Corporate Accounting Assignment: AASB 3 Business Combination Analysis

VerifiedAdded on 2021/10/10

|7

|1928

|141

Homework Assignment

AI Summary

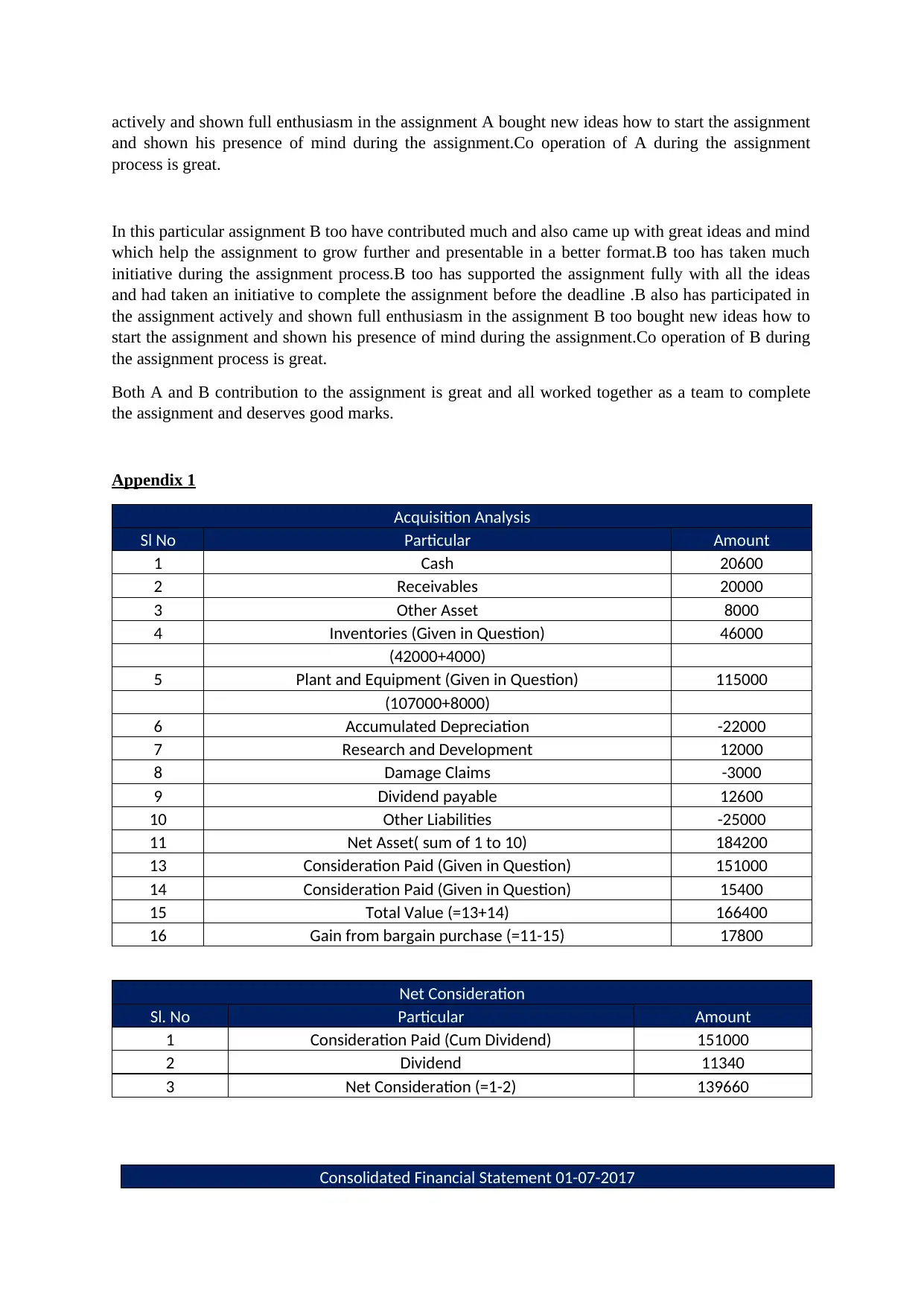

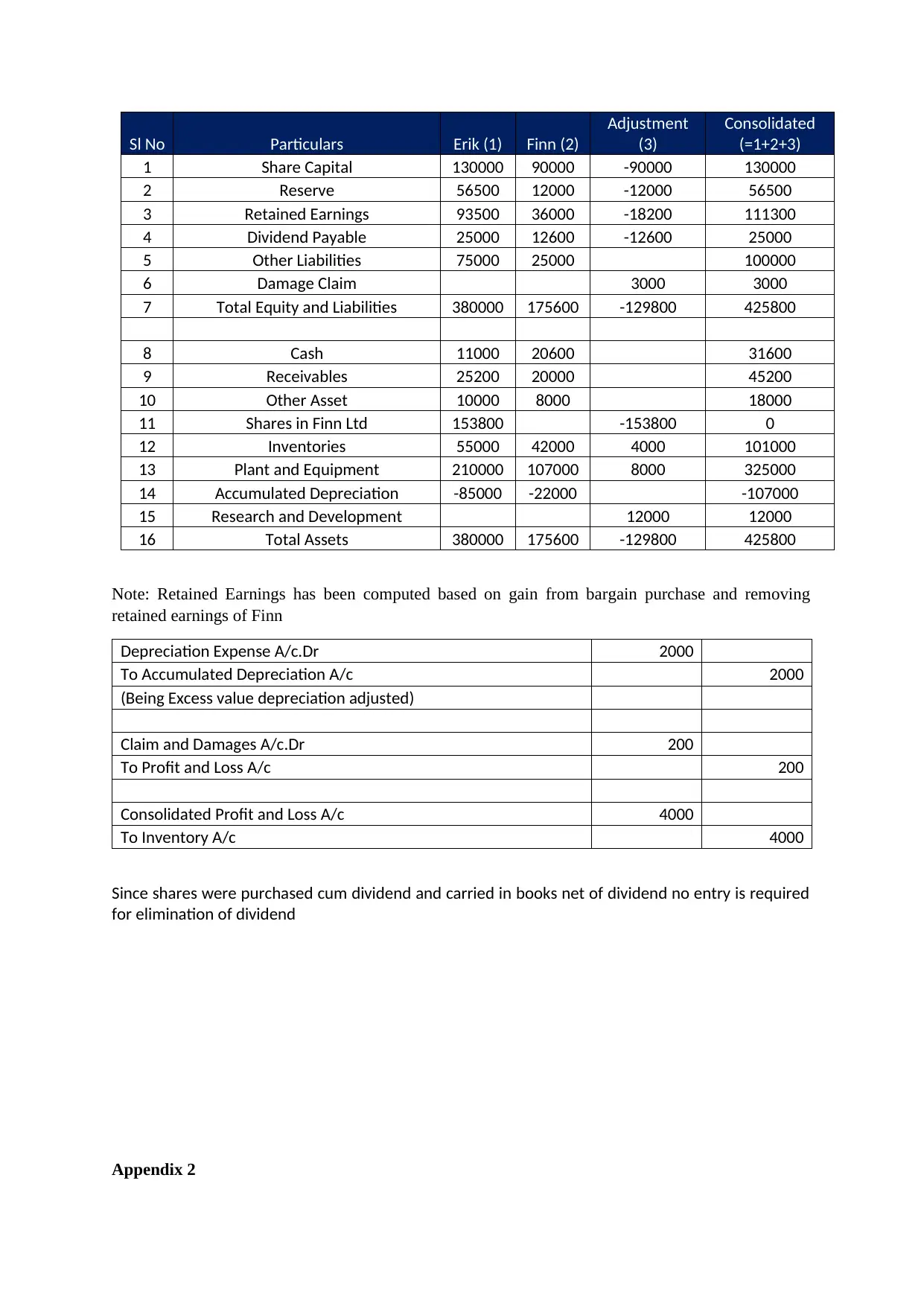

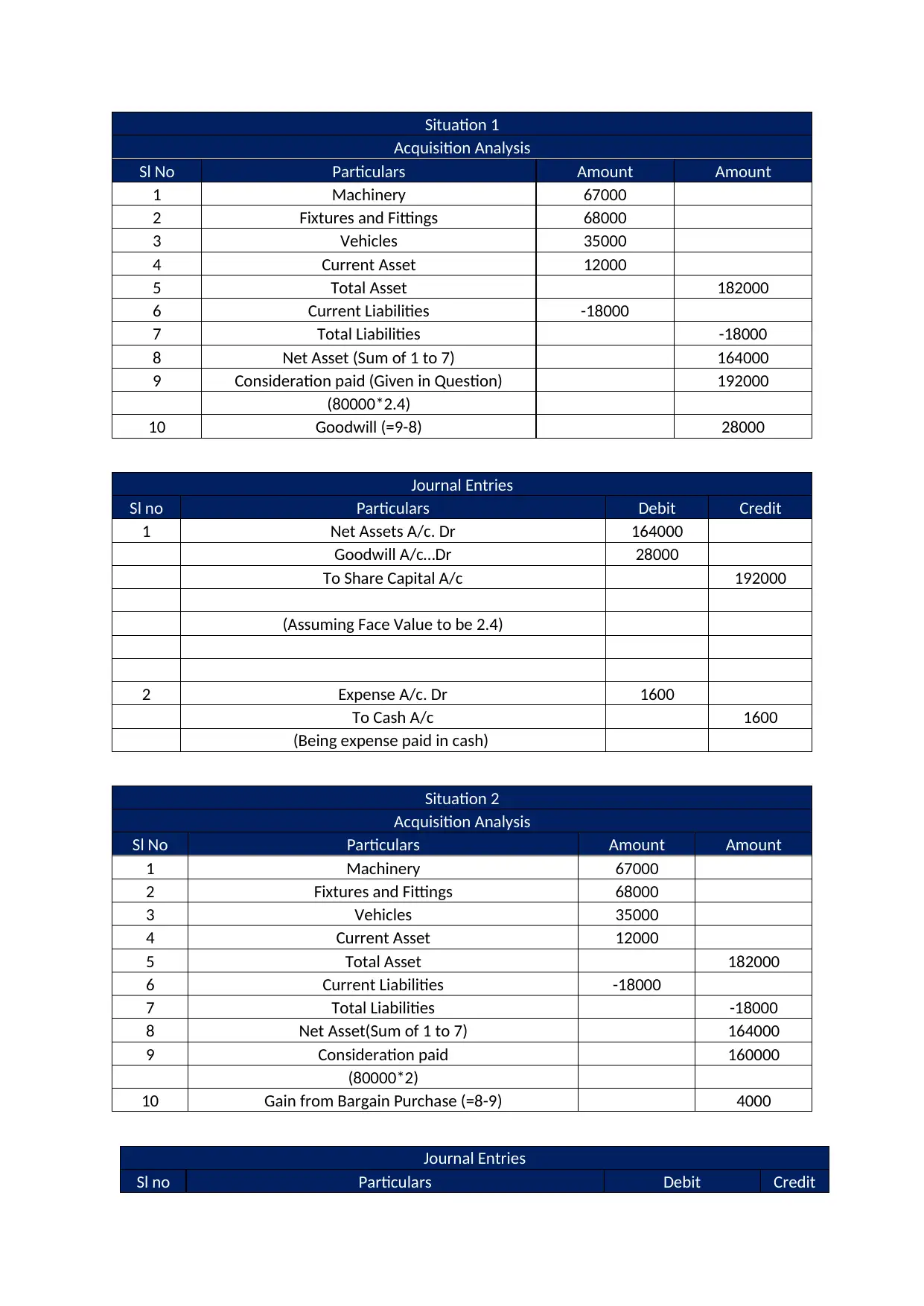

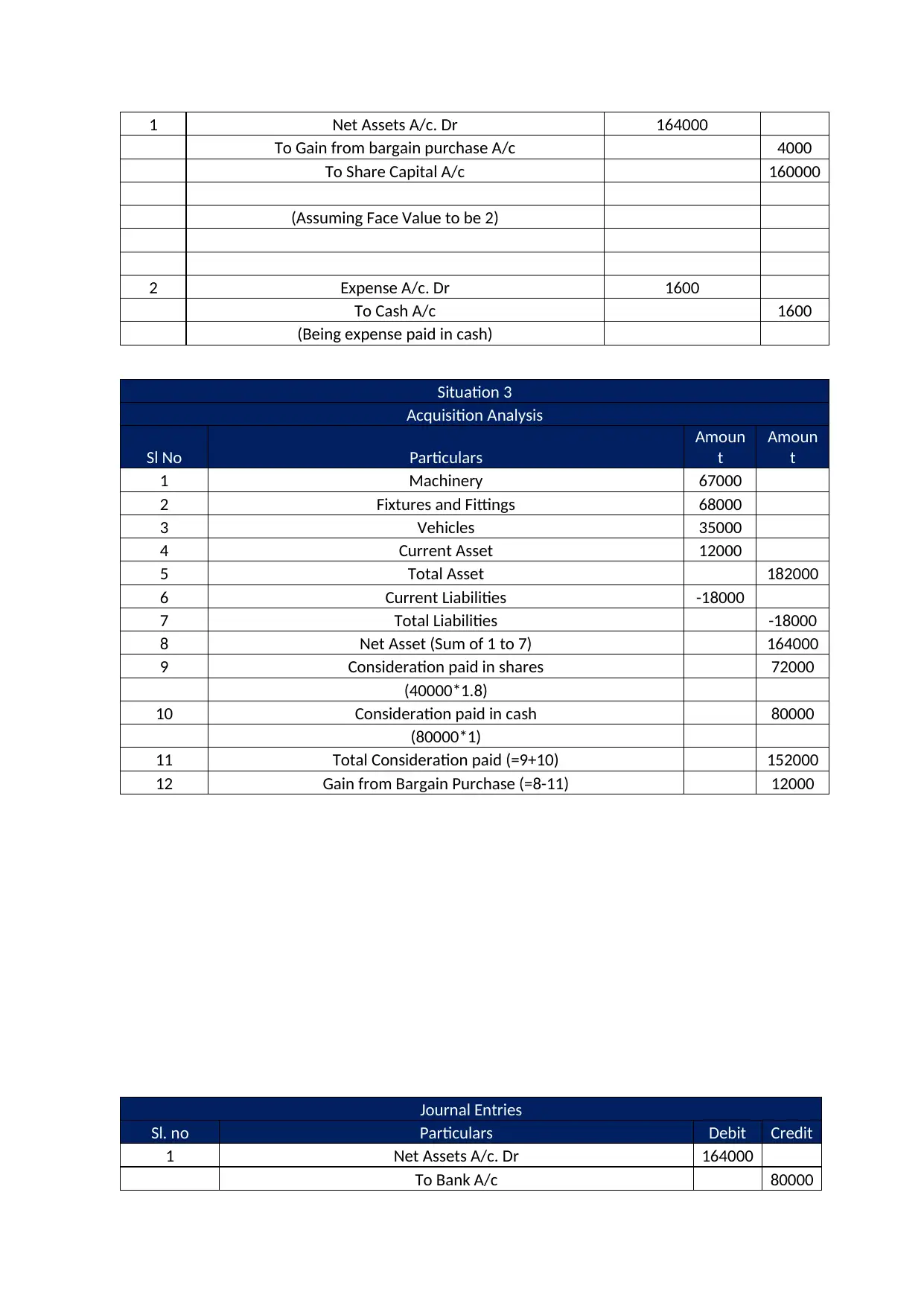

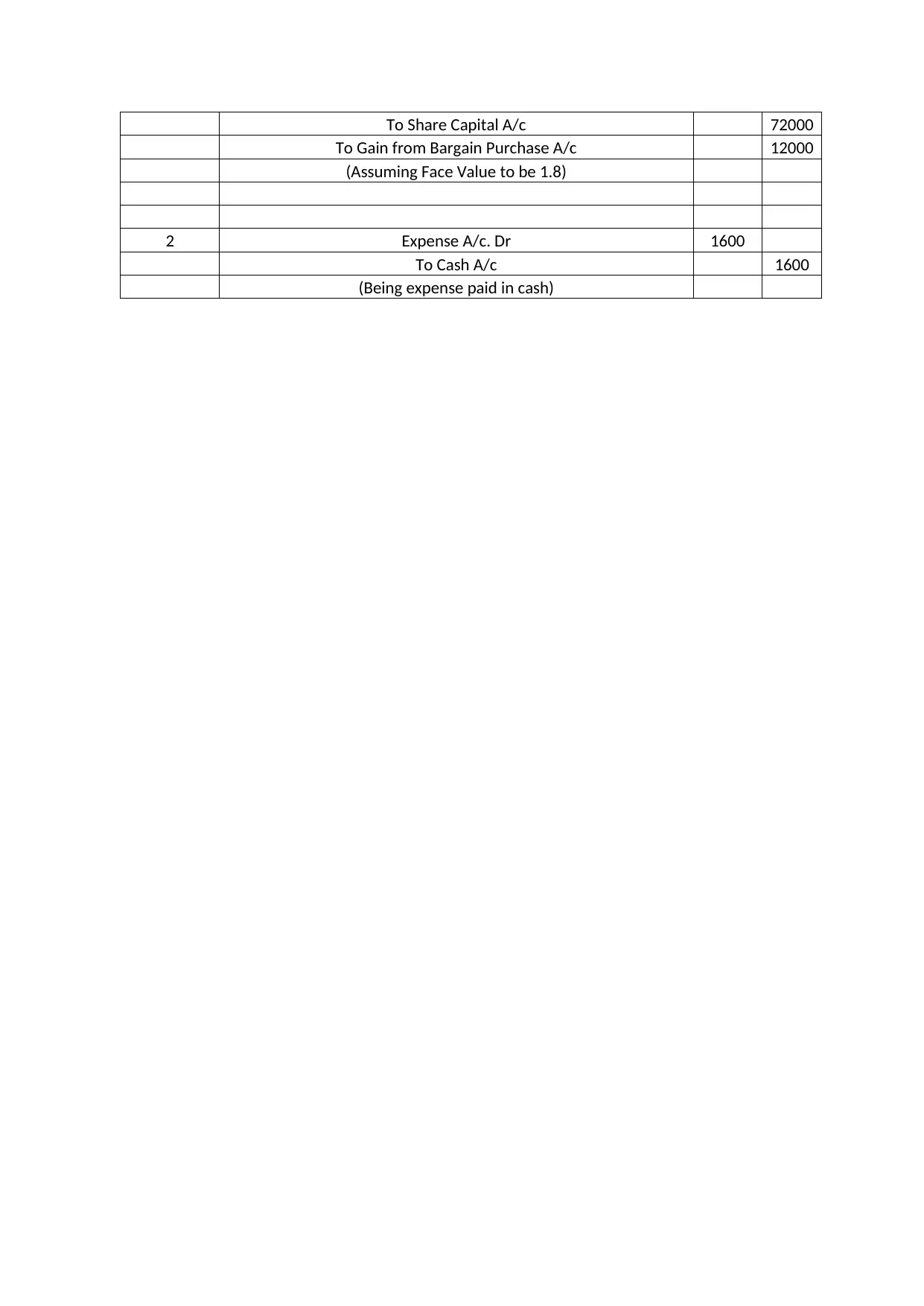

This assignment delves into the Australian Accounting Standards Board (AASB) 3, focusing on business combinations and acquisition analysis. It examines the application of AASB 3 to ensure the relevance, reliability, and comparability of financial statements. The assignment outlines key terms like acquirer, non-controlling interest, and subsidiary, along with the acquisition method, including the identification of the acquirer, determination of the acquisition date, and the recognition of assets, liabilities, and non-controlling interests. It emphasizes the importance of recognizing goodwill or gain from bargain purchases and the use of fair value for asset and liability valuation. The analysis includes case studies that apply AASB 3 to various scenarios, such as acquisitions involving share considerations and cash payments, and the computation of goodwill or bargain gains. The solution also provides insights into consolidated financial statements, including necessary adjustments for depreciation, liabilities, and inventory, alongside journal entries for different acquisition scenarios. Additionally, the assignment includes a peer review section highlighting the contributions of team members. The appendix provides detailed acquisition analyses and consolidated financial statements, along with relevant journal entries.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.