Tax Expenditures and Financial Reporting

VerifiedAdded on 2020/05/28

|12

|2943

|26

AI Summary

The assignment analyzes income tax expenditures as presented in a firm's (BSA) annual report. It explains how current and deferred taxes are calculated, highlighting the differences between taxable profit and reported profit due to various income items and expenses. The analysis emphasizes temporary variances in asset and liability carrying amounts that contribute to deferred tax recognition.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

University Name

Student Name

Authors’ Note

Corporate Accounting

University Name

Student Name

Authors’ Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

CORPORATE ACCOUNTING

Table of Contents

Solution to Question i.................................................................................................................2

Solution to Question ii...............................................................................................................3

Solution to Question iii..............................................................................................................5

Solution to Question IV.............................................................................................................6

Solution to Question v................................................................................................................7

Solution to Question VI.............................................................................................................8

Solution to Question vii.............................................................................................................9

References:...............................................................................................................................11

CORPORATE ACCOUNTING

Table of Contents

Solution to Question i.................................................................................................................2

Solution to Question ii...............................................................................................................3

Solution to Question iii..............................................................................................................5

Solution to Question IV.............................................................................................................6

Solution to Question v................................................................................................................7

Solution to Question VI.............................................................................................................8

Solution to Question vii.............................................................................................................9

References:...............................................................................................................................11

3

CORPORATE ACCOUNTING

Solution to Question i

Essentially, there are three different items presented in the balance sheet statement of the

corporations and one of the important financial items is necessarily equity. There is not an

exception in case of the selected company BSA limited company. As per the balance sheet of

the company declared during the year 2016, there are necessarily three different items under

the segment equity and these include issued capital, retained earnings as well as reserves. In

actual fact, issued capital can be referred to as the business equity (Bhasin, 2015). Essentially,

business corporations mainly draw a specific proportion of the capital necessary for the

business concern. However, the enumeration of the issued capital is carried out by

multiplying total number of shares of chiefly stock outstanding by the par values of mainly

shares. As per the annual declaration of the company BSA limited, issued capital can be

observed to be $97592000 in 2016 as compared to the figure of 2015 that is $97592000.

Essentially, the key items under issued capital are necessarily issues of particularly ordinary

shares, costs associated to share issue as well as income tax associated to the share issue. The

following financial item under the section of equity includes reserves. In essence, under the

themes of financial accounting, reserve can be regarded as an element of the equity of the

company BSA limited company. As such, this can be referred to as the additional amount

apart from basic capital share. As per the annual declaration of the corporation presented in

the year 2016, there subsists an $1410000 in reserves in the year 2016 when compared to the

figure recorded in the year ago period, that is $1410000. In the company BSA limited

company, there exist three different elements of equity reserves that include reserve for

equity settled advantage, reserve for foreign currency translation together with research for

hedging. The subsequent item mentioned under the section equity of the firm BSA limited is

necessarily retained earnings. This stands for the total profit as well as losses of the

CORPORATE ACCOUNTING

Solution to Question i

Essentially, there are three different items presented in the balance sheet statement of the

corporations and one of the important financial items is necessarily equity. There is not an

exception in case of the selected company BSA limited company. As per the balance sheet of

the company declared during the year 2016, there are necessarily three different items under

the segment equity and these include issued capital, retained earnings as well as reserves. In

actual fact, issued capital can be referred to as the business equity (Bhasin, 2015). Essentially,

business corporations mainly draw a specific proportion of the capital necessary for the

business concern. However, the enumeration of the issued capital is carried out by

multiplying total number of shares of chiefly stock outstanding by the par values of mainly

shares. As per the annual declaration of the company BSA limited, issued capital can be

observed to be $97592000 in 2016 as compared to the figure of 2015 that is $97592000.

Essentially, the key items under issued capital are necessarily issues of particularly ordinary

shares, costs associated to share issue as well as income tax associated to the share issue. The

following financial item under the section of equity includes reserves. In essence, under the

themes of financial accounting, reserve can be regarded as an element of the equity of the

company BSA limited company. As such, this can be referred to as the additional amount

apart from basic capital share. As per the annual declaration of the corporation presented in

the year 2016, there subsists an $1410000 in reserves in the year 2016 when compared to the

figure recorded in the year ago period, that is $1410000. In the company BSA limited

company, there exist three different elements of equity reserves that include reserve for

equity settled advantage, reserve for foreign currency translation together with research for

hedging. The subsequent item mentioned under the section equity of the firm BSA limited is

necessarily retained earnings. This stands for the total profit as well as losses of the

4

CORPORATE ACCOUNTING

corporation particularly calculated from the time of formation lessened by any dividend

disbursement to shareholders (Ramanna, 2014).

