HI5020 Corporate Accounting: Qantas Airways Financial Statement

VerifiedAdded on 2023/06/11

|12

|2953

|123

Report

AI Summary

This report provides a detailed financial analysis of Qantas Airways based on its annual reports. It covers the cash flow statement, examining items such as cash receipts from customers, payments to suppliers, interest earned and paid, and investments in property, plant, and equipment. A comparative assessment of cash flows from operating, investing, and financing activities is conducted. The report also analyzes the other comprehensive income statement, focusing on foreign currency translation reserves and cash flow hedge reserves. Furthermore, it delves into Qantas Airways' corporate income tax accounting policies, including deferred tax assets and liabilities, and reconciles the differences between reported tax expenses and standard tax rates. The analysis identifies key factors influencing these differences, such as joint venture income and non-taxable income from property disposal. The report concludes by evaluating the consistency and clarity of Qantas Airways' tax treatment.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................3

Other comprehensive income statement:.........................................................................................5

Requirement (iii):.........................................................................................................................5

Requirement (iv):.........................................................................................................................5

Requirement (v):..........................................................................................................................5

Accounting for corporate income tax:.............................................................................................6

Requirement (vi):.........................................................................................................................6

Requirement (vii):........................................................................................................................6

Requirement (viii):.......................................................................................................................6

Requirement (ix):.........................................................................................................................7

Requirement (x):..........................................................................................................................8

Requirement (xi):.........................................................................................................................8

References:....................................................................................................................................10

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................3

Other comprehensive income statement:.........................................................................................5

Requirement (iii):.........................................................................................................................5

Requirement (iv):.........................................................................................................................5

Requirement (v):..........................................................................................................................5

Accounting for corporate income tax:.............................................................................................6

Requirement (vi):.........................................................................................................................6

Requirement (vii):........................................................................................................................6

Requirement (viii):.......................................................................................................................6

Requirement (ix):.........................................................................................................................7

Requirement (x):..........................................................................................................................8

Requirement (xi):.........................................................................................................................8

References:....................................................................................................................................10

2CORPORATE ACCOUNTING

Cash flow statement:

Requirement (i):

By evaluating the annual report of Qantas Airways in 2017, certain items are observed to

be inherent in various sections of the cash flow statement of the airline. From the operating

activities, the main items are cash payments to and receipts from the suppliers and customers

respectively, interest earned and paid, dividend obtained and payment of income tax. The sales

that are made on credit and the payments are collected later on could be termed as receipts from

the customers (DeFusco et al. 2015). There is fall in this item from $17,320 million in 2016 to

$16,947 million in 2017 due to the fact that it has extended additional time to the debtors. On the

contrary, fall in supplier payments is inherent in 2017 as well, since Qantas has to clear its stocks

from the last year for liquidating them into cash. Interest earned and paid could be defined as the

amounts that Qantas has made from loans provided and loans undertaken. As a portion of the

collected loans is repaid, interest paid is observed to increase over the year (Investor.qantas.com

2018). The short-term as well as long-term receipts are taken into account as interest received

and this item has increased in 2017, as additional amounts are collected from the loans provided.

The main items classified under cash flows from investments include the amount incurred

for purchasing property, plant and equipment and the amount earned for disposal of property,

plant and equipment. On the contrary, these assets fetch economic advantages to the

organisation, which are classified in the form of proceeds (Kroes and Manikas 2014). Another

item listed under this section includes aircraft operating lease refinancing. This is a type of

Cash flow statement:

Requirement (i):

By evaluating the annual report of Qantas Airways in 2017, certain items are observed to

be inherent in various sections of the cash flow statement of the airline. From the operating

activities, the main items are cash payments to and receipts from the suppliers and customers

respectively, interest earned and paid, dividend obtained and payment of income tax. The sales

that are made on credit and the payments are collected later on could be termed as receipts from

the customers (DeFusco et al. 2015). There is fall in this item from $17,320 million in 2016 to

$16,947 million in 2017 due to the fact that it has extended additional time to the debtors. On the

contrary, fall in supplier payments is inherent in 2017 as well, since Qantas has to clear its stocks

from the last year for liquidating them into cash. Interest earned and paid could be defined as the

amounts that Qantas has made from loans provided and loans undertaken. As a portion of the

collected loans is repaid, interest paid is observed to increase over the year (Investor.qantas.com

2018). The short-term as well as long-term receipts are taken into account as interest received

and this item has increased in 2017, as additional amounts are collected from the loans provided.

The main items classified under cash flows from investments include the amount incurred

for purchasing property, plant and equipment and the amount earned for disposal of property,

plant and equipment. On the contrary, these assets fetch economic advantages to the

organisation, which are classified in the form of proceeds (Kroes and Manikas 2014). Another

item listed under this section includes aircraft operating lease refinancing. This is a type of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

refinancing loan, which Qantas has used for minimising the monthly payment and rate of

interest. This amount is observed to decrease from $778 million in 2016 to $651 million in 2017.

Certain items are deemed to be inherent in the cash flows from financing activities of

Qantas Airways, as per its annual report in 2017. These items constitute of payments for buyback

of shares, capital returns and treasury shares, proceeds from and repayments of borrowings and

dividends paid to shareholders and non-controlling interests. The buyback of shares is an

initiative, in which an organisation purchases its own shares from the market, as the management

believes that the shares are undervalued (Bollerslev, Xu and Zhou 2015). A fall in this item could

be identified from the latest annual report of Qantas from $500 million in 2016 to $366 million

in 2017. The capital return denotes the principal payments back to the capital owners, which go

beyond the growth of a business organisation. No such payments have been made by Qantas in

the year 2017, while the capital return payments amounted to $505 million in 2016. Treasury

stock is a type of stock kept aside for obtaining funds or paying for future investments (Robinson

and Sensoy 2016). In case of Qantas, increase in this item could be observed from $75 million in

2016 to $198 million in 2017, as they would be issued for raising additional funds in future.

The proceeds from borrowings have been $419 million in 2017, while no such payments

were observed in 2016. On the other hand, the payment of borrowings has fallen from $807

million in 2016 to $453 million in 2017. This is because the airline has limited its loan payments

and adequate amount has been received from the provided loans. Finally, it has been observed

from the annual report of Qantas Airways that the organisation has made payments to the

shareholders and other non-controlling interests in 2017, while no such payments are observed in

2016.

refinancing loan, which Qantas has used for minimising the monthly payment and rate of

interest. This amount is observed to decrease from $778 million in 2016 to $651 million in 2017.

Certain items are deemed to be inherent in the cash flows from financing activities of

Qantas Airways, as per its annual report in 2017. These items constitute of payments for buyback

of shares, capital returns and treasury shares, proceeds from and repayments of borrowings and

dividends paid to shareholders and non-controlling interests. The buyback of shares is an

initiative, in which an organisation purchases its own shares from the market, as the management

believes that the shares are undervalued (Bollerslev, Xu and Zhou 2015). A fall in this item could

be identified from the latest annual report of Qantas from $500 million in 2016 to $366 million

in 2017. The capital return denotes the principal payments back to the capital owners, which go

beyond the growth of a business organisation. No such payments have been made by Qantas in

the year 2017, while the capital return payments amounted to $505 million in 2016. Treasury

stock is a type of stock kept aside for obtaining funds or paying for future investments (Robinson

and Sensoy 2016). In case of Qantas, increase in this item could be observed from $75 million in

2016 to $198 million in 2017, as they would be issued for raising additional funds in future.

The proceeds from borrowings have been $419 million in 2017, while no such payments

were observed in 2016. On the other hand, the payment of borrowings has fallen from $807

million in 2016 to $453 million in 2017. This is because the airline has limited its loan payments

and adequate amount has been received from the provided loans. Finally, it has been observed

from the annual report of Qantas Airways that the organisation has made payments to the

shareholders and other non-controlling interests in 2017, while no such payments are observed in

