Course ID: Corporate Accounting

VerifiedAdded on 2021/05/31

|14

|2586

|156

AI Summary

2018 Cash flows from investing activities: Some of the important categories of information included under the “cash from investing activities” are listed below as follows: “Payments for property, plant and equipment” “Payments for intangible assets” “Payments for business and shares in controlled entities (net of cash acquired)” “Payments for joint ventures and associated entities” “Payments for other investments” “Proceeds from sale of property, plant and equipment” “Payments for other investments” “Payments for other investments”

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................6

Other comprehensive income statement:.........................................................................................8

Requirement (iii):.........................................................................................................................8

Requirement (iv):.........................................................................................................................8

Requirement (v):..........................................................................................................................8

Accounting for corporate income tax:.............................................................................................9

Requirement (vi):.........................................................................................................................9

Requirement (vii):........................................................................................................................9

Requirement (viii):.......................................................................................................................9

Requirement (ix):.........................................................................................................................9

Requirement (x):........................................................................................................................10

Requirement (xi):.......................................................................................................................11

References......................................................................................................................................12

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................6

Other comprehensive income statement:.........................................................................................8

Requirement (iii):.........................................................................................................................8

Requirement (iv):.........................................................................................................................8

Requirement (v):..........................................................................................................................8

Accounting for corporate income tax:.............................................................................................9

Requirement (vi):.........................................................................................................................9

Requirement (vii):........................................................................................................................9

Requirement (viii):.......................................................................................................................9

Requirement (ix):.........................................................................................................................9

Requirement (x):........................................................................................................................10

Requirement (xi):.......................................................................................................................11

References......................................................................................................................................12

2CORPORATE ACCOUNTING

Cash flow statement:

Requirement (i):

The main depictions of the report are based on cash flow statement prepared for “Telstra

Corporation Ltd”. Telstra is known as one of the most renowned telecommunications brand

across Australia “offering full range of communications services and competing in all

telecommunications markets”. The report is prepared as per the segmentation of cash flow based

on “operating activities, investing activities and financing activities” (Francis, Pinnuck and

Watanabe 2014).

