Corporate Accounting Report: Dexus Limited and GPT Group Analysis

VerifiedAdded on 2023/01/13

|13

|3843

|56

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, focusing on two ASX-listed real estate investment companies, GPT Group and Dexus Limited. It begins by identifying various sources of funds employed by these companies, including retained earnings, short-term and long-term debts, common stock, and other equities. The report then evaluates the evolution of these funding sources over three financial years, highlighting significant changes. A key aspect of the analysis involves determining the proportion of internally and externally generated funds for each company. Furthermore, the report explains the merits and shortcomings of each funding source. The analysis extends to a critical evaluation of the types of liabilities presented in the companies' balance sheets, differentiating between interest-bearing and non-interest-bearing liabilities. The report also examines key provisions under AASB 137, such as provisions, contingency liabilities, and contingency assets, and assesses the companies' references to this standard in their annual reports. Finally, the report identifies and critically examines the different categories of assets recorded in the companies' balance sheets and the measurement bases used for asset recording.

Corporate

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Identify the different sources of fund which is used by the chosen organization....................3

2. Evaluate the evolution of sources of fund over the last three financial years and focus on the

changes of various sources of fund..............................................................................................3

3. Identify the fund's percentage which internally as well as externally generated for each

company.......................................................................................................................................5

4. Explain the merits or shortcoming of different sources which used by the selected

companies....................................................................................................................................6

5. Critically evaluate the types of liabilities which mentioned in the selected company's

balance sheet and also identify that which one is interest bearing & which one not...................8

6. Critically examine the key provision under the AASB 137 such as Provision, Contingency

Liability and Contingency Assets................................................................................................8

7. Evaluate the selected company made any reference regarding AASB 137 in their annual

report............................................................................................................................................9

8. Identify different categories of assets which recorded in the company's balance sheet........10

9. Critically examine the measurement which followed by the organizations to record their

assets..........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES .............................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Identify the different sources of fund which is used by the chosen organization....................3

2. Evaluate the evolution of sources of fund over the last three financial years and focus on the

changes of various sources of fund..............................................................................................3

3. Identify the fund's percentage which internally as well as externally generated for each

company.......................................................................................................................................5

4. Explain the merits or shortcoming of different sources which used by the selected

companies....................................................................................................................................6

5. Critically evaluate the types of liabilities which mentioned in the selected company's

balance sheet and also identify that which one is interest bearing & which one not...................8

6. Critically examine the key provision under the AASB 137 such as Provision, Contingency

Liability and Contingency Assets................................................................................................8

7. Evaluate the selected company made any reference regarding AASB 137 in their annual

report............................................................................................................................................9

8. Identify different categories of assets which recorded in the company's balance sheet........10

9. Critically examine the measurement which followed by the organizations to record their

assets..........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES .............................................................................................................................13

INTRODUCTION

Corporate accounting is branch of accounting and it help the business to prepare final

accounts, cash flow statements and further analyse the results to make future decisions. In this

type of accounting, organizations only consider the monetary terms and records in appropriate

for the further analysis (Aburous, 2016). This report based on the two companies which is listed

in ASX that is Australian Stock Exchange. GPT group and Dexus Limited selected for the better

understanding of these concept. GPT group is real estate investment company which founded in

1971 and its headquarter situated in MLC Centre, Sydney, Australia. On the other side, Dexus

Limited also real estate investment company which manage the high profile portfolio of

Australian properties that valued at $ 31.8 billion.

This assessment cover the various topics such as different sources of finance and the

proportion of funds which company generated internally as well as externally. In addition

identify the liabilities and assets of the organizations which mentioned in their balance sheet and

examine the different key provision under the AASB 137. Along with this, evaluate the

measurement basis at the time of recording assets in the companies.

MAIN BODY

1. Identify the different sources of fund which is used by the chosen organization

There are various sources which is used by the organizations in order to fulfil their

financial requirement. Both companies such as Dexus limited and GPT group using below

mention source of funds which are as followed:

Retained earnings

Short term funds

Long term funds

Common stock

Comprehensive income

Other equities

2. Evaluate the evolution of sources of fund over the last three financial years and focus on the

changes of various sources of fund

GPT group follow the different source of funds which are discussed below:

Corporate accounting is branch of accounting and it help the business to prepare final

accounts, cash flow statements and further analyse the results to make future decisions. In this

type of accounting, organizations only consider the monetary terms and records in appropriate

for the further analysis (Aburous, 2016). This report based on the two companies which is listed

in ASX that is Australian Stock Exchange. GPT group and Dexus Limited selected for the better

understanding of these concept. GPT group is real estate investment company which founded in

1971 and its headquarter situated in MLC Centre, Sydney, Australia. On the other side, Dexus

Limited also real estate investment company which manage the high profile portfolio of

Australian properties that valued at $ 31.8 billion.

This assessment cover the various topics such as different sources of finance and the

proportion of funds which company generated internally as well as externally. In addition

identify the liabilities and assets of the organizations which mentioned in their balance sheet and

examine the different key provision under the AASB 137. Along with this, evaluate the

measurement basis at the time of recording assets in the companies.

MAIN BODY

1. Identify the different sources of fund which is used by the chosen organization

There are various sources which is used by the organizations in order to fulfil their

financial requirement. Both companies such as Dexus limited and GPT group using below

mention source of funds which are as followed:

Retained earnings

Short term funds

Long term funds

Common stock

Comprehensive income

Other equities

2. Evaluate the evolution of sources of fund over the last three financial years and focus on the

changes of various sources of fund

GPT group follow the different source of funds which are discussed below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Short term funds: Company required short terms debt which they had to repay within

one year and with the help of it GPT group able to perform their daily basis activities or fulfil the

financial requirements (Agrawal and Cooper, 2017). In 2018 company required around $ 20

million and in the previous years they were $ 49 million in both 2017 or 2016. it is observed that

company reduces their short term debt around $ 29 million.

Long term funds: Company required long term debt to make necessary changes in the

business operations or maximise the productivity. GOT group had long term debt in 2016 was

around $ 2948 million, in 2017 it was $ 3281 million and in 2018 it was $ 3599 million

(Financial report of GPT Group, 2020). It is clearly mentioned that, company required more

finance to perform their operations because long term debt increases every year.

Retain earnings: This earning secure by the company to for the future purpose or any

uninvited event. In 2016, GPT retain around $ 124 million, $ 950 million or $ 1945 million in

2017 or 2018 respectively. It is analysed that company raise their earning for for the further

actions which is beneficial for the company.

