Preparing Consolidated Financial Statements for Erik Ltd's Group

VerifiedAdded on 2022/12/22

|10

|1388

|37

AI Summary

This document provides a step-by-step guide on how to prepare consolidated financial statements for Erik Ltd's group at 1 July 2017. It includes calculation analysis, consolidation journal entries, consolidated worksheet, and financial consolidated statement.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Student Name:

Student Number:

Authors Note:

Corporate Accounting

Student Name:

Student Number:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING

Table of Contents

1. Preparing the consolidated financial statements for Erik Ltd’s group at 1 July 2017...........2

Calculation analysis:..................................................................................................................2

Consolidation journal entries:....................................................................................................2

Consolidated worksheet:............................................................................................................3

Financial consolidated statement:..............................................................................................4

2. Preparing the consolidated worksheet entries for Erik Ltd’s group at 30 June 2018:...........5

3. Report on financial analysis and calculation:.........................................................................7

References and Bibliography:....................................................................................................9

Table of Contents

1. Preparing the consolidated financial statements for Erik Ltd’s group at 1 July 2017...........2

Calculation analysis:..................................................................................................................2

Consolidation journal entries:....................................................................................................2

Consolidated worksheet:............................................................................................................3

Financial consolidated statement:..............................................................................................4

2. Preparing the consolidated worksheet entries for Erik Ltd’s group at 30 June 2018:...........5

3. Report on financial analysis and calculation:.........................................................................7

References and Bibliography:....................................................................................................9

2CORPORATE ACCOUNTING

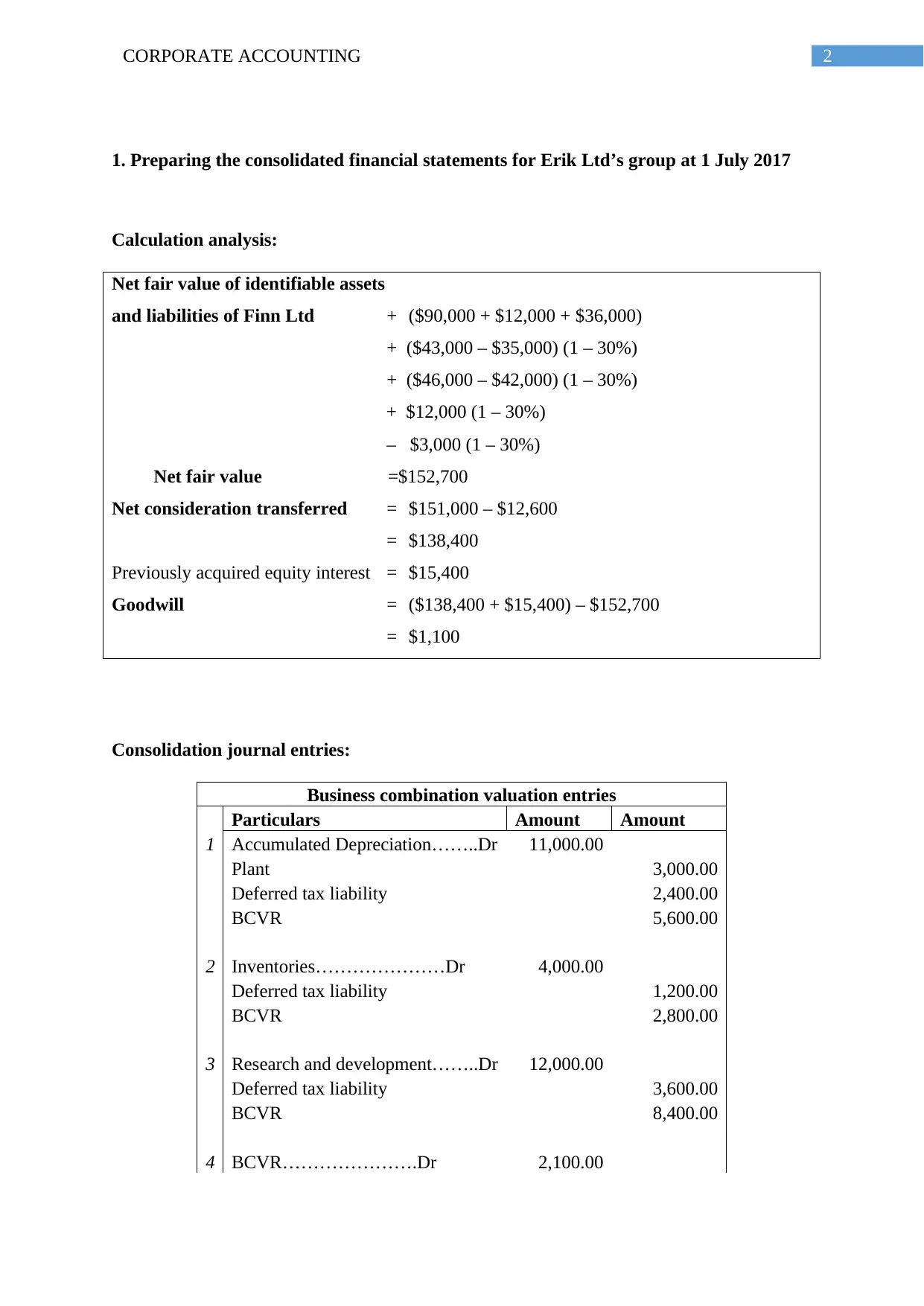

1. Preparing the consolidated financial statements for Erik Ltd’s group at 1 July 2017

Calculation analysis:

Net fair value of identifiable assets

and liabilities of Finn Ltd + ($90,000 + $12,000 + $36,000)

+ ($43,000 – $35,000) (1 – 30%)

+ ($46,000 – $42,000) (1 – 30%)

+ $12,000 (1 – 30%)

– $3,000 (1 – 30%)

Net fair value =$152,700

Net consideration transferred = $151,000 – $12,600

= $138,400

Previously acquired equity interest = $15,400

Goodwill = ($138,400 + $15,400) – $152,700

= $1,100

Consolidation journal entries:

Business combination valuation entries

Particulars Amount Amount

1 Accumulated Depreciation……..Dr 11,000.00

Plant 3,000.00

Deferred tax liability 2,400.00

BCVR 5,600.00

2 Inventories…………………Dr 4,000.00

Deferred tax liability 1,200.00

BCVR 2,800.00

3 Research and development……..Dr 12,000.00

Deferred tax liability 3,600.00

BCVR 8,400.00

4 BCVR………………….Dr 2,100.00

1. Preparing the consolidated financial statements for Erik Ltd’s group at 1 July 2017

Calculation analysis:

Net fair value of identifiable assets

and liabilities of Finn Ltd + ($90,000 + $12,000 + $36,000)

+ ($43,000 – $35,000) (1 – 30%)

+ ($46,000 – $42,000) (1 – 30%)

+ $12,000 (1 – 30%)

– $3,000 (1 – 30%)

Net fair value =$152,700

Net consideration transferred = $151,000 – $12,600

= $138,400

Previously acquired equity interest = $15,400

Goodwill = ($138,400 + $15,400) – $152,700

= $1,100

Consolidation journal entries:

Business combination valuation entries

Particulars Amount Amount

1 Accumulated Depreciation……..Dr 11,000.00

Plant 3,000.00

Deferred tax liability 2,400.00

BCVR 5,600.00

2 Inventories…………………Dr 4,000.00

Deferred tax liability 1,200.00

BCVR 2,800.00

3 Research and development……..Dr 12,000.00

Deferred tax liability 3,600.00

BCVR 8,400.00

4 BCVR………………….Dr 2,100.00

3CORPORATE ACCOUNTING

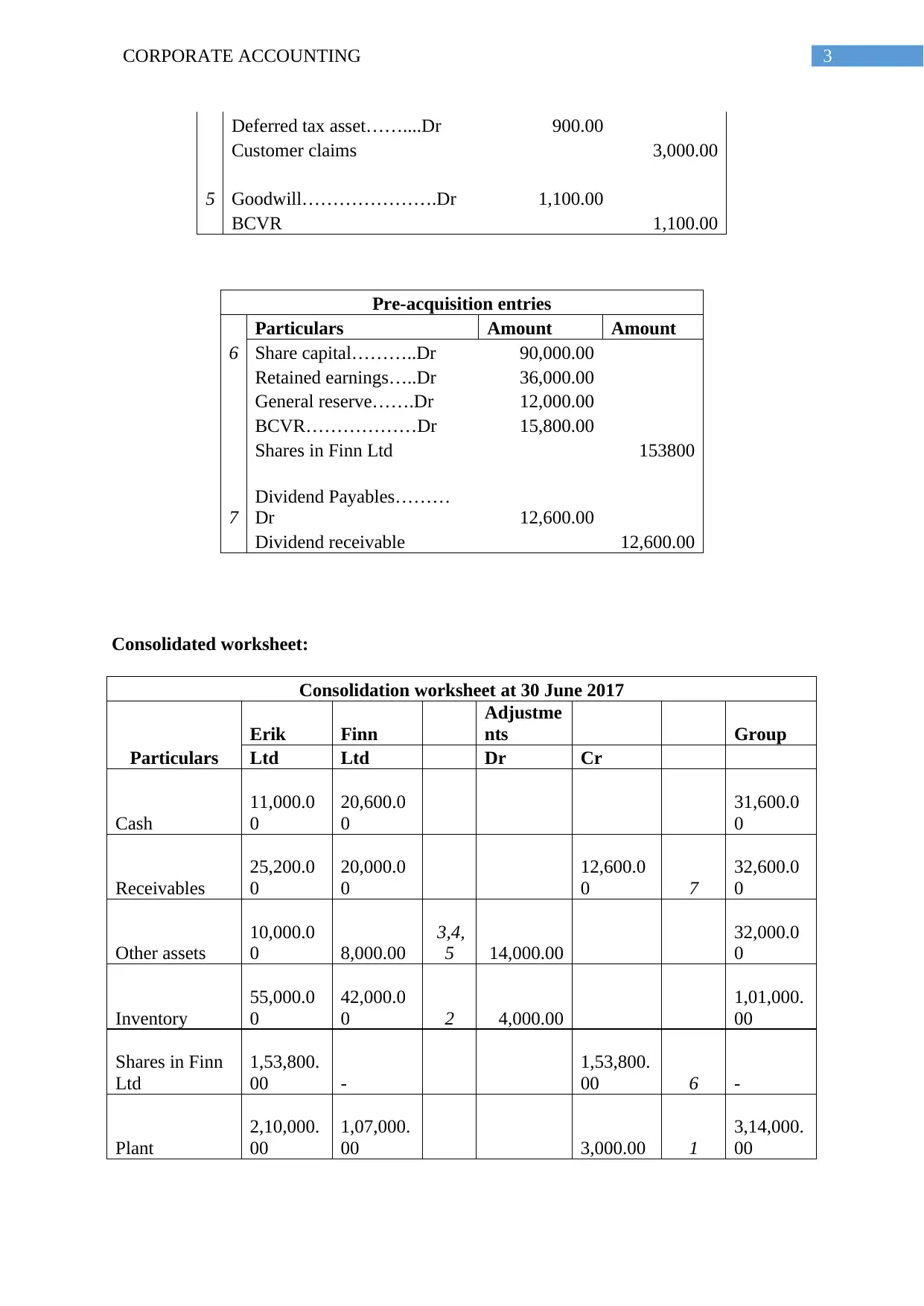

Deferred tax asset……....Dr 900.00

Customer claims 3,000.00

5 Goodwill………………….Dr 1,100.00

BCVR 1,100.00

Pre-acquisition entries

Particulars Amount Amount

6 Share capital………..Dr 90,000.00

Retained earnings…..Dr 36,000.00

General reserve…….Dr 12,000.00

BCVR………………Dr 15,800.00

Shares in Finn Ltd 153800

7

Dividend Payables………

Dr 12,600.00

Dividend receivable 12,600.00

Consolidated worksheet:

Consolidation worksheet at 30 June 2017

Particulars

Erik Finn

Adjustme

nts Group

Ltd Ltd Dr Cr

Cash

11,000.0

0

20,600.0

0

31,600.0

0

Receivables

25,200.0

0

20,000.0

0

12,600.0

0 7

32,600.0

0

Other assets

10,000.0

0 8,000.00

3,4,

5 14,000.00

32,000.0

0

Inventory

55,000.0

0

42,000.0

0 2 4,000.00

1,01,000.

00

Shares in Finn

Ltd

1,53,800.

00 -

1,53,800.

00 6 -

Plant

2,10,000.

00

1,07,000.

00 3,000.00 1

3,14,000.

00

Deferred tax asset……....Dr 900.00

Customer claims 3,000.00

5 Goodwill………………….Dr 1,100.00

BCVR 1,100.00

Pre-acquisition entries

Particulars Amount Amount

6 Share capital………..Dr 90,000.00

Retained earnings…..Dr 36,000.00

General reserve…….Dr 12,000.00

BCVR………………Dr 15,800.00

Shares in Finn Ltd 153800

7

Dividend Payables………

Dr 12,600.00

Dividend receivable 12,600.00

Consolidated worksheet:

Consolidation worksheet at 30 June 2017

Particulars

Erik Finn

Adjustme

nts Group

Ltd Ltd Dr Cr

Cash

11,000.0

0

20,600.0

0

31,600.0

0

Receivables

25,200.0

0

20,000.0

0

12,600.0

0 7

32,600.0

0

Other assets

10,000.0

0 8,000.00

3,4,

5 14,000.00

32,000.0

0

Inventory

55,000.0

0

42,000.0

0 2 4,000.00

1,01,000.

00

Shares in Finn

Ltd

1,53,800.

00 -

1,53,800.

00 6 -

Plant

2,10,000.

00

1,07,000.

00 3,000.00 1

3,14,000.

00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING

Accum

depreciation

-

85,000.0

0

-

22,000.0

0 1 11,000.00

-

96,000.0

0

3,80,000.

00

1,75,600.

00

4,15,200.

00

Dividend

payable

25,000.0

0

12,600.0

0 7 12,600.00

25,000.0

0

Other liabilities

75,000.0

0

25,000.0

0

10,200.0

0

1,1,2,

3

1,10,200.

00

Share capital

1,30,000.

00

90,000.0

0 90,000.00

1,30,000.

00

Retained

earnings

93,500.0

0

36,000.0

0 36,000.00

93,500.0

0

General reserve

56,500.0

0

12,000.0

0 12,000.00

56,500.0

0

BCVR - - 4,6 17,900.00

17,900.0

0

1,2,3,

5 -

3,80,000.

00

1,75,600.

00

4,15,200.

