Corporate Accounting Analysis: Financial Performance of Companies

VerifiedAdded on 2020/10/05

|17

|5220

|357

Report

AI Summary

This report presents a detailed corporate accounting analysis of three companies: Clean Seas Seafood Limited, Bellamys Australia Limited, and Elders Limited. The analysis begins with an examination of equity, including share capital, share rights reserves, and accumulated losses, over a three-year period, providing percentage changes and comparative insights. The report then delves into the calculation and interpretation of liabilities, including trade payables, borrowings, and provisions, highlighting significant changes and their implications for each company's financial health. A comparative analysis of debt and equity positions is also provided. The report further explores cash flow statements, explaining each item and presenting comparative analyses of the three companies' financial capabilities. Additionally, the report addresses other comprehensive income statements, including explanations for items reported and not reported in the income statement, and calculates other comprehensive income statements to evaluate the performance of company managers. Finally, the report examines accounting for corporate income tax, calculating effective tax rates, commenting on deferred tax assets and liabilities, evaluating changes in deferred tax assets/liabilities, and calculating cash tax amounts and rates. The report concludes with a comprehensive overview of the financial performance and accounting practices of the selected companies.

CORPORATE

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Corporate accounting is known for special branch of accounting which developed by

companies in order to measure their financial capabilities. The present assessment is developed

to analyse financial capabilities of companies. Such companies are Clean Seas Seafood limited,

Bellamys Australia limited and Elders limited. Calculation of change in equity is to be prepared

in this report for reflecting every item of equity in order to develop effective understanding of

change over past three years with comparative analysis of debt and equity. Lastly, calculation of

cash flow is provided.

Corporate accounting is known for special branch of accounting which developed by

companies in order to measure their financial capabilities. The present assessment is developed

to analyse financial capabilities of companies. Such companies are Clean Seas Seafood limited,

Bellamys Australia limited and Elders limited. Calculation of change in equity is to be prepared

in this report for reflecting every item of equity in order to develop effective understanding of

change over past three years with comparative analysis of debt and equity. Lastly, calculation of

cash flow is provided.

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

EQUITY AND LIABILITY............................................................................................................4

1. Calculation of each item of equity with understanding of three chosen companies .........4

2. Calculation of each item of liability with understanding of three chosen companies........6

3. Comparative analysis of debt and equity of three chosen companies................................8

CASH FLOW STATEMENT..........................................................................................................9

4. Explanation of each item of cash flow with understanding of three companies................9

5. Calculation of cash flow statement with understanding of three chosen companies.......10

6. Comparative analysis of chosen three companies............................................................11

OTHER COMPREHENSIVE INCOME STATEMENT..............................................................11

7. Explanation of Items which stated in other comprehensive income for each company. .11

8. Explanation of reason for not reporting items in income statement.................................12

9. Calculation of other comprehensive income statements to evaluate performance of

managers of companies........................................................................................................12

10. Explanation of including OCI for measuring performance of managers of company...13

ACCOUNTING FOR CORPORATE INCOME TAX..................................................................13

11. Tax expenses which shown in financial statements of selected companies...................13

12. Calculation of effective tax rate of selected companies.................................................13

13. Comment on deferred tax assets and liabilities which recorded in balance sheet of selected

companies.............................................................................................................................14

14. Evaluation of changes in deferred tax assets/ liabilities.................................................14

15. Calculation of cash tax amount of all three companies using book tax, change in deferred

tax asset and liabilities..........................................................................................................15

16. Calculation of the cash tax rate of all three companies..................................................16

17. Difference between cash tax rate and book tax rate.......................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

EQUITY AND LIABILITY............................................................................................................4

1. Calculation of each item of equity with understanding of three chosen companies .........4

2. Calculation of each item of liability with understanding of three chosen companies........6

3. Comparative analysis of debt and equity of three chosen companies................................8

CASH FLOW STATEMENT..........................................................................................................9

4. Explanation of each item of cash flow with understanding of three companies................9

5. Calculation of cash flow statement with understanding of three chosen companies.......10

6. Comparative analysis of chosen three companies............................................................11

OTHER COMPREHENSIVE INCOME STATEMENT..............................................................11

7. Explanation of Items which stated in other comprehensive income for each company. .11

8. Explanation of reason for not reporting items in income statement.................................12

9. Calculation of other comprehensive income statements to evaluate performance of

managers of companies........................................................................................................12

10. Explanation of including OCI for measuring performance of managers of company...13

ACCOUNTING FOR CORPORATE INCOME TAX..................................................................13

11. Tax expenses which shown in financial statements of selected companies...................13

12. Calculation of effective tax rate of selected companies.................................................13

13. Comment on deferred tax assets and liabilities which recorded in balance sheet of selected

companies.............................................................................................................................14

14. Evaluation of changes in deferred tax assets/ liabilities.................................................14

15. Calculation of cash tax amount of all three companies using book tax, change in deferred

tax asset and liabilities..........................................................................................................15

16. Calculation of the cash tax rate of all three companies..................................................16

17. Difference between cash tax rate and book tax rate.......................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is known for special branch of accounting which develop for

preparing accounting statements of company such as preparation of final accounts, cash flow

statement. It is also used to analyse and interpret financial results and for accounting of

amalgamation, absorption, etc. The present assessment is developed to analyse financial

capabilities of companies. Such companies are Clean Seas Seafood limited which operates in

aquaculture industry through 2 segments that is Finfish sales and Tuna operations. Bellamys

Australia limited which deals in producing and marketing organic food and formula of products

for babies, and Elders limited which deals in providing products based on agriculture business.

Firstly, calculation of change in equity is to be prepared in this report for reflecting every

item of equity in order to develop effective understanding of change over past three years with

comparative analysis of debt and equity. Further, calculation of cash flow of the selected

companies will be prepared in order to comparatively analyse financial capabilities of

organisations. Lastly, in this assessment accounting of effective cash tax rate will be provided in

order to develop better understanding of performance of companies in business market.

