Corporate Accounting | Sample Assignment

VerifiedAdded on 2021/06/15

|10

|2270

|17

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING

Cash flow statement:

Requirement (i):

In order to fulfil the criteria of this assignment, the organisation chosen is Virgin

Australia Limited, which is operating in the aviation industry of Australia. The airline has found

itself listed on the ASX and its ticker symbol is VAH. It contains certain sections in its cash flow

statement and they are elucidated briefly as follows:

Cash flows from operating activities:

This section involves various items listed, which are considered as significant business

aspects for Virgin Australia Group. The items listed include the following:

Amounts collected from the customers

Amounts paid to the staffs and suppliers

Receipt and payment of finance income and finance expense

The customer receipts are those amounts obtained from credit sales (Reid & Myddelton,

2017). Since the organisation has tightened its credit policy, it has experienced a significant

increase in amounts received from the customers. The supplier and staff payments are the

amounts that Virgin has purchased on credit and salaries to the employees. There is considerable

increase in this item, as Virgin Australia has to meet the rising consumer demand by buying

additional materials from the suppliers. Finance income could be explained as the revenue made

and reported on the monetary statements of a business organisation. Since some part of the loans

provided could not be accumulated, a rising trend could be observed in finance income

(Virginaustralia.com, 2018). The short-term and long-term dues of the airline are considered in

Cash flow statement:

Requirement (i):

In order to fulfil the criteria of this assignment, the organisation chosen is Virgin

Australia Limited, which is operating in the aviation industry of Australia. The airline has found

itself listed on the ASX and its ticker symbol is VAH. It contains certain sections in its cash flow

statement and they are elucidated briefly as follows:

Cash flows from operating activities:

This section involves various items listed, which are considered as significant business

aspects for Virgin Australia Group. The items listed include the following:

Amounts collected from the customers

Amounts paid to the staffs and suppliers

Receipt and payment of finance income and finance expense

The customer receipts are those amounts obtained from credit sales (Reid & Myddelton,

2017). Since the organisation has tightened its credit policy, it has experienced a significant

increase in amounts received from the customers. The supplier and staff payments are the

amounts that Virgin has purchased on credit and salaries to the employees. There is considerable

increase in this item, as Virgin Australia has to meet the rising consumer demand by buying

additional materials from the suppliers. Finance income could be explained as the revenue made

and reported on the monetary statements of a business organisation. Since some part of the loans

provided could not be accumulated, a rising trend could be observed in finance income

(Virginaustralia.com, 2018). The short-term and long-term dues of the airline are considered in

2CORPORATE ACCOUNTING

the form of finance income and decline is inherent in this item in 2017, as the payment of interest

on loans taken is minimised.

Cash flows from investing activities:

The main items listed under this section comprise of payments for and proceedings from

property, plant and equipment, proceeds from and advances to deposits and others. It is

necessary to pay certain amount for acquiring property, plant and equipment and payments are to

be made for carrying out the overall business operations. On the other hand, as these assets

provide economic benefits to the organisation, which are considered as proceeds. It could be

observed that Virgin Australia has minimised its investment in this item and due to this, it has

not generated adequate cash flows from such items, as it has sold a part of its property, plant and

equipment. The deposit proceeds and payments are financial instruments. in which the

organisation would earn and pay the principal along with interest obtained and interest paid

(Collins, Hribar & Tian, 2014). Due to higher payments of interests, the proceeds are deemed to

be lower than payments.

Cash flows from financing activities:

The main items that are included under this head are repayment of and proceed from

borrowings, equity distributions and other items. In loan agreements, the lenders disburse

amounts to the borrowers (Miao, Teoh & Zhu, 2016). In accordance with the latest annual report

of Virgin Australia, the organisation has failed to increase the earnings from borrowings. On the

other hand, it has made more borrowing payments in the year 2017. Equity distribution signifies

the annual cash flow, which is given to the shareholders of an organisation. For Virgin, the

amount has declined in 2017, since emphasis has been placed on maximising retained earnings.

the form of finance income and decline is inherent in this item in 2017, as the payment of interest

on loans taken is minimised.

Cash flows from investing activities:

The main items listed under this section comprise of payments for and proceedings from

property, plant and equipment, proceeds from and advances to deposits and others. It is

necessary to pay certain amount for acquiring property, plant and equipment and payments are to

be made for carrying out the overall business operations. On the other hand, as these assets

provide economic benefits to the organisation, which are considered as proceeds. It could be

observed that Virgin Australia has minimised its investment in this item and due to this, it has

not generated adequate cash flows from such items, as it has sold a part of its property, plant and

equipment. The deposit proceeds and payments are financial instruments. in which the

organisation would earn and pay the principal along with interest obtained and interest paid

(Collins, Hribar & Tian, 2014). Due to higher payments of interests, the proceeds are deemed to

be lower than payments.

Cash flows from financing activities:

The main items that are included under this head are repayment of and proceed from

borrowings, equity distributions and other items. In loan agreements, the lenders disburse

amounts to the borrowers (Miao, Teoh & Zhu, 2016). In accordance with the latest annual report

of Virgin Australia, the organisation has failed to increase the earnings from borrowings. On the

other hand, it has made more borrowing payments in the year 2017. Equity distribution signifies

the annual cash flow, which is given to the shareholders of an organisation. For Virgin, the

amount has declined in 2017, since emphasis has been placed on maximising retained earnings.

3CORPORATE ACCOUNTING

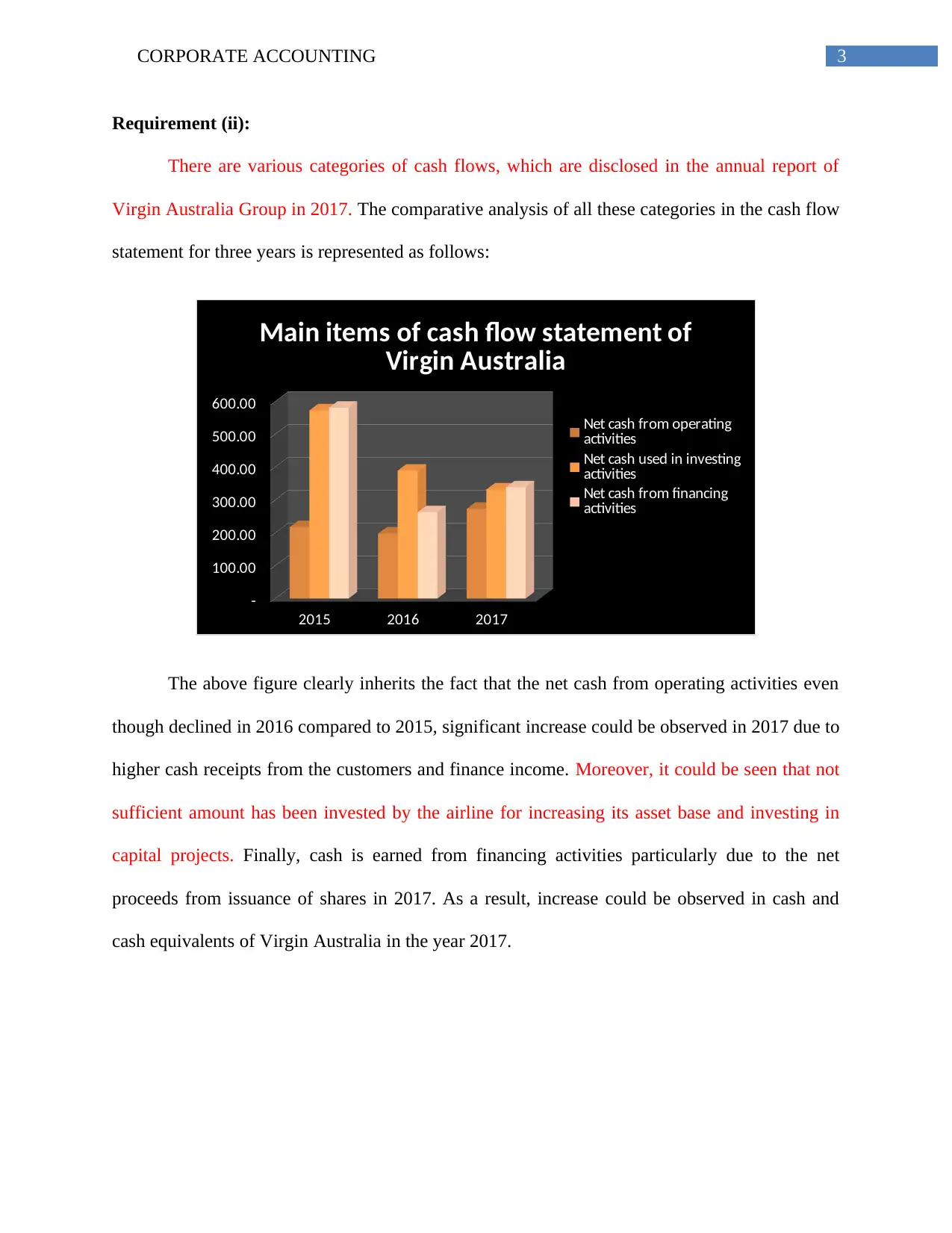

Requirement (ii):

There are various categories of cash flows, which are disclosed in the annual report of

Virgin Australia Group in 2017. The comparative analysis of all these categories in the cash flow

statement for three years is represented as follows:

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Main items of cash flow statement of

Virgin Australia

Net cash from operating

activities

Net cash used in investing

activities

Net cash from financing

activities

The above figure clearly inherits the fact that the net cash from operating activities even

though declined in 2016 compared to 2015, significant increase could be observed in 2017 due to

higher cash receipts from the customers and finance income. Moreover, it could be seen that not

sufficient amount has been invested by the airline for increasing its asset base and investing in

capital projects. Finally, cash is earned from financing activities particularly due to the net

proceeds from issuance of shares in 2017. As a result, increase could be observed in cash and

cash equivalents of Virgin Australia in the year 2017.

Requirement (ii):

There are various categories of cash flows, which are disclosed in the annual report of

Virgin Australia Group in 2017. The comparative analysis of all these categories in the cash flow

statement for three years is represented as follows:

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Main items of cash flow statement of

Virgin Australia

Net cash from operating

activities

Net cash used in investing

activities

Net cash from financing

activities

The above figure clearly inherits the fact that the net cash from operating activities even

though declined in 2016 compared to 2015, significant increase could be observed in 2017 due to

higher cash receipts from the customers and finance income. Moreover, it could be seen that not

sufficient amount has been invested by the airline for increasing its asset base and investing in

capital projects. Finally, cash is earned from financing activities particularly due to the net

proceeds from issuance of shares in 2017. As a result, increase could be observed in cash and

cash equivalents of Virgin Australia in the year 2017.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING

Other comprehensive income statement:

Requirement (iii):

According to the annual report of Virgin Australia Group in 2017, the main items listed

in the comprehensive income statement comprise of the following:

“Foreign currency translation reserve”

“Cash flow hedge reserve”

“Income tax benefit or expense”

Requirement (iv):

As commented by Collins, Hribar & Tian (2014), for foreign currency translation reserve,

it is necessary to necessary to ascertain the currency, in which the foreign unit operates. After

such ascertainment, it is crucial to regauge the financial reports of the foreign unit to the

domestic currency and accordingly, profits or losses would be measured based on currency

translation. Cash flow hedge reserve is important for minimising the cash flow variations, as

certain risk changes are inherent like debt interest rate and rate of floatation (Graham & Lin,

2018). On the other hand, income tax expense is the amount incurred on profit before tax of the

organisation.

Requirement (v):

In the words of Nejad & Ahmad (2017), the expanded view of net income is considered

as other comprehensive income. Virgin uses this statement for providing important details on the

values of the above-mentioned items. The main reason that these items are mentioned under

other comprehensive income statement is that they provide comprehensive and holistic overview

Other comprehensive income statement:

Requirement (iii):

According to the annual report of Virgin Australia Group in 2017, the main items listed

in the comprehensive income statement comprise of the following:

“Foreign currency translation reserve”

“Cash flow hedge reserve”

“Income tax benefit or expense”

Requirement (iv):

As commented by Collins, Hribar & Tian (2014), for foreign currency translation reserve,

it is necessary to necessary to ascertain the currency, in which the foreign unit operates. After

such ascertainment, it is crucial to regauge the financial reports of the foreign unit to the

domestic currency and accordingly, profits or losses would be measured based on currency

translation. Cash flow hedge reserve is important for minimising the cash flow variations, as

certain risk changes are inherent like debt interest rate and rate of floatation (Graham & Lin,

2018). On the other hand, income tax expense is the amount incurred on profit before tax of the

organisation.

Requirement (v):

In the words of Nejad & Ahmad (2017), the expanded view of net income is considered

as other comprehensive income. Virgin uses this statement for providing important details on the

values of the above-mentioned items. The main reason that these items are mentioned under

other comprehensive income statement is that they provide comprehensive and holistic overview

5CORPORATE ACCOUNTING

of the drivers related to business operations and thus, they are not disclosed in the income

statement (Nejad & Ahmad, 2017).

Accounting for corporate income tax:

Requirement (vi):

Tax expense is taken into account as an important obligation of an organisation due to

federal, municipal and state governments of the nation. In case of Virgin Australia, it has not

incurred tax expense; instead, it has obtained income tax benefit in both the years 2016 and 2017.

It could be observed that Virgin Australia has managed to earn income tax benefits in both the

years 2016 and 2017.

Requirement (vii):

The significant rise in operating expenses has resulted in loss for Virgin Australia, as

stated in its annual report before tax. A tax rate of 30% is to be charged on the earnings before

tax so that the final profit that is available in the hands of the organisation could be ascertained.

However, since the airline has incurred loss before income tax, it is not possible to account for

income tax expense. Hence, it is not possible to determine whether the tax expense of the airline

that needs to be mentioned in the income statement is calculated by using 30% tax rate on profit

before income tax expense (Dyreng, Hoopes & Wilde, 2016).

Requirement (viii):

There are various situations due to which the organisations mainly incur deferred tax

assets. This might be due to the fact that taxes are paid before earnings are realised or the tax

payments made have exceeded the actual tax amount to be incurred. On the other hand, deferred

tax liabilities are those, which are evaluated or they are due for the existing period, since

of the drivers related to business operations and thus, they are not disclosed in the income

statement (Nejad & Ahmad, 2017).

Accounting for corporate income tax:

Requirement (vi):

Tax expense is taken into account as an important obligation of an organisation due to

federal, municipal and state governments of the nation. In case of Virgin Australia, it has not

incurred tax expense; instead, it has obtained income tax benefit in both the years 2016 and 2017.

It could be observed that Virgin Australia has managed to earn income tax benefits in both the

years 2016 and 2017.

Requirement (vii):

The significant rise in operating expenses has resulted in loss for Virgin Australia, as

stated in its annual report before tax. A tax rate of 30% is to be charged on the earnings before

tax so that the final profit that is available in the hands of the organisation could be ascertained.

However, since the airline has incurred loss before income tax, it is not possible to account for

income tax expense. Hence, it is not possible to determine whether the tax expense of the airline

that needs to be mentioned in the income statement is calculated by using 30% tax rate on profit

before income tax expense (Dyreng, Hoopes & Wilde, 2016).

Requirement (viii):

There are various situations due to which the organisations mainly incur deferred tax

assets. This might be due to the fact that taxes are paid before earnings are realised or the tax

payments made have exceeded the actual tax amount to be incurred. On the other hand, deferred

tax liabilities are those, which are evaluated or they are due for the existing period, since

6CORPORATE ACCOUNTING

payments are not yet made (Taylor & Richardson, 2014). For Virgin Australia, the deferred tax

assets amount to $1,017.6 million in 2017, which were $857.9 million in 2016. On the other

hand, the deferred tax liabilities have been $463.4 million in 2017 compared to $434.4 million in

2016. Since Virgin Australia has incurred additional amount on depreciation due to the variation

in depreciation rate, deferred tax assets have deemed to occur in the year. Recognition of

deferred tax liabilities is made due to temporary variations in profits, due to which it has

obtained tax benefits in both 2016 and 2017.

Requirement (ix):

For the ASX listed entities, it is necessary to pay income tax for complying with the

taxation law of the nation. According to the annual report of Virgin Australia, it has been

evaluated that the current tax assets constitute of the expected tax payable or receivable on

taxable income or loss for the specific period. They are gauged with the help of tax rates and tax

laws enacted at the reporting year (Dowling, 2014). However, the airline has recognised net loss

in the year 2017 and the same amounts are reported in the section of reconciliation of net loss to

net cash from operations in its annual report. The main reason that these two items depict the

same values is that no excess tax expenses are incurred on the part of the organisation in both the

years.

Requirement (x):

In accordance with the annual report of Virgin Australia in 2017, it could be observed

that the organisation has not incurred any income tax expense in both the years 2016 and 2017.

Instead, it has earned income tax benefit in the stated years and this is the main reason that

income tax paid is not included as an item in the cash flow statement of the organisation

(Bennedsen & Zeume, 2017).

payments are not yet made (Taylor & Richardson, 2014). For Virgin Australia, the deferred tax

assets amount to $1,017.6 million in 2017, which were $857.9 million in 2016. On the other

hand, the deferred tax liabilities have been $463.4 million in 2017 compared to $434.4 million in

2016. Since Virgin Australia has incurred additional amount on depreciation due to the variation

in depreciation rate, deferred tax assets have deemed to occur in the year. Recognition of

deferred tax liabilities is made due to temporary variations in profits, due to which it has

obtained tax benefits in both 2016 and 2017.

Requirement (ix):

For the ASX listed entities, it is necessary to pay income tax for complying with the

taxation law of the nation. According to the annual report of Virgin Australia, it has been

evaluated that the current tax assets constitute of the expected tax payable or receivable on

taxable income or loss for the specific period. They are gauged with the help of tax rates and tax

laws enacted at the reporting year (Dowling, 2014). However, the airline has recognised net loss

in the year 2017 and the same amounts are reported in the section of reconciliation of net loss to

net cash from operations in its annual report. The main reason that these two items depict the

same values is that no excess tax expenses are incurred on the part of the organisation in both the

years.

Requirement (x):

In accordance with the annual report of Virgin Australia in 2017, it could be observed

that the organisation has not incurred any income tax expense in both the years 2016 and 2017.

Instead, it has earned income tax benefit in the stated years and this is the main reason that

income tax paid is not included as an item in the cash flow statement of the organisation

(Bennedsen & Zeume, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

Requirement (xi):

After critical assessment of the tax treatment of Virgin Australia, the surprising element

that has been found is that it has suffered loss before incurring income tax expense in both 2016

and 2017, due to which it has earned income tax benefit. As a result, it has become difficult to

relate the actual tax expense paid with the prevailing tax rate of the nation. In addition, since no

income tax expense has been incurred, there is no mentioning of income tax paid in the cash flow

statement of the organisation. However, it has made relevant disclosures regarding the income

tax benefits obtained and this helped in acquiring knowledge about its tax treatment.

Requirement (xi):

After critical assessment of the tax treatment of Virgin Australia, the surprising element

that has been found is that it has suffered loss before incurring income tax expense in both 2016

and 2017, due to which it has earned income tax benefit. As a result, it has become difficult to

relate the actual tax expense paid with the prevailing tax rate of the nation. In addition, since no

income tax expense has been incurred, there is no mentioning of income tax paid in the cash flow

statement of the organisation. However, it has made relevant disclosures regarding the income

tax benefits obtained and this helped in acquiring knowledge about its tax treatment.

8CORPORATE ACCOUNTING

References:

Virginaustralia.com. (2018). Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/

2017-annual-report.pdf

Reid, W., & Myddelton, D. R. (2017). Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Miao, B., Teoh, S. H., & Zhu, Z. (2016). Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), 473-515.

Collins, D. W., Hribar, P., & Tian, X. S. (2014). Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics, 58(2-3), 173-200.

Nejad, M. Y., Ahmad, A., & Embong, Z. (2018). Value Relevance Of Other Comprehensive

Income. Asian Journal of Accounting and Governance, 8, 133-144.

Graham, R. C., & Lin, K. C. (2018). The influence of other comprehensive income on

discretionary expenditures. Journal of Business Finance & Accounting, 45(1-2), 72-91.

Nejad, M. Y., & Ahmad, A. (2017). Value Relevance of available-for-sale financial instruments

(AFS) and revaluation surplus of PPE (REV) components of other comprehensive income.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Marchini, P. L., & D'Este, C. (2015). Comprehensive Income: which potential effects on firms’

performance evaluation and users’ decision process?. Financial reporting.

References:

Virginaustralia.com. (2018). Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/

2017-annual-report.pdf

Reid, W., & Myddelton, D. R. (2017). Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Miao, B., Teoh, S. H., & Zhu, Z. (2016). Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), 473-515.

Collins, D. W., Hribar, P., & Tian, X. S. (2014). Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics, 58(2-3), 173-200.

Nejad, M. Y., Ahmad, A., & Embong, Z. (2018). Value Relevance Of Other Comprehensive

Income. Asian Journal of Accounting and Governance, 8, 133-144.

Graham, R. C., & Lin, K. C. (2018). The influence of other comprehensive income on

discretionary expenditures. Journal of Business Finance & Accounting, 45(1-2), 72-91.

Nejad, M. Y., & Ahmad, A. (2017). Value Relevance of available-for-sale financial instruments

(AFS) and revaluation surplus of PPE (REV) components of other comprehensive income.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Marchini, P. L., & D'Este, C. (2015). Comprehensive Income: which potential effects on firms’

performance evaluation and users’ decision process?. Financial reporting.

9CORPORATE ACCOUNTING

Dyreng, S. D., Hoopes, J. L., & Wilde, J. H. (2016). Public pressure and corporate tax

behavior. Journal of Accounting Research, 54(1), 147-186.

Taylor, G., & Richardson, G. (2014). Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

1-15.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Bennedsen, M., & Zeume, S. (2017). Corporate tax havens and transparency. The Review of

Financial Studies, 31(4), 1221-1264.

Dyreng, S. D., Hoopes, J. L., & Wilde, J. H. (2016). Public pressure and corporate tax

behavior. Journal of Accounting Research, 54(1), 147-186.

Taylor, G., & Richardson, G. (2014). Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

1-15.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Bennedsen, M., & Zeume, S. (2017). Corporate tax havens and transparency. The Review of

Financial Studies, 31(4), 1221-1264.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.