Common stock: With the help of company's balance sheet, it is observed that GPT has $

8130 million of common stock 2016, $ 8141 million in 2017 and in 2018 it was around $ 8152

million stock. There is not enough difference in the common stock in different period.

Comprehensive income: In the GPT Group, balance sheet shows that company had

other income around $ 16 million in 2016. In 2017, it was $ 9 million and ($ 8 million) in 2018

that was loss for the company.

Other equity: With the help of balance sheet of the company, it is observed that GPT

Group has $ 13 millions of other equities in 2016 (Atanasov and Black, 2016). In 2017, it was $

8 million and $ 13 million in 2018. There is a fluctuation in the other equities due to requirement

of liquidity in the organizations.

Dexus limited using below mention source of funds to fulfil their financial requirements:

Short term funds: Company was taken short term loan in 2016 around $ 316 million, $

149 million in 2017 and in 2018 it was $ 205 million. It has been analysed that Dexus limited

borrow different amount of loan in the different years.

Long term funds: With the help of financial statement of the company it is observed that

Dexus had long term debt around $ 3371 million in 2016. On the other side, it was reduces in

one year and with the help of it GPT group able to perform their daily basis activities or fulfil the

financial requirements (Agrawal and Cooper, 2017). In 2018 company required around $ 20

million and in the previous years they were $ 49 million in both 2017 or 2016. it is observed that

company reduces their short term debt around $ 29 million.

Long term funds: Company required long term debt to make necessary changes in the

business operations or maximise the productivity. GOT group had long term debt in 2016 was

around $ 2948 million, in 2017 it was $ 3281 million and in 2018 it was $ 3599 million

(Financial report of GPT Group, 2020). It is clearly mentioned that, company required more

finance to perform their operations because long term debt increases every year.

Retain earnings: This earning secure by the company to for the future purpose or any

uninvited event. In 2016, GPT retain around $ 124 million, $ 950 million or $ 1945 million in

2017 or 2018 respectively. It is analysed that company raise their earning for for the further

actions which is beneficial for the company.

Common stock: With the help of company's balance sheet, it is observed that GPT has $

8130 million of common stock 2016, $ 8141 million in 2017 and in 2018 it was around $ 8152

million stock. There is not enough difference in the common stock in different period.

Comprehensive income: In the GPT Group, balance sheet shows that company had

other income around $ 16 million in 2016. In 2017, it was $ 9 million and ($ 8 million) in 2018

that was loss for the company.

Other equity: With the help of balance sheet of the company, it is observed that GPT

Group has $ 13 millions of other equities in 2016 (Atanasov and Black, 2016). In 2017, it was $

8 million and $ 13 million in 2018. There is a fluctuation in the other equities due to requirement

of liquidity in the organizations.

Dexus limited using below mention source of funds to fulfil their financial requirements:

Short term funds: Company was taken short term loan in 2016 around $ 316 million, $

149 million in 2017 and in 2018 it was $ 205 million. It has been analysed that Dexus limited

borrow different amount of loan in the different years.

Long term funds: With the help of financial statement of the company it is observed that

Dexus had long term debt around $ 3371 million in 2016. On the other side, it was reduces in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 and remain $ 2698 million and again increases in 2018, it was around $ 3155 million. It is

analysed that company depend on long term debts which increases yearly.

Retain earnings: It is analysed that financial performance of company in terms of retain

earning was $ 1634 million in 2016 and in 2017 it was around $ 2373 million. In 2018, it was $

3616 million which continues increases (Financial report of Dexus Limited, 2020). It indicates

that company has strong financial position in the market because of high value of their retain

earning in every year.

Common stock: In the Dexus limited, there are some common stocks such as in 2016 it

was $ 5910 million, in 2017 it was around $ 6402 million and in 2018, it was $ 6404 million. It is

observed that organizations increases their stock level through issuing funds.

Comprehensive income: In Dexus Limited, comprehensive income or loss mentioned in

the balance sheet and it is settled with the retain earning (Bedford and Ziegler, 2016). In 2016, it

was $ 43 million and in the next two years it was constant that is 2017 or 2018. Company does

not gain but not occur loss for the same.

Other equity: Equity is the essential source of fund which is used by the organizations

and in Dexus Limited its value around $ 9 million in the period of 2016. After that it became

negative and having loss around $ 16 million in 2018.

3. Identify the fund's percentage which internally as well as externally generated for each

company

Both organizations such as Dexus Limited or GPT Group arrange funds from internal as

well as external sources. They also contributed in some proportion which mentioned in the table.

Dexus Limited:

Funds generated from internal sources Percentage of Funds

Sales of assets 10%

Issue equities 3% of equity

Loan from partners 5%

Insurance recovery 5%

Funds generated from external sources Percentage of Funds

analysed that company depend on long term debts which increases yearly.

Retain earnings: It is analysed that financial performance of company in terms of retain

earning was $ 1634 million in 2016 and in 2017 it was around $ 2373 million. In 2018, it was $

3616 million which continues increases (Financial report of Dexus Limited, 2020). It indicates

that company has strong financial position in the market because of high value of their retain

earning in every year.

Common stock: In the Dexus limited, there are some common stocks such as in 2016 it

was $ 5910 million, in 2017 it was around $ 6402 million and in 2018, it was $ 6404 million. It is

observed that organizations increases their stock level through issuing funds.

Comprehensive income: In Dexus Limited, comprehensive income or loss mentioned in

the balance sheet and it is settled with the retain earning (Bedford and Ziegler, 2016). In 2016, it

was $ 43 million and in the next two years it was constant that is 2017 or 2018. Company does

not gain but not occur loss for the same.

Other equity: Equity is the essential source of fund which is used by the organizations

and in Dexus Limited its value around $ 9 million in the period of 2016. After that it became

negative and having loss around $ 16 million in 2018.

3. Identify the fund's percentage which internally as well as externally generated for each

company

Both organizations such as Dexus Limited or GPT Group arrange funds from internal as

well as external sources. They also contributed in some proportion which mentioned in the table.