EQUITY AND LIABILITY

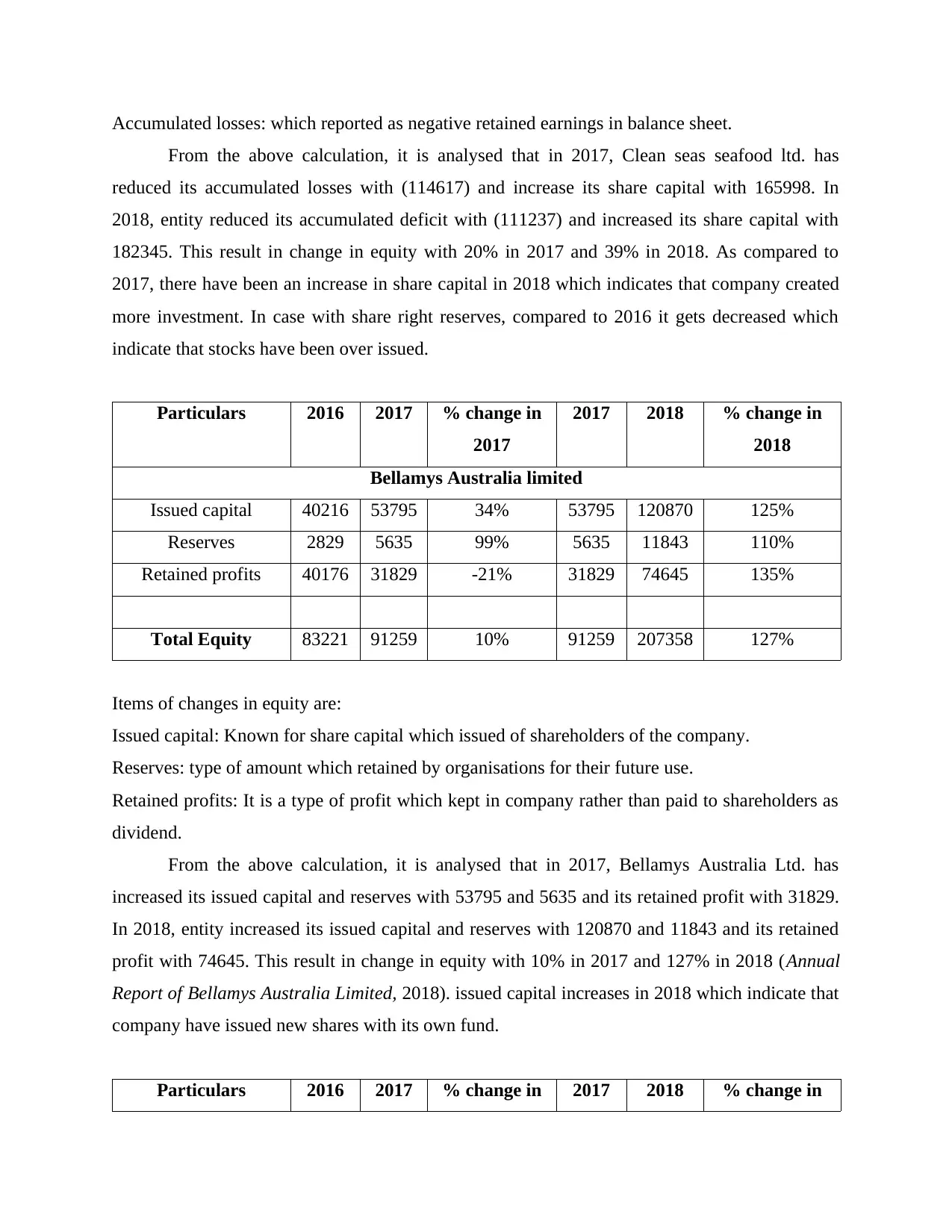

1. Calculation of each item of equity with understanding of three chosen companies

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Clean seas seafood limited

Share Capital 157736 165998 5% 165998 182345 10%

Share rights reserve 0 172 100% 172 661 284%

accumulated losses -114819 -114617 0% -114617 -111237 -3%

Total Equity 42917 51553 20% 51553 71769 39%

Items of changes in equity are:

Share capital: which is known as part of capital of company that arise because of issue of shares.

Share rights reserves: which is a dividend of subscription rights in order to buy additional

securities in company.

Corporate accounting is known for special branch of accounting which develop for

preparing accounting statements of company such as preparation of final accounts, cash flow

statement. It is also used to analyse and interpret financial results and for accounting of

amalgamation, absorption, etc. The present assessment is developed to analyse financial

capabilities of companies. Such companies are Clean Seas Seafood limited which operates in

aquaculture industry through 2 segments that is Finfish sales and Tuna operations. Bellamys

Australia limited which deals in producing and marketing organic food and formula of products

for babies, and Elders limited which deals in providing products based on agriculture business.

Firstly, calculation of change in equity is to be prepared in this report for reflecting every

item of equity in order to develop effective understanding of change over past three years with

comparative analysis of debt and equity. Further, calculation of cash flow of the selected

companies will be prepared in order to comparatively analyse financial capabilities of

organisations. Lastly, in this assessment accounting of effective cash tax rate will be provided in

order to develop better understanding of performance of companies in business market.

EQUITY AND LIABILITY

1. Calculation of each item of equity with understanding of three chosen companies

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Clean seas seafood limited

Share Capital 157736 165998 5% 165998 182345 10%

Share rights reserve 0 172 100% 172 661 284%

accumulated losses -114819 -114617 0% -114617 -111237 -3%

Total Equity 42917 51553 20% 51553 71769 39%

Items of changes in equity are:

Share capital: which is known as part of capital of company that arise because of issue of shares.

Share rights reserves: which is a dividend of subscription rights in order to buy additional

securities in company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accumulated losses: which reported as negative retained earnings in balance sheet.

From the above calculation, it is analysed that in 2017, Clean seas seafood ltd. has

reduced its accumulated losses with (114617) and increase its share capital with 165998. In

2018, entity reduced its accumulated deficit with (111237) and increased its share capital with

182345. This result in change in equity with 20% in 2017 and 39% in 2018. As compared to

2017, there have been an increase in share capital in 2018 which indicates that company created

more investment. In case with share right reserves, compared to 2016 it gets decreased which

indicate that stocks have been over issued.

