Corporate Accounting Report: Fair Value Disclosures and Analysis

VerifiedAdded on 2023/06/05

|8

|1972

|135

Report

AI Summary

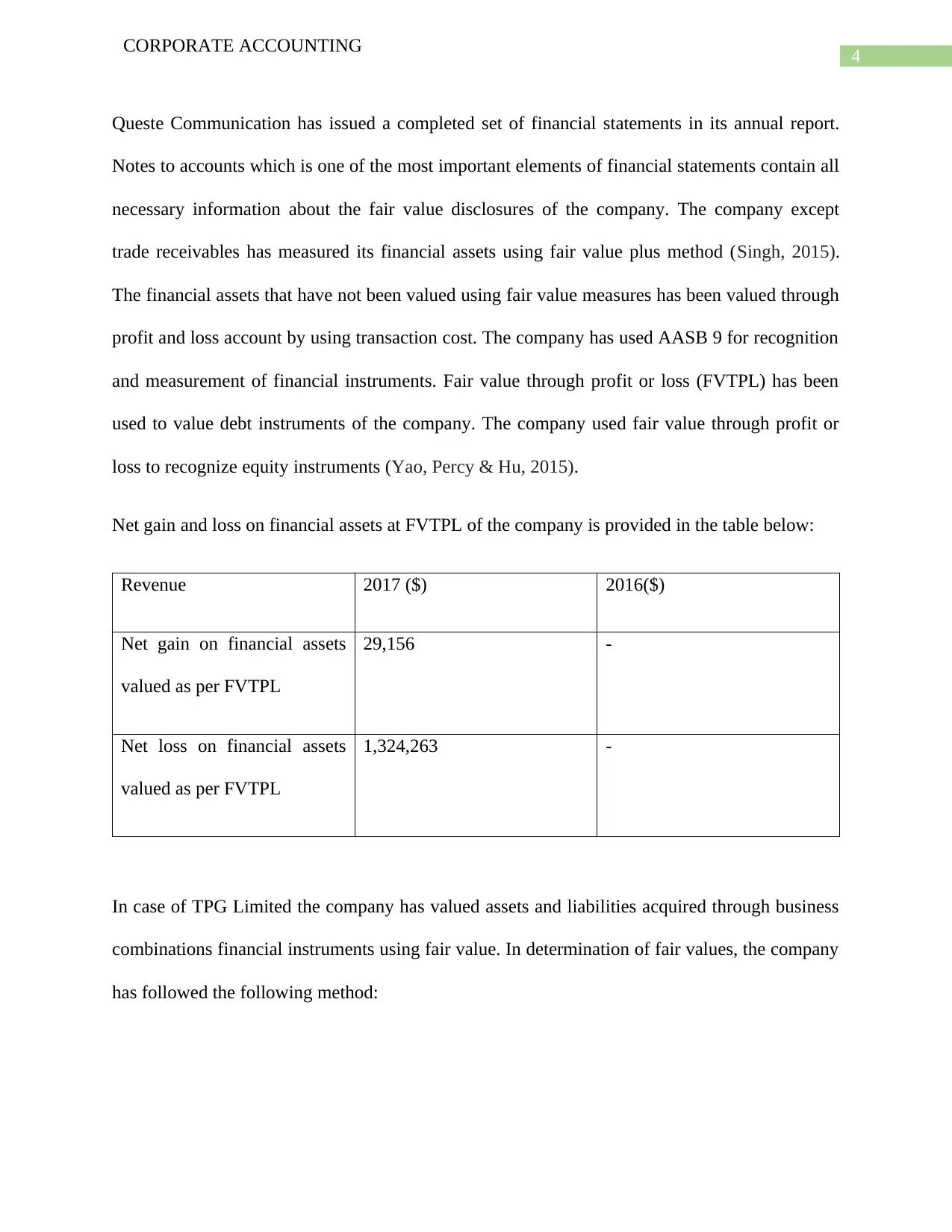

This report delves into the concept of corporate accounting, specifically focusing on fair value accounting (FVA). It begins by tracing the evolution of accounting and the introduction of FVA, which aims to disclose the value of assets and liabilities at potential market prices. The report acknowledges the debates surrounding FVA, especially in light of accounting scandals, while highlighting its relevance in corporate reporting. It contrasts FVA with historical costing, discussing the advantages and disadvantages of each method. The report then examines the use of FVA in two Australian companies, Queste Communications Limited and TPG Telecom Limited, analyzing their financial disclosures and valuation methods for various assets and liabilities, including property, plant, and equipment, intangible assets, inventories, and trade receivables. The report uses the annual reports to demonstrate the practical application of FVA. The report concludes by emphasizing the importance of the integrity of management in financial reporting and the need for ongoing development and improvement in accounting practices.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.