Corporate Accounting Report: Financial Analysis of Two Companies

VerifiedAdded on 2022/08/24

|11

|3173

|16

Report

AI Summary

This report offers a detailed analysis of corporate accounting practices, focusing on the financial performance of Boral Ltd and Evolution Mining Ltd for the year 2019. It examines the companies' capital structures, comparing their use of debt and equity financing, and analyzes trends in capital mix over time. The report also explores the pros and cons of different funding sources and assesses how the companies report their assets and liabilities, including provisions, contingent liabilities, and contingent assets in accordance with AASB 137. Furthermore, the analysis includes an examination of the recognition criteria for assets and the overall financial performance of the businesses, providing a comprehensive overview of their accounting and financial strategies as presented in their annual reports.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive Summary

The main purpose of the analysis is to identify the reporting process which is

followed by the businesses of Boral and Evolution Mining Ltd for the year 2019. The

analysis also shows past year trends in terms of increase or decrease in equity and

debt capital which is used by the management of the company. The assessment

also discloses the reporting pattern for assets and liabilities which are used by the

business along with appropriate disclosures which are shown in the financial

statements of the business. The financial performance of the business is also shown

in numerical terms in the analysis which is covered below in details.

CORPORATE ACCOUNTING

Executive Summary

The main purpose of the analysis is to identify the reporting process which is

followed by the businesses of Boral and Evolution Mining Ltd for the year 2019. The

analysis also shows past year trends in terms of increase or decrease in equity and

debt capital which is used by the management of the company. The assessment

also discloses the reporting pattern for assets and liabilities which are used by the

business along with appropriate disclosures which are shown in the financial

statements of the business. The financial performance of the business is also shown

in numerical terms in the analysis which is covered below in details.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction...................................................................................................................3

Discussion....................................................................................................................3

Different sources of Funds........................................................................................3

Changes in the Capital Mix.......................................................................................4

Percentage of Different Sources of Funds................................................................5

Pros and Cons of Different Sources of Business.....................................................5

Liabilities of the Businesses......................................................................................6

Provisions, Contingent Liabilities and Contingent Assets........................................7

Reporting for AASB 137............................................................................................7

Classification of Assets.............................................................................................8

Recognition Criteria...................................................................................................9

Conclusion....................................................................................................................9

Reference...................................................................................................................10

CORPORATE ACCOUNTING

Table of Contents

Introduction...................................................................................................................3

Discussion....................................................................................................................3

Different sources of Funds........................................................................................3

Changes in the Capital Mix.......................................................................................4

Percentage of Different Sources of Funds................................................................5

Pros and Cons of Different Sources of Business.....................................................5

Liabilities of the Businesses......................................................................................6

Provisions, Contingent Liabilities and Contingent Assets........................................7

Reporting for AASB 137............................................................................................7

Classification of Assets.............................................................................................8

Recognition Criteria...................................................................................................9

Conclusion....................................................................................................................9

Reference...................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction

The process of accounting is a dynamic process which effectively records all

transactions and presents the financial information of a business in a report format

so that the investors can take decisions based on the same. In most of businesses,

some funds are required for appropriately funding the activities and carrying outs its

work processes. The assessment considers a similar direction for analysis and

considers two companies which belong to the same industry for the purpose of

analysis. The companies which are selected are Evolution Mining Group and Boral

Ltd which are engaged in mining activities and are listed in ASX. The corporate

reporting process which is followed by this company would be considered in the

analysis in terms of assets and liabilities which are reported in the annual reports of

the companies (Maas, Schaltegger and Crutzen 2016). Further the assessment

would be identifying if there is any presence of provisions or contingent liabilities or

contingent assets in either of the companies so that adherence to AASB 137

‘Provisions, Contingent Liabilities and Contingent Assets” can be established.

Discussion

Different sources of Funds

The sources of funds which is utilized by a business are mainly equity capital

and debt capital for which an appropriate mixture is made regarding the source of

funds which is used by a business. The funds are used by businesses for the

purpose of conducting different activities of a business. The annual report for the

