HI5020: Corporate Accounting Report: Westpac & ANZ Analysis

VerifiedAdded on 2023/06/03

|17

|4387

|74

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting, focusing on financial statements and the application of accounting principles in business contexts. The report examines key components of financial statements including owner's equity, cash flow statements, and other comprehensive income statements. A comparative analysis is conducted, using the Westpac Banking Group and ANZ Banking Group as examples, to illustrate the practical application of accounting concepts in the corporate world. The analysis includes a detailed examination of owner's equity items, changes in cash flows, and the reporting of various items in the other comprehensive income statement. The report also provides insights into the debt and equity positions of the chosen companies. The report aims to improve understanding of corporate accounting and its use in financial analysis within businesses.

Corporate Accounting 1

Corporate Accounting

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 2

Executive Summary

This report aims to create a better understanding of corporate accounting and its use in financial

analysis in businesses. Corporate accounting was termed as the study of accounting process

which clears the concept related to corporate activities and financial decisions. Reliability and

relevancy of accounting and financial has been explained in this assuagement on the basis of

financial and operational changes occurred in business transactions. This work articulates about

owner’s equity, their sources, and cash flow demands and study of changes in financial

statements and of the annual report of chosen, for this purpose, company which have been taken

for example are Westpac Banking group & ANZ banking group. This report depicts the specific

knowledge of financial accounting analysis in corporate business.

Executive Summary

This report aims to create a better understanding of corporate accounting and its use in financial

analysis in businesses. Corporate accounting was termed as the study of accounting process

which clears the concept related to corporate activities and financial decisions. Reliability and

relevancy of accounting and financial has been explained in this assuagement on the basis of

financial and operational changes occurred in business transactions. This work articulates about

owner’s equity, their sources, and cash flow demands and study of changes in financial

statements and of the annual report of chosen, for this purpose, company which have been taken

for example are Westpac Banking group & ANZ banking group. This report depicts the specific

knowledge of financial accounting analysis in corporate business.

Corporate Accounting 3

Table of Contents

Executive Summary.........................................................................................................................2

Introduction:....................................................................................................................................4

Owner’s Equity................................................................................................................................5

Cash Flows Statement......................................................................................................................7

Other Comprehensive Income Statement........................................................................................9

Accounting for Corporate Income Tax..........................................................................................11

Conclusion:....................................................................................................................................15

References......................................................................................................................................16

Table of Contents

Executive Summary.........................................................................................................................2

Introduction:....................................................................................................................................4

Owner’s Equity................................................................................................................................5

Cash Flows Statement......................................................................................................................7

Other Comprehensive Income Statement........................................................................................9

Accounting for Corporate Income Tax..........................................................................................11

Conclusion:....................................................................................................................................15

References......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 4

Introduction:

The annual report depicts a clear picture of financial status and condition of companies.

Financial statements are verified and analyzed in order to review the stability and position of the

company. In this reading, the major purpose of preparing this report is to make proper and

effective understanding of various financial statements which includes four parts, owner’s

equity, cash flow statements, income statements and comparative analysis between both chosen

company. Westpac banking and ANZ banking group will be taken into observation for financial

analysis which includes sources of owner’s equity and changes, comparative analysis of cash

flow changes within organizations etc. it will depict the knowledge of debt and equity relation

incurred in financial last financial years.

Introduction:

The annual report depicts a clear picture of financial status and condition of companies.

Financial statements are verified and analyzed in order to review the stability and position of the

company. In this reading, the major purpose of preparing this report is to make proper and

effective understanding of various financial statements which includes four parts, owner’s

equity, cash flow statements, income statements and comparative analysis between both chosen

company. Westpac banking and ANZ banking group will be taken into observation for financial

analysis which includes sources of owner’s equity and changes, comparative analysis of cash

flow changes within organizations etc. it will depict the knowledge of debt and equity relation

incurred in financial last financial years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 5

Owner’s Equity

(I)List of each item of equity and understanding & Changes in each item of equity

Owner’s equity: Owner’s equity is that equity which can be taken as a source of organizational

assets. Owner’s equity is the major word which can be used in the terms of a list of equity which

includes following things:

Common Stock: the common stock of owner’s equity can be taken ass ordinary shares of the

company, which was 275 in 2017 in Westpac Company; it was higher than the common stock of

ANZ Banking Limited.

Preferred Stock: Preferred stock: The unit of the share which is entitled to the stakeholders as a

fixed unit of dividend, whose payment has given the higher priority than the other ordinary stock

in the company. In 2017 Preferred stock of the Westpac banking was 2750 and 1974 in 2016

which has been increasing in the last five years. ANZ banking group’s preferred equity was nil

from last two years.

Retain Earning: Retained earnings are those profits which can be divided into profit, cash,

bonuses and dividend among shareholders. Total retain profit were 26,100 in 2017 of Westpac

banking and ANZ defined Retained profit around 18765 in 2017.

Accumulated other comprehensive income

In financial accounts of Westpac and ANZ banking group, it is needed to make of list of equity

items mentioned in the balance sheet of the companies.

In the financial statement of Westpac banking group, equity items which listed are: banking

corporations, total non-controlling interests, reserves, retained profits etc. on the other hand the

list of equity stated in the financial statement of ANZ Banking Group Company are: common

stocks, merged stocks and retained earning etc. The company has treasury stock which was in the

form of paid-in capital (Law, 2018).

Owner’s Equity

(I)List of each item of equity and understanding & Changes in each item of equity

Owner’s equity: Owner’s equity is that equity which can be taken as a source of organizational

assets. Owner’s equity is the major word which can be used in the terms of a list of equity which

includes following things:

Common Stock: the common stock of owner’s equity can be taken ass ordinary shares of the

company, which was 275 in 2017 in Westpac Company; it was higher than the common stock of

ANZ Banking Limited.

Preferred Stock: Preferred stock: The unit of the share which is entitled to the stakeholders as a

fixed unit of dividend, whose payment has given the higher priority than the other ordinary stock

in the company. In 2017 Preferred stock of the Westpac banking was 2750 and 1974 in 2016

which has been increasing in the last five years. ANZ banking group’s preferred equity was nil

from last two years.

Retain Earning: Retained earnings are those profits which can be divided into profit, cash,

bonuses and dividend among shareholders. Total retain profit were 26,100 in 2017 of Westpac

banking and ANZ defined Retained profit around 18765 in 2017.

Accumulated other comprehensive income

In financial accounts of Westpac and ANZ banking group, it is needed to make of list of equity

items mentioned in the balance sheet of the companies.

In the financial statement of Westpac banking group, equity items which listed are: banking

corporations, total non-controlling interests, reserves, retained profits etc. on the other hand the

list of equity stated in the financial statement of ANZ Banking Group Company are: common

stocks, merged stocks and retained earning etc. The company has treasury stock which was in the

form of paid-in capital (Law, 2018).

Corporate Accounting 6

Changes in cash proceed and expenditure off the company regarding projects to offer and boost

assets of the company. Common stock is a type of corporate value proprietorship, a sort of

security. The terms voting offer and standard offer are likewise utilized as often as possible in

different parts of the world. Thus there is the reason behind changes in equity lists when

reserves, cash and profits make large effects on it due to changes. Turing of profits: changes in

stocks’ equity such as retained earnings, cash, merged stock etc would be increased with the

increment in business profits. A preferred stock is a class of proprietorship in an enterprise that

has a higher case on its advantages and profit than basic stock. Favoured offers by and large have

a profit that must be paid out before profits to basic investors, and the offers, as a rule, don't

convey voting rights. In the financial statement of Westpac Company, the retained earnings and

other stock’s equity are increased from last five years. Retained earnings are the benefits that an

organization has earned to date, less any profits or different disseminations paid to financial

specialists. This sum is balanced at whatever point there is a passage to the bookkeeping records

that effects an income or cost account. Retained earnings were 26,100 in 2107 which was

increased due to business profits. In the financial statement of the ANZ banking group, all lists of

equity are decreased years by years. In 2016, it was 77, 46 m and in 2017, it was reduced due to

total deposits and investment in a number of the asset (Khan, et. al., 2016). Accumulated other

comprehensive income is a general record account that is ordered inside the value segment of the

monetary record. It is utilized to gather undiscovered increases and hidden misfortunes on those

details in the salary articulation that are characterized inside the other thorough pay class.

(II)Comparative analysis of the debt and equity position between both firms:

ANZ banking group & Westpac banking group: Deferred no cash items and deferral payments of

different compensation emphasizes. Such deferral part granted as an equity performance ANZ

banking group and vested from last 3 years which increased the effect upon debt and equity

relation in the company. On another hand, Westpac Company has created debt issues around

Changes in cash proceed and expenditure off the company regarding projects to offer and boost

assets of the company. Common stock is a type of corporate value proprietorship, a sort of

security. The terms voting offer and standard offer are likewise utilized as often as possible in

different parts of the world. Thus there is the reason behind changes in equity lists when

reserves, cash and profits make large effects on it due to changes. Turing of profits: changes in

stocks’ equity such as retained earnings, cash, merged stock etc would be increased with the

increment in business profits. A preferred stock is a class of proprietorship in an enterprise that

has a higher case on its advantages and profit than basic stock. Favoured offers by and large have

a profit that must be paid out before profits to basic investors, and the offers, as a rule, don't

convey voting rights. In the financial statement of Westpac Company, the retained earnings and

other stock’s equity are increased from last five years. Retained earnings are the benefits that an

organization has earned to date, less any profits or different disseminations paid to financial

specialists. This sum is balanced at whatever point there is a passage to the bookkeeping records

that effects an income or cost account. Retained earnings were 26,100 in 2107 which was

increased due to business profits. In the financial statement of the ANZ banking group, all lists of

equity are decreased years by years. In 2016, it was 77, 46 m and in 2017, it was reduced due to

total deposits and investment in a number of the asset (Khan, et. al., 2016). Accumulated other

comprehensive income is a general record account that is ordered inside the value segment of the

monetary record. It is utilized to gather undiscovered increases and hidden misfortunes on those

details in the salary articulation that are characterized inside the other thorough pay class.

(II)Comparative analysis of the debt and equity position between both firms:

ANZ banking group & Westpac banking group: Deferred no cash items and deferral payments of

different compensation emphasizes. Such deferral part granted as an equity performance ANZ

banking group and vested from last 3 years which increased the effect upon debt and equity

relation in the company. On another hand, Westpac Company has created debt issues around

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 7

168,356 and 169,902 in 2016. Total retain profit were 26,100 in 2017 and reserve was 794

million as per the list of the equity. The position and debt-equity condition of the Westpac

banking are good (Gordon, et. al., 2017).

Cash Flows Statement

(III)List each item reported in the cash flows statement and discussion of changes into of

each item.

Westpac Banking group:

In the financial statement and cash flow statement of Westpac banking group, it has been

segregated into three parts, in the operating cash flow point view, interest is given and received;

dividend received excluding life insurance and other non related noncash items have been

mentioned. In other life businesses, receipts from shareholders, the interest of dividend have

been given. Total cash operation activities were 2820 million in 2017 and 5497 million in 2016.

The total cash flow from investing activity includes proceeds and purchase of available of resale

securities, net purchase for assets intangible and purchase of disposal and property. Total cash

flow from investing activity was 1698 million in 2017 which were in loss. And it was 7245

million loss which less more than 2017. The reason of behind such kind of changes was

company faced losses due to higher purchases than sales from which companies faced

difficulties in cash

Flow from investing activity (Gitman, et. al., 2015).

ANZ banking group: in the year of 2017, cash from operating activities around 6060 and total

cash flow were around 23657 million in the company the major fluctuation behind this changes

in income tax paid and operating expenses and income. Cash flow form fund management and

insurance business created great differences between in the cash flow from operations in last two

years. Cash flow from investing activity was around 14,410 and 9776 loss in both the year 2017

168,356 and 169,902 in 2016. Total retain profit were 26,100 in 2017 and reserve was 794

million as per the list of the equity. The position and debt-equity condition of the Westpac

banking are good (Gordon, et. al., 2017).

Cash Flows Statement

(III)List each item reported in the cash flows statement and discussion of changes into of

each item.

Westpac Banking group:

In the financial statement and cash flow statement of Westpac banking group, it has been

segregated into three parts, in the operating cash flow point view, interest is given and received;

dividend received excluding life insurance and other non related noncash items have been

mentioned. In other life businesses, receipts from shareholders, the interest of dividend have

been given. Total cash operation activities were 2820 million in 2017 and 5497 million in 2016.

The total cash flow from investing activity includes proceeds and purchase of available of resale

securities, net purchase for assets intangible and purchase of disposal and property. Total cash

flow from investing activity was 1698 million in 2017 which were in loss. And it was 7245

million loss which less more than 2017. The reason of behind such kind of changes was

company faced losses due to higher purchases than sales from which companies faced

difficulties in cash

Flow from investing activity (Gitman, et. al., 2015).

ANZ banking group: in the year of 2017, cash from operating activities around 6060 and total

cash flow were around 23657 million in the company the major fluctuation behind this changes

in income tax paid and operating expenses and income. Cash flow form fund management and

insurance business created great differences between in the cash flow from operations in last two

years. Cash flow from investing activity was around 14,410 and 9776 loss in both the year 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 8

and 2016 respectively. The reason behind such changes was the availability of resale of assets,

higher purchases than sales activity and Sandal dealer finance divestment (Patel, et. al., 2017).

(IV) Comparative analysis of organizational three broad categories of cash flows

Comparative analysis between both companies:

Cash flow from operating activities: in the financial statement of the ANZ banking group, the

cash flow from operating activity in 2017 was 6060 and in Westpac banking group it was around

2820 million in 2017. In 2016 it was 23,367, so in the comparative analysis, it can be observed

that Westpac banking company condition is better than the ANZ banking group (Gordon, et. al.,

2017).

Cash flow from investment: in this activity, Westpac Company invests in the purchase of

available securities of resale assets, purchase of property and equipment and proceeds from share

entitlement offers, due to this, cash flow from investing activity was 1698 million in 2017 and

7245 million in 2016 (Free Cash Flow, .2016) ANZ banking group invested in net increment of

debt shares, redemption on loan capital, proceeded from exercise of employee options and

dividend reinvestment plan under while. Total cash flow from investment was 552 million and

3573 million in 2017 and 2106 respectively. On the other hand, the total investment cash flow

for ANZ was & in 2017 and 2016 (Flannery, 2016).

Company 2017(in $) 2016(in $) 2015(in $)

Westpac banking group 9,356000 8,393000 4,685000

ANZ BANKING limited 5,184,389 6,804,740 5,071,462

(V)Insights that you can get from the comparative analysis:

Comparative analysis: there are a number of items which are involved in the statement of cash

flow related to hedges, foreign investment, proceeds and purchase of resale and available

and 2016 respectively. The reason behind such changes was the availability of resale of assets,

higher purchases than sales activity and Sandal dealer finance divestment (Patel, et. al., 2017).

(IV) Comparative analysis of organizational three broad categories of cash flows

Comparative analysis between both companies:

Cash flow from operating activities: in the financial statement of the ANZ banking group, the

cash flow from operating activity in 2017 was 6060 and in Westpac banking group it was around

2820 million in 2017. In 2016 it was 23,367, so in the comparative analysis, it can be observed

that Westpac banking company condition is better than the ANZ banking group (Gordon, et. al.,

2017).

Cash flow from investment: in this activity, Westpac Company invests in the purchase of

available securities of resale assets, purchase of property and equipment and proceeds from share

entitlement offers, due to this, cash flow from investing activity was 1698 million in 2017 and

7245 million in 2016 (Free Cash Flow, .2016) ANZ banking group invested in net increment of

debt shares, redemption on loan capital, proceeded from exercise of employee options and

dividend reinvestment plan under while. Total cash flow from investment was 552 million and

3573 million in 2017 and 2106 respectively. On the other hand, the total investment cash flow

for ANZ was & in 2017 and 2016 (Flannery, 2016).

Company 2017(in $) 2016(in $) 2015(in $)

Westpac banking group 9,356000 8,393000 4,685000

ANZ BANKING limited 5,184,389 6,804,740 5,071,462

(V)Insights that you can get from the comparative analysis:

Comparative analysis: there are a number of items which are involved in the statement of cash

flow related to hedges, foreign investment, proceeds and purchase of resale and available

Corporate Accounting 9

investment, incomes tax or stables security and unsecured loans and advances. The reason for not

including such things in the other financial statement is that results related to all transactions

occur rarely. Hence while preparing incomes and expenses, dividend and other business

transactions, which occurs on a regular basis which affects cash flow behaviour are basically

related to discounting operations from cash flow activity is based on stables security holder

(Hall, et. al., 2016). The Air New Zealand is also making the payment of the tax and for that, the

expenses which have been recognized in the income statements is $150 (Air New Zealand

limited, 2018). These are the amounts which are calculated on the net profit which has been

made by the companies in the current financial year.

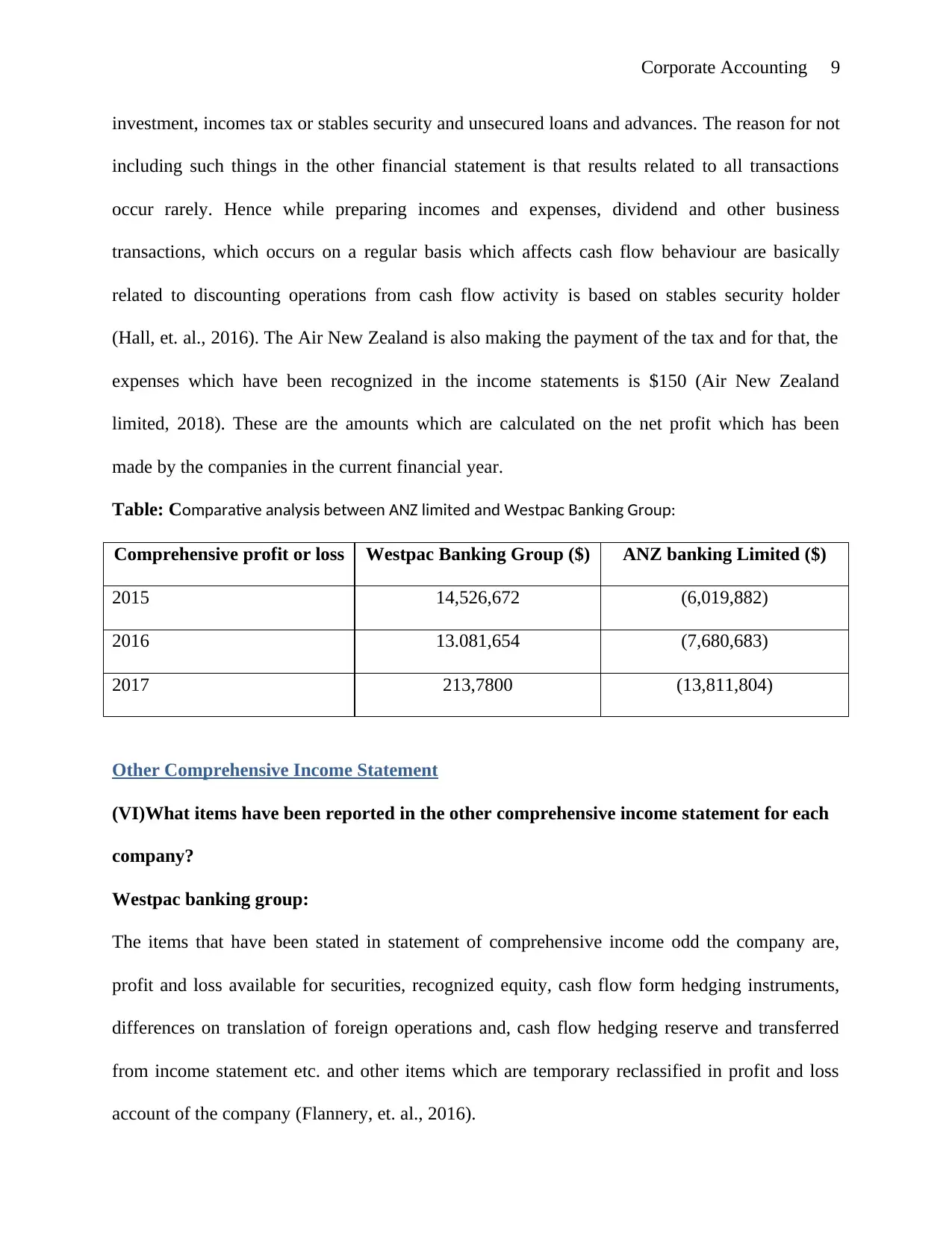

Table: Comparative analysis between ANZ limited and Westpac Banking Group:

Comprehensive profit or loss Westpac Banking Group ($) ANZ banking Limited ($)

2015 14,526,672 (6,019,882)

2016 13.081,654 (7,680,683)

2017 213,7800 (13,811,804)

Other Comprehensive Income Statement

(VI)What items have been reported in the other comprehensive income statement for each

company?

Westpac banking group:

The items that have been stated in statement of comprehensive income odd the company are,

profit and loss available for securities, recognized equity, cash flow form hedging instruments,

differences on translation of foreign operations and, cash flow hedging reserve and transferred

from income statement etc. and other items which are temporary reclassified in profit and loss

account of the company (Flannery, et. al., 2016).

investment, incomes tax or stables security and unsecured loans and advances. The reason for not

including such things in the other financial statement is that results related to all transactions

occur rarely. Hence while preparing incomes and expenses, dividend and other business

transactions, which occurs on a regular basis which affects cash flow behaviour are basically

related to discounting operations from cash flow activity is based on stables security holder

(Hall, et. al., 2016). The Air New Zealand is also making the payment of the tax and for that, the

expenses which have been recognized in the income statements is $150 (Air New Zealand

limited, 2018). These are the amounts which are calculated on the net profit which has been

made by the companies in the current financial year.

Table: Comparative analysis between ANZ limited and Westpac Banking Group:

Comprehensive profit or loss Westpac Banking Group ($) ANZ banking Limited ($)

2015 14,526,672 (6,019,882)

2016 13.081,654 (7,680,683)

2017 213,7800 (13,811,804)

Other Comprehensive Income Statement

(VI)What items have been reported in the other comprehensive income statement for each

company?

Westpac banking group:

The items that have been stated in statement of comprehensive income odd the company are,

profit and loss available for securities, recognized equity, cash flow form hedging instruments,

differences on translation of foreign operations and, cash flow hedging reserve and transferred

from income statement etc. and other items which are temporary reclassified in profit and loss

account of the company (Flannery, et. al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 10

ANZ banking group:

The items which are listed in the financial comprehensive of the company are reclassified items

of profit and loss account, cash flow hedging activities related to investment and projects, shares

of associates within other comprehensive income, credit instrument of financial liabilities at par

and fair value. The foreign currency translations are there which have been included in this and

with that, the other incomes from the investments are also incorporated. The defined benefits

which are there are also taken into consideration in this. The tax which is there in relation to

them is also taken into account and the same is also made for the Air New Zealand.

(Vii) Reasons for items not been reported in Income Statement:

The net income statement means profit and loss statements are considered as long-term capital

financial books of the company t measure long-term financial performance. Its’ results are

oriented with the past movement basically to measure the progress of the entity of the

companies. But comprehensive income statement is the new concept which indicates informs

performance and possibilities to obtain accounting results related to expenses and incomes.

Comprehensive income stats those entries and transactions which are net income and gains

directly recorded in the equity, its results are disclosed at the end of the financial year in the

profit and loss account but calculation which are not made in P&L account would be shown in

the comprehensive income statements (Bratten, et. al., 2016).

(viii) Comparative analysis of the items shown in the other comprehensive income

statement section for the two companies.

Comparative analysis of the comprehensive income statement of both companies:

Comprehensive income statement of Westpac Company includes various entries such as profit

and loss on available sale series of securities which was 7997 million in 2017 and

Comprehensive incomes statement of ANZ Banking group stats that profit or losses from sales

for securities were around 72 million losses. Remeasurement gain of issues of shares and

ANZ banking group:

The items which are listed in the financial comprehensive of the company are reclassified items

of profit and loss account, cash flow hedging activities related to investment and projects, shares

of associates within other comprehensive income, credit instrument of financial liabilities at par

and fair value. The foreign currency translations are there which have been included in this and

with that, the other incomes from the investments are also incorporated. The defined benefits

which are there are also taken into consideration in this. The tax which is there in relation to

them is also taken into account and the same is also made for the Air New Zealand.

(Vii) Reasons for items not been reported in Income Statement:

The net income statement means profit and loss statements are considered as long-term capital

financial books of the company t measure long-term financial performance. Its’ results are

oriented with the past movement basically to measure the progress of the entity of the

companies. But comprehensive income statement is the new concept which indicates informs

performance and possibilities to obtain accounting results related to expenses and incomes.

Comprehensive income stats those entries and transactions which are net income and gains

directly recorded in the equity, its results are disclosed at the end of the financial year in the

profit and loss account but calculation which are not made in P&L account would be shown in

the comprehensive income statements (Bratten, et. al., 2016).

(viii) Comparative analysis of the items shown in the other comprehensive income

statement section for the two companies.

Comparative analysis of the comprehensive income statement of both companies:

Comprehensive income statement of Westpac Company includes various entries such as profit

and loss on available sale series of securities which was 7997 million in 2017 and

Comprehensive incomes statement of ANZ Banking group stats that profit or losses from sales

for securities were around 72 million losses. Remeasurement gain of issues of shares and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 11

attributive changes in benefit plans were 11 million in ANZ Banking Company. Company has

earned around 3 million form fair values of changes in credit risk of financial liabilities. On the

other hand, the Westpac banking group has losses around 164 million amount from the fair value

of attributable changes in financial liabilities. Remeasurement of definite profit obtained from

equity based on net tax value was around 3 million as a profit. Total comprehensive profit for the

year was 7991 million in the FY2017 for Westpac banking group and ANZ banking earned

around 5135 million in 2017 financial years which were less than Westpac (Black, 2016).

Accounting for Corporate Income Tax

(x) Tax expenses shown in the latest financial statements of companies:

ANZ banking group:

Income tax expenses recognized which are recognized in the income statement of the company

in the form of current expense tax were 2778 million and adjustment recognized in the relation to

previous year tax expenses were around 23 million presenting loss. Toa income tax expenses

chargeable in income tax statement were 2458 m. in 2017, where the tax expense of Westpac

Banking group has been rated around 30% statutory rate of Australian standards. Total tax

expense from adjustable business rates tax duties were 1 million in the loss. Total income tax

expenses were 3518 million in 2017 which was comparatively higher than the ANZ banking

group (Air New Zealand limited. 2018)

(xi) Calculate the effective tax rate

Westpac banking group:

Income tax expense / earnings before tax = 3518 (million) / 11515 (million) *100

= 30.55%

ANZ banking group:

Income tax expense / earnings before tax = 2458 / 8178 * 100

= 30.05%

attributive changes in benefit plans were 11 million in ANZ Banking Company. Company has

earned around 3 million form fair values of changes in credit risk of financial liabilities. On the

other hand, the Westpac banking group has losses around 164 million amount from the fair value

of attributable changes in financial liabilities. Remeasurement of definite profit obtained from

equity based on net tax value was around 3 million as a profit. Total comprehensive profit for the

year was 7991 million in the FY2017 for Westpac banking group and ANZ banking earned

around 5135 million in 2017 financial years which were less than Westpac (Black, 2016).

