Corporate Accounting: A Comparative Financial Analysis of Two Firms

VerifiedAdded on 2023/06/05

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

CORPORATE ACCOUNTING

Executive summary:

An organization has number of stakeholders who have different interests associated with

the functions of such organization. In order to inform these stakeholders about the financial

performance, position and future plans an organization prepare and issue annual reports to its

stakeholders. In order to evaluate the annual reports of two organizations in real world this would

be a helpful document to the readers. Aura Energy Limited Austex Oil Limited are two entities

whose annual reports shall be evaluated in this document with the objective of assessing the

financial states of both these entities and how the entities have performed in recent years.

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Owners’ equity:...............................................................................................................................3

Comparative analysis of debt and equity position:......................................................................4

Cash flow statement:....................................................................................................................5

Other comprehensive income statement:.........................................................................................9

Accounting for Corporate Income Tax:.........................................................................................11

Conclusion:....................................................................................................................................14

References:....................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Introduction:

Before getting into discussion about the various aspects of the financial statements of

both Aura Energy Limited and Austex Oil Limited it is essential to get a brief introduction about

both these entities. This will provide the readers a frame of reference while assessing the

information about the two entities provide in the annual reports these entities.

Aura Energy Limited is a minerals company based in Australia that lusted its shares in

Australian Securities Exchange (ASX) for the first time in 2006. Since then the company has

made rapid strides to make its own place in minerals industry in Australia, Europe and Africa.

With acquisition of number of projects in Sweden and Mauritania where number of occurrences

of poly-metallic and uranium have taken place, the company has made significant mark in the

minerals industry.

A public company listed as AOK in ASX Austex Oil Limited has specific focus on USA market.

The company has number of projects in USA to explore and develop oil and gas leases in the

country. The company already has number of oil and gas leases in Oklahoma and Kansas. Also

the company has more than 10,500 net acre of oil and gas leases in the Mississippi Lime Play.

Owners’ equity:

Aura Energy Limited:

Issued capital: It represent the amount of share capital issued by the company. For the year

ending in June, 2016 the balance in issued share capital is $32,784,203 with corresponding

balance in the account in the previous year was $31,311,988. The increase is due to the issue of

additional shares during the year net of transaction costs (Tschopp and Huefner, 2015).

Paraphrase This Document

CORPORATE ACCOUNTING

Accumulated losses: It represent the amount of loss incurred and accumulated over the years by

the company. At the beginning of the financial year 2015-16 the balance in accumulated losses

was $18,451,415. Due to option exercised during the year for $104,151 the accumulated losses at

the end of 2015-16 is $19,973,039 (Dahmen and Rodríguez, 2014).

Reserves: This includes options reserve and foreign exchange translation reserve. In 2015 the

balance in reserves was $901,252 which increased to $1,029,542 by the end of June 30, 2016.

The increase was mainly due to the options issued during the year (Macve, 2015).

Austex Oil Limited:

Issued capital: The Company had an issued capital of $90,014,494 in 2015 that rose to

$90,197,424 in 2016 due to share based payment issue of $182,930.

Reserves: Balance in the reserves account as on January 01, 2016 was 2,056,023 was increased

by $146,922 and $669,409 for share based payments and options exercise respectively. A

reduction of $182,930 and $26,766 for share based payment issue and other comprehensive net

of tax respectively increased the balance in the reserves to $2,662,658 as the end of December

31, 2016 (Penman, 2016).

Accumulated losses: Loss during the year 2016 of $8,904,075 increased the accumulated loss

balance of $50,424,706 on January 01, 2016 to $59,328,781 at the end of December, 2016.

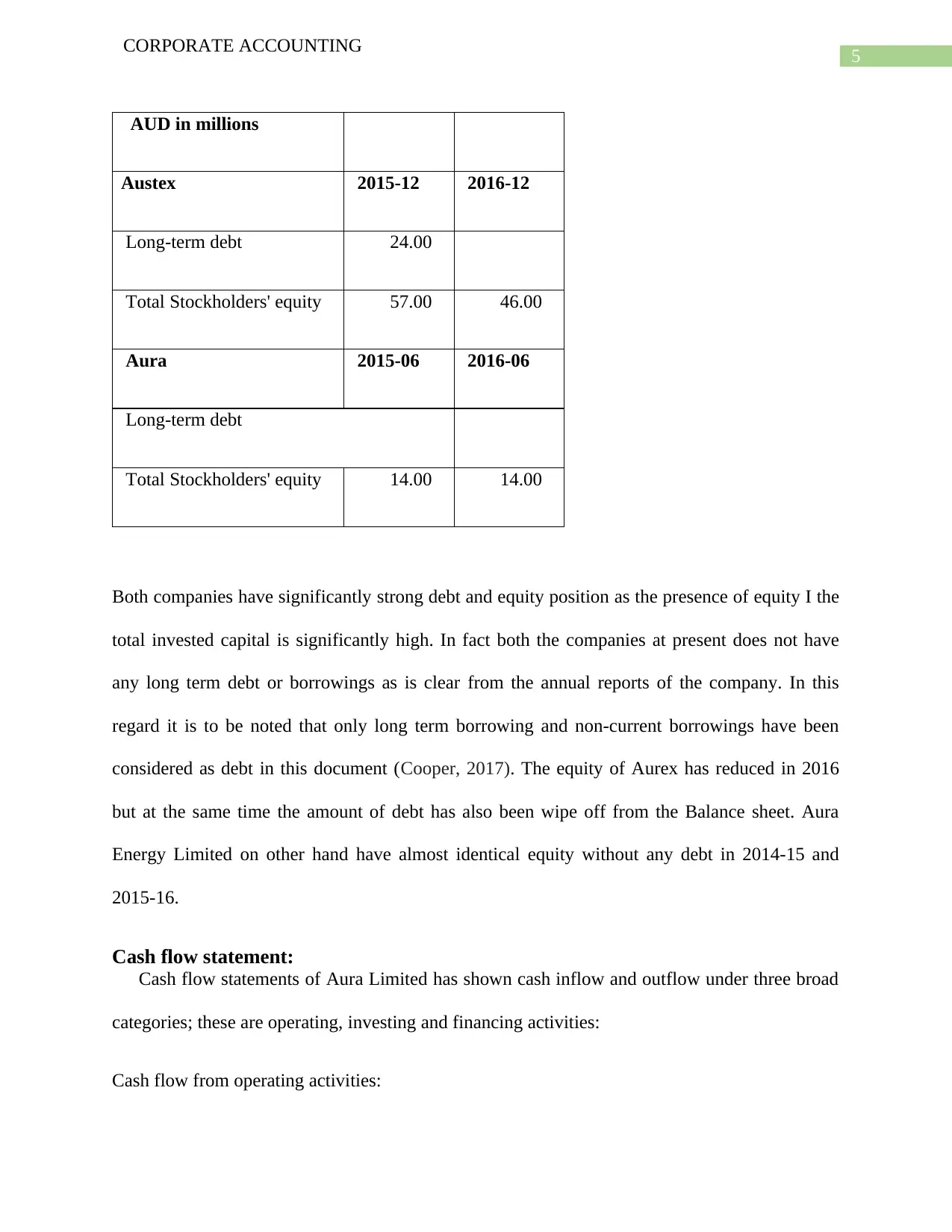

Comparative analysis of debt and equity position:

In order to conduct comparative analysis between two companies of debt and equity

position it is necessary to have the table containing information about debt and equity of the

company (Nobes, 2014).

CORPORATE ACCOUNTING

AUD in millions

Austex 2015-12 2016-12

Long-term debt 24.00

Total Stockholders' equity 57.00 46.00

Aura 2015-06 2016-06

Long-term debt

Total Stockholders' equity 14.00 14.00

Both companies have significantly strong debt and equity position as the presence of equity I the

total invested capital is significantly high. In fact both the companies at present does not have

any long term debt or borrowings as is clear from the annual reports of the company. In this

regard it is to be noted that only long term borrowing and non-current borrowings have been

considered as debt in this document (Cooper, 2017). The equity of Aurex has reduced in 2016

but at the same time the amount of debt has also been wipe off from the Balance sheet. Aura

Energy Limited on other hand have almost identical equity without any debt in 2014-15 and

2015-16.

Cash flow statement:

Cash flow statements of Aura Limited has shown cash inflow and outflow under three broad

categories; these are operating, investing and financing activities:

Cash flow from operating activities:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Cash receipts from customers: Aura has disclosed that it has received no amount from customers

in neither of the two years mentioned here, in 2015 and 2016. Austex Oil Limited on the other

hand has reported that it has received $9,811,746 from customers in 2016. The company in fact

had received $15,407,514 a year ago from customers. The reduction in the receipts of cash from

customers is due to the inability of the company to maintain its revenue (Tinkelman and Fan,

2018).

Interest received: Aura Energy Limited showed cash receipts of $4,907 in 2016 and $19,159 in

2015 as interests. No such income has been reported by Austex Limited under operating

activities.

Payment to suppliers and employees for Aura Energy Limited in 2015 was $1,074,840 has

reduced to $892,505 due to reduction in exploration and development of oil filed. The cash

payment of Austex Oil has also reduced under this head from $9,946,209 in 2015 to $7,106,545

in 2016 due to the same reason (Hughes and Poi, 2016).

Aura Limited in addition has also reported payment of exploration costs of $1,190,561 in 2016.

A significantly less amount compared to $1,438,205 in previous year again suggesting a huge

drop in operational scale of the company.

Finance costs of $998,149 in 2016 and $1,007.253 in 2015 have been disclosed in the cash flow

statement of Austex. The decrease in finance cost is due to the reduction in loan amount (Vogel,

2014).

Net cash used in investing activities:

Paraphrase This Document

CORPORATE ACCOUNTING

Acquisition of plant and equipment is the only item shown under investing activities of Aura

Energy. In 2015 the company paid cash of $3,285 to purchase plant and equipment. No cash

flows occurred under investing activities of the company in 2016.

Austex on the other hand has made cash payment of $3,250,000 for purchase of business,

$206,522 for purchase of property, plant and equipment and $752,679 as development

expenditures in the year 2016. In 2015 the company merely invested $2,762,781. The reason for

such sharp increase in investment activities is the payment for acquiring a business in 2016

(Tayeh, Al-Jarrah and Tarhini, 2015).

Financing activities:

In 2016 Aura has issued shares and received $1,365,639 as proceeds and cash payment of

$59,324 for capital raising costs. In a year back in 2015 the company received $2,879,083 from

financing activities due to significant amount of cash received from issue of shares.

Austex Oil Limited has used $2,966,060 cash for repayment of loan and $5,400,000 for restricted

loan term. In 2015 the company received proceeds of $8,000,000 as borrowings thus, in 2015 the

net cash flow from financing activities was very much in positive (Dumont and Schmit, 2014).

Comparative analysis of three broad categories of cash flows:

Annual reports of the two companies have made it possible to accumulate the information about

the cash flows under three broad categories. The accumulated data of Aura and Austex have

summarized in the table below to facilitate the comparison between the two companies.

Aura Energy Limited

Years 2014 2015 2016

CORPORATE ACCOUNTING

Cash flows from operating activities (1,927,032.0

0)

(2,493,886.0

0)

(1,929,551.0

0)

Cash flow from investing activities (3,285.

00)

Cash flow from financing activities 469,943.

00

2,879,083.

00

1,306,315.

00

Austex Oil Limited

Years 2014 2015 2016

Cash flows from operating activities 10,578,169.

00

4,476,674.

00

1,704,196.

00

Cash flow from investing activities (34,605,279.0

0)

(2,762,781.0

0)

(4,209,231.0

0)

Cash flow from financing activities 21,947,946.

00

7,846,010.

00

8,366,060.

00

(Loughran and McDonald, 2016)

Aura Energy Limited has struggled to earn positive cash flows from any of the three categories.

From 2014 to 2016 the company has failed to earn positive cash flows from business operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

In all these years the company have used cash in operating activities. In 2016 the company has

used $1,929,551 in operating activities and has collected $1,306,315 from financing activities.

Austex comparatively has performed better as in all the three years the company has earned

positive cash flows from operating activities. In 2016 the company however generated lowest

amount of cash flows out of three years mentioned in the table with $1,704,196. The cash

generated from financing activities in the same year has been $8,366,060 (Campbell, Downes

and Schwartz, 2015).

It is clear from the above that Austex has better position as far as its cash position is concerned

compared to Aura Energy Limited. However, there are still lots of room for improvement for

Austex in the future to improve its cash management (Lee, 2014).

Other comprehensive income statement:

As per accounting standards applicable in Australia (AASBs), entities must provide a

comprehensive income statement along with ordinary income statement to disclose items of

income and expenditures that though affect the profitability of the organization but is not to be

reported in the ordinary income statement while calculating the net income of the organization.

Thus, in other comprehensive income statements items below the line of net income are reported.

Such items include gain / (losses) from change in actuarial valuation, gain or loss on translation

of foreign transactions (Foerster, Tsagarelis and Wang, 2016).

Other comprehensive income statement of Austex Oil Limited only includes $26,766 as loss due

to exchange differences in foreign currency transactions. In 2015 it was around $20,611.

Similarly, Aura Energy Limited has also reported impact of foreign currency movement in other

comprehensive income statement. Gains of $31,563 and $13,327 in 2016 and 2015 respectively

Paraphrase This Document

CORPORATE ACCOUNTING

have been stated in other comprehensive income statement of the company (Collins, Hribar and

Tian, 2014).

The reason such items have not been reported in profit and loss account of these companies

because this are not gains or losses from ordinary course of business.

Comparative analysis:

Aura Energy Limited

Years 2016 2015

Net other comprehensive income / (loss) 31563 13327

Austex Oil Limited

Years 2

,016

2

,015

Net other comprehensive income / (loss) (26,76

6.00)

(20,611

.00)

(Hanna, Li, and Shaw, 2018)

The above table clearly explains the difference between the net comprehensive income or losses

attributable two different companies. It is clear that Aura Energy Limited has been able to

manage the foreign currency movement better in both the year 2015 and 2016. However, Austex

has failed to manage its foreign currency transactions. Thus in both the year the company has

incurred losses from foreign currency movements.

CORPORATE ACCOUNTING

Thus, if these items would have been included in the income statement then the amount of profit

in case of Aura would have been increased and profit of Austex would have been deceased.

However, since bot the companies have incurred losses thus, in cash of Aura losses would have

been reduced and losses would have been higher for Austex (Yasseen, Jansen and Small, 2016).

Yes, the comprehensive income should be considered at the time of evaluating the performance

of managers since managing the foreign currencies is an integral part of the overall management

of an organization (Black, 2016).

Accounting for Corporate Income Tax:

For the year 2016

Item

no.

Amount in $ Aura Energy

Limited

Austex Oil

Limited

(x) Income tax expense / (benefit) (148,608.00) (207,363.0

0)

(xi) Effective tax rate for the companies

Income tax expense / (benefit) (148,608.00) (207,363.0

0)

Loss before income tax benefits (1,774,383.00) (9,158,546.0

0)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Effective tax rate for the companies 8.

38 2.26

Aura Energy Limited has higher effective tax rate

(xii) Deferred tax assets - -

Deferred tax liabilities - -

(Morris, 2017)

Though none of the companies have either deferred tax assets or deferred tax liabilities however,

an entity generally recognize deferred tax assets and deferred tax liabilities in case there is any

items of revenue and expenditures that have time differences and have been adjusted for

determination of taxable profit and losses that are expected to be reversed in the future (Bratten,

Causholli and Khan, 2016).

There has be no changed in deferred tax assets or deferred tax liabilities since the neither of the

two companies have any deferred tax assets and deferred tax liabilities as per the financial

statements of the companies (Bauman and Shaw, 2016).

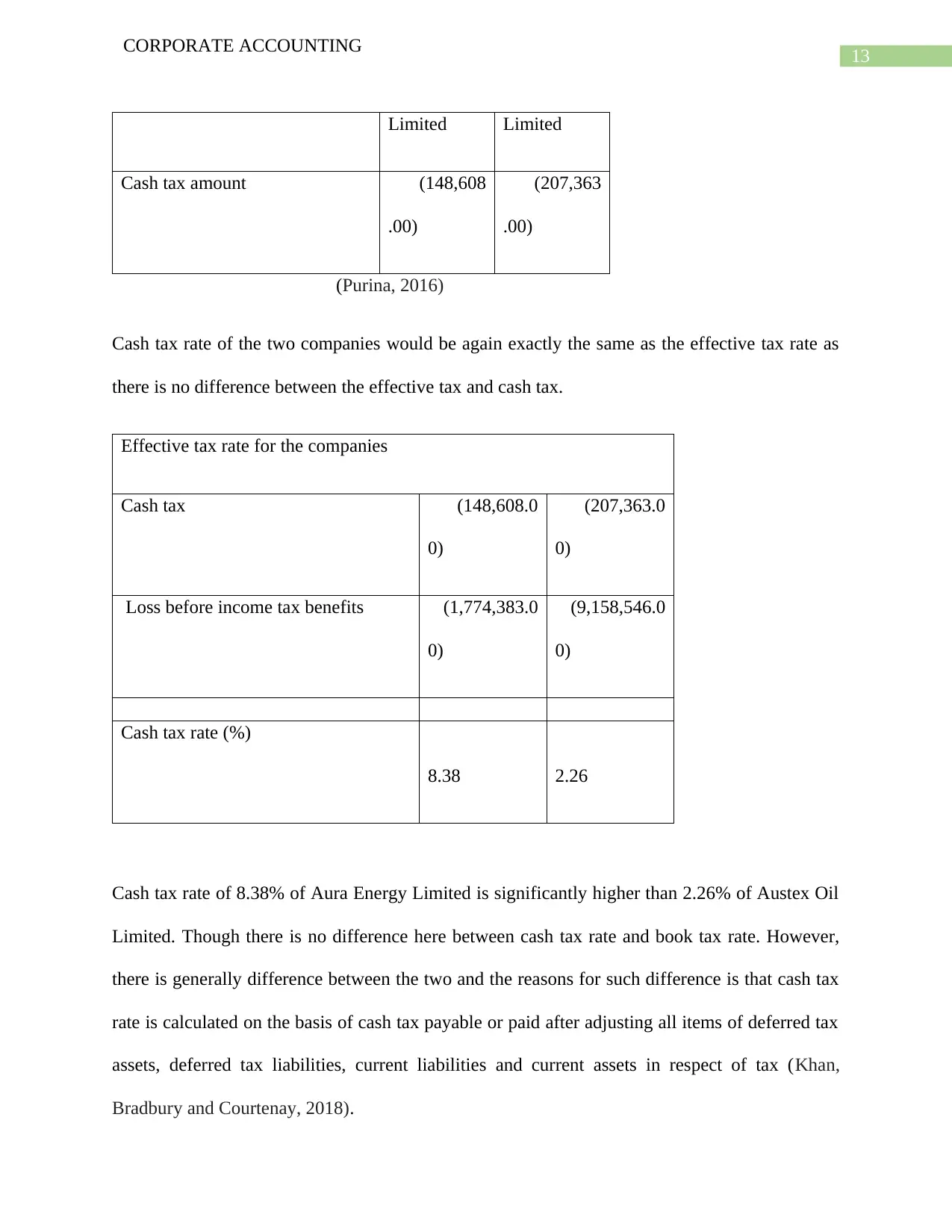

The cash tax amount for Aura Energy and Austex Oil Limited would be same as that of tax

benefits since none of the companies have any deferred tax assets, deferred tax liabilities of

current income tax liabilities or assets. Hence, cash tax amount of Aura Energy Limited and

Austex Oil Limited would be as following:

Amount in $ Aura Energy Austex Oil

Paraphrase This Document

CORPORATE ACCOUNTING

Limited Limited

Cash tax amount (148,608

.00)

(207,363

.00)

(Purina, 2016)

Cash tax rate of the two companies would be again exactly the same as the effective tax rate as

there is no difference between the effective tax and cash tax.

Effective tax rate for the companies

Cash tax (148,608.0

0)

(207,363.0

0)

Loss before income tax benefits (1,774,383.0

0)

(9,158,546.0

0)

Cash tax rate (%)

8.38 2.26

Cash tax rate of 8.38% of Aura Energy Limited is significantly higher than 2.26% of Austex Oil

Limited. Though there is no difference here between cash tax rate and book tax rate. However,

there is generally difference between the two and the reasons for such difference is that cash tax

rate is calculated on the basis of cash tax payable or paid after adjusting all items of deferred tax

assets, deferred tax liabilities, current liabilities and current assets in respect of tax (Khan,

Bradbury and Courtenay, 2018).

CORPORATE ACCOUNTING

Conclusion:

The discussion about the financial performance and position of Aura Energy Limited and

Austex Oil Limited shows that none of the two companies have performed according to the

expectation of the management. Both the companies have even strolled to earn profit from

business in last few years. The management of the two companies must immediately formulate

an effective strategy to ensure that the performances of these companies can be improved in the

future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

References:

Bauman, M.P. and Shaw, K.W., 2016. Balance sheet classification and the valuation of deferred

taxes. Research in Accounting Regulation, 28(2), pp.77-85. [Online] Available from:

http://scholarspress.us/journals/IMR/pdf/IMR-2-2016/IMR-v12n2art4.pdf [Accessed 21

September 2018]

Black, D.E., 2016. Other comprehensive income: a review and directions for future

research. Accounting & Finance, 56(1), pp.9-45. [Online] Available from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/acfi.12186 [Accessed 21 September 2018]

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315. [Online] Available from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/auar.12181 [Accessed 21 September 2018]

Campbell, J.L., Downes, J.F. and Schwartz, W.C., 2015. Do sophisticated investors use the

information provided by the fair value of cash flow hedges?. Review of Accounting

Studies, 20(2), pp.934-975. [Online] Available from:

https://link.springer.com/article/10.1007/s11142-015-9318-y [Accessed 21 September 2018]

Collins, D.W., Hribar, P. and Tian, X.S., 2014. Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics, 58(2-3), pp.173-

200.

Cooper, S., 2017. Corporate social performance: A stakeholder approach. Routledge.

Paraphrase This Document

CORPORATE ACCOUNTING

Dahmen, P. and Rodríguez, E., 2014. Financial literacy and the success of small businesses: An

observation from a small business development center. Numeracy, 7(1), p.3. [Online] Available

from: https://scholarcommons.usf.edu/numeracy/vol7/iss1/art3/ [Accessed 21 September 2018]

Dumont, G. and Schmit, M., 2014. Tier-1 MFIs' Financial Performance: Cash-Flow Statement

Analysis Version 2.0 (No. 13/054). CEB Working Paper.

Foerster, S., Tsagarelis, J. and Wang, G., 2016. Are Cash Flows Better Stock Return Predictors

Than Profits?. Financial Analysts Journal, 73(1), pp.73-99. [Online] Available from:

https://www.cfapubs.org/doi/abs/10.2469/faj.v73.n1.2 [Accessed 21 September 2018]

Hanna, J.D., Li, Z. and Shaw, W., 2018. Banks’ deferred tax assets during the financial

crisis. Review of Quantitative Finance and Accounting, pp.1-24.

Hughes, T. and Poi, B., 2016. Improved deposit modeling: using Moody’s Analytics forecasts of

bank financial statements to augment internal data. Moody’s Analytics, working paper.

Khan, S., Bradbury, M.E. and Courtenay, S., 2018. Value Relevance of Comprehensive

Income. Australian Accounting Review, 28(2), pp.279-287. [Online] Available from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/auar.12181 [Accessed 21 September 2018]

Lee, T.A., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an Accounting

Practice. Routledge.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230. [Online] Available from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/1475-679X.12123 [Accessed 21 September

2018]

CORPORATE ACCOUNTING

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities: An

Evaluation of FASB's Attempt at Standards Simplification. Journal of Accounting & Finance

(2158-3625), 17(8).

Nobes, C., 2014. International classification of financial reporting. Routledge.

Penman, S.H., 2016. The design of financial statements. [Online] Available from:

https://academiccommons.columbia.edu/doi/10.7916/D82N5DNK [Accessed 21 September

2018]

Purina, M., 2016. Deferred Tax under IAS 12 in the chosen Czech and Russian

companies. Procedia-Social and Behavioral Sciences, 220, pp.382-390. [Online] Available from:

https://www.sciencedirect.com/science/article/pii/S1877042816306139 [Accessed 21 September 2018]

Tayeh, M., Al-Jarrah, I.M. and Tarhini, A., 2015. Accounting vs. market-based measures of firm

performance related to information technology investments. International Review of Social

Sciences and Humanities, 9(1), pp.129-145.

Tinkelman, D. and Fan, X., 2018. What Weekly Sparklines Could Add to Financial

Statements. Journal of Corporate Accounting & Finance, 29(1), pp.46-52. [Online] Available

from: https://onlinelibrary.wiley.com/doi/abs/10.1002/jcaf.22311 [Accessed 21 September 2018]

Tschopp, D. and Huefner, R.J., 2015. Comparing the Evolution of CSR Reporting to that of

Financial Reporting. Journal of Business Ethics, 127(3), pp.565-577.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis. Cambridge

University Press.

Yasseen, Y., Jansen, J. and Small, R., 2016. Accounting for deferred taxation: accounting

technical. Professional Accountant, 2016(27), pp.14-16. [Online] Available from:

https://www.ingentaconnect.com/content/sabinet/account/2016/00002016/00000027/art00005 [Accessed

21 September 2018]

Paraphrase This Document

CORPORATE ACCOUNTING

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.