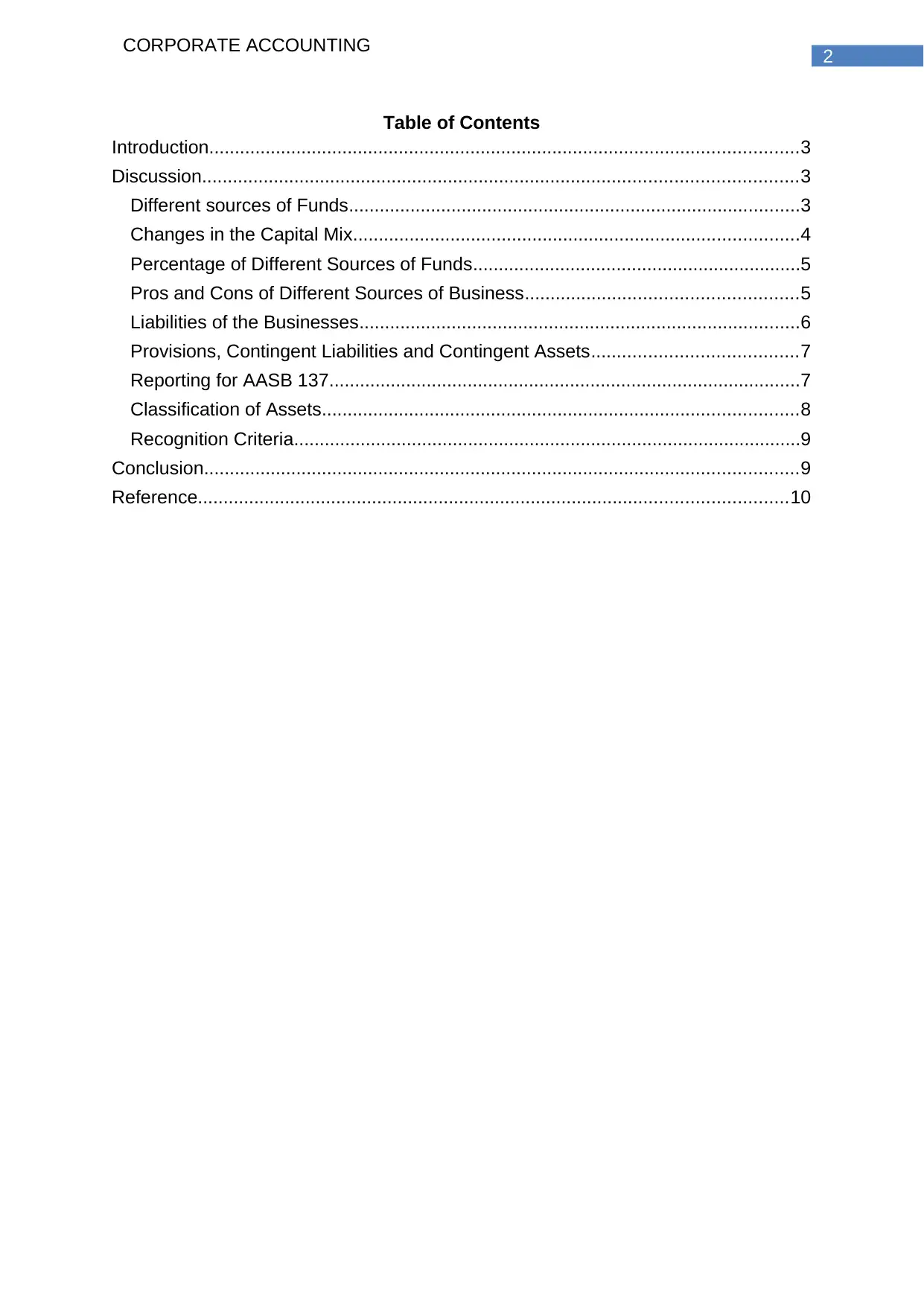

business of Evolution Mining Ltd is considered for 2019 and the same shows that the

business utilizes both debt and equity capitals for the purpose of financing the

operations and also for meeting urgent obligations of the business (Bennett,

Schaltegger and Zvezdov 2013). The debt and equity mixture for the business for the

year shows that around 92% of the capital is funded by equity capital and the same

has increased from previous year which shows that Evolution Mining Ltd is more

reliant on utilization of equity capital in replacement of debt capital.

Figure 1: (Capital Mix from the Balance Sheet of Evolution Mining Ltd)

Source: (Evolutionmining.com.au. 2020)

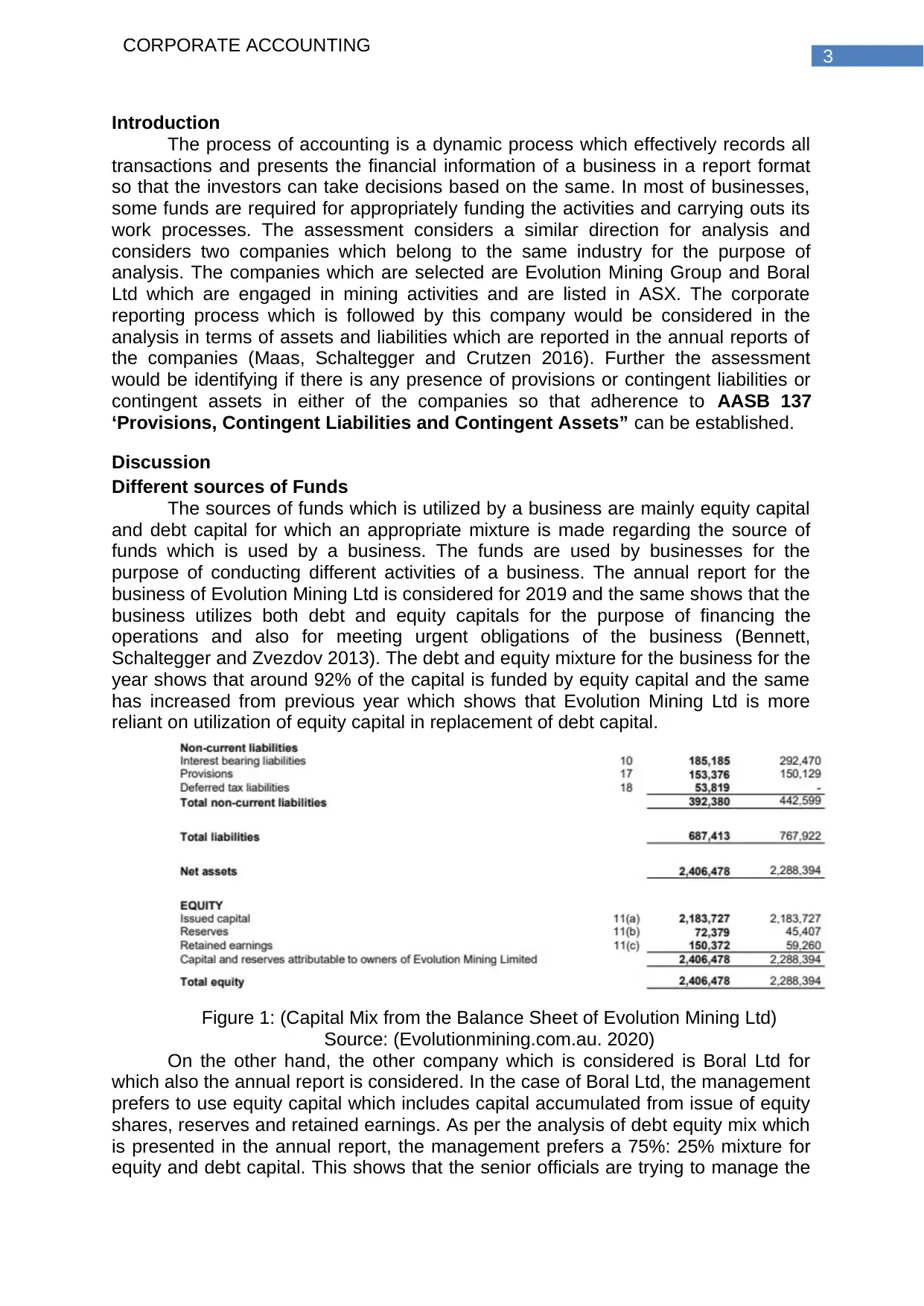

On the other hand, the other company which is considered is Boral Ltd for

which also the annual report is considered. In the case of Boral Ltd, the management

prefers to use equity capital which includes capital accumulated from issue of equity

shares, reserves and retained earnings. As per the analysis of debt equity mix which

is presented in the annual report, the management prefers a 75%: 25% mixture for

equity and debt capital. This shows that the senior officials are trying to manage the