Dexus Limited:

Funds generated from internal sources Percentage of Funds

Sales of assets 10%

Issue equities 3% of equity

Loan from partners 5%

Insurance recovery 5%

Funds generated from external sources Percentage of Funds

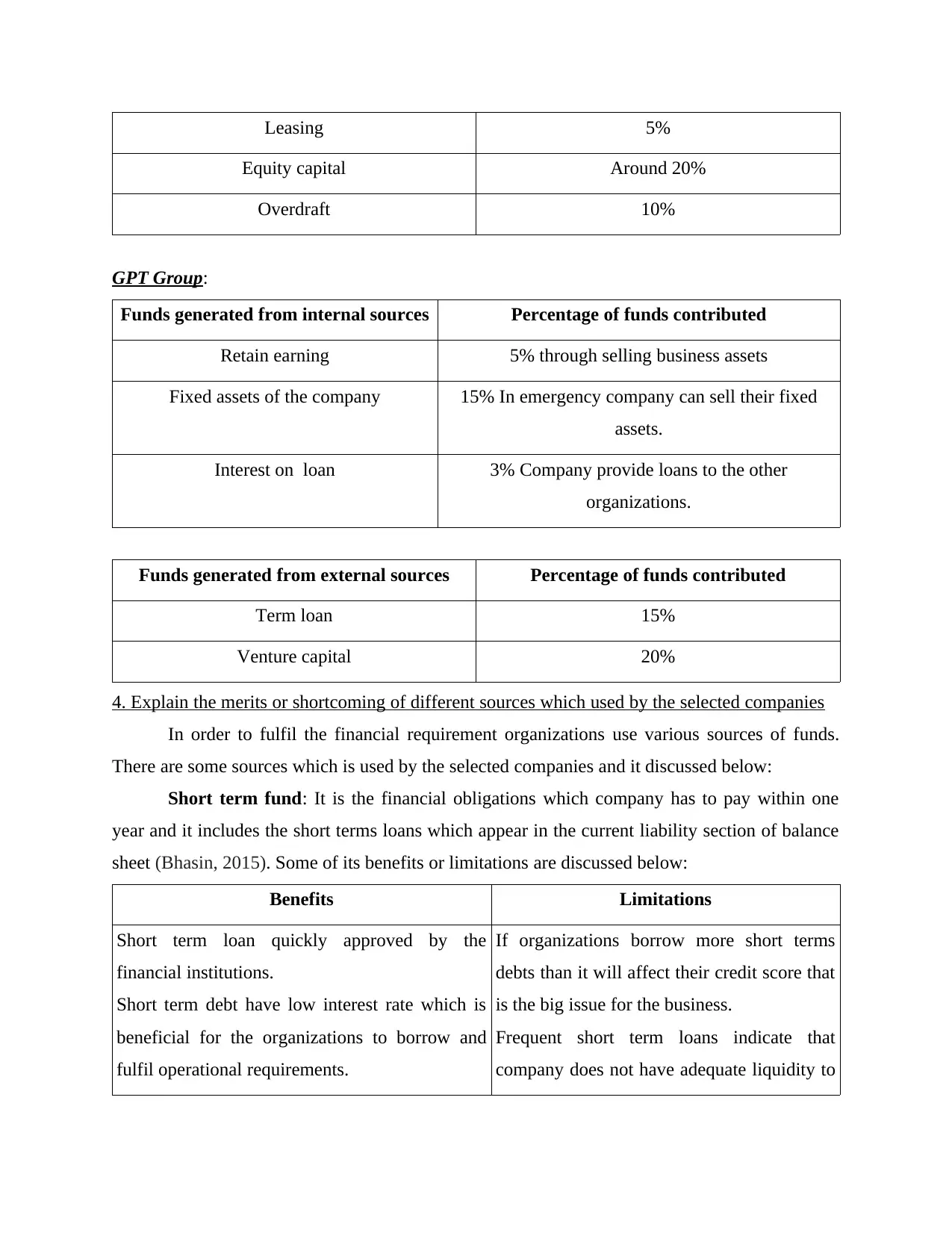

Leasing 5%

Equity capital Around 20%

Overdraft 10%

GPT Group:

Funds generated from internal sources Percentage of funds contributed

Retain earning 5% through selling business assets

Fixed assets of the company 15% In emergency company can sell their fixed

assets.

Interest on loan 3% Company provide loans to the other

organizations.

Funds generated from external sources Percentage of funds contributed

Term loan 15%

Venture capital 20%

4. Explain the merits or shortcoming of different sources which used by the selected companies

In order to fulfil the financial requirement organizations use various sources of funds.

There are some sources which is used by the selected companies and it discussed below:

Short term fund: It is the financial obligations which company has to pay within one

year and it includes the short terms loans which appear in the current liability section of balance

sheet (Bhasin, 2015). Some of its benefits or limitations are discussed below:

Benefits Limitations

Short term loan quickly approved by the

financial institutions.

Short term debt have low interest rate which is

beneficial for the organizations to borrow and

fulfil operational requirements.

If organizations borrow more short terms

debts than it will affect their credit score that

is the big issue for the business.

Frequent short term loans indicate that

company does not have adequate liquidity to

Equity capital Around 20%

Overdraft 10%

GPT Group:

Funds generated from internal sources Percentage of funds contributed

Retain earning 5% through selling business assets

Fixed assets of the company 15% In emergency company can sell their fixed

assets.

Interest on loan 3% Company provide loans to the other

organizations.

Funds generated from external sources Percentage of funds contributed

Term loan 15%

Venture capital 20%

4. Explain the merits or shortcoming of different sources which used by the selected companies

In order to fulfil the financial requirement organizations use various sources of funds.

There are some sources which is used by the selected companies and it discussed below:

Short term fund: It is the financial obligations which company has to pay within one

year and it includes the short terms loans which appear in the current liability section of balance

sheet (Bhasin, 2015). Some of its benefits or limitations are discussed below:

Benefits Limitations

Short term loan quickly approved by the

financial institutions.

Short term debt have low interest rate which is

beneficial for the organizations to borrow and

fulfil operational requirements.

If organizations borrow more short terms

debts than it will affect their credit score that

is the big issue for the business.

Frequent short term loans indicate that

company does not have adequate liquidity to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

