Corporate Accounting and Financial Reporting: Lease Accounting Report

VerifiedAdded on 2021/05/31

|8

|1428

|28

Report

AI Summary

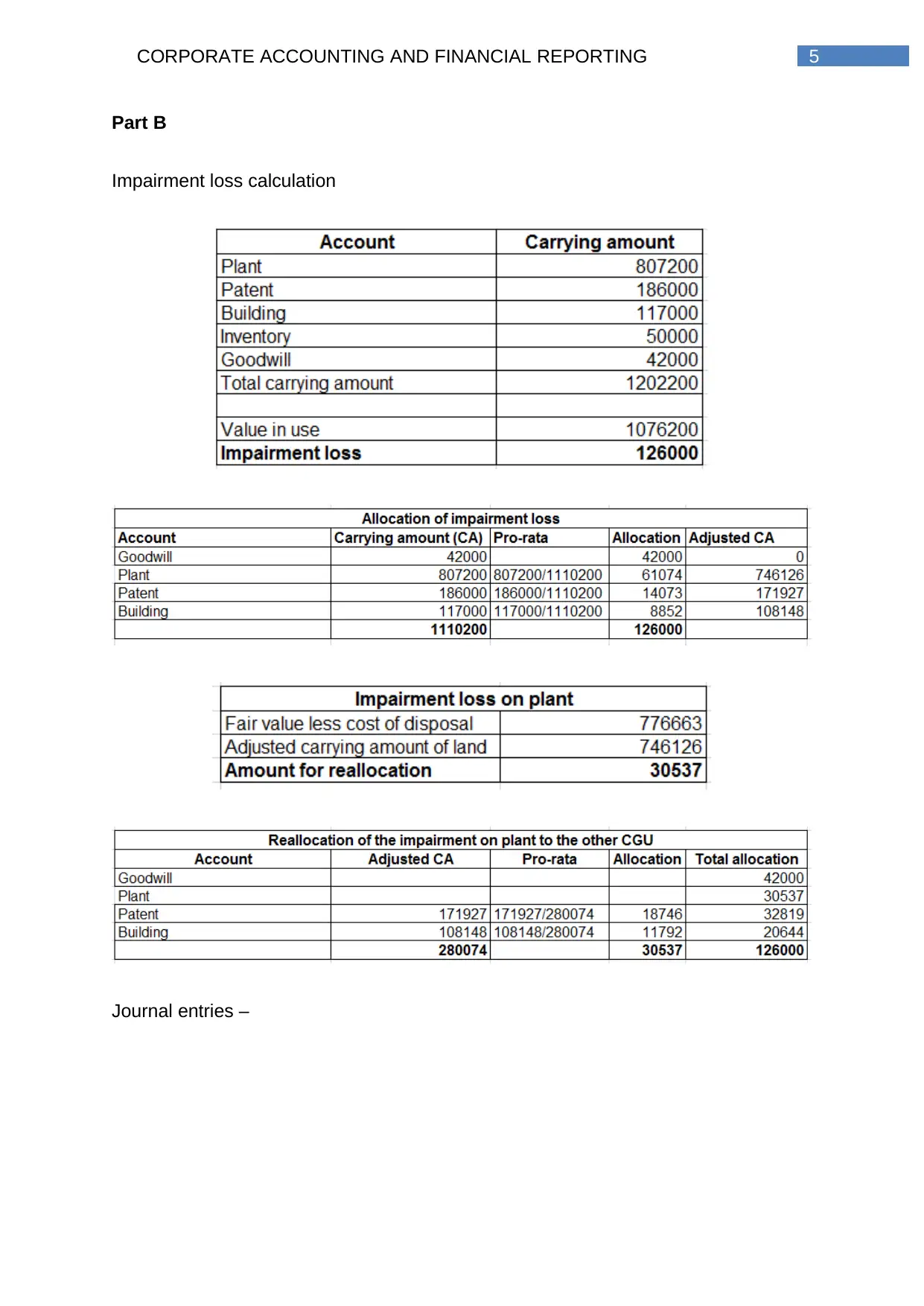

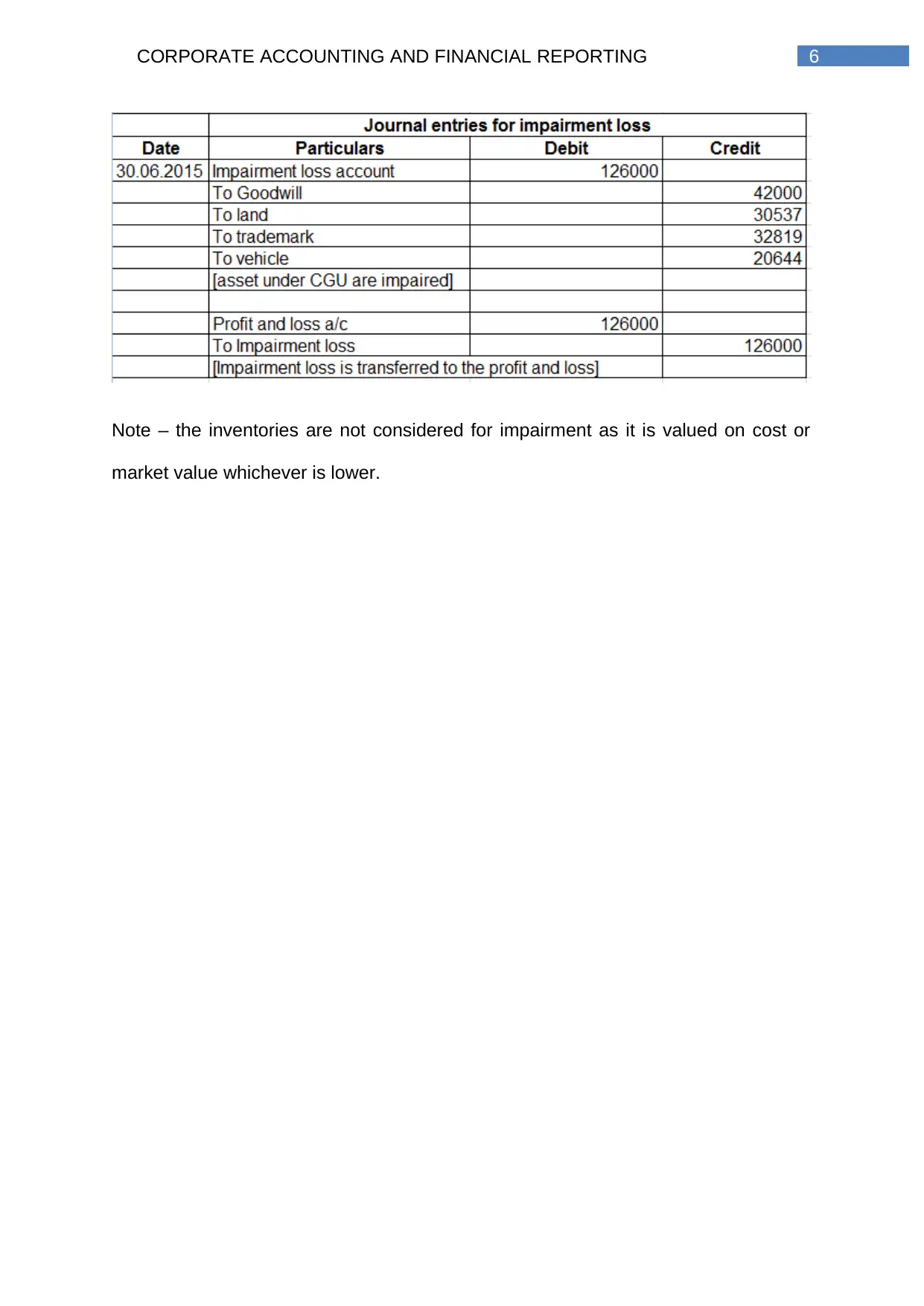

This report provides a comprehensive overview of corporate accounting and financial reporting, specifically focusing on accounting for finance leases by lessees. It defines a lease and explains the roles of the lessor and lessee, emphasizing the legal obligations involved. The report details the lessee's analysis of lease liabilities and right-to-use assets at the lease's inception, including the calculation of lease liability using present value and the incremental borrowing rate. It outlines the ongoing accounting procedures for finance leases, such as amortization of the right-to-use asset and interest on lease liability, and the treatment of impairment and variable lease payments. The report references AASB 16 and discusses the criteria for classifying a lease as a finance lease versus an operating lease, highlighting factors like risk and reward transfer. It also explains the components of lease payments, including fixed and variable payments, and the reporting of leases in financial statements, including the income statement, balance sheet, and cash flow statement. The report covers disclosure requirements, including both qualitative and quantitative information, and concludes with a discussion of impairment loss calculations and journal entries, excluding inventories. The report draws on several academic references to support its analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.