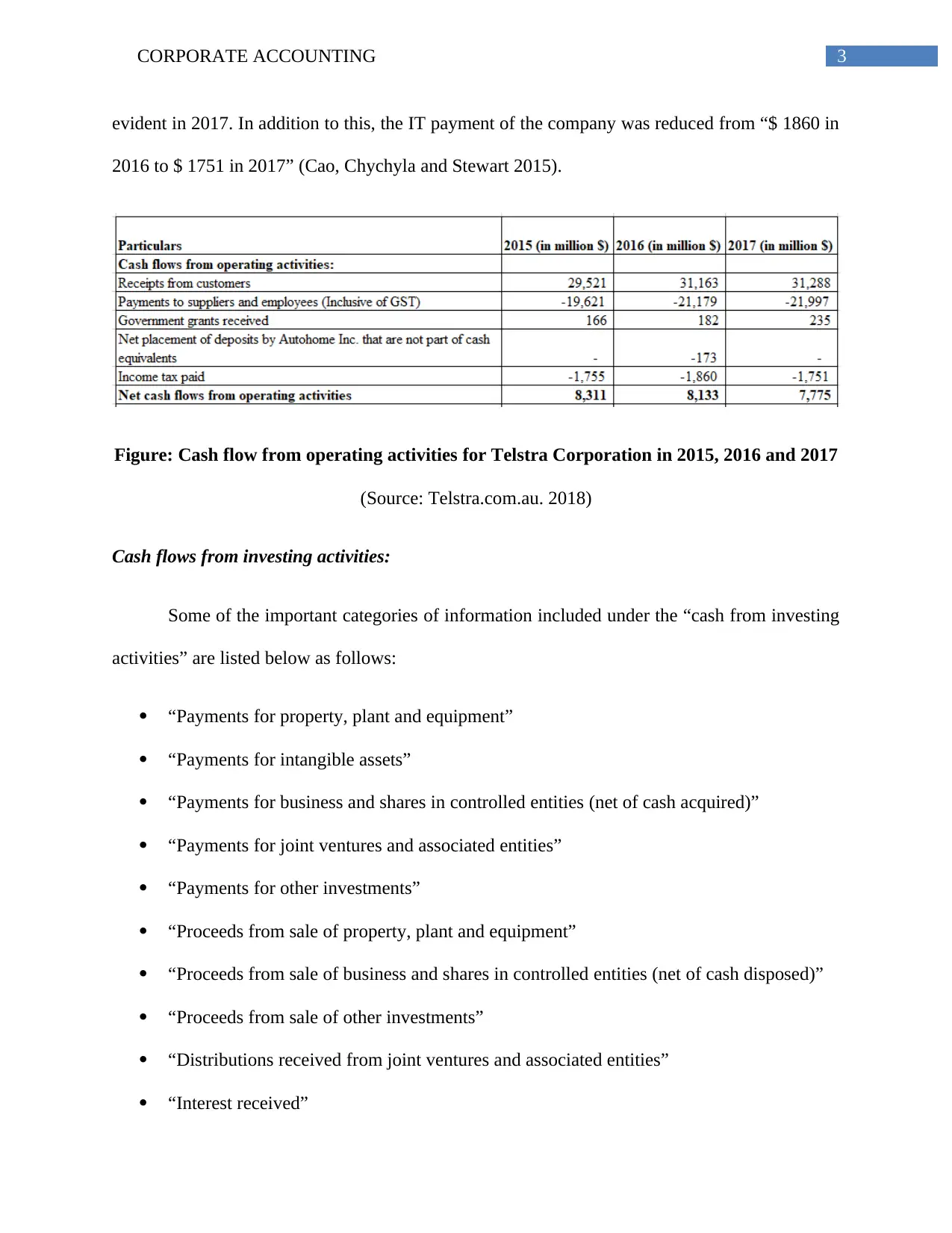

Cash flows from operating activities:

The important excerpts from cash from the operating activities are included with the

“Receipts from customers”, “Payments to suppliers and employees (Inclusive of GST)”,

“Government grants received”, “Net placement of deposits by Autohome Inc. that are not part of

cash equivalents” along with several types of other IT payment. The company has further

experienced a considerable amount of improvement in terms of extrapolating higher receipts

from the customers (Accounting Management 2015). The increased amount of receipts of

customer is depicted with increase of receipt from $ 31163 in 2016 to $ 31288 in 2017. The

increasing nature of operations had to pay more amount of cash to the suppliers and employees

in 2017 compared to those on 2015 and 2016. In 2016, Telstra Corporation is comprised of “Net

placement of deposits by Autohome Inc. that were not part of cash equivalents”. It needs to be

also discerned that the considerable amount of increase in the assistance by government was

Cash flow statement:

Requirement (i):

The main depictions of the report are based on cash flow statement prepared for “Telstra

Corporation Ltd”. Telstra is known as one of the most renowned telecommunications brand

across Australia “offering full range of communications services and competing in all

telecommunications markets”. The report is prepared as per the segmentation of cash flow based

on “operating activities, investing activities and financing activities” (Francis, Pinnuck and

Watanabe 2014).

Cash flows from operating activities:

The important excerpts from cash from the operating activities are included with the

“Receipts from customers”, “Payments to suppliers and employees (Inclusive of GST)”,

“Government grants received”, “Net placement of deposits by Autohome Inc. that are not part of

cash equivalents” along with several types of other IT payment. The company has further

experienced a considerable amount of improvement in terms of extrapolating higher receipts

from the customers (Accounting Management 2015). The increased amount of receipts of

customer is depicted with increase of receipt from $ 31163 in 2016 to $ 31288 in 2017. The

increasing nature of operations had to pay more amount of cash to the suppliers and employees

in 2017 compared to those on 2015 and 2016. In 2016, Telstra Corporation is comprised of “Net

placement of deposits by Autohome Inc. that were not part of cash equivalents”. It needs to be

also discerned that the considerable amount of increase in the assistance by government was

3CORPORATE ACCOUNTING

evident in 2017. In addition to this, the IT payment of the company was reduced from “$ 1860 in

2016 to $ 1751 in 2017” (Cao, Chychyla and Stewart 2015).

Figure: Cash flow from operating activities for Telstra Corporation in 2015, 2016 and 2017

(Source: Telstra.com.au. 2018)

Cash flows from investing activities:

Some of the important categories of information included under the “cash from investing

activities” are listed below as follows:

“Payments for property, plant and equipment”

“Payments for intangible assets”

“Payments for business and shares in controlled entities (net of cash acquired)”

“Payments for joint ventures and associated entities”

“Payments for other investments”

“Proceeds from sale of property, plant and equipment”

“Proceeds from sale of business and shares in controlled entities (net of cash disposed)”

“Proceeds from sale of other investments”

“Distributions received from joint ventures and associated entities”

“Interest received”

evident in 2017. In addition to this, the IT payment of the company was reduced from “$ 1860 in

2016 to $ 1751 in 2017” (Cao, Chychyla and Stewart 2015).