Solution to Question ii

Diverse types of expenses are incurred by business concerns that include selling expenditures

and administrative expenditures among many others. Essentially, one of such kind of expends

also include tax expenditure. Additionally, tax expenditure can be regarded as a major

accountability of the firm due to the federal, state as well as municipal governments of the

nation (Gitman et al., 2015). The enumeration of the tax expenditure is carried out by

multiplying the apt tax of the company by the earnings before taxes after factoring certain

key elements such as non-deductible items, tax assets/resources as well as liabilities (Mats

Andersson et al., 2016). As such, there exists no exception in case of the corporation BSA

Limited as the corporation also has tax expends. As per the annual declaration of the

corporation BSA Limited, the company has registered loss of $(3014000) from mainly

continuing operations specifically from income tax. In accordance with the directives of the

Australian taxation law, the rate of corporate tax for particularly Australian firm is 30%.

Founded on the rate of tax of 30%, the total tax expends of the firm BSA limited is $795000

in 2016 and $1564000. Essentially, this can be considered to be primary tax expends of the

corporation for the financial year 2016. Nevertheless, it can be hereby witnessed that there

has been decrease in the overall tax expenditure of the firm owing to the decrease in overall

earnings of the business corporation in the financial year 2016 as compared to the year 2015.

CORPORATE ACCOUNTING

corporation particularly calculated from the time of formation lessened by any dividend

disbursement to shareholders (Ramanna, 2014).

Solution to Question ii

Diverse types of expenses are incurred by business concerns that include selling expenditures

and administrative expenditures among many others. Essentially, one of such kind of expends

also include tax expenditure. Additionally, tax expenditure can be regarded as a major

accountability of the firm due to the federal, state as well as municipal governments of the

nation (Gitman et al., 2015). The enumeration of the tax expenditure is carried out by

multiplying the apt tax of the company by the earnings before taxes after factoring certain

key elements such as non-deductible items, tax assets/resources as well as liabilities (Mats

Andersson et al., 2016). As such, there exists no exception in case of the corporation BSA

Limited as the corporation also has tax expends. As per the annual declaration of the

corporation BSA Limited, the company has registered loss of $(3014000) from mainly

continuing operations specifically from income tax. In accordance with the directives of the

Australian taxation law, the rate of corporate tax for particularly Australian firm is 30%.

Founded on the rate of tax of 30%, the total tax expends of the firm BSA limited is $795000

in 2016 and $1564000. Essentially, this can be considered to be primary tax expends of the

corporation for the financial year 2016. Nevertheless, it can be hereby witnessed that there

has been decrease in the overall tax expenditure of the firm owing to the decrease in overall

earnings of the business corporation in the financial year 2016 as compared to the year 2015.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

CORPORATE ACCOUNTING

Solution to Question iii

Based on the above discussion it can be hereby mentioned that the business entity BSA

Limited has registered a loss of $3014000 in the FY 2016. However, the profit was recorded

to be $ 5449000 in the FY 2015.

Furthermore, the annual report of the business concern mentions that the income tax expends

of the firm enumerated at the rate of 30% in the FY 2016. With the rate of 30%, the total

income tax expends of the corporation BSA Limited need to be ($904000) in the FY 2016

and $1632 in the FY 2015.

Essentially, the total benefit for the specific years that can be reconciled shows that loss/profit

of the firm from the continuing operations stands at ($3014000) in the FY 2016 as compared

to ($5439000). Essentially, the income tax enumerated at the rate of 30% stands at ($904000)

in the FY 2016 as compared to the year ago figure of $1632000. Moreover, a distinct

variance in the tax expenditure of the corporation BSA Limited can be observed in the

financial declaration of the corporation. Particularly, in case of BSA Limited, there are

certain financial items that can be either included or else excluded from the preliminary total

tax expenditure. Essentially, these financial items can be regarded as the reasons for the

variances in the total amount of tax expenditure (Schaltegger et al., 2017). Specifically in

case of BSA Limited, there is different financial items that have additional impacts on the

entire tax expends of the corporation. As per the annual financial declaration of the

corporation, the first and foremost item in this regard is the non-deductible expenditure that

can be analysed for the purpose of determination of taxable gains. The item that need to be

adjusted for include the allowances for research and development (Warren & Jones, 2017).

