Corporate Accounting : Assignment

VerifiedAdded on 2021/06/18

|9

|1721

|17

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HI5020 Corporate Accounting

Assessment 2 – AUSDRILL LIMITED

STUDENT ID:

[Pick the date]

Assessment 2 – AUSDRILL LIMITED

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting

The company selected for this task is AUSDRILL.

CASH FLOWS STATEMENT

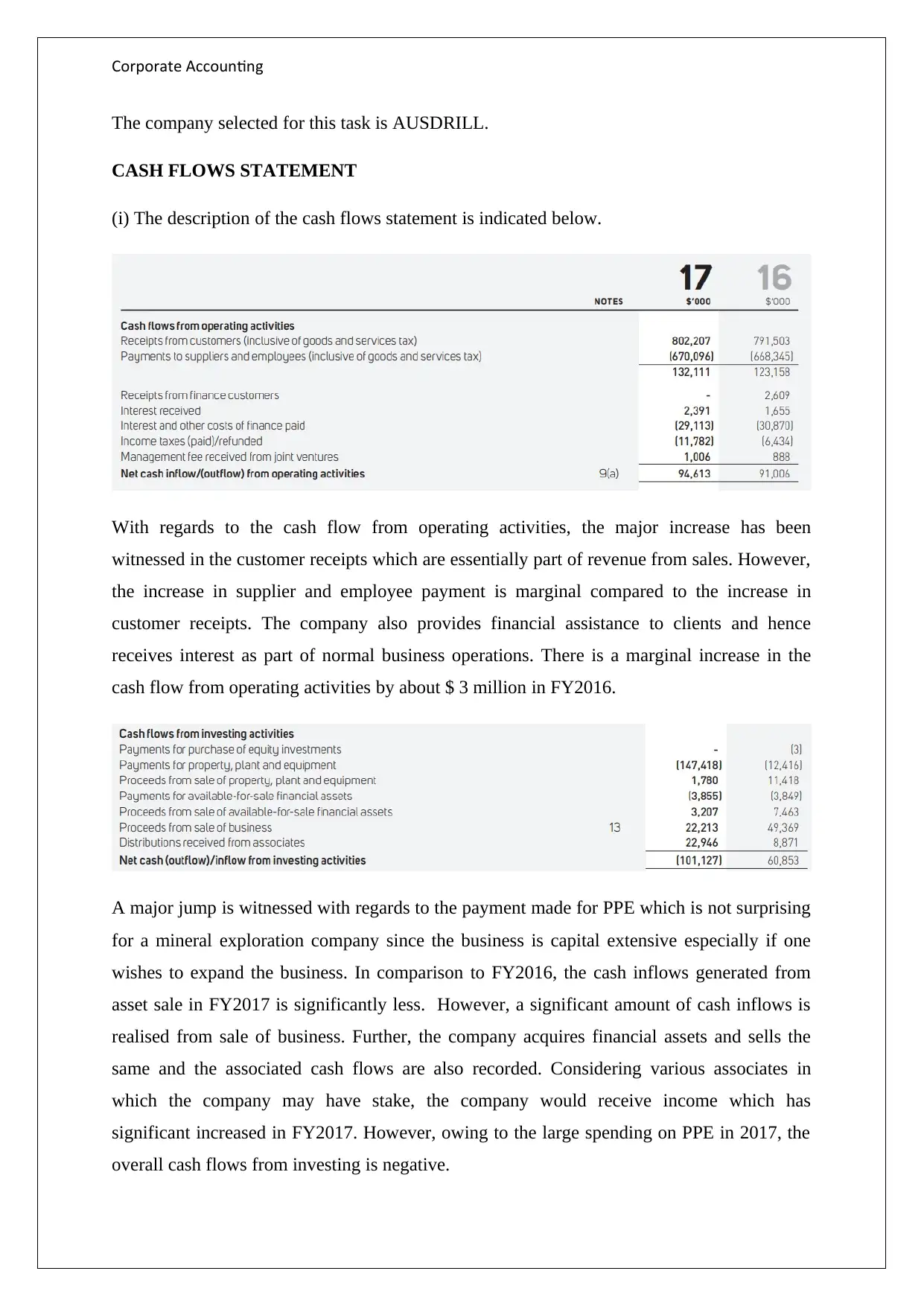

(i) The description of the cash flows statement is indicated below.

With regards to the cash flow from operating activities, the major increase has been

witnessed in the customer receipts which are essentially part of revenue from sales. However,

the increase in supplier and employee payment is marginal compared to the increase in

customer receipts. The company also provides financial assistance to clients and hence

receives interest as part of normal business operations. There is a marginal increase in the

cash flow from operating activities by about $ 3 million in FY2016.