2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

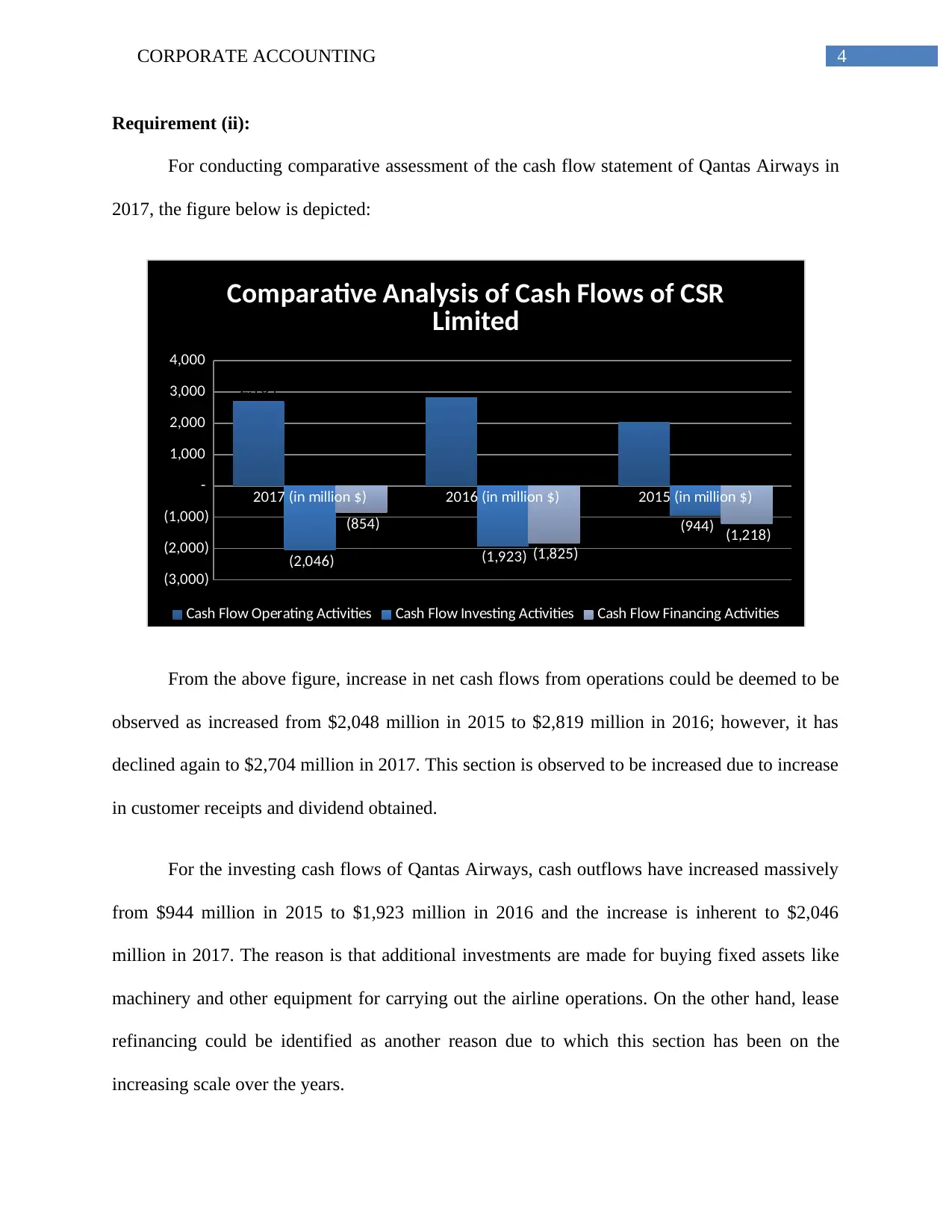

Requirement (ii):

For conducting comparative assessment of the cash flow statement of Qantas Airways in

2017, the figure below is depicted:

2017 (in million $) 2016 (in million $) 2015 (in million $)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,000

4,000

2,704

(2,046) (1,923)

(944)(854)

(1,825)

(1,218)

Comparative Analysis of Cash Flows of CSR

Limited

Cash Flow Operating Activities Cash Flow Investing Activities Cash Flow Financing Activities

From the above figure, increase in net cash flows from operations could be deemed to be

observed as increased from $2,048 million in 2015 to $2,819 million in 2016; however, it has

declined again to $2,704 million in 2017. This section is observed to be increased due to increase

in customer receipts and dividend obtained.

For the investing cash flows of Qantas Airways, cash outflows have increased massively

from $944 million in 2015 to $1,923 million in 2016 and the increase is inherent to $2,046

million in 2017. The reason is that additional investments are made for buying fixed assets like

machinery and other equipment for carrying out the airline operations. On the other hand, lease

refinancing could be identified as another reason due to which this section has been on the

increasing scale over the years.

Requirement (ii):

For conducting comparative assessment of the cash flow statement of Qantas Airways in

2017, the figure below is depicted:

2017 (in million $) 2016 (in million $) 2015 (in million $)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,000

4,000

2,704

(2,046) (1,923)

(944)(854)

(1,825)

(1,218)

Comparative Analysis of Cash Flows of CSR

Limited

Cash Flow Operating Activities Cash Flow Investing Activities Cash Flow Financing Activities

From the above figure, increase in net cash flows from operations could be deemed to be

observed as increased from $2,048 million in 2015 to $2,819 million in 2016; however, it has

declined again to $2,704 million in 2017. This section is observed to be increased due to increase

in customer receipts and dividend obtained.

For the investing cash flows of Qantas Airways, cash outflows have increased massively

from $944 million in 2015 to $1,923 million in 2016 and the increase is inherent to $2,046

million in 2017. The reason is that additional investments are made for buying fixed assets like

machinery and other equipment for carrying out the airline operations. On the other hand, lease

refinancing could be identified as another reason due to which this section has been on the

increasing scale over the years.

5CORPORATE ACCOUNTING

In relation to financing cash flows of Qantas Airways, increasing trend could be observed

as well like that of investing cash flows from 2015 to 2016; however, declining trend could be

observed in 2017. This is due to the fact that it has minimised its borrowing repayment in 2017

and no dividends have been incurred for non-controlling interests. All these causes are primarily

responsible for decrease in financing cash outflows in the year 2017.

Other comprehensive income statement:

Requirement (iii):

The main items that are included in this statement include foreign currency translation

reserve, cash flow hedge reserve and income tax benefits.

Requirement (iv):

With the help of foreign currency translation reserve, it becomes possible for Qantas

Airways to exchange the currency used by the foreign subsidiary to the currency that is used by

the parent subsidiary for the purpose of financial reporting (Brigham et al. 2016). The intention

is to report profits or losses in the currency of the parent entity. Cash flow hedge reserve is used

for reducing the exposure due to the considerable differences in the positions of assets and

liabilities of Qantas Airways. Income tax benefits are obtained based on the consideration of the

various items disclosed in the other comprehensive income statement (Lee 2014).

Requirement (v):

There are various reasons that Qantas Airways prepare the other comprehensive income

statement. One of them is that the users are provided with crucial information for various income

aspects. Moreover, a holistic and fair overview of different items could be obtained from the

In relation to financing cash flows of Qantas Airways, increasing trend could be observed

as well like that of investing cash flows from 2015 to 2016; however, declining trend could be

observed in 2017. This is due to the fact that it has minimised its borrowing repayment in 2017

and no dividends have been incurred for non-controlling interests. All these causes are primarily

responsible for decrease in financing cash outflows in the year 2017.

Other comprehensive income statement:

Requirement (iii):

The main items that are included in this statement include foreign currency translation

reserve, cash flow hedge reserve and income tax benefits.

Requirement (iv):

With the help of foreign currency translation reserve, it becomes possible for Qantas

Airways to exchange the currency used by the foreign subsidiary to the currency that is used by

the parent subsidiary for the purpose of financial reporting (Brigham et al. 2016). The intention

is to report profits or losses in the currency of the parent entity. Cash flow hedge reserve is used

for reducing the exposure due to the considerable differences in the positions of assets and

liabilities of Qantas Airways. Income tax benefits are obtained based on the consideration of the

various items disclosed in the other comprehensive income statement (Lee 2014).

Requirement (v):

There are various reasons that Qantas Airways prepare the other comprehensive income

statement. One of them is that the users are provided with crucial information for various income

aspects. Moreover, a holistic and fair overview of different items could be obtained from the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

other comprehensive income statement. Due to these causes, certain items are not disclosed in

the income statement of Qantas Airways (Ramsey 2018).

Accounting for corporate income tax:

Requirement (vi):

As identified after critical evaluation of the annual report of Qantas Airways in 2017, the

airline has been obliged highly in carrying out its tax accounting policies, as laid down in the

Australian taxation law. The prevailing corporate rate of tax in Australia has been 30% over the

years. It has been identified from the income statement of the airline that the taxation expense

has been $1,424 million in 2017 and $789 million in 2016.

Requirement (vii):

The tax accounting policy that Qantas Airways follows discloses the difference between

the reported tax expense and the tax expense that would have been incurred by following the

standard tax rate for the airline. Certain causes are deemed to be inherent that they do not

resemble each other. The part of net income received from the joint venture agreements is the

major influential dynamic, as the excess payment of tax is attuned to the real tax expenses (Guay,

Samuels and Taylor 2016). The non-taxable income associated with the disposal of property is a

primary cause because of this difference due to which additional tax payment has been made in

both the years. The underpayment and overpayment of corporate tax in 2016 and 2017 is another

cause behind the difference, as Qantas Airways is required to spend the deficit corporate tax

payment; however, it would be possible to earn benefits from excess payment of corporate tax

(Robinson et al. 2015).

other comprehensive income statement. Due to these causes, certain items are not disclosed in

the income statement of Qantas Airways (Ramsey 2018).

Accounting for corporate income tax:

Requirement (vi):

As identified after critical evaluation of the annual report of Qantas Airways in 2017, the

airline has been obliged highly in carrying out its tax accounting policies, as laid down in the

Australian taxation law. The prevailing corporate rate of tax in Australia has been 30% over the

years. It has been identified from the income statement of the airline that the taxation expense

has been $1,424 million in 2017 and $789 million in 2016.

Requirement (vii):

The tax accounting policy that Qantas Airways follows discloses the difference between

the reported tax expense and the tax expense that would have been incurred by following the

standard tax rate for the airline. Certain causes are deemed to be inherent that they do not

resemble each other. The part of net income received from the joint venture agreements is the

major influential dynamic, as the excess payment of tax is attuned to the real tax expenses (Guay,

Samuels and Taylor 2016). The non-taxable income associated with the disposal of property is a

primary cause because of this difference due to which additional tax payment has been made in

both the years. The underpayment and overpayment of corporate tax in 2016 and 2017 is another

cause behind the difference, as Qantas Airways is required to spend the deficit corporate tax

payment; however, it would be possible to earn benefits from excess payment of corporate tax

(Robinson et al. 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

Requirement (viii):

In compliance with the annual report of Qantas Airways in 2017, sufficient disclosures

are carried out in relation to deferred tax assets and deferred tax liabilities. For the airline,

deferred tax assets are deemed to decline considerably from $333 million in 2016 to $39 million

in 2017. However, it has not reported any deferred tax liability in both the years 2016 and 2017.

There are many reasons to include deferred tax assets, as their disclosures are considered

relevant for the users of the financial statements of a business organisation (Woellner et al.

2016). For Qantas, the reporting of these assets is made, as it has incurred taxes in advances

more than the amount to be incurred actually and these prepaid tax payments are taken into

account as assets. Moreover, Qantas has minimised its depreciation expense due to the

differences in the policies that are needed for developing the profit and loss statement of the

airline. Therefore, the depreciation amount falling short is considered as liability (Freebairn

2015).

Requirement (ix):

After evaluating the latest annual report of Qantas Airways, the airline has mentioned

about income tax payable or current tax assets in the same. It has mentioned about the current tax

liabilities in its annual report as well. However, no realisation in terms of monetary value has

been made by Qantas Airways for current tax assets and current tax liabilities in both the years

2016 and 2017. Hence, there is no similarity that could be identified between the tax paid and tax

payable, as per the latest annual report of the airline. This is because it has not considered a

number of items in current tax assets, which are taken into account in order to arrive at the

overall income tax expense. They are current tax assets, current tax liabilities and deferred tax

expense (Bennedsen and Zeume 2017). Thus, deferred tax expense occupies a certain part of the

Requirement (viii):

In compliance with the annual report of Qantas Airways in 2017, sufficient disclosures

are carried out in relation to deferred tax assets and deferred tax liabilities. For the airline,

deferred tax assets are deemed to decline considerably from $333 million in 2016 to $39 million

in 2017. However, it has not reported any deferred tax liability in both the years 2016 and 2017.

There are many reasons to include deferred tax assets, as their disclosures are considered

relevant for the users of the financial statements of a business organisation (Woellner et al.

2016). For Qantas, the reporting of these assets is made, as it has incurred taxes in advances

more than the amount to be incurred actually and these prepaid tax payments are taken into

account as assets. Moreover, Qantas has minimised its depreciation expense due to the

differences in the policies that are needed for developing the profit and loss statement of the

airline. Therefore, the depreciation amount falling short is considered as liability (Freebairn

2015).

Requirement (ix):

After evaluating the latest annual report of Qantas Airways, the airline has mentioned

about income tax payable or current tax assets in the same. It has mentioned about the current tax

liabilities in its annual report as well. However, no realisation in terms of monetary value has

been made by Qantas Airways for current tax assets and current tax liabilities in both the years

2016 and 2017. Hence, there is no similarity that could be identified between the tax paid and tax

payable, as per the latest annual report of the airline. This is because it has not considered a

number of items in current tax assets, which are taken into account in order to arrive at the

overall income tax expense. They are current tax assets, current tax liabilities and deferred tax

expense (Bennedsen and Zeume 2017). Thus, deferred tax expense occupies a certain part of the

8CORPORATE ACCOUNTING

income tax expense of the airline or the case might be that it has not spent the overall expenses in

adherence to the income tax regulation. Thus, considerable reasons could be held responsible

that income tax expense and income tax payable do not match with each other (Taylor,

Richardson and Taplin 2015).

Requirement (x):

It has already been evaluated that the Qantas Airways has reported income tax expense of

$1,424 million in 2017 and $789 million in 2016. On the other hand, the reported income tax

expense in the cash flow statement has been nil in both the years. This implies clearly the

variation between the two disclosed amounts. In such instance, it is to be mentioned that the

amount of corporate tax disclosed in the profit and loss statement is the sum of money spent in

the present accounting year of the airline and the payment needs to be cleared in the future year

(Graetz and Warren 2016). On the other hand, the income tax payment in the cash flow statement

comprises of the statement of the past year and tax payments made in advance. By taking into

account all these reasons, there is significant difference observed in income tax expense in the

cash flow statement and profit and loss statement of Qantas Airways (Wilde and Wilson 2017).

Requirement (xi):

In accordance with the evaluation of the revealed financial information, there is absence

of surprising or confusing components could be inherent in the tax treatment of Qantas Airways.

The reason is that the airline has delivered all essential clarifications and descriptions regarding

tax expense in the form of financial notes disclosed in the annual report. Moreover, the financial

statement users would not face issues in obtaining an overview of the taxation policies of Qantas

Airways, as it has conformed to the prevailing rules and standards laid out in the Australian

taxation law. The organisation has to spend lower amount of depreciation, since the rules are

income tax expense of the airline or the case might be that it has not spent the overall expenses in

adherence to the income tax regulation. Thus, considerable reasons could be held responsible

that income tax expense and income tax payable do not match with each other (Taylor,

Richardson and Taplin 2015).

Requirement (x):

It has already been evaluated that the Qantas Airways has reported income tax expense of

$1,424 million in 2017 and $789 million in 2016. On the other hand, the reported income tax

expense in the cash flow statement has been nil in both the years. This implies clearly the

variation between the two disclosed amounts. In such instance, it is to be mentioned that the

amount of corporate tax disclosed in the profit and loss statement is the sum of money spent in

the present accounting year of the airline and the payment needs to be cleared in the future year

(Graetz and Warren 2016). On the other hand, the income tax payment in the cash flow statement

comprises of the statement of the past year and tax payments made in advance. By taking into

account all these reasons, there is significant difference observed in income tax expense in the

cash flow statement and profit and loss statement of Qantas Airways (Wilde and Wilson 2017).

Requirement (xi):

In accordance with the evaluation of the revealed financial information, there is absence

of surprising or confusing components could be inherent in the tax treatment of Qantas Airways.

The reason is that the airline has delivered all essential clarifications and descriptions regarding

tax expense in the form of financial notes disclosed in the annual report. Moreover, the financial

statement users would not face issues in obtaining an overview of the taxation policies of Qantas

Airways, as it has conformed to the prevailing rules and standards laid out in the Australian

taxation law. The organisation has to spend lower amount of depreciation, since the rules are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

varied while developing the income statement. Hence, the amount of depreciation, which is

short, is considered as the form of liability. Lastly, it becomes possible for the users in forming a

critical overview of deferred tax assets and deferred tax liabilities and income tax treatment after

critical interpretation of the tax operations of the airline.

varied while developing the income statement. Hence, the amount of depreciation, which is

short, is considered as the form of liability. Lastly, it becomes possible for the users in forming a

critical overview of deferred tax assets and deferred tax liabilities and income tax treatment after

critical interpretation of the tax operations of the airline.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

References:

Investor.qantas.com., 2018. Qantas | 2017 Annual Report. [online] Available at:

http://investor.qantas.com/annual-report-2017/ [Accessed 31 May 2018].

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E., 2015. Quantitative

investment analysis. John Wiley & Sons.

Kroes, J.R. and Manikas, A.S., 2014. Cash flow management and manufacturing firm financial

performance: A longitudinal perspective. International Journal of Production Economics, 148,

pp.37-50.

Bollerslev, T., Xu, L. and Zhou, H., 2015. Stock return and cash flow predictability: The role of

volatility risk. Journal of Econometrics, 187(2), pp.458-471.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-543.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Lee, T.A. ed., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an Accounting

Practice. Routledge.

Ramsey, E.D., 2018. A Comprehensive Review of Accounting through Case Studies (Doctoral

dissertation, The University of Mississippi).

Guay, W., Samuels, D. and Taylor, D., 2016. Guiding through the fog: Financial statement

complexity and voluntary disclosure. Journal of Accounting and Economics, 62(2-3), pp.234-

269.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

References:

Investor.qantas.com., 2018. Qantas | 2017 Annual Report. [online] Available at:

http://investor.qantas.com/annual-report-2017/ [Accessed 31 May 2018].

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E., 2015. Quantitative

investment analysis. John Wiley & Sons.

Kroes, J.R. and Manikas, A.S., 2014. Cash flow management and manufacturing firm financial

performance: A longitudinal perspective. International Journal of Production Economics, 148,

pp.37-50.

Bollerslev, T., Xu, L. and Zhou, H., 2015. Stock return and cash flow predictability: The role of

volatility risk. Journal of Econometrics, 187(2), pp.458-471.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-543.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Lee, T.A. ed., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an Accounting

Practice. Routledge.

Ramsey, E.D., 2018. A Comprehensive Review of Accounting through Case Studies (Doctoral

dissertation, The University of Mississippi).

Guay, W., Samuels, D. and Taylor, D., 2016. Guiding through the fog: Financial statement

complexity and voluntary disclosure. Journal of Accounting and Economics, 62(2-3), pp.234-

269.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

11CORPORATE ACCOUNTING

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation Law

2016. OUP Catalogue.

Freebairn, J., 2015. Who Pays the Australian Corporate Income Tax?. Australian Economic

Review, 48(4), pp.357-368.

Bennedsen, M. and Zeume, S., 2017. Corporate tax havens and transparency. The Review of

Financial Studies, 31(4), pp.1221-1264.

Taylor, G., Richardson, G. and Taplin, R., 2015. Determinants of tax haven utilization: evidence

from Australian firms. Accounting & Finance, 55(2), pp.545-574.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder taxes.

Wilde, J.H. and Wilson, R.J., 2017. Perspectives on Corporate Tax Avoidance: Observations

from the Past Decade.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation Law

2016. OUP Catalogue.

Freebairn, J., 2015. Who Pays the Australian Corporate Income Tax?. Australian Economic

Review, 48(4), pp.357-368.

Bennedsen, M. and Zeume, S., 2017. Corporate tax havens and transparency. The Review of

Financial Studies, 31(4), pp.1221-1264.

Taylor, G., Richardson, G. and Taplin, R., 2015. Determinants of tax haven utilization: evidence

from Australian firms. Accounting & Finance, 55(2), pp.545-574.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder taxes.

Wilde, J.H. and Wilson, R.J., 2017. Perspectives on Corporate Tax Avoidance: Observations

from the Past Decade.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.