CORPORATE ACCOUNTING

Introduction

The process of accounting is a dynamic process which effectively records all

transactions and presents the financial information of a business in a report format

so that the investors can take decisions based on the same. In most of businesses,

some funds are required for appropriately funding the activities and carrying outs its

work processes. The assessment considers a similar direction for analysis and

considers two companies which belong to the same industry for the purpose of

analysis. The companies which are selected are Evolution Mining Group and Boral

Ltd which are engaged in mining activities and are listed in ASX. The corporate

reporting process which is followed by this company would be considered in the

analysis in terms of assets and liabilities which are reported in the annual reports of

the companies (Maas, Schaltegger and Crutzen 2016). Further the assessment

would be identifying if there is any presence of provisions or contingent liabilities or

contingent assets in either of the companies so that adherence to AASB 137

‘Provisions, Contingent Liabilities and Contingent Assets” can be established.

Discussion

Different sources of Funds

The sources of funds which is utilized by a business are mainly equity capital

and debt capital for which an appropriate mixture is made regarding the source of

funds which is used by a business. The funds are used by businesses for the

purpose of conducting different activities of a business. The annual report for the

business of Evolution Mining Ltd is considered for 2019 and the same shows that the

business utilizes both debt and equity capitals for the purpose of financing the

operations and also for meeting urgent obligations of the business (Bennett,

Schaltegger and Zvezdov 2013). The debt and equity mixture for the business for the

year shows that around 92% of the capital is funded by equity capital and the same

has increased from previous year which shows that Evolution Mining Ltd is more

reliant on utilization of equity capital in replacement of debt capital.

Figure 1: (Capital Mix from the Balance Sheet of Evolution Mining Ltd)

Source: (Evolutionmining.com.au. 2020)

On the other hand, the other company which is considered is Boral Ltd for

which also the annual report is considered. In the case of Boral Ltd, the management

prefers to use equity capital which includes capital accumulated from issue of equity

shares, reserves and retained earnings. As per the analysis of debt equity mix which

is presented in the annual report, the management prefers a 75%: 25% mixture for

equity and debt capital. This shows that the senior officials are trying to manage the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

risks which equity capital brings into the fold. An extract from the balance sheet for

the company is shown below reflecting the capital mixture which is used by the

business for the purpose of financing the activities of the business.

Figure 2: (Capital Mix from the Balance Sheet of Boral Ltd)

Source: (Boral.com. 2020)

Changes in the Capital Mix

The decision to use a particular source of fund lies with the senior

management of a company and therefore it is probable that it will be changing over a

particular time period. The annual report for the present period as well past years

would be considered for identifying the trend in the capital mix which is used by a

business. The situation for Evolution Mining Ltd reveals that the business is trying to

reduce the debt capital which is utilized by the business and increase the equity

capital mix for the business. The debt capital which is used by the management is

shown to be $ 292.47 million in 2018 which is then shown to have reduced in 2019

and the amount is shown to be $ 185.19 million in 2019. In addition to this, the equity

sources of capital such as reserves and retained earnings have increased over the

years which shows that the management is dedicated to reduce the risks which is

associated with the use of debt capital in a business.

On the other hand, the senior officials of Boral Ltd are also trying to attain an

optimum capital structure which can manage the risks and return for the business

appropriately. The senior executives have reduced the debt capital over the years

while at the same time increase the equity capital mixture for the business (Tschopp

and Nastanski 2014). The objective of the senior management is to currently achieve

a lower risk status in the operations and thereby also maintain efficiency in the

operations of the business. The management of Boral Ltd is trying to ensure that

interest burden over the company is lower as the same directly impacts the finance

costs.

CORPORATE ACCOUNTING

risks which equity capital brings into the fold. An extract from the balance sheet for

the company is shown below reflecting the capital mixture which is used by the

business for the purpose of financing the activities of the business.

Figure 2: (Capital Mix from the Balance Sheet of Boral Ltd)

Source: (Boral.com. 2020)

Changes in the Capital Mix

The decision to use a particular source of fund lies with the senior

management of a company and therefore it is probable that it will be changing over a

particular time period. The annual report for the present period as well past years

would be considered for identifying the trend in the capital mix which is used by a

business. The situation for Evolution Mining Ltd reveals that the business is trying to

reduce the debt capital which is utilized by the business and increase the equity

capital mix for the business. The debt capital which is used by the management is

shown to be $ 292.47 million in 2018 which is then shown to have reduced in 2019

and the amount is shown to be $ 185.19 million in 2019. In addition to this, the equity

sources of capital such as reserves and retained earnings have increased over the

years which shows that the management is dedicated to reduce the risks which is

associated with the use of debt capital in a business.

On the other hand, the senior officials of Boral Ltd are also trying to attain an

optimum capital structure which can manage the risks and return for the business

appropriately. The senior executives have reduced the debt capital over the years

while at the same time increase the equity capital mixture for the business (Tschopp

and Nastanski 2014). The objective of the senior management is to currently achieve

a lower risk status in the operations and thereby also maintain efficiency in the

operations of the business. The management of Boral Ltd is trying to ensure that

interest burden over the company is lower as the same directly impacts the finance

costs.

