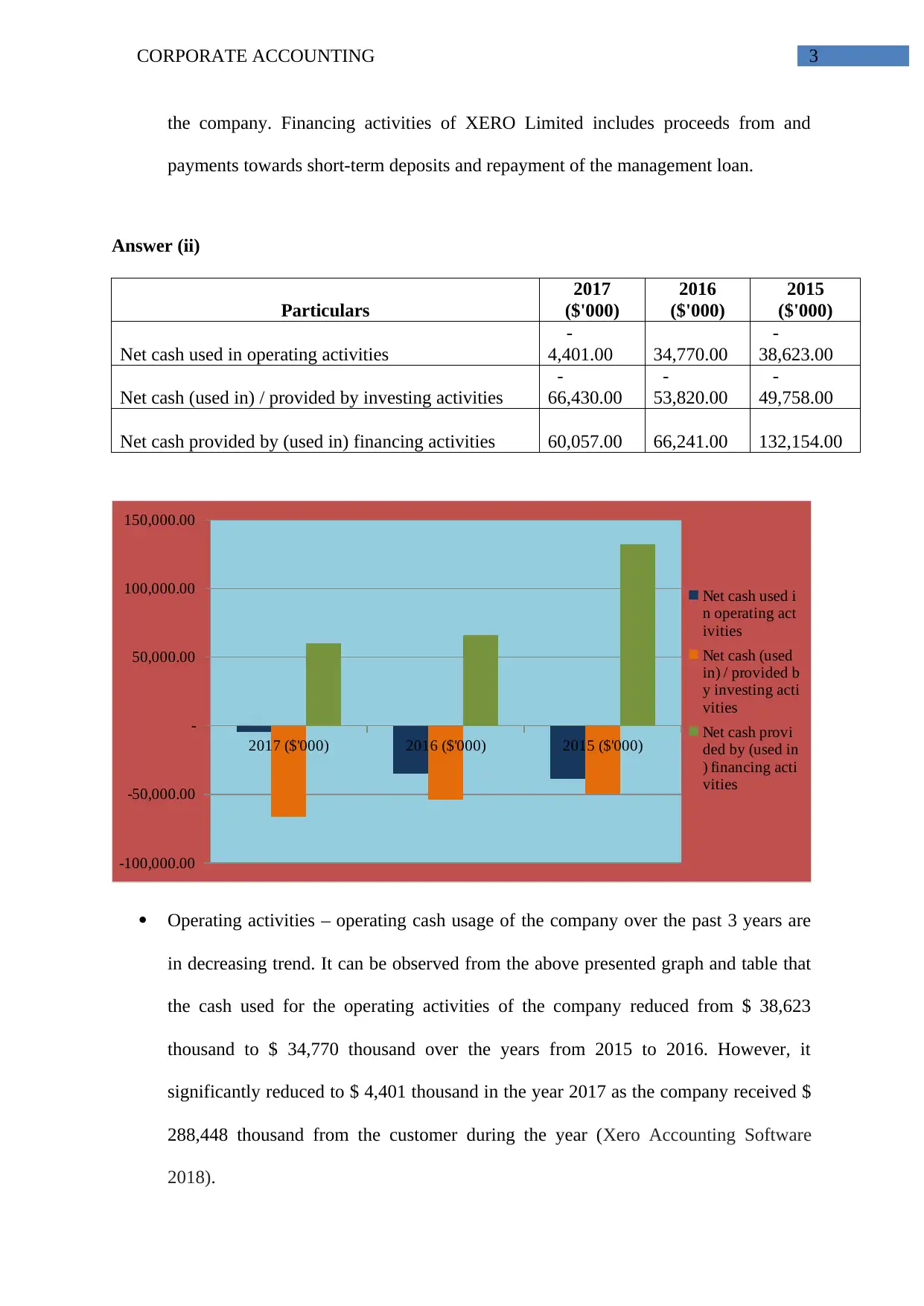

Answer (ii)

Particulars

2017

($'000)

2016

($'000)

2015

($'000)

Net cash used in operating activities

-

4,401.00 34,770.00

-

38,623.00

Net cash (used in) / provided by investing activities

-

66,430.00

-

53,820.00

-

49,758.00

Net cash provided by (used in) financing activities 60,057.00 66,241.00 132,154.00

