Corporate Accounting and Reporting: Acquisition and Goodwill Analysis

VerifiedAdded on 2022/11/09

|8

|921

|489

Report

AI Summary

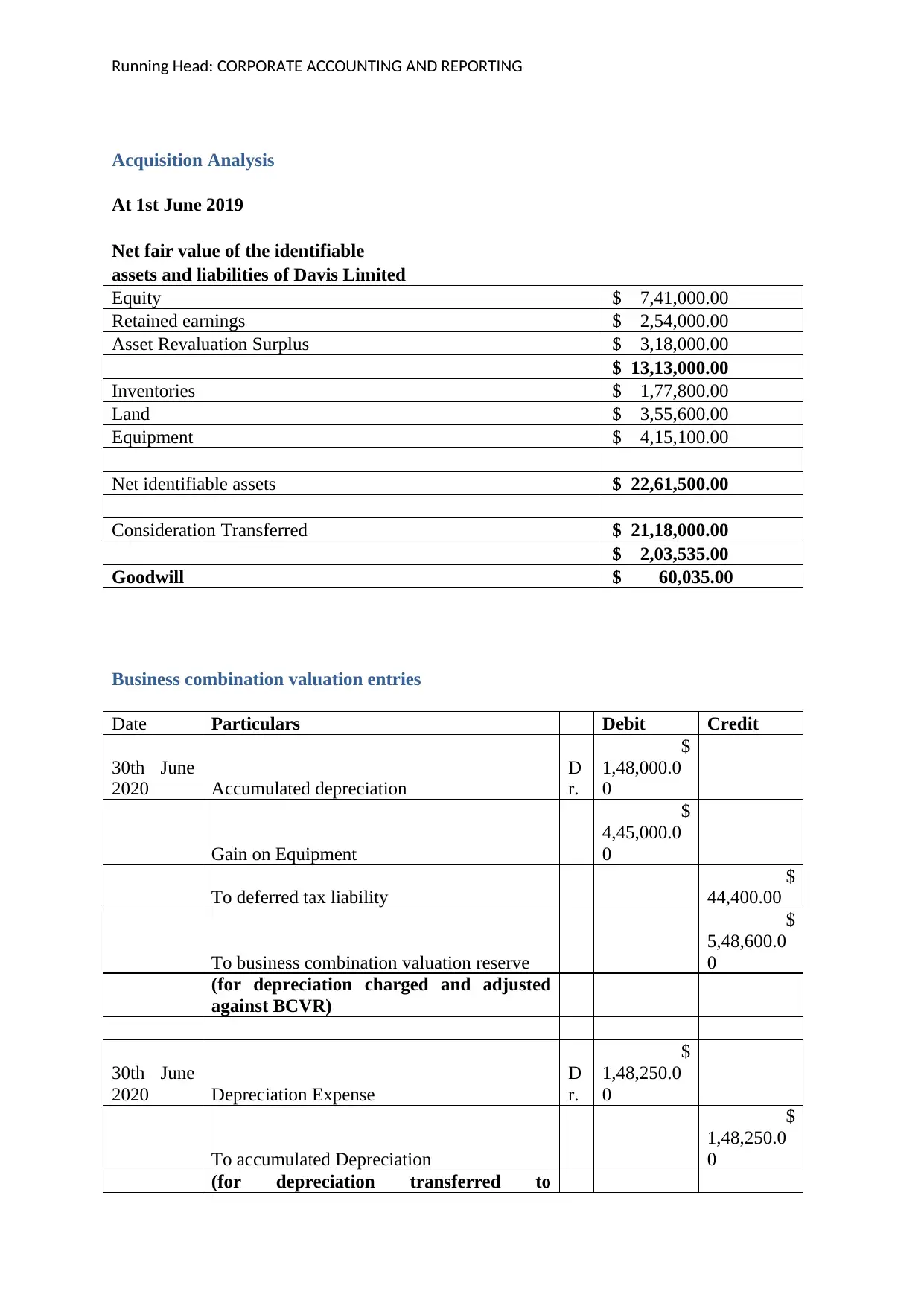

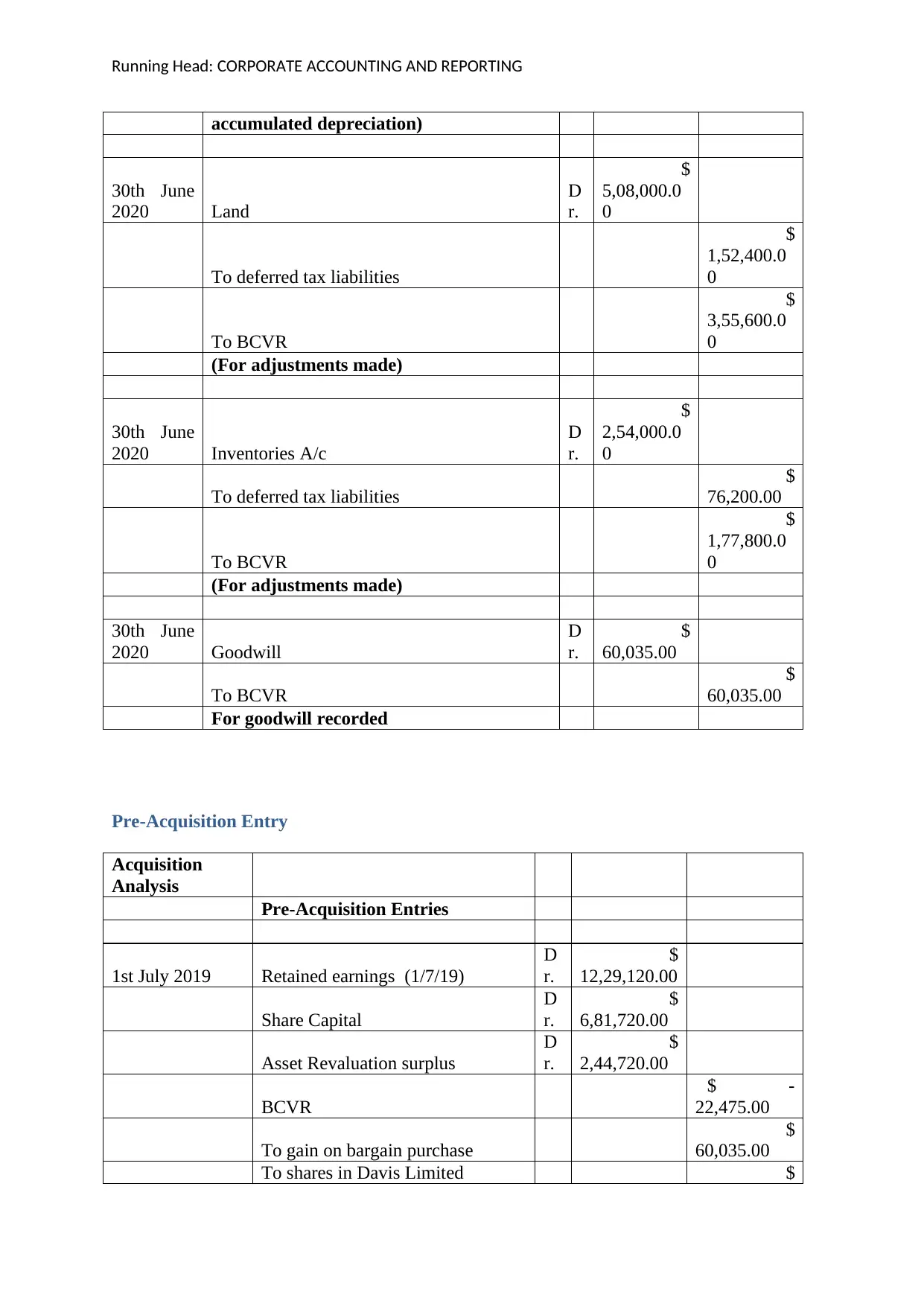

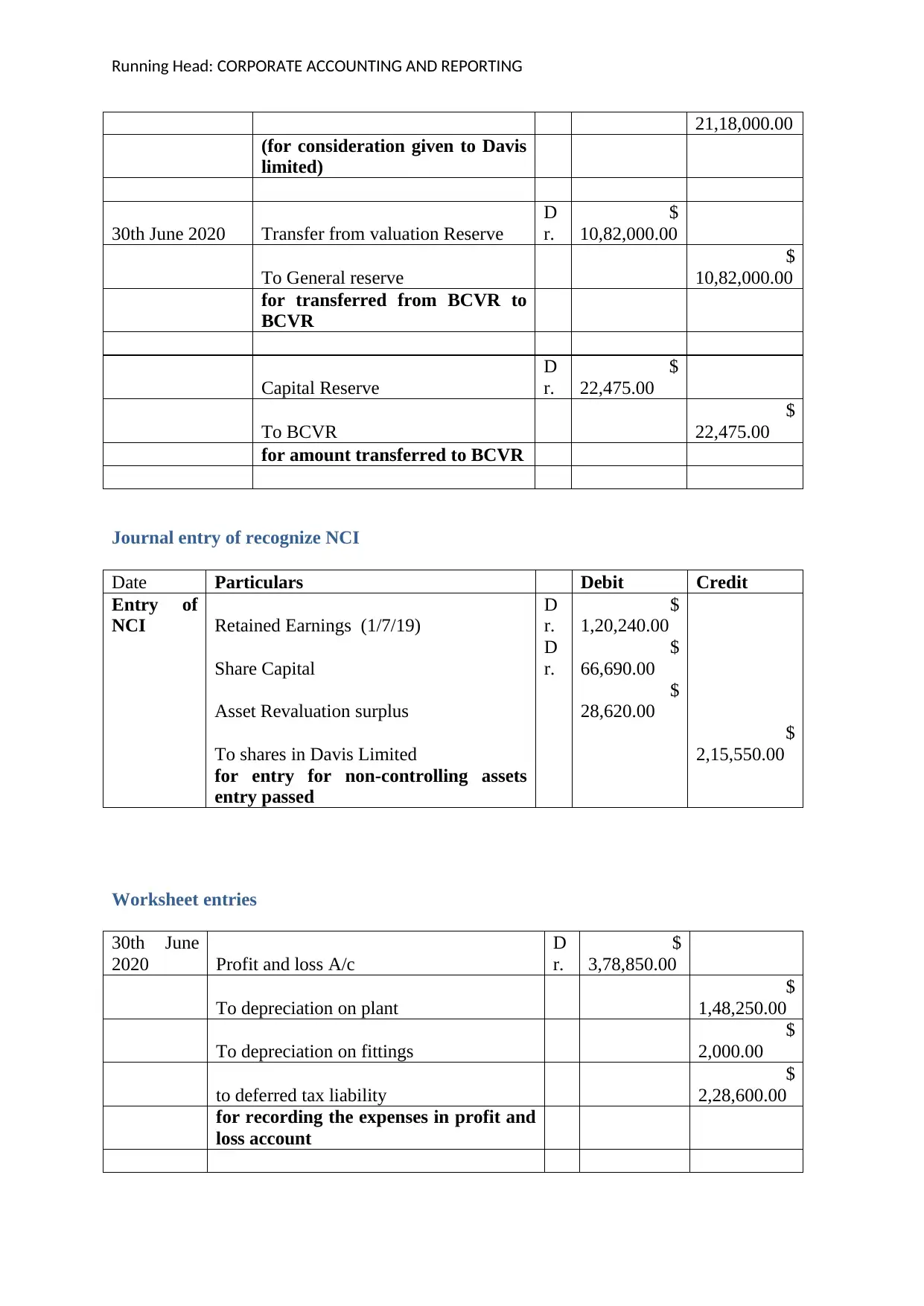

This report provides a detailed analysis of corporate accounting and reporting, focusing on business combinations, acquisition analysis, and goodwill. It includes a table of contents, followed by an examination of acquisition analysis, detailing the net fair value of identifiable assets and liabilities, consideration transferred, and goodwill calculation. The report then presents business combination valuation entries, pre-acquisition entries, and journal entries for recognizing non-controlling interests (NCI). Worksheet entries and an explanation of goodwill are also included, clarifying its role as an intangible asset and the methods for its calculation. The report concludes with references, offering a comprehensive overview of corporate accounting practices.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.