Accounting Report: Analysis of Impairment of Assets under IAS 36

VerifiedAdded on 2020/06/06

|9

|2003

|36

Report

AI Summary

This report provides a detailed analysis of the impairment of assets under IAS 36, focusing on the mandatory standards for financial reporting. It explains the circumstances under which an impairment test must be conducted, emphasizing the importance of determining the recoverable amount, which i...

Corporate Accounting

and Reporting

and Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

Index of Tables

Table 1 Calculation of impairment loss against all the assets in CGU...........................................4

Table 2 Allocation of extra impairment loss of patent on other assets in CGU..............................5

Table 3 Journal entry of Gali Ltd...................................................................................................5

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

Index of Tables

Table 1 Calculation of impairment loss against all the assets in CGU...........................................4

Table 2 Allocation of extra impairment loss of patent on other assets in CGU..............................5

Table 3 Journal entry of Gali Ltd...................................................................................................5

INTRODUCTION

According to the Company Act of Australia, every firm is mandatory obliged to prepare

accounts and publish it after auditing. In the globalized world, firms need to comply with

international accounting and reporting standard to prepare their annual statements. IAS 36 lay

down rules and regulations on impairment of assets that entities follow to assure that assets are

not carry forwarded beyond its recoverable amount. The current research thoroughly explains the

circumstances when an impairment test must be carry out and make journal entries for the

impairment loss with supporting calculations.

PART A

IAS 36, impairment of assets sets out the mandatory standards that company need to

comply with for reporting their assets. It states that every firm need to reduce their assets

carrying value to its recoverable amount (Buschhüter and Striegel, 2011). Here, recoverable

amount is the amount that is higher of the following:

Arm length price: Fair value less disposal cost/cost of sell

Value in use: It is the potential cash inflows that an asset expects to generate, the amount

is discounted to reflect its present value at an appropriate discounting rate (Husmann and

Schmidt, 2008).

The key principle of the IAS 36 is that any asssets in the financial statement cannot be

carried forwarded more than its expected recoverable price though its sales or use. If in any

circumstance, the carrying amount of assets exceeds the recoverable money, then, such assets is

called impaired. Amount by which carrying value is reducing to its recoverable price is

recognizing as impairment loss. The standard also applies on the group of assets that do not

generate cash inflows separately or individually, called cash generating units (CGU). The

standard applies for many assets except those on which, other specific standard applies such as

inventory, financial assets under IFRS 9, investment property, biological assets, deferred tax

assets, assets from employee benefits, non-current assets available for sale.

Page 1 of 9

According to the Company Act of Australia, every firm is mandatory obliged to prepare

accounts and publish it after auditing. In the globalized world, firms need to comply with

international accounting and reporting standard to prepare their annual statements. IAS 36 lay

down rules and regulations on impairment of assets that entities follow to assure that assets are

not carry forwarded beyond its recoverable amount. The current research thoroughly explains the

circumstances when an impairment test must be carry out and make journal entries for the

impairment loss with supporting calculations.

PART A

IAS 36, impairment of assets sets out the mandatory standards that company need to

comply with for reporting their assets. It states that every firm need to reduce their assets

carrying value to its recoverable amount (Buschhüter and Striegel, 2011). Here, recoverable

amount is the amount that is higher of the following:

Arm length price: Fair value less disposal cost/cost of sell

Value in use: It is the potential cash inflows that an asset expects to generate, the amount

is discounted to reflect its present value at an appropriate discounting rate (Husmann and

Schmidt, 2008).

The key principle of the IAS 36 is that any asssets in the financial statement cannot be

carried forwarded more than its expected recoverable price though its sales or use. If in any

circumstance, the carrying amount of assets exceeds the recoverable money, then, such assets is

called impaired. Amount by which carrying value is reducing to its recoverable price is

recognizing as impairment loss. The standard also applies on the group of assets that do not

generate cash inflows separately or individually, called cash generating units (CGU). The

standard applies for many assets except those on which, other specific standard applies such as

inventory, financial assets under IFRS 9, investment property, biological assets, deferred tax

assets, assets from employee benefits, non-current assets available for sale.

