Analyzing Deferred Tax Assets in Australian Financial Reporting

VerifiedAdded on 2020/05/28

|12

|3009

|48

AI Summary

The assignment delves into the nuances of deferred tax assets as outlined by Australian Accounting Standards (AASB) 112 and 119. It explores the recognition and measurement of such assets, particularly concerning employee benefits. By examining various aspects like temporary differenc...

Running head: CORPORATE ACCOUNTING

Corporate Accounting

University Name

Student Name

Authors’ Note

Corporate Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2CORPORATE ACCOUNTING

Table of Contents

Solution to Question i.................................................................................................................2

Answer to Question ii.................................................................................................................3

Answer to Question iii...............................................................................................................4

Solution to Question iv...............................................................................................................7

Answer to Question v:................................................................................................................8

Solution to Question vi...............................................................................................................9

Solution to Question vii...........................................................................................................10

References................................................................................................................................11

Table of Contents

Solution to Question i.................................................................................................................2

Answer to Question ii.................................................................................................................3

Answer to Question iii...............................................................................................................4

Solution to Question iv...............................................................................................................7

Answer to Question v:................................................................................................................8

Solution to Question vi...............................................................................................................9

Solution to Question vii...........................................................................................................10

References................................................................................................................................11

3CORPORATE ACCOUNTING

Solution to Question i

List of items of equity

The annual report of the firm BSA limited reflects the fact that the equity of the firm consists

of the items issued capital, reserves, profit reserve as well as accumulated losses. The issued

capital stands at $97592000 during 2016 and has the remained the same as compared to 2015.

The item “reserves” listed under equity of BSA Limited is recorded to be $1410000 for both

the year 2015 and 2016. The accumulated losses of the firm are recorded to be ($63024000)

while it increased to ($65243000). There are important items that are positioned under issued

capital are necessarily ordinary shares that a specific corporation issues, together with

specified costs that are associated to share issue plus income tax linked share issue (Tran,

2015). According to the balance sheet statement of the corporation BSA Limited, there are

four different items that are clubbed under the equity items namely the issued capital,

reserves, accumulated losses and the profit reserve of the firm. According to the annual report

of the corporation, the issued capital can be witnessed to be $97592000 during the financial

year 2016 in comparison to the figure registered to be $97592000 during the financial year

2015. Further, under the concept of financial accounting, principally reserves can be

considered as a specific component of equity of the firm BSA Limited. For itself, it can be

indicated as a supplementary amount besides fundamental capital share. The yearly

pronouncement of BSA shows that reserves stand at $1410000 in comparison to figure

documented year ago and that was equal to $1410000. Again, the consequent item stated

under the head equity of the corporation BSA Limited is essentially retained income.

Fundamentally, this stands for the overall profit/losses of the firm mainly enumerated since

the time of arrangement reduced by the dividend pay-out to firm’s shareholders (Tran, 2015).

Solution to Question i

List of items of equity

The annual report of the firm BSA limited reflects the fact that the equity of the firm consists

of the items issued capital, reserves, profit reserve as well as accumulated losses. The issued

capital stands at $97592000 during 2016 and has the remained the same as compared to 2015.

The item “reserves” listed under equity of BSA Limited is recorded to be $1410000 for both

the year 2015 and 2016. The accumulated losses of the firm are recorded to be ($63024000)

while it increased to ($65243000). There are important items that are positioned under issued

capital are necessarily ordinary shares that a specific corporation issues, together with

specified costs that are associated to share issue plus income tax linked share issue (Tran,

2015). According to the balance sheet statement of the corporation BSA Limited, there are

four different items that are clubbed under the equity items namely the issued capital,

reserves, accumulated losses and the profit reserve of the firm. According to the annual report

of the corporation, the issued capital can be witnessed to be $97592000 during the financial

year 2016 in comparison to the figure registered to be $97592000 during the financial year

2015. Further, under the concept of financial accounting, principally reserves can be

considered as a specific component of equity of the firm BSA Limited. For itself, it can be

indicated as a supplementary amount besides fundamental capital share. The yearly

pronouncement of BSA shows that reserves stand at $1410000 in comparison to figure

documented year ago and that was equal to $1410000. Again, the consequent item stated

under the head equity of the corporation BSA Limited is essentially retained income.

Fundamentally, this stands for the overall profit/losses of the firm mainly enumerated since

the time of arrangement reduced by the dividend pay-out to firm’s shareholders (Tran, 2015).

You're viewing a preview

Unlock full access by subscribing today!

4CORPORATE ACCOUNTING

Answer to Question ii

Several categories of expends are incurred by corporations that comprises of selling expends

and administrative expends. In essence, one of these types of expenditures include tax

expends. The financial statement of the firm reflects loss of amount $ (3014000) incurred

from continuing actions from particularly income tax. In addition, tax expends can be

considered as a major responsibility of the business concern owing to the federal, state along

with municipal governing bodies of the country. The calculation of tax expends is executed

by the multiplying the suitable tax of the corporation by the company’s earnings before taxes

after specifically factoring specific components namely non-deductible accounts, tax

assets/liabilities (Tran, 2015). Fundamentally, there subsists no exception even in case of the

business concern BSA Limited since the business concern incurs certain tax expends. As per

the rules of the Australian taxation regulations, the corporate tax rate for specifically

Australian corporations is approximately 30%. Based on the tax rate of approximately 30%,

the entire tax expenditure of the corporation BSA Limited is around $795000 recorded during

the financial year 2016. In essence, this can be regarded to be main tax expenditure of the

corporation for 2016. Nonetheless, this can be hereby observed that there has been decline in

the tax expenditure on the whole due to the reduction in overall income of the firm during the

year 2016 in comparison to the year 2015.

