A New Era for Heritage Sites

VerifiedAdded on 2019/11/26

|16

|2094

|173

Report

AI Summary

The assignment content discusses the importance of heritage sites as assets that can boost the economy of an area through tourism and commercialization. It also presents journal entries related to biological assets, harvesting of agriculture produce, and sales transactions, which are governed by accounting standards AASB 141, AASB 116, and Deegan (2013). Additionally, it provides segment reporting for profit, revenue, and asset statements, which complies with the disclosure notes of AASB 8.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Student’s Name

Course Code

Corporate Accounting

Student’s Name

Course Code

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

CORPORATE ACCOUNTING

Question 1

Climate change has been in vogue for Financial Institutions recently (Deegan

2013).Climate resistance and low carbon has been given emphasis. Mainstream financing has

been the platform for climate issues. Formulation of national and international policies can be

made for industries to be transparent. Capacitating the industries to make changes for climate

issues is the next target. All like-minded investors have been grouping to collaborate for the

climate change for capital inflow. Climate change is risky for economy and hence for investment

sector as whole.

Ethical investment which is called Socially Responsible Investments has developed

recently. Investors are seen reluctant in investing in ventures of arms or alcohol which are of

hostile nature. Now investment is being done on merits of goods that are environmental

protection, ethical employment, recycling and conservation (Deegan 2013). Ethical investors

follow activism in which they convince each other to make positive amendments in the type of

their investments. They do not restrict any investment strategy but modify it for gaining

sustainability in the business.

CORPORATE ACCOUNTING

Question 1

Climate change has been in vogue for Financial Institutions recently (Deegan

2013).Climate resistance and low carbon has been given emphasis. Mainstream financing has

been the platform for climate issues. Formulation of national and international policies can be

made for industries to be transparent. Capacitating the industries to make changes for climate

issues is the next target. All like-minded investors have been grouping to collaborate for the

climate change for capital inflow. Climate change is risky for economy and hence for investment

sector as whole.

Ethical investment which is called Socially Responsible Investments has developed

recently. Investors are seen reluctant in investing in ventures of arms or alcohol which are of

hostile nature. Now investment is being done on merits of goods that are environmental

protection, ethical employment, recycling and conservation (Deegan 2013). Ethical investors

follow activism in which they convince each other to make positive amendments in the type of

their investments. They do not restrict any investment strategy but modify it for gaining

sustainability in the business.

2

CORPORATE ACCOUNTING

Question 2

There are several policies and procedures published by the government of country for

corporate to maintain the sustainability of the companies within that particular territories. Since

1980’s companies are bound to fulfill responsibilities towards society and environment.

Company is liable for the adverse effects of noise and chemicals produced towards environment.

But it can be managed by the benefits of employment given to the local citizens without any

legal compliance.

CSR is to be held up by every organization to show their concern towards society and

environment. Health campaigns should be organized to tackle the issues created due to noise and

chemicals. It may incur cost to the company but its benefits are more farfetched. A CSR

committee can be made to organize these activities and manage affairs with the government as

per requirement. Sustainability report should be published each year as per the amendments of

authorities and government. CSR activities should comply with GRI norms.

CORPORATE ACCOUNTING

Question 2

There are several policies and procedures published by the government of country for

corporate to maintain the sustainability of the companies within that particular territories. Since

1980’s companies are bound to fulfill responsibilities towards society and environment.

Company is liable for the adverse effects of noise and chemicals produced towards environment.

But it can be managed by the benefits of employment given to the local citizens without any

legal compliance.

CSR is to be held up by every organization to show their concern towards society and

environment. Health campaigns should be organized to tackle the issues created due to noise and

chemicals. It may incur cost to the company but its benefits are more farfetched. A CSR

committee can be made to organize these activities and manage affairs with the government as

per requirement. Sustainability report should be published each year as per the amendments of

authorities and government. CSR activities should comply with GRI norms.

3

CORPORATE ACCOUNTING

Question 3

The $50,000 has been spent on development of general understanding of water flow

dynamics would be considered as research and will be written off as incurred.

The $30,000 spent for the purpose of knowledge gathering of surfboard which is

expected from local surfers will be considered as research and would be written off as

incurred.

There are $90,000 and $1, 90,000 have been spent on testing and refining and prototype

has been considered as development expenditure will be capitalized.

CORPORATE ACCOUNTING

Question 3

The $50,000 has been spent on development of general understanding of water flow

dynamics would be considered as research and will be written off as incurred.

The $30,000 spent for the purpose of knowledge gathering of surfboard which is

expected from local surfers will be considered as research and would be written off as

incurred.

There are $90,000 and $1, 90,000 have been spent on testing and refining and prototype

has been considered as development expenditure will be capitalized.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

CORPORATE ACCOUNTING

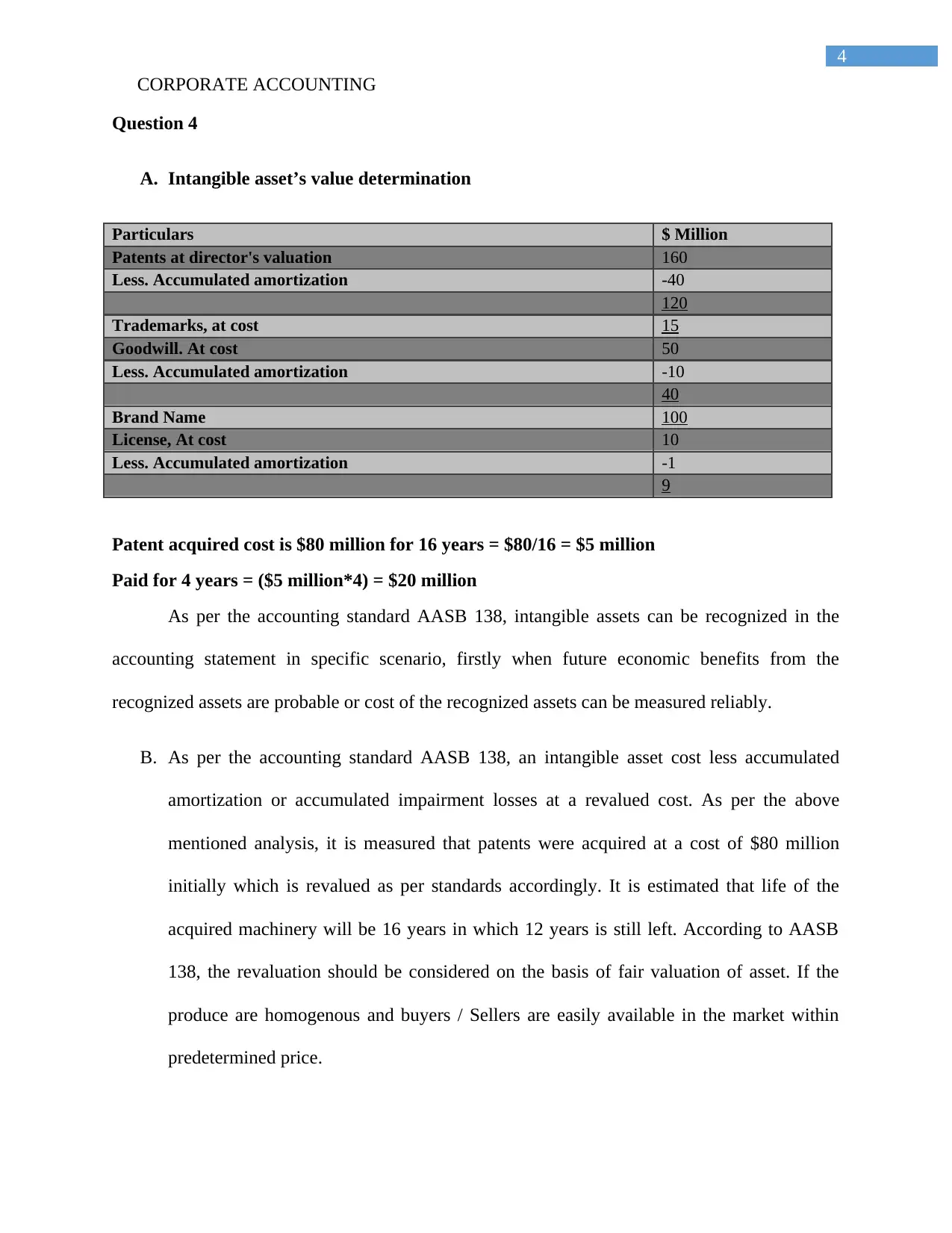

Question 4

A. Intangible asset’s value determination

Particulars $ Million

Patents at director's valuation 160

Less. Accumulated amortization -40

120

Trademarks, at cost 15

Goodwill. At cost 50

Less. Accumulated amortization -10

40

Brand Name 100

License, At cost 10

Less. Accumulated amortization -1

9

Patent acquired cost is $80 million for 16 years = $80/16 = $5 million

Paid for 4 years = ($5 million*4) = $20 million

As per the accounting standard AASB 138, intangible assets can be recognized in the

accounting statement in specific scenario, firstly when future economic benefits from the

recognized assets are probable or cost of the recognized assets can be measured reliably.

B. As per the accounting standard AASB 138, an intangible asset cost less accumulated

amortization or accumulated impairment losses at a revalued cost. As per the above

mentioned analysis, it is measured that patents were acquired at a cost of $80 million

initially which is revalued as per standards accordingly. It is estimated that life of the

acquired machinery will be 16 years in which 12 years is still left. According to AASB

138, the revaluation should be considered on the basis of fair valuation of asset. If the

produce are homogenous and buyers / Sellers are easily available in the market within

predetermined price.

CORPORATE ACCOUNTING

Question 4

A. Intangible asset’s value determination

Particulars $ Million

Patents at director's valuation 160

Less. Accumulated amortization -40

120

Trademarks, at cost 15

Goodwill. At cost 50

Less. Accumulated amortization -10

40

Brand Name 100

License, At cost 10

Less. Accumulated amortization -1

9

Patent acquired cost is $80 million for 16 years = $80/16 = $5 million

Paid for 4 years = ($5 million*4) = $20 million

As per the accounting standard AASB 138, intangible assets can be recognized in the

accounting statement in specific scenario, firstly when future economic benefits from the

recognized assets are probable or cost of the recognized assets can be measured reliably.

B. As per the accounting standard AASB 138, an intangible asset cost less accumulated

amortization or accumulated impairment losses at a revalued cost. As per the above

mentioned analysis, it is measured that patents were acquired at a cost of $80 million

initially which is revalued as per standards accordingly. It is estimated that life of the

acquired machinery will be 16 years in which 12 years is still left. According to AASB

138, the revaluation should be considered on the basis of fair valuation of asset. If the

produce are homogenous and buyers / Sellers are easily available in the market within

predetermined price.

5

CORPORATE ACCOUNTING

Patent at cost-Accumulated amortization (4 years out of total 16 years life)

Net carrying value = (80 million-20 million =60 million)

Trade Mark

As per the accounting standard AASB 138, Intangible assets with indefinite useful life

are not subject to amortize, there are always possibility that trademark can be renewed

indefinitely will be considered as cost less impairment losses. Initially the intangible assets are

recognized as expenditure but afterwards it is a part of cost incurred by the company.

Goodwill

As per AASB 138, goodwill is an intangible asset which has been purchased and

amortized on the basis of straight line depreciation method. Goodwill is only recognized when it

is externally acquired by the companies. It is always considered the goodwill at cost after

deduction of accumulated amortization.

CORPORATE ACCOUNTING

Patent at cost-Accumulated amortization (4 years out of total 16 years life)

Net carrying value = (80 million-20 million =60 million)

Trade Mark

As per the accounting standard AASB 138, Intangible assets with indefinite useful life

are not subject to amortize, there are always possibility that trademark can be renewed

indefinitely will be considered as cost less impairment losses. Initially the intangible assets are

recognized as expenditure but afterwards it is a part of cost incurred by the company.

Goodwill

As per AASB 138, goodwill is an intangible asset which has been purchased and

amortized on the basis of straight line depreciation method. Goodwill is only recognized when it

is externally acquired by the companies. It is always considered the goodwill at cost after

deduction of accumulated amortization.

6

CORPORATE ACCOUNTING

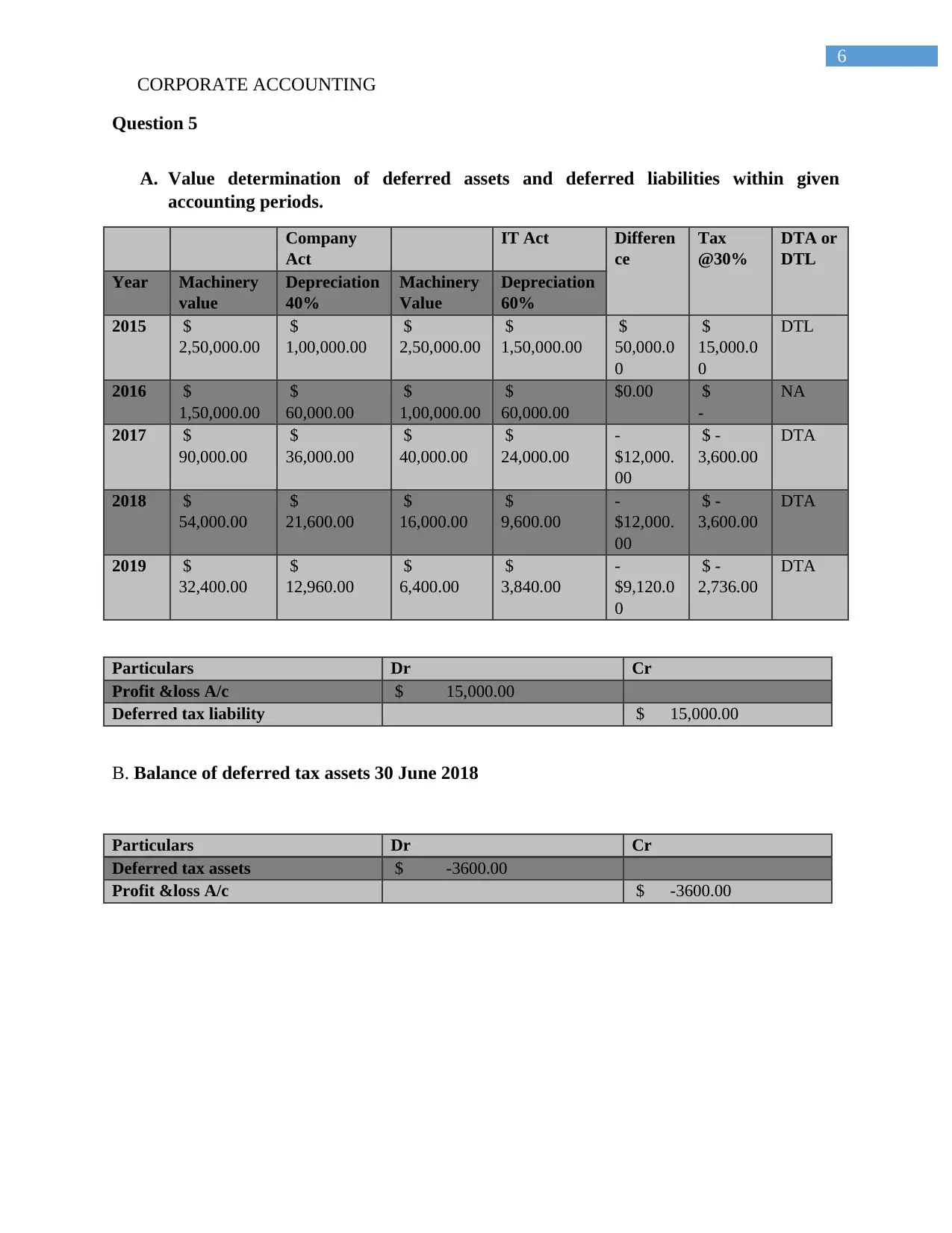

Question 5

A. Value determination of deferred assets and deferred liabilities within given

accounting periods.

Company

Act

IT Act Differen

ce

Tax

@30%

DTA or

DTL

Year Machinery

value

Depreciation

40%

Machinery

Value

Depreciation

60%

2015 $

2,50,000.00

$

1,00,000.00

$

2,50,000.00

$

1,50,000.00

$

50,000.0

0

$

15,000.0

0

DTL

2016 $

1,50,000.00

$

60,000.00

$

1,00,000.00

$

60,000.00

$0.00 $

-

NA

2017 $

90,000.00

$

36,000.00

$

40,000.00

$

24,000.00

-

$12,000.

00

$ -

3,600.00

DTA

2018 $

54,000.00

$

21,600.00

$

16,000.00

$

9,600.00

-

$12,000.

00

$ -

3,600.00

DTA

2019 $

32,400.00

$

12,960.00

$

6,400.00

$

3,840.00

-

$9,120.0

0

$ -

2,736.00

DTA

Particulars Dr Cr

Profit &loss A/c $ 15,000.00

Deferred tax liability $ 15,000.00

B. Balance of deferred tax assets 30 June 2018

Particulars Dr Cr

Deferred tax assets $ -3600.00

Profit &loss A/c $ -3600.00

CORPORATE ACCOUNTING

Question 5

A. Value determination of deferred assets and deferred liabilities within given

accounting periods.

Company

Act

IT Act Differen

ce

Tax

@30%

DTA or

DTL

Year Machinery

value

Depreciation

40%

Machinery

Value

Depreciation

60%

2015 $

2,50,000.00

$

1,00,000.00

$

2,50,000.00

$

1,50,000.00

$

50,000.0

0

$

15,000.0

0

DTL

2016 $

1,50,000.00

$

60,000.00

$

1,00,000.00

$

60,000.00

$0.00 $

-

NA

2017 $

90,000.00

$

36,000.00

$

40,000.00

$

24,000.00

-

$12,000.

00

$ -

3,600.00

DTA

2018 $

54,000.00

$

21,600.00

$

16,000.00

$

9,600.00

-

$12,000.

00

$ -

3,600.00

DTA

2019 $

32,400.00

$

12,960.00

$

6,400.00

$

3,840.00

-

$9,120.0

0

$ -

2,736.00

DTA

Particulars Dr Cr

Profit &loss A/c $ 15,000.00

Deferred tax liability $ 15,000.00

B. Balance of deferred tax assets 30 June 2018

Particulars Dr Cr

Deferred tax assets $ -3600.00

Profit &loss A/c $ -3600.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

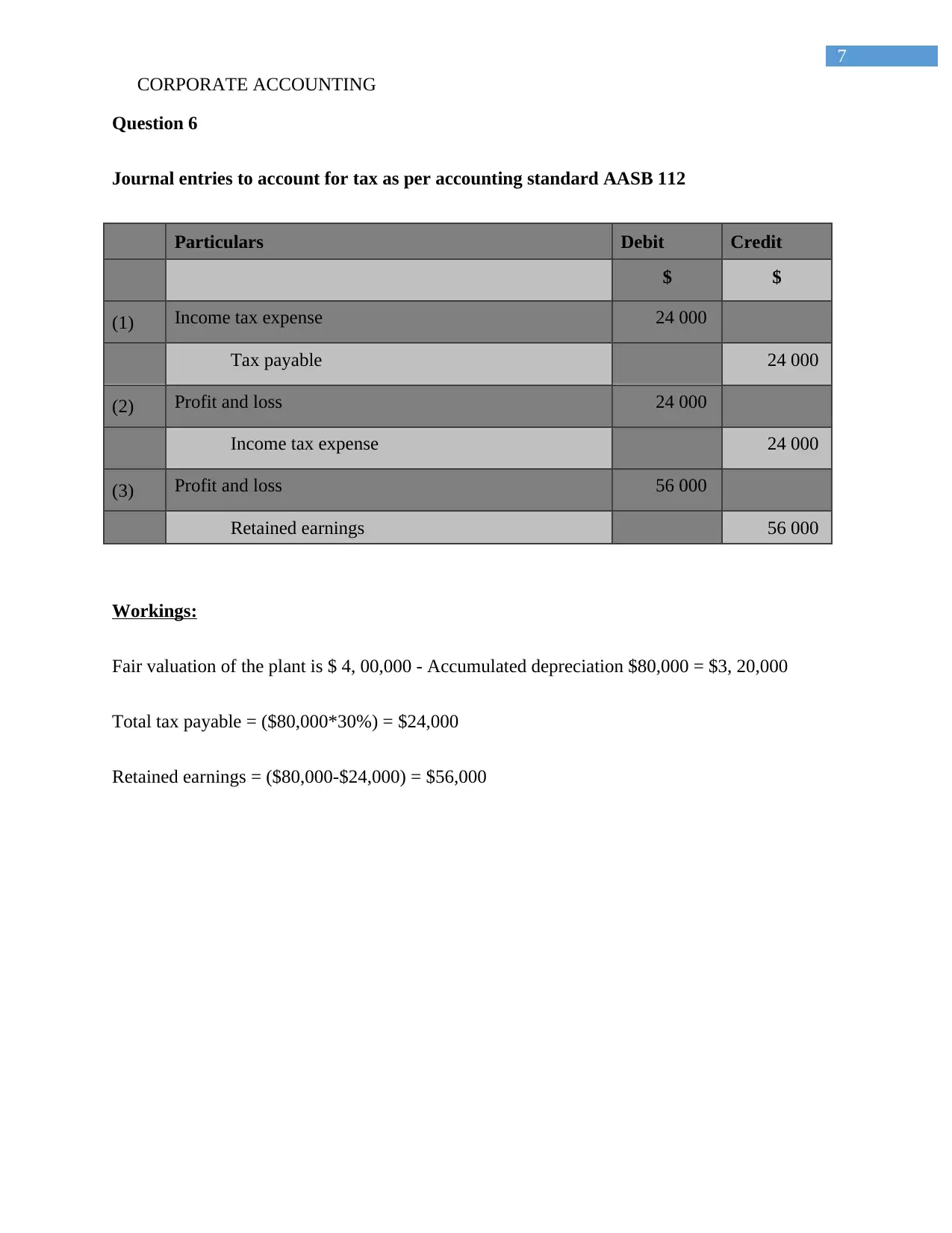

Question 6

Journal entries to account for tax as per accounting standard AASB 112

Particulars Debit Credit

$ $

(1) Income tax expense 24 000

Tax payable 24 000

(2) Profit and loss 24 000

Income tax expense 24 000

(3) Profit and loss 56 000

Retained earnings 56 000

Workings:

Fair valuation of the plant is $ 4, 00,000 - Accumulated depreciation $80,000 = $3, 20,000

Total tax payable = ($80,000*30%) = $24,000

Retained earnings = ($80,000-$24,000) = $56,000

CORPORATE ACCOUNTING

Question 6

Journal entries to account for tax as per accounting standard AASB 112

Particulars Debit Credit

$ $

(1) Income tax expense 24 000

Tax payable 24 000

(2) Profit and loss 24 000

Income tax expense 24 000

(3) Profit and loss 56 000

Retained earnings 56 000

Workings:

Fair valuation of the plant is $ 4, 00,000 - Accumulated depreciation $80,000 = $3, 20,000

Total tax payable = ($80,000*30%) = $24,000

Retained earnings = ($80,000-$24,000) = $56,000

8

CORPORATE ACCOUNTING

Question 7

Heritage Assets strengthen the economy. Their significance is much more than being a

tourist destination. Jobs are generated by their development as the number of visitors increase.

Creation of jobs improves the condition of economy of that place (Deegan 2013). Cost incurred

in maintenance of assets should be seen as an investment. Prime investors are private players,

government and municipality for its upkeep. After investment is gives handsome returns and

profits. When the Heritage place becomes famous business opportunities start to grow. Shops,

restaurants and street vendors thrive in that area.

Legacy of the heritage becomes center of attraction. Heritage Sites have been converted

into government offices in many places successfully. Due to commercialization of the locality

the quality and amount of business grows which helps the economy to flourish (Deegan

2013).Hence it can be said that these heritage places are assets and not liabilities as they do

wonders to add to the economy of that area.

CORPORATE ACCOUNTING

Question 7

Heritage Assets strengthen the economy. Their significance is much more than being a

tourist destination. Jobs are generated by their development as the number of visitors increase.

Creation of jobs improves the condition of economy of that place (Deegan 2013). Cost incurred

in maintenance of assets should be seen as an investment. Prime investors are private players,

government and municipality for its upkeep. After investment is gives handsome returns and

profits. When the Heritage place becomes famous business opportunities start to grow. Shops,

restaurants and street vendors thrive in that area.

Legacy of the heritage becomes center of attraction. Heritage Sites have been converted

into government offices in many places successfully. Due to commercialization of the locality

the quality and amount of business grows which helps the economy to flourish (Deegan

2013).Hence it can be said that these heritage places are assets and not liabilities as they do

wonders to add to the economy of that area.

9

CORPORATE ACCOUNTING

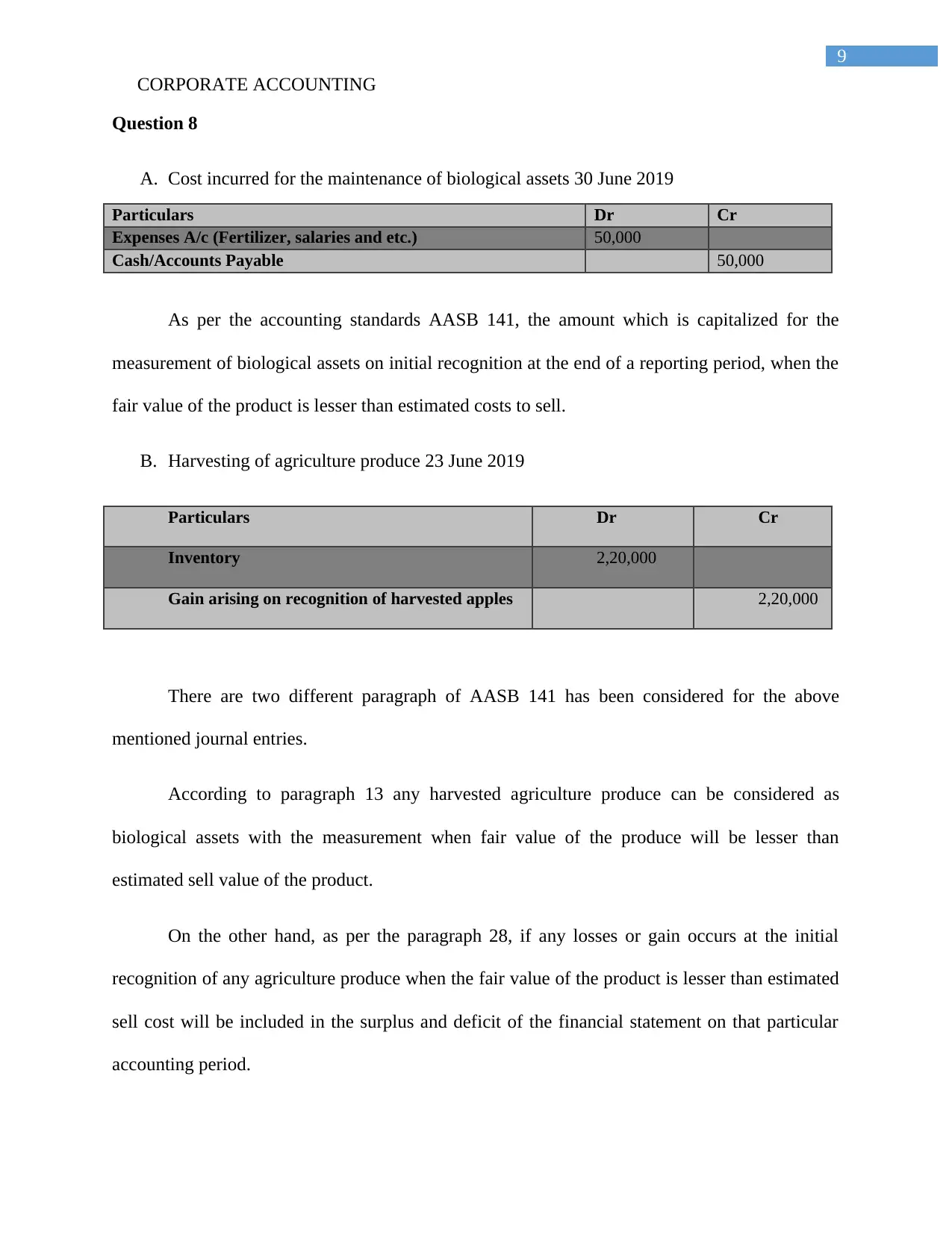

Question 8

A. Cost incurred for the maintenance of biological assets 30 June 2019

Particulars Dr Cr

Expenses A/c (Fertilizer, salaries and etc.) 50,000

Cash/Accounts Payable 50,000

As per the accounting standards AASB 141, the amount which is capitalized for the

measurement of biological assets on initial recognition at the end of a reporting period, when the

fair value of the product is lesser than estimated costs to sell.

B. Harvesting of agriculture produce 23 June 2019

Particulars Dr Cr

Inventory 2,20,000

Gain arising on recognition of harvested apples 2,20,000

There are two different paragraph of AASB 141 has been considered for the above

mentioned journal entries.

According to paragraph 13 any harvested agriculture produce can be considered as

biological assets with the measurement when fair value of the produce will be lesser than

estimated sell value of the product.

On the other hand, as per the paragraph 28, if any losses or gain occurs at the initial

recognition of any agriculture produce when the fair value of the product is lesser than estimated

sell cost will be included in the surplus and deficit of the financial statement on that particular

accounting period.

CORPORATE ACCOUNTING

Question 8

A. Cost incurred for the maintenance of biological assets 30 June 2019

Particulars Dr Cr

Expenses A/c (Fertilizer, salaries and etc.) 50,000

Cash/Accounts Payable 50,000

As per the accounting standards AASB 141, the amount which is capitalized for the

measurement of biological assets on initial recognition at the end of a reporting period, when the

fair value of the product is lesser than estimated costs to sell.

B. Harvesting of agriculture produce 23 June 2019

Particulars Dr Cr

Inventory 2,20,000

Gain arising on recognition of harvested apples 2,20,000

There are two different paragraph of AASB 141 has been considered for the above

mentioned journal entries.

According to paragraph 13 any harvested agriculture produce can be considered as

biological assets with the measurement when fair value of the produce will be lesser than

estimated sell value of the product.

On the other hand, as per the paragraph 28, if any losses or gain occurs at the initial

recognition of any agriculture produce when the fair value of the product is lesser than estimated

sell cost will be included in the surplus and deficit of the financial statement on that particular

accounting period.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

CORPORATE ACCOUNTING

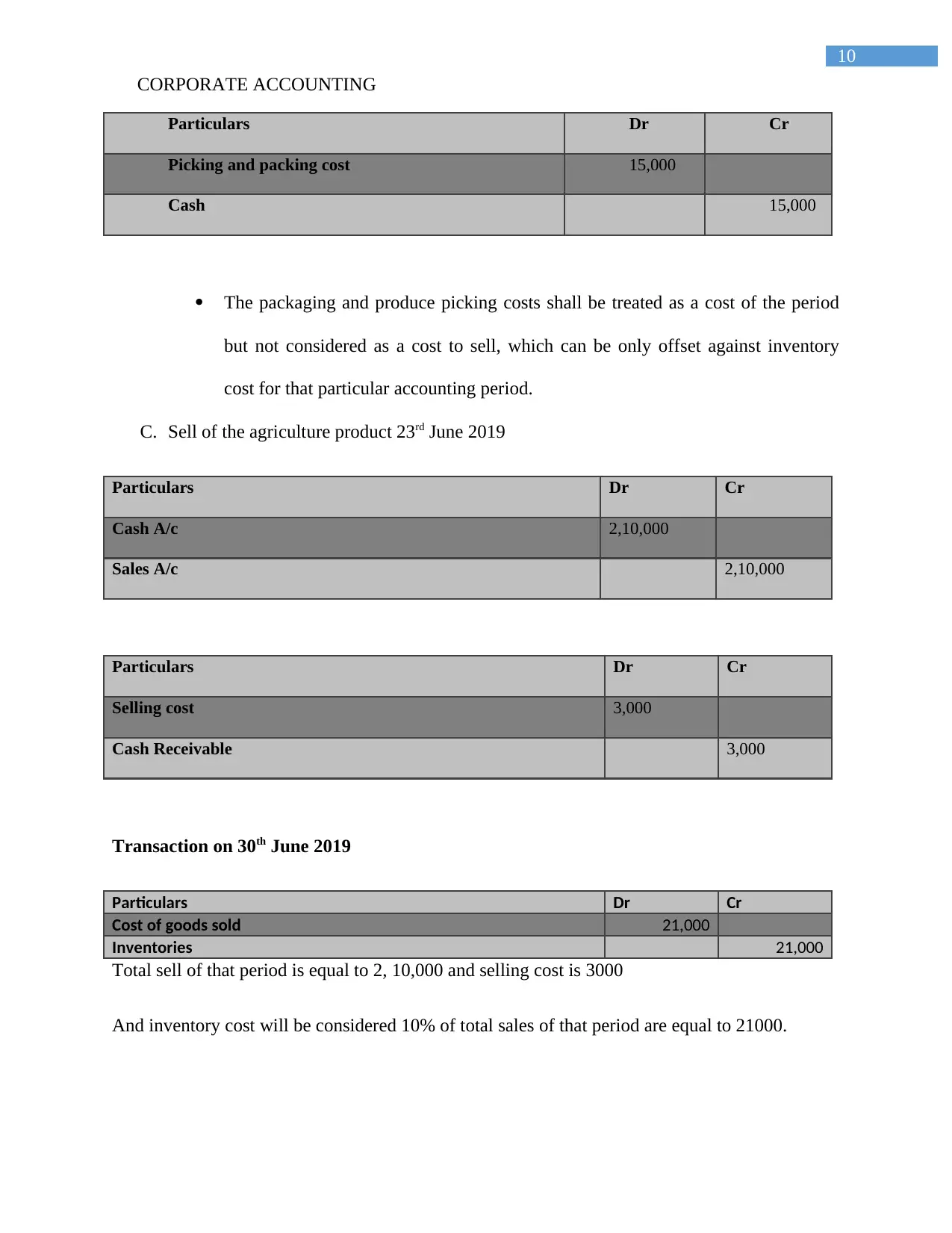

Particulars Dr Cr

Picking and packing cost 15,000

Cash 15,000

The packaging and produce picking costs shall be treated as a cost of the period

but not considered as a cost to sell, which can be only offset against inventory

cost for that particular accounting period.

C. Sell of the agriculture product 23rd June 2019

Particulars Dr Cr

Cash A/c 2,10,000

Sales A/c 2,10,000

Particulars Dr Cr

Selling cost 3,000

Cash Receivable 3,000

Transaction on 30th June 2019

Particulars Dr Cr

Cost of goods sold 21,000

Inventories 21,000

Total sell of that period is equal to 2, 10,000 and selling cost is 3000

And inventory cost will be considered 10% of total sales of that period are equal to 21000.

CORPORATE ACCOUNTING

Particulars Dr Cr

Picking and packing cost 15,000

Cash 15,000

The packaging and produce picking costs shall be treated as a cost of the period

but not considered as a cost to sell, which can be only offset against inventory

cost for that particular accounting period.

C. Sell of the agriculture product 23rd June 2019

Particulars Dr Cr

Cash A/c 2,10,000

Sales A/c 2,10,000

Particulars Dr Cr

Selling cost 3,000

Cash Receivable 3,000

Transaction on 30th June 2019

Particulars Dr Cr

Cost of goods sold 21,000

Inventories 21,000

Total sell of that period is equal to 2, 10,000 and selling cost is 3000

And inventory cost will be considered 10% of total sales of that period are equal to 21000.

11

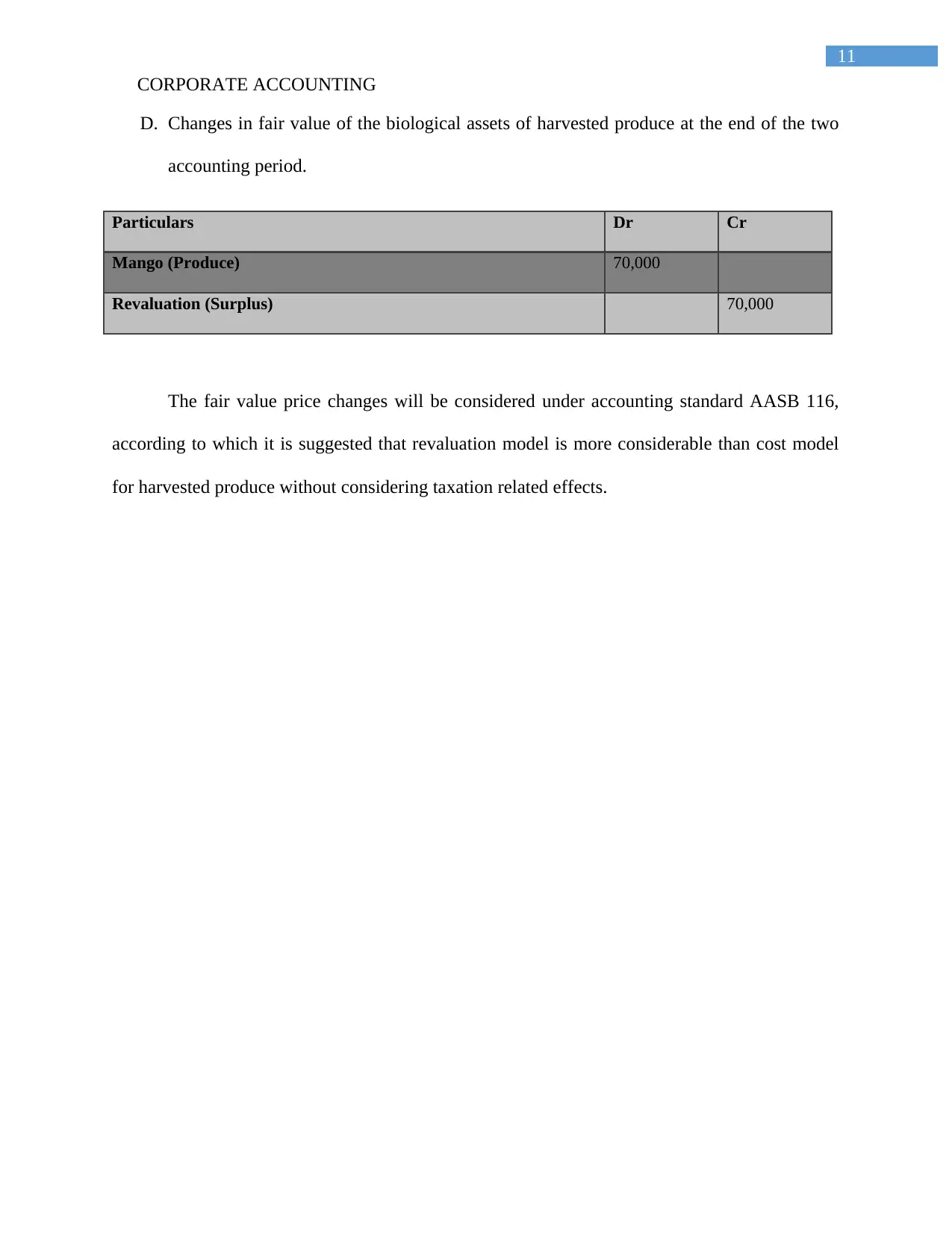

CORPORATE ACCOUNTING

D. Changes in fair value of the biological assets of harvested produce at the end of the two

accounting period.

Particulars Dr Cr

Mango (Produce) 70,000

Revaluation (Surplus) 70,000

The fair value price changes will be considered under accounting standard AASB 116,

according to which it is suggested that revaluation model is more considerable than cost model

for harvested produce without considering taxation related effects.

CORPORATE ACCOUNTING

D. Changes in fair value of the biological assets of harvested produce at the end of the two

accounting period.

Particulars Dr Cr

Mango (Produce) 70,000

Revaluation (Surplus) 70,000

The fair value price changes will be considered under accounting standard AASB 116,

according to which it is suggested that revaluation model is more considerable than cost model

for harvested produce without considering taxation related effects.

12

CORPORATE ACCOUNTING

Question 9

Implications passed for the quantitative tests given in the paragraph 13 of AASB are

following:

Profit on absolute amount is 10% of the reported combined profit for operating segments

without any loss record (Deegan 2013).

Declared assets earn 10% profit on combined assets of operational segments.

Listed revenue in operational segments is less than 70% of reportable segments. These

will not comply with paragraph 13 if applied (Deegan 2013).

If reportable segment of operation is identified as significant by management then it

should be immediately reported if it is not in compliance with Paragraph 13.

Reportable operational segments in real-time comply with quantitative threshold then

previous fragmented data for comparison should be recurring to masquerade into individual

fragment even if it differs from Paragraph 13 (Deegan 2013).

CORPORATE ACCOUNTING

Question 9

Implications passed for the quantitative tests given in the paragraph 13 of AASB are

following:

Profit on absolute amount is 10% of the reported combined profit for operating segments

without any loss record (Deegan 2013).

Declared assets earn 10% profit on combined assets of operational segments.

Listed revenue in operational segments is less than 70% of reportable segments. These

will not comply with paragraph 13 if applied (Deegan 2013).

If reportable segment of operation is identified as significant by management then it

should be immediately reported if it is not in compliance with Paragraph 13.

Reportable operational segments in real-time comply with quantitative threshold then

previous fragmented data for comparison should be recurring to masquerade into individual

fragment even if it differs from Paragraph 13 (Deegan 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