2017 ($'000) 2016 ($'000) 2015 ($'000)

-100,000.00

-50,000.00

-

50,000.00

100,000.00

150,000.00

Net cash used i

n operating act

ivities

Net cash (used

in) / provided b

y investing acti

vities

Net cash provi

ded by (used in

) financing acti

vities

Operating activities – operating cash usage of the company over the past 3 years are

in decreasing trend. It can be observed from the above presented graph and table that

the cash used for the operating activities of the company reduced from $ 38,623

thousand to $ 34,770 thousand over the years from 2015 to 2016. However, it

significantly reduced to $ 4,401 thousand in the year 2017 as the company received $

288,448 thousand from the customer during the year (Xero Accounting Software

2018).

the company. Financing activities of XERO Limited includes proceeds from and

payments towards short-term deposits and repayment of the management loan.

Answer (ii)

Particulars

2017

($'000)

2016

($'000)

2015

($'000)

Net cash used in operating activities

-

4,401.00 34,770.00

-

38,623.00

Net cash (used in) / provided by investing activities

-

66,430.00

-

53,820.00

-

49,758.00

Net cash provided by (used in) financing activities 60,057.00 66,241.00 132,154.00

2017 ($'000) 2016 ($'000) 2015 ($'000)

-100,000.00

-50,000.00

-

50,000.00

100,000.00

150,000.00

Net cash used i

n operating act

ivities

Net cash (used

in) / provided b

y investing acti

vities

Net cash provi

ded by (used in

) financing acti

vities

Operating activities – operating cash usage of the company over the past 3 years are

in decreasing trend. It can be observed from the above presented graph and table that

the cash used for the operating activities of the company reduced from $ 38,623

thousand to $ 34,770 thousand over the years from 2015 to 2016. However, it

significantly reduced to $ 4,401 thousand in the year 2017 as the company received $

288,448 thousand from the customer during the year (Xero Accounting Software

2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 4

Investing activities – investing cash usage of the company over the past 3 years are in

increasing trend. It can be observed from the above presented graph and table that the

cash used for the investing activities of the company increased from $ 49,758

thousand to $ 53,820 thousand over the years from 2015 to 2016 and it further

increased to $ 66,430 thousands in the year 2017 (Xero Accounting Software 2018.)

Financing activities – cash generated from financing activities of the company over

the past 3 years are in decreasing trend. It can be observed from the above presented

graph and table that the cash generated from the financing activities of the company

significantly reduced from $ 132,154 thousand to $ 66,241 thousand over the years

from 2015 to 2016 and it further increased to $ 60,057 thousands in the year 2017.

Reason of significant reduction over the years from 205 to 2016 is that the company

did not issue any shares in 2016 and proceeds from the short-term deposits were

significantly reduced from $ 403,000 thousands to $ 210,000 thousands over the years

from 2017 to 2016 (Xero Accounting Software 2018).

Answer (iii)

Other comprehensive loss of XERO Limited for the year ended 2017 amounted to $

68,442,000 as compared to $ 86,185,000 for the year 2016. Various items recognized by the

company under its comprehensive income statement are movement in the cash flow hedges

that amounted to $ 20,29,000, translation of the international subsidiaries amounted to $

14,15,000 and other comprehensive income amounted to $ 615,000.

Answer (iv)

The cash flow hedges that is included in the comprehensive income statement of the

company is the derivative in FECs (Forward exchange contracts) for reducing risks in such a

way that the changes in the exchange rates will have an impact on the cash flows of the

company. The hedges are recognized as highly probable under the forecasting of the

transactions. Further the difference in exchange rates arises from the translation of

Investing activities – investing cash usage of the company over the past 3 years are in

increasing trend. It can be observed from the above presented graph and table that the

cash used for the investing activities of the company increased from $ 49,758

thousand to $ 53,820 thousand over the years from 2015 to 2016 and it further

increased to $ 66,430 thousands in the year 2017 (Xero Accounting Software 2018.)

Financing activities – cash generated from financing activities of the company over

the past 3 years are in decreasing trend. It can be observed from the above presented

graph and table that the cash generated from the financing activities of the company

significantly reduced from $ 132,154 thousand to $ 66,241 thousand over the years

from 2015 to 2016 and it further increased to $ 60,057 thousands in the year 2017.