Page 1 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to the standard, establishment needs to conduct an annual impairment test for

intangible assets and business goodwill as well. As per the standard, it is mandatory for the

company to carry out impairment assets every year for the following:

Intangible assets that have indefinite useful lives

All the intangible assets of the business entity that is not yet available for the use

Goodwill that is the result of business combination

For all above-mentioned assets, there is no requirement of any evidence or indication of

impairment. However, other assets requires performing an impairment test when, there is an

evidence of impairment available. As per the standard, whenever an asset is being impaired, then

the amount is recognizing immediately as profit or loss in the statement of comprehensive

income (Impairment Accounting – The Basics of IAS 36 Impairment of Assets, 2008). In CGU, it

is necessary to reduce goodwill first and thereafter, other assets are reduced based on pro-rata

allotment. Assets that are subjected to depreciation is adjusted in future years so as to allocate its

revised carrying value over its remaining useful life. Notably, the impairment loss on the

goodwill cannot be reverse whereas other assets loss can be favorably resolved by reversing the

loss in the profit and loss account, on reversal, carrying value is increases.

Australian Accounting Standard Board (AASB) 136 states that the indication of

impairment can found from either of internal or external sources that are present here as under:

External sources:

Decline in market value

Adverse/unfavorable changes in the entity’s market

Increase in the interest rate

Net assets of the company above market capitalization

Internal sources:

Physical change or Obsolescence

Part of restructuring, idle assets or held for disposal

If an assets perform worse than expectation

Page 2 of 9

intangible assets and business goodwill as well. As per the standard, it is mandatory for the

company to carry out impairment assets every year for the following:

Intangible assets that have indefinite useful lives

All the intangible assets of the business entity that is not yet available for the use

Goodwill that is the result of business combination

For all above-mentioned assets, there is no requirement of any evidence or indication of

impairment. However, other assets requires performing an impairment test when, there is an

evidence of impairment available. As per the standard, whenever an asset is being impaired, then

the amount is recognizing immediately as profit or loss in the statement of comprehensive

income (Impairment Accounting – The Basics of IAS 36 Impairment of Assets, 2008). In CGU, it

is necessary to reduce goodwill first and thereafter, other assets are reduced based on pro-rata

allotment. Assets that are subjected to depreciation is adjusted in future years so as to allocate its

revised carrying value over its remaining useful life. Notably, the impairment loss on the

goodwill cannot be reverse whereas other assets loss can be favorably resolved by reversing the

loss in the profit and loss account, on reversal, carrying value is increases.

Australian Accounting Standard Board (AASB) 136 states that the indication of

impairment can found from either of internal or external sources that are present here as under:

External sources:

Decline in market value

Adverse/unfavorable changes in the entity’s market

Increase in the interest rate

Net assets of the company above market capitalization

Internal sources:

Physical change or Obsolescence

Part of restructuring, idle assets or held for disposal

If an assets perform worse than expectation

Page 2 of 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If investment in joint venture, associates and subsidiaries, carrying amount exceeds

investee’s assets or dividend goes beyond investee’s total comprehensive income

The standard recognizes impairment loss when recoverable amount fall below the

carrying value. The loss on impairment treats as an expense unless it is relate to such assets, that

impairment loss on revaluation treated as revaluation decrease.

CGU is defined as the smallest group of identifiable assets that are obtaining cash flow

from its continual use and which is independent of cash inflows from the other assets of the

enterprise (Wittsiepe, 2008). With reference to CGU, AASB 136 allows establishment to use a

segment as CGU where the segment is equal to the smallest assets group that are deriving

independent cash flows. Within the CGU< if there is no goodwill amount and company

recognize an impairment loss then such loss is assigned across all of the assets that are the part of

CGU on pro-rate basis using carrying value of each separate assets in relation to the total

carrying amount of CGU. Its impairment losses treat similarly to that of individual business

assets. However, on the other side, when a CGU includes goodwill also, than in line with the

AASB 136 goodwill’s carrying amount is reduced to the possible extent means zero and other

assets on pro-rata basis (IAS 36 Impairment of Assets, 2017).

AASB 136 presents key disclosure requirements for impairment loss in the annual

account of the business unit, that are presented here as under:

The amount recognized as impairment loss must disclose in the profit or loss account.

Any reversal of the loss should recognize in profit or loss account.

Impairment loss on the assets that revalued earlier must recognize directly in the business

equity during the period.

Any reversal of impairment loss on revalued assets needs to be report directly in equity in

relevant period.