Figure: Cash flow from operating activities for Telstra Corporation in 2015, 2016 and 2017

(Source: Telstra.com.au. 2018)

Cash flows from investing activities:

Some of the important categories of information included under the “cash from investing

activities” are listed below as follows:

“Payments for property, plant and equipment”

“Payments for intangible assets”

“Payments for business and shares in controlled entities (net of cash acquired)”

“Payments for joint ventures and associated entities”

“Payments for other investments”

“Proceeds from sale of property, plant and equipment”

“Proceeds from sale of business and shares in controlled entities (net of cash disposed)”

“Proceeds from sale of other investments”

“Distributions received from joint ventures and associated entities”

“Interest received”

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING

“Other investing activities”

The payment considerations for “property, plant and equipment” are included from the

proceeds as a result of deposits and advances. Moreover, the payments related to “property, plant

and equipment” are formed as a part of amount which are essential to conduct business activity.

On the other hand, the inclusion of these assets has been beneficial in providing different types

of “economic benefits” to “Telstra Corporations” which are considered from proceeds. It is to be

also understood that the organisation has experienced a significant amount of increase in terms of

proceeds from investments and sales which are clearly shown with adequate cash generated in

the particulars under the fixed assets. The proceeds are further formed under a contract

specifying the total time for payment and the amount which are to be included with the interest

amount payable. Despite of this, the different types of interpretation of information have shown

that overall cash utilised in the investment activities has been depicted with more payments than

received in the subsequent years. The main rationale for such a situation is mainly because of

“payments for intangible assets and PPE” (Biscarri 2014).

“Other investing activities”

The payment considerations for “property, plant and equipment” are included from the

proceeds as a result of deposits and advances. Moreover, the payments related to “property, plant

and equipment” are formed as a part of amount which are essential to conduct business activity.

On the other hand, the inclusion of these assets has been beneficial in providing different types

of “economic benefits” to “Telstra Corporations” which are considered from proceeds. It is to be

also understood that the organisation has experienced a significant amount of increase in terms of

proceeds from investments and sales which are clearly shown with adequate cash generated in

the particulars under the fixed assets. The proceeds are further formed under a contract

specifying the total time for payment and the amount which are to be included with the interest

amount payable. Despite of this, the different types of interpretation of information have shown

that overall cash utilised in the investment activities has been depicted with more payments than

received in the subsequent years. The main rationale for such a situation is mainly because of

“payments for intangible assets and PPE” (Biscarri 2014).

5CORPORATE ACCOUNTING

Figure: Cash flow from investing activities for Telstra Corporation in 2015, 2016 and 2017

(Source: Telstra.com.au. 2018)

