Dakota Office Products Case Study: Profitability Analysis and Costing

VerifiedAdded on 2022/08/13

|10

|1303

|12

Case Study

AI Summary

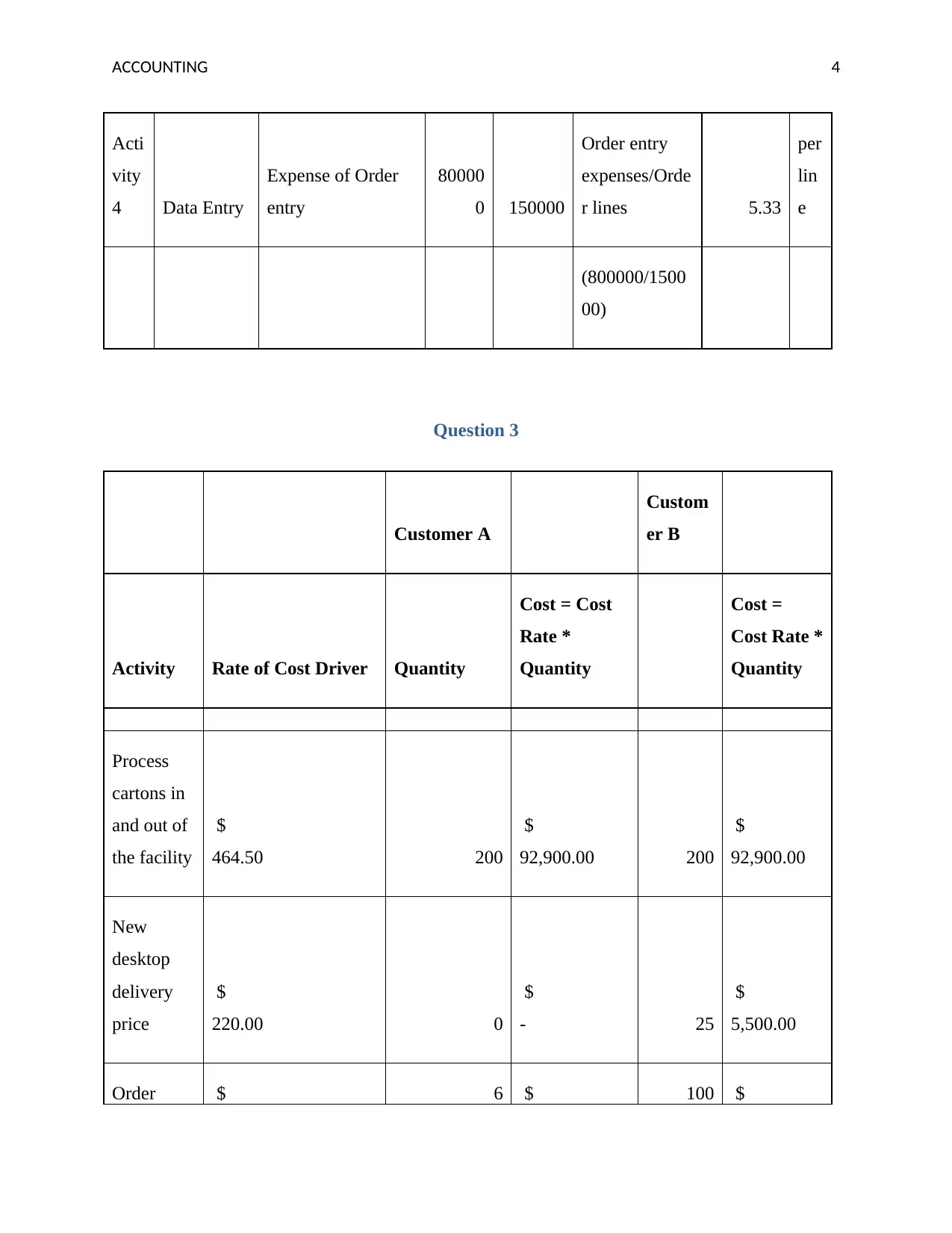

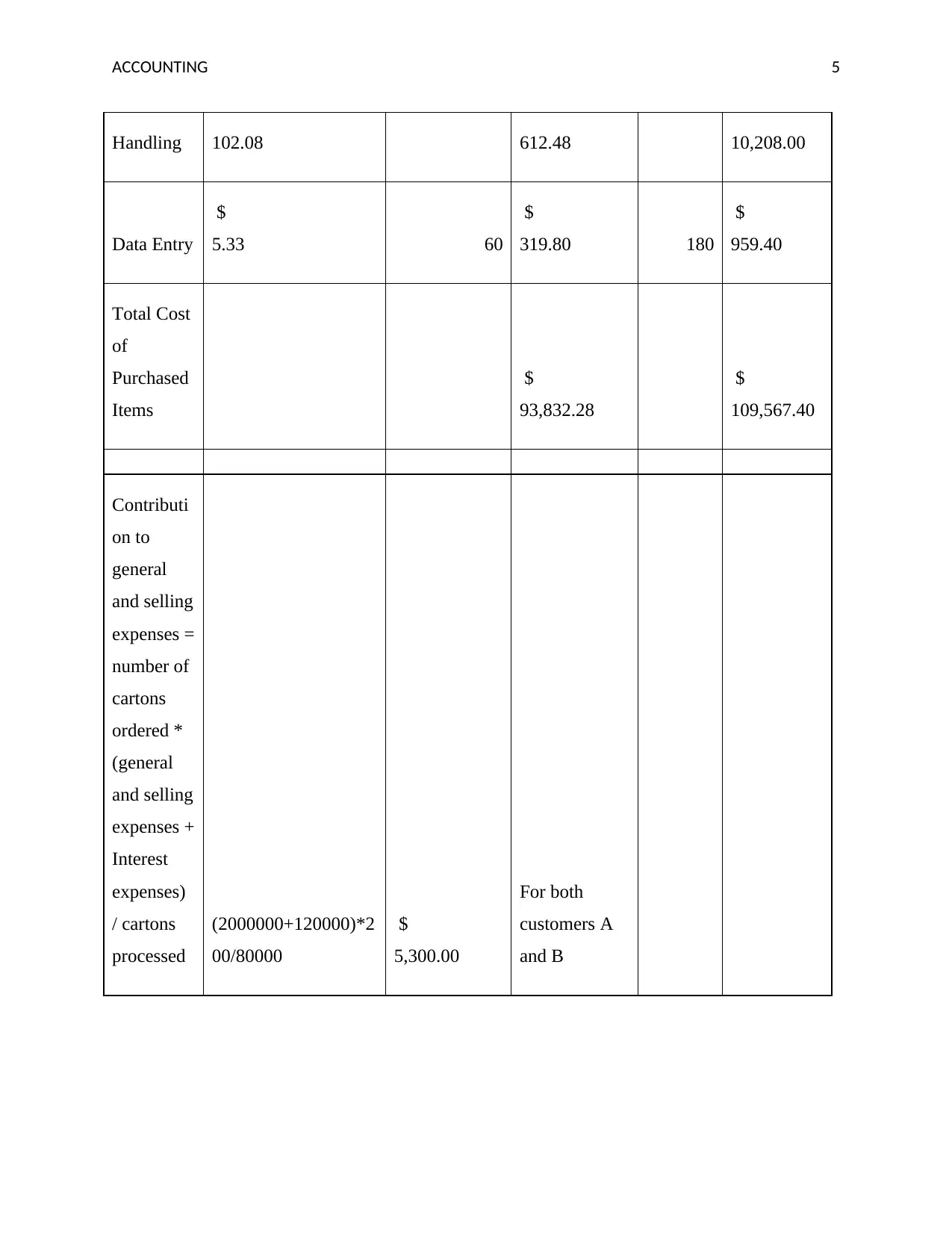

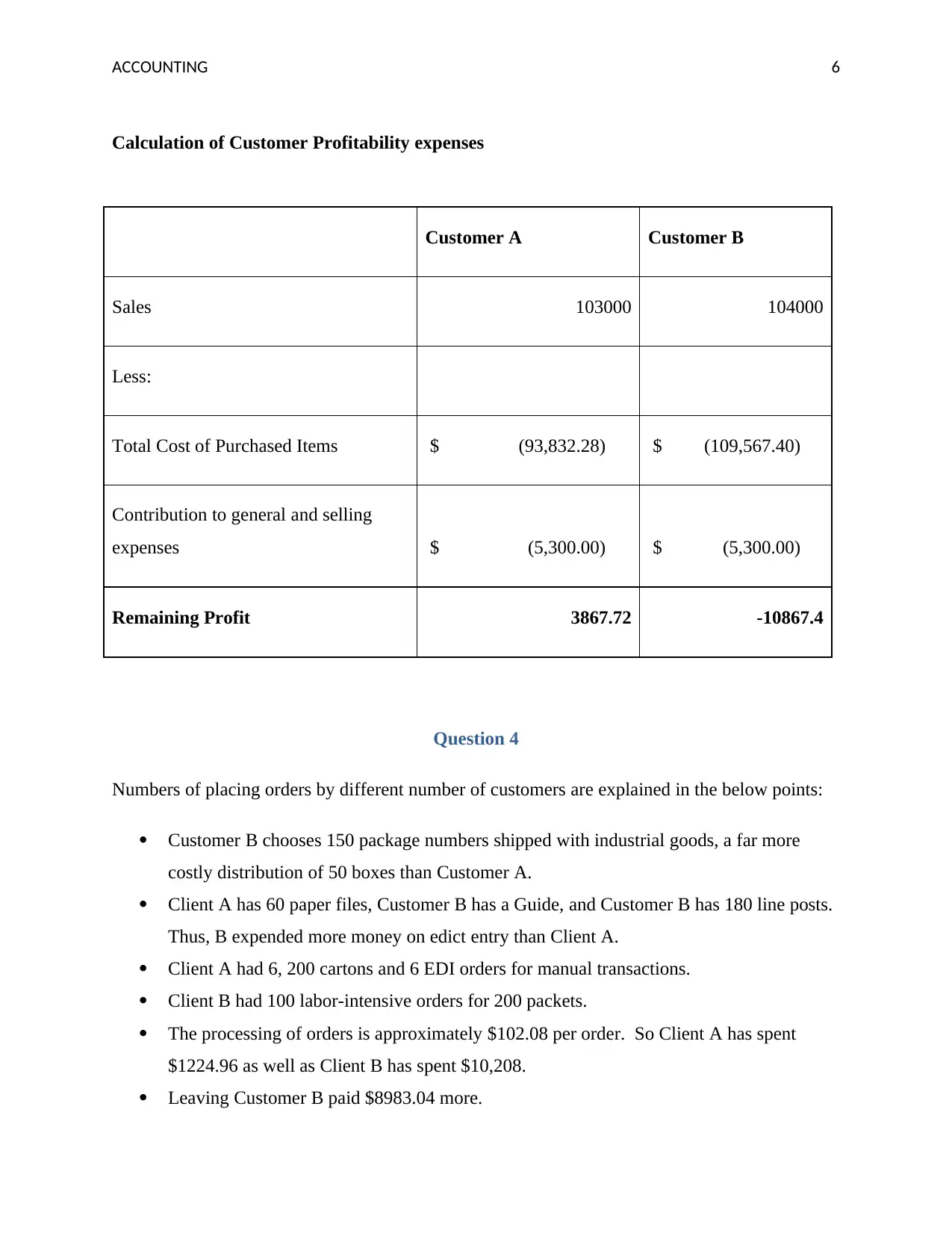

This assignment analyzes the Dakota Office Products (DOP) case, focusing on its financial performance and costing methods. The analysis begins by identifying the inadequacies of DOP's existing pricing system, which led to financial losses despite increased sales. An activity-based costing (ABC) system is developed, and activity cost-driver rates are calculated. The profitability of two customers, Customer A and Customer B, is then calculated using the ABC system. Differences in profitability are explained by analyzing the activities and costs associated with each customer, such as order sizes, delivery methods, and data entry requirements. The limitations of the profitability estimates are discussed, and additional information needed for a more comprehensive analysis is suggested. The analysis concludes with recommendations for price adjustments and operational changes to improve DOP's profitability, including shifting to EDI orders and incentivizing large orders. The student's analysis provides insights into cost management, pricing strategies, and customer profitability within a distribution business.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.