5

CORPORATE ACCOUNTING

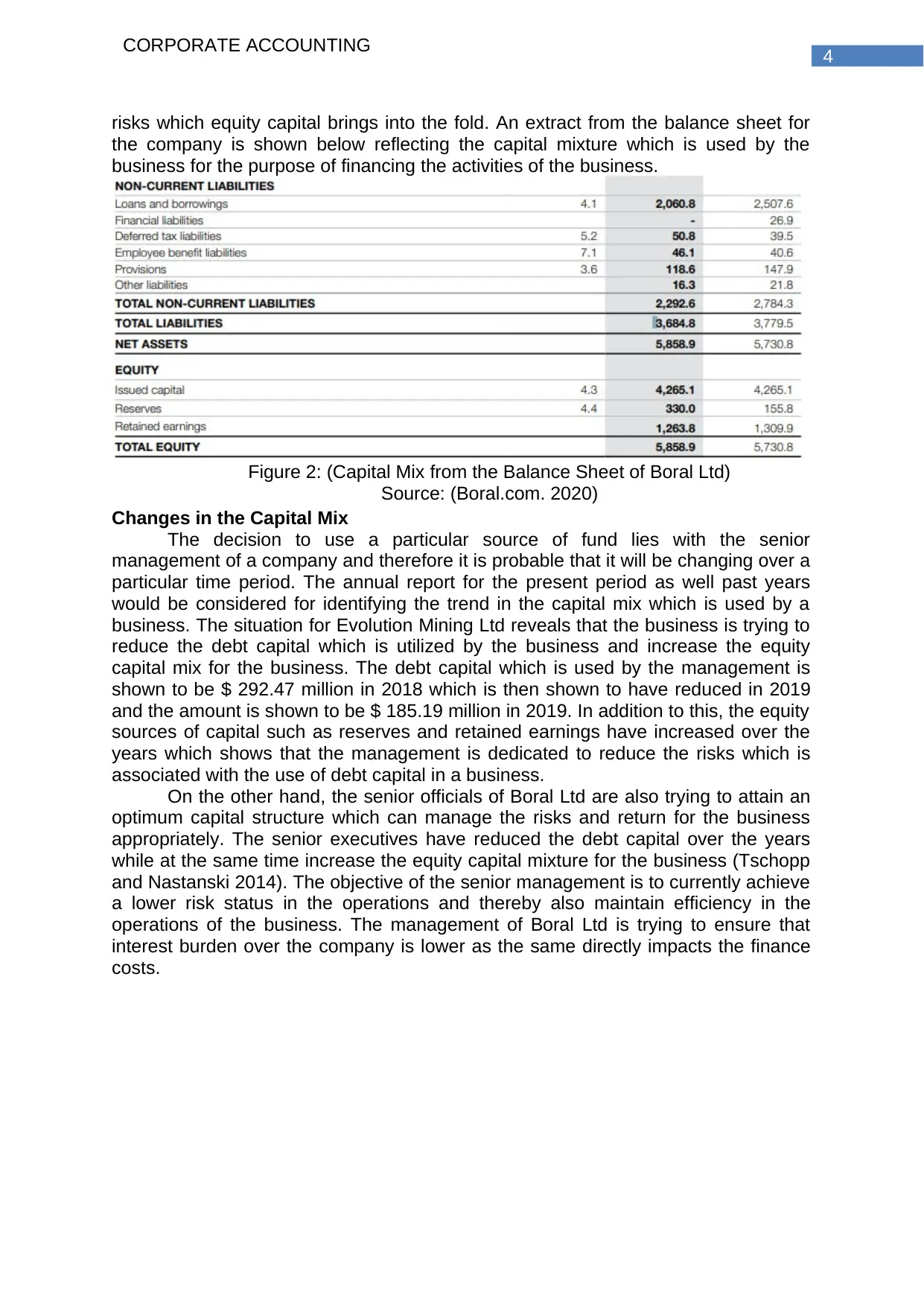

Percentage of Different Sources of Funds

Figure 3: (Percentage of Funds used by both of the Companies)

Source: (Created by the Author)

The above table shows the different mixes for capital which is used by both

the companies and the same is represented in the form of percentage and the

percentage for the same has changed over the years for both the companies which

shows that both companies has made changes in the capital structure which is

utilized by the business. In the case of both the companies, it is evident that the

management is using more percentage of equity capital and slightly adding debt

capital for the purpose of achieving the leverage effective.

Pros and Cons of Different Sources of Business

The different sources of funds which is used by different businesses helps the

businesses to appropriate select the most appropriate source of capital which is

utilized by the business. The capital structure which is used by the business of Boral

Ltd and Evolution Mining Ltd is mostly similar and therefore the same are discussed

in details along with pros and cons below:

Equity Share Capital

Advantages

The application of equity capital source in a business is considered to be

permanent and therefore it is one of the most preferred source of financing for

the business (Christensen, Cottrell and Baker 2013). The repayment for such

a source of funding is not required unless the business goes into liquidation.

The business which is utilizing such a fund source has no obligation to pay

regular dividends and the percentage and payments of dividends depend on

the profit margin which is achieved by the business.

Disadvantages

The use of equity capital does not provide any other advantage to the

business such as tax benefits or leverage effect in the operations of the

business. In addition to this, use of equity share capital is considered to be a

costly source of capital considering the nature of operations of the business.

The use of equity segregates the ownership of the business among the

shareholders and therefore hampers quick decision making process for a

business.

CORPORATE ACCOUNTING

Percentage of Different Sources of Funds

Figure 3: (Percentage of Funds used by both of the Companies)

Source: (Created by the Author)

The above table shows the different mixes for capital which is used by both

the companies and the same is represented in the form of percentage and the

percentage for the same has changed over the years for both the companies which

shows that both companies has made changes in the capital structure which is

utilized by the business. In the case of both the companies, it is evident that the

management is using more percentage of equity capital and slightly adding debt

capital for the purpose of achieving the leverage effective.

Pros and Cons of Different Sources of Business

The different sources of funds which is used by different businesses helps the

businesses to appropriate select the most appropriate source of capital which is

utilized by the business. The capital structure which is used by the business of Boral

Ltd and Evolution Mining Ltd is mostly similar and therefore the same are discussed

in details along with pros and cons below:

Equity Share Capital

Advantages

The application of equity capital source in a business is considered to be

permanent and therefore it is one of the most preferred source of financing for

the business (Christensen, Cottrell and Baker 2013). The repayment for such

a source of funding is not required unless the business goes into liquidation.

The business which is utilizing such a fund source has no obligation to pay

regular dividends and the percentage and payments of dividends depend on

the profit margin which is achieved by the business.

Disadvantages

The use of equity capital does not provide any other advantage to the

business such as tax benefits or leverage effect in the operations of the

business. In addition to this, use of equity share capital is considered to be a

costly source of capital considering the nature of operations of the business.

The use of equity segregates the ownership of the business among the

shareholders and therefore hampers quick decision making process for a

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

Debt Capital

Advantages

One of the main advantage of using debt capital in a business is the leverage

effect which is brought into the equation and the same reduces the impact of

taxes as interest payments which is associated with debt capital is tax

deductible.

In addition to this, the ownership in case of debt capital does not segregate

and therefore the management of a company is free to take quick decisions

for the operations of the business.

Disadvantages

The interest burden which the management of the company needs to bear in

case of debt capital is one of the main disadvantages and the same creates a

charge against the profits which is generated by the business. The interest

burden is one of the major factors which discourages businesses against use

of debt capital.

The use of debt capital in a business always comes against a collateral

security and therefore in most of the cases, it creates a charge against the

asset which is to be used by the business.

Retained Earnings

Advantages

The retained earnings do not form of capital which is collected by issue of

shares but the same is created through savings which is accumulated by the

business.

Disadvantages

The use of this form of capital impacts the reserves which are kept by the

business and depletes the same and therefore in case of emergency, the

business would be helpless.

Liabilities of the Businesses

The liabilities are obligation which every business needs to pay and the same

are represented appropriately in the balance sheet of the company in an appropriate

presentation. It is to be noted that the total of the liabilities and equity for a business

must be equal to the assets which is possessed by the business. The annual report

for the business of Evolution Mining Ltd shows the breakup of total liabilities on the

basis of current and non-liabilities (Christ and Burritt 2017). The current liabilities

section for Evolution Mining Ltd shows that the liabilities which are of current nature

and includes short term loans, trade payables, provisions which is created by the

business. The trade payables are the largest amount which is shown in the balance

sheet which is of $ 156.83 million and the same is shown to have increased

significantly over the period. In the case of non-current liabilities, interest bearing

liabilities is the largest amount presented and the figure for the same is shown to be

$ 185.16 million. The business is trying to reduce the debt capital for the business

which is evident from the reduction of debt which is used by the business. Another

item which is presented in the financial statements is deferred tax liabilities which are

shown to be of $ 53.19 million for 2019.

The annual position for the business which is represented in the financial

statements is clear for Boral Ltd for 2019. The presentation of financial information

shows that the management has appropriately presented financial information

especially liabilities with appropriate disclosures relating to the same. The managers

of Boral ltd reveal that trade payables and short-term loans for the entity is at the

values of $ 832.6 million and $ 339.7 million. The balance of employee based

CORPORATE ACCOUNTING

Debt Capital

Advantages

One of the main advantage of using debt capital in a business is the leverage

effect which is brought into the equation and the same reduces the impact of

taxes as interest payments which is associated with debt capital is tax

deductible.

In addition to this, the ownership in case of debt capital does not segregate

and therefore the management of a company is free to take quick decisions

for the operations of the business.

Disadvantages

The interest burden which the management of the company needs to bear in

case of debt capital is one of the main disadvantages and the same creates a

charge against the profits which is generated by the business. The interest

burden is one of the major factors which discourages businesses against use

of debt capital.

The use of debt capital in a business always comes against a collateral

security and therefore in most of the cases, it creates a charge against the

asset which is to be used by the business.

Retained Earnings

Advantages

The retained earnings do not form of capital which is collected by issue of

shares but the same is created through savings which is accumulated by the

business.

Disadvantages

The use of this form of capital impacts the reserves which are kept by the

business and depletes the same and therefore in case of emergency, the

business would be helpless.

Liabilities of the Businesses

The liabilities are obligation which every business needs to pay and the same

are represented appropriately in the balance sheet of the company in an appropriate

presentation. It is to be noted that the total of the liabilities and equity for a business

must be equal to the assets which is possessed by the business. The annual report

for the business of Evolution Mining Ltd shows the breakup of total liabilities on the

basis of current and non-liabilities (Christ and Burritt 2017). The current liabilities

section for Evolution Mining Ltd shows that the liabilities which are of current nature

and includes short term loans, trade payables, provisions which is created by the

business. The trade payables are the largest amount which is shown in the balance

sheet which is of $ 156.83 million and the same is shown to have increased

significantly over the period. In the case of non-current liabilities, interest bearing

liabilities is the largest amount presented and the figure for the same is shown to be

$ 185.16 million. The business is trying to reduce the debt capital for the business

which is evident from the reduction of debt which is used by the business. Another

item which is presented in the financial statements is deferred tax liabilities which are

shown to be of $ 53.19 million for 2019.

The annual position for the business which is represented in the financial

statements is clear for Boral Ltd for 2019. The presentation of financial information

shows that the management has appropriately presented financial information

especially liabilities with appropriate disclosures relating to the same. The managers

of Boral ltd reveal that trade payables and short-term loans for the entity is at the

values of $ 832.6 million and $ 339.7 million. The balance of employee based

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

liabilities and provisions are appropriately presented in the financial statements

(Warren and Jones 2018). The non-current liability which is presented by the

business is shown to be loans and other interest based liabilities for the business.

The liabilities of the business in terms of total figure are represented to be a little

higher than previous year.

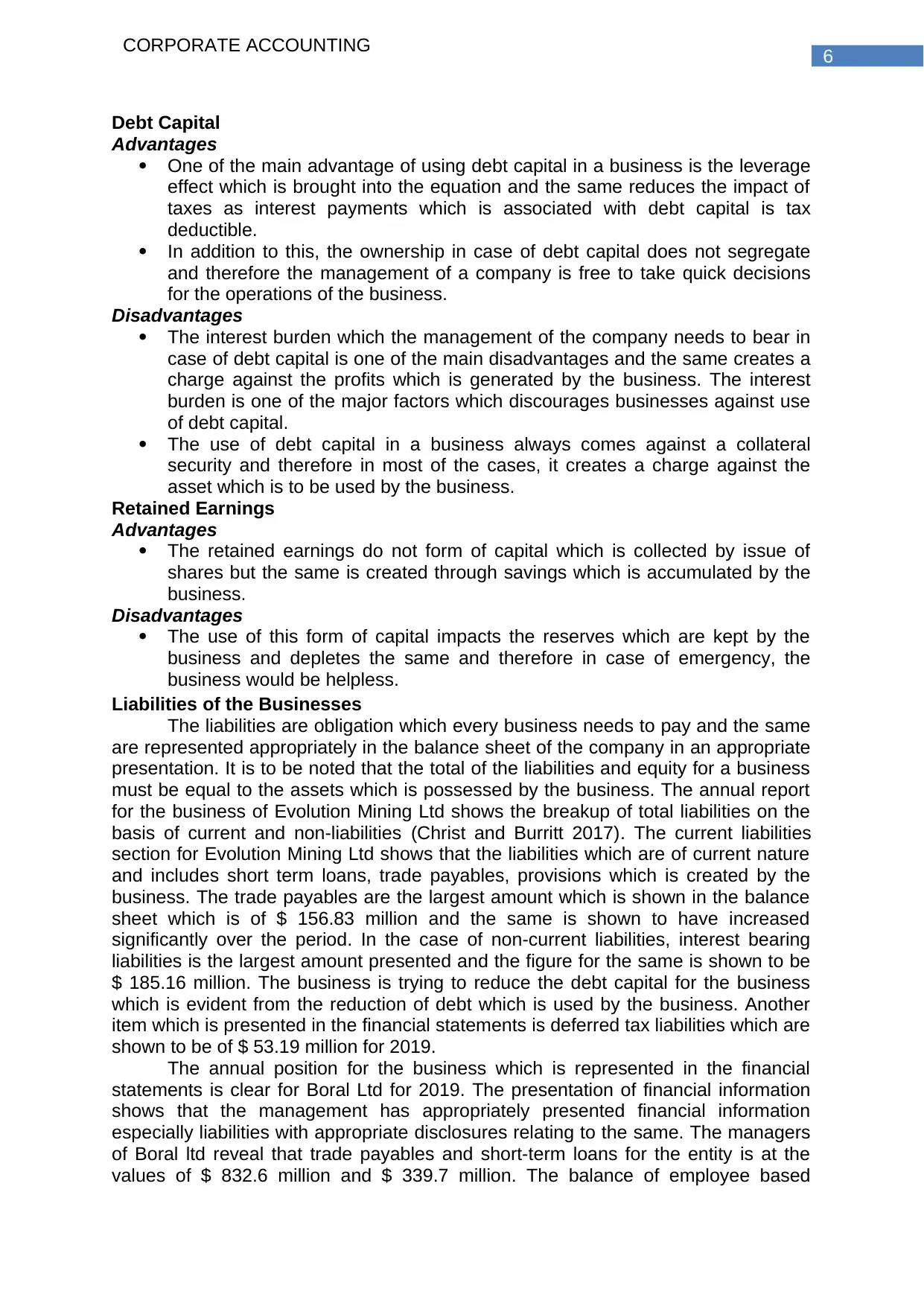

Provisions, Contingent Liabilities and Contingent Assets

The provisions which is stated in by AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets”, makes it clear that the these items needs to be

represented in the financial statements of the business for better presentation of

financial information of the business. The standard further points out that proper

disclosures needs to provided so that a level of transparency is maintained in the

reporting framework of the business (Honggowati et al. 2017). The standard requires

businesses to appropriately disclose all losses or [provisions which is created by the

business during the period.

Reporting for AASB 137

The business of Evolution Mining Ltd has appropriately presented the

contingent assets, liabilities and provisions in the annual report and the same is

provided as per the requirement of relevant accounting standard of the business. An

extract of the reporting process which is provided in the financial statement is

presented below:

The group has claims and guarantees which are covered in the annual report

of the company and the same is properly presented with full disclosures. The above

extracts shows the disclosures which is provided and the same is also evidence of

the adjustment which is made by the business in terms of such elements in the

financial statements.