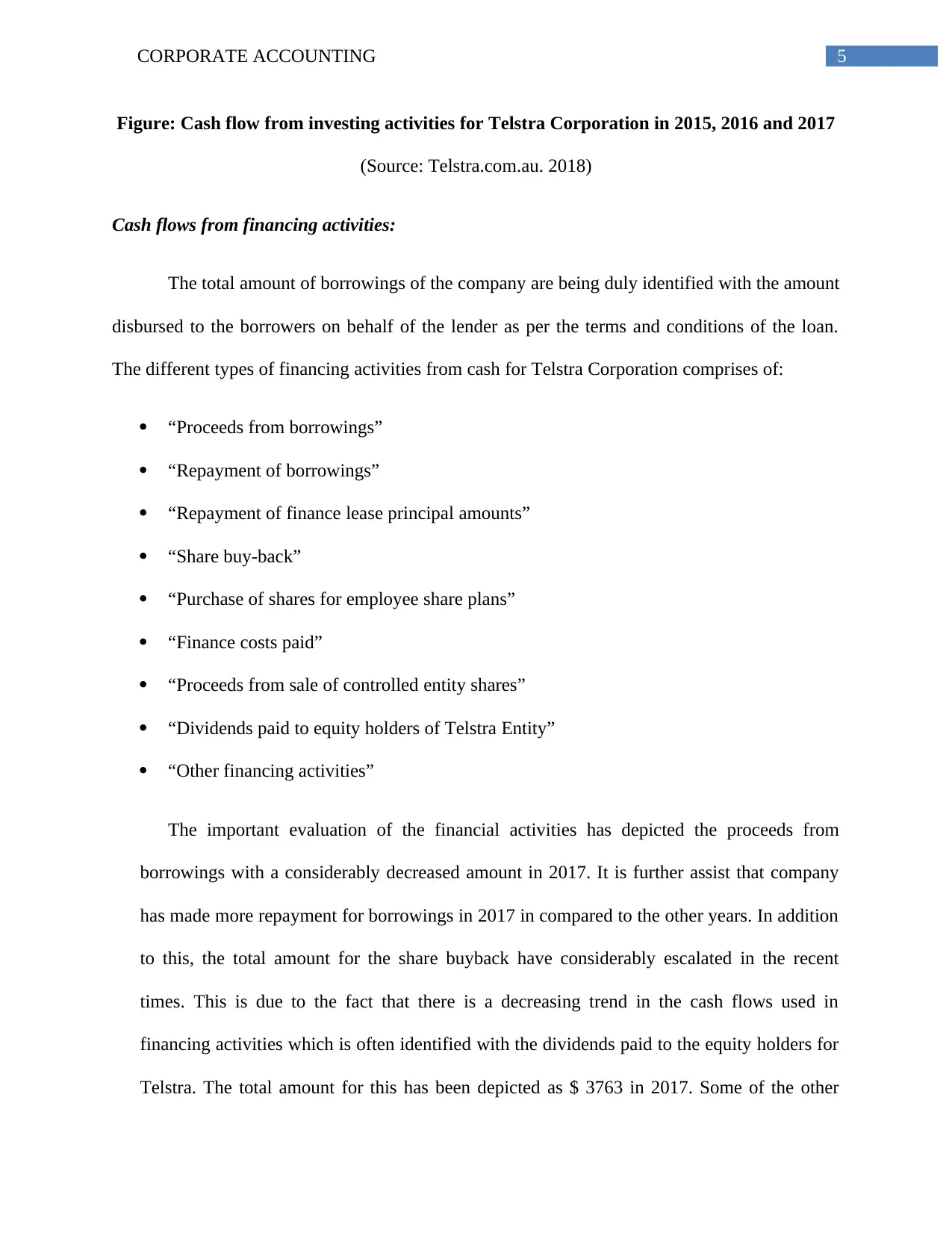

Cash flows from financing activities:

The total amount of borrowings of the company are being duly identified with the amount

disbursed to the borrowers on behalf of the lender as per the terms and conditions of the loan.

The different types of financing activities from cash for Telstra Corporation comprises of:

“Proceeds from borrowings”

“Repayment of borrowings”

“Repayment of finance lease principal amounts”

“Share buy-back”

“Purchase of shares for employee share plans”

“Finance costs paid”

“Proceeds from sale of controlled entity shares”

“Dividends paid to equity holders of Telstra Entity”

“Other financing activities”

The important evaluation of the financial activities has depicted the proceeds from

borrowings with a considerably decreased amount in 2017. It is further assist that company

has made more repayment for borrowings in 2017 in compared to the other years. In addition

to this, the total amount for the share buyback have considerably escalated in the recent

times. This is due to the fact that there is a decreasing trend in the cash flows used in

financing activities which is often identified with the dividends paid to the equity holders for

Telstra. The total amount for this has been depicted as $ 3763 in 2017. Some of the other

Figure: Cash flow from investing activities for Telstra Corporation in 2015, 2016 and 2017

(Source: Telstra.com.au. 2018)

Cash flows from financing activities:

The total amount of borrowings of the company are being duly identified with the amount

disbursed to the borrowers on behalf of the lender as per the terms and conditions of the loan.