00

Financial consolidated statement:

Erik Ltd

Consolidated Statement of Financial Position as at 1 July 2017

Particulars Amount Amount

Current assets

Cash 31,600.00

Receivables 32,600.00

Inventory 1,01,000.00

Total current assets 1,65,200.00

Non-Current Assets

Other assets 32,000.00

Plant 3,14,000.00

Accum depreciation -96,000.00

Total non-current assets 2,50,000.00

Total Assets 4,15,200.00

Accum

depreciation

-

85,000.0

0

-

22,000.0

0 1 11,000.00

-

96,000.0

0

3,80,000.

00

1,75,600.

00

4,15,200.

00

Dividend

payable

25,000.0

0

12,600.0

0 7 12,600.00

25,000.0

0

Other liabilities

75,000.0

0

25,000.0

0

10,200.0

0

1,1,2,

3

1,10,200.

00

Share capital

1,30,000.

00

90,000.0

0 90,000.00

1,30,000.

00

Retained

earnings

93,500.0

0

36,000.0

0 36,000.00

93,500.0

0

General reserve

56,500.0

0

12,000.0

0 12,000.00

56,500.0

0

BCVR - - 4,6 17,900.00

17,900.0

0

1,2,3,

5 -

3,80,000.

00

1,75,600.

00

4,15,200.

00

Financial consolidated statement:

Erik Ltd

Consolidated Statement of Financial Position as at 1 July 2017

Particulars Amount Amount

Current assets

Cash 31,600.00

Receivables 32,600.00

Inventory 1,01,000.00

Total current assets 1,65,200.00

Non-Current Assets

Other assets 32,000.00

Plant 3,14,000.00

Accum depreciation -96,000.00

Total non-current assets 2,50,000.00

Total Assets 4,15,200.00

5CORPORATE ACCOUNTING

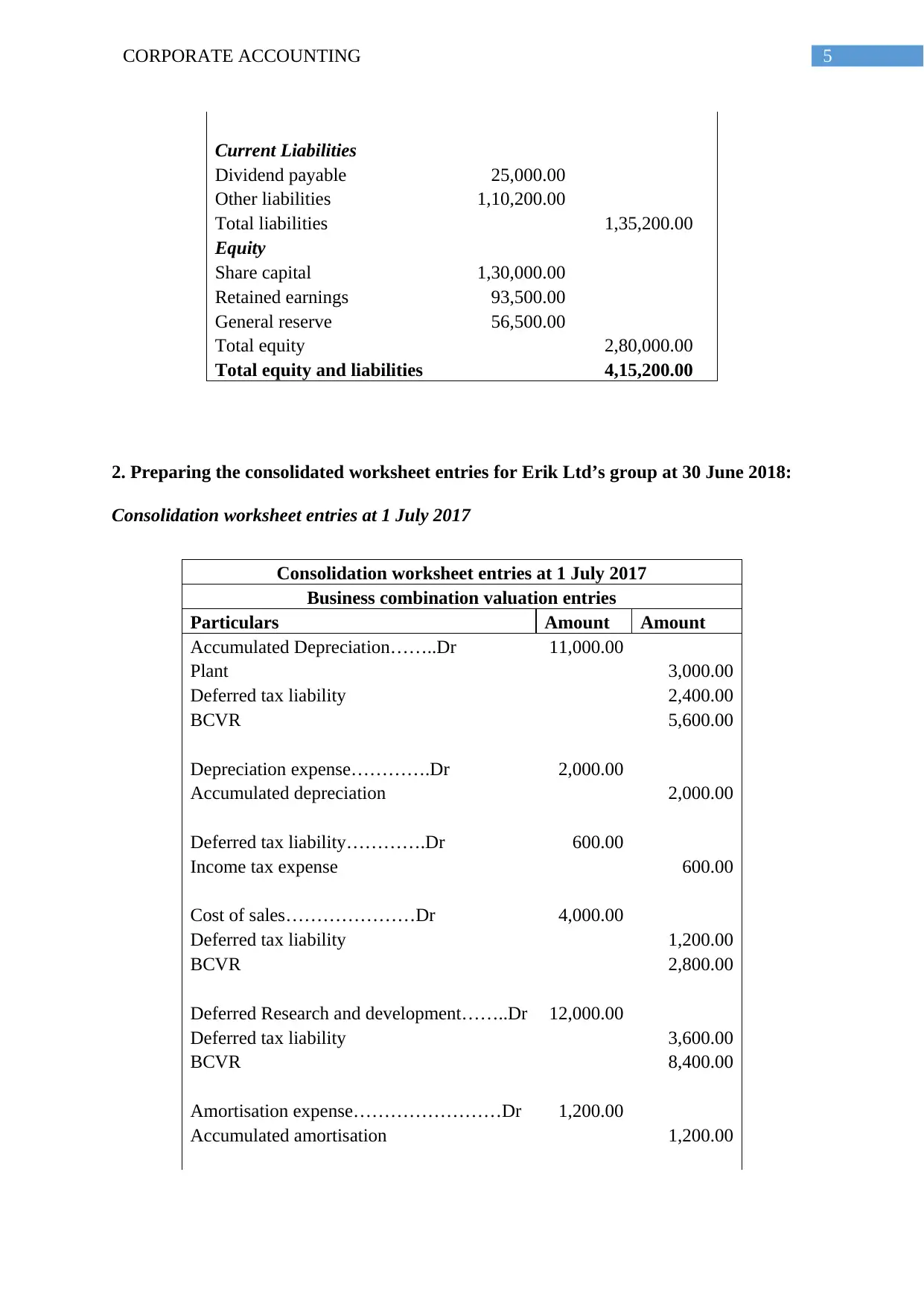

Current Liabilities

Dividend payable 25,000.00

Other liabilities 1,10,200.00

Total liabilities 1,35,200.00

Equity

Share capital 1,30,000.00

Retained earnings 93,500.00

General reserve 56,500.00

Total equity 2,80,000.00

Total equity and liabilities 4,15,200.00

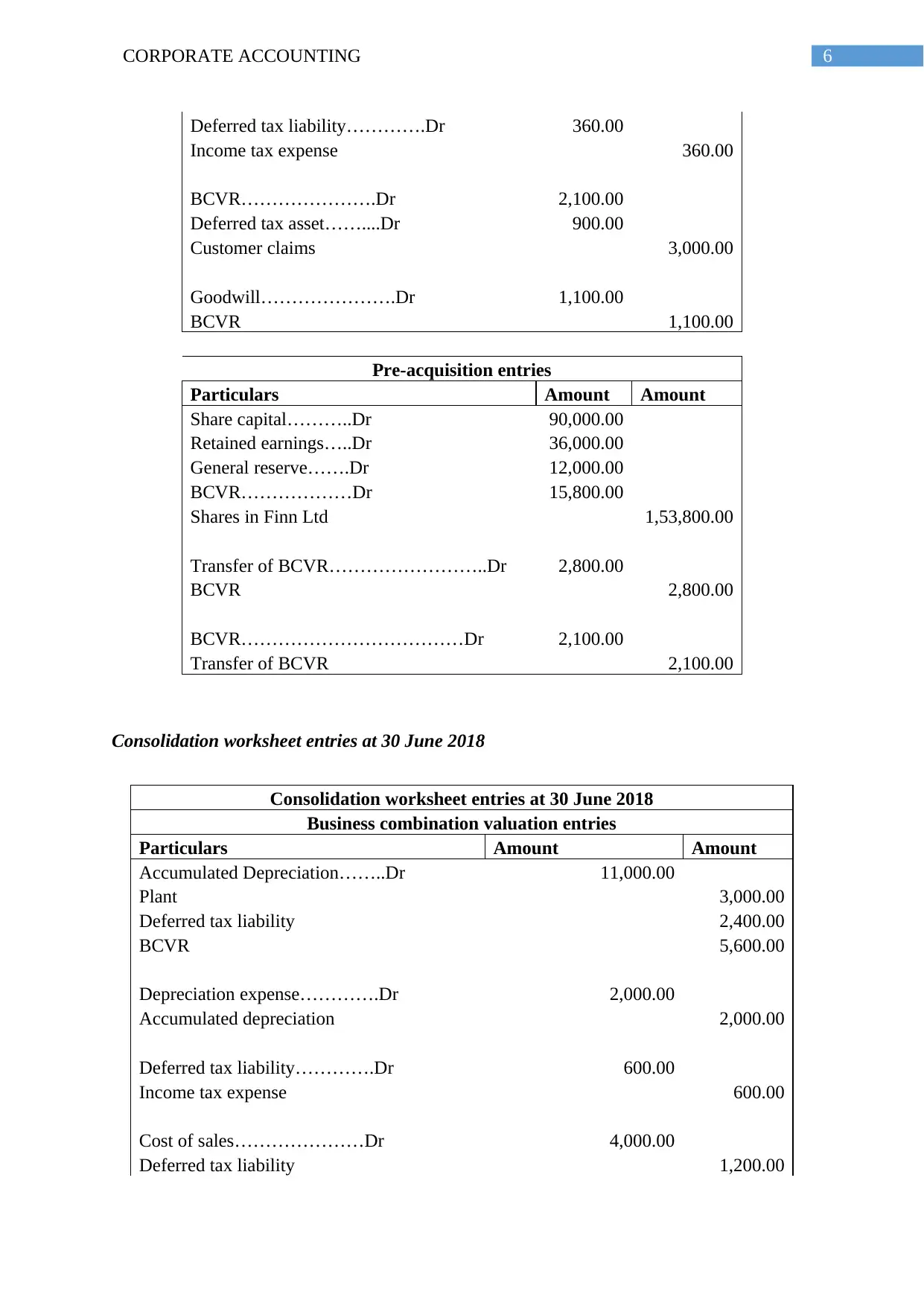

2. Preparing the consolidated worksheet entries for Erik Ltd’s group at 30 June 2018:

Consolidation worksheet entries at 1 July 2017

Consolidation worksheet entries at 1 July 2017

Business combination valuation entries

Particulars Amount Amount

Accumulated Depreciation……..Dr 11,000.00

Plant 3,000.00

Deferred tax liability 2,400.00

BCVR 5,600.00

Depreciation expense………….Dr 2,000.00

Accumulated depreciation 2,000.00

Deferred tax liability………….Dr 600.00

Income tax expense 600.00

Cost of sales…………………Dr 4,000.00

Deferred tax liability 1,200.00

BCVR 2,800.00

Deferred Research and development……..Dr 12,000.00

Deferred tax liability 3,600.00

BCVR 8,400.00

Amortisation expense……………………Dr 1,200.00

Accumulated amortisation 1,200.00

Current Liabilities

Dividend payable 25,000.00

Other liabilities 1,10,200.00

Total liabilities 1,35,200.00

Equity

Share capital 1,30,000.00

Retained earnings 93,500.00

General reserve 56,500.00

Total equity 2,80,000.00

Total equity and liabilities 4,15,200.00

2. Preparing the consolidated worksheet entries for Erik Ltd’s group at 30 June 2018:

Consolidation worksheet entries at 1 July 2017