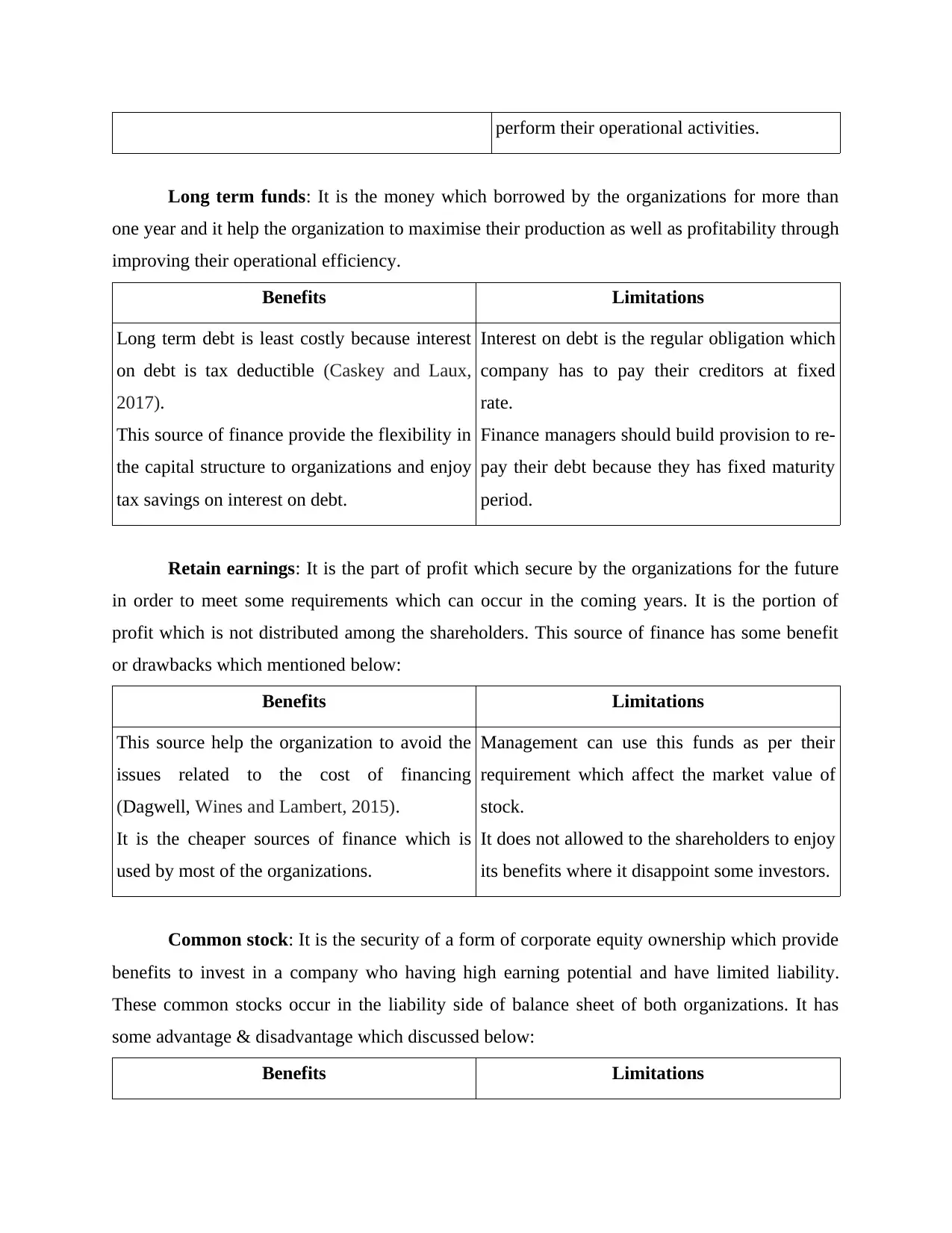

perform their operational activities.

Long term funds: It is the money which borrowed by the organizations for more than

one year and it help the organization to maximise their production as well as profitability through

improving their operational efficiency.

Benefits Limitations

Long term debt is least costly because interest

on debt is tax deductible (Caskey and Laux,

2017).

This source of finance provide the flexibility in

the capital structure to organizations and enjoy

tax savings on interest on debt.

Interest on debt is the regular obligation which

company has to pay their creditors at fixed

rate.

Finance managers should build provision to re-

pay their debt because they has fixed maturity

period.

Retain earnings: It is the part of profit which secure by the organizations for the future

in order to meet some requirements which can occur in the coming years. It is the portion of

profit which is not distributed among the shareholders. This source of finance has some benefit

or drawbacks which mentioned below:

Benefits Limitations

This source help the organization to avoid the

issues related to the cost of financing

(Dagwell, Wines and Lambert, 2015).

It is the cheaper sources of finance which is

used by most of the organizations.

Management can use this funds as per their

requirement which affect the market value of

stock.

It does not allowed to the shareholders to enjoy

its benefits where it disappoint some investors.

Common stock: It is the security of a form of corporate equity ownership which provide

benefits to invest in a company who having high earning potential and have limited liability.

These common stocks occur in the liability side of balance sheet of both organizations. It has

some advantage & disadvantage which discussed below:

Benefits Limitations

Long term funds: It is the money which borrowed by the organizations for more than

one year and it help the organization to maximise their production as well as profitability through

improving their operational efficiency.

Benefits Limitations

Long term debt is least costly because interest

on debt is tax deductible (Caskey and Laux,

2017).

This source of finance provide the flexibility in

the capital structure to organizations and enjoy

tax savings on interest on debt.

Interest on debt is the regular obligation which

company has to pay their creditors at fixed

rate.

Finance managers should build provision to re-

pay their debt because they has fixed maturity

period.

Retain earnings: It is the part of profit which secure by the organizations for the future

in order to meet some requirements which can occur in the coming years. It is the portion of

profit which is not distributed among the shareholders. This source of finance has some benefit

or drawbacks which mentioned below:

Benefits Limitations

This source help the organization to avoid the

issues related to the cost of financing

(Dagwell, Wines and Lambert, 2015).

It is the cheaper sources of finance which is

used by most of the organizations.

Management can use this funds as per their

requirement which affect the market value of

stock.

It does not allowed to the shareholders to enjoy

its benefits where it disappoint some investors.

Common stock: It is the security of a form of corporate equity ownership which provide

benefits to invest in a company who having high earning potential and have limited liability.

These common stocks occur in the liability side of balance sheet of both organizations. It has

some advantage & disadvantage which discussed below:

Benefits Limitations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

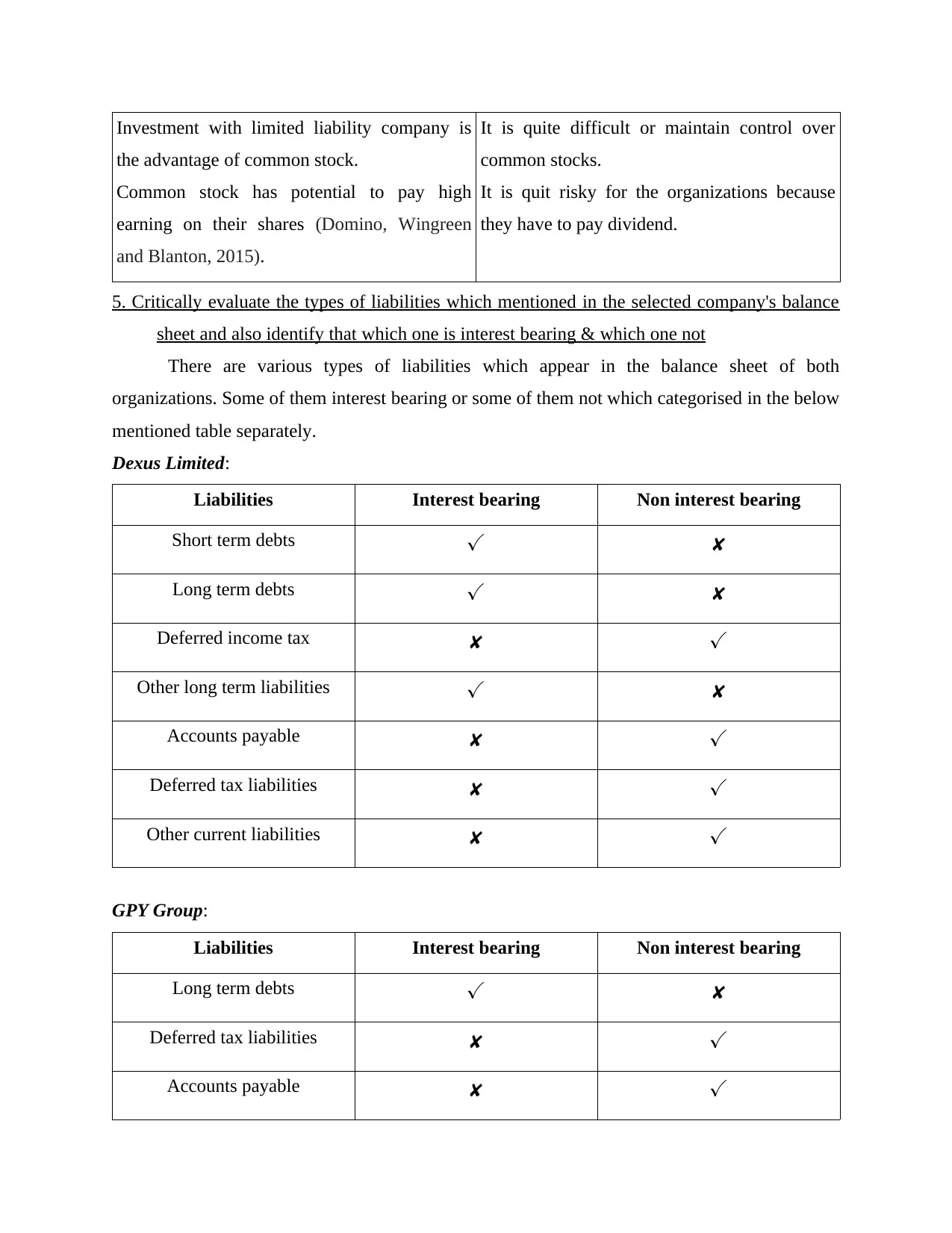

Investment with limited liability company is

the advantage of common stock.

Common stock has potential to pay high

earning on their shares (Domino, Wingreen

and Blanton, 2015).

It is quite difficult or maintain control over

common stocks.

It is quit risky for the organizations because

they have to pay dividend.

5. Critically evaluate the types of liabilities which mentioned in the selected company's balance

sheet and also identify that which one is interest bearing & which one not

There are various types of liabilities which appear in the balance sheet of both

organizations. Some of them interest bearing or some of them not which categorised in the below

mentioned table separately.

Dexus Limited:

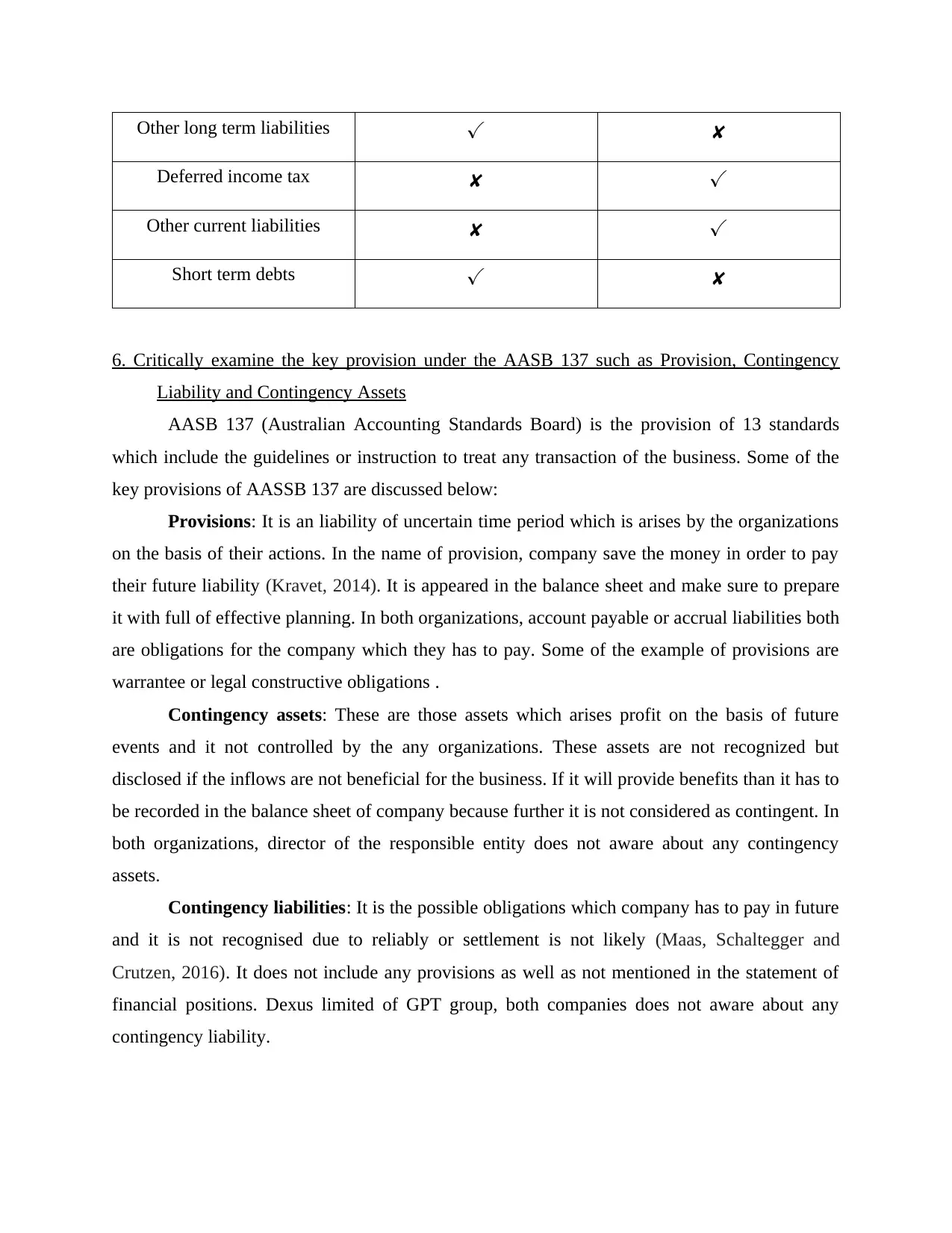

Liabilities Interest bearing Non interest bearing

Short term debts ✓ ✘

Long term debts ✓ ✘

Deferred income tax ✘ ✓

Other long term liabilities ✓ ✘

Accounts payable ✘ ✓

Deferred tax liabilities ✘ ✓

Other current liabilities ✘ ✓

GPY Group:

Liabilities Interest bearing Non interest bearing

Long term debts ✓ ✘

Deferred tax liabilities ✘ ✓

Accounts payable ✘ ✓

the advantage of common stock.