The different types of financing activities from cash for Telstra Corporation comprises of:

“Proceeds from borrowings”

“Repayment of borrowings”

“Repayment of finance lease principal amounts”

“Share buy-back”

“Purchase of shares for employee share plans”

“Finance costs paid”

“Proceeds from sale of controlled entity shares”

“Dividends paid to equity holders of Telstra Entity”

“Other financing activities”

The important evaluation of the financial activities has depicted the proceeds from

borrowings with a considerably decreased amount in 2017. It is further assist that company

has made more repayment for borrowings in 2017 in compared to the other years. In addition

to this, the total amount for the share buyback have considerably escalated in the recent

times. This is due to the fact that there is a decreasing trend in the cash flows used in

financing activities which is often identified with the dividends paid to the equity holders for

Telstra. The total amount for this has been depicted as $ 3763 in 2017. Some of the other

6CORPORATE ACCOUNTING

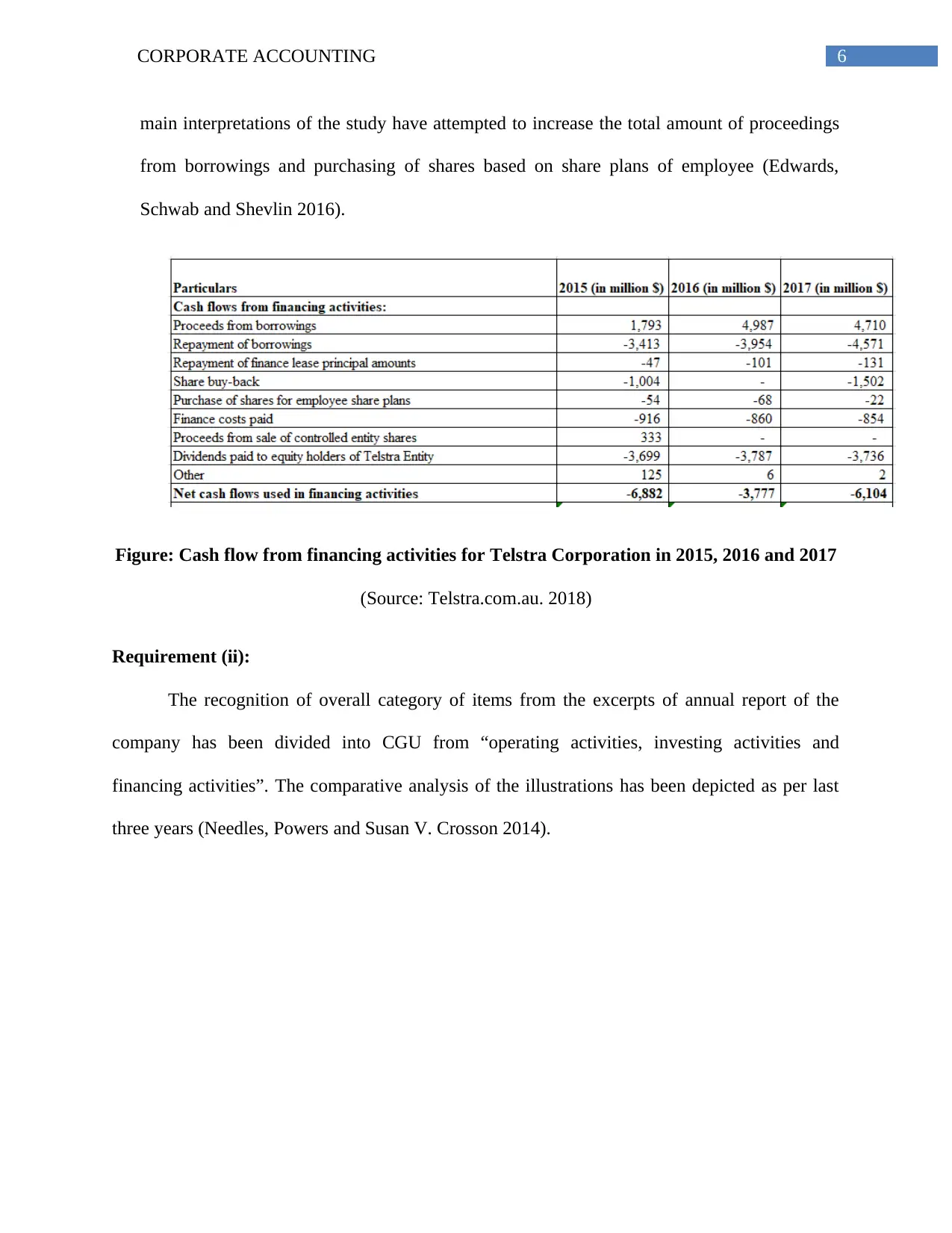

main interpretations of the study have attempted to increase the total amount of proceedings

from borrowings and purchasing of shares based on share plans of employee (Edwards,

Schwab and Shevlin 2016).