Consolidation worksheet entries at 1 July 2017

Business combination valuation entries

Particulars Amount Amount

Accumulated Depreciation……..Dr 11,000.00

Plant 3,000.00

Deferred tax liability 2,400.00

BCVR 5,600.00

Depreciation expense………….Dr 2,000.00

Accumulated depreciation 2,000.00

Deferred tax liability………….Dr 600.00

Income tax expense 600.00

Cost of sales…………………Dr 4,000.00

Deferred tax liability 1,200.00

BCVR 2,800.00

Deferred Research and development……..Dr 12,000.00

Deferred tax liability 3,600.00

BCVR 8,400.00

Amortisation expense……………………Dr 1,200.00

Accumulated amortisation 1,200.00

6CORPORATE ACCOUNTING

Deferred tax liability………….Dr 360.00

Income tax expense 360.00

BCVR………………….Dr 2,100.00

Deferred tax asset……....Dr 900.00

Customer claims 3,000.00

Goodwill………………….Dr 1,100.00

BCVR 1,100.00

Pre-acquisition entries

Particulars Amount Amount

Share capital………..Dr 90,000.00

Retained earnings…..Dr 36,000.00

General reserve…….Dr 12,000.00

BCVR………………Dr 15,800.00

Shares in Finn Ltd 1,53,800.00

Transfer of BCVR……………………..Dr 2,800.00

BCVR 2,800.00

BCVR………………………………Dr 2,100.00

Transfer of BCVR 2,100.00

Consolidation worksheet entries at 30 June 2018

Consolidation worksheet entries at 30 June 2018

Business combination valuation entries

Particulars Amount Amount

Accumulated Depreciation……..Dr 11,000.00

Plant 3,000.00

Deferred tax liability 2,400.00

BCVR 5,600.00

Depreciation expense………….Dr 2,000.00

Accumulated depreciation 2,000.00

Deferred tax liability………….Dr 600.00

Income tax expense 600.00

Cost of sales…………………Dr 4,000.00

Deferred tax liability 1,200.00

Deferred tax liability………….Dr 360.00

Income tax expense 360.00

BCVR………………….Dr 2,100.00

Deferred tax asset……....Dr 900.00

Customer claims 3,000.00

Goodwill………………….Dr 1,100.00

BCVR 1,100.00

Pre-acquisition entries

Particulars Amount Amount

Share capital………..Dr 90,000.00

Retained earnings…..Dr 36,000.00

