Corporate Accounting: Financial Reporting Regulation, AASB Participation in Setting Global Standards, and Equity Analysis

VerifiedAI Summary

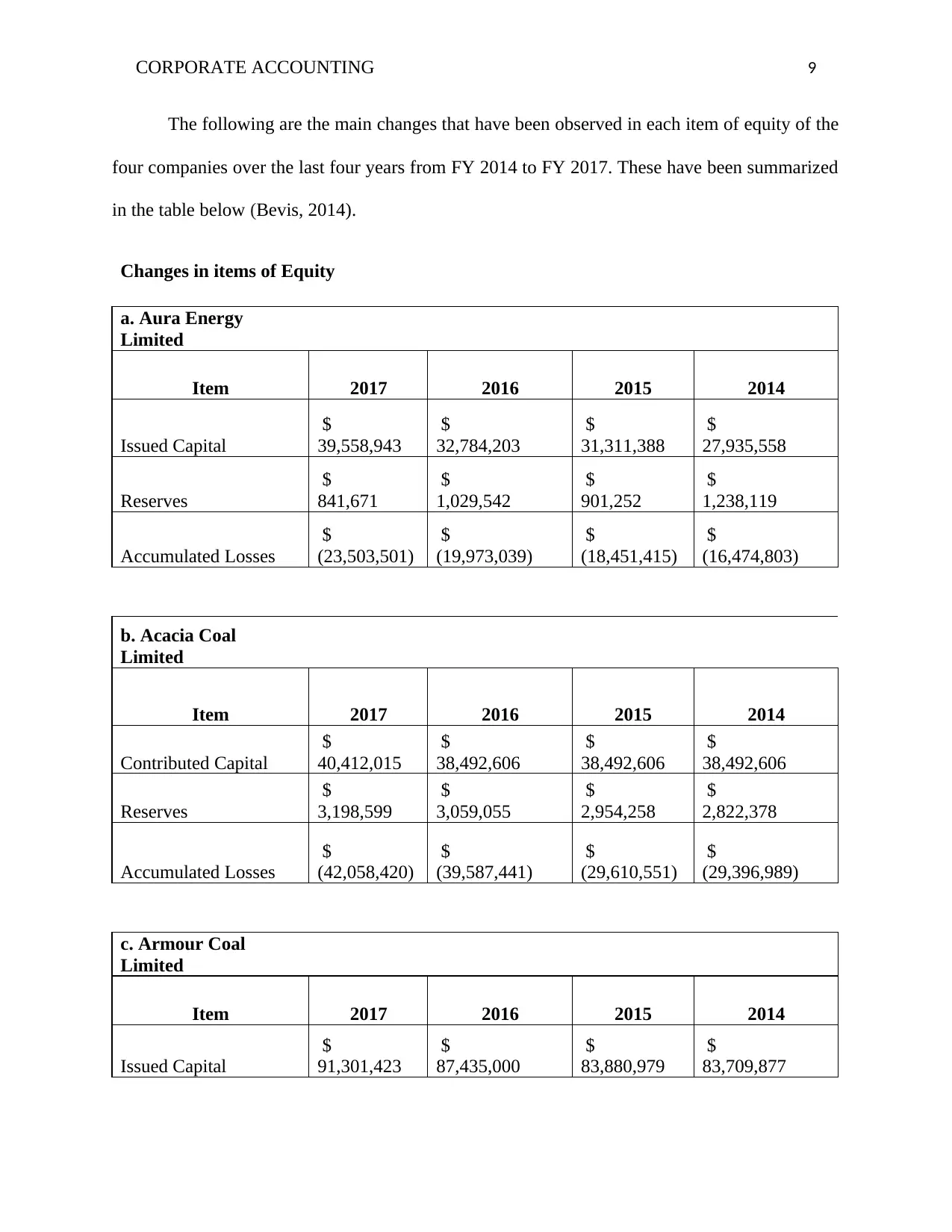

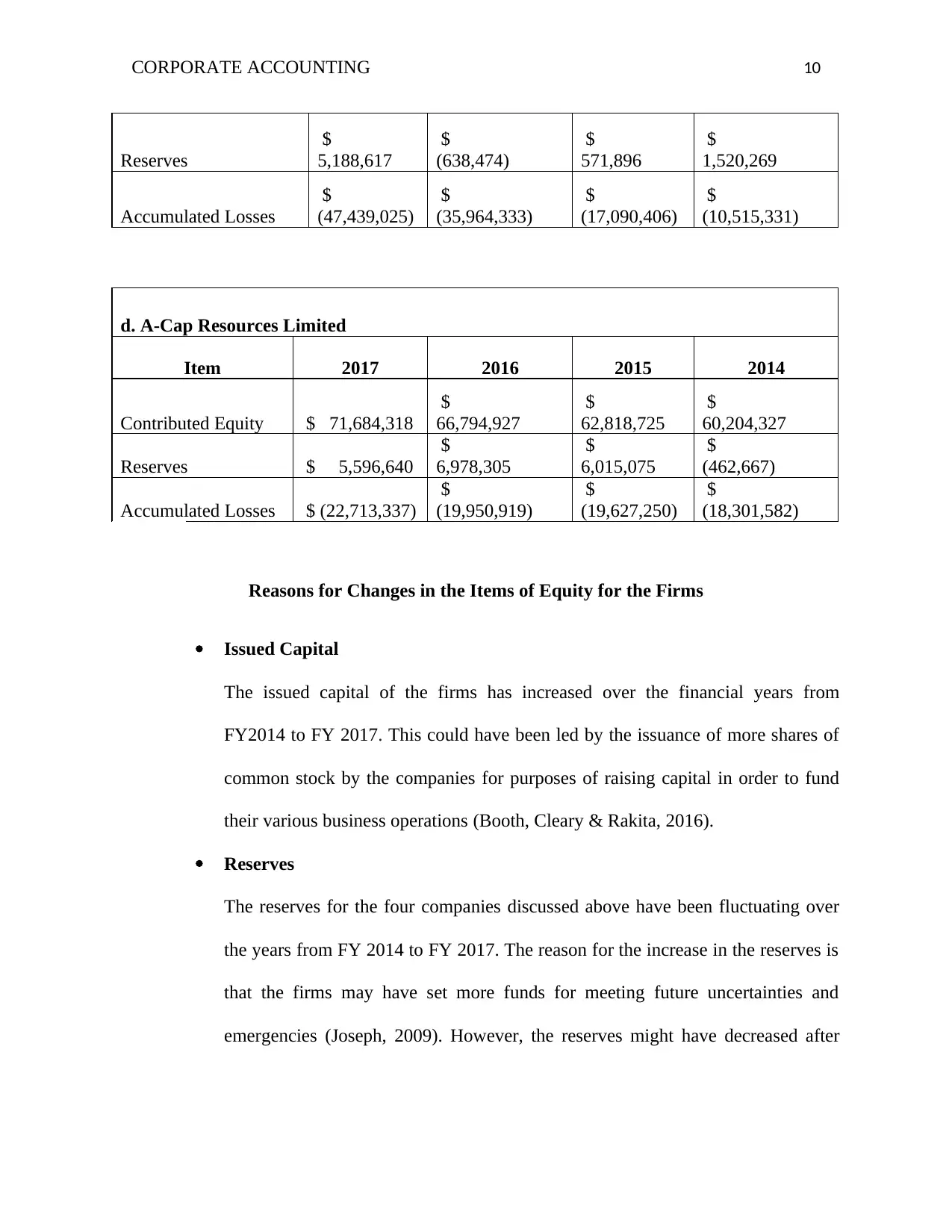

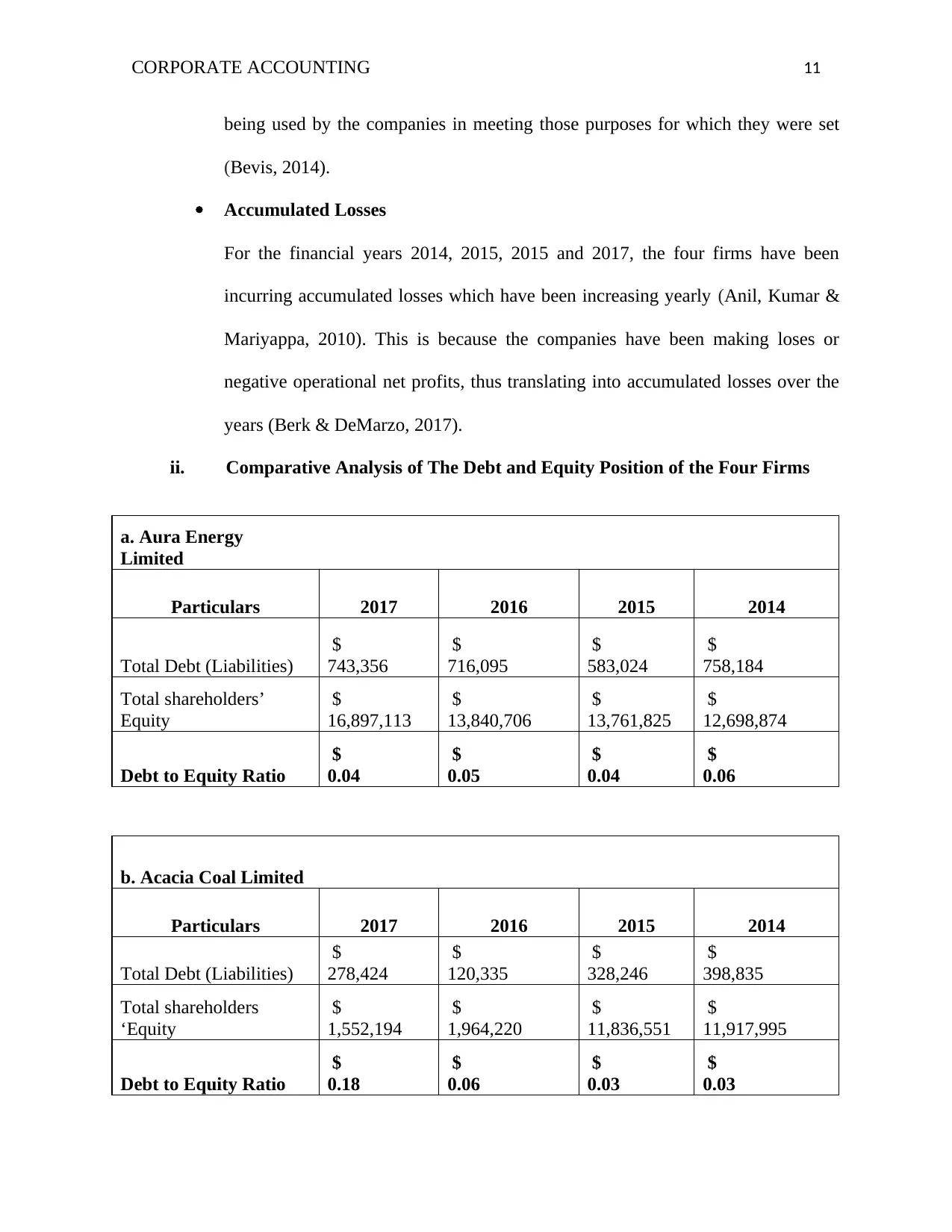

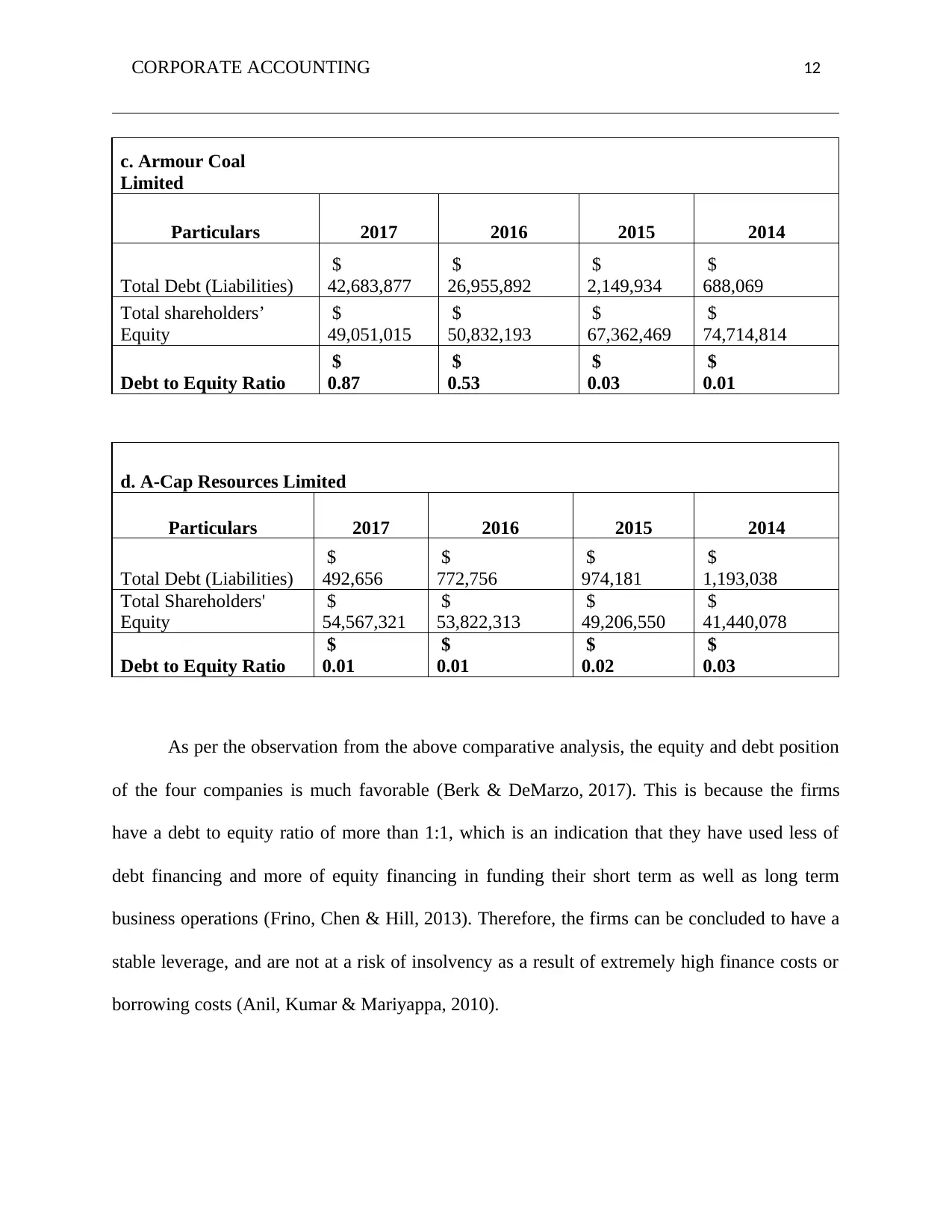

This paper discusses whether financial accounting and reporting should be regulated, how AASB participates in setting global standards of accounting, and equity analysis of four public limited companies listed on the Australian Securities Exchange. The four firms have a favorable debt and equity position since they have used more of equity financing in funding most of their business operations. However, they have been making operational losses for the Financial Years 2014 all through 2017, which have consequentially translated into increasingly huge accumulated losses.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)