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Bellamys Australia limited

Issued capital 40216 53795 34% 53795 120870 125%

Reserves 2829 5635 99% 5635 11843 110%

Retained profits 40176 31829 -21% 31829 74645 135%

Total Equity 83221 91259 10% 91259 207358 127%

Items of changes in equity are:

Issued capital: Known for share capital which issued of shareholders of the company.

Reserves: type of amount which retained by organisations for their future use.

Retained profits: It is a type of profit which kept in company rather than paid to shareholders as

dividend.

From the above calculation, it is analysed that in 2017, Bellamys Australia Ltd. has

increased its issued capital and reserves with 53795 and 5635 and its retained profit with 31829.

In 2018, entity increased its issued capital and reserves with 120870 and 11843 and its retained

profit with 74645. This result in change in equity with 10% in 2017 and 127% in 2018 (Annual

Report of Bellamys Australia Limited, 2018). issued capital increases in 2018 which indicate that

company have issued new shares with its own fund.

Particulars 2016 2017 % change in 2017 2018 % change in

From the above calculation, it is analysed that in 2017, Clean seas seafood ltd. has

reduced its accumulated losses with (114617) and increase its share capital with 165998. In

2018, entity reduced its accumulated deficit with (111237) and increased its share capital with

182345. This result in change in equity with 20% in 2017 and 39% in 2018. As compared to

2017, there have been an increase in share capital in 2018 which indicates that company created

more investment. In case with share right reserves, compared to 2016 it gets decreased which

indicate that stocks have been over issued.

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Bellamys Australia limited

Issued capital 40216 53795 34% 53795 120870 125%

Reserves 2829 5635 99% 5635 11843 110%

Retained profits 40176 31829 -21% 31829 74645 135%

Total Equity 83221 91259 10% 91259 207358 127%

Items of changes in equity are:

Issued capital: Known for share capital which issued of shareholders of the company.

Reserves: type of amount which retained by organisations for their future use.

Retained profits: It is a type of profit which kept in company rather than paid to shareholders as

dividend.

From the above calculation, it is analysed that in 2017, Bellamys Australia Ltd. has

increased its issued capital and reserves with 53795 and 5635 and its retained profit with 31829.

In 2018, entity increased its issued capital and reserves with 120870 and 11843 and its retained

profit with 74645. This result in change in equity with 10% in 2017 and 127% in 2018 (Annual

Report of Bellamys Australia Limited, 2018). issued capital increases in 2018 which indicate that

company have issued new shares with its own fund.

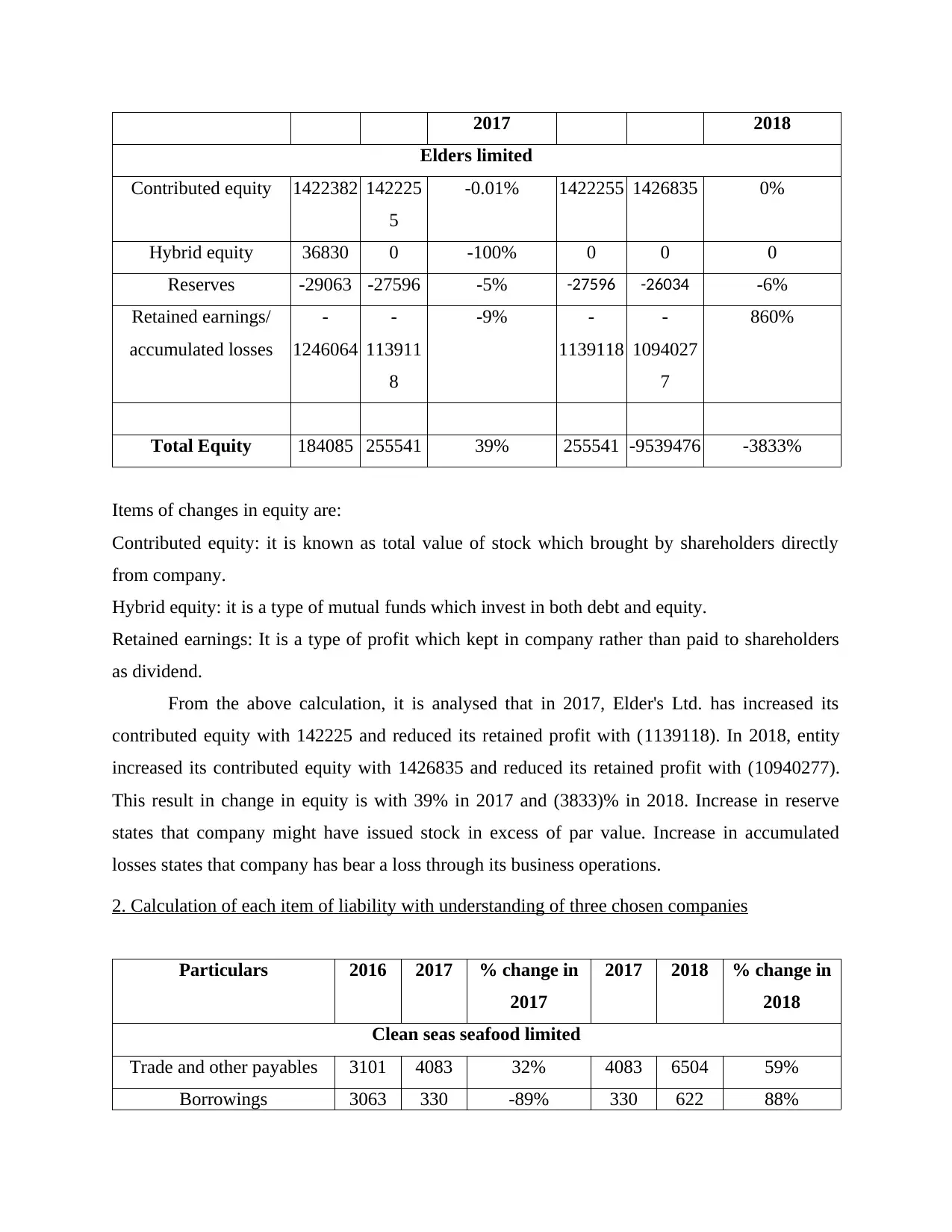

Particulars 2016 2017 % change in 2017 2018 % change in

2017 2018

Elders limited

Contributed equity 1422382 142225

5

-0.01% 1422255 1426835 0%

Hybrid equity 36830 0 -100% 0 0 0

Reserves -29063 -27596 -5% -27596 -26034 -6%

Retained earnings/

accumulated losses

-

1246064

-

113911

8

-9% -

1139118

-

1094027

7

860%

Total Equity 184085 255541 39% 255541 -9539476 -3833%

Items of changes in equity are:

Contributed equity: it is known as total value of stock which brought by shareholders directly

from company.