General reserve…….Dr 12,000.00

BCVR………………Dr 15,800.00

Shares in Finn Ltd 1,53,800.00

Transfer of BCVR……………………..Dr 2,800.00

BCVR 2,800.00

BCVR………………………………Dr 2,100.00

Transfer of BCVR 2,100.00

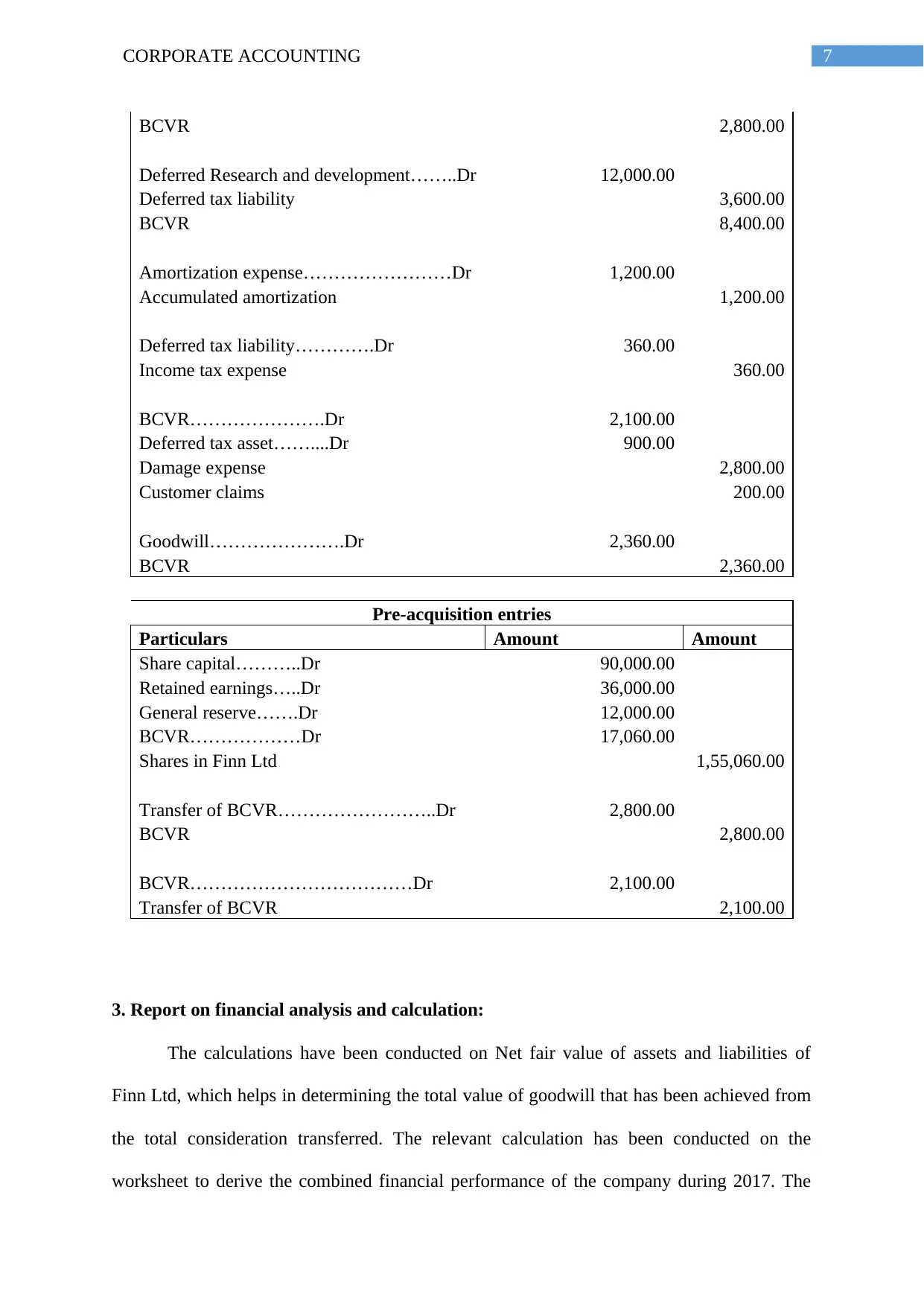

Consolidation worksheet entries at 30 June 2018

Consolidation worksheet entries at 30 June 2018

Business combination valuation entries

Particulars Amount Amount

Accumulated Depreciation……..Dr 11,000.00

Plant 3,000.00

Deferred tax liability 2,400.00

BCVR 5,600.00

Depreciation expense………….Dr 2,000.00

Accumulated depreciation 2,000.00

Deferred tax liability………….Dr 600.00

Income tax expense 600.00

Cost of sales…………………Dr 4,000.00

Deferred tax liability 1,200.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

BCVR 2,800.00

Deferred Research and development……..Dr 12,000.00

Deferred tax liability 3,600.00

BCVR 8,400.00

Amortization expense……………………Dr 1,200.00

Accumulated amortization 1,200.00

Deferred tax liability………….Dr 360.00

Income tax expense 360.00

BCVR………………….Dr 2,100.00

Deferred tax asset……....Dr 900.00

Damage expense 2,800.00

Customer claims 200.00

Goodwill………………….Dr 2,360.00

BCVR 2,360.00

Pre-acquisition entries

Particulars Amount Amount

Share capital………..Dr 90,000.00

Retained earnings…..Dr 36,000.00

General reserve…….Dr 12,000.00

BCVR………………Dr 17,060.00

Shares in Finn Ltd 1,55,060.00

Transfer of BCVR……………………..Dr 2,800.00

BCVR 2,800.00

BCVR………………………………Dr 2,100.00

Transfer of BCVR 2,100.00

3. Report on financial analysis and calculation:

The calculations have been conducted on Net fair value of assets and liabilities of

Finn Ltd, which helps in determining the total value of goodwill that has been achieved from

the total consideration transferred. The relevant calculation has been conducted on the

worksheet to derive the combined financial performance of the company during 2017. The