A major jump is witnessed with regards to the payment made for PPE which is not surprising

for a mineral exploration company since the business is capital extensive especially if one

wishes to expand the business. In comparison to FY2016, the cash inflows generated from

asset sale in FY2017 is significantly less. However, a significant amount of cash inflows is

realised from sale of business. Further, the company acquires financial assets and sells the

same and the associated cash flows are also recorded. Considering various associates in

which the company may have stake, the company would receive income which has

significant increased in FY2017. However, owing to the large spending on PPE in 2017, the

overall cash flows from investing is negative.

The company selected for this task is AUSDRILL.

CASH FLOWS STATEMENT

(i) The description of the cash flows statement is indicated below.

With regards to the cash flow from operating activities, the major increase has been

witnessed in the customer receipts which are essentially part of revenue from sales. However,

the increase in supplier and employee payment is marginal compared to the increase in

customer receipts. The company also provides financial assistance to clients and hence

receives interest as part of normal business operations. There is a marginal increase in the

cash flow from operating activities by about $ 3 million in FY2016.

A major jump is witnessed with regards to the payment made for PPE which is not surprising

for a mineral exploration company since the business is capital extensive especially if one

wishes to expand the business. In comparison to FY2016, the cash inflows generated from

asset sale in FY2017 is significantly less. However, a significant amount of cash inflows is

realised from sale of business. Further, the company acquires financial assets and sells the

same and the associated cash flows are also recorded. Considering various associates in

which the company may have stake, the company would receive income which has

significant increased in FY2017. However, owing to the large spending on PPE in 2017, the

overall cash flows from investing is negative.