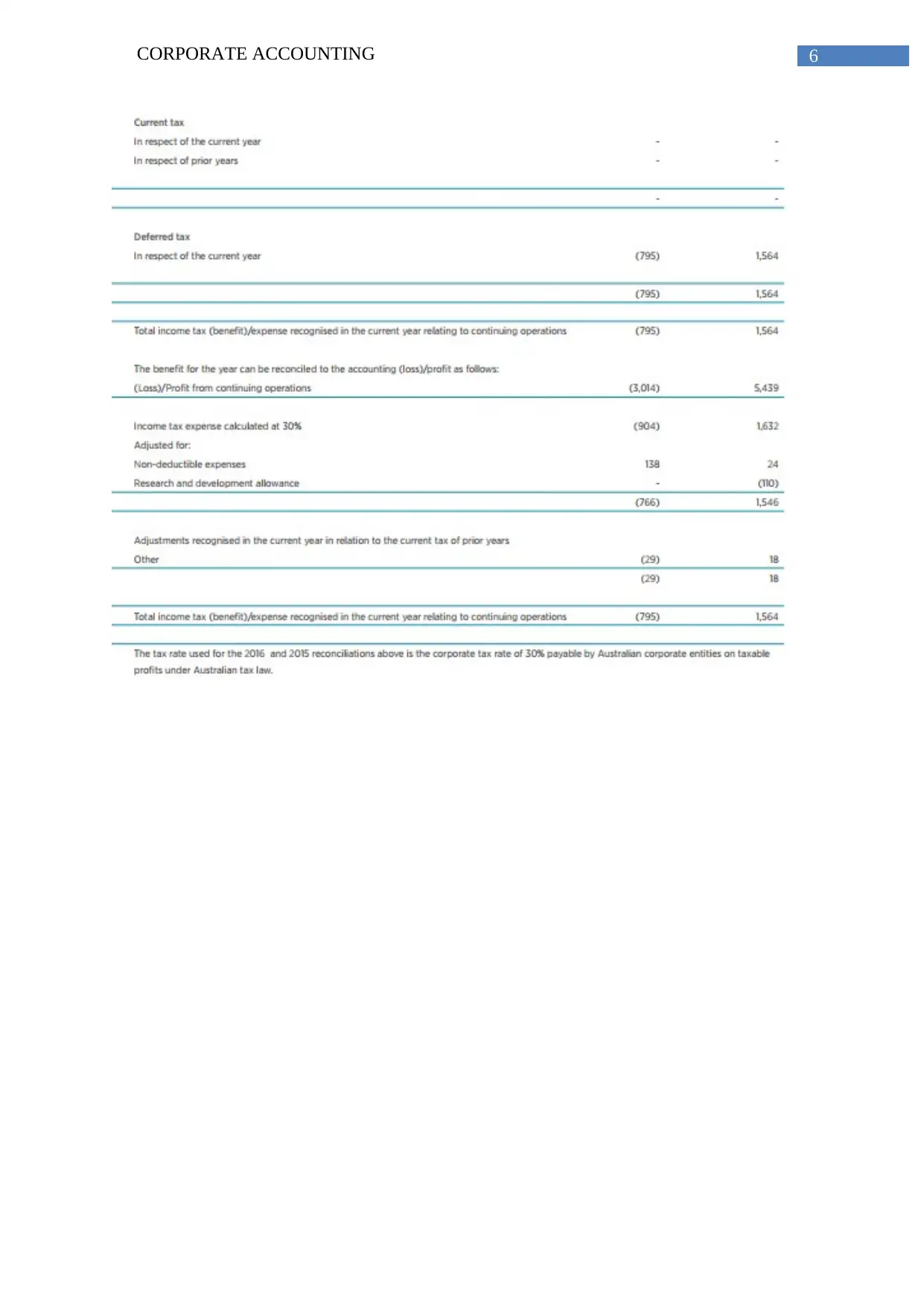

Answer to Question iii

It can be hereby stated that the business corporation BSA Limited has recorded a loss

amounting to $3014000 during the financial year 2016. Nevertheless, profit was registered to

be around $5449000 during the financial 2015. The financial statement replicates the overall

advantage for a specified time period that can again be reconciled and has documented a

loss/profit from continuing operations of the firm (Bentwood & Lee, 2012). However, that

Answer to Question ii

Several categories of expends are incurred by corporations that comprises of selling expends

and administrative expends. In essence, one of these types of expenditures include tax

expends. The financial statement of the firm reflects loss of amount $ (3014000) incurred

from continuing actions from particularly income tax. In addition, tax expends can be

considered as a major responsibility of the business concern owing to the federal, state along

with municipal governing bodies of the country. The calculation of tax expends is executed

by the multiplying the suitable tax of the corporation by the company’s earnings before taxes

after specifically factoring specific components namely non-deductible accounts, tax

assets/liabilities (Tran, 2015). Fundamentally, there subsists no exception even in case of the

business concern BSA Limited since the business concern incurs certain tax expends. As per

the rules of the Australian taxation regulations, the corporate tax rate for specifically

Australian corporations is approximately 30%. Based on the tax rate of approximately 30%,

the entire tax expenditure of the corporation BSA Limited is around $795000 recorded during

the financial year 2016. In essence, this can be regarded to be main tax expenditure of the

corporation for 2016. Nonetheless, this can be hereby observed that there has been decline in

the tax expenditure on the whole due to the reduction in overall income of the firm during the

year 2016 in comparison to the year 2015.

Answer to Question iii

It can be hereby stated that the business corporation BSA Limited has recorded a loss

amounting to $3014000 during the financial year 2016. Nevertheless, profit was registered to

be around $5449000 during the financial 2015. The financial statement replicates the overall

advantage for a specified time period that can again be reconciled and has documented a

loss/profit from continuing operations of the firm (Bentwood & Lee, 2012). However, that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5CORPORATE ACCOUNTING

can be seen to be at ($3014000) in 2016 whereas it was documented to be ($5439000) in

2015. In addition to this, the annual report of the corporation states that the income tax

expenditure of the corporation calculated at the rate 30% during the financial year 2016.

Essentially using 30% tax rate, the overall income tax expenditure of the firm BSA Limited

stands at ($904000) during the financial year 2016 and around $1632 during the financial

year 2015.

Principally, there are certain specified items that can be incorporated or barred from the

expenditure on tax at initial period. In actual fact, BSA Limited’s income tax expenditure

calculated at the specific rate of 30% amounts to ($904000) during the year 2016 in

comparison to the year ago figure registered to be $1632000. Furthermore, a distinct variation

in the tax expend of the firm can be witnessed in the annual financial statement of the

business concern (Hanlon et al., 2014). The specified financial items can be considered as the

causes of differences in the overall tax expenditure. In particular, in this present case of BSA

Limited, there subsist diverse financial items that have additional influence on the overall tax

expenditure of the firm. According to the yearly pecuniary reports of the firm, the most

important item is particularly the non-deductible expends that again can be evaluated for

determining taxable gains. In essence, the item that has the need to be appropriately adjusted

is the allowance for firm’s research and development (R&D) (Jin et al., 2015). In addition to

this, adjustments can also be identified in the period in association to the present tax of

previous years and this necessarily stands at ($29000) during the year 2016 and ($18000)

during the year 2015. Evaluation of the financial assertions of the corporation thus reflects

the overall income tax otherwise expends recognized during the current years related to

continuing operations that essentially remains at ($766000), whilst the same is recorded to be

$1546000 during the financial year 2015.

can be seen to be at ($3014000) in 2016 whereas it was documented to be ($5439000) in

2015. In addition to this, the annual report of the corporation states that the income tax

expenditure of the corporation calculated at the rate 30% during the financial year 2016.

Essentially using 30% tax rate, the overall income tax expenditure of the firm BSA Limited

stands at ($904000) during the financial year 2016 and around $1632 during the financial

year 2015.

Principally, there are certain specified items that can be incorporated or barred from the

expenditure on tax at initial period. In actual fact, BSA Limited’s income tax expenditure

calculated at the specific rate of 30% amounts to ($904000) during the year 2016 in

comparison to the year ago figure registered to be $1632000. Furthermore, a distinct variation

in the tax expend of the firm can be witnessed in the annual financial statement of the

business concern (Hanlon et al., 2014). The specified financial items can be considered as the

causes of differences in the overall tax expenditure. In particular, in this present case of BSA

Limited, there subsist diverse financial items that have additional influence on the overall tax

expenditure of the firm. According to the yearly pecuniary reports of the firm, the most

important item is particularly the non-deductible expends that again can be evaluated for

determining taxable gains. In essence, the item that has the need to be appropriately adjusted

is the allowance for firm’s research and development (R&D) (Jin et al., 2015). In addition to

this, adjustments can also be identified in the period in association to the present tax of

previous years and this necessarily stands at ($29000) during the year 2016 and ($18000)

during the year 2015. Evaluation of the financial assertions of the corporation thus reflects

the overall income tax otherwise expends recognized during the current years related to

continuing operations that essentially remains at ($766000), whilst the same is recorded to be

$1546000 during the financial year 2015.

6CORPORATE ACCOUNTING

You're viewing a preview

Unlock full access by subscribing today!

7CORPORATE ACCOUNTING

Answer iv

As rightly put forward by Burkhauser et al., (2015), firm’s tax assets otherwise liabilities

(indicating the deferred) can be referred to as key themes of the tax procedure of business

concerns. Nevertheless, corporations BSA Limited, it can be stated corporation’s tax asset of

the firm that is the deferred ones stands at $7795000 in 2016. In addition to this, taxable

variances correlated to firm’s investments can be observed mainly in joint ventures.

Burkhauser et al., (2015) suggests that deferred tax assets refer to a particular circumstance in

which the companies pay out taxes in advance that is calculated on firm’s particular financial

assets. In addition to this, contrarily, income tax liabilities (deferred) replicate a particular

state where differences can be witnessed in specifically firm’s profit and tax carrying value of

corporations. As per accounting regulations and associated accounting treatment rules there

are specified causes for enhancement of tax, firm’s assets otherwise liabilities (referring to

the deferred ones). Consequently, excess pay off for depreciation along with taxable rate of

depreciation, the firm BSA Limited shall certainly not have to make disbursements for

supplementary tax in the following year. Therefore, this can be considered as an asset.

Nevertheless, for tax assets of BSA Limited (deferred), variation in depreciation plus tax rate

associated might possibly lead to surplus pay-out (Richardson et al., 2015). The surplus pay

out for depreciation is primarily owing to variation in depreciation along with tax rate

associated to depreciation. Due to deferred tax liabilities of corporation, this might have

occurred that owing to temporary differences in profits of the firm, the firm had the need to

provide less payment for calculated taxes in the current period (Badenhorst & Ferreira, 2016).

Thus, it is imperative for the firm to make payments in the following years.

Answer iv

As rightly put forward by Burkhauser et al., (2015), firm’s tax assets otherwise liabilities

(indicating the deferred) can be referred to as key themes of the tax procedure of business

concerns. Nevertheless, corporations BSA Limited, it can be stated corporation’s tax asset of

the firm that is the deferred ones stands at $7795000 in 2016. In addition to this, taxable

variances correlated to firm’s investments can be observed mainly in joint ventures.

Burkhauser et al., (2015) suggests that deferred tax assets refer to a particular circumstance in

which the companies pay out taxes in advance that is calculated on firm’s particular financial

assets. In addition to this, contrarily, income tax liabilities (deferred) replicate a particular

state where differences can be witnessed in specifically firm’s profit and tax carrying value of

corporations. As per accounting regulations and associated accounting treatment rules there

are specified causes for enhancement of tax, firm’s assets otherwise liabilities (referring to

the deferred ones). Consequently, excess pay off for depreciation along with taxable rate of

depreciation, the firm BSA Limited shall certainly not have to make disbursements for

supplementary tax in the following year. Therefore, this can be considered as an asset.

Nevertheless, for tax assets of BSA Limited (deferred), variation in depreciation plus tax rate

associated might possibly lead to surplus pay-out (Richardson et al., 2015). The surplus pay

out for depreciation is primarily owing to variation in depreciation along with tax rate

associated to depreciation. Due to deferred tax liabilities of corporation, this might have

occurred that owing to temporary differences in profits of the firm, the firm had the need to

provide less payment for calculated taxes in the current period (Badenhorst & Ferreira, 2016).

Thus, it is imperative for the firm to make payments in the following years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CORPORATE ACCOUNTING

Answer v:

Present tax asset otherwise income tax that is necessarily payable can be considered as a

significant feature of the business concern. As per the annual report of the firm BSA limited,

the business concern has explained as regards the present tax assets. According to the

financial pronouncements of the corporation BSA Limited, It can thus be mentioned that the

firm has not yet pronounced any specific amount for specifically the current tax assets during

FY 2016. Nonetheless, in the year 2016, the company registered $795000 as corporation’s tax

assets (deferred) in FY 2016 and $1546000 in the FY2015.

Subsistence of a fundamental variance in income tax pay-out plus income tax that BSA needs

to disburse can be observed. However, the particular cause behind that might be the existence

of the specified gap (King, 2016). The subsistence of firm’s tax assets (referring to deferred)

might be cited as the probable reason. In itself, variances that exist between rules stipulated

for managerial accounting and rules of treatment of firm’s taxes can also be stated as the

fuelling reason of this observed aspect. However, there are several examples in which

business concern pays off additional amount of tax assets as compared to tax assets (deferred)

that subsequently lead to the difference. In this case, the example of depreciation can be

mentioned. Differences for particularly depreciation can necessarily be witnessed under the

context of financial accounting as well as tax accounting for different rate of depreciation

(Taylor & Richardson, 2014). Hence, the entire amount of depreciation that is payable can

one hand be augmented and on the other hand be lessened.

Answer vi

The corporation under consideration BSA Limited essentially pays out tax as can be observed

from firm’s income declaration and cash flow pronouncements. According to the income

statement, the firm replicates the whole amount of tax expenditure utilizing tax rate of

Answer v:

Present tax asset otherwise income tax that is necessarily payable can be considered as a

significant feature of the business concern. As per the annual report of the firm BSA limited,

the business concern has explained as regards the present tax assets. According to the

financial pronouncements of the corporation BSA Limited, It can thus be mentioned that the

firm has not yet pronounced any specific amount for specifically the current tax assets during

FY 2016. Nonetheless, in the year 2016, the company registered $795000 as corporation’s tax

assets (deferred) in FY 2016 and $1546000 in the FY2015.

Subsistence of a fundamental variance in income tax pay-out plus income tax that BSA needs

to disburse can be observed. However, the particular cause behind that might be the existence

of the specified gap (King, 2016). The subsistence of firm’s tax assets (referring to deferred)

might be cited as the probable reason. In itself, variances that exist between rules stipulated

for managerial accounting and rules of treatment of firm’s taxes can also be stated as the

fuelling reason of this observed aspect. However, there are several examples in which

business concern pays off additional amount of tax assets as compared to tax assets (deferred)

that subsequently lead to the difference. In this case, the example of depreciation can be

mentioned. Differences for particularly depreciation can necessarily be witnessed under the

context of financial accounting as well as tax accounting for different rate of depreciation

(Taylor & Richardson, 2014). Hence, the entire amount of depreciation that is payable can

one hand be augmented and on the other hand be lessened.

Answer vi

The corporation under consideration BSA Limited essentially pays out tax as can be observed

from firm’s income declaration and cash flow pronouncements. According to the income

statement, the firm replicates the whole amount of tax expenditure utilizing tax rate of

9CORPORATE ACCOUNTING

specifically 30% on the profit gained from different continuing operations. In essence, firm’s

income tax expends replicate the entire sum of the payable present tax along with the

deferred tax (Detzen et al., 2016). Essentially, the tax amount that the firm has the need to

pay depends on generated taxable profit for specified time. However, it can be observed in

the given case that the taxable profit is different from the gains and this can be seen in the

profit/loss pronouncement of the firm. Particularly, this is due to diverse items of income in

addition to expends that are essentially taxable or else deductible in specific time periods

together with diverse other items that are not taxable else wise deductible. Thus, tax

expenditure is said to be mentioned under BSA’s flow of cash from different functioning.

Particularly, under this specific division of cash flow, specific items of firm’s income

assertion are treated in a different manner. This necessarily means that specific alterations

take place in current assets/liabilities of the corporation (Jones, 2017). According to the cash

flow statement of the firm, specific reductions in particular components of tax expenditure

has been stated that indicates towards cash utilization. Particularly, this refers to the fact that

certain elements of tax expenditure have been closed before considering consolidated

statement. It is due to this reason; differences on tax expenditure can be witnessed in the

income statement along with cash flow statement.

specifically 30% on the profit gained from different continuing operations. In essence, firm’s

income tax expends replicate the entire sum of the payable present tax along with the

deferred tax (Detzen et al., 2016). Essentially, the tax amount that the firm has the need to

pay depends on generated taxable profit for specified time. However, it can be observed in

the given case that the taxable profit is different from the gains and this can be seen in the

profit/loss pronouncement of the firm. Particularly, this is due to diverse items of income in

addition to expends that are essentially taxable or else deductible in specific time periods

together with diverse other items that are not taxable else wise deductible. Thus, tax

expenditure is said to be mentioned under BSA’s flow of cash from different functioning.