Hybrid equity: it is a type of mutual funds which invest in both debt and equity.

Retained earnings: It is a type of profit which kept in company rather than paid to shareholders

as dividend.

From the above calculation, it is analysed that in 2017, Elder's Ltd. has increased its

contributed equity with 142225 and reduced its retained profit with (1139118). In 2018, entity

increased its contributed equity with 1426835 and reduced its retained profit with (10940277).

This result in change in equity is with 39% in 2017 and (3833)% in 2018. Increase in reserve

states that company might have issued stock in excess of par value. Increase in accumulated

losses states that company has bear a loss through its business operations.

2. Calculation of each item of liability with understanding of three chosen companies

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Clean seas seafood limited

Trade and other payables 3101 4083 32% 4083 6504 59%

Borrowings 3063 330 -89% 330 622 88%

Elders limited

Contributed equity 1422382 142225

5

-0.01% 1422255 1426835 0%

Hybrid equity 36830 0 -100% 0 0 0

Reserves -29063 -27596 -5% -27596 -26034 -6%

Retained earnings/

accumulated losses

-

1246064

-

113911

8

-9% -

1139118

-

1094027

7

860%

Total Equity 184085 255541 39% 255541 -9539476 -3833%

Items of changes in equity are:

Contributed equity: it is known as total value of stock which brought by shareholders directly

from company.

Hybrid equity: it is a type of mutual funds which invest in both debt and equity.

Retained earnings: It is a type of profit which kept in company rather than paid to shareholders

as dividend.

From the above calculation, it is analysed that in 2017, Elder's Ltd. has increased its

contributed equity with 142225 and reduced its retained profit with (1139118). In 2018, entity

increased its contributed equity with 1426835 and reduced its retained profit with (10940277).

This result in change in equity is with 39% in 2017 and (3833)% in 2018. Increase in reserve

states that company might have issued stock in excess of par value. Increase in accumulated

losses states that company has bear a loss through its business operations.

2. Calculation of each item of liability with understanding of three chosen companies

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Clean seas seafood limited

Trade and other payables 3101 4083 32% 4083 6504 59%

Borrowings 3063 330 -89% 330 622 88%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

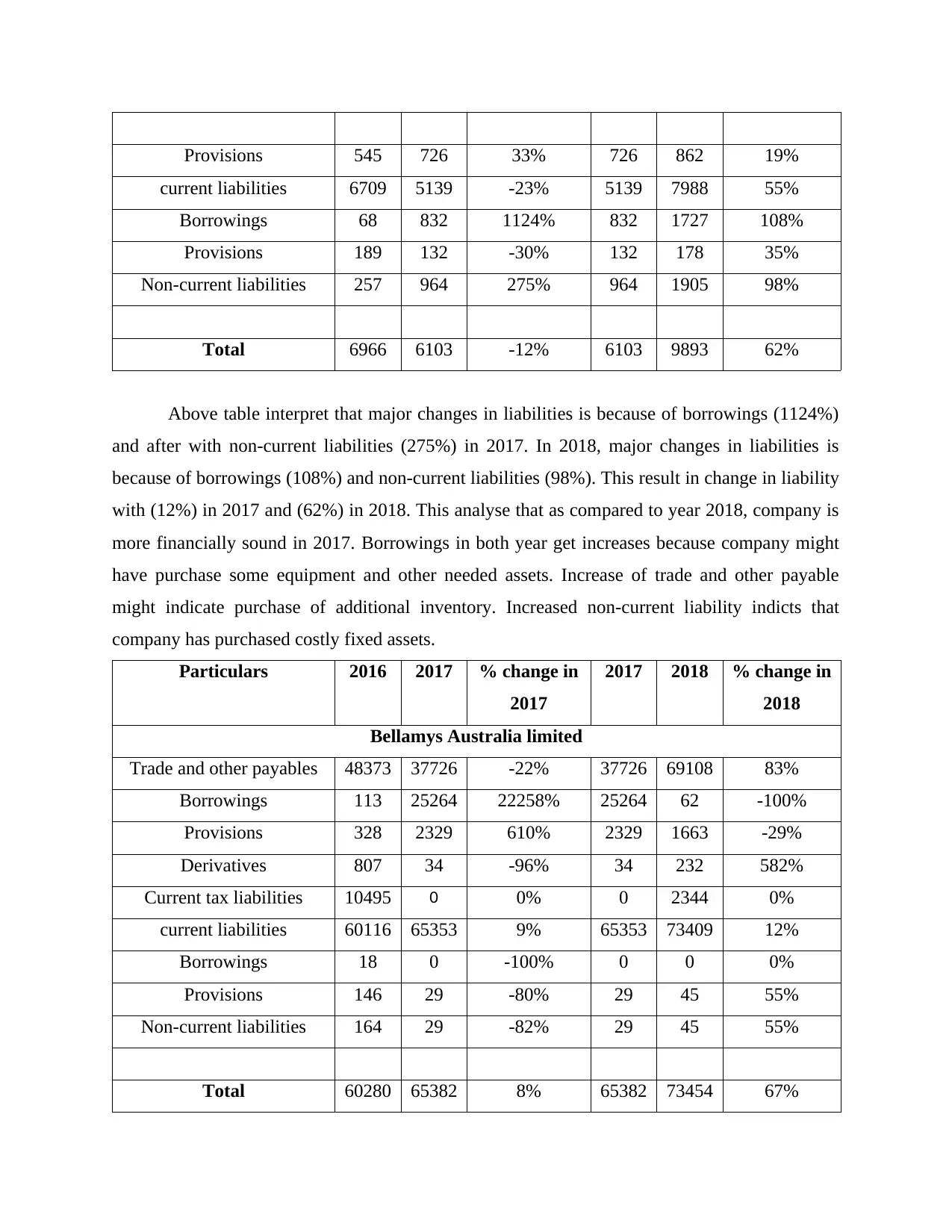

Provisions 545 726 33% 726 862 19%

current liabilities 6709 5139 -23% 5139 7988 55%

Borrowings 68 832 1124% 832 1727 108%

Provisions 189 132 -30% 132 178 35%

Non-current liabilities 257 964 275% 964 1905 98%

Total 6966 6103 -12% 6103 9893 62%

Above table interpret that major changes in liabilities is because of borrowings (1124%)

and after with non-current liabilities (275%) in 2017. In 2018, major changes in liabilities is

because of borrowings (108%) and non-current liabilities (98%). This result in change in liability

with (12%) in 2017 and (62%) in 2018. This analyse that as compared to year 2018, company is

more financially sound in 2017. Borrowings in both year get increases because company might

have purchase some equipment and other needed assets. Increase of trade and other payable

might indicate purchase of additional inventory. Increased non-current liability indicts that

company has purchased costly fixed assets.

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Bellamys Australia limited

Trade and other payables 48373 37726 -22% 37726 69108 83%

Borrowings 113 25264 22258% 25264 62 -100%

Provisions 328 2329 610% 2329 1663 -29%

Derivatives 807 34 -96% 34 232 582%

Current tax liabilities 10495 0 0% 0 2344 0%

current liabilities 60116 65353 9% 65353 73409 12%

Borrowings 18 0 -100% 0 0 0%

Provisions 146 29 -80% 29 45 55%

Non-current liabilities 164 29 -82% 29 45 55%

Total 60280 65382 8% 65382 73454 67%

current liabilities 6709 5139 -23% 5139 7988 55%

Borrowings 68 832 1124% 832 1727 108%

Provisions 189 132 -30% 132 178 35%

Non-current liabilities 257 964 275% 964 1905 98%

Total 6966 6103 -12% 6103 9893 62%

Above table interpret that major changes in liabilities is because of borrowings (1124%)

and after with non-current liabilities (275%) in 2017. In 2018, major changes in liabilities is

because of borrowings (108%) and non-current liabilities (98%). This result in change in liability

with (12%) in 2017 and (62%) in 2018. This analyse that as compared to year 2018, company is

more financially sound in 2017. Borrowings in both year get increases because company might

have purchase some equipment and other needed assets. Increase of trade and other payable

might indicate purchase of additional inventory. Increased non-current liability indicts that

company has purchased costly fixed assets.

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Bellamys Australia limited

Trade and other payables 48373 37726 -22% 37726 69108 83%

Borrowings 113 25264 22258% 25264 62 -100%

Provisions 328 2329 610% 2329 1663 -29%

Derivatives 807 34 -96% 34 232 582%

Current tax liabilities 10495 0 0% 0 2344 0%

current liabilities 60116 65353 9% 65353 73409 12%

Borrowings 18 0 -100% 0 0 0%

Provisions 146 29 -80% 29 45 55%

Non-current liabilities 164 29 -82% 29 45 55%

Total 60280 65382 8% 65382 73454 67%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

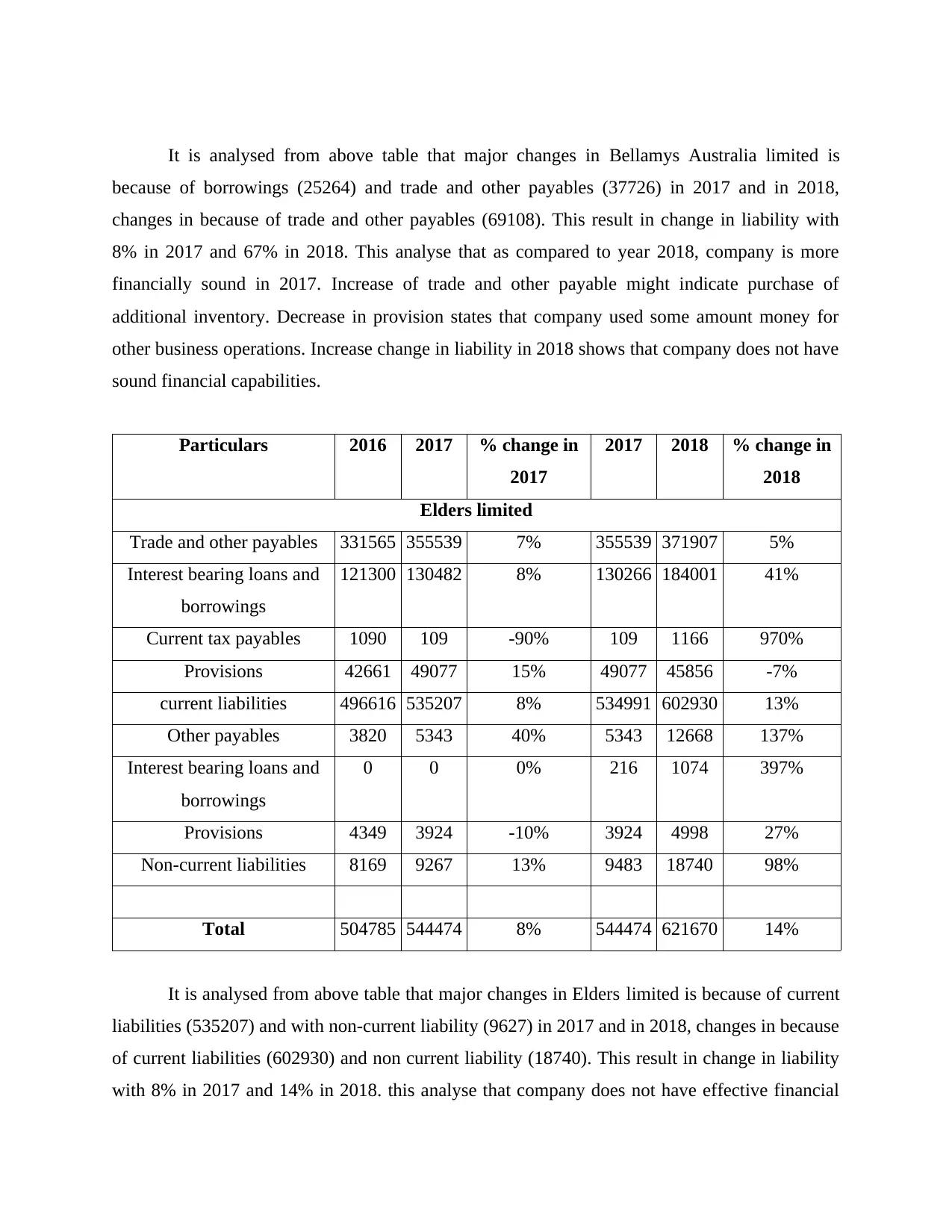

It is analysed from above table that major changes in Bellamys Australia limited is

because of borrowings (25264) and trade and other payables (37726) in 2017 and in 2018,

changes in because of trade and other payables (69108). This result in change in liability with

8% in 2017 and 67% in 2018. This analyse that as compared to year 2018, company is more

financially sound in 2017. Increase of trade and other payable might indicate purchase of

additional inventory. Decrease in provision states that company used some amount money for

other business operations. Increase change in liability in 2018 shows that company does not have

sound financial capabilities.

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Elders limited

Trade and other payables 331565 355539 7% 355539 371907 5%

Interest bearing loans and

borrowings

121300 130482 8% 130266 184001 41%

Current tax payables 1090 109 -90% 109 1166 970%

Provisions 42661 49077 15% 49077 45856 -7%

current liabilities 496616 535207 8% 534991 602930 13%

Other payables 3820 5343 40% 5343 12668 137%

Interest bearing loans and

borrowings

0 0 0% 216 1074 397%

Provisions 4349 3924 -10% 3924 4998 27%

Non-current liabilities 8169 9267 13% 9483 18740 98%

Total 504785 544474 8% 544474 621670 14%

It is analysed from above table that major changes in Elders limited is because of current

liabilities (535207) and with non-current liability (9627) in 2017 and in 2018, changes in because

of current liabilities (602930) and non current liability (18740). This result in change in liability

with 8% in 2017 and 14% in 2018. this analyse that company does not have effective financial

because of borrowings (25264) and trade and other payables (37726) in 2017 and in 2018,

changes in because of trade and other payables (69108). This result in change in liability with

8% in 2017 and 67% in 2018. This analyse that as compared to year 2018, company is more

financially sound in 2017. Increase of trade and other payable might indicate purchase of

additional inventory. Decrease in provision states that company used some amount money for

other business operations. Increase change in liability in 2018 shows that company does not have

sound financial capabilities.

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Elders limited

Trade and other payables 331565 355539 7% 355539 371907 5%

Interest bearing loans and

borrowings

121300 130482 8% 130266 184001 41%

Current tax payables 1090 109 -90% 109 1166 970%

Provisions 42661 49077 15% 49077 45856 -7%

current liabilities 496616 535207 8% 534991 602930 13%

Other payables 3820 5343 40% 5343 12668 137%

Interest bearing loans and

borrowings

0 0 0% 216 1074 397%

Provisions 4349 3924 -10% 3924 4998 27%

Non-current liabilities 8169 9267 13% 9483 18740 98%

Total 504785 544474 8% 544474 621670 14%

It is analysed from above table that major changes in Elders limited is because of current

liabilities (535207) and with non-current liability (9627) in 2017 and in 2018, changes in because

of current liabilities (602930) and non current liability (18740). This result in change in liability

with 8% in 2017 and 14% in 2018. this analyse that company does not have effective financial

capabilities (Annual Report of Elders Limited, 2017). increase current tax payable shows that

company did not have paid its income because of transaction which tool place in current period.

Increase in interest bearing loan and borrowing indicate that company might have purchase some

equipment and other needed assets.

3. Comparative analysis of debt and equity of three chosen companies

Particular

s

Clean seas

seafood

limited

Debt equity

position

Bellamys

Australia

Ltd

Debt equity

position

Elders

Ltd

Debt

equity

position

Debt 9893 12% 73454 26% 621670 -7%

Equity 71769 88% 207358 74% -9539476 107%

Total 81662 100% 280812 100% -8917806 100%

The above table is evaluating comparative analysis of capital structure of selected

companies. The ideal structure is 40:60 for organisations but here limited debt is of Elders Ltd.

In comparison to Elder Ltd., other companies has huge debt comparatively to equity as they

should control their liability for effective capital structure.

CASH FLOW STATEMENT

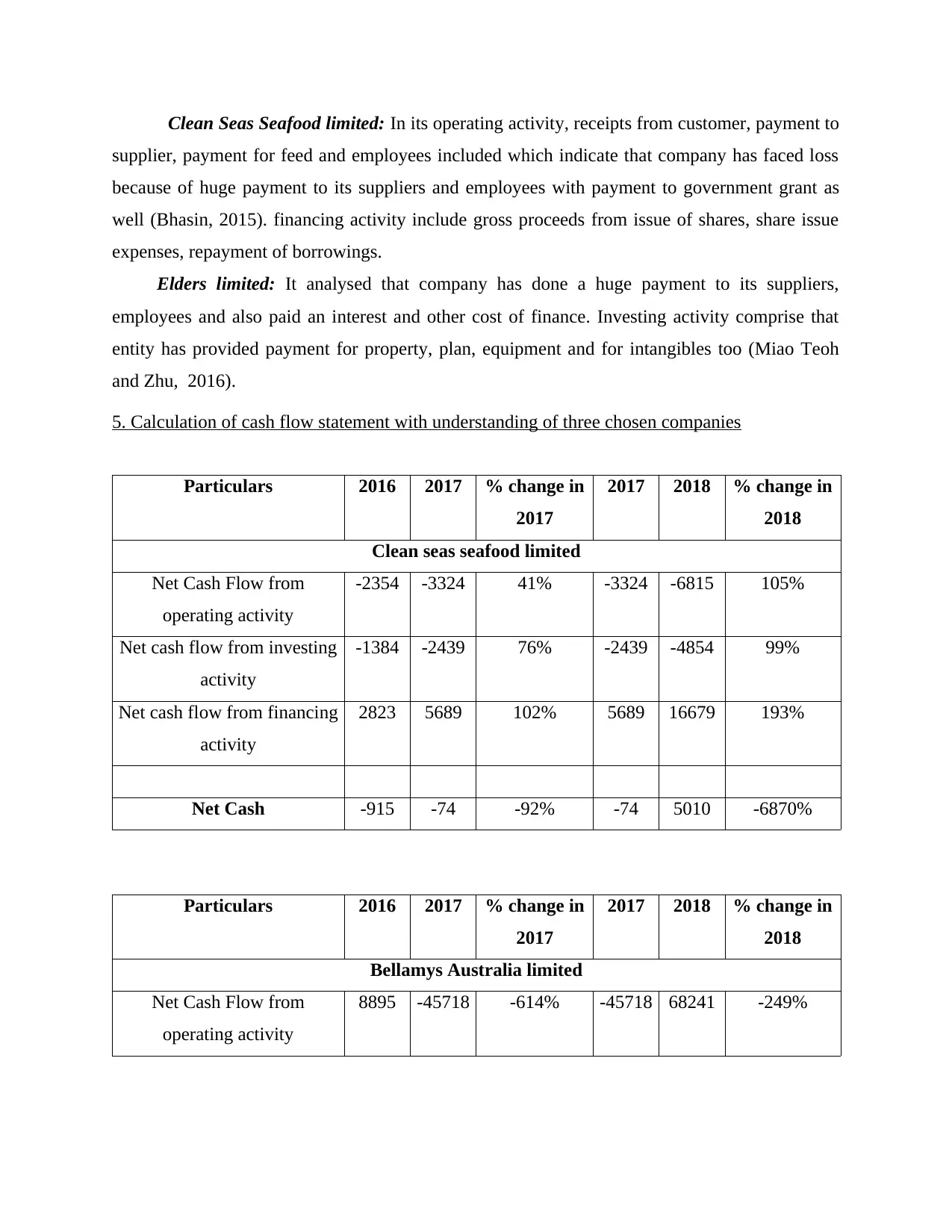

4. Explanation of each item of cash flow with understanding of three companies

Primary purpose of establishing cash flow statements in business is to find information

regarding cash receipts, cash payments and net change in cash which arises because of operating,

investing and financing activities (Ahiadorme, Gyeke-Dako and Abor, 2018).

Bellamys Australia limited: It is analysed that organisation have generated effective cash

through cash receipt from customer, suppliers and employees (Annual Report of Bellamys

Australia Limited, 2017). With its investing activities, it is comprised that from sale of property,

plant and equipment and purchase of property, plant and equipment effective asset will get

developed for improving business operations. With financing activities, proceed from share

issue, borrowings etc. which indicate sound financial capability of company.

company did not have paid its income because of transaction which tool place in current period.

Increase in interest bearing loan and borrowing indicate that company might have purchase some

equipment and other needed assets.

3. Comparative analysis of debt and equity of three chosen companies

Particular

s

Clean seas

seafood

limited

Debt equity

position

Bellamys

Australia

Ltd

Debt equity

position

Elders

Ltd

Debt

equity

position

Debt 9893 12% 73454 26% 621670 -7%

Equity 71769 88% 207358 74% -9539476 107%

Total 81662 100% 280812 100% -8917806 100%

The above table is evaluating comparative analysis of capital structure of selected

companies. The ideal structure is 40:60 for organisations but here limited debt is of Elders Ltd.

In comparison to Elder Ltd., other companies has huge debt comparatively to equity as they

should control their liability for effective capital structure.

CASH FLOW STATEMENT

4. Explanation of each item of cash flow with understanding of three companies

Primary purpose of establishing cash flow statements in business is to find information

regarding cash receipts, cash payments and net change in cash which arises because of operating,

investing and financing activities (Ahiadorme, Gyeke-Dako and Abor, 2018).

Bellamys Australia limited: It is analysed that organisation have generated effective cash

through cash receipt from customer, suppliers and employees (Annual Report of Bellamys

Australia Limited, 2017). With its investing activities, it is comprised that from sale of property,

plant and equipment and purchase of property, plant and equipment effective asset will get

developed for improving business operations. With financing activities, proceed from share

issue, borrowings etc. which indicate sound financial capability of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Clean Seas Seafood limited: In its operating activity, receipts from customer, payment to

supplier, payment for feed and employees included which indicate that company has faced loss

because of huge payment to its suppliers and employees with payment to government grant as

well (Bhasin, 2015). financing activity include gross proceeds from issue of shares, share issue

expenses, repayment of borrowings.

Elders limited: It analysed that company has done a huge payment to its suppliers,

employees and also paid an interest and other cost of finance. Investing activity comprise that

entity has provided payment for property, plan, equipment and for intangibles too (Miao Teoh

and Zhu, 2016).

5. Calculation of cash flow statement with understanding of three chosen companies

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Clean seas seafood limited

Net Cash Flow from

operating activity

-2354 -3324 41% -3324 -6815 105%

Net cash flow from investing

activity

-1384 -2439 76% -2439 -4854 99%

Net cash flow from financing

activity

2823 5689 102% 5689 16679 193%

Net Cash -915 -74 -92% -74 5010 -6870%

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Bellamys Australia limited

Net Cash Flow from

operating activity

8895 -45718 -614% -45718 68241 -249%

supplier, payment for feed and employees included which indicate that company has faced loss

because of huge payment to its suppliers and employees with payment to government grant as

well (Bhasin, 2015). financing activity include gross proceeds from issue of shares, share issue

expenses, repayment of borrowings.