PART B

According to the scenario, Gali Ltd had determined its Fine China division as Cash

Generating Unit (CGU) contains number of assets including building, patent, fittings, inventory

and goodwill. As per AASB 136, impairment test needs to be perform to determine the amount

Page 3 of 9

investee’s assets or dividend goes beyond investee’s total comprehensive income

The standard recognizes impairment loss when recoverable amount fall below the

carrying value. The loss on impairment treats as an expense unless it is relate to such assets, that

impairment loss on revaluation treated as revaluation decrease.

CGU is defined as the smallest group of identifiable assets that are obtaining cash flow

from its continual use and which is independent of cash inflows from the other assets of the

enterprise (Wittsiepe, 2008). With reference to CGU, AASB 136 allows establishment to use a

segment as CGU where the segment is equal to the smallest assets group that are deriving

independent cash flows. Within the CGU< if there is no goodwill amount and company

recognize an impairment loss then such loss is assigned across all of the assets that are the part of

CGU on pro-rate basis using carrying value of each separate assets in relation to the total

carrying amount of CGU. Its impairment losses treat similarly to that of individual business

assets. However, on the other side, when a CGU includes goodwill also, than in line with the

AASB 136 goodwill’s carrying amount is reduced to the possible extent means zero and other

assets on pro-rata basis (IAS 36 Impairment of Assets, 2017).

AASB 136 presents key disclosure requirements for impairment loss in the annual

account of the business unit, that are presented here as under:

The amount recognized as impairment loss must disclose in the profit or loss account.

Any reversal of the loss should recognize in profit or loss account.

Impairment loss on the assets that revalued earlier must recognize directly in the business

equity during the period.

Any reversal of impairment loss on revalued assets needs to be report directly in equity in

relevant period.

PART B

According to the scenario, Gali Ltd had determined its Fine China division as Cash

Generating Unit (CGU) contains number of assets including building, patent, fittings, inventory

and goodwill. As per AASB 136, impairment test needs to be perform to determine the amount

Page 3 of 9

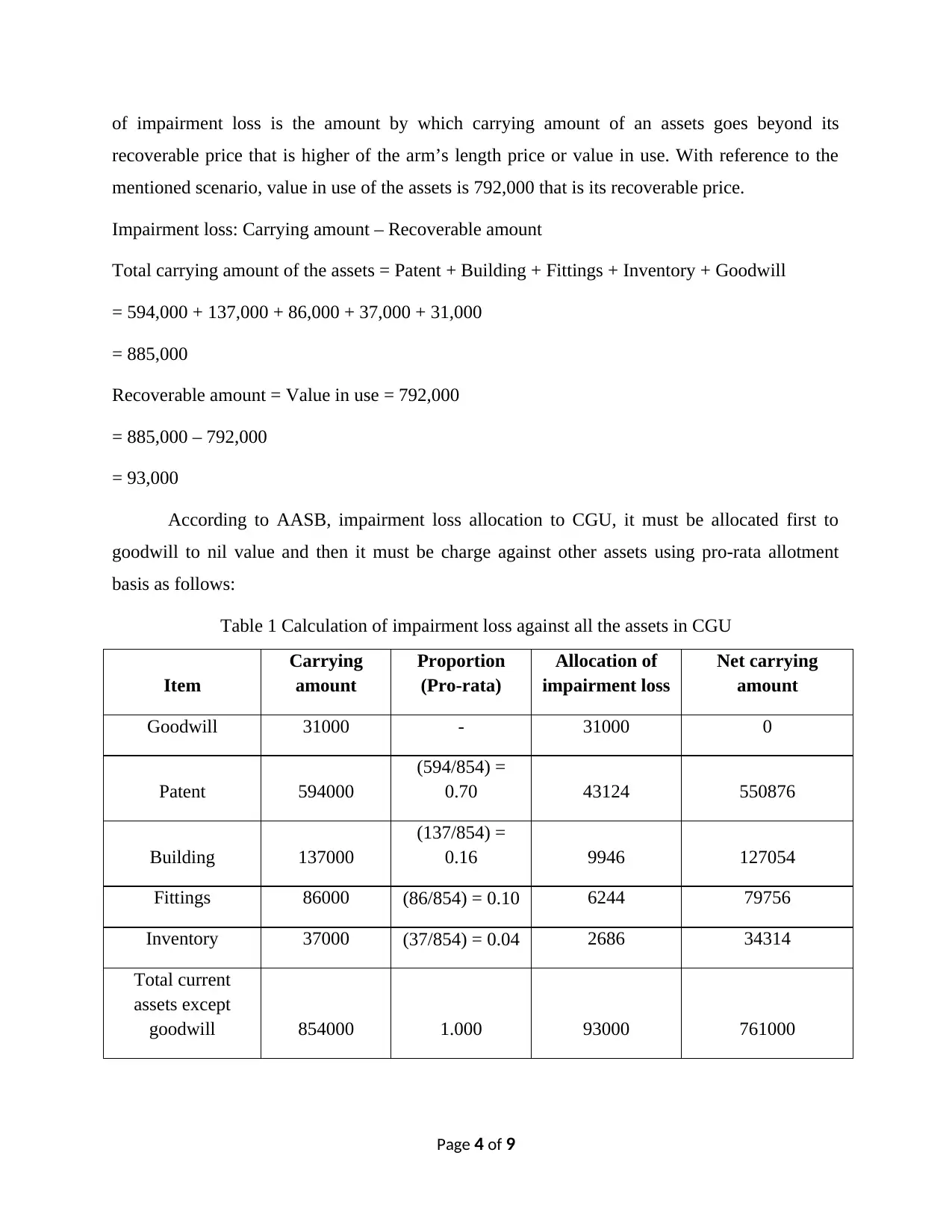

of impairment loss is the amount by which carrying amount of an assets goes beyond its

recoverable price that is higher of the arm’s length price or value in use. With reference to the

mentioned scenario, value in use of the assets is 792,000 that is its recoverable price.

Impairment loss: Carrying amount – Recoverable amount

Total carrying amount of the assets = Patent + Building + Fittings + Inventory + Goodwill

= 594,000 + 137,000 + 86,000 + 37,000 + 31,000

= 885,000

Recoverable amount = Value in use = 792,000

= 885,000 – 792,000

= 93,000

According to AASB, impairment loss allocation to CGU, it must be allocated first to

goodwill to nil value and then it must be charge against other assets using pro-rata allotment

basis as follows:

Table 1 Calculation of impairment loss against all the assets in CGU

Item

Carrying

amount

Proportion

(Pro-rata)

Allocation of

impairment loss

Net carrying

amount

Goodwill 31000 - 31000 0

Patent 594000

(594/854) =

0.70 43124 550876

Building 137000

(137/854) =

0.16 9946 127054

Fittings 86000 (86/854) = 0.10 6244 79756

Inventory 37000 (37/854) = 0.04 2686 34314

Total current

assets except

goodwill 854000 1.000 93000 761000

Page 4 of 9

recoverable price that is higher of the arm’s length price or value in use. With reference to the

mentioned scenario, value in use of the assets is 792,000 that is its recoverable price.

Impairment loss: Carrying amount – Recoverable amount

Total carrying amount of the assets = Patent + Building + Fittings + Inventory + Goodwill

= 594,000 + 137,000 + 86,000 + 37,000 + 31,000

= 885,000

Recoverable amount = Value in use = 792,000

= 885,000 – 792,000

= 93,000

According to AASB, impairment loss allocation to CGU, it must be allocated first to

goodwill to nil value and then it must be charge against other assets using pro-rata allotment

basis as follows:

Table 1 Calculation of impairment loss against all the assets in CGU

Item

Carrying

amount

Proportion

(Pro-rata)

Allocation of

impairment loss

Net carrying

amount

Goodwill 31000 - 31000 0

Patent 594000

(594/854) =

0.70 43124 550876

Building 137000

(137/854) =

0.16 9946 127054

Fittings 86000 (86/854) = 0.10 6244 79756

Inventory 37000 (37/854) = 0.04 2686 34314

Total current

assets except

goodwill 854000 1.000 93000 761000

Page 4 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

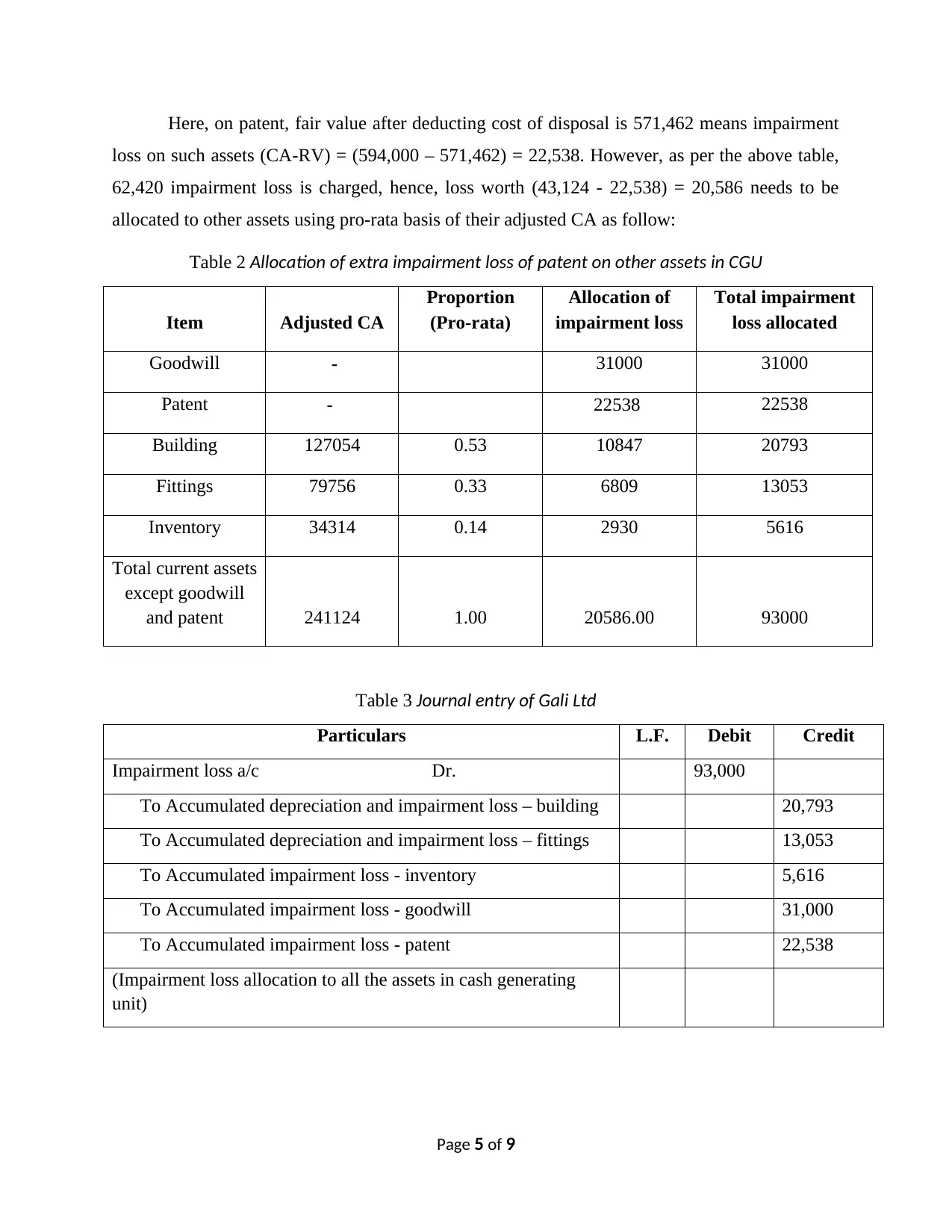

Here, on patent, fair value after deducting cost of disposal is 571,462 means impairment

loss on such assets (CA-RV) = (594,000 – 571,462) = 22,538. However, as per the above table,

62,420 impairment loss is charged, hence, loss worth (43,124 - 22,538) = 20,586 needs to be

allocated to other assets using pro-rata basis of their adjusted CA as follow:

Table 2 Allocation of extra impairment loss of patent on other assets in CGU

Item Adjusted CA

Proportion

(Pro-rata)

Allocation of

impairment loss

Total impairment

loss allocated

Goodwill - 31000 31000

Patent - 22538 22538

Building 127054 0.53 10847 20793

Fittings 79756 0.33 6809 13053

Inventory 34314 0.14 2930 5616

Total current assets

except goodwill

and patent 241124 1.00 20586.00 93000

Table 3 Journal entry of Gali Ltd

Particulars L.F. Debit Credit

Impairment loss a/c Dr. 93,000

To Accumulated depreciation and impairment loss – building 20,793

To Accumulated depreciation and impairment loss – fittings 13,053

To Accumulated impairment loss - inventory 5,616

To Accumulated impairment loss - goodwill 31,000

To Accumulated impairment loss - patent 22,538

(Impairment loss allocation to all the assets in cash generating

unit)

Page 5 of 9

loss on such assets (CA-RV) = (594,000 – 571,462) = 22,538. However, as per the above table,