Corporate Accounting

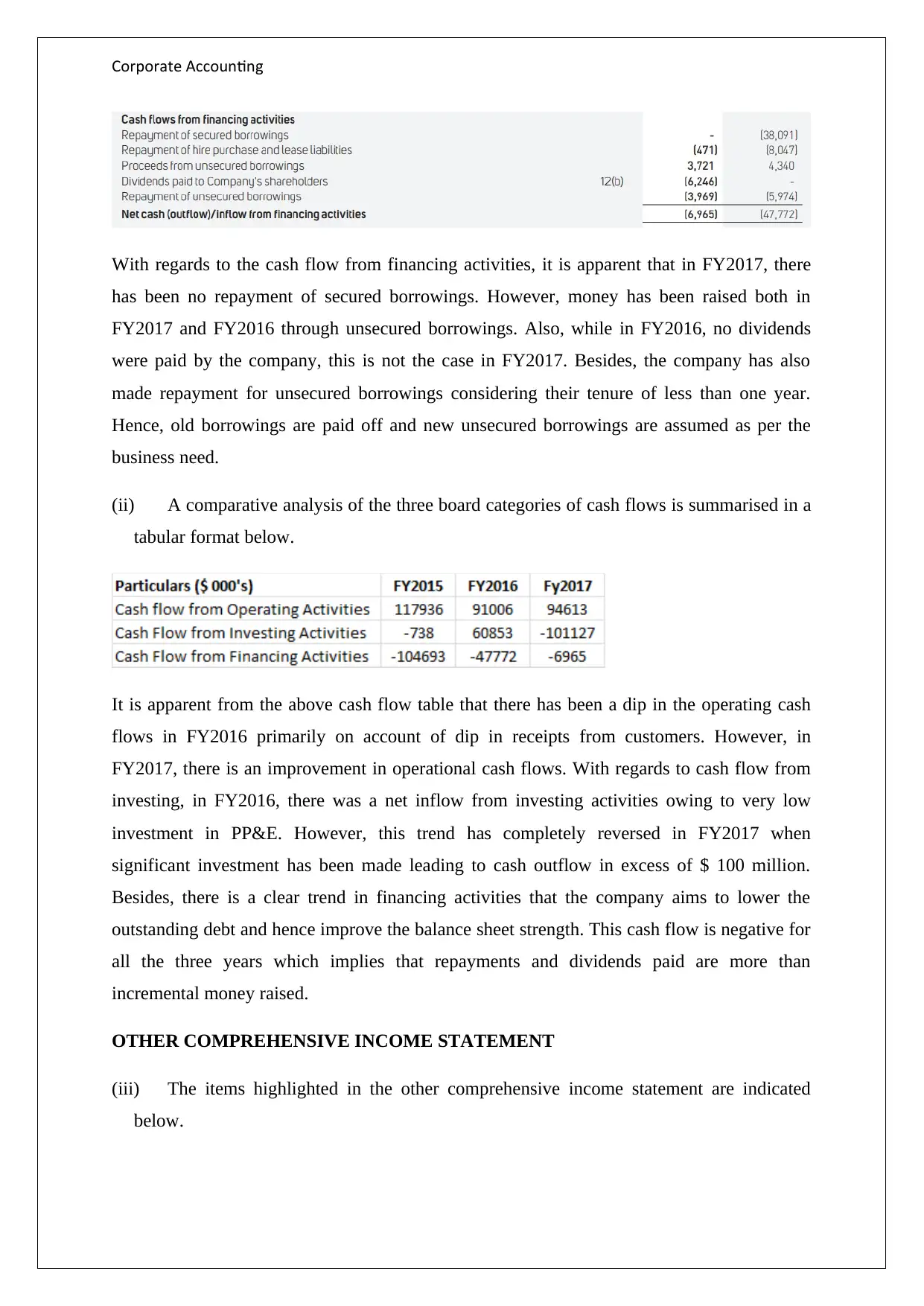

With regards to the cash flow from financing activities, it is apparent that in FY2017, there

has been no repayment of secured borrowings. However, money has been raised both in

FY2017 and FY2016 through unsecured borrowings. Also, while in FY2016, no dividends

were paid by the company, this is not the case in FY2017. Besides, the company has also

made repayment for unsecured borrowings considering their tenure of less than one year.

Hence, old borrowings are paid off and new unsecured borrowings are assumed as per the

business need.

(ii) A comparative analysis of the three board categories of cash flows is summarised in a

tabular format below.

It is apparent from the above cash flow table that there has been a dip in the operating cash

flows in FY2016 primarily on account of dip in receipts from customers. However, in

FY2017, there is an improvement in operational cash flows. With regards to cash flow from

investing, in FY2016, there was a net inflow from investing activities owing to very low

investment in PP&E. However, this trend has completely reversed in FY2017 when

significant investment has been made leading to cash outflow in excess of $ 100 million.

Besides, there is a clear trend in financing activities that the company aims to lower the

outstanding debt and hence improve the balance sheet strength. This cash flow is negative for

all the three years which implies that repayments and dividends paid are more than

incremental money raised.

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) The items highlighted in the other comprehensive income statement are indicated

below.

With regards to the cash flow from financing activities, it is apparent that in FY2017, there

has been no repayment of secured borrowings. However, money has been raised both in

FY2017 and FY2016 through unsecured borrowings. Also, while in FY2016, no dividends

were paid by the company, this is not the case in FY2017. Besides, the company has also

made repayment for unsecured borrowings considering their tenure of less than one year.

Hence, old borrowings are paid off and new unsecured borrowings are assumed as per the

business need.

(ii) A comparative analysis of the three board categories of cash flows is summarised in a

tabular format below.

It is apparent from the above cash flow table that there has been a dip in the operating cash

flows in FY2016 primarily on account of dip in receipts from customers. However, in

FY2017, there is an improvement in operational cash flows. With regards to cash flow from

investing, in FY2016, there was a net inflow from investing activities owing to very low

investment in PP&E. However, this trend has completely reversed in FY2017 when

significant investment has been made leading to cash outflow in excess of $ 100 million.

Besides, there is a clear trend in financing activities that the company aims to lower the

outstanding debt and hence improve the balance sheet strength. This cash flow is negative for

all the three years which implies that repayments and dividends paid are more than

incremental money raised.

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) The items highlighted in the other comprehensive income statement are indicated

below.

Corporate Accounting

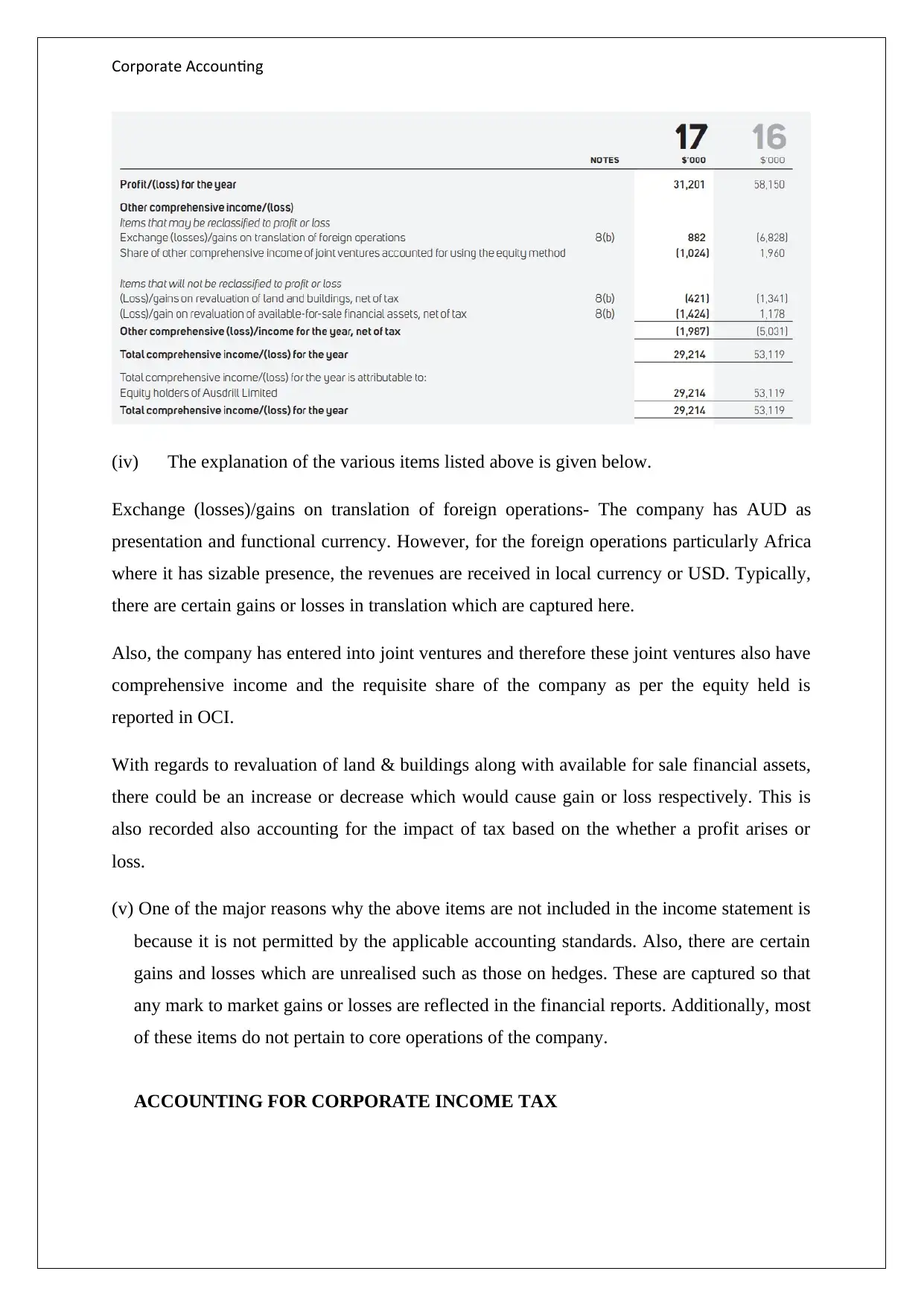

(iv) The explanation of the various items listed above is given below.

Exchange (losses)/gains on translation of foreign operations- The company has AUD as

presentation and functional currency. However, for the foreign operations particularly Africa

where it has sizable presence, the revenues are received in local currency or USD. Typically,

there are certain gains or losses in translation which are captured here.

Also, the company has entered into joint ventures and therefore these joint ventures also have

comprehensive income and the requisite share of the company as per the equity held is

reported in OCI.

With regards to revaluation of land & buildings along with available for sale financial assets,

there could be an increase or decrease which would cause gain or loss respectively. This is

also recorded also accounting for the impact of tax based on the whether a profit arises or

loss.

(v) One of the major reasons why the above items are not included in the income statement is

because it is not permitted by the applicable accounting standards. Also, there are certain

gains and losses which are unrealised such as those on hedges. These are captured so that

any mark to market gains or losses are reflected in the financial reports. Additionally, most

of these items do not pertain to core operations of the company.

ACCOUNTING FOR CORPORATE INCOME TAX

(iv) The explanation of the various items listed above is given below.

Exchange (losses)/gains on translation of foreign operations- The company has AUD as

presentation and functional currency. However, for the foreign operations particularly Africa

where it has sizable presence, the revenues are received in local currency or USD. Typically,

there are certain gains or losses in translation which are captured here.

Also, the company has entered into joint ventures and therefore these joint ventures also have

comprehensive income and the requisite share of the company as per the equity held is

reported in OCI.

With regards to revaluation of land & buildings along with available for sale financial assets,

there could be an increase or decrease which would cause gain or loss respectively. This is

also recorded also accounting for the impact of tax based on the whether a profit arises or

loss.

(v) One of the major reasons why the above items are not included in the income statement is

because it is not permitted by the applicable accounting standards. Also, there are certain

gains and losses which are unrealised such as those on hedges. These are captured so that

any mark to market gains or losses are reflected in the financial reports. Additionally, most

of these items do not pertain to core operations of the company.

ACCOUNTING FOR CORPORATE INCOME TAX

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Accounting

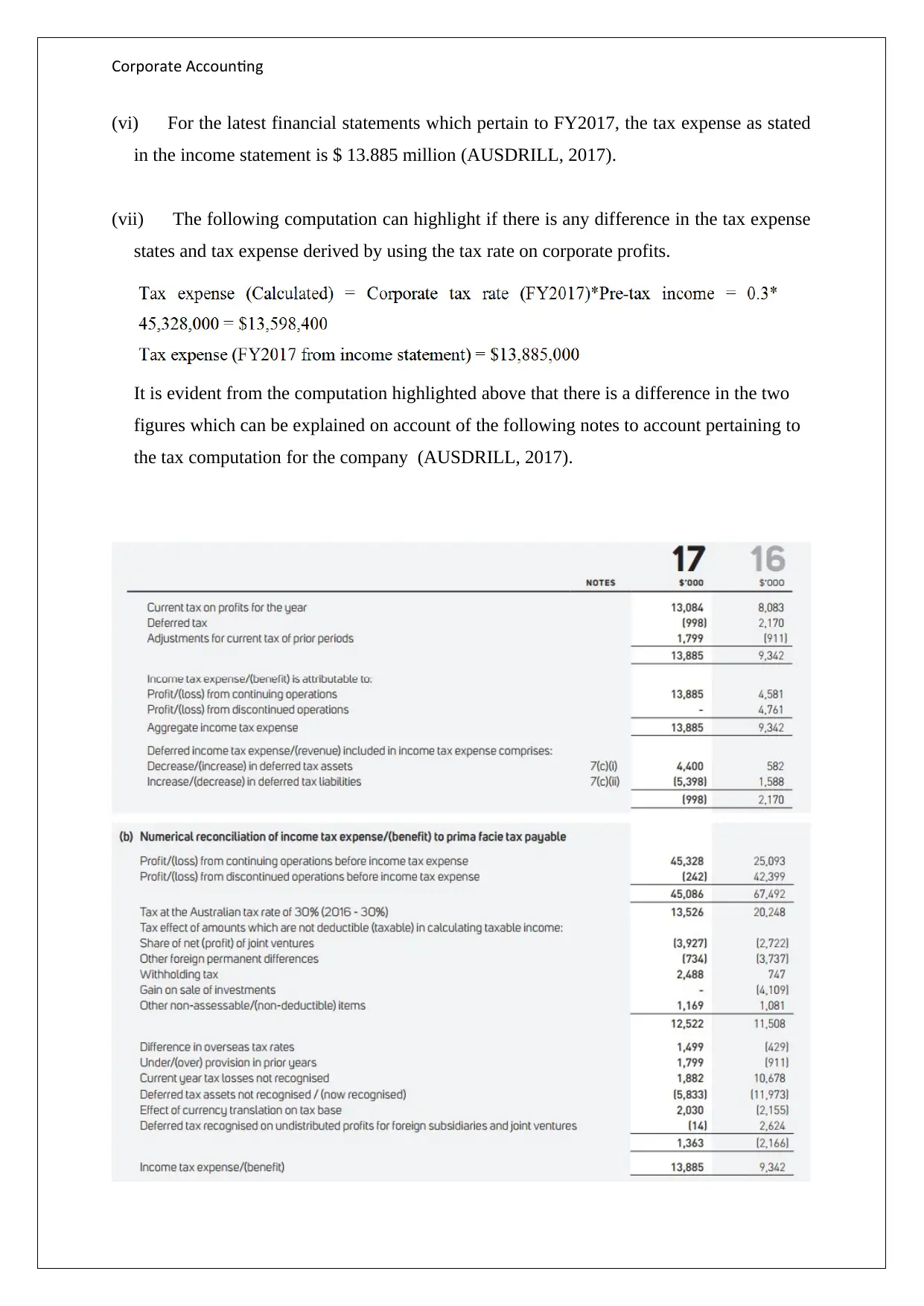

(vi) For the latest financial statements which pertain to FY2017, the tax expense as stated

in the income statement is $ 13.885 million (AUSDRILL, 2017).

(vii) The following computation can highlight if there is any difference in the tax expense

states and tax expense derived by using the tax rate on corporate profits.

It is evident from the computation highlighted above that there is a difference in the two

figures which can be explained on account of the following notes to account pertaining to

the tax computation for the company (AUSDRILL, 2017).

(vi) For the latest financial statements which pertain to FY2017, the tax expense as stated

in the income statement is $ 13.885 million (AUSDRILL, 2017).

(vii) The following computation can highlight if there is any difference in the tax expense

states and tax expense derived by using the tax rate on corporate profits.

It is evident from the computation highlighted above that there is a difference in the two

figures which can be explained on account of the following notes to account pertaining to

the tax computation for the company (AUSDRILL, 2017).

Corporate Accounting

The above notes to account clearly highlight that there are adjustments made in relation to

deferred tax assets, withholding tax, difference in tax rates in different jurisdictions along

with differences in rules for computation taxable income and accounting income

(AUSDRILL, 2017).

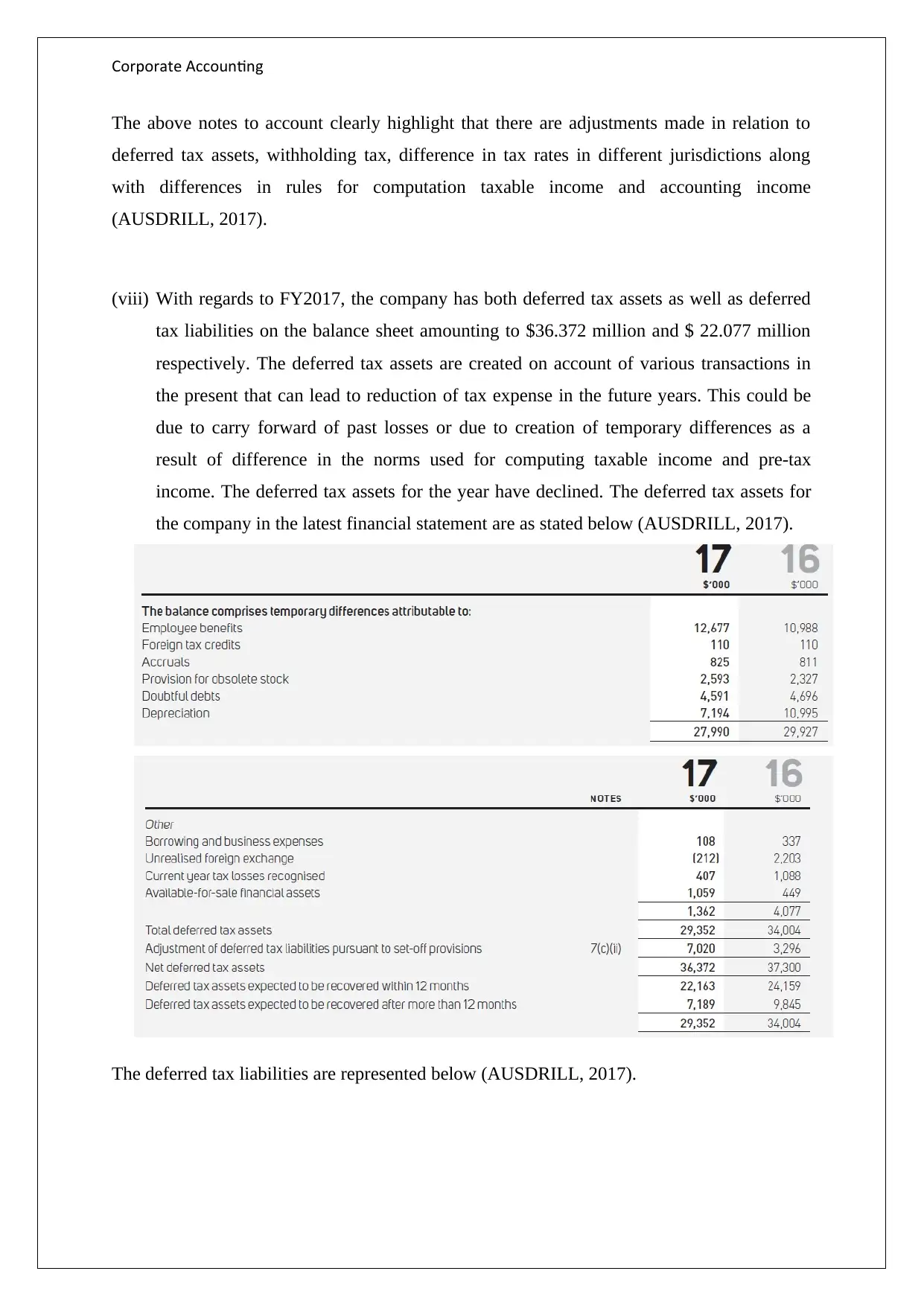

(viii) With regards to FY2017, the company has both deferred tax assets as well as deferred

tax liabilities on the balance sheet amounting to $36.372 million and $ 22.077 million

respectively. The deferred tax assets are created on account of various transactions in

the present that can lead to reduction of tax expense in the future years. This could be

due to carry forward of past losses or due to creation of temporary differences as a

result of difference in the norms used for computing taxable income and pre-tax

income. The deferred tax assets for the year have declined. The deferred tax assets for

the company in the latest financial statement are as stated below (AUSDRILL, 2017).

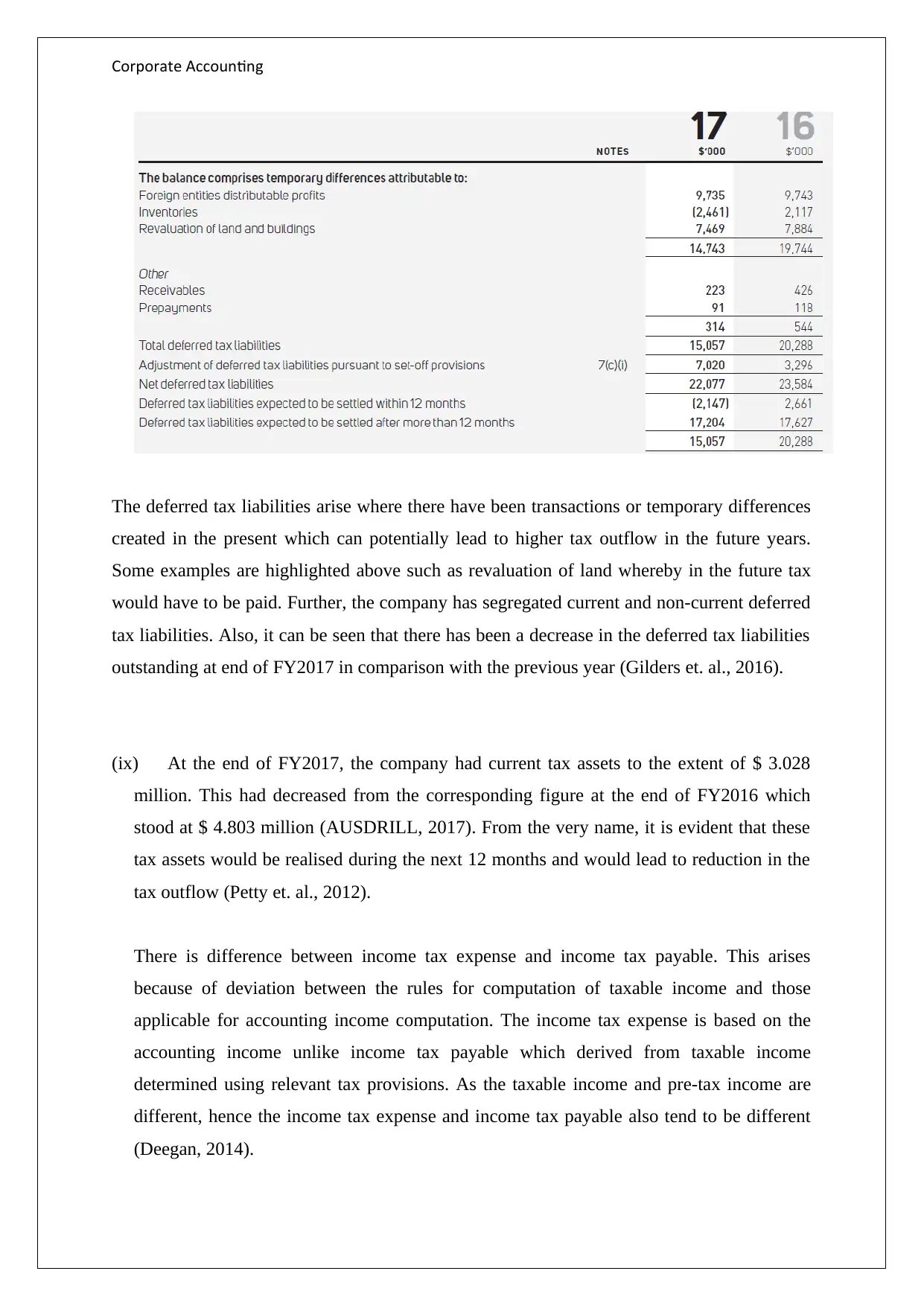

The deferred tax liabilities are represented below (AUSDRILL, 2017).

The above notes to account clearly highlight that there are adjustments made in relation to

deferred tax assets, withholding tax, difference in tax rates in different jurisdictions along

with differences in rules for computation taxable income and accounting income

(AUSDRILL, 2017).

(viii) With regards to FY2017, the company has both deferred tax assets as well as deferred

tax liabilities on the balance sheet amounting to $36.372 million and $ 22.077 million

respectively. The deferred tax assets are created on account of various transactions in

the present that can lead to reduction of tax expense in the future years. This could be

due to carry forward of past losses or due to creation of temporary differences as a

result of difference in the norms used for computing taxable income and pre-tax

income. The deferred tax assets for the year have declined. The deferred tax assets for

the company in the latest financial statement are as stated below (AUSDRILL, 2017).

The deferred tax liabilities are represented below (AUSDRILL, 2017).

Corporate Accounting

The deferred tax liabilities arise where there have been transactions or temporary differences

created in the present which can potentially lead to higher tax outflow in the future years.

Some examples are highlighted above such as revaluation of land whereby in the future tax

would have to be paid. Further, the company has segregated current and non-current deferred

tax liabilities. Also, it can be seen that there has been a decrease in the deferred tax liabilities

outstanding at end of FY2017 in comparison with the previous year (Gilders et. al., 2016).

