Holmes Institute: Corporate Accounting Report - Telstra and TPG

VerifiedAdded on 2023/06/04

|27

|5087

|482

Report

AI Summary

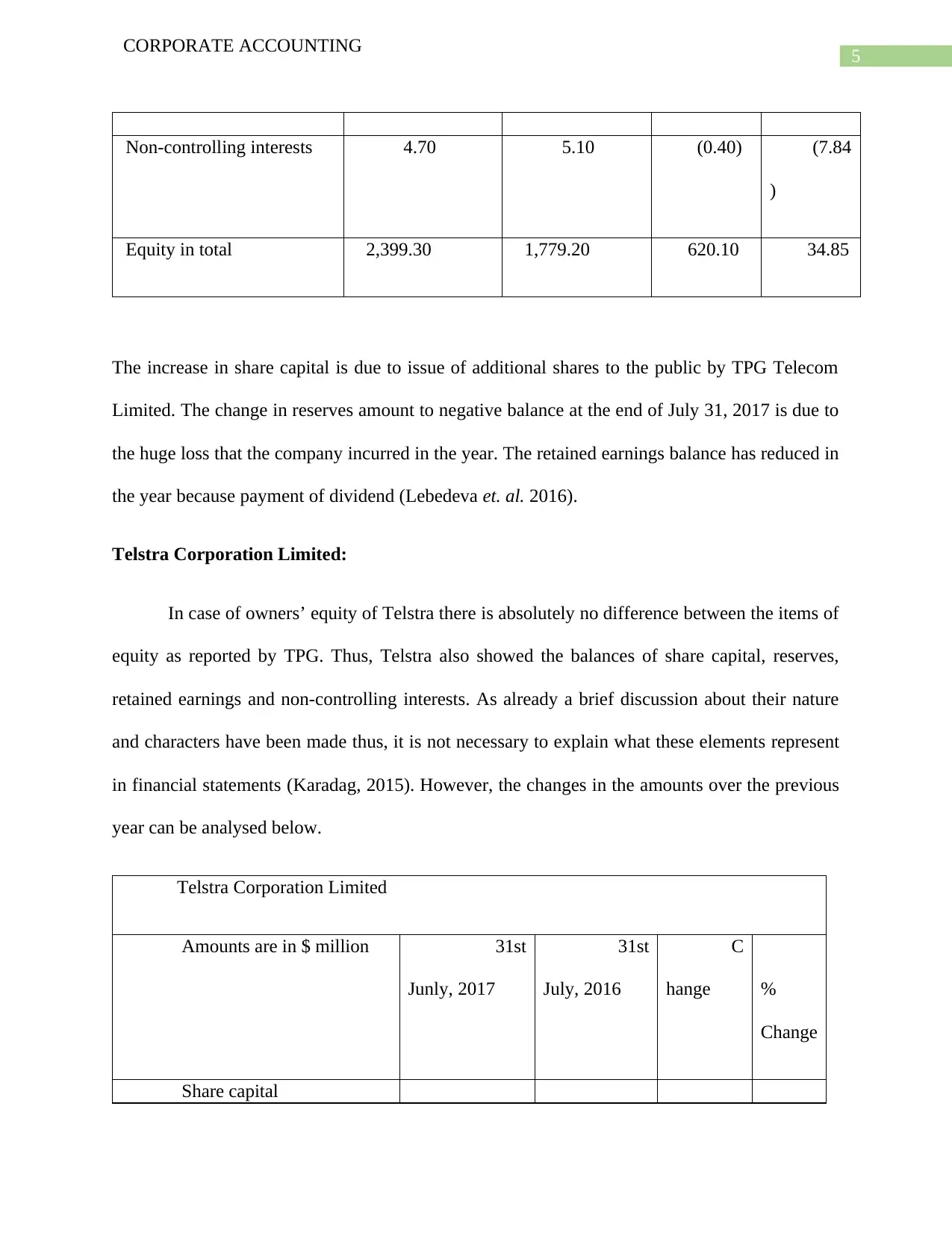

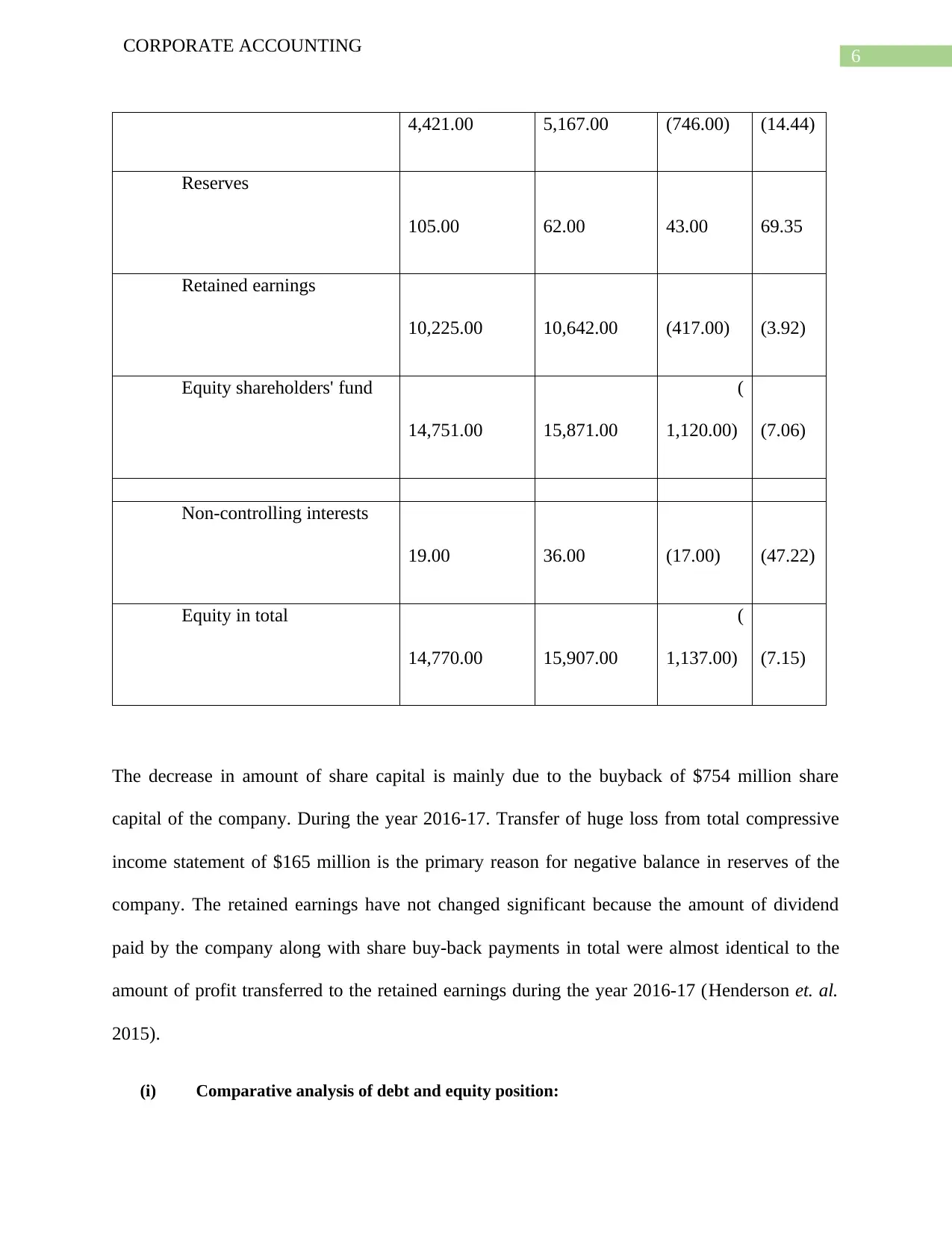

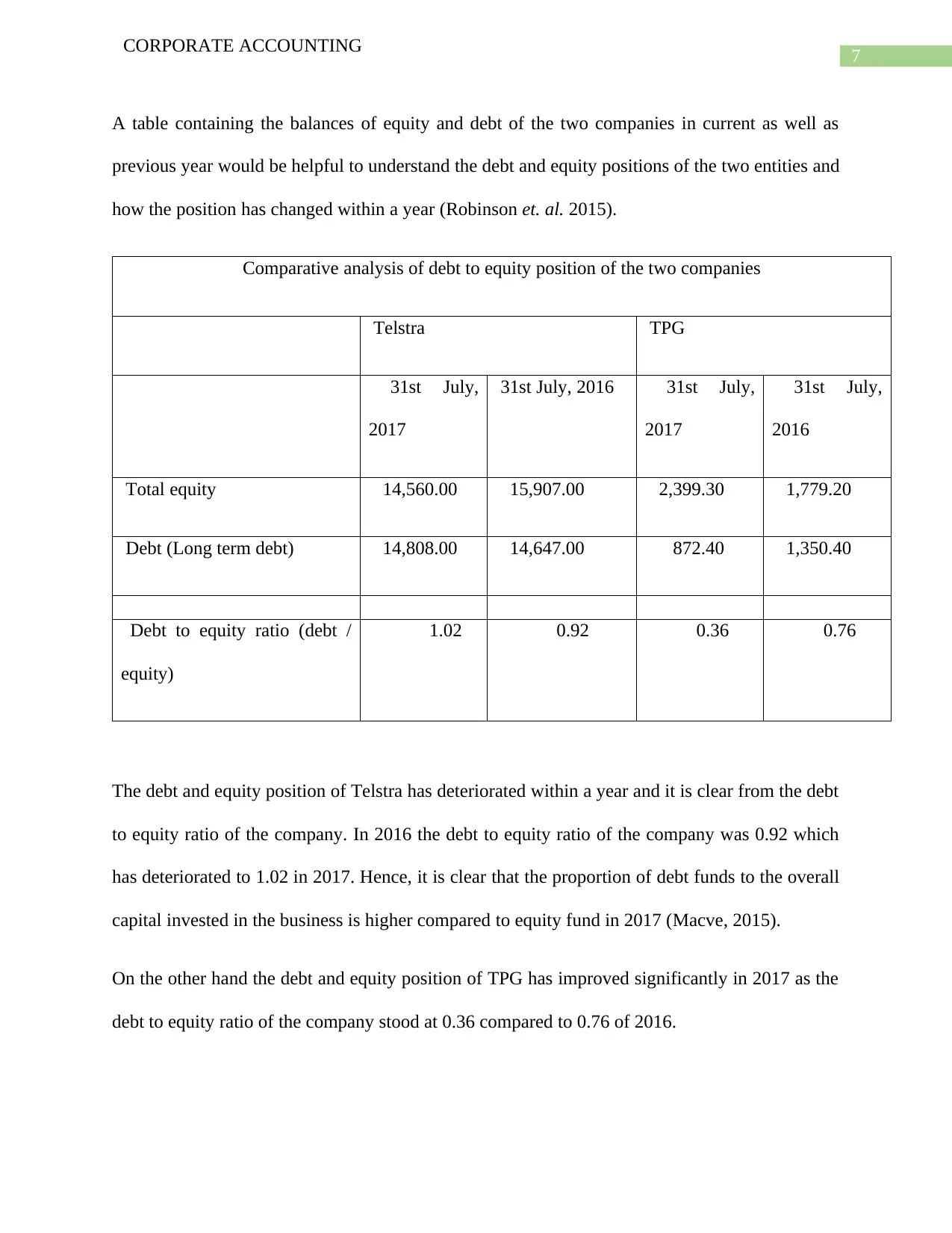

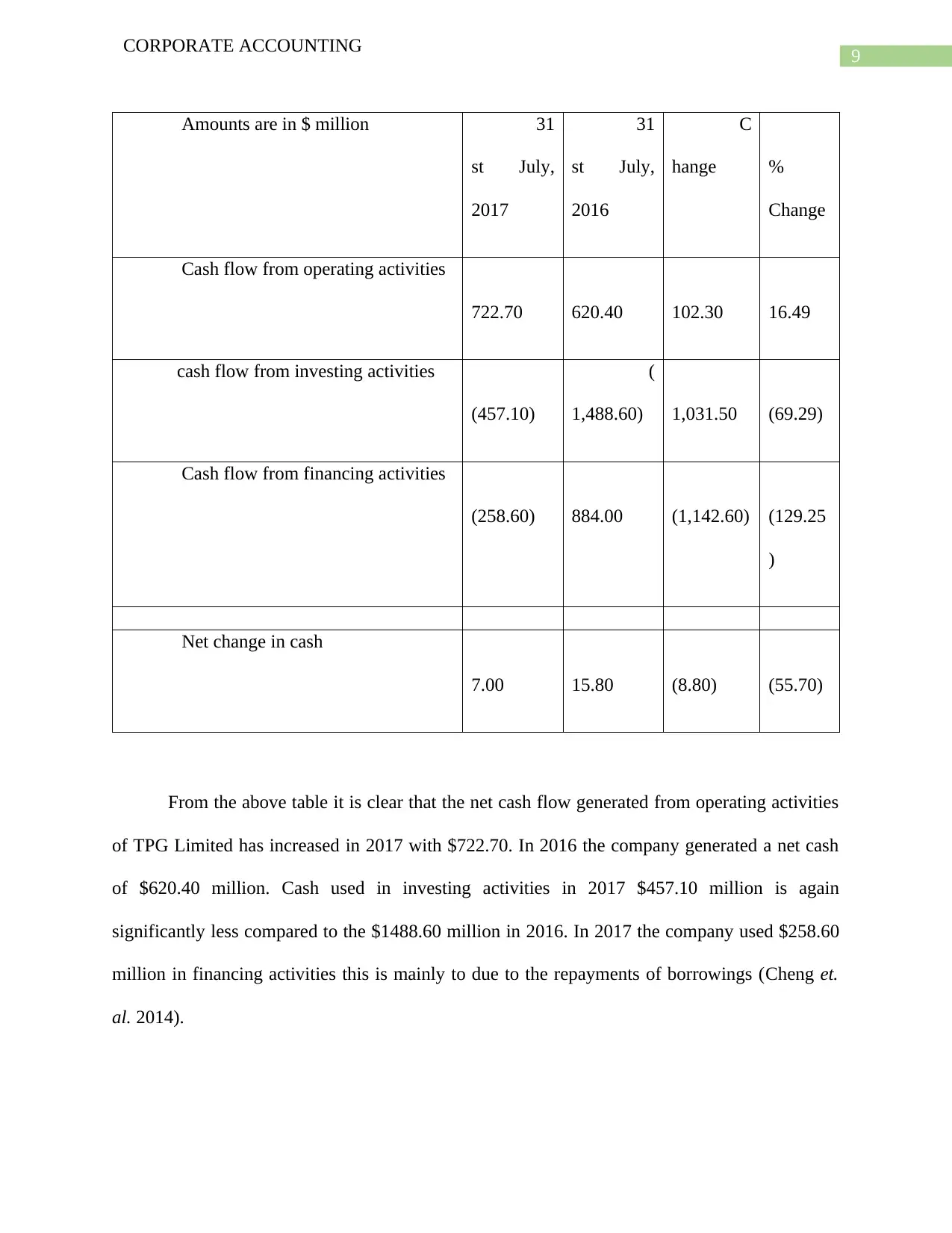

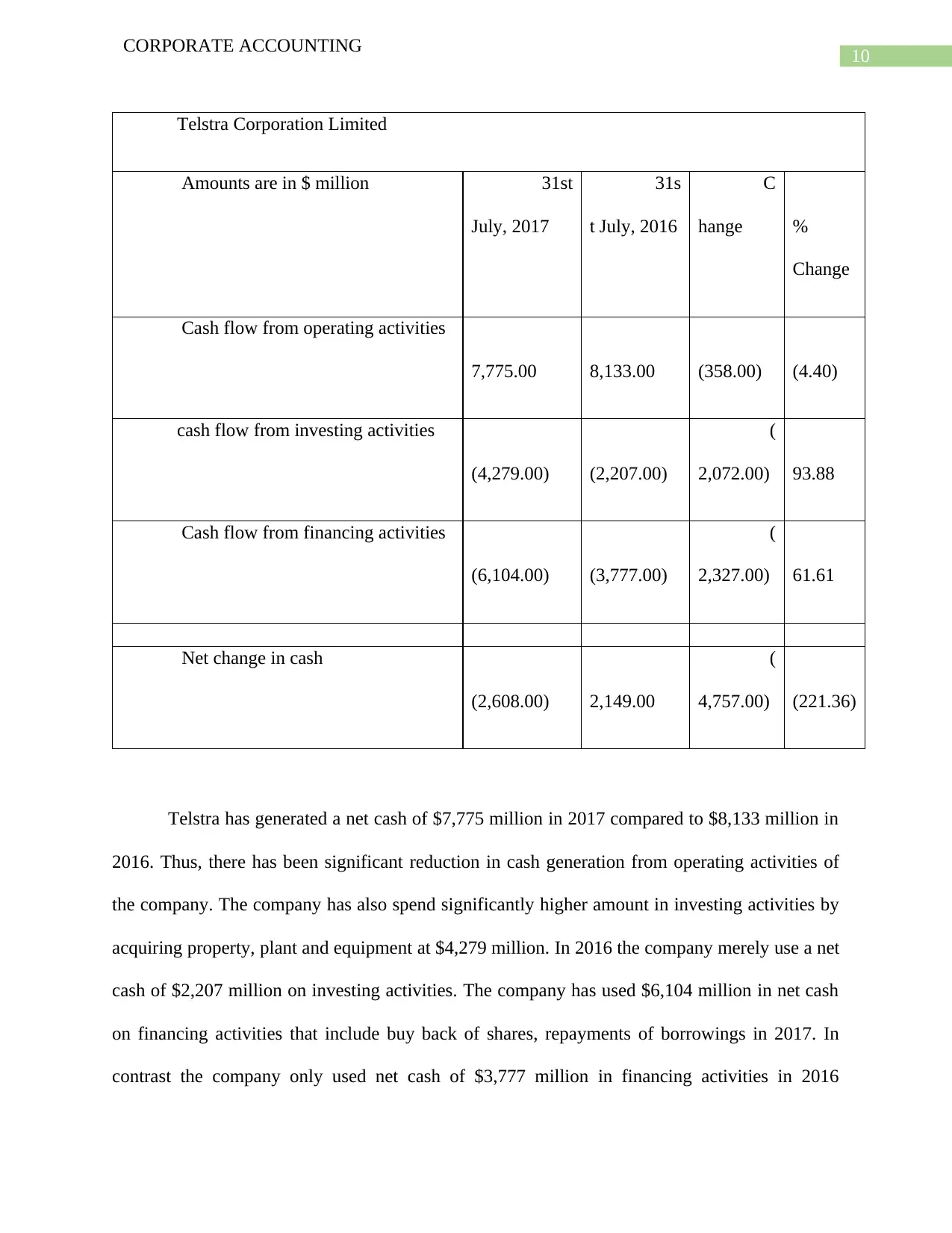

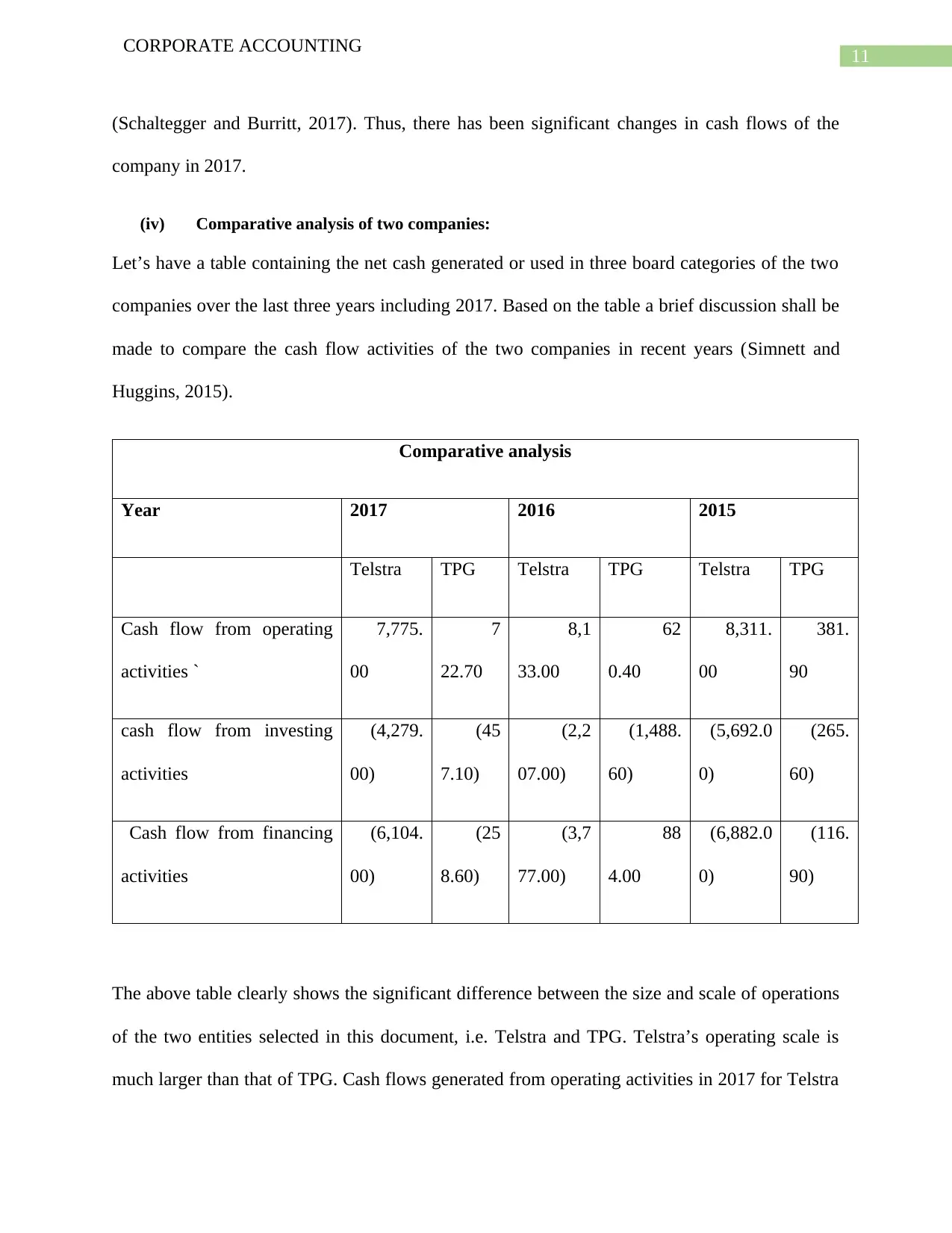

This report provides a comprehensive analysis of the financial statements of two Australian Securities Exchange (ASX) listed companies, Telstra Corporation Limited and TPG Telecom Limited, as required by a Corporate Accounting assignment. The report begins with an executive summary and introduction to both companies, followed by an in-depth examination of their owners' equity, including share capital, reserves, retained earnings, and non-controlling interests, with comparative analyses of changes over time. The analysis extends to cash flow statements, comparing operating, investing, and financing activities, along with a comparative debt to equity analysis. The report also delves into the other comprehensive income statements, identifying key items like foreign exchange translation effects and fair value changes. Finally, the report covers corporate income tax accounting and concludes with a summary of the findings, providing a thorough overview of the financial performance and positions of Telstra and TPG Telecom.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.