Figure: Cash flow from financing activities for Telstra Corporation in 2015, 2016 and 2017

(Source: Telstra.com.au. 2018)

Requirement (ii):

The recognition of overall category of items from the excerpts of annual report of the

company has been divided into CGU from “operating activities, investing activities and

financing activities”. The comparative analysis of the illustrations has been depicted as per last

three years (Needles, Powers and Susan V. Crosson 2014).

main interpretations of the study have attempted to increase the total amount of proceedings

from borrowings and purchasing of shares based on share plans of employee (Edwards,

Schwab and Shevlin 2016).

Figure: Cash flow from financing activities for Telstra Corporation in 2015, 2016 and 2017

(Source: Telstra.com.au. 2018)

Requirement (ii):

The recognition of overall category of items from the excerpts of annual report of the

company has been divided into CGU from “operating activities, investing activities and

financing activities”. The comparative analysis of the illustrations has been depicted as per last

three years (Needles, Powers and Susan V. Crosson 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

2015 2016 2017

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Comparative analysis of cash flow categories of Telstra

Corporation Ltd.

Net cash flows from operating

activities

Net cash flows used in investing

activities

Net cash flows used in financing

activities

Figure: Comparative analysis of cash flow categories of Telstra Corporation Ltd.

(Source: As Created by The Author)

The inference made in the graphical representation of data suggest that the cash flow in

terms of operating activities have decreased over the years. This is mainly due to the fact of

increasing amount of cash paid to the employees and suppliers including the GST amount.

Whereas, the net cash flow from the investing activities are depicted with the considerable

amount of increase from 2015 to 2016 because of the shares in controlled entities and various

types of proceeds from sales of business (Karpoff et al. 2017). However, in this particular

category, a significant decrease was observed in 2017 as the company spent more amount of

2015 2016 2017

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Comparative analysis of cash flow categories of Telstra

Corporation Ltd.

Net cash flows from operating

activities

Net cash flows used in investing

activities

Net cash flows used in financing

activities

Figure: Comparative analysis of cash flow categories of Telstra Corporation Ltd.

(Source: As Created by The Author)

The inference made in the graphical representation of data suggest that the cash flow in

terms of operating activities have decreased over the years. This is mainly due to the fact of

increasing amount of cash paid to the employees and suppliers including the GST amount.

Whereas, the net cash flow from the investing activities are depicted with the considerable

amount of increase from 2015 to 2016 because of the shares in controlled entities and various

types of proceeds from sales of business (Karpoff et al. 2017). However, in this particular

category, a significant decrease was observed in 2017 as the company spent more amount of

8CORPORATE ACCOUNTING

expenses on intangible assets. It needs to be for the discerned that although there was an increase

in the proceeds from sales in 2017 for other investment activities, this amount had negligible

effect due to increasing payments for fixed assets like “property plant and equipment” and

“payment for intangible assets”. Henceforth, the various factors associated to payment for PPE,

the company has been experiencing an overall cash crunch pertaining to the investing activities

in the FY 2017 (Needles, Powers and Susan V. Crosson 2014).

Other comprehensive income statement:

Requirement (iii):

The financial statement analysis of “Telstra corporations Ltd” have been conducive in

identifying the other comprehensive income with inclusion of items such as “Foreign currency

translation reserve, Cash flow hedging reserve and Foreign currency basis spread reserve” (Bay,

Catasús and Johed 2014).

Requirement (iv):

Some of the main consideration of the information evaluated by the company is based on

the reserve for foreign currency translation associated to conversion of outcomes related to

foreign subsidiaries. These subsidiaries are often considered as the of “parent firm to the

reporting currency”. The important consideration for maintenance of cash flow hedging reserve

is beneficial for the company and interpretation of exposure to radiation is in cash flow of asset

or liability pertaining to the changes in risk areas like “rate of interest on debt instrument

associated to floating rate”. In addition to this, the IT expense is considered to be incurred on

part of the PBT earned by Telstra (Financial Reporting Council 2014).

expenses on intangible assets. It needs to be for the discerned that although there was an increase

in the proceeds from sales in 2017 for other investment activities, this amount had negligible

effect due to increasing payments for fixed assets like “property plant and equipment” and

“payment for intangible assets”. Henceforth, the various factors associated to payