ACCT7104 Case Study: Analysis of ONYA Ltd Acquisition of Remit

VerifiedAdded on 2022/12/30

|15

|2775

|77

Case Study

AI Summary

This case study analyzes the acquisition of Remit Pty Ltd by ONYA Ltd, focusing on the financial and accounting implications of the transaction. It examines the calculation of goodwill, the treatment of intangible assets (customer relationships, commercialized software, and brand name), and the preparation of consolidated financial statements. The analysis references relevant accounting standards issued by the AASB, specifically AASB 3 and AASB 138, to ensure proper accounting for the acquisition. The case study provides a detailed breakdown of the acquisition analysis, including the identification of identifiable assets and liabilities, and the subsequent impact on ONYA Ltd's financial position. It also offers recommendations for a smooth implementation of the acquisition process, considering the significant premium paid over Remit's net asset value. The study concludes with a report to the CFO and addresses the valuation of goodwill and intangible assets. The case study also emphasizes the importance of disclosures to ensure the reliability of financial information.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Author Note

Corporate Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Abstract

This document contains an analysis of the acquisition of Remit Pty by the ONYA group. It

includes the calculation of the amount of goodwill arising from the acquisition and the treatment

of the intangible assets arising from the same. This is done with reference to the relevant

accounting standards issued by the AASB and also by referring to various sources of literature.

The knowledge acquired is used in knowing the impact of the acquisition on the acquiring

company. A consolidated financial statement of the company after acquisition is prepared to

make the users understand the impact of the acquisition on the company. It ends with providing a

set of recommendations to be followed by the company in implementing the acquisition process

in a smooth manner.

Abstract

This document contains an analysis of the acquisition of Remit Pty by the ONYA group. It

includes the calculation of the amount of goodwill arising from the acquisition and the treatment

of the intangible assets arising from the same. This is done with reference to the relevant

accounting standards issued by the AASB and also by referring to various sources of literature.

The knowledge acquired is used in knowing the impact of the acquisition on the acquiring

company. A consolidated financial statement of the company after acquisition is prepared to

make the users understand the impact of the acquisition on the company. It ends with providing a

set of recommendations to be followed by the company in implementing the acquisition process

in a smooth manner.

2CORPORATE ACCOUNTING

Table of Contents

Introduction..................................................................................................................................2

Acquisition Analysis....................................................................................................................2

Treatment of Intangible Assets acquired by ONYA Ltd.............................................................5

Consolidated Financial Statements of ONYA Group..................................................................6

Report to the CFO........................................................................................................................8

Recommendations........................................................................................................................9

References..................................................................................................................................10

Appendix....................................................................................................................................11

Table of Contents

Introduction..................................................................................................................................2

Acquisition Analysis....................................................................................................................2

Treatment of Intangible Assets acquired by ONYA Ltd.............................................................5

Consolidated Financial Statements of ONYA Group..................................................................6

Report to the CFO........................................................................................................................8

Recommendations........................................................................................................................9

References..................................................................................................................................10

Appendix....................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction

According to paragraph 3 of AASB 3 that deals with business combinations, the company

acquiring the business of another company acquires the assets and liabilities of another business

that constitute the entire business. If the assets do not constitute the complete business, then it

will be considered only to be an asset acquisition (AASB 2014). In the given situation, ONYA

Ltd. is the acquiring company and it is acquiring the business of Remit Pty Ltd for a purchase

consideration of $120 million cash. However, the value of the net assets of the company is much

less than this and is valued at $8.2 million. The CFO of ONYA Ltd., Wendy Patton suggested

that Remit has a large amount of intangible assets and hence the amount being paid by ONYA

Ltd. is justified as it would allow ONYA Ltd. to access major markets that would be extremely

helpful to the company (AASB 2014).

Acquisition Analysis

In a business acquisition, goodwill is defined as an intangible asset that cannot directly be

identified with a particular business but is helpful in identifying the overall value of the business.

According to paragraph 10 of AASB 3, the acquirer company shall recognise the identifiable

assets and liabilities of the acquiring company, separately from the goodwill and any non-

controlling interest in the acquiree company. In order to meet the definition of identifiable assets

and liabilities, the assets and liabilities should meet their definitions as mentioned in AASB 1048

(Standard 2015). The paragraph 18 of AASB 3 suggests that the measurement of these assets

and liabilities should take place at their acquisition date fair values. To measure the amount of

goodwill arising from a particular transaction, the paragraph 32 of AASB 3 suggests that an

acquirer can recognise goodwill from an acquisition only if the consideration transferred by the

acquirer on the date of acquisition exceeds the net of the acquisition-date amounts of the

Introduction

According to paragraph 3 of AASB 3 that deals with business combinations, the company

acquiring the business of another company acquires the assets and liabilities of another business

that constitute the entire business. If the assets do not constitute the complete business, then it

will be considered only to be an asset acquisition (AASB 2014). In the given situation, ONYA

Ltd. is the acquiring company and it is acquiring the business of Remit Pty Ltd for a purchase

consideration of $120 million cash. However, the value of the net assets of the company is much

less than this and is valued at $8.2 million. The CFO of ONYA Ltd., Wendy Patton suggested

that Remit has a large amount of intangible assets and hence the amount being paid by ONYA

Ltd. is justified as it would allow ONYA Ltd. to access major markets that would be extremely

helpful to the company (AASB 2014).

Acquisition Analysis

In a business acquisition, goodwill is defined as an intangible asset that cannot directly be

identified with a particular business but is helpful in identifying the overall value of the business.

According to paragraph 10 of AASB 3, the acquirer company shall recognise the identifiable

assets and liabilities of the acquiring company, separately from the goodwill and any non-

controlling interest in the acquiree company. In order to meet the definition of identifiable assets

and liabilities, the assets and liabilities should meet their definitions as mentioned in AASB 1048

(Standard 2015). The paragraph 18 of AASB 3 suggests that the measurement of these assets

and liabilities should take place at their acquisition date fair values. To measure the amount of

goodwill arising from a particular transaction, the paragraph 32 of AASB 3 suggests that an

acquirer can recognise goodwill from an acquisition only if the consideration transferred by the

acquirer on the date of acquisition exceeds the net of the acquisition-date amounts of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

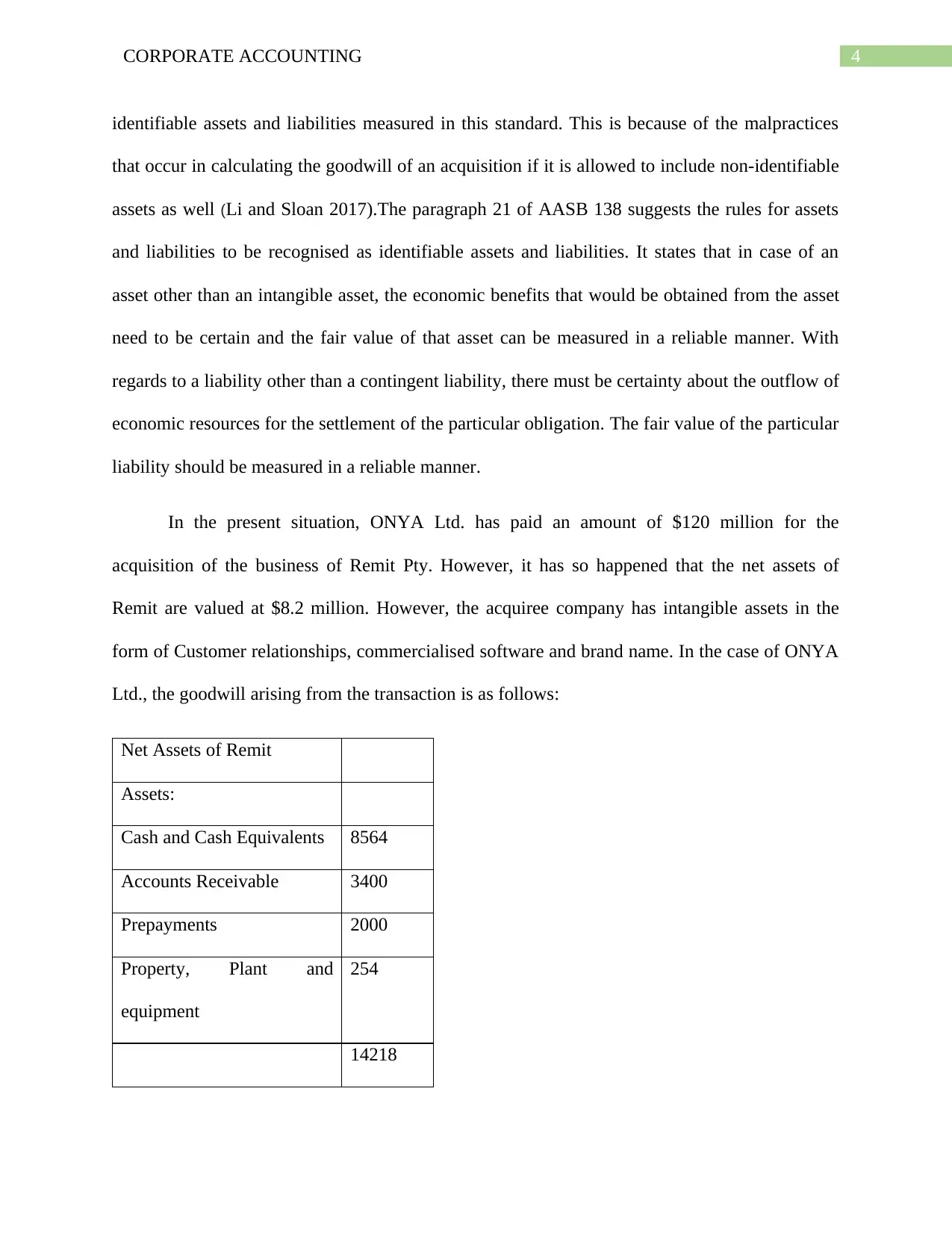

identifiable assets and liabilities measured in this standard. This is because of the malpractices

that occur in calculating the goodwill of an acquisition if it is allowed to include non-identifiable

assets as well (Li and Sloan 2017).The paragraph 21 of AASB 138 suggests the rules for assets

and liabilities to be recognised as identifiable assets and liabilities. It states that in case of an

asset other than an intangible asset, the economic benefits that would be obtained from the asset

need to be certain and the fair value of that asset can be measured in a reliable manner. With

regards to a liability other than a contingent liability, there must be certainty about the outflow of

economic resources for the settlement of the particular obligation. The fair value of the particular

liability should be measured in a reliable manner.

In the present situation, ONYA Ltd. has paid an amount of $120 million for the

acquisition of the business of Remit Pty. However, it has so happened that the net assets of

Remit are valued at $8.2 million. However, the acquiree company has intangible assets in the

form of Customer relationships, commercialised software and brand name. In the case of ONYA

Ltd., the goodwill arising from the transaction is as follows:

Net Assets of Remit

Assets:

Cash and Cash Equivalents 8564

Accounts Receivable 3400

Prepayments 2000

Property, Plant and

equipment

254

14218

identifiable assets and liabilities measured in this standard. This is because of the malpractices

that occur in calculating the goodwill of an acquisition if it is allowed to include non-identifiable

assets as well (Li and Sloan 2017).The paragraph 21 of AASB 138 suggests the rules for assets

and liabilities to be recognised as identifiable assets and liabilities. It states that in case of an

asset other than an intangible asset, the economic benefits that would be obtained from the asset

need to be certain and the fair value of that asset can be measured in a reliable manner. With

regards to a liability other than a contingent liability, there must be certainty about the outflow of

economic resources for the settlement of the particular obligation. The fair value of the particular

liability should be measured in a reliable manner.

