Corporate Accounting Report: Income Statement, Balance Sheet Analysis

VerifiedAdded on 2020/07/23

|9

|1211

|32

Report

AI Summary

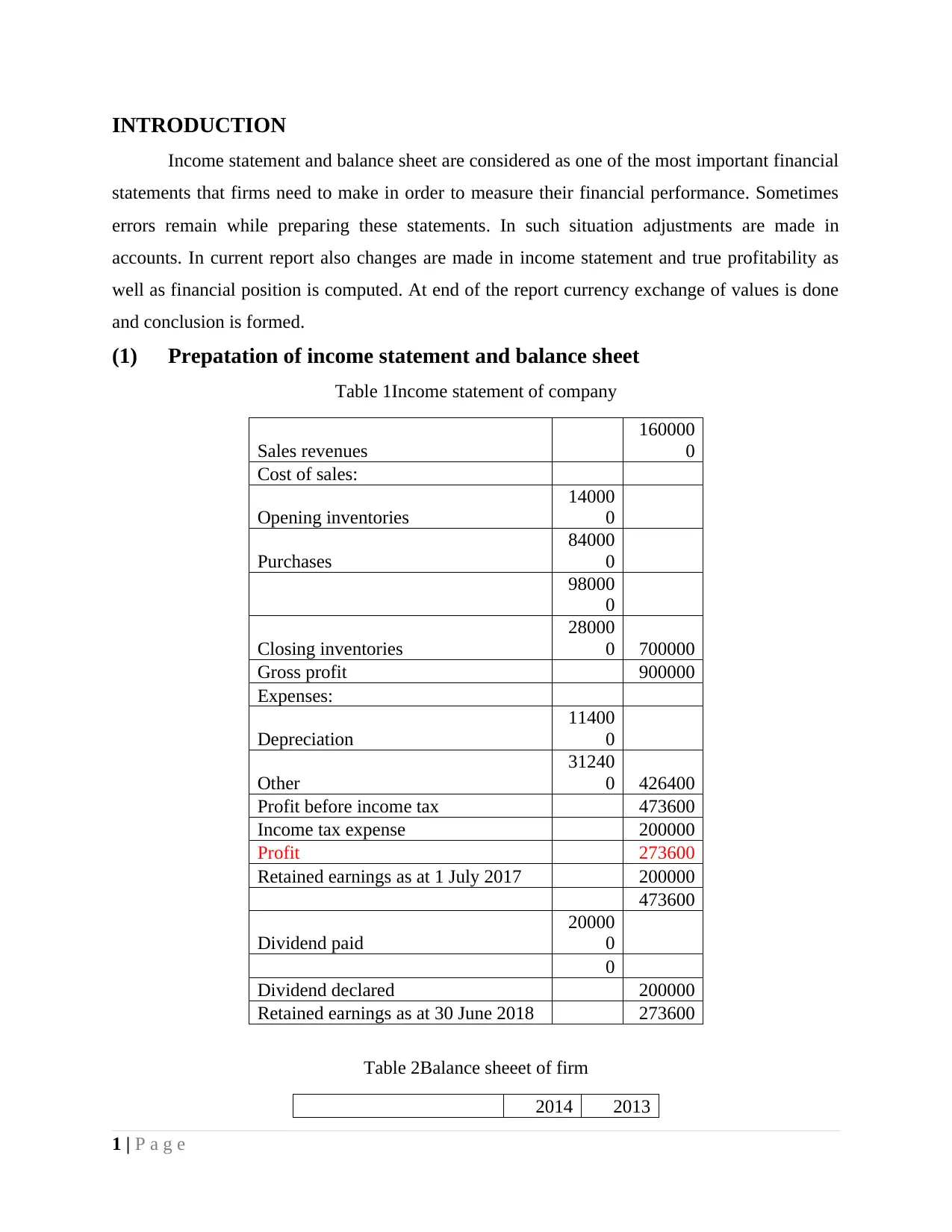

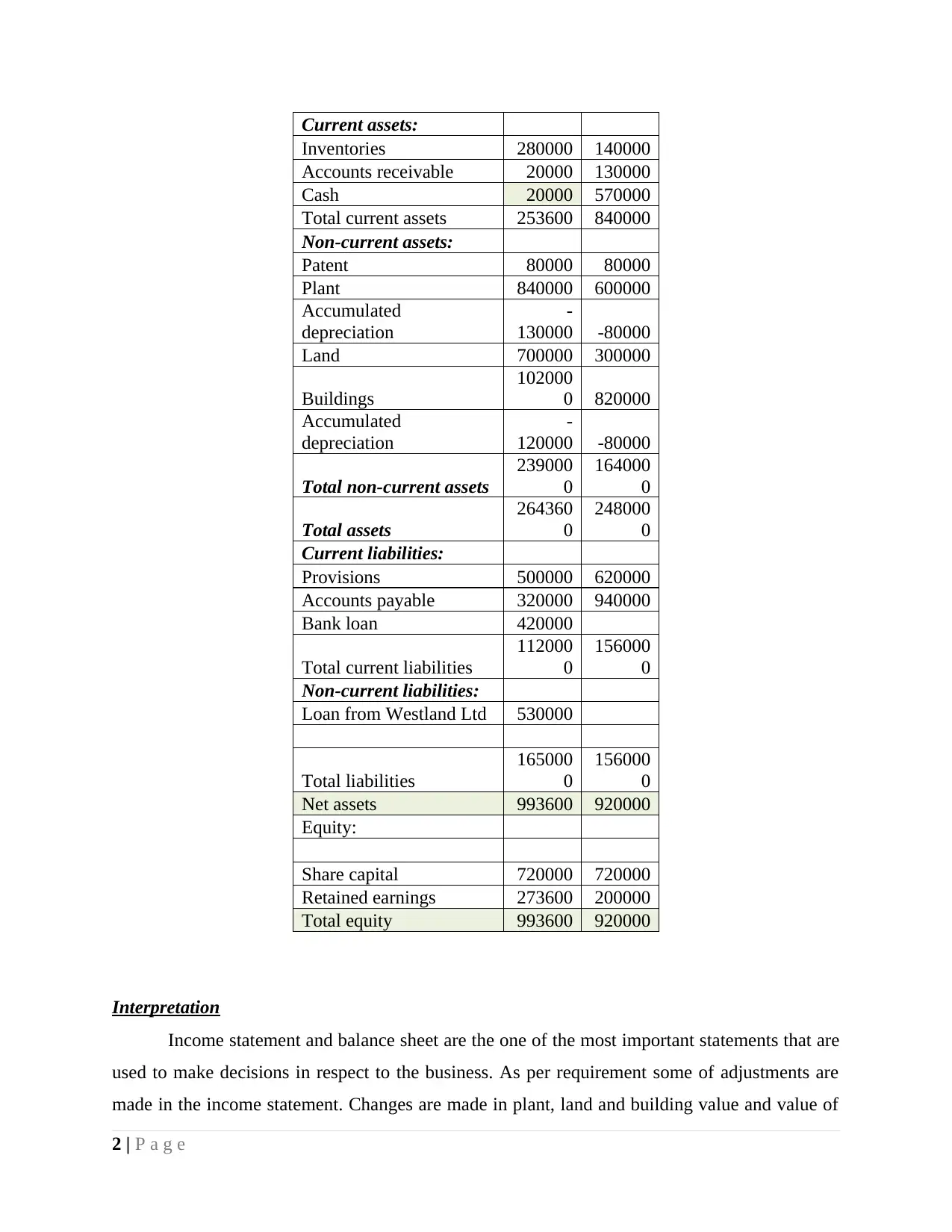

This report provides an analysis of corporate accounting practices, focusing on the preparation and interpretation of income statements and balance sheets. It begins with the initial preparation of these financial statements, highlighting adjustments made to reflect true profitability and financial position. The report then delves into the currency exchange of values, specifically converting financial data into AUD, and explains the methodologies used. Key adjustments include modifications to asset values, the handling of bank loans and interest, and the correction of dividend appropriations. The conclusion emphasizes the relationship between assets, liabilities, and shareholder equity. The report includes detailed tables illustrating the income statement and balance sheet, both before and after currency conversion, along with interpretations of the data and references to relevant accounting literature and online resources. The report demonstrates the importance of accurate financial reporting and the impact of currency fluctuations on financial statements.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.