Corporate Accounting and Reporting Assignment: Impairment

VerifiedAdded on 2020/04/07

|8

|1768

|73

Homework Assignment

AI Summary

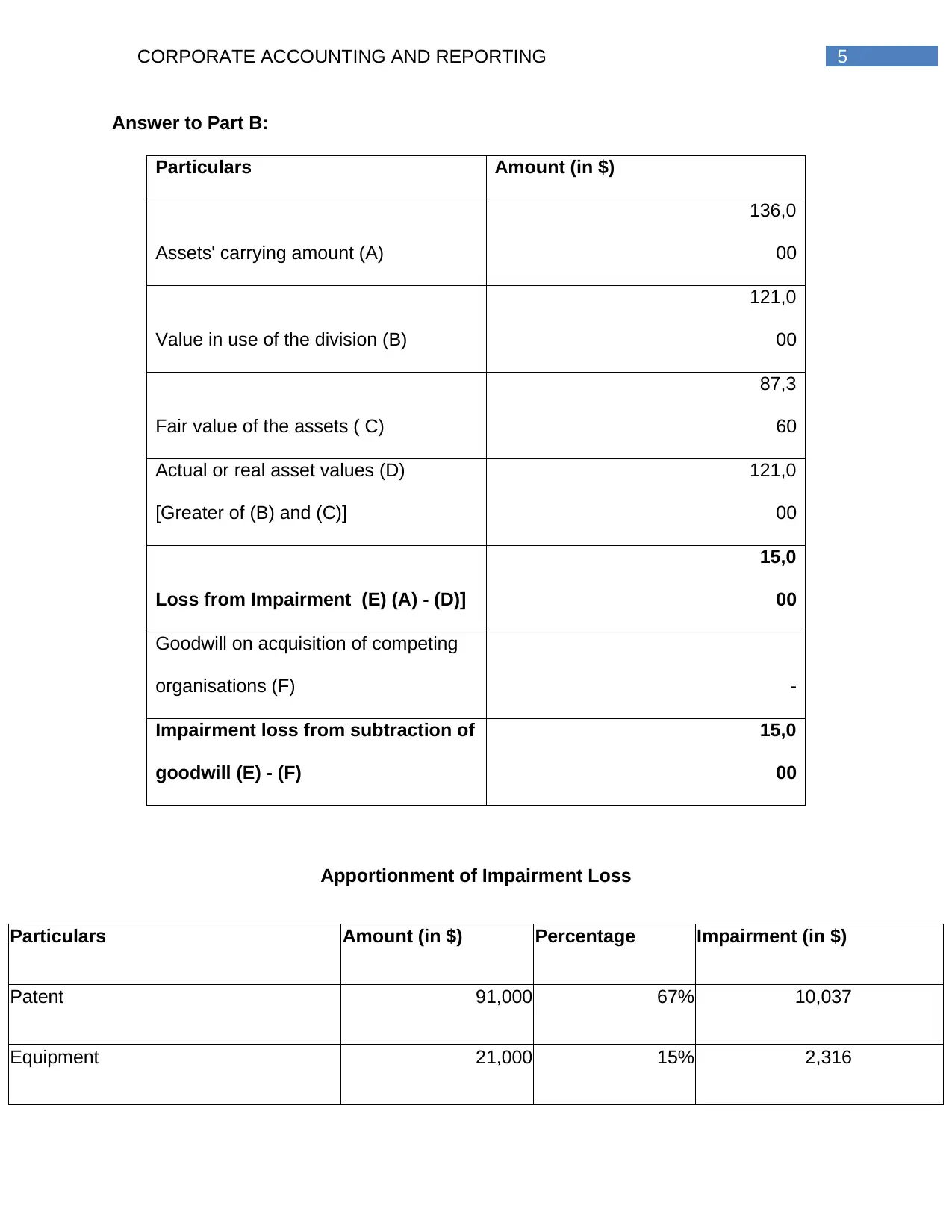

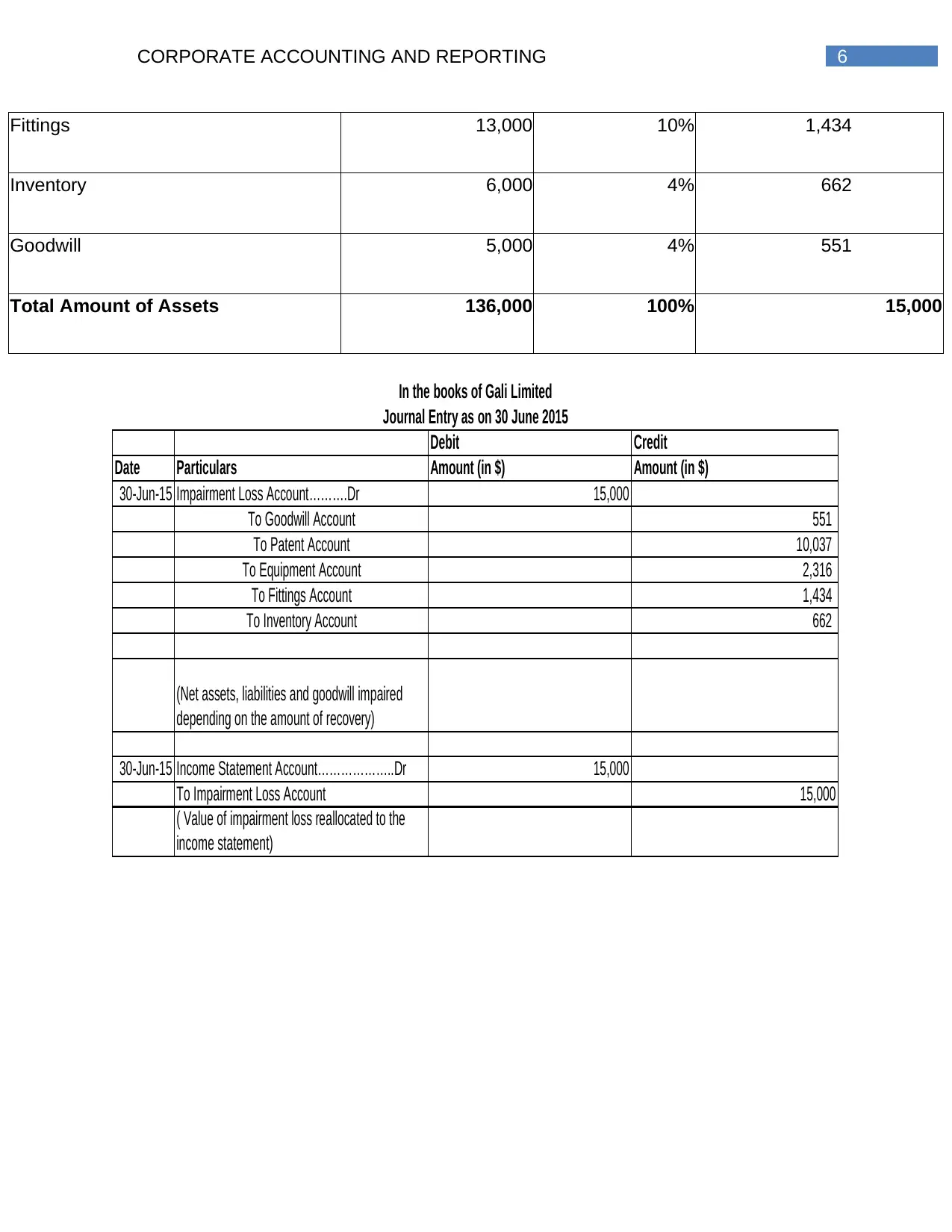

This document presents a detailed solution to a corporate accounting assignment, focusing on the impairment of assets. The solution begins by explaining the key accounting principles related to asset valuation and impairment as per AASB 136, including the concepts of recoverable value and impairment loss. It describes the two primary methods for asset impairment: the revaluation model and the cost model, outlining how impairment losses are recognized under each model. The document also addresses impairment loss reversal, detailing the conditions and procedures for reversing impairment losses under both models. The solution further includes a practical example demonstrating the reversal of impairment loss using the cost model. Part B of the assignment provides a breakdown of an impairment loss calculation, including the apportionment of the loss across different asset categories such as patents, equipment, and goodwill. The assignment references relevant accounting standards and provides a clear understanding of how to account for and report asset impairment in financial statements.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.