Reason of significant reduction over the years from 205 to 2016 is that the company

did not issue any shares in 2016 and proceeds from the short-term deposits were

significantly reduced from $ 403,000 thousands to $ 210,000 thousands over the years

from 2017 to 2016 (Xero Accounting Software 2018).

Answer (iii)

Other comprehensive loss of XERO Limited for the year ended 2017 amounted to $

68,442,000 as compared to $ 86,185,000 for the year 2016. Various items recognized by the

company under its comprehensive income statement are movement in the cash flow hedges

that amounted to $ 20,29,000, translation of the international subsidiaries amounted to $

14,15,000 and other comprehensive income amounted to $ 615,000.

Answer (iv)

The cash flow hedges that is included in the comprehensive income statement of the

company is the derivative in FECs (Forward exchange contracts) for reducing risks in such a

way that the changes in the exchange rates will have an impact on the cash flows of the

company. The hedges are recognized as highly probable under the forecasting of the

transactions. Further the difference in exchange rates arises from the translation of

CORPORATE ACCOUNTING 5

international subsidiaries is recorded as the separate component of equity. Amount of

differences are recognized under the statement of comprehensive statement only when the

foreign operations are disposed-off (Titman, Keown and Martin 2017).

Answer (v)

Items of expenses and incomes those are not recognized under the income statement

or comprehensive income statement of the company are recorded under the statement of

comprehensive statement (Sethi 2016). The statement helps the user to get better and clear

picture of the company’s profitability position. The amount of losses or incomes those are

already been recognized are recorded in the income statement. However, the unrealized items

of investments are included in the other comprehensive income statement (Warren and Jones

2018). It helps the investors and financial analysts to measure the fair value of the investment

of the company.

Answer (vi)

The net income remains with the company after paying off the expenses and adjusting

for various non-assessable and disallowed items are considered as the amount chargeable to

tax. The tax is applicable at the rate enacted or substantially enacted by the jurisdiction

(Weygandt, Kimmel and Kieso 2015). Further the amount of tax expenses is adjusted for

deferred tax assets or deferred tax liabilities that arise due to temporary differences. Income

tax expenses for XERO Limited as per the latest financial report is $ 19,87,000 as compared

to $ 15,12,000 for the previous year.

Answer (vii)

The income tax rate applicable to the company by the appropriate authority is 28%.

Net loss of the company before tax payment for the year ended 2017 amounted to $

67,070,000. However, Income tax expenses for XERO Limited for the same period amounted

to $ 19,87,000. However, the tax expenses do not match with the applicable rate on the

income of the company as the company had loss for the period (Narotzki 2017). The reason

of difference is that the expenses of income tax includes the adjustments for prior period,

effect of the prior period’s development and research credit, utilisation of tax loss, deferred

tax and impact of changes in the foreign currency.

international subsidiaries is recorded as the separate component of equity. Amount of

differences are recognized under the statement of comprehensive statement only when the

foreign operations are disposed-off (Titman, Keown and Martin 2017).

Answer (v)

Items of expenses and incomes those are not recognized under the income statement

or comprehensive income statement of the company are recorded under the statement of

comprehensive statement (Sethi 2016). The statement helps the user to get better and clear

picture of the company’s profitability position. The amount of losses or incomes those are

already been recognized are recorded in the income statement. However, the unrealized items

of investments are included in the other comprehensive income statement (Warren and Jones

2018). It helps the investors and financial analysts to measure the fair value of the investment

of the company.

Answer (vi)

The net income remains with the company after paying off the expenses and adjusting

for various non-assessable and disallowed items are considered as the amount chargeable to

tax. The tax is applicable at the rate enacted or substantially enacted by the jurisdiction

(Weygandt, Kimmel and Kieso 2015). Further the amount of tax expenses is adjusted for

deferred tax assets or deferred tax liabilities that arise due to temporary differences. Income

tax expenses for XERO Limited as per the latest financial report is $ 19,87,000 as compared

to $ 15,12,000 for the previous year.

Answer (vii)

The income tax rate applicable to the company by the appropriate authority is 28%.

