Group Assignment: Corporate Accounting (ACC2CRE) - Semester 2, 2018

VerifiedAdded on 2023/06/04

|16

|2342

|376

Project

AI Summary

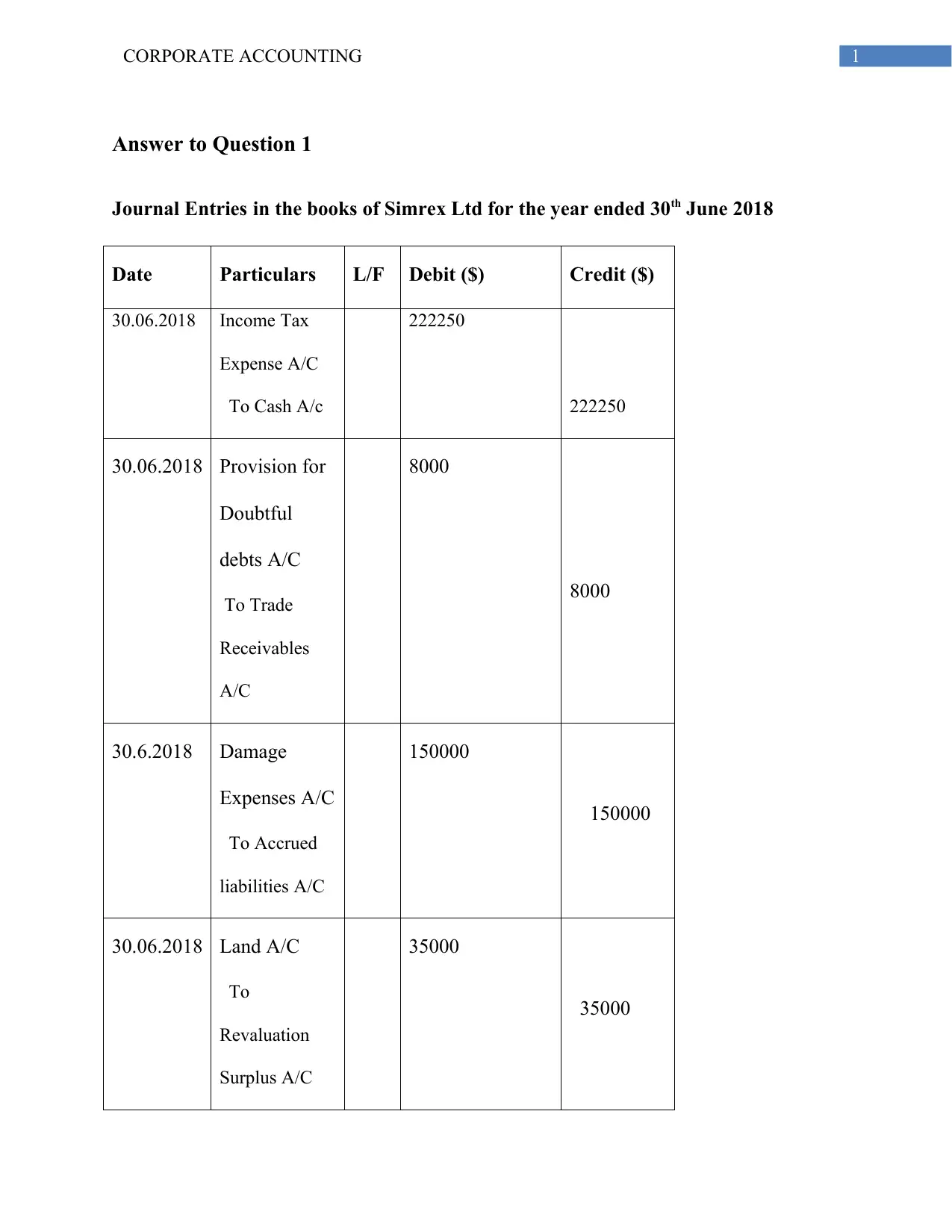

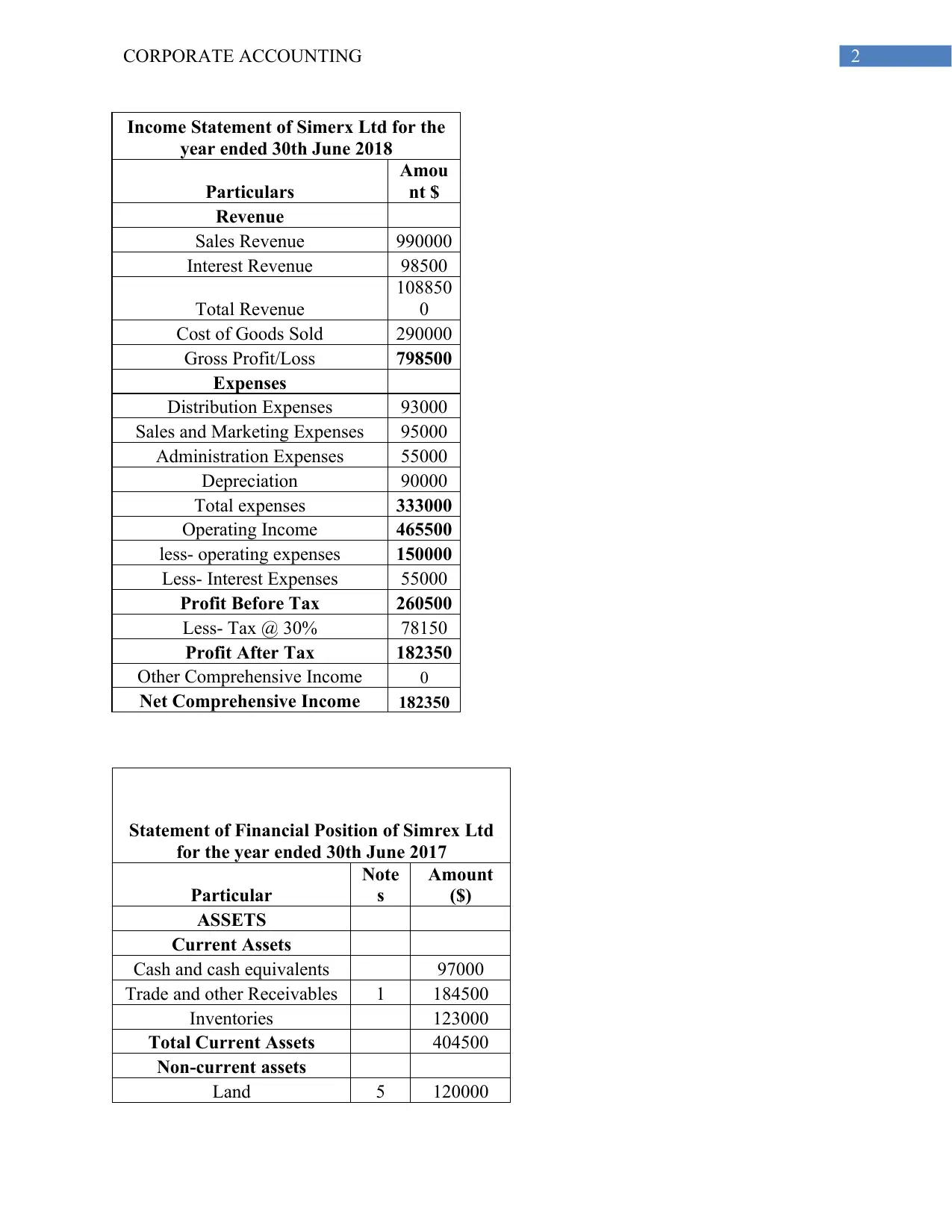

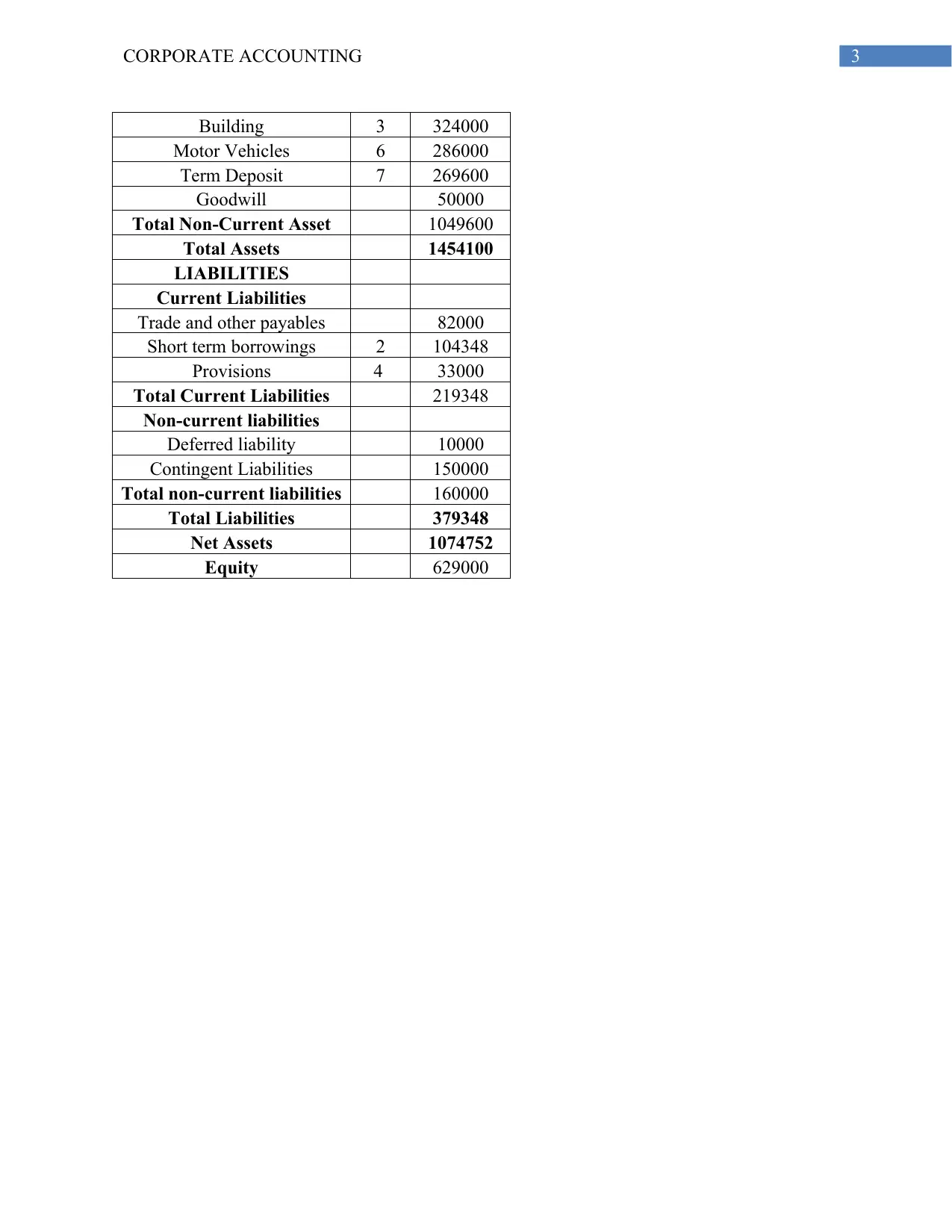

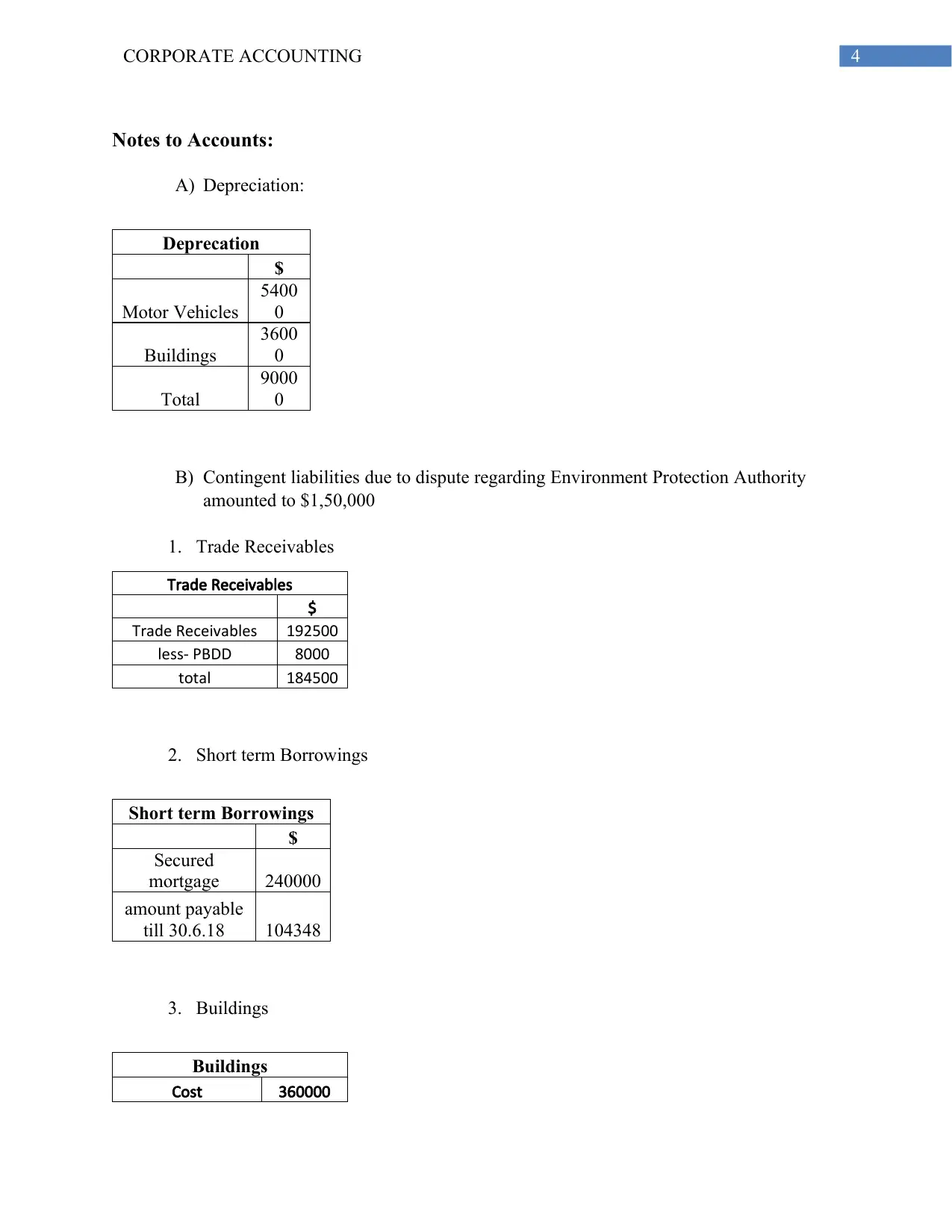

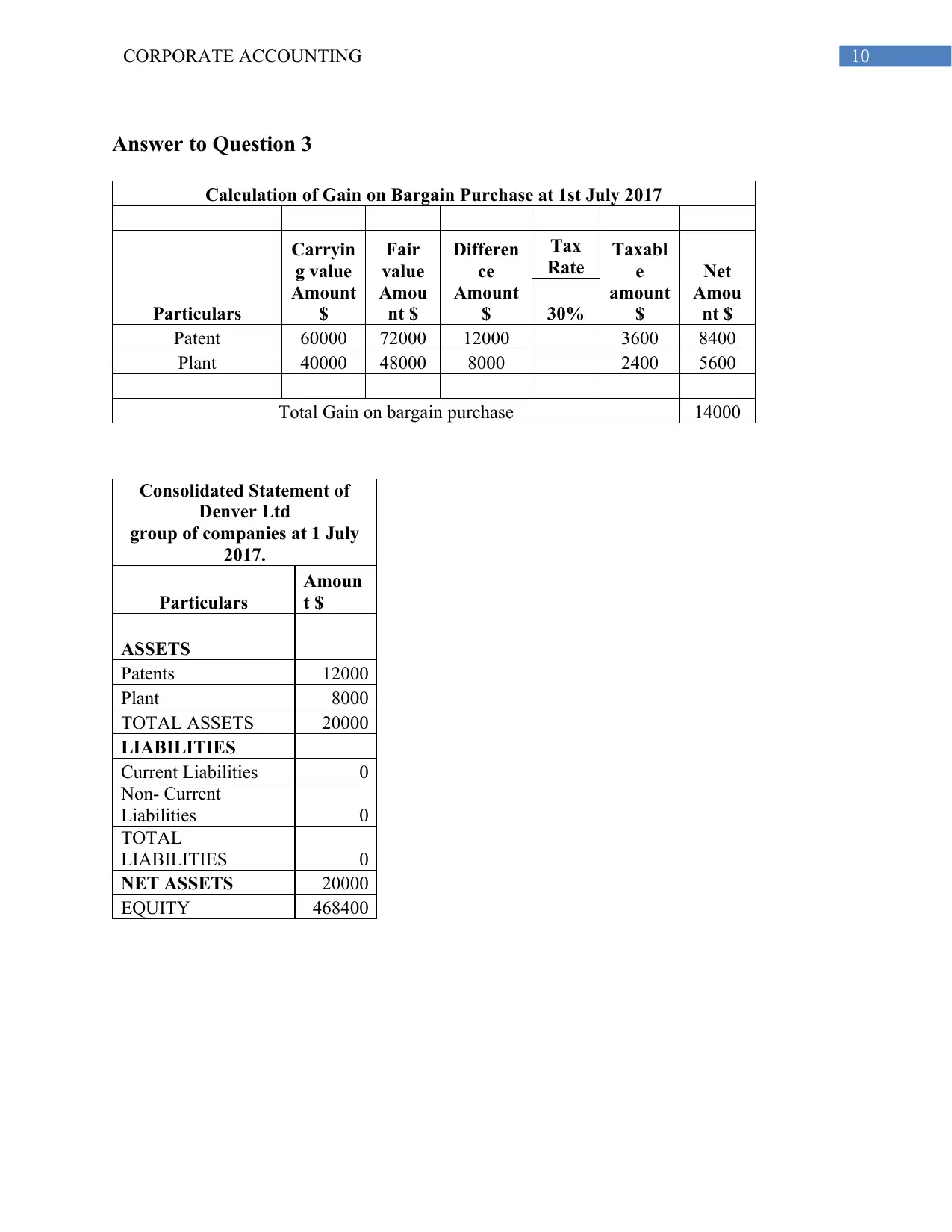

This assignment solution provides a detailed analysis of corporate accounting principles. It includes journal entries for various transactions, an income statement, a statement of financial position, and notes to the accounts. The solution also covers tax calculations, including taxable income and deferred tax liabilities, and demonstrates the application of accounting standards like AASB. Furthermore, the assignment delves into corporate social responsibility (CSR), discussing its benefits and the importance of sustainability reporting, using Pental Ltd as a case study. The document concludes with relevant references to support the analysis and findings. The assignment demonstrates a strong understanding of financial reporting, taxation, and CSR, offering a comprehensive view of corporate accounting practices.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.