Corporate Accounting: Analysis of Owner's Equity, Cash Flow Statement, and Accounting for Taxation of Myer Holdings Limited and Kathmandu Holdings Limited

Added on 2023-06-03

13 Pages4130 Words429 Views

1

Corporate Accounting

Name of the Student:

Name of the University:

Corporate Accounting

Name of the Student:

Name of the University:

2

Table of Contents

Corporate Accounting................................................................................................................1

Introduction................................................................................................................................3

Owner’s Equity..........................................................................................................................3

Equity items of Myer Holdings Limited................................................................................3

Equity items of Kathmandu Holdings Limited......................................................................4

Analysis for the debt equity position of the selected companies...........................................4

Cash Flow Statement..................................................................................................................4

Other comprehensive income.....................................................................................................8

Other comprehensive income statement’s items of Myer Holding Limited..........................8

Other comprehensive income statement items of Kathmandu Holding Limited...................9

Comparative analysis.............................................................................................................9

Performance evaluation by other comprehensive income.....................................................9

Accounting for corporate income tax.......................................................................................10

Tax expenses........................................................................................................................10

Effective tax rate..................................................................................................................10

Deferred tax assets/ liabilities..............................................................................................10

Change in Deferred tax liabilities........................................................................................11

Calculation of cash tax rate..................................................................................................11

Reasons for the difference between the cash tax rate and book tax rate..............................11

Conclusion................................................................................................................................11

Reference List..........................................................................................................................12

Table of Contents

Corporate Accounting................................................................................................................1

Introduction................................................................................................................................3

Owner’s Equity..........................................................................................................................3

Equity items of Myer Holdings Limited................................................................................3

Equity items of Kathmandu Holdings Limited......................................................................4

Analysis for the debt equity position of the selected companies...........................................4

Cash Flow Statement..................................................................................................................4

Other comprehensive income.....................................................................................................8

Other comprehensive income statement’s items of Myer Holding Limited..........................8

Other comprehensive income statement items of Kathmandu Holding Limited...................9

Comparative analysis.............................................................................................................9

Performance evaluation by other comprehensive income.....................................................9

Accounting for corporate income tax.......................................................................................10

Tax expenses........................................................................................................................10

Effective tax rate..................................................................................................................10

Deferred tax assets/ liabilities..............................................................................................10

Change in Deferred tax liabilities........................................................................................11

Calculation of cash tax rate..................................................................................................11

Reasons for the difference between the cash tax rate and book tax rate..............................11

Conclusion................................................................................................................................11

Reference List..........................................................................................................................12

3

Introduction

In this study, the annual report of two companies trading in Australian Securities Exchange

has been taken to carry out the study. The two companies which has been taken are

Kathmandu Holdings Limited and the other one is Myer Holdings Limited. The code in

which the company is traded in the Australian Stock Exchange is KMD and MYR for

Kathmandu Holdings Limited and Myer Holdings Limited respectively. This research paper

analyses and interprets the cash flow statement, owner’s equity and accounting for taxation of

the two companies. Analysis of owner’s equity helps to understand how the book value of the

equity of the owner has changed over a specific period of time (Coleman, Cotei and Farhat,

2016). Cash flow statement of an organization helps to understand the cash inflow and

outflow of the organization through various activities. Finally, the statement related to

accounting for taxation helps to find out various tax related information of companies.

Owner’s Equity

Equity items of Myer Holdings Limited

Retained Earnings –The accumulated profits of any organization is known as the retained

earnings. Myer Holdings Limited has an amount of $16,426,000 as contributed capital at the

end of 2016 and the end of 2017 it has a contributed capital of $49,276,000. The change in

the contributed capital is due to the profit, which has been generated by Myer Holdings

Limited in 2017.

Contributed Equity –When the shareholder pays a particular amount to get hold of the share

of that organization it is known as contributed equity. Contributed equity includes additional

paid up capital as well as paid up share capital. At the end of 2016 Myer Holdings Limited

has an amount of $739,329,000 as contributed capital whereas at the end of 2017 the

contributed capital declined to the amount of $73,329,000. The reason behind the decline of

the contributed capital is due to the issue of share capital and acquisition treasury amounting

to $187000 and $196,000 respectively.

Reserves – Any organization keep or retain a portion of the accumulated profit for further

expenses that a company may incur in the near future. At the end of 2016 the reserves of

Myer Holdings Limited were -$11,056,000 whereas at the end of 2017 the amount Myer

Holdings Limited has reserved is -$8,67,000. It can be concluded that the change in the

reserve from 2016 to 2017 due to various reasons including the share scheme provision of

employees and other comprehensive income.

Introduction

In this study, the annual report of two companies trading in Australian Securities Exchange

has been taken to carry out the study. The two companies which has been taken are

Kathmandu Holdings Limited and the other one is Myer Holdings Limited. The code in

which the company is traded in the Australian Stock Exchange is KMD and MYR for

Kathmandu Holdings Limited and Myer Holdings Limited respectively. This research paper

analyses and interprets the cash flow statement, owner’s equity and accounting for taxation of

the two companies. Analysis of owner’s equity helps to understand how the book value of the

equity of the owner has changed over a specific period of time (Coleman, Cotei and Farhat,

2016). Cash flow statement of an organization helps to understand the cash inflow and

outflow of the organization through various activities. Finally, the statement related to

accounting for taxation helps to find out various tax related information of companies.

Owner’s Equity

Equity items of Myer Holdings Limited

Retained Earnings –The accumulated profits of any organization is known as the retained

earnings. Myer Holdings Limited has an amount of $16,426,000 as contributed capital at the

end of 2016 and the end of 2017 it has a contributed capital of $49,276,000. The change in

the contributed capital is due to the profit, which has been generated by Myer Holdings

Limited in 2017.

Contributed Equity –When the shareholder pays a particular amount to get hold of the share

of that organization it is known as contributed equity. Contributed equity includes additional

paid up capital as well as paid up share capital. At the end of 2016 Myer Holdings Limited

has an amount of $739,329,000 as contributed capital whereas at the end of 2017 the

contributed capital declined to the amount of $73,329,000. The reason behind the decline of

the contributed capital is due to the issue of share capital and acquisition treasury amounting

to $187000 and $196,000 respectively.

Reserves – Any organization keep or retain a portion of the accumulated profit for further

expenses that a company may incur in the near future. At the end of 2016 the reserves of

Myer Holdings Limited were -$11,056,000 whereas at the end of 2017 the amount Myer

Holdings Limited has reserved is -$8,67,000. It can be concluded that the change in the

reserve from 2016 to 2017 due to various reasons including the share scheme provision of

employees and other comprehensive income.

4

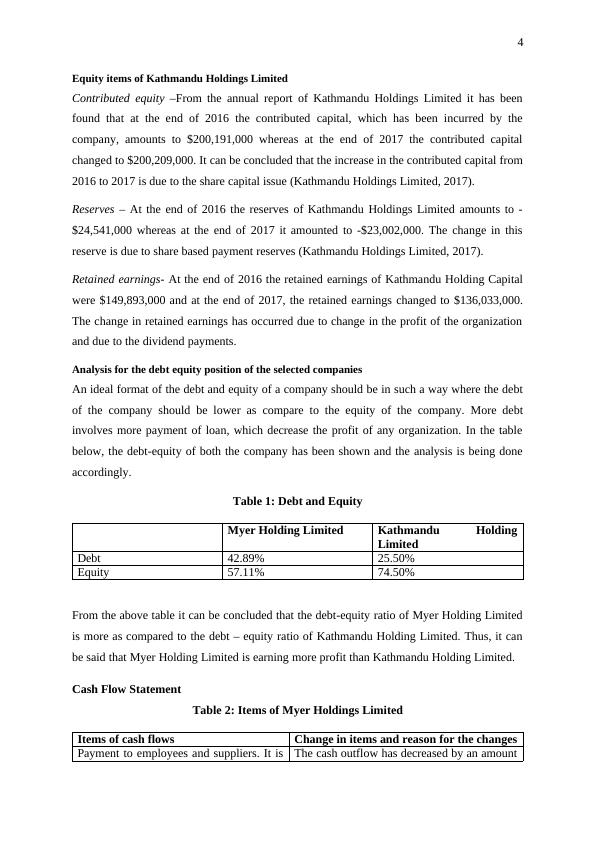

Equity items of Kathmandu Holdings Limited

Contributed equity –From the annual report of Kathmandu Holdings Limited it has been

found that at the end of 2016 the contributed capital, which has been incurred by the

company, amounts to $200,191,000 whereas at the end of 2017 the contributed capital

changed to $200,209,000. It can be concluded that the increase in the contributed capital from

2016 to 2017 is due to the share capital issue (Kathmandu Holdings Limited, 2017).

Reserves – At the end of 2016 the reserves of Kathmandu Holdings Limited amounts to -

$24,541,000 whereas at the end of 2017 it amounted to -$23,002,000. The change in this

reserve is due to share based payment reserves (Kathmandu Holdings Limited, 2017).

Retained earnings- At the end of 2016 the retained earnings of Kathmandu Holding Capital

were $149,893,000 and at the end of 2017, the retained earnings changed to $136,033,000.

The change in retained earnings has occurred due to change in the profit of the organization

and due to the dividend payments.

Analysis for the debt equity position of the selected companies

An ideal format of the debt and equity of a company should be in such a way where the debt

of the company should be lower as compare to the equity of the company. More debt

involves more payment of loan, which decrease the profit of any organization. In the table

below, the debt-equity of both the company has been shown and the analysis is being done

accordingly.

Table 1: Debt and Equity

Myer Holding Limited Kathmandu Holding Limited

Debt 42.89% 25.50%

Equity 57.11% 74.50%

From the above table it can be concluded that the debt-equity ratio of Myer Holding Limited

is more as compared to the debt – equity ratio of Kathmandu Holding Limited. Thus, it can

be said that Myer Holding Limited is earning more profit than Kathmandu Holding Limited.

Cash Flow Statement

Table 2: Items of Myer Holdings Limited

Items of cash flows Change in items and reason for the changes

Payment to employees and suppliers. It is the The cash outflow has decreased by an amount of

Equity items of Kathmandu Holdings Limited

Contributed equity –From the annual report of Kathmandu Holdings Limited it has been

found that at the end of 2016 the contributed capital, which has been incurred by the

company, amounts to $200,191,000 whereas at the end of 2017 the contributed capital

changed to $200,209,000. It can be concluded that the increase in the contributed capital from

2016 to 2017 is due to the share capital issue (Kathmandu Holdings Limited, 2017).

Reserves – At the end of 2016 the reserves of Kathmandu Holdings Limited amounts to -

$24,541,000 whereas at the end of 2017 it amounted to -$23,002,000. The change in this

reserve is due to share based payment reserves (Kathmandu Holdings Limited, 2017).

Retained earnings- At the end of 2016 the retained earnings of Kathmandu Holding Capital

were $149,893,000 and at the end of 2017, the retained earnings changed to $136,033,000.

The change in retained earnings has occurred due to change in the profit of the organization

and due to the dividend payments.

Analysis for the debt equity position of the selected companies

An ideal format of the debt and equity of a company should be in such a way where the debt

of the company should be lower as compare to the equity of the company. More debt

involves more payment of loan, which decrease the profit of any organization. In the table

below, the debt-equity of both the company has been shown and the analysis is being done

accordingly.

Table 1: Debt and Equity

Myer Holding Limited Kathmandu Holding Limited

Debt 42.89% 25.50%

Equity 57.11% 74.50%

From the above table it can be concluded that the debt-equity ratio of Myer Holding Limited

is more as compared to the debt – equity ratio of Kathmandu Holding Limited. Thus, it can

be said that Myer Holding Limited is earning more profit than Kathmandu Holding Limited.

Cash Flow Statement

Table 2: Items of Myer Holdings Limited

Items of cash flows Change in items and reason for the changes

Payment to employees and suppliers. It is the The cash outflow has decreased by an amount of

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Corporate Accounting Analysis of Myer Holding and Kathmandu Holdings Ltdlg...

|18

|4290

|486

Financial Analysis and Evaluation of Myer and Kathmandu Holding Limitedlg...

|16

|4029

|385

Corporate Accounting: Analysis of Myer Holdings and Kathmandu Holdings Limitedlg...

|31

|3496

|244

Corporate Accounting: Comparative Analysis of Myer Holdings Limited and Kathmandu Holdings Limitedlg...

|24

|5133

|492

Corporate Accounting: Process and Importance in Organizationslg...

|18

|4140

|468

Corporate Accounting: PDFlg...

|19

|5194

|233