62,420 impairment loss is charged, hence, loss worth (43,124 - 22,538) = 20,586 needs to be

allocated to other assets using pro-rata basis of their adjusted CA as follow:

Table 2 Allocation of extra impairment loss of patent on other assets in CGU

Item Adjusted CA

Proportion

(Pro-rata)

Allocation of

impairment loss

Total impairment

loss allocated

Goodwill - 31000 31000

Patent - 22538 22538

Building 127054 0.53 10847 20793

Fittings 79756 0.33 6809 13053

Inventory 34314 0.14 2930 5616

Total current assets

except goodwill

and patent 241124 1.00 20586.00 93000

Table 3 Journal entry of Gali Ltd

Particulars L.F. Debit Credit

Impairment loss a/c Dr. 93,000

To Accumulated depreciation and impairment loss – building 20,793

To Accumulated depreciation and impairment loss – fittings 13,053

To Accumulated impairment loss - inventory 5,616

To Accumulated impairment loss - goodwill 31,000

To Accumulated impairment loss - patent 22,538

(Impairment loss allocation to all the assets in cash generating

unit)

Page 5 of 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the findings of the study, it is clear that AASB 136 and IAS 36 necessitates for the

enterprises to conduct impairment test per year for the intangible assets with indefinite useful

lives, not available for use and goodwill in business combination. In order to find out impairment

loss, recoverable amount (higher of FV-cost of sale or value in use) is compare with carrying

amount and to the extent to which, CA> RV is recognized as loss in profit or loss account.

Although assets are allocate on pro-rata basis, however, if CGU comprises any amount for

goodwill, then, its value must be charge first for impairment loss and thereafter, remainder assets

carrying amount is used. According to the result, total impairment loss of 93,000 is charged

against building by 20,793, fittings by 13,053, inventory by 5,616, goodwill by 31,000 and

patent by 22,538 respectively.

Page 6 of 9

From the findings of the study, it is clear that AASB 136 and IAS 36 necessitates for the

enterprises to conduct impairment test per year for the intangible assets with indefinite useful

lives, not available for use and goodwill in business combination. In order to find out impairment

loss, recoverable amount (higher of FV-cost of sale or value in use) is compare with carrying

amount and to the extent to which, CA> RV is recognized as loss in profit or loss account.

Although assets are allocate on pro-rata basis, however, if CGU comprises any amount for

goodwill, then, its value must be charge first for impairment loss and thereafter, remainder assets

carrying amount is used. According to the result, total impairment loss of 93,000 is charged

against building by 20,793, fittings by 13,053, inventory by 5,616, goodwill by 31,000 and

patent by 22,538 respectively.

Page 6 of 9

REFERENCES

Books and Journals

Buschhüter, M. and Striegel, A., 2011. IAS 36–Impairment of Assets. In Kommentar

Internationale Rechnungslegung IFRS. Gabler. 15(4). pp. 888-954.

Husmann, S. and Schmidt, M., 2008. The discount rate: A note on IAS 36. Accounting in

Europe. 5(1). pp.49-62.

Wittsiepe, R., 2008. IAS 36—Impairment of Assets. IFRS for Small and Medium-Sized

Enterprises: Structuring the Transition Process. 14(3). pp.140-155.

Online

IAS 36 Impairment of Assets. 2017. [Online]. Available through: <

https://www.iasplus.com/en/standards/ias/ias36>.

Impairment Accounting – The Basics of IAS 36 Impairment of Assets. 2008. [PDF]. Available

through: <

http://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_

36_Impairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf>.

Page 7 of 9

Books and Journals

Buschhüter, M. and Striegel, A., 2011. IAS 36–Impairment of Assets. In Kommentar

Internationale Rechnungslegung IFRS. Gabler. 15(4). pp. 888-954.

Husmann, S. and Schmidt, M., 2008. The discount rate: A note on IAS 36. Accounting in

Europe. 5(1). pp.49-62.

Wittsiepe, R., 2008. IAS 36—Impairment of Assets. IFRS for Small and Medium-Sized

Enterprises: Structuring the Transition Process. 14(3). pp.140-155.

Online

IAS 36 Impairment of Assets. 2017. [Online]. Available through: <

https://www.iasplus.com/en/standards/ias/ias36>.

Impairment Accounting – The Basics of IAS 36 Impairment of Assets. 2008. [PDF]. Available

through: <

http://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_

36_Impairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf>.

Page 7 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.