Particularly, under this specific division of cash flow, specific items of firm’s income

assertion are treated in a different manner. This necessarily means that specific alterations

take place in current assets/liabilities of the corporation (Jones, 2017). According to the cash

flow statement of the firm, specific reductions in particular components of tax expenditure

has been stated that indicates towards cash utilization. Particularly, this refers to the fact that

certain elements of tax expenditure have been closed before considering consolidated

statement. It is due to this reason; differences on tax expenditure can be witnessed in the

income statement along with cash flow statement.

You're viewing a preview

Unlock full access by subscribing today!

10CORPORATE ACCOUNTING

Answer to vii

The company BSA Limited has implemented and executed the process by sticking to the

pertinent regulations along with stipulations of particularly Australian Taxation Regulation.

Furthermore, the company BSA Limited has arranged and presented all the requisite

explanations along with rationalizations of diverse taxation issues namely tax rate, different

deferred tax assets/liabilities along with the present taxation accountabilities. Tax accounting

system as can be observed from the annual report of the firm helps in mentioning that there

lie no doubt or confusion in the scheme of tax accounting (Cardwell, 2015). Nevertheless,

there also exist certain important factors in the process of treatment of taxation of the firm

BSA Limited. According to the annual pecuniary declarations of the firm BSA Limited,

income tax expends represent the entire sum of the tax payable in the present period in

addition to deferred tax. However, for the present tax that is necessarily payable by the

corporation is primarily based on the enumerated taxable profit for a specific year.

Nonetheless, the taxable profit varies as has been reflected in the consolidated statement of

the business entity, mainly profit/loss along with comprehensive earning due to diverse

income items as well as expenditures that are essentially taxable or else deductible (Belz et

al., 2016). Basically, the deferred tax is essentially registered on the temporary differences

that subsist between carrying amounts of specifically asset/liabilities reflected in the

consolidated financial declarations. Tax assets otherwise liabilities (referring to the deferred

ones) can necessarily be associated to BSA Limited’s employee benefits. In addition to this,

this can be recognized and enumerated according to rules mentioned under AASB 112 for

enumeration of firm’s taxes as well as AASB 119 for presentation of benefits made available

to employees (Aasb.gov.au., 2018).

Answer to vii

The company BSA Limited has implemented and executed the process by sticking to the

pertinent regulations along with stipulations of particularly Australian Taxation Regulation.

Furthermore, the company BSA Limited has arranged and presented all the requisite

explanations along with rationalizations of diverse taxation issues namely tax rate, different

deferred tax assets/liabilities along with the present taxation accountabilities. Tax accounting

system as can be observed from the annual report of the firm helps in mentioning that there

lie no doubt or confusion in the scheme of tax accounting (Cardwell, 2015). Nevertheless,

there also exist certain important factors in the process of treatment of taxation of the firm

BSA Limited. According to the annual pecuniary declarations of the firm BSA Limited,

income tax expends represent the entire sum of the tax payable in the present period in

addition to deferred tax. However, for the present tax that is necessarily payable by the

corporation is primarily based on the enumerated taxable profit for a specific year.

Nonetheless, the taxable profit varies as has been reflected in the consolidated statement of

the business entity, mainly profit/loss along with comprehensive earning due to diverse

income items as well as expenditures that are essentially taxable or else deductible (Belz et

al., 2016). Basically, the deferred tax is essentially registered on the temporary differences

that subsist between carrying amounts of specifically asset/liabilities reflected in the

consolidated financial declarations. Tax assets otherwise liabilities (referring to the deferred

ones) can necessarily be associated to BSA Limited’s employee benefits. In addition to this,

this can be recognized and enumerated according to rules mentioned under AASB 112 for

enumeration of firm’s taxes as well as AASB 119 for presentation of benefits made available

to employees (Aasb.gov.au., 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11CORPORATE ACCOUNTING

References

Australian Accounting Standards Board (AASB) - Home. (2018). Aasb.gov.au. Retrieved 24

January 2018, from http://www.aasb.gov.au/

Badenhorst, W. M., & Ferreira, P. H. (2016). The Financial Crisis and the Value‐relevance of

Recognised Deferred Tax Assets. Australian Accounting Review, 26(3), 291-300.

Belz, T., von Hagen, D., & Steffens, C. (2016). Taxes and firm size: political cost or political

power?.

Bentwood, S., & Lee, P. (2012). Benchmark management during Australia's transition to

international accounting standards. Abacus, 48(1), 59-85.

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

181-205.

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

181-205.

Cardwell, J. (2015). Alternative assets insights: A new tax system for managed investment

trusts. Taxation in Australia, 50(1), 46.

Detzen, D., Stork genannt Wersborg, T., & Zülch, H. (2016). Impairment of Goodwill and

Deferred Taxes Under IFRS. Australian Accounting Review, 26(3), 301-311.

Hanlon, D., Navissi, F., & Soepriyanto, G. (2014). The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2),

87-99.

References

Australian Accounting Standards Board (AASB) - Home. (2018). Aasb.gov.au. Retrieved 24

January 2018, from http://www.aasb.gov.au/

Badenhorst, W. M., & Ferreira, P. H. (2016). The Financial Crisis and the Value‐relevance of

Recognised Deferred Tax Assets. Australian Accounting Review, 26(3), 291-300.

Belz, T., von Hagen, D., & Steffens, C. (2016). Taxes and firm size: political cost or political

power?.

Bentwood, S., & Lee, P. (2012). Benchmark management during Australia's transition to

international accounting standards. Abacus, 48(1), 59-85.

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

181-205.

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

181-205.

Cardwell, J. (2015). Alternative assets insights: A new tax system for managed investment

trusts. Taxation in Australia, 50(1), 46.

Detzen, D., Stork genannt Wersborg, T., & Zülch, H. (2016). Impairment of Goodwill and

Deferred Taxes Under IFRS. Australian Accounting Review, 26(3), 301-311.

Hanlon, D., Navissi, F., & Soepriyanto, G. (2014). The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2),

87-99.

12CORPORATE ACCOUNTING

Jin, K., Shan, Y., & Taylor, S. (2015). Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

90-107.

Jones, D. (2017). Mid market focus: Income or capital?: Taxpayer draws a blank. Taxation in

Australia, 51(7), 357.

King, A. (2016). Mid market focus: The new attribution tax regime for MITs: Part

1. Taxation in Australia, 50(10), 590.

Richardson, G., Taylor, G., & Lanis, R. (2015). The impact of financial distress on corporate

tax avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, 44-53.

Taylor, G., & Richardson, G. (2014). Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting &

Economics, 10(1), 1-15.

Tran, A. (2015). Can Taxable Income Be Estimated from Financial Reports of Listed

Companies in Australia. Austl. Tax F., 30, 569.

Jin, K., Shan, Y., & Taylor, S. (2015). Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

90-107.

Jones, D. (2017). Mid market focus: Income or capital?: Taxpayer draws a blank. Taxation in

Australia, 51(7), 357.

King, A. (2016). Mid market focus: The new attribution tax regime for MITs: Part

1. Taxation in Australia, 50(10), 590.

Richardson, G., Taylor, G., & Lanis, R. (2015). The impact of financial distress on corporate

tax avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, 44-53.

Taylor, G., & Richardson, G. (2014). Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting &

Economics, 10(1), 1-15.

Tran, A. (2015). Can Taxable Income Be Estimated from Financial Reports of Listed

Companies in Australia. Austl. Tax F., 30, 569.

You're viewing a preview

Unlock full access by subscribing today!

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.