(ix) At the end of FY2017, the company had current tax assets to the extent of $ 3.028

million. This had decreased from the corresponding figure at the end of FY2016 which

stood at $ 4.803 million (AUSDRILL, 2017). From the very name, it is evident that these

tax assets would be realised during the next 12 months and would lead to reduction in the

tax outflow (Petty et. al., 2012).

There is difference between income tax expense and income tax payable. This arises

because of deviation between the rules for computation of taxable income and those

applicable for accounting income computation. The income tax expense is based on the

accounting income unlike income tax payable which derived from taxable income

determined using relevant tax provisions. As the taxable income and pre-tax income are

different, hence the income tax expense and income tax payable also tend to be different

(Deegan, 2014).

The deferred tax liabilities arise where there have been transactions or temporary differences

created in the present which can potentially lead to higher tax outflow in the future years.

Some examples are highlighted above such as revaluation of land whereby in the future tax

would have to be paid. Further, the company has segregated current and non-current deferred

tax liabilities. Also, it can be seen that there has been a decrease in the deferred tax liabilities

outstanding at end of FY2017 in comparison with the previous year (Gilders et. al., 2016).

(ix) At the end of FY2017, the company had current tax assets to the extent of $ 3.028

million. This had decreased from the corresponding figure at the end of FY2016 which

stood at $ 4.803 million (AUSDRILL, 2017). From the very name, it is evident that these

tax assets would be realised during the next 12 months and would lead to reduction in the

tax outflow (Petty et. al., 2012).

There is difference between income tax expense and income tax payable. This arises

because of deviation between the rules for computation of taxable income and those

applicable for accounting income computation. The income tax expense is based on the

accounting income unlike income tax payable which derived from taxable income

determined using relevant tax provisions. As the taxable income and pre-tax income are

different, hence the income tax expense and income tax payable also tend to be different

(Deegan, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

(x) For FY2017, the income tax paid by the company amounts to $ 11.782 million. However,

the tax expense for the corresponding period is $ 13.885 million (AUSDRILL,2017). It is

apparent that there is difference between the above mentioned two figures. A potential

reason for mismatch is that the tax expense reflected in the income statement is prepared

on accrual basis. In contrast, the cash flow statement highlights actual tax that has been

paid. Also, the income tax expense is based on pre-tax income based on accounting norms.

However, the income tax paid is derived from taxable income based on taxation norms

(Barkoczy, 2017).

(xi) One of the key aspects related to the tax treatment of companies is the reconciliation

required between tax expense and income tax payable. It was quite fascinating yet at the

same time complex to witness the creation of temporary differences and how these tend to

reflect in the form of deferred tax assets and liabilities. While doing theoretical studies,

application of corporate tax seems a straight forward tax of multiplying the pre –tax

income with the applicable corporate tax rate but this exercise has enabled me to

understand that it is a much more complex and intriguing task.

(x) For FY2017, the income tax paid by the company amounts to $ 11.782 million. However,

the tax expense for the corresponding period is $ 13.885 million (AUSDRILL,2017). It is

apparent that there is difference between the above mentioned two figures. A potential

reason for mismatch is that the tax expense reflected in the income statement is prepared

on accrual basis. In contrast, the cash flow statement highlights actual tax that has been

paid. Also, the income tax expense is based on pre-tax income based on accounting norms.

However, the income tax paid is derived from taxable income based on taxation norms

(Barkoczy, 2017).

(xi) One of the key aspects related to the tax treatment of companies is the reconciliation

required between tax expense and income tax payable. It was quite fascinating yet at the

same time complex to witness the creation of temporary differences and how these tend to

reflect in the form of deferred tax assets and liabilities. While doing theoretical studies,

application of corporate tax seems a straight forward tax of multiplying the pre –tax

income with the applicable corporate tax rate but this exercise has enabled me to

understand that it is a much more complex and intriguing task.

Corporate Accounting

References

AUSDRILL (2017), Annual Report FY2017, [Online] Available at

http://www.ausdrill.com.au/images/ausdrill/files/20170823_AUSDRILL_ANNUAL_REPOR

T_2017.pdf (Accessed May 17, 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University

Press.

Deegan, C. (2014). Financial Accounting Theory, 4th ed. Sydney: McGraw-Hill

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016, 9th ed. Sydney: LexisNexis/Butterworths.

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education, French

Forest Australia.

References

AUSDRILL (2017), Annual Report FY2017, [Online] Available at

http://www.ausdrill.com.au/images/ausdrill/files/20170823_AUSDRILL_ANNUAL_REPOR

T_2017.pdf (Accessed May 17, 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University

Press.

Deegan, C. (2014). Financial Accounting Theory, 4th ed. Sydney: McGraw-Hill

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016, 9th ed. Sydney: LexisNexis/Butterworths.

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education, French

Forest Australia.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.