Net loss of the company before tax payment for the year ended 2017 amounted to $

67,070,000. However, Income tax expenses for XERO Limited for the same period amounted

to $ 19,87,000. However, the tax expenses do not match with the applicable rate on the

income of the company as the company had loss for the period (Narotzki 2017). The reason

of difference is that the expenses of income tax includes the adjustments for prior period,

effect of the prior period’s development and research credit, utilisation of tax loss, deferred

tax and impact of changes in the foreign currency.

CORPORATE ACCOUNTING 6

Answer (viii)

The company recognizes the deferred tax with regard to the temporary differences

among the asset’s and liability’s carrying amount determined for the purpose of recording in

the financial statement and the amount determined for the purpose of taxation. Further, the

deferred tax amount is determined on the basis of expected method in which the carrying

amount of the liabilities and assets are realised at the end of the period through the applicable

tax rate on the company (Laux 2013). The amount for deferred tax is recorded in the financial

statement up to the amount that is apparent to be available from future taxable profit against

of which the asset is usable. Amount of deferred tax assets recorded by the company under

the non-current section of balance sheet for the year ended 2017 was $ 20,65,000.

Answer (ix)

Income tax or current tax payable by the company for the year ended 2017 by XERO

Limited was amounted to $ 11,05,000. On the other hand, the income tax expenses for the

company as per the latest financial report is $ 19,87,000. Expense of income tax is the

amount the company is liable to pay as per the applicable taxation rules. However, the

payable amount of income tax is computed through applying the applicable tax rates on the

company (Melloni, Lai and Stacchezzini 2018). The income tax expense is recorded in the

income statement of the company whereas the current tax is recorded in the cash flow

statement of the company. Owing to all these differences the amount of current tax does not

match with the amount of income tax expenses.

Answer (x)

The income tax expenses for the company as per the latest financial report is $

19,87,000. On the other hand, the income tax paid as recorded in the cash flow statement of

the company was $ 20,93,000. The amount of tax expenses under the income statement of the

company varies from the amount recorded as income tax paid in the cash flow statement as

the income tax paid is the amount of tax on the operating activities of the company. On the

other hand the income tax expenses is the amount of tax applicable on the revenue of the

company left after paying off all the expenses like operating expenses, investing expenses,

selling and administration expenses and financing expenses (Maaloul and Zéghal 2015).

Answer (viii)

The company recognizes the deferred tax with regard to the temporary differences

among the asset’s and liability’s carrying amount determined for the purpose of recording in

the financial statement and the amount determined for the purpose of taxation. Further, the

deferred tax amount is determined on the basis of expected method in which the carrying

amount of the liabilities and assets are realised at the end of the period through the applicable

tax rate on the company (Laux 2013). The amount for deferred tax is recorded in the financial

statement up to the amount that is apparent to be available from future taxable profit against

of which the asset is usable. Amount of deferred tax assets recorded by the company under

the non-current section of balance sheet for the year ended 2017 was $ 20,65,000.

Answer (ix)

Income tax or current tax payable by the company for the year ended 2017 by XERO

Limited was amounted to $ 11,05,000. On the other hand, the income tax expenses for the

company as per the latest financial report is $ 19,87,000. Expense of income tax is the

amount the company is liable to pay as per the applicable taxation rules. However, the

payable amount of income tax is computed through applying the applicable tax rates on the

company (Melloni, Lai and Stacchezzini 2018). The income tax expense is recorded in the

income statement of the company whereas the current tax is recorded in the cash flow

statement of the company. Owing to all these differences the amount of current tax does not

match with the amount of income tax expenses.

Answer (x)

The income tax expenses for the company as per the latest financial report is $

19,87,000. On the other hand, the income tax paid as recorded in the cash flow statement of

the company was $ 20,93,000. The amount of tax expenses under the income statement of the

company varies from the amount recorded as income tax paid in the cash flow statement as

the income tax paid is the amount of tax on the operating activities of the company. On the

other hand the income tax expenses is the amount of tax applicable on the revenue of the

company left after paying off all the expenses like operating expenses, investing expenses,

selling and administration expenses and financing expenses (Maaloul and Zéghal 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 7

Answer (xi)

Difficult and confusing part – the most confusing and difficult pat was the treatment of

deferred tax. The deferred tax is recognised for the temporary difference. However, no

particular indication is mentioned that can be considered as the benchmark for temporary

differences. Whether the difference will be temporary or permanent that will be determined

on the basis of the knowledge, experience and judgement of the user. Therefore, someone

mat treat the particular difference as temporary whereas the same may be treated by someone

else as permanent. Therefore, the treatment of permanent as well as temporary difference is

not easy and confusing.