Common stock has potential to pay high

earning on their shares (Domino, Wingreen

and Blanton, 2015).

It is quite difficult or maintain control over

common stocks.

It is quit risky for the organizations because

they have to pay dividend.

5. Critically evaluate the types of liabilities which mentioned in the selected company's balance

sheet and also identify that which one is interest bearing & which one not

There are various types of liabilities which appear in the balance sheet of both

organizations. Some of them interest bearing or some of them not which categorised in the below

mentioned table separately.

Dexus Limited:

Liabilities Interest bearing Non interest bearing

Short term debts ✓ ✘

Long term debts ✓ ✘

Deferred income tax ✘ ✓

Other long term liabilities ✓ ✘

Accounts payable ✘ ✓

Deferred tax liabilities ✘ ✓

Other current liabilities ✘ ✓

GPY Group:

Liabilities Interest bearing Non interest bearing

Long term debts ✓ ✘

Deferred tax liabilities ✘ ✓

Accounts payable ✘ ✓

Other long term liabilities ✓ ✘

Deferred income tax ✘ ✓

Other current liabilities ✘ ✓

Short term debts ✓ ✘

6. Critically examine the key provision under the AASB 137 such as Provision, Contingency

Liability and Contingency Assets

AASB 137 (Australian Accounting Standards Board) is the provision of 13 standards

which include the guidelines or instruction to treat any transaction of the business. Some of the

key provisions of AASSB 137 are discussed below:

Provisions: It is an liability of uncertain time period which is arises by the organizations

on the basis of their actions. In the name of provision, company save the money in order to pay

their future liability (Kravet, 2014). It is appeared in the balance sheet and make sure to prepare

it with full of effective planning. In both organizations, account payable or accrual liabilities both

are obligations for the company which they has to pay. Some of the example of provisions are

warrantee or legal constructive obligations .

Contingency assets: These are those assets which arises profit on the basis of future

events and it not controlled by the any organizations. These assets are not recognized but

disclosed if the inflows are not beneficial for the business. If it will provide benefits than it has to

be recorded in the balance sheet of company because further it is not considered as contingent. In

both organizations, director of the responsible entity does not aware about any contingency

assets.

Contingency liabilities: It is the possible obligations which company has to pay in future

and it is not recognised due to reliably or settlement is not likely (Maas, Schaltegger and

Crutzen, 2016). It does not include any provisions as well as not mentioned in the statement of

financial positions. Dexus limited of GPT group, both companies does not aware about any

contingency liability.

Deferred income tax ✘ ✓

Other current liabilities ✘ ✓

Short term debts ✓ ✘

6. Critically examine the key provision under the AASB 137 such as Provision, Contingency

Liability and Contingency Assets

AASB 137 (Australian Accounting Standards Board) is the provision of 13 standards

which include the guidelines or instruction to treat any transaction of the business. Some of the

key provisions of AASSB 137 are discussed below:

Provisions: It is an liability of uncertain time period which is arises by the organizations

on the basis of their actions. In the name of provision, company save the money in order to pay

their future liability (Kravet, 2014). It is appeared in the balance sheet and make sure to prepare

it with full of effective planning. In both organizations, account payable or accrual liabilities both

are obligations for the company which they has to pay. Some of the example of provisions are

warrantee or legal constructive obligations .

Contingency assets: These are those assets which arises profit on the basis of future

events and it not controlled by the any organizations. These assets are not recognized but

disclosed if the inflows are not beneficial for the business. If it will provide benefits than it has to

be recorded in the balance sheet of company because further it is not considered as contingent. In

both organizations, director of the responsible entity does not aware about any contingency

assets.

Contingency liabilities: It is the possible obligations which company has to pay in future

and it is not recognised due to reliably or settlement is not likely (Maas, Schaltegger and

Crutzen, 2016). It does not include any provisions as well as not mentioned in the statement of

financial positions. Dexus limited of GPT group, both companies does not aware about any

contingency liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7. Evaluate the selected company made any reference regarding AASB 137 in their annual report

AASB 137 is the standard of regarding provision, contingency assets or liability which

followed by the organizations and further perform their activities accordingly. It includes the

various principles and standards which implemented by both organizations to develop

provisions, maintain their assets or liability in well manner.

Contingency liabilities are not similar to the common liability of business. There are two

type of obligations such as possible or present which mentioned below: \

Present obligations: It is the obligations which has proper evidence and it appear in the

balance sheet. Also ensure that, it will meet the criteria which specified in the mentioned

standards (Raiborn and Sivitanides, 2015). Company settle the outflow of resources which

provide economic benefits.

Possible obligations: It is the liability which can be generated in the future and it largely

depend on the present obligations. It provide the economic advantage to make provisions for this.

It is also observed that selected organizations does not have any provisions regarding

contingency liabilities. On the other hand, there is no contingency assets but these selected

organizations made different provisions.