In the present situation, ONYA Ltd. has paid an amount of $120 million for the

acquisition of the business of Remit Pty. However, it has so happened that the net assets of

Remit are valued at $8.2 million. However, the acquiree company has intangible assets in the

form of Customer relationships, commercialised software and brand name. In the case of ONYA

Ltd., the goodwill arising from the transaction is as follows:

Net Assets of Remit

Assets:

Cash and Cash Equivalents 8564

Accounts Receivable 3400

Prepayments 2000

Property, Plant and

equipment

254

14218

5CORPORATE ACCOUNTING

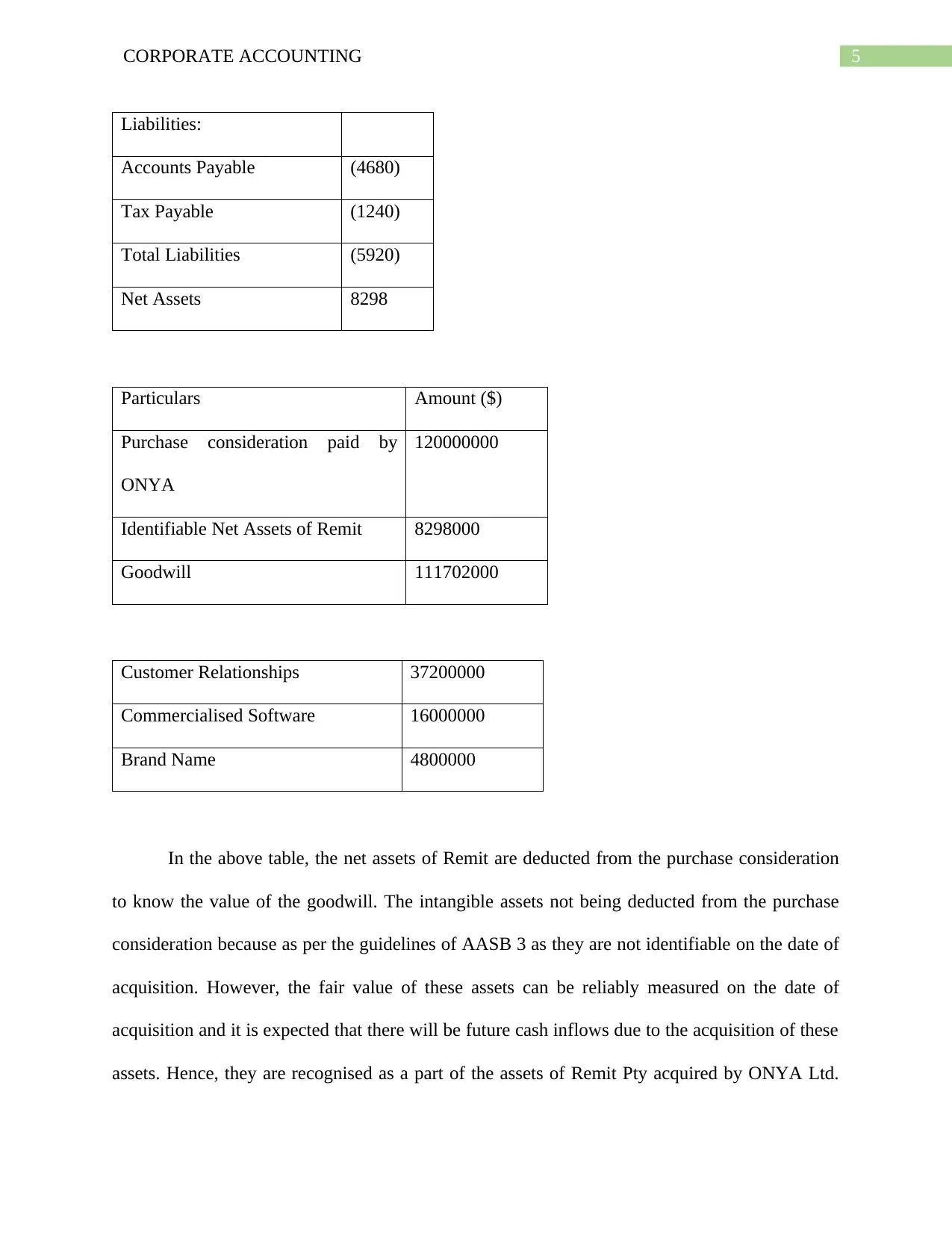

Liabilities:

Accounts Payable (4680)

Tax Payable (1240)

Total Liabilities (5920)

Net Assets 8298

Particulars Amount ($)

Purchase consideration paid by

ONYA

120000000

Identifiable Net Assets of Remit 8298000

Goodwill 111702000

Customer Relationships 37200000

Commercialised Software 16000000

Brand Name 4800000

In the above table, the net assets of Remit are deducted from the purchase consideration

to know the value of the goodwill. The intangible assets not being deducted from the purchase

consideration because as per the guidelines of AASB 3 as they are not identifiable on the date of

acquisition. However, the fair value of these assets can be reliably measured on the date of

acquisition and it is expected that there will be future cash inflows due to the acquisition of these

assets. Hence, they are recognised as a part of the assets of Remit Pty acquired by ONYA Ltd.

Liabilities:

Accounts Payable (4680)

Tax Payable (1240)

Total Liabilities (5920)

Net Assets 8298

Particulars Amount ($)

Purchase consideration paid by

ONYA

120000000

Identifiable Net Assets of Remit 8298000

Goodwill 111702000

Customer Relationships 37200000

Commercialised Software 16000000

Brand Name 4800000

In the above table, the net assets of Remit are deducted from the purchase consideration

to know the value of the goodwill. The intangible assets not being deducted from the purchase

consideration because as per the guidelines of AASB 3 as they are not identifiable on the date of

acquisition. However, the fair value of these assets can be reliably measured on the date of

acquisition and it is expected that there will be future cash inflows due to the acquisition of these

assets. Hence, they are recognised as a part of the assets of Remit Pty acquired by ONYA Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

Hence, the goodwill arising from the acquisition of the business is valued at $1117020000. The

total intangible assets of Remit Pty excluding the goodwill are arrived at $58000000.

Treatment of Intangible Assets acquired by ONYA Ltd.

As per the guidelines of AASB 3, if an intangible asset is acquired as a part of a business

combination then the assets are to be recognised at their fair value on the date of acquisition in

the books of accounts. This is also treated as the cost of the assets. This fair value is an indicator

of the acquirer’s expectations about the future economic benefits that will be received from the

acquisition of these assets. This standard also suggests that an acquiree shall recognise an

intangible asset arising from a business combination without considering whether these assets

were recognised at the time of acquiring the business or not. The AASB 112 suggests that the

income tax liability existing in the books of the acquiree becomes the tax liability of the

acquiring company (AASB 2013). In case of subsequent treatment of the intangible assets, there

are two methods that are allowed by AASB 138. They are the cost method and the revaluation

method. As per paragraph 74 of AASB 138, after recognising these particular intangible assets,

they are carried forward in the future books of accounts at cost less any accumulated

depreciation or amortisation or impairment losses arising on these particular assets. As stated in

paragraph 75 of AASB 138, the revaluation model is another method of recognising the value of

the intangible assets. This model suggests that after the process of initial recognition, an asset

shall be carried forward at any revalued amount, which is the fair value of the assets less

amortisation expenses, accumulated depreciation and subsequent impairment losses (Hu, Percy

and Yao 2015). In this case, fair value of an asset is measured by referring to the value of an

asset in an active market. However, the revaluations made in the value of the asset shall be done

on a regular basis so that the revalued amount does not significantly differ from the fair value of

Hence, the goodwill arising from the acquisition of the business is valued at $1117020000. The

total intangible assets of Remit Pty excluding the goodwill are arrived at $58000000.

Treatment of Intangible Assets acquired by ONYA Ltd.

As per the guidelines of AASB 3, if an intangible asset is acquired as a part of a business

combination then the assets are to be recognised at their fair value on the date of acquisition in

the books of accounts. This is also treated as the cost of the assets. This fair value is an indicator

of the acquirer’s expectations about the future economic benefits that will be received from the

acquisition of these assets. This standard also suggests that an acquiree shall recognise an

intangible asset arising from a business combination without considering whether these assets

were recognised at the time of acquiring the business or not. The AASB 112 suggests that the

income tax liability existing in the books of the acquiree becomes the tax liability of the

acquiring company (AASB 2013). In case of subsequent treatment of the intangible assets, there

are two methods that are allowed by AASB 138. They are the cost method and the revaluation

method. As per paragraph 74 of AASB 138, after recognising these particular intangible assets,

they are carried forward in the future books of accounts at cost less any accumulated

depreciation or amortisation or impairment losses arising on these particular assets. As stated in

paragraph 75 of AASB 138, the revaluation model is another method of recognising the value of

the intangible assets. This model suggests that after the process of initial recognition, an asset

shall be carried forward at any revalued amount, which is the fair value of the assets less

amortisation expenses, accumulated depreciation and subsequent impairment losses (Hu, Percy

and Yao 2015). In this case, fair value of an asset is measured by referring to the value of an

asset in an active market. However, the revaluations made in the value of the asset shall be done

on a regular basis so that the revalued amount does not significantly differ from the fair value of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

the asset (Laing and Perrin 2014). While using the revaluation model, it is to be noted that the

intangible assets that were not previously recognised as assets shall not be revalued. This is also

the case with intangible assets that were identified at amounts other than their costs. In a

situation where only a part of an asset has been identified as an intangible asset because the asset

failed to meet the criteria for recognition until midway of the process, even then the revaluation

model is to be applied on the entire asset. While it is suggested that both the fair value method

and the acquisition method have their own set of benefits and limitations, the emphasis on

disclosures should be increased to ensure that the books of accounts show more reliable

information (Kaya 2013).

Consolidated Financial Statements of ONYA Group

The consolidated financial statements of ONYA Group on 1 January 2019, immediately

after acquiring Remit Pty are as follows:

Current Assets: $000

Cash and cash equivalents 151428

Trade and other receivables 32532

Inventories 432

Prepayments 2000

Total Current Assets 186392

Non-Current Assets

Receivables 4796

Equity accounted 15328

the asset (Laing and Perrin 2014). While using the revaluation model, it is to be noted that the

intangible assets that were not previously recognised as assets shall not be revalued. This is also

the case with intangible assets that were identified at amounts other than their costs. In a

situation where only a part of an asset has been identified as an intangible asset because the asset

failed to meet the criteria for recognition until midway of the process, even then the revaluation

model is to be applied on the entire asset. While it is suggested that both the fair value method

and the acquisition method have their own set of benefits and limitations, the emphasis on

disclosures should be increased to ensure that the books of accounts show more reliable

information (Kaya 2013).

Consolidated Financial Statements of ONYA Group

The consolidated financial statements of ONYA Group on 1 January 2019, immediately

after acquiring Remit Pty are as follows:

Current Assets: $000

Cash and cash equivalents 151428

Trade and other receivables 32532

Inventories 432

Prepayments 2000

Total Current Assets 186392

Non-Current Assets

Receivables 4796

Equity accounted 15328

8CORPORATE ACCOUNTING

investments

Property, Plant and

equipment (Net)

37806

Intangible assets 114030644

Total Non-current assets 114088574

Total Assets 114274966

Current Liabilities:

Trade and other payables 44056

Borrowings 976

Unearned revenue 104688

Provisions 26442

Tax Payable 1240

Total Current Liabilities 177402

Non-Current Liabilities:

Borrowings 1002900

Provisions 26442

Total Non-Current

Liabilities

1029342

Total Liabilities 1206744

Net Assets 113068222

investments

Property, Plant and

equipment (Net)

37806

Intangible assets 114030644

Total Non-current assets 114088574

Total Assets 114274966

Current Liabilities:

Trade and other payables 44056

Borrowings 976

Unearned revenue 104688

Provisions 26442

Tax Payable 1240

Total Current Liabilities 177402

Non-Current Liabilities:

Borrowings 1002900

Provisions 26442

Total Non-Current

Liabilities

1029342

Total Liabilities 1206744

Net Assets 113068222

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Report to the CFO

It has been identified that mergers and acquisitions when done appropriately have a

positive impact on the companies undertaking them (Stiebale 2016). From the analysis of the

acquisition of Remit Pty by ONYA Ltd., it can be suggested that the acquisition is an extremely

costly procedure for ONYA Ltd. This is because even though the value of the net assets of the

company is only $8.2 million, the company is paying an amount of $120 million for acquiring

the same. This is over $112 million on the value of the assets of the company. Even if the

intangible assets worth $58 million are taken into consideration, the company is still paying an

additional amount of $54 million over the net assets of the company. This is because of the

value created by the investment made in acquiring the company (Kliestik et al. 2018). Due to this

acquisition by ONYA Ltd., the total current assets of the company have gone up by $13964000.

There has been an increase in the non-current assets by $254000. The intangible assets in the

form of customer relationships, commercialised software and brand name of Remit have together

contributed an amount of $58000000 to the intangible assets of the company. This also enables

the company to use the expertise and customer base of Remit for its own benefit. The amount of

goodwill other than these intangible assets has been paid by the company as it is expected that

the acquisition will be beneficial to the company. The current liabilities of the company will go

up by $5920000 while the non-current or long term liabilities of the company will remain

unchanged. There will be an increase in the overall net asset value of the company. Due to this

acquisition, the company does not suffer from any additional obligations in the long run.

However, it will have to meet the short term liabilities and will have to find the required cash to

do the same.

Report to the CFO

It has been identified that mergers and acquisitions when done appropriately have a

positive impact on the companies undertaking them (Stiebale 2016). From the analysis of the

acquisition of Remit Pty by ONYA Ltd., it can be suggested that the acquisition is an extremely

costly procedure for ONYA Ltd. This is because even though the value of the net assets of the

company is only $8.2 million, the company is paying an amount of $120 million for acquiring

the same. This is over $112 million on the value of the assets of the company. Even if the

intangible assets worth $58 million are taken into consideration, the company is still paying an

additional amount of $54 million over the net assets of the company. This is because of the

value created by the investment made in acquiring the company (Kliestik et al. 2018). Due to this

acquisition by ONYA Ltd., the total current assets of the company have gone up by $13964000.

There has been an increase in the non-current assets by $254000. The intangible assets in the

form of customer relationships, commercialised software and brand name of Remit have together

contributed an amount of $58000000 to the intangible assets of the company. This also enables

the company to use the expertise and customer base of Remit for its own benefit. The amount of

goodwill other than these intangible assets has been paid by the company as it is expected that

the acquisition will be beneficial to the company. The current liabilities of the company will go

up by $5920000 while the non-current or long term liabilities of the company will remain

unchanged. There will be an increase in the overall net asset value of the company. Due to this

acquisition, the company does not suffer from any additional obligations in the long run.

However, it will have to meet the short term liabilities and will have to find the required cash to

do the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Recommendations

From the above discussion, it is clear that ONYA Ltd. is acquiring Remit Pty for a

consideration of $120 million that is much higher than the value of the net assets shown in the

books of accounts. The accounting for the entire acquisition should be done using the relevant

accounting standards suggested by the Australian Accounting Standards Board (AASB).

According to the guidelines of AASB 3, at the time of acquisition of the new business, it is

important for ONYA Ltd. to calculate all the identifiable assets and liabilities available in the

books of acquiree on the date of acquisition. They are to be deducted from the purchase

consideration paid by ONYA to arrive at the amount of goodwill. Other intangible assets arising

from the acquisition should not be included in the calculation of goodwill due to their uncertain

nature. As per the guidelines of AASB 138, intangible assets arising from a business

combination should initially be recognised at the fair value in the consolidated financial

statements prepared immediately after acquisition and further carried forward at cost less

deductible expenses or at revalued amounts of the assets. It also states that the intangible assets

or liabilities should be recognised only if the company is sure about the future economic inflows

or outflows occurring through them and their fair value can be reasonably measured on the date

of acquisition of the business. In this situation, the acquiring company is paying a total amount of

$58000000 for acquiring the intangible assets owned by Remit. In accordance with the principles

of AASB 112 dealing with Income Taxes, the income tax liability of the acquiree company shall

become a part of the tax liability of the acquiring company. AASB 138 further suggests that the

intangible assets that were acquired by the company as a part of the acquisition deal should be

recorded at their fair value and the assets that were not recorded at fair value cannot be treated

using the revaluation method of accounting.

Recommendations

From the above discussion, it is clear that ONYA Ltd. is acquiring Remit Pty for a

consideration of $120 million that is much higher than the value of the net assets shown in the

books of accounts. The accounting for the entire acquisition should be done using the relevant

accounting standards suggested by the Australian Accounting Standards Board (AASB).

According to the guidelines of AASB 3, at the time of acquisition of the new business, it is

important for ONYA Ltd. to calculate all the identifiable assets and liabilities available in the

books of acquiree on the date of acquisition. They are to be deducted from the purchase

consideration paid by ONYA to arrive at the amount of goodwill. Other intangible assets arising

from the acquisition should not be included in the calculation of goodwill due to their uncertain

nature. As per the guidelines of AASB 138, intangible assets arising from a business

combination should initially be recognised at the fair value in the consolidated financial

statements prepared immediately after acquisition and further carried forward at cost less

deductible expenses or at revalued amounts of the assets. It also states that the intangible assets

or liabilities should be recognised only if the company is sure about the future economic inflows

or outflows occurring through them and their fair value can be reasonably measured on the date

of acquisition of the business. In this situation, the acquiring company is paying a total amount of

$58000000 for acquiring the intangible assets owned by Remit. In accordance with the principles

of AASB 112 dealing with Income Taxes, the income tax liability of the acquiree company shall

become a part of the tax liability of the acquiring company. AASB 138 further suggests that the

intangible assets that were acquired by the company as a part of the acquisition deal should be

recorded at their fair value and the assets that were not recorded at fair value cannot be treated

using the revaluation method of accounting.

11CORPORATE ACCOUNTING

References

AASB, C.A.S., 2013. Events after the Reporting Period.

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

AASB, C.A.S., 2014. Financial Instruments. Project Summary.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Kaya, C.T., 2013. Fair Value versus Historical Cost: which is actually more" Fair"?. Journal of

Accounting & Finance, (60).

Kliestik, T., Kovacova, M., Podhorska, I. and Kliestikova, J., 2018. Searching for key sources of

goodwill creation as new global managerial challenge. Polish Journal of Management

Studies, 17.

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116 non-

current asset measurement models. International Journal of Critical Accounting, 6(5/6), pp.509-

519.

Li, K.K. and Sloan, R.G., 2017. Has goodwill accounting gone bad?. Review of Accounting

Studies, 22(2), pp.964-1003.

Standard, I.A., 2015. Presentation of Financial Statements. Balance Sheet, 54, p.80A.

Stiebale, J., 2016. Cross-border M&As and innovative activity of acquiring and target

firms. Journal of International Economics, 99, pp.1-15.

References

AASB, C.A.S., 2013. Events after the Reporting Period.

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

AASB, C.A.S., 2014. Financial Instruments. Project Summary.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Kaya, C.T., 2013. Fair Value versus Historical Cost: which is actually more" Fair"?. Journal of

Accounting & Finance, (60).

Kliestik, T., Kovacova, M., Podhorska, I. and Kliestikova, J., 2018. Searching for key sources of

goodwill creation as new global managerial challenge. Polish Journal of Management

Studies, 17.

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116 non-

current asset measurement models. International Journal of Critical Accounting, 6(5/6), pp.509-

519.

Li, K.K. and Sloan, R.G., 2017. Has goodwill accounting gone bad?. Review of Accounting

Studies, 22(2), pp.964-1003.

Standard, I.A., 2015. Presentation of Financial Statements. Balance Sheet, 54, p.80A.

Stiebale, J., 2016. Cross-border M&As and innovative activity of acquiring and target

firms. Journal of International Economics, 99, pp.1-15.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.