Corporate Accounting: BHP Billiton Financial Report Analysis

VerifiedAdded on 2023/06/12

|15

|3087

|130

AI Summary

This report analyses the financial information of BHP Billiton and provides recommendations for compliance disclosure. It also discusses pre and post-acquisition entries and their adjustment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Corporate Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................2

Part A:........................................................................................................................................2

Answer to 1 A:.......................................................................................................................2

Qualitative characteristics of the relevance and comparability:............................................2

Disclosing environmental reporting practices:.......................................................................4

Explanation of Disclosure of opinion:.......................................................................................6

Recommendations to top management to strengthen compliance in future reporting:..............7

Answer to Part B:.......................................................................................................................7

Answer to question 1:.............................................................................................................7

Answer to question 2:.............................................................................................................8

Answer to question 3:.............................................................................................................9

Answer to question 4:.............................................................................................................9

Answer to question 5:...........................................................................................................10

Conclusion:..............................................................................................................................10

Reference List:.........................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................2

Part A:........................................................................................................................................2

Answer to 1 A:.......................................................................................................................2

Qualitative characteristics of the relevance and comparability:............................................2

Disclosing environmental reporting practices:.......................................................................4

Explanation of Disclosure of opinion:.......................................................................................6

Recommendations to top management to strengthen compliance in future reporting:..............7

Answer to Part B:.......................................................................................................................7

Answer to question 1:.............................................................................................................7

Answer to question 2:.............................................................................................................8

Answer to question 3:.............................................................................................................9

Answer to question 4:.............................................................................................................9

Answer to question 5:...........................................................................................................10

Conclusion:..............................................................................................................................10

Reference List:.........................................................................................................................12

2CORPORATE ACCOUNTING

Introduction:

In the corporate accounting analysing the financial reports are considered as the vital

element. The financial statement that are provided by the company acts as the tool for

measuring the annual performance of the company. The statement of financial position,

income statement and cash flow statement acts the vital medium of providing the

shareholders with the necessary information regarding the overall performance of the

organization (Crowther 2016).

The present report is based on the understanding of the corporate reporting

environment of the BHP Billiton. The report would be assessing the financial information’s

of the company presented through the information disclosure and would also provide the top

management with the recommendations relating to the compliance disclosure. The report

would further focus on the adjustment related to the acquisition provided in the annual report

of BHP Billiton.

Part A:

Answer to 1 A:

Qualitative characteristics of the relevance and comparability:

The qualitative characteristics of an organizations financial statement is largely

consisting of the comparability, consistency and dependability (Kareiva et al. 2015). The

report presently emphasis on the BHP Billiton comparability and relevance of the annual

reports.

Relevance: The element of relevance of financial report provides that the financial

statements should be relevant to the numerous kinds of needs of an organizations shareholder.

The statement of financial position serves as tool in decision making for the stakeholders and

requires a due care in preparing the financial statements (Boyd and Golden 2016). Relevant

Introduction:

In the corporate accounting analysing the financial reports are considered as the vital

element. The financial statement that are provided by the company acts as the tool for

measuring the annual performance of the company. The statement of financial position,

income statement and cash flow statement acts the vital medium of providing the

shareholders with the necessary information regarding the overall performance of the

organization (Crowther 2016).

The present report is based on the understanding of the corporate reporting

environment of the BHP Billiton. The report would be assessing the financial information’s

of the company presented through the information disclosure and would also provide the top

management with the recommendations relating to the compliance disclosure. The report

would further focus on the adjustment related to the acquisition provided in the annual report

of BHP Billiton.

Part A:

Answer to 1 A:

Qualitative characteristics of the relevance and comparability:

The qualitative characteristics of an organizations financial statement is largely

consisting of the comparability, consistency and dependability (Kareiva et al. 2015). The

report presently emphasis on the BHP Billiton comparability and relevance of the annual

reports.

Relevance: The element of relevance of financial report provides that the financial

statements should be relevant to the numerous kinds of needs of an organizations shareholder.

The statement of financial position serves as tool in decision making for the stakeholders and

requires a due care in preparing the financial statements (Boyd and Golden 2016). Relevant