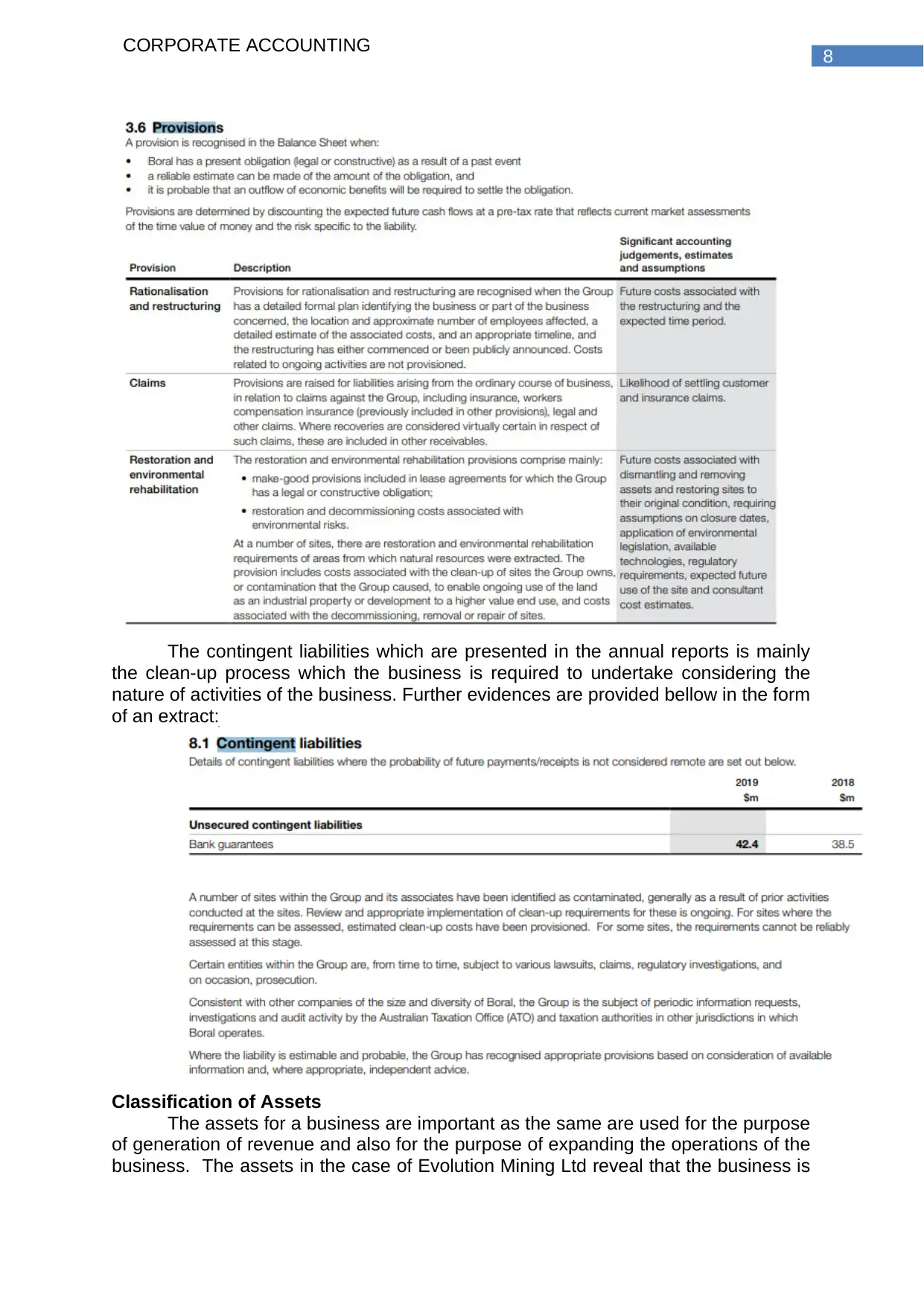

In the case of Boral Ltd, the senior officials of the business have also taken

appropriate steps for presenting the contingent liabilities and provisions so that a

level of accuracy is maintained. The business during the period has created

provision of $ 23.8 million for a restoration project of a limestone quarry and in

addition to this; the company has also made provisions for various losses which is

estimated by the business (Ramanna 2013). An extract of the notes to accounts of

the business is presented below showing the disclosures which is provided by the

management.

CORPORATE ACCOUNTING

liabilities and provisions are appropriately presented in the financial statements

(Warren and Jones 2018). The non-current liability which is presented by the

business is shown to be loans and other interest based liabilities for the business.

The liabilities of the business in terms of total figure are represented to be a little

higher than previous year.

Provisions, Contingent Liabilities and Contingent Assets

The provisions which is stated in by AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets”, makes it clear that the these items needs to be

represented in the financial statements of the business for better presentation of

financial information of the business. The standard further points out that proper

disclosures needs to provided so that a level of transparency is maintained in the

reporting framework of the business (Honggowati et al. 2017). The standard requires

businesses to appropriately disclose all losses or [provisions which is created by the

business during the period.

Reporting for AASB 137

The business of Evolution Mining Ltd has appropriately presented the

contingent assets, liabilities and provisions in the annual report and the same is

provided as per the requirement of relevant accounting standard of the business. An

extract of the reporting process which is provided in the financial statement is

presented below:

The group has claims and guarantees which are covered in the annual report

of the company and the same is properly presented with full disclosures. The above

extracts shows the disclosures which is provided and the same is also evidence of

the adjustment which is made by the business in terms of such elements in the

financial statements.

In the case of Boral Ltd, the senior officials of the business have also taken

appropriate steps for presenting the contingent liabilities and provisions so that a

level of accuracy is maintained. The business during the period has created

provision of $ 23.8 million for a restoration project of a limestone quarry and in

addition to this; the company has also made provisions for various losses which is

estimated by the business (Ramanna 2013). An extract of the notes to accounts of

the business is presented below showing the disclosures which is provided by the

management.

8

CORPORATE ACCOUNTING

The contingent liabilities which are presented in the annual reports is mainly

the clean-up process which the business is required to undertake considering the

nature of activities of the business. Further evidences are provided bellow in the form

of an extract:

Classification of Assets

The assets for a business are important as the same are used for the purpose

of generation of revenue and also for the purpose of expanding the operations of the

business. The assets in the case of Evolution Mining Ltd reveal that the business is

CORPORATE ACCOUNTING

The contingent liabilities which are presented in the annual reports is mainly

the clean-up process which the business is required to undertake considering the

nature of activities of the business. Further evidences are provided bellow in the form

of an extract:

Classification of Assets

The assets for a business are important as the same are used for the purpose

of generation of revenue and also for the purpose of expanding the operations of the

business. The assets in the case of Evolution Mining Ltd reveal that the business is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

following conceptual framework for the purpose of reporting and has shown

classification on the basis of current assets and non-current assets (Zeitun and Tian

2014). The current assets involve trade receivables, other current assets and tax

assets while non-current assets contain fixed assets for the business. The assets of

the business are fairly represented along with proper disclosures related to the

same.

The management of Boral Ltd has also presented similar aspects in reporting

and properly provided classification of the assets along with proper disclosures

related to the same. As both the companies are from mining industry therefore, the

assets and liabilities which are shown in case of both the companies are quite

similar.

Recognition Criteria

The recognition of different aspects of reporting for both the companies are

done on the basis of conceptual framework and the sane also involves guidance’s

which is from relevant accounting standards. Fixed assets for both the companies

are measured at cost less accumulated depreciation and impairment losses. The

inventory for both the companies is followed either in cost basis or market value

basis (Uyar 2016). In addition to this, ledger accounts are used for the

mathematically accuracy of the financial statements of the business. The recognition

criteria which is followed by the business is appropriately presented in the notes to

accounts section of the annual reports.

Conclusion

The above analysis effectively shows the information which is shown in the

financial statements of a business considering different elements which are covered

in the annual report of a business. The analysis covers the types of capital which is

utilize by the business for the purpose of financing the operations of the business

and also shows changes in the capital structure of the business during the period.

Both the companies, Evolution Mining Ltd and Boral Ltd is shown to have more

reliance on equity share capital more than debt capital for the business. The analysis

also covers reporting for items which are extraordinary in nature such as contingent

assets and liabilities and whether the same has been included in the financial

statements of the business.

Reference

CORPORATE ACCOUNTING

following conceptual framework for the purpose of reporting and has shown

classification on the basis of current assets and non-current assets (Zeitun and Tian

2014). The current assets involve trade receivables, other current assets and tax

assets while non-current assets contain fixed assets for the business. The assets of

the business are fairly represented along with proper disclosures related to the

same.

The management of Boral Ltd has also presented similar aspects in reporting

and properly provided classification of the assets along with proper disclosures

related to the same. As both the companies are from mining industry therefore, the

assets and liabilities which are shown in case of both the companies are quite

similar.

Recognition Criteria

The recognition of different aspects of reporting for both the companies are

done on the basis of conceptual framework and the sane also involves guidance’s

which is from relevant accounting standards. Fixed assets for both the companies

are measured at cost less accumulated depreciation and impairment losses. The

inventory for both the companies is followed either in cost basis or market value

basis (Uyar 2016). In addition to this, ledger accounts are used for the

mathematically accuracy of the financial statements of the business. The recognition

criteria which is followed by the business is appropriately presented in the notes to

accounts section of the annual reports.

Conclusion

The above analysis effectively shows the information which is shown in the

financial statements of a business considering different elements which are covered

in the annual report of a business. The analysis covers the types of capital which is

utilize by the business for the purpose of financing the operations of the business

and also shows changes in the capital structure of the business during the period.

Both the companies, Evolution Mining Ltd and Boral Ltd is shown to have more

reliance on equity share capital more than debt capital for the business. The analysis

also covers reporting for items which are extraordinary in nature such as contingent

assets and liabilities and whether the same has been included in the financial

statements of the business.

Reference

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Bennett, M.D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices

in management accounting for sustainability (pp. 1-56). London: ICAEW.

Boral.com. (2020). Annual Reports | Boral. [online] Available at:

https://www.boral.com/news/annual-reports [Accessed 14 Jan. 2020].

Christ, K.L. and Burritt, R.L., 2017. Water management accounting: A framework for

corporate practice. Journal of cleaner production, 152, pp.379-386.

Christensen, T., Cottrell, D. and Baker, R., 2013. Advanced financial accounting.

McGraw-Hill.

Evolutionmining.com.au. (2020). Reports – Evolution Mining. [online] Available at:

https://evolutionmining.com.au/reports/ [Accessed 23 Jan. 2020].

Honggowati, S., Rahmawati, R., Aryani, Y.A. and Probohudono, A.N., 2017.

Corporate governance and strategic management accounting disclosure. Indonesian

Journal of Sustainability Accounting and Management, 1(1), pp.23-30.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Ramanna, K., 2013. A framework for research on corporate accountability

reporting. Accounting Horizons, 27(2), pp.409-432.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of

corporate social responsibility reporting standards. Journal of Business

Ethics, 125(1), pp.147-162.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of

Corporate Accounting & Finance, 27(4), pp.27-30.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Zeitun, R. and Tian, G.G., 2014. Capital structure and corporate performance:

evidence from Jordan. Australasian Accounting Business & Finance Journal,

Forthcoming.

CORPORATE ACCOUNTING

Bennett, M.D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices

in management accounting for sustainability (pp. 1-56). London: ICAEW.

Boral.com. (2020). Annual Reports | Boral. [online] Available at:

https://www.boral.com/news/annual-reports [Accessed 14 Jan. 2020].

Christ, K.L. and Burritt, R.L., 2017. Water management accounting: A framework for

corporate practice. Journal of cleaner production, 152, pp.379-386.

Christensen, T., Cottrell, D. and Baker, R., 2013. Advanced financial accounting.

McGraw-Hill.

Evolutionmining.com.au. (2020). Reports – Evolution Mining. [online] Available at:

https://evolutionmining.com.au/reports/ [Accessed 23 Jan. 2020].

Honggowati, S., Rahmawati, R., Aryani, Y.A. and Probohudono, A.N., 2017.

Corporate governance and strategic management accounting disclosure. Indonesian

Journal of Sustainability Accounting and Management, 1(1), pp.23-30.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Ramanna, K., 2013. A framework for research on corporate accountability

reporting. Accounting Horizons, 27(2), pp.409-432.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of

corporate social responsibility reporting standards. Journal of Business

Ethics, 125(1), pp.147-162.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of

Corporate Accounting & Finance, 27(4), pp.27-30.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Zeitun, R. and Tian, G.G., 2014. Capital structure and corporate performance:

evidence from Jordan. Australasian Accounting Business & Finance Journal,

Forthcoming.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.