Accounting for Corporate Income Tax

(x) Tax expenses shown in the latest financial statements of companies:

ANZ banking group:

Income tax expenses recognized which are recognized in the income statement of the company

in the form of current expense tax were 2778 million and adjustment recognized in the relation to

previous year tax expenses were around 23 million presenting loss. Toa income tax expenses

chargeable in income tax statement were 2458 m. in 2017, where the tax expense of Westpac

Banking group has been rated around 30% statutory rate of Australian standards. Total tax

expense from adjustable business rates tax duties were 1 million in the loss. Total income tax

expenses were 3518 million in 2017 which was comparatively higher than the ANZ banking

group (Air New Zealand limited. 2018)

(xi) Calculate the effective tax rate

Westpac banking group:

Income tax expense / earnings before tax = 3518 (million) / 11515 (million) *100

= 30.55%

ANZ banking group:

Income tax expense / earnings before tax = 2458 / 8178 * 100

= 30.05%

Corporate Accounting 12

An effective tax of Westpac banking group is higher than a tax of ANZ banking group.

(xii) Deferred tax assets/liabilities reported in the balance sheet:

Deferred tax liability and asset are accounted for using the comprehensive tax balance with the

flow changes in reclassified in guaranteed temporary differences to carry out deferred tax

liabilities and assets. Deferred tax assets and liabilities affect income tax gain and losses or

companies attributive credit to be setting them off and carried forward. Deferred tax expense

related to the origin of reversal of temporary differences was 257 losses. Deferred tax assets were

457 million in Australia of ANZ banking group and 38 m in Asia Pacific areas in 2017. The total

was 623 million in 2017. Deferred tax assets recognized by profit and loss account was 1804

million and recognized in equity was nil (zero) in FY17 due to the availability of resale

revaluation reserve in Westpac banking group (Atanasov and Black, 2016).

(xiii) Reason for increase or decrease in the deferred tax assets or in the deferred tax

liability:

Yes, it is observed that there is a changes in deferred tax assets and liabilities in the financial

year of 2017 in both companies financial statement, financial statement of both company

indicates that total deferred tax assets from equity was nil and deferred tax assets from resale

from recognized directly in profit and loss were 1804 which was 1639 million in 2016. Total

deferred tax assets were 603 million, 465 million respectively in 2016 and 2015 in ANZ banking

group. In the case of Westpac Banking group, the deferred tax asset was 545 million in 2017 and

liabilities were 10 million in FY17. It was decreased compared to FY2016 when it was 36

million. Total deferred tax liability to set deferred tax asset were 580 million in loss (Coleman,

et. al., 2016).

An effective tax of Westpac banking group is higher than a tax of ANZ banking group.

(xii) Deferred tax assets/liabilities reported in the balance sheet:

Deferred tax liability and asset are accounted for using the comprehensive tax balance with the

flow changes in reclassified in guaranteed temporary differences to carry out deferred tax

liabilities and assets. Deferred tax assets and liabilities affect income tax gain and losses or

companies attributive credit to be setting them off and carried forward. Deferred tax expense

related to the origin of reversal of temporary differences was 257 losses. Deferred tax assets were

457 million in Australia of ANZ banking group and 38 m in Asia Pacific areas in 2017. The total

was 623 million in 2017. Deferred tax assets recognized by profit and loss account was 1804

million and recognized in equity was nil (zero) in FY17 due to the availability of resale

revaluation reserve in Westpac banking group (Atanasov and Black, 2016).

(xiii) Reason for increase or decrease in the deferred tax assets or in the deferred tax

liability:

Yes, it is observed that there is a changes in deferred tax assets and liabilities in the financial

year of 2017 in both companies financial statement, financial statement of both company

indicates that total deferred tax assets from equity was nil and deferred tax assets from resale

from recognized directly in profit and loss were 1804 which was 1639 million in 2016. Total

deferred tax assets were 603 million, 465 million respectively in 2016 and 2015 in ANZ banking

group. In the case of Westpac Banking group, the deferred tax asset was 545 million in 2017 and

liabilities were 10 million in FY17. It was decreased compared to FY2016 when it was 36

million. Total deferred tax liability to set deferred tax asset were 580 million in loss (Coleman,

et. al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.