CORPORATE ACCOUNTING

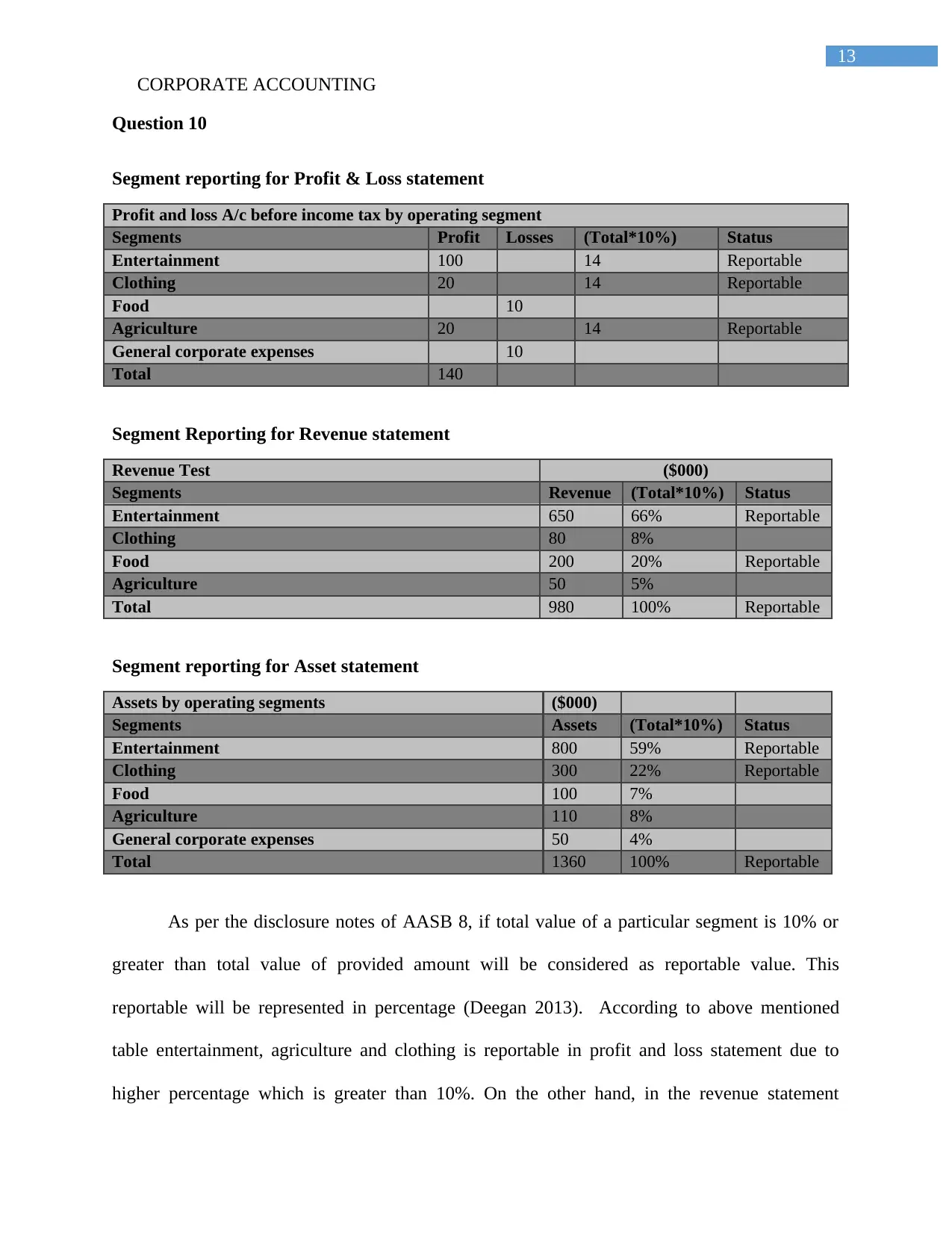

Question 10

Segment reporting for Profit & Loss statement

Profit and loss A/c before income tax by operating segment

Segments Profit Losses (Total*10%) Status

Entertainment 100 14 Reportable

Clothing 20 14 Reportable

Food 10

Agriculture 20 14 Reportable

General corporate expenses 10

Total 140

Segment Reporting for Revenue statement

Revenue Test ($000)

Segments Revenue (Total*10%) Status

Entertainment 650 66% Reportable

Clothing 80 8%

Food 200 20% Reportable

Agriculture 50 5%

Total 980 100% Reportable

Segment reporting for Asset statement

Assets by operating segments ($000)

Segments Assets (Total*10%) Status

Entertainment 800 59% Reportable

Clothing 300 22% Reportable

Food 100 7%

Agriculture 110 8%

General corporate expenses 50 4%

Total 1360 100% Reportable

As per the disclosure notes of AASB 8, if total value of a particular segment is 10% or

greater than total value of provided amount will be considered as reportable value. This

reportable will be represented in percentage (Deegan 2013). According to above mentioned

table entertainment, agriculture and clothing is reportable in profit and loss statement due to

higher percentage which is greater than 10%. On the other hand, in the revenue statement

CORPORATE ACCOUNTING

Question 10

Segment reporting for Profit & Loss statement

Profit and loss A/c before income tax by operating segment

Segments Profit Losses (Total*10%) Status

Entertainment 100 14 Reportable

Clothing 20 14 Reportable

Food 10

Agriculture 20 14 Reportable

General corporate expenses 10

Total 140

Segment Reporting for Revenue statement

Revenue Test ($000)

Segments Revenue (Total*10%) Status

Entertainment 650 66% Reportable

Clothing 80 8%

Food 200 20% Reportable

Agriculture 50 5%

Total 980 100% Reportable

Segment reporting for Asset statement

Assets by operating segments ($000)

Segments Assets (Total*10%) Status

Entertainment 800 59% Reportable

Clothing 300 22% Reportable

Food 100 7%

Agriculture 110 8%

General corporate expenses 50 4%

Total 1360 100% Reportable

As per the disclosure notes of AASB 8, if total value of a particular segment is 10% or

greater than total value of provided amount will be considered as reportable value. This

reportable will be represented in percentage (Deegan 2013). According to above mentioned

table entertainment, agriculture and clothing is reportable in profit and loss statement due to

higher percentage which is greater than 10%. On the other hand, in the revenue statement

14

CORPORATE ACCOUNTING

entertainment and food segments are highly reportable whereas, in the assets statement

entertainment again with clothing segment is reportable.

CORPORATE ACCOUNTING

entertainment and food segments are highly reportable whereas, in the assets statement

entertainment again with clothing segment is reportable.

15

CORPORATE ACCOUNTING

References

Bebbington, J., Unerman, J. and O'Dwyer, B. eds., 2014. Sustainability accounting and

accountability. Routledge.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

CORPORATE ACCOUNTING

References

Bebbington, J., Unerman, J. and O'Dwyer, B. eds., 2014. Sustainability accounting and

accountability. Routledge.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.