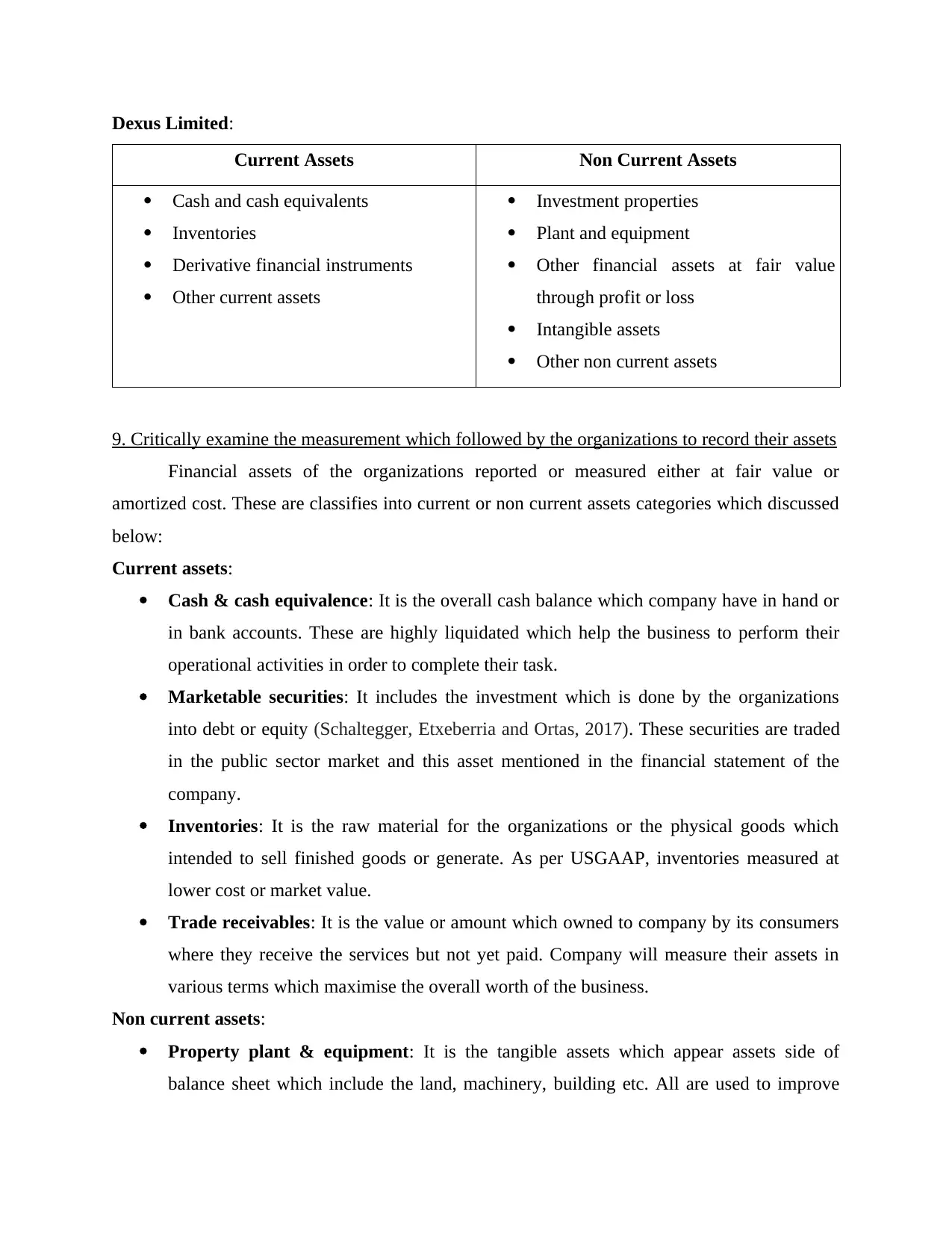

8. Identify different categories of assets which recorded in the company's balance sheet

As per the balance sheet of both organizations such as GPT group of Dexus limited, all

the identified assets mentioned in the below table as per their nature or appear in the financial

statements. There are both companies assets divided into current and non current categories

which mentioned below:

GPT group:

Current Assets Non Current Assets

Cash

Receivables

Inventory

Deferred income tax

Prepaid expenses

Other current assets

Property, plant & equipment

Investments

Intangible assets

Deferred income tax

Other long term assets

AASB 137 is the standard of regarding provision, contingency assets or liability which

followed by the organizations and further perform their activities accordingly. It includes the

various principles and standards which implemented by both organizations to develop

provisions, maintain their assets or liability in well manner.

Contingency liabilities are not similar to the common liability of business. There are two

type of obligations such as possible or present which mentioned below: \

Present obligations: It is the obligations which has proper evidence and it appear in the

balance sheet. Also ensure that, it will meet the criteria which specified in the mentioned

standards (Raiborn and Sivitanides, 2015). Company settle the outflow of resources which

provide economic benefits.

Possible obligations: It is the liability which can be generated in the future and it largely

depend on the present obligations. It provide the economic advantage to make provisions for this.

It is also observed that selected organizations does not have any provisions regarding

contingency liabilities. On the other hand, there is no contingency assets but these selected

organizations made different provisions.

8. Identify different categories of assets which recorded in the company's balance sheet

As per the balance sheet of both organizations such as GPT group of Dexus limited, all

the identified assets mentioned in the below table as per their nature or appear in the financial

statements. There are both companies assets divided into current and non current categories

which mentioned below:

GPT group:

Current Assets Non Current Assets

Cash

Receivables

Inventory

Deferred income tax

Prepaid expenses

Other current assets

Property, plant & equipment

Investments

Intangible assets

Deferred income tax

Other long term assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

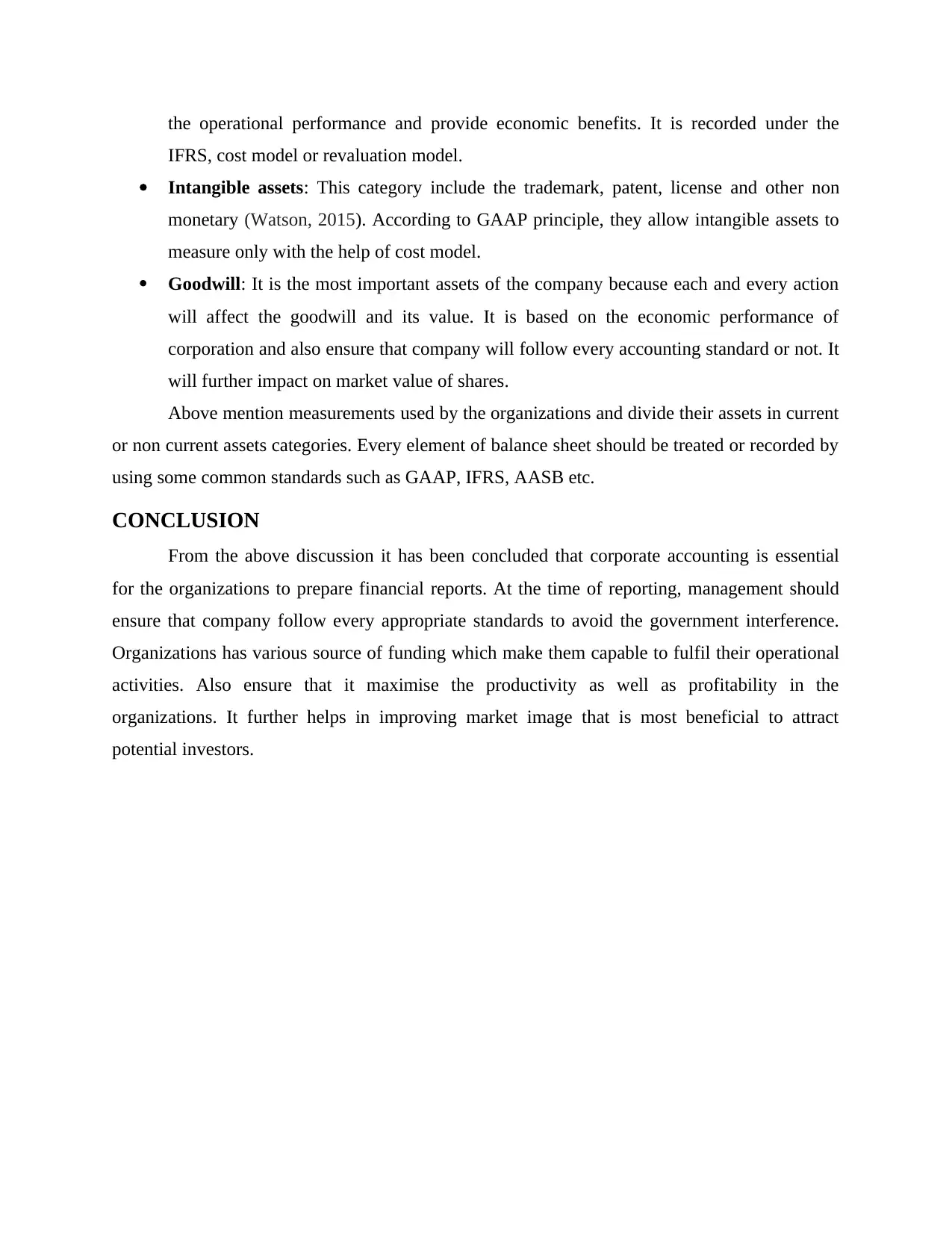

Dexus Limited:

Current Assets Non Current Assets

Cash and cash equivalents

Inventories

Derivative financial instruments

Other current assets

Investment properties

Plant and equipment

Other financial assets at fair value

through profit or loss

Intangible assets

Other non current assets

9. Critically examine the measurement which followed by the organizations to record their assets

Financial assets of the organizations reported or measured either at fair value or

amortized cost. These are classifies into current or non current assets categories which discussed

below:

Current assets:

Cash & cash equivalence: It is the overall cash balance which company have in hand or

in bank accounts. These are highly liquidated which help the business to perform their

operational activities in order to complete their task.

Marketable securities: It includes the investment which is done by the organizations

into debt or equity (Schaltegger, Etxeberria and Ortas, 2017). These securities are traded

in the public sector market and this asset mentioned in the financial statement of the

company.

Inventories: It is the raw material for the organizations or the physical goods which

intended to sell finished goods or generate. As per USGAAP, inventories measured at

lower cost or market value.

Trade receivables: It is the value or amount which owned to company by its consumers

where they receive the services but not yet paid. Company will measure their assets in

various terms which maximise the overall worth of the business.

Non current assets:

Property plant & equipment: It is the tangible assets which appear assets side of

balance sheet which include the land, machinery, building etc. All are used to improve

Current Assets Non Current Assets

Cash and cash equivalents

Inventories

Derivative financial instruments

Other current assets

Investment properties

Plant and equipment

Other financial assets at fair value

through profit or loss

Intangible assets

Other non current assets

9. Critically examine the measurement which followed by the organizations to record their assets

Financial assets of the organizations reported or measured either at fair value or

amortized cost. These are classifies into current or non current assets categories which discussed

below:

Current assets:

Cash & cash equivalence: It is the overall cash balance which company have in hand or

in bank accounts. These are highly liquidated which help the business to perform their

operational activities in order to complete their task.

Marketable securities: It includes the investment which is done by the organizations

into debt or equity (Schaltegger, Etxeberria and Ortas, 2017). These securities are traded

in the public sector market and this asset mentioned in the financial statement of the

company.

Inventories: It is the raw material for the organizations or the physical goods which

intended to sell finished goods or generate. As per USGAAP, inventories measured at

lower cost or market value.

Trade receivables: It is the value or amount which owned to company by its consumers

where they receive the services but not yet paid. Company will measure their assets in

various terms which maximise the overall worth of the business.

Non current assets:

Property plant & equipment: It is the tangible assets which appear assets side of

balance sheet which include the land, machinery, building etc. All are used to improve

the operational performance and provide economic benefits. It is recorded under the

IFRS, cost model or revaluation model.

Intangible assets: This category include the trademark, patent, license and other non

monetary (Watson, 2015). According to GAAP principle, they allow intangible assets to

measure only with the help of cost model.

Goodwill: It is the most important assets of the company because each and every action

will affect the goodwill and its value. It is based on the economic performance of

corporation and also ensure that company will follow every accounting standard or not. It

will further impact on market value of shares.

Above mention measurements used by the organizations and divide their assets in current

or non current assets categories. Every element of balance sheet should be treated or recorded by

using some common standards such as GAAP, IFRS, AASB etc.

CONCLUSION

From the above discussion it has been concluded that corporate accounting is essential

for the organizations to prepare financial reports. At the time of reporting, management should

ensure that company follow every appropriate standards to avoid the government interference.

Organizations has various source of funding which make them capable to fulfil their operational

activities. Also ensure that it maximise the productivity as well as profitability in the

organizations. It further helps in improving market image that is most beneficial to attract

potential investors.

IFRS, cost model or revaluation model.

Intangible assets: This category include the trademark, patent, license and other non

monetary (Watson, 2015). According to GAAP principle, they allow intangible assets to

measure only with the help of cost model.

Goodwill: It is the most important assets of the company because each and every action

will affect the goodwill and its value. It is based on the economic performance of

corporation and also ensure that company will follow every accounting standard or not. It

will further impact on market value of shares.

Above mention measurements used by the organizations and divide their assets in current

or non current assets categories. Every element of balance sheet should be treated or recorded by

using some common standards such as GAAP, IFRS, AASB etc.

CONCLUSION

From the above discussion it has been concluded that corporate accounting is essential

for the organizations to prepare financial reports. At the time of reporting, management should

ensure that company follow every appropriate standards to avoid the government interference.

Organizations has various source of funding which make them capable to fulfil their operational

activities. Also ensure that it maximise the productivity as well as profitability in the

organizations. It further helps in improving market image that is most beneficial to attract

potential investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.