Also, adjustments are recognized in the present year in association to the current tax of prior

years and other and this amounts to ($29000) in the FY 2016 and ($18000) in the FY2015.

CORPORATE ACCOUNTING

Solution to Question iii

Based on the above discussion it can be hereby mentioned that the business entity BSA

Limited has registered a loss of $3014000 in the FY 2016. However, the profit was recorded

to be $ 5449000 in the FY 2015.

Furthermore, the annual report of the business concern mentions that the income tax expends

of the firm enumerated at the rate of 30% in the FY 2016. With the rate of 30%, the total

income tax expends of the corporation BSA Limited need to be ($904000) in the FY 2016

and $1632 in the FY 2015.

Essentially, the total benefit for the specific years that can be reconciled shows that loss/profit

of the firm from the continuing operations stands at ($3014000) in the FY 2016 as compared

to ($5439000). Essentially, the income tax enumerated at the rate of 30% stands at ($904000)

in the FY 2016 as compared to the year ago figure of $1632000. Moreover, a distinct

variance in the tax expenditure of the corporation BSA Limited can be observed in the

financial declaration of the corporation. Particularly, in case of BSA Limited, there are

certain financial items that can be either included or else excluded from the preliminary total

tax expenditure. Essentially, these financial items can be regarded as the reasons for the

variances in the total amount of tax expenditure (Schaltegger et al., 2017). Specifically in

case of BSA Limited, there is different financial items that have additional impacts on the

entire tax expends of the corporation. As per the annual financial declaration of the

corporation, the first and foremost item in this regard is the non-deductible expenditure that

can be analysed for the purpose of determination of taxable gains. The item that need to be

adjusted for include the allowances for research and development (Warren & Jones, 2017).

Also, adjustments are recognized in the present year in association to the current tax of prior

years and other and this amounts to ($29000) in the FY 2016 and ($18000) in the FY2015.

6

CORPORATE ACCOUNTING

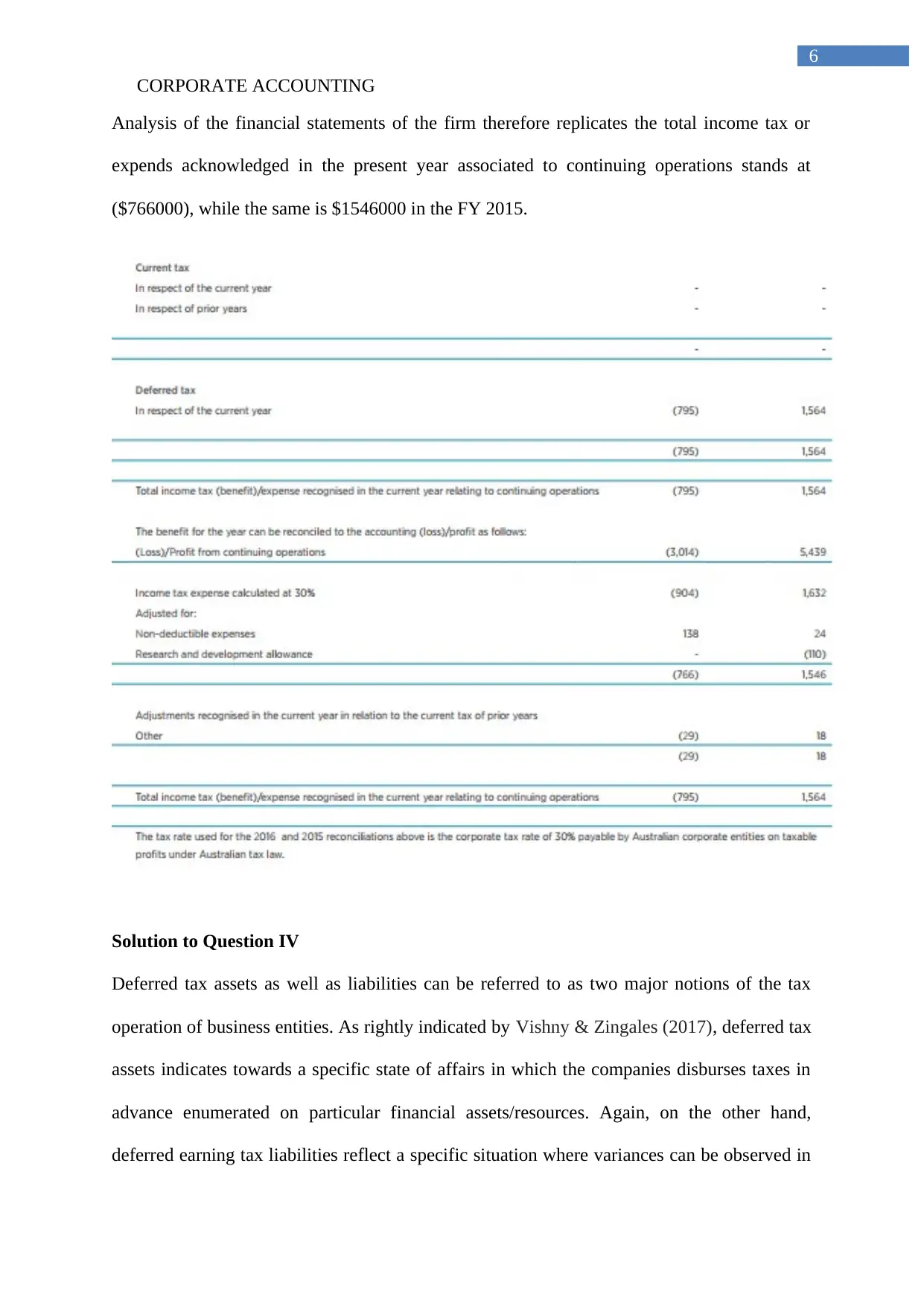

Analysis of the financial statements of the firm therefore replicates the total income tax or

expends acknowledged in the present year associated to continuing operations stands at

($766000), while the same is $1546000 in the FY 2015.

Solution to Question IV

Deferred tax assets as well as liabilities can be referred to as two major notions of the tax

operation of business entities. As rightly indicated by Vishny & Zingales (2017), deferred tax

assets indicates towards a specific state of affairs in which the companies disburses taxes in

advance enumerated on particular financial assets/resources. Again, on the other hand,

deferred earning tax liabilities reflect a specific situation where variances can be observed in

CORPORATE ACCOUNTING

Analysis of the financial statements of the firm therefore replicates the total income tax or

expends acknowledged in the present year associated to continuing operations stands at

($766000), while the same is $1546000 in the FY 2015.

Solution to Question IV

Deferred tax assets as well as liabilities can be referred to as two major notions of the tax

operation of business entities. As rightly indicated by Vishny & Zingales (2017), deferred tax

assets indicates towards a specific state of affairs in which the companies disburses taxes in

advance enumerated on particular financial assets/resources. Again, on the other hand,

deferred earning tax liabilities reflect a specific situation where variances can be observed in

7

CORPORATE ACCOUNTING

particularly profit as well as tax carrying value of the corporation. However, in case of the

business entity BSA Limited, it can be observed that the company has $7795000 as deferred

tax assets during the year 2016. However, the deferred tax liabilities are detected for

particularly taxable variances related to investments in specifically subsidiaries as well as

associates along with the interests that are in joint ventures. Taking into account specific

directives of accounting and rules of deferred tax liabilities or assets, it can be said that there

are specific reasons for the increase of deferred tax assets as well as liabilities (Robinson et

al., 2015). However, particularly in case of deferred tax assets, the reason might be the

surplus payment for depreciation by the corporation owing to the variances in the

depreciation and taxable rate of depreciation. As a result of surplus disbursement for

depreciation, the business entity BSA Limited will not have to make payments for additional

tax in subsequent year, thereby, it can be regarded as an asset. Essentially, for deferred tax

assets, the reason might ne the excess disbursement of depreciation by the corporation owing

to the variances in depreciation and taxable rate of depreciation. Owing to deferred tax

liabilities, it might have happened that because of temporary variances in profits of the

corporation, the corporation had to make comparatively less payments for taxes in the present

year (Tazik & Mohamed, 2014). Therefore, it is necessary for the corporation to pay the

amount in the subsequent years.

Solution to Question v

Current tax assets/resources or income tax that is payable can be regarded as an important

feature for the business corporation. As mentioned in the annual declaration of the business

concern BSA Limited, the corporation has illustrated about the current tax assets. As per the

financial statements of the firm BSA Limited, it can be seen that BSA Limited has not

declared about any amount for particularly present tax assets during the financial year 2016.