New insights – one new insight obtained from analysing the financial statement of the

company is that the income tax expenses and income tax paid by the company is not same

and not calculated or treated in the same way. The income tax paid is the amount of tax on

the operating activities of the company whereas the income tax expenses is the amount of tax

applicable on the revenue of the company left after paying off all the expenses like operating

expenses, investing expenses, selling and administration expenses and financing expenses.

Answer (xi)

Difficult and confusing part – the most confusing and difficult pat was the treatment of

deferred tax. The deferred tax is recognised for the temporary difference. However, no

particular indication is mentioned that can be considered as the benchmark for temporary

differences. Whether the difference will be temporary or permanent that will be determined

on the basis of the knowledge, experience and judgement of the user. Therefore, someone

mat treat the particular difference as temporary whereas the same may be treated by someone

else as permanent. Therefore, the treatment of permanent as well as temporary difference is

not easy and confusing.

New insights – one new insight obtained from analysing the financial statement of the

company is that the income tax expenses and income tax paid by the company is not same

and not calculated or treated in the same way. The income tax paid is the amount of tax on

the operating activities of the company whereas the income tax expenses is the amount of tax

applicable on the revenue of the company left after paying off all the expenses like operating

expenses, investing expenses, selling and administration expenses and financing expenses.

CORPORATE ACCOUNTING 8

Reference

Chang, X., Dasgupta, S., Wong, G., and Yao, J. 2014. Cash-flow sensitivities and the

allocation of internal cash flow. The Review of Financial Studies, 27(12), 3628-3657.

Laux, R. C. 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), 1357-1383.

Maaloul, A. and Zéghal, D., 2015. Financial statement informativeness and intellectual

capital disclosure: An empirical analysis. Journal of Financial Reporting and

Accounting, 13(1), pp.66-90.

Melloni, G., Lai, A. and Stacchezzini, R., 2018. Integrated reporting and narrative

accountability: The role of preparers. Accounting, Auditing and Accountability Journal, p.1.

Narotzki, D., 2017. Corporate Social Responsibility and Taxation: A Chance to Develop the

Theory.

Sarfaty, G.A., 2015. Measuring corporate accountability through global indicators. The Quiet

Power of Indicators: Measuring Governance, Corruption, and Rule of Law, p.103.

Sethi, S., 2016. Globalization and self-regulation: The crucial role that corporate codes of

conduct play in global business. Springer.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial and managerial accounting.

John Wiley and Sons.

Xero Accounting Software. 2018. Online Accounting Software – Free Trial, Free Support |

Xero. [online] Available at: https://www.xero.com/ [Accessed 21 May 2018].

Reference

Chang, X., Dasgupta, S., Wong, G., and Yao, J. 2014. Cash-flow sensitivities and the

allocation of internal cash flow. The Review of Financial Studies, 27(12), 3628-3657.

Laux, R. C. 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), 1357-1383.

Maaloul, A. and Zéghal, D., 2015. Financial statement informativeness and intellectual

capital disclosure: An empirical analysis. Journal of Financial Reporting and

Accounting, 13(1), pp.66-90.

Melloni, G., Lai, A. and Stacchezzini, R., 2018. Integrated reporting and narrative

accountability: The role of preparers. Accounting, Auditing and Accountability Journal, p.1.

Narotzki, D., 2017. Corporate Social Responsibility and Taxation: A Chance to Develop the

Theory.

Sarfaty, G.A., 2015. Measuring corporate accountability through global indicators. The Quiet

Power of Indicators: Measuring Governance, Corruption, and Rule of Law, p.103.

Sethi, S., 2016. Globalization and self-regulation: The crucial role that corporate codes of

conduct play in global business. Springer.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial and managerial accounting.

John Wiley and Sons.

Xero Accounting Software. 2018. Online Accounting Software – Free Trial, Free Support |

Xero. [online] Available at: https://www.xero.com/ [Accessed 21 May 2018].

CORPORATE ACCOUNTING 9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 10

CORPORATE ACCOUNTING 11

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.