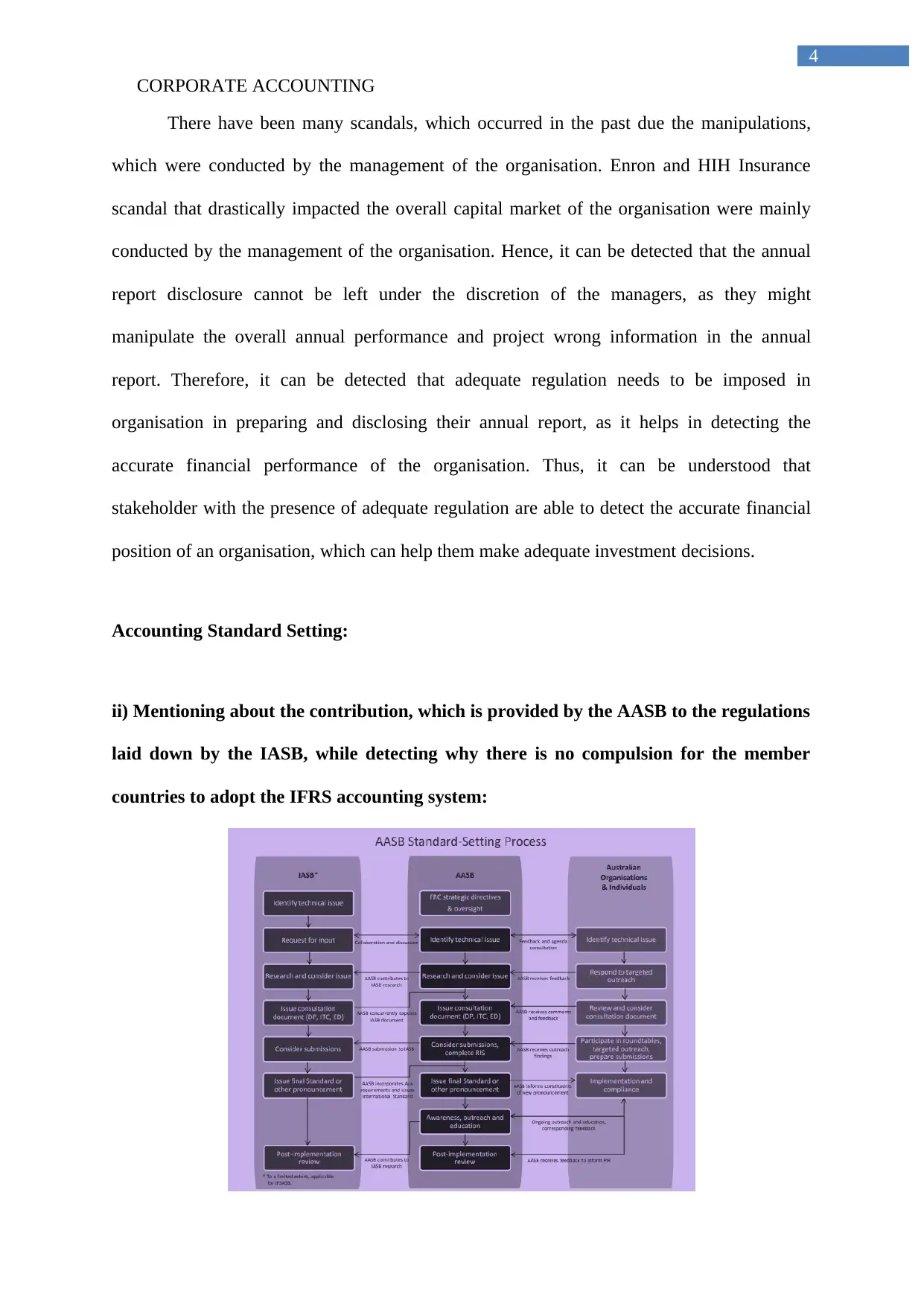

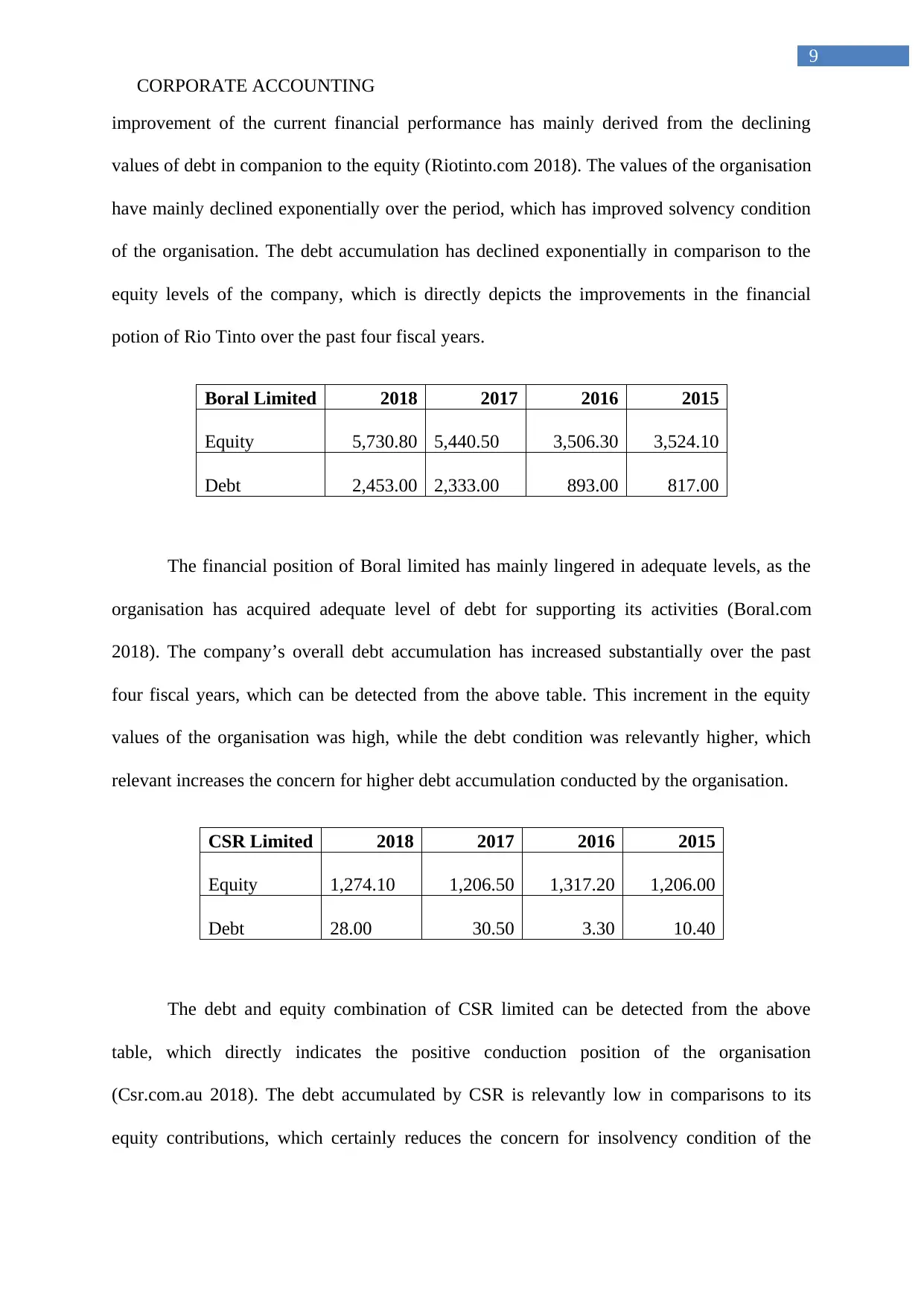

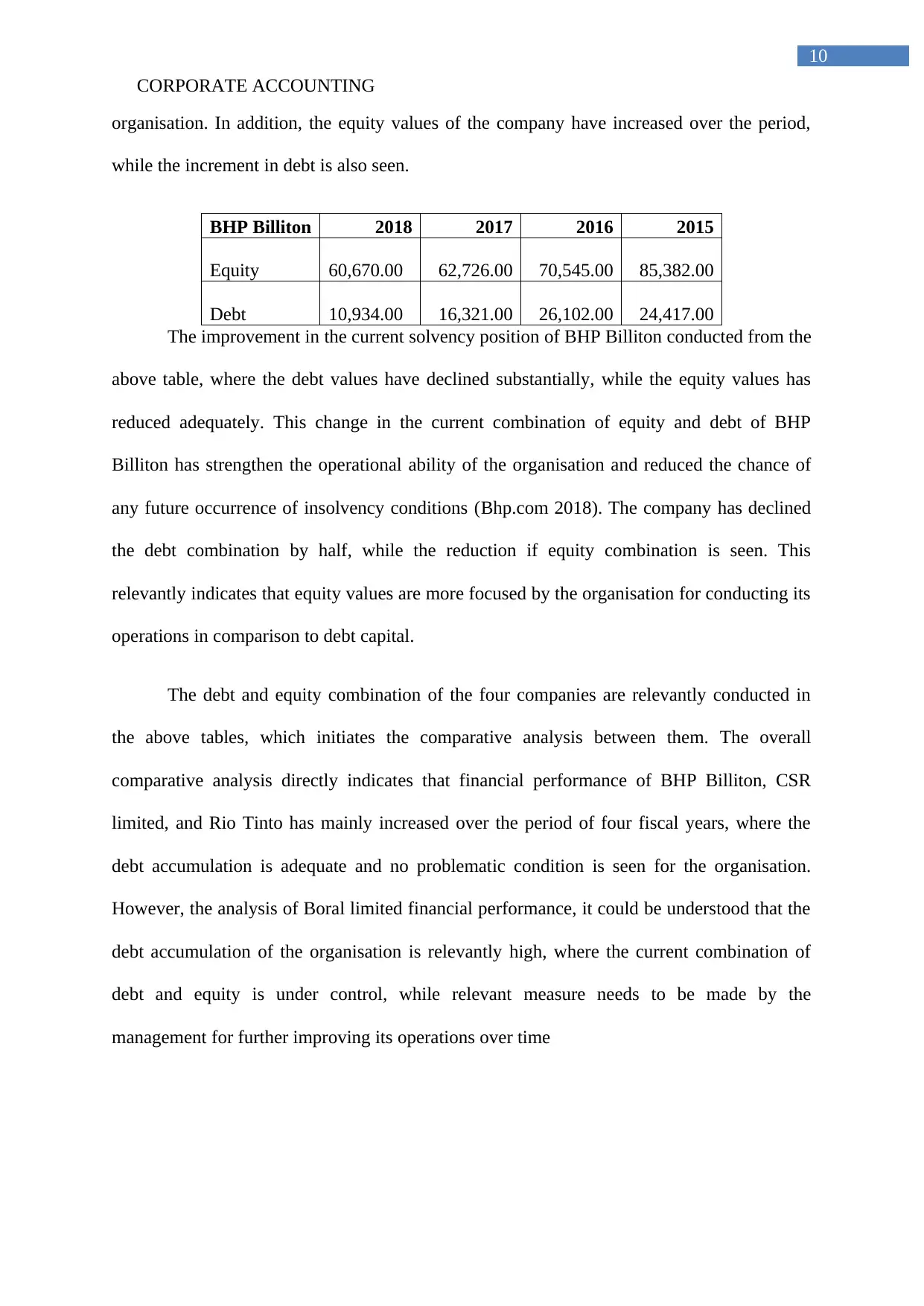

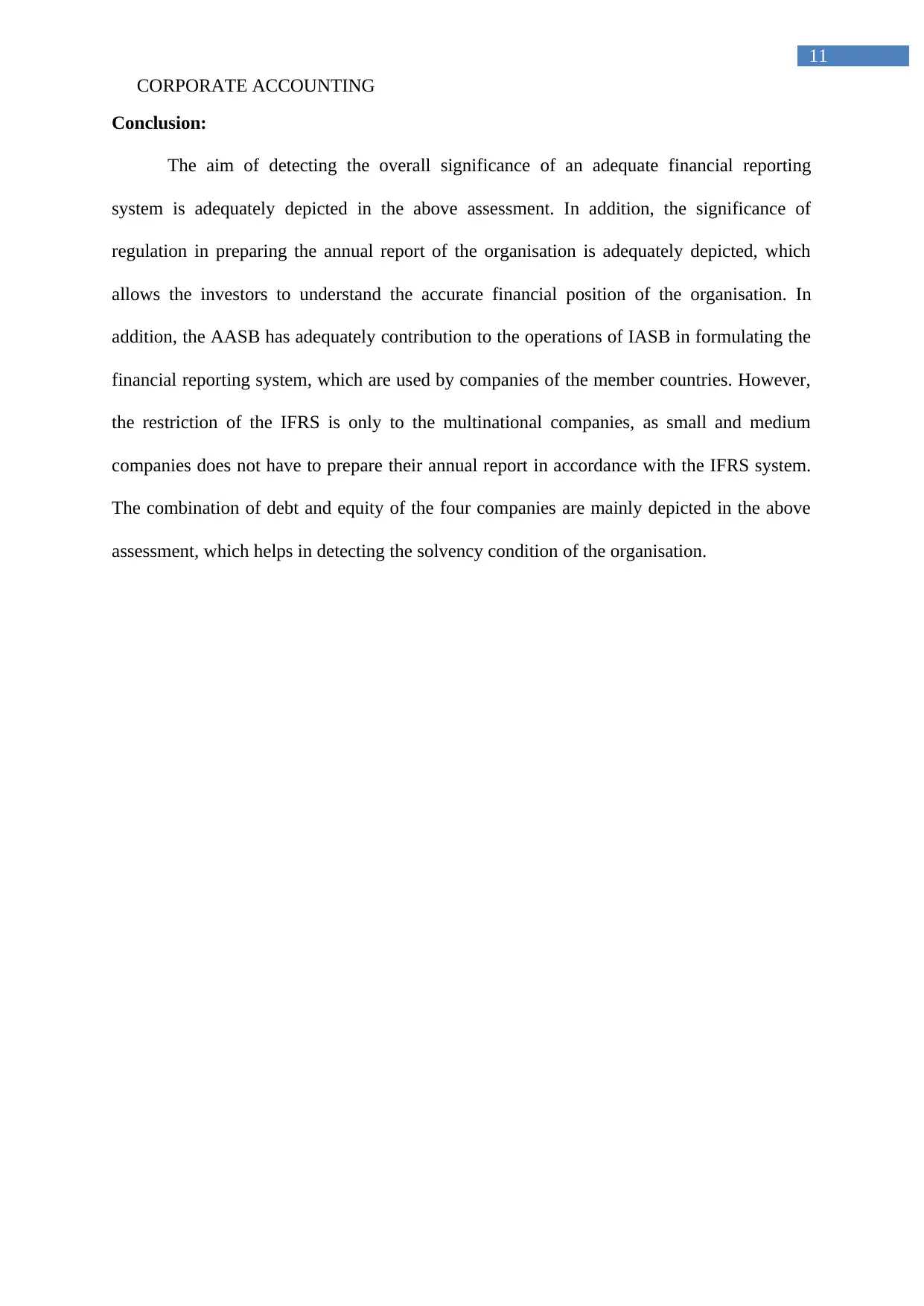

The report aims in detecting the financial reporting system and standards, which can be used by the organisation for depicting their accurate financial performance in the annual report. The assessment also aims in evaluating the overall contributions, which has been conducted by the Australian Accounting Standard Board in drafting the conceptual framework for the organisation. The debt and equity combination for the selected companies are mainly conducted in the assessment for deriving their current solvency condition. In addition, the comparative analysis is conducted on the overall four companies for detecting their operational capability, which has been noticed from the equity and debt combinations.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)