CORPORATE ACCOUNTING

particularly profit as well as tax carrying value of the corporation. However, in case of the

business entity BSA Limited, it can be observed that the company has $7795000 as deferred

tax assets during the year 2016. However, the deferred tax liabilities are detected for

particularly taxable variances related to investments in specifically subsidiaries as well as

associates along with the interests that are in joint ventures. Taking into account specific

directives of accounting and rules of deferred tax liabilities or assets, it can be said that there

are specific reasons for the increase of deferred tax assets as well as liabilities (Robinson et

al., 2015). However, particularly in case of deferred tax assets, the reason might be the

surplus payment for depreciation by the corporation owing to the variances in the

depreciation and taxable rate of depreciation. As a result of surplus disbursement for

depreciation, the business entity BSA Limited will not have to make payments for additional

tax in subsequent year, thereby, it can be regarded as an asset. Essentially, for deferred tax

assets, the reason might ne the excess disbursement of depreciation by the corporation owing

to the variances in depreciation and taxable rate of depreciation. Owing to deferred tax

liabilities, it might have happened that because of temporary variances in profits of the

corporation, the corporation had to make comparatively less payments for taxes in the present

year (Tazik & Mohamed, 2014). Therefore, it is necessary for the corporation to pay the

amount in the subsequent years.

Solution to Question v

Current tax assets/resources or income tax that is payable can be regarded as an important

feature for the business corporation. As mentioned in the annual declaration of the business

concern BSA Limited, the corporation has illustrated about the current tax assets. As per the

financial statements of the firm BSA Limited, it can be seen that BSA Limited has not

declared about any amount for particularly present tax assets during the financial year 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE ACCOUNTING

Nevertheless, during the year 2016, the corporation recorded $795000 as firm’s deferred tax

in 2016 and $1546000 in 2015.

In business entities, it can be observed that there exists a basic variance between income tax

expends and income tax that is payable and certain specific causes can be held accountable

for this gap. The first reason is the existence of deferred tax assets. Essentially, there are

several instances where corporation disburses additional tax assets in comparison to deferred

tax assets that generate the variance. The following reason is the distinction between the

regulations of financial accounting and the regulations of tax accounting. In this regard, the

instance of depreciation can be stated (Maynard, 2017). Variances for depreciation can be

observed under the financial accounting in addition to tax accounting for varied depreciation

rate. Therefore, the total amount of depreciation payable can either be enhanced or lessened.

Therefore, these are the primary causes behind the variances between income tax payable and

income tax expends.

Solution to Question VI

Analysis of financial statements of the firm BSA Limited reveals the fact that the company

incurs tax expends, as mentioned in the income statement as well as statement of flow of

cash. As per the income statement, the corporation reflects the entire amount of tax expends

using the tax rate of particularly 30% on the earned profit from diverse continuing operations

before tax. Essentially, the income tax expenditure reflects the total sum of the payable

current tax as well as the deferred tax. Essentially, the current tax payable is mainly founded

on the overall taxable profit for the particular year. Essentially, the taxable profit varies from

the profit that is reflected in the consolidated statement of both profit and loss as well as other

comprehensive earnings statement. This is owing to different items of earnings plus

expenditures that are necessarily taxable or in other terms deductible in different other years

CORPORATE ACCOUNTING

Nevertheless, during the year 2016, the corporation recorded $795000 as firm’s deferred tax

in 2016 and $1546000 in 2015.

In business entities, it can be observed that there exists a basic variance between income tax

expends and income tax that is payable and certain specific causes can be held accountable

for this gap. The first reason is the existence of deferred tax assets. Essentially, there are

several instances where corporation disburses additional tax assets in comparison to deferred

tax assets that generate the variance. The following reason is the distinction between the

regulations of financial accounting and the regulations of tax accounting. In this regard, the

instance of depreciation can be stated (Maynard, 2017). Variances for depreciation can be

observed under the financial accounting in addition to tax accounting for varied depreciation

rate. Therefore, the total amount of depreciation payable can either be enhanced or lessened.

Therefore, these are the primary causes behind the variances between income tax payable and

income tax expends.

Solution to Question VI

Analysis of financial statements of the firm BSA Limited reveals the fact that the company

incurs tax expends, as mentioned in the income statement as well as statement of flow of

cash. As per the income statement, the corporation reflects the entire amount of tax expends

using the tax rate of particularly 30% on the earned profit from diverse continuing operations

before tax. Essentially, the income tax expenditure reflects the total sum of the payable

current tax as well as the deferred tax. Essentially, the current tax payable is mainly founded

on the overall taxable profit for the particular year. Essentially, the taxable profit varies from

the profit that is reflected in the consolidated statement of both profit and loss as well as other

comprehensive earnings statement. This is owing to different items of earnings plus

expenditures that are necessarily taxable or in other terms deductible in different other years

9

CORPORATE ACCOUNTING

along with items that are never taxable or else deductible (Sunder, 2016). In this perspective,

it hereby needs to be stated that the tax expends come under the flow of cash from operating

actions. Under this specific segment of cash flow statement, certain items of corporation’s

income statements are treated differently. This implies that certain changes occur in the

current assets as well as current liabilities of the firm. In the present case of BSA Limited,

disbursements for income tax can be regarded as a current asset. As mentioned in the

company’s statement of flow of cash, certain reductions in the elements of tax expends has

been mentioned that refers to the usage of cash. This implies that certain components of tax

expends have been stopped before taking into consideration consolidated statement. Because

of these reasons, the variances on tax expends can be observed in the statement of income

and statement of flow of cash (Weygandt et al., 2015). There are certain particular reasons for

this difference in the total amounts of income tax expends (Lisowsky et al., 2017).

Solution to Question vii

After observation of tax treatment in the financial assertions of BSA Limited, it can be stated

that there exists no element of doubt and confusion in the process of treatment of tax. BSA

has carried out by adhering to the directives as well as stipulations of the Australian Taxation

Law. Also, BSA has presented all the requisite illustrations as well rationalization of different

taxation matters such as rate of tax, diverse deferred tax assets as well as liabilities and

currant taxation liabilities among many others. Nonetheless, there are certain striking factors

in the treatment of taxation of the reporting entity BSA. The significant accounting policies

illustrated in the annual report of the corporation shows that tax assets as well as liabilities

(deferred) are associated to employee benefit arrangements and are recognized and

enumerated as per AASB 112 (for income taxes) and AASB 119 (for Employee Benefits)

(Tran, 2015). As per the annual report of the firm BSA, income tax expenditures reflect the

CORPORATE ACCOUNTING

along with items that are never taxable or else deductible (Sunder, 2016). In this perspective,

it hereby needs to be stated that the tax expends come under the flow of cash from operating

actions. Under this specific segment of cash flow statement, certain items of corporation’s

income statements are treated differently. This implies that certain changes occur in the

current assets as well as current liabilities of the firm. In the present case of BSA Limited,

disbursements for income tax can be regarded as a current asset. As mentioned in the

company’s statement of flow of cash, certain reductions in the elements of tax expends has

been mentioned that refers to the usage of cash. This implies that certain components of tax

expends have been stopped before taking into consideration consolidated statement. Because

of these reasons, the variances on tax expends can be observed in the statement of income

and statement of flow of cash (Weygandt et al., 2015). There are certain particular reasons for

this difference in the total amounts of income tax expends (Lisowsky et al., 2017).

Solution to Question vii

After observation of tax treatment in the financial assertions of BSA Limited, it can be stated

that there exists no element of doubt and confusion in the process of treatment of tax. BSA

has carried out by adhering to the directives as well as stipulations of the Australian Taxation

Law. Also, BSA has presented all the requisite illustrations as well rationalization of different

taxation matters such as rate of tax, diverse deferred tax assets as well as liabilities and

currant taxation liabilities among many others. Nonetheless, there are certain striking factors

in the treatment of taxation of the reporting entity BSA. The significant accounting policies

illustrated in the annual report of the corporation shows that tax assets as well as liabilities

(deferred) are associated to employee benefit arrangements and are recognized and

enumerated as per AASB 112 (for income taxes) and AASB 119 (for Employee Benefits)

(Tran, 2015). As per the annual report of the firm BSA, income tax expenditures reflect the

10

CORPORATE ACCOUNTING

total sum of the payable tax in the current period plus the deferred tax. For the current tax that

is payable by the firm is mainly founded on the calculated taxable profit for a particular year

(Hanlon et al., 2014). However, the taxable profit differs as presented in the reporting entity’s

consolidated statement of particularly profit or else loss as well as other comprehensive

income owing to different income items and expends that are necessarily taxable else wise

deductible. Fundamentally, the deferred tax is primarily recognized on the temporary

variances that exist between the carrying amounts of particularly assets as well as liabilities

presented in the consolidated pecuniary statements.

CORPORATE ACCOUNTING

total sum of the payable tax in the current period plus the deferred tax. For the current tax that

is payable by the firm is mainly founded on the calculated taxable profit for a particular year

(Hanlon et al., 2014). However, the taxable profit differs as presented in the reporting entity’s

consolidated statement of particularly profit or else loss as well as other comprehensive

income owing to different income items and expends that are necessarily taxable else wise

deductible. Fundamentally, the deferred tax is primarily recognized on the temporary

variances that exist between the carrying amounts of particularly assets as well as liabilities

presented in the consolidated pecuniary statements.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

CORPORATE ACCOUNTING

References:

Bhasin, M. L. (2015). Corporate accounting fraud: A case study of Satyam Computers

Limited.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hanlon, D., Navissi, F., & Soepriyanto, G. (2014). The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2),

87-99.

Lisowsky, P., Minnis, M., & Sutherland, A. (2017). Economic growth and financial statement

verification. Journal of Accounting Research.

Mats Andersson, A. P., Bolton, P., Herz, B., Rogers, J., Accounting, S., Eccles, R. G., &

Youmans, T. (2016). APPLIED CORPORATE FINANCE. Journal of Applied Corporate

Finance, 28(2), 47.

Maynard, J. (2017). Financial accounting, reporting, and analysis. Oxford University Press.

Ramanna, K. (2014). Political standards: Accounting for legitimacy.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Schaltegger, S., Etxeberria, I. Á., & Ortas, E. (2017). Innovating Corporate Accounting and

Reporting for Sustainability–Attributes and Challenges. Sustainable Development, 25(2),

113-122.

CORPORATE ACCOUNTING

References:

Bhasin, M. L. (2015). Corporate accounting fraud: A case study of Satyam Computers

Limited.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hanlon, D., Navissi, F., & Soepriyanto, G. (2014). The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2),

87-99.

Lisowsky, P., Minnis, M., & Sutherland, A. (2017). Economic growth and financial statement

verification. Journal of Accounting Research.

Mats Andersson, A. P., Bolton, P., Herz, B., Rogers, J., Accounting, S., Eccles, R. G., &

Youmans, T. (2016). APPLIED CORPORATE FINANCE. Journal of Applied Corporate

Finance, 28(2), 47.

Maynard, J. (2017). Financial accounting, reporting, and analysis. Oxford University Press.

Ramanna, K. (2014). Political standards: Accounting for legitimacy.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Schaltegger, S., Etxeberria, I. Á., & Ortas, E. (2017). Innovating Corporate Accounting and

Reporting for Sustainability–Attributes and Challenges. Sustainable Development, 25(2),

113-122.

12

CORPORATE ACCOUNTING

Sunder, S. (2016). Rethinking financial reporting: standards, norms and

institutions. Foundations and Trends® in Accounting, 11(1–2), 1-118.

Tazik, H., & Mohamed, Z. M. (2014, February). Accounting information system

effectiveness, foreign ownership and timeliness of corporate financial report. In 5th Asia-

Pacific Business Research Conference (pp. 17-18).

Tran, A. (2015). Can taxable income be estimated from financial reports of listed companies

in Australia?. Browser Download This Paper.

Vishny, R., & Zingales, L. (2017). Corporate Finance. Journal of Political Economy, 125(6),

1805-1812.

Warren, C. S., & Jones, J. (2017). Corporate financial accounting. Cengage Learning.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

CORPORATE ACCOUNTING

Sunder, S. (2016). Rethinking financial reporting: standards, norms and

institutions. Foundations and Trends® in Accounting, 11(1–2), 1-118.

Tazik, H., & Mohamed, Z. M. (2014, February). Accounting information system

effectiveness, foreign ownership and timeliness of corporate financial report. In 5th Asia-

Pacific Business Research Conference (pp. 17-18).

Tran, A. (2015). Can taxable income be estimated from financial reports of listed companies

in Australia?. Browser Download This Paper.

Vishny, R., & Zingales, L. (2017). Corporate Finance. Journal of Political Economy, 125(6),

1805-1812.

Warren, C. S., & Jones, J. (2017). Corporate financial accounting. Cengage Learning.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.