Elders limited: It analysed that company has done a huge payment to its suppliers,

employees and also paid an interest and other cost of finance. Investing activity comprise that

entity has provided payment for property, plan, equipment and for intangibles too (Miao Teoh

and Zhu, 2016).

5. Calculation of cash flow statement with understanding of three chosen companies

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Clean seas seafood limited

Net Cash Flow from

operating activity

-2354 -3324 41% -3324 -6815 105%

Net cash flow from investing

activity

-1384 -2439 76% -2439 -4854 99%

Net cash flow from financing

activity

2823 5689 102% 5689 16679 193%

Net Cash -915 -74 -92% -74 5010 -6870%

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Bellamys Australia limited

Net Cash Flow from

operating activity

8895 -45718 -614% -45718 68241 -249%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net cash flow from investing

activity

-2402 -472 -80% -472 -17981 3710%

Net cash flow from financing

activity

-6230 31173 -600% 31173 19898 -36%

Net Cash 263 -15017 -5810% -15017 70158 -567%

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Elders limited

Net Cash Flow from

operating activity

48676 81599 68% 81599 -12132 -115%

Net cash flow from investing

activity

-27292 -42011 54% -42011 -38391 -9%

Net cash flow from financing

activity

13098 -39553 -402% -39553 26978 -168%

Net Cash 34482 35 -100% 35 -23545 -67371%

6. Comparative analysis of chosen three companies

Clean seas seafood

limited

Bellamys Australia

limited

Elders limited

Particulars 2017 2018 2017 2018 2017 2018

Net Cash Flow from

operating activity

41% 105% -614% -249% 68% -115%

Net cash flow from

investing activity

76% 99% -80% 3710% 54% -9%

Net cash flow from

financing activity

102% 193% -600% -36% -402% -168%

activity

-2402 -472 -80% -472 -17981 3710%

Net cash flow from financing

activity

-6230 31173 -600% 31173 19898 -36%

Net Cash 263 -15017 -5810% -15017 70158 -567%

Particulars 2016 2017 % change in

2017

2017 2018 % change in

2018

Elders limited

Net Cash Flow from

operating activity

48676 81599 68% 81599 -12132 -115%

Net cash flow from investing

activity

-27292 -42011 54% -42011 -38391 -9%

Net cash flow from financing

activity

13098 -39553 -402% -39553 26978 -168%

Net Cash 34482 35 -100% 35 -23545 -67371%

6. Comparative analysis of chosen three companies

Clean seas seafood

limited

Bellamys Australia

limited

Elders limited

Particulars 2017 2018 2017 2018 2017 2018

Net Cash Flow from

operating activity

41% 105% -614% -249% 68% -115%

Net cash flow from

investing activity

76% 99% -80% 3710% 54% -9%

Net cash flow from

financing activity

102% 193% -600% -36% -402% -168%

From the above calculation it is analysed that highest cash has been generated by Clean

seas seafood company through its operating activity in 2018. Through investing activity huge

cash is generated by Bellamys Australia Ltd. and from financing activity, clean seas seafood Ltd

has used the highest cash (Harrison and van der Laan Smith, 2015).

OTHER COMPREHENSIVE INCOME STATEMENT

7. Explanation of Items which stated in other comprehensive income for each company

Clean Seas Seafood Limited:

According to annual report of entity, it is analysed that company has bear a loss from its business

operation (Annual Report of Clean Seas Seafood Limited, 2017). A clear indication of facing loss

in financial year also predicted when there is a negative operating activities. This reason predicts

reason for not preparing other comprehensive income as this will not impact profit which

attributable to shareholders.

Bellamys Australia Ltd:

It has statement of other comprehensive income which consist of changes in fair value of cash

which helps against altering value of liabilities and exchange different arising from transaction

which include foreign operations and foreign currency transactions in financial statements

(Bauman and Shaw, 2016).

Elders Ltd:

Entity have also prepared other comprehensive income in order to record its foreign operations

and foreign currency transactions. It consists of exchange difference which arising from

transactions (Annual Report of Elders Limited, 2018).

8. Explanation of reason for not reporting items in income statement

These are the values which cannot be realised until they get sold and any type of

adjustment which done in the middle of year will be recognised in this statement. It is also not

recorded in income statement because of accounting standards as they are not contributed in net

margin. On the other hand, it is directly claimed as other margin where such types of transactions

are recorded as investments because of which this is eliminated from financial statement as it

will realise profit and loss.

seas seafood company through its operating activity in 2018. Through investing activity huge

cash is generated by Bellamys Australia Ltd. and from financing activity, clean seas seafood Ltd

has used the highest cash (Harrison and van der Laan Smith, 2015).

OTHER COMPREHENSIVE INCOME STATEMENT

7. Explanation of Items which stated in other comprehensive income for each company

Clean Seas Seafood Limited:

According to annual report of entity, it is analysed that company has bear a loss from its business

operation (Annual Report of Clean Seas Seafood Limited, 2017). A clear indication of facing loss

in financial year also predicted when there is a negative operating activities. This reason predicts

reason for not preparing other comprehensive income as this will not impact profit which

attributable to shareholders.

Bellamys Australia Ltd:

It has statement of other comprehensive income which consist of changes in fair value of cash

which helps against altering value of liabilities and exchange different arising from transaction

which include foreign operations and foreign currency transactions in financial statements

(Bauman and Shaw, 2016).

Elders Ltd:

Entity have also prepared other comprehensive income in order to record its foreign operations

and foreign currency transactions. It consists of exchange difference which arising from

transactions (Annual Report of Elders Limited, 2018).

8. Explanation of reason for not reporting items in income statement

These are the values which cannot be realised until they get sold and any type of

adjustment which done in the middle of year will be recognised in this statement. It is also not

recorded in income statement because of accounting standards as they are not contributed in net

margin. On the other hand, it is directly claimed as other margin where such types of transactions

are recorded as investments because of which this is eliminated from financial statement as it

will realise profit and loss.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.