BCVR 2,800.00

Deferred Research and development……..Dr 12,000.00

Deferred tax liability 3,600.00

BCVR 8,400.00

Amortization expense……………………Dr 1,200.00

Accumulated amortization 1,200.00

Deferred tax liability………….Dr 360.00

Income tax expense 360.00

BCVR………………….Dr 2,100.00

Deferred tax asset……....Dr 900.00

Damage expense 2,800.00

Customer claims 200.00

Goodwill………………….Dr 2,360.00

BCVR 2,360.00

Pre-acquisition entries

Particulars Amount Amount

Share capital………..Dr 90,000.00

Retained earnings…..Dr 36,000.00

General reserve…….Dr 12,000.00

BCVR………………Dr 17,060.00

Shares in Finn Ltd 1,55,060.00

Transfer of BCVR……………………..Dr 2,800.00

BCVR 2,800.00

BCVR………………………………Dr 2,100.00

Transfer of BCVR 2,100.00

3. Report on financial analysis and calculation:

The calculations have been conducted on Net fair value of assets and liabilities of

Finn Ltd, which helps in determining the total value of goodwill that has been achieved from

the total consideration transferred. The relevant calculation has been conducted on the

worksheet to derive the combined financial performance of the company during 2017. The

8CORPORATE ACCOUNTING

relevant dividend declared by the subsidiary are adequately presented in the acquisition and

recognized entirely. The relevant entries of the BCVR activities which comprises of

depreciation of the plant during the current period, sale of the inventories during the current

period, amortization of the research and development during the current period, and

settlement of the contingent liability. Moreover, the Pre-acquisition entries mainly comprise

of where relevant Transfer from business-combination valuation reserve and business-

combination valuation reserve are mainly conducted to derive relevant values (Hoyle,

Schaefer and Doupnik 2015). The valuation would eventually help in determining the

goodwill values, which is at the levels of 2,360. The calculations have indicated that the

performance Erik Ltd has increased, where the assets has improved from 380,000 to 415,200.

This improvements indicates about the financial performance of the organization will

relevantly generate high level of income from the acquisition.

relevant dividend declared by the subsidiary are adequately presented in the acquisition and

recognized entirely. The relevant entries of the BCVR activities which comprises of

depreciation of the plant during the current period, sale of the inventories during the current

period, amortization of the research and development during the current period, and

settlement of the contingent liability. Moreover, the Pre-acquisition entries mainly comprise

of where relevant Transfer from business-combination valuation reserve and business-

combination valuation reserve are mainly conducted to derive relevant values (Hoyle,

Schaefer and Doupnik 2015). The valuation would eventually help in determining the

goodwill values, which is at the levels of 2,360. The calculations have indicated that the

performance Erik Ltd has increased, where the assets has improved from 380,000 to 415,200.

This improvements indicates about the financial performance of the organization will

relevantly generate high level of income from the acquisition.

9CORPORATE ACCOUNTING

References and Bibliography:

Dandago, K.I. and Rufai, A.S., 2014. Information technology and accounting information

system in the Nigerian banking industry. Asian Economic and Financial Review, 4(5),

pp.655-670.

Gillis, P., Petty, R. and Suddaby, R., 2014. The transnational regulation of accounting:

insights, gaps and an agenda for future research. Accounting, Auditing & Accountability

Journal, 27(6), pp.894-902.

Gillis, P., Petty, R., Suddaby, R. and Nobes, C., 2014. The development of national and

transnational regulation on the scope of consolidation. Accounting, auditing & accountability

journal.

Gray, S.J. ed., 2014. International accounting and transnational decisions. Butterworth-

Heinemann.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Leitner-Hanetseder, S. and Stockinger, M., 2014, March. How does the elimination of the

proportionate consolidation method for joint venture investments influence European

companies. In ACRN Proceedings in Finance and Risk Series 2013: Proceedings of the 13th

FRAP Conference in Cambridge (Vol. 2).

Raudla, R. and Tammel, K., 2015. Creating shared service centres for public sector

accounting. Accounting, Auditing & Accountability Journal, 28(2), pp.158-179.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

References and Bibliography:

Dandago, K.I. and Rufai, A.S., 2014. Information technology and accounting information

system in the Nigerian banking industry. Asian Economic and Financial Review, 4(5),

pp.655-670.

Gillis, P., Petty, R. and Suddaby, R., 2014. The transnational regulation of accounting:

insights, gaps and an agenda for future research. Accounting, Auditing & Accountability

Journal, 27(6), pp.894-902.

Gillis, P., Petty, R., Suddaby, R. and Nobes, C., 2014. The development of national and

transnational regulation on the scope of consolidation. Accounting, auditing & accountability

journal.

Gray, S.J. ed., 2014. International accounting and transnational decisions. Butterworth-

Heinemann.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Leitner-Hanetseder, S. and Stockinger, M., 2014, March. How does the elimination of the

proportionate consolidation method for joint venture investments influence European

companies. In ACRN Proceedings in Finance and Risk Series 2013: Proceedings of the 13th

FRAP Conference in Cambridge (Vol. 2).

Raudla, R. and Tammel, K., 2015. Creating shared service centres for public sector

accounting. Accounting, Auditing & Accountability Journal, 28(2), pp.158-179.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.