3CORPORATE ACCOUNTING

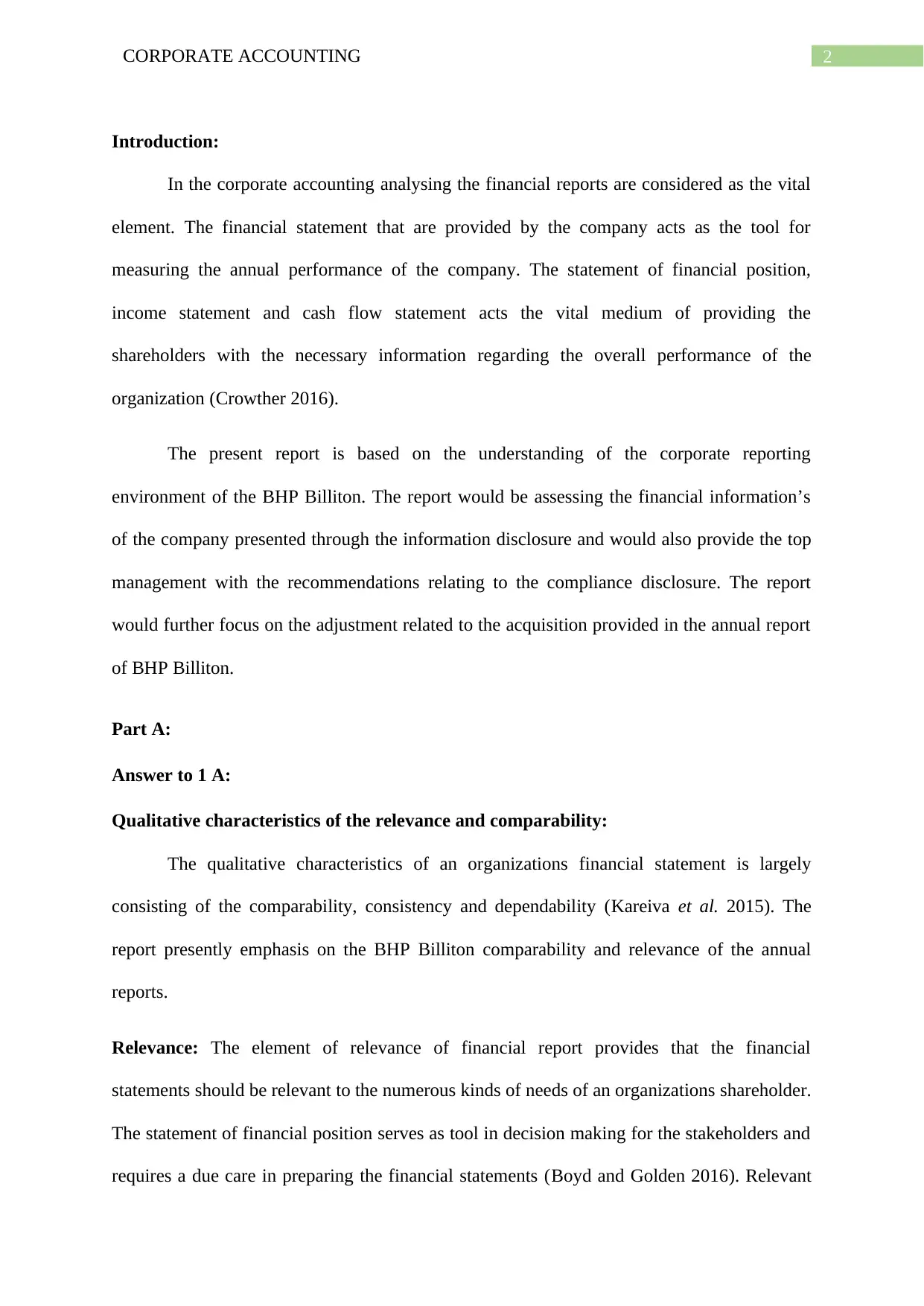

information contained in the financial statements should not be omitted as this may result in

negative consequences. For BHP financial statements the payment of dividends, total income

and net amount of cash flow are held as important aspects of the company. An illustrations of

the example has been provided below;

Table 1: Table representing Dividend Paid

(Source: BHP Billiton 2018)

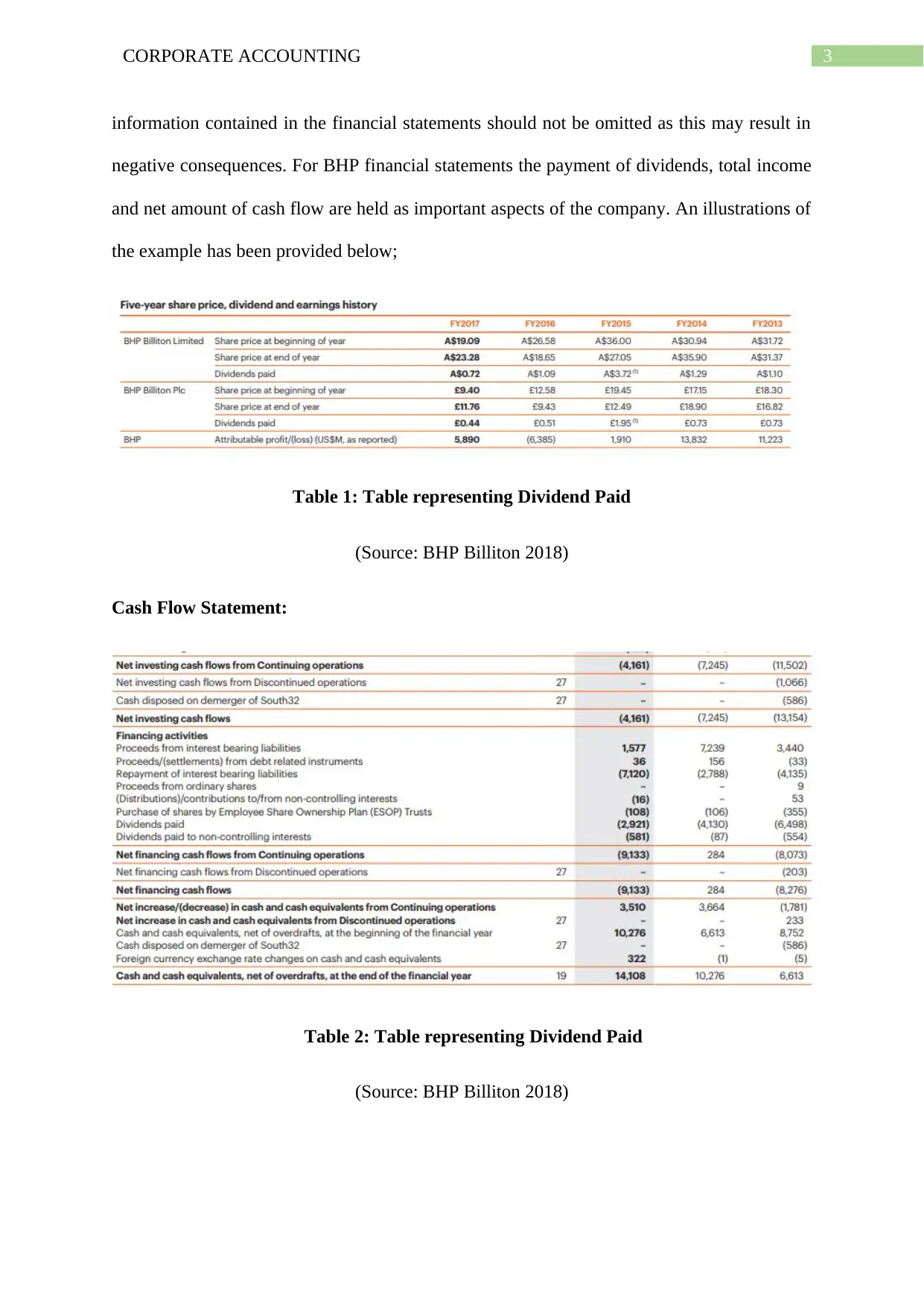

Cash Flow Statement:

Table 2: Table representing Dividend Paid

(Source: BHP Billiton 2018)

information contained in the financial statements should not be omitted as this may result in

negative consequences. For BHP financial statements the payment of dividends, total income

and net amount of cash flow are held as important aspects of the company. An illustrations of

the example has been provided below;

Table 1: Table representing Dividend Paid

(Source: BHP Billiton 2018)

Cash Flow Statement:

Table 2: Table representing Dividend Paid

(Source: BHP Billiton 2018)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING

Comparability: The comparability aspects of the financial statement is held as the

noteworthy aspects in the preparation of the financial statements (Stent and Dowler 2015).

The financial statements provide the value investors with the useful information in decision

making. Furthermore, the financial statements act as the meaningful tool in identifying the

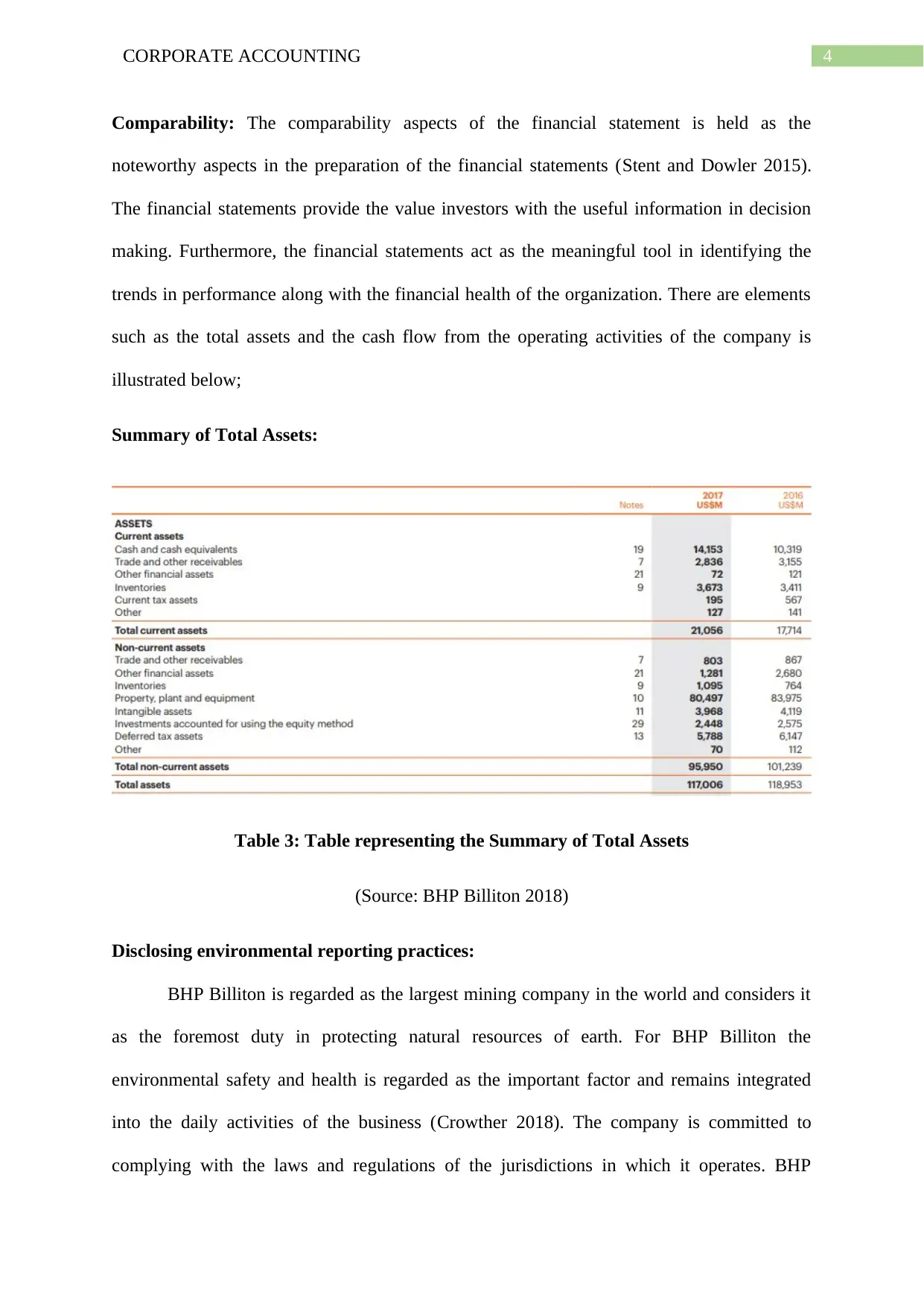

trends in performance along with the financial health of the organization. There are elements

such as the total assets and the cash flow from the operating activities of the company is

illustrated below;

Summary of Total Assets:

Table 3: Table representing the Summary of Total Assets

(Source: BHP Billiton 2018)

Disclosing environmental reporting practices:

BHP Billiton is regarded as the largest mining company in the world and considers it

as the foremost duty in protecting natural resources of earth. For BHP Billiton the

environmental safety and health is regarded as the important factor and remains integrated

into the daily activities of the business (Crowther 2018). The company is committed to

complying with the laws and regulations of the jurisdictions in which it operates. BHP

Comparability: The comparability aspects of the financial statement is held as the

noteworthy aspects in the preparation of the financial statements (Stent and Dowler 2015).

The financial statements provide the value investors with the useful information in decision

making. Furthermore, the financial statements act as the meaningful tool in identifying the

trends in performance along with the financial health of the organization. There are elements

such as the total assets and the cash flow from the operating activities of the company is

illustrated below;

Summary of Total Assets:

Table 3: Table representing the Summary of Total Assets

(Source: BHP Billiton 2018)

Disclosing environmental reporting practices:

BHP Billiton is regarded as the largest mining company in the world and considers it

as the foremost duty in protecting natural resources of earth. For BHP Billiton the

environmental safety and health is regarded as the important factor and remains integrated

into the daily activities of the business (Crowther 2018). The company is committed to

complying with the laws and regulations of the jurisdictions in which it operates. BHP

5CORPORATE ACCOUNTING

Billiton aims to go past the legal and the regulatory requirements. The company identifies the

responsibilities of minimizing the environmental impact and contributing to the enduring

benefits. BHP Billiton has separate set of segment in their annual statement which is

dedicated towards disclosing the environmental reports. The below listed are the disclosure

that are provided under the heads of the environmental disclosure of the annual reports.

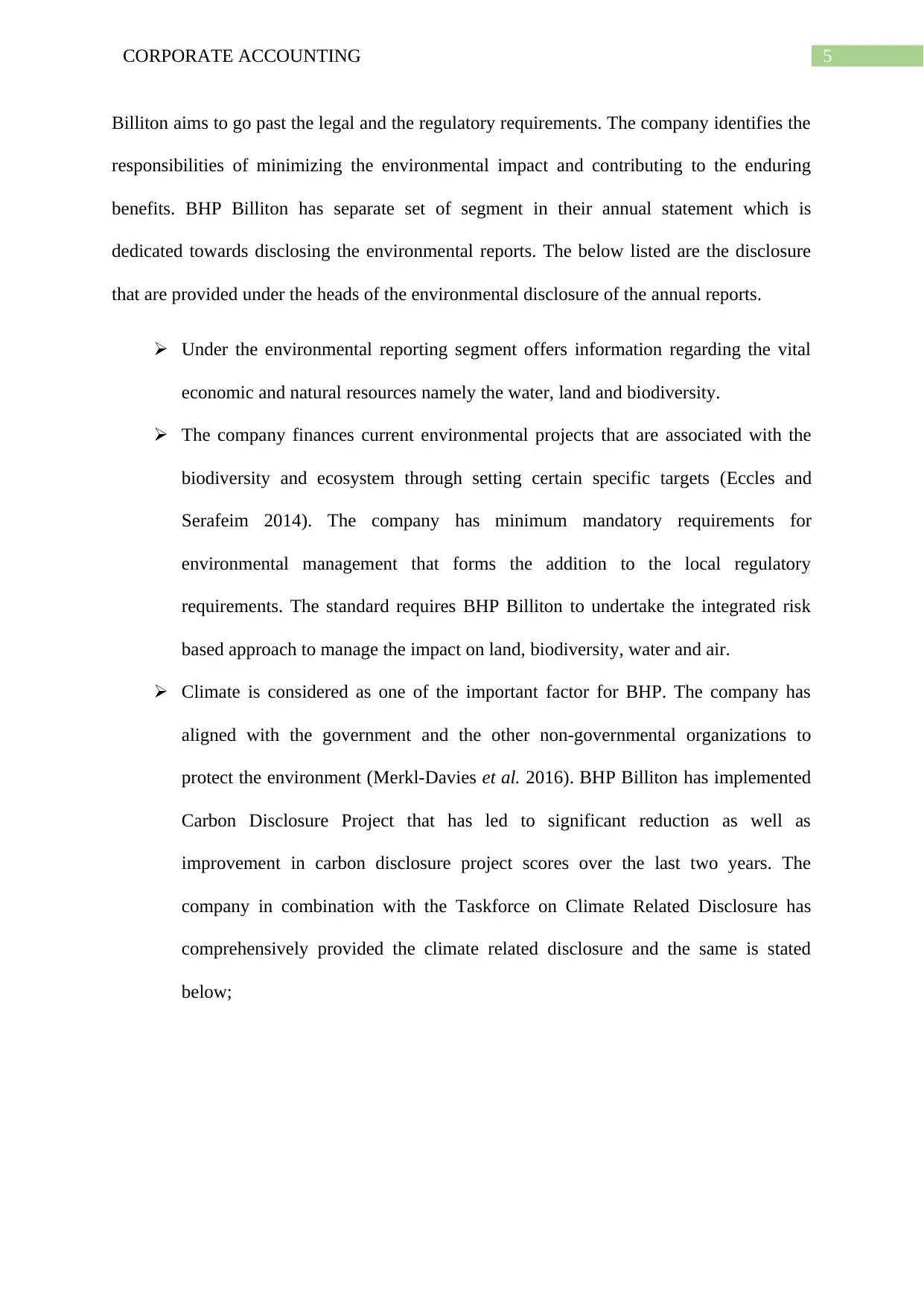

Under the environmental reporting segment offers information regarding the vital

economic and natural resources namely the water, land and biodiversity.

The company finances current environmental projects that are associated with the

biodiversity and ecosystem through setting certain specific targets (Eccles and

Serafeim 2014). The company has minimum mandatory requirements for

environmental management that forms the addition to the local regulatory

requirements. The standard requires BHP Billiton to undertake the integrated risk

based approach to manage the impact on land, biodiversity, water and air.

Climate is considered as one of the important factor for BHP. The company has

aligned with the government and the other non-governmental organizations to

protect the environment (Merkl-Davies et al. 2016). BHP Billiton has implemented

Carbon Disclosure Project that has led to significant reduction as well as

improvement in carbon disclosure project scores over the last two years. The

company in combination with the Taskforce on Climate Related Disclosure has

comprehensively provided the climate related disclosure and the same is stated

below;

Billiton aims to go past the legal and the regulatory requirements. The company identifies the

responsibilities of minimizing the environmental impact and contributing to the enduring

benefits. BHP Billiton has separate set of segment in their annual statement which is

dedicated towards disclosing the environmental reports. The below listed are the disclosure

that are provided under the heads of the environmental disclosure of the annual reports.

Under the environmental reporting segment offers information regarding the vital

economic and natural resources namely the water, land and biodiversity.

The company finances current environmental projects that are associated with the

biodiversity and ecosystem through setting certain specific targets (Eccles and

Serafeim 2014). The company has minimum mandatory requirements for

environmental management that forms the addition to the local regulatory

requirements. The standard requires BHP Billiton to undertake the integrated risk

based approach to manage the impact on land, biodiversity, water and air.

Climate is considered as one of the important factor for BHP. The company has

aligned with the government and the other non-governmental organizations to

protect the environment (Merkl-Davies et al. 2016). BHP Billiton has implemented

Carbon Disclosure Project that has led to significant reduction as well as

improvement in carbon disclosure project scores over the last two years. The

company in combination with the Taskforce on Climate Related Disclosure has

comprehensively provided the climate related disclosure and the same is stated

below;

6CORPORATE ACCOUNTING

Explanation of Disclosure of opinion:

On analysing the annual report of the BHP Billiton it can be stated that the company

has provided a robust disclosure of the company’s overall performance (Barkemeyer et al.

2015). As the centre part of BHP Billiton involves mining activities the company has

provided a disclosure regarding the numerous features of mining and other environmental

related activities. The major areas covered in the disclosure includes;

a. Taxation and transparency

b. Environmental reports

c. Sustainability reports

d. Detailed disclosure of financial information

e. Report on energy consumption

f. Anti-competitive policy

g. Anti-corruption policy

Explanation of Disclosure of opinion:

On analysing the annual report of the BHP Billiton it can be stated that the company

has provided a robust disclosure of the company’s overall performance (Barkemeyer et al.

2015). As the centre part of BHP Billiton involves mining activities the company has

provided a disclosure regarding the numerous features of mining and other environmental

related activities. The major areas covered in the disclosure includes;

a. Taxation and transparency

b. Environmental reports

c. Sustainability reports

d. Detailed disclosure of financial information

e. Report on energy consumption

f. Anti-competitive policy

g. Anti-corruption policy

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

As evident from the above stated important disclosure elements BHP Billiton in its annual

statements has provided sufficient amount of disclosure regarding the all the necessary

elements contained in report.

Recommendations to top management to strengthen compliance in future reporting:

Two important recommendations can be provided to the top management as the

measure of strengthening the compliance in disclosure is stated below;

a. A recommendations can be provided to the top management regarding more use of

graphical representation of data relating to the financial performance of the company

(Bianchi Martini et al. 2016). The graphical representation should not only remain

limited to financial aspects but should also cover the environmental and biodiversity

report as well. This will enable the users in better understanding of the both the

financial and non-financial parameters.

b. Another recommendations can be made in the areas of sustainability reporting. This

includes more detailed information regarding the environmental impact and climate

change based on the quantitative as well as the qualitative aspects (Busco 2016). It is

recommended that BHP Billiton should provide a five year tabular representation

regarding carbon disclosure project. This would enable the users of financial

statement to make a comparative analysis and better overall understanding of the BHP

Billiton environmental related activities.

Answer to Part B:

Answer to question 1:

There are numerous vital aspects that are associated with the pre-acquisition entities

while preparing the consolidated financial statements. Below listed are some of the important

considerations;

As evident from the above stated important disclosure elements BHP Billiton in its annual

statements has provided sufficient amount of disclosure regarding the all the necessary

elements contained in report.

Recommendations to top management to strengthen compliance in future reporting:

Two important recommendations can be provided to the top management as the

measure of strengthening the compliance in disclosure is stated below;

a. A recommendations can be provided to the top management regarding more use of

graphical representation of data relating to the financial performance of the company

(Bianchi Martini et al. 2016). The graphical representation should not only remain

limited to financial aspects but should also cover the environmental and biodiversity

report as well. This will enable the users in better understanding of the both the

financial and non-financial parameters.

b. Another recommendations can be made in the areas of sustainability reporting. This

includes more detailed information regarding the environmental impact and climate

change based on the quantitative as well as the qualitative aspects (Busco 2016). It is

recommended that BHP Billiton should provide a five year tabular representation

regarding carbon disclosure project. This would enable the users of financial

statement to make a comparative analysis and better overall understanding of the BHP

Billiton environmental related activities.

Answer to Part B:

Answer to question 1:

There are numerous vital aspects that are associated with the pre-acquisition entities

while preparing the consolidated financial statements. Below listed are some of the important

considerations;

8CORPORATE ACCOUNTING

a. To avoid counting the assets twice of the concerned company.

b. The pre-acquisition entries helps in preventing the counting of equities twice of an

organization.

c. With the objective of identifying any form of gain or bargain procurement for an

organization.

Answer to question 2:

There are namely two major conditions that requires sufficient attention at the time of

paying dividend during the acquisition date of an organization. The below listed are the two

criteria’s;

a. Cum Dividend Payment: Given the circumstances that during the date of

acquisition, the subsidiary company paying the dividends and in such a situation it is

noticed that the dividends are declared and the same is included with the final sum in

the books of accounts of the company (Ioannou and Serafeim 2017). In the event of

cum dividend, even though the dividend is paid on the acquisition date, it is held for

deductions from the total amount of procurement worth of the merger. This results in

the acceptance of the dividends during the date of such acquisition (Dumay 2016). If

it is found that during the middle of the year, the procedure is repeated again then a

customary procedure is employed by the company to take the dividend and these

dividends are adjusted with the consolidated monetary reports at the end of the

financial year.

b. Payment of Ex-Dividend: On noticing that the subsidiary company is making

payment of the ex-dividend during the acquisition date, then such dividend is not

included into the financial statement the company and as a result this dividends are

not accounted into the while preparing the financial reports (Jin, Shan and Taylor

2015).

a. To avoid counting the assets twice of the concerned company.

b. The pre-acquisition entries helps in preventing the counting of equities twice of an

organization.

c. With the objective of identifying any form of gain or bargain procurement for an

organization.

Answer to question 2:

There are namely two major conditions that requires sufficient attention at the time of

paying dividend during the acquisition date of an organization. The below listed are the two

criteria’s;

a. Cum Dividend Payment: Given the circumstances that during the date of

acquisition, the subsidiary company paying the dividends and in such a situation it is

noticed that the dividends are declared and the same is included with the final sum in

the books of accounts of the company (Ioannou and Serafeim 2017). In the event of

cum dividend, even though the dividend is paid on the acquisition date, it is held for

deductions from the total amount of procurement worth of the merger. This results in

the acceptance of the dividends during the date of such acquisition (Dumay 2016). If

it is found that during the middle of the year, the procedure is repeated again then a

customary procedure is employed by the company to take the dividend and these

dividends are adjusted with the consolidated monetary reports at the end of the

financial year.

b. Payment of Ex-Dividend: On noticing that the subsidiary company is making

payment of the ex-dividend during the acquisition date, then such dividend is not

included into the financial statement the company and as a result this dividends are

not accounted into the while preparing the financial reports (Jin, Shan and Taylor

2015).

9CORPORATE ACCOUNTING

Answer to question 3:

The difference between the pre dividends and the post dividends are considered to be

the significant part of the financial report from the viewpoint of company (Perera and Chand

2015). When the dividend is declared by the company originating from the pre-acquisition

profits and then it is received by the purchaser then the sum of investment is entirely

subtracted from the total investment costs. Any form of dividend that is received from the

pre-acquisition profit is referred as the pre-acquisition dividend (Chand, Patel and White

2015). In the statement of profit and loss account the post dividends are credit and as a result

the dividends that are received obtained the profits of the post-acquisition it is defined as the

post-acquisition dividend. As a result of this differentiating between the origination sources is

necessary resulting the two dividends to be suffixes of pre and post.

Answer to question 4:

During the acquisition analysis procedure, the financial consideration that is

transferred is compared with several types of assets of the subsidiary company that is

acquired. However, the goodwill that is present in the books of accounts of the company is

not accounted as the identifiable assets (Newberry 2015). While in the subsidiary company

accounting books, the goodwill entirely omitted and does not forms the part of the books of

accounts of the subsidiary company.

There are namely two procedure of computing the value of goodwill. This includes

namely the partial goodwill method and the full goodwill method. Under each of the

identified procedure goodwill that is received on the date of acquisition by the subsidiary

company is treated separately (Cho et al. 2015). Under the partial goodwill method, goodwill

that are received from the transaction is recorded into the company’s books of accounts.

While in the full goodwill method there are certain reservations. Under the full goodwill

method the company takes into the consideration that goodwill that is received from the

Answer to question 3:

The difference between the pre dividends and the post dividends are considered to be

the significant part of the financial report from the viewpoint of company (Perera and Chand

2015). When the dividend is declared by the company originating from the pre-acquisition

profits and then it is received by the purchaser then the sum of investment is entirely

subtracted from the total investment costs. Any form of dividend that is received from the

pre-acquisition profit is referred as the pre-acquisition dividend (Chand, Patel and White

2015). In the statement of profit and loss account the post dividends are credit and as a result

the dividends that are received obtained the profits of the post-acquisition it is defined as the

post-acquisition dividend. As a result of this differentiating between the origination sources is

necessary resulting the two dividends to be suffixes of pre and post.

Answer to question 4:

During the acquisition analysis procedure, the financial consideration that is

transferred is compared with several types of assets of the subsidiary company that is

acquired. However, the goodwill that is present in the books of accounts of the company is

not accounted as the identifiable assets (Newberry 2015). While in the subsidiary company

accounting books, the goodwill entirely omitted and does not forms the part of the books of

accounts of the subsidiary company.

There are namely two procedure of computing the value of goodwill. This includes

namely the partial goodwill method and the full goodwill method. Under each of the

identified procedure goodwill that is received on the date of acquisition by the subsidiary

company is treated separately (Cho et al. 2015). Under the partial goodwill method, goodwill

that are received from the transaction is recorded into the company’s books of accounts.

While in the full goodwill method there are certain reservations. Under the full goodwill

method the company takes into the consideration that goodwill that is received from the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE ACCOUNTING

subsidiary company together with the goodwill that is earned during the company transaction.

The differences between such goodwill is computed and the difference is taken into the

consideration as the parent company goodwill.

Answer to question 5:

When a controlling interest is acquired by the parent company into the subsidiary then

the carrying value of the subsidiary assets is not equivalent to the fair value. Therefore, there

are certain adjustments that is required to be made (Chand, Patel and White 2015). An

important factor governing the adjustment is that there are net fair value of the assets that is

acquired in the amalgamation and consolidation procedure. When an organization obtains any

kind of assets during the acquisition procedure from the large pool of assets of other firm,

there requires a certain forms of adjustments.

The primary reason behind this is that when an asset is acquired by the company in

the acquisition procedure the asset possess certain specific sum of fair worth along with

certain market worth. There always prevails a differences between the two assets and this

results in providing true and fair view of the financial books of accounts since the assets is

reflected at the current net value in the consolidated financial reports (Jin, Shan and Taylor

2015). If the company fails to records these assets then they might have to pay higher amount

of taxes given that the market value of the assets is considered by ignoring the assets net

current worth. This would ultimately contribute to the loss of the company.

Conclusion:

The most important aspects of the corporate accounting is the existence of disclosure

reports of an organization activities. Corporate accounting is held as the significant tool of

measuring performance and it is associated with the numerous forms of operations that is

subsidiary company together with the goodwill that is earned during the company transaction.

The differences between such goodwill is computed and the difference is taken into the

consideration as the parent company goodwill.

Answer to question 5:

When a controlling interest is acquired by the parent company into the subsidiary then

the carrying value of the subsidiary assets is not equivalent to the fair value. Therefore, there

are certain adjustments that is required to be made (Chand, Patel and White 2015). An

important factor governing the adjustment is that there are net fair value of the assets that is

acquired in the amalgamation and consolidation procedure. When an organization obtains any

kind of assets during the acquisition procedure from the large pool of assets of other firm,

there requires a certain forms of adjustments.

The primary reason behind this is that when an asset is acquired by the company in

the acquisition procedure the asset possess certain specific sum of fair worth along with

certain market worth. There always prevails a differences between the two assets and this

results in providing true and fair view of the financial books of accounts since the assets is

reflected at the current net value in the consolidated financial reports (Jin, Shan and Taylor

2015). If the company fails to records these assets then they might have to pay higher amount

of taxes given that the market value of the assets is considered by ignoring the assets net

current worth. This would ultimately contribute to the loss of the company.

Conclusion:

The most important aspects of the corporate accounting is the existence of disclosure

reports of an organization activities. Corporate accounting is held as the significant tool of

measuring performance and it is associated with the numerous forms of operations that is

11CORPORATE ACCOUNTING

performed by the company along with the numerous aspects of operations that are performed

during the accounting year.

An organization usually gains value when in the disclosure report of the company

contains both the financial as well as the non-financial parameters. Likewise for the BHP

Billiton, the company has upheld the standards of disclosing both the financial and non-

financial information. The report also provides a discussion of pre and post-acquisition

entries and their overall adjustment. The report accordingly displays the corporate accounting

as the important tool of accounting in the modern world of financial disclosure.

performed by the company along with the numerous aspects of operations that are performed

during the accounting year.

An organization usually gains value when in the disclosure report of the company

contains both the financial as well as the non-financial parameters. Likewise for the BHP

Billiton, the company has upheld the standards of disclosing both the financial and non-

financial information. The report also provides a discussion of pre and post-acquisition

entries and their overall adjustment. The report accordingly displays the corporate accounting

as the important tool of accounting in the modern world of financial disclosure.

12CORPORATE ACCOUNTING

Reference List:

Crowther, D., 2016. A social critique of corporate reporting: Semiotics and web-based

integrated reporting. Routledge.

Kareiva, P.M., McNally, B.W., McCormick, S., Miller, T. and Ruckelshaus, M., 2015.

Improving global environmental management with standard corporate reporting. Proceedings

of the National Academy of Sciences, 112(24), pp.7375-7382.

Boyd, G. and Golden, J.S., 2016. Enhancing firm GHG reporting: using index numbers to

report corporate level measures of sustainability. International Journal of Green

Technology, 2, pp.29-37.

Stent, W. and Dowler, T., 2015. Early assessments of the gap between integrated reporting

and current corporate reporting. Meditari Accountancy Research, 23(1), pp.92-117.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting.

Eccles, R.G. and Serafeim, G., 2014. Corporate and integrated reporting: A functional

perspective.

Merkl-Davies, D.M., Brennan, N.M. and Vourvachis, P., 2016. Text Analysis Methodologies

in Corporate Reporting Narratives Research. In Conference Paper. Retrieved February 15th.

Barkemeyer, R., Stringer, L.C., Hollins, J.A. and Josephi, F., 2015. Corporate reporting on

solutions to wicked problems: Sustainable land management in the mining

sector. Environmental science & policy, 48, pp.196-209.

Reference List:

Crowther, D., 2016. A social critique of corporate reporting: Semiotics and web-based

integrated reporting. Routledge.

Kareiva, P.M., McNally, B.W., McCormick, S., Miller, T. and Ruckelshaus, M., 2015.

Improving global environmental management with standard corporate reporting. Proceedings

of the National Academy of Sciences, 112(24), pp.7375-7382.

Boyd, G. and Golden, J.S., 2016. Enhancing firm GHG reporting: using index numbers to

report corporate level measures of sustainability. International Journal of Green

Technology, 2, pp.29-37.

Stent, W. and Dowler, T., 2015. Early assessments of the gap between integrated reporting

and current corporate reporting. Meditari Accountancy Research, 23(1), pp.92-117.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting.

Eccles, R.G. and Serafeim, G., 2014. Corporate and integrated reporting: A functional

perspective.

Merkl-Davies, D.M., Brennan, N.M. and Vourvachis, P., 2016. Text Analysis Methodologies

in Corporate Reporting Narratives Research. In Conference Paper. Retrieved February 15th.

Barkemeyer, R., Stringer, L.C., Hollins, J.A. and Josephi, F., 2015. Corporate reporting on

solutions to wicked problems: Sustainable land management in the mining

sector. Environmental science & policy, 48, pp.196-209.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CORPORATE ACCOUNTING

Bianchi Martini, S., Corvino, A., Doni, F. and Rigolini, A., 2016. Relational capital

disclosure, corporate reporting and company performance: Evidence from Europe. Journal of

Intellectual capital, 17(2), pp.186-217.

Busco, C.A., 2016. Integrated Reporting. Springer,.

Ioannou, I. and Serafeim, G., 2017. The consequences of mandatory corporate sustainability

reporting.

Dumay, J., 2016. A critical reflection on the future of intellectual capital: from reporting to

disclosure. Journal of Intellectual capital, 17(1), pp.168-184.

Depoers, F., Jeanjean, T. and Jérôme, T., 2016. Voluntary disclosure of greenhouse gas

emissions: Contrasting the carbon disclosure project and corporate reports. Journal of

Business Ethics, 134(3), pp.445-461.

Depoers, F., Jeanjean, T. and Jérôme, T., 2016. Voluntary disclosure of greenhouse gas

emissions: Contrasting the carbon disclosure project and corporate reports. Journal of

Business Ethics, 134(3), pp.445-461.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in

Accounting, 31(1), pp.165-178.

Chand, P., Patel, A. and White, M., 2015. Adopting international financial reporting

standards for small and medium‐sized enterprises. Australian Accounting Review, 25(2),

pp.139-154.

Bianchi Martini, S., Corvino, A., Doni, F. and Rigolini, A., 2016. Relational capital

disclosure, corporate reporting and company performance: Evidence from Europe. Journal of

Intellectual capital, 17(2), pp.186-217.

Busco, C.A., 2016. Integrated Reporting. Springer,.

Ioannou, I. and Serafeim, G., 2017. The consequences of mandatory corporate sustainability

reporting.

Dumay, J., 2016. A critical reflection on the future of intellectual capital: from reporting to

disclosure. Journal of Intellectual capital, 17(1), pp.168-184.

Depoers, F., Jeanjean, T. and Jérôme, T., 2016. Voluntary disclosure of greenhouse gas

emissions: Contrasting the carbon disclosure project and corporate reports. Journal of

Business Ethics, 134(3), pp.445-461.

Depoers, F., Jeanjean, T. and Jérôme, T., 2016. Voluntary disclosure of greenhouse gas

emissions: Contrasting the carbon disclosure project and corporate reports. Journal of

Business Ethics, 134(3), pp.445-461.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in

Accounting, 31(1), pp.165-178.

Chand, P., Patel, A. and White, M., 2015. Adopting international financial reporting

standards for small and medium‐sized enterprises. Australian Accounting Review, 25(2),

pp.139-154.

14CORPORATE ACCOUNTING

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Cho, C.H., Laine, M., Roberts, R.W. and Rodrigue, M., 2015. Organized hypocrisy,

organizational façades, and sustainability reporting. Accounting, Organizations and

Society, 40, pp.78-94.

BHP Billiton. (2018). BHP Annual Reporting 2017. [online] Available at:

https://www.bhp.com/investor-centre/annual-reporting-2017 [Accessed 31 May 2018].

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Cho, C.H., Laine, M., Roberts, R.W. and Rodrigue, M., 2015. Organized hypocrisy,

organizational façades, and sustainability reporting. Accounting, Organizations and

Society, 40, pp.78-94.

BHP Billiton. (2018). BHP Annual Reporting 2017. [online] Available at:

https://www.bhp.com/investor-centre/annual-reporting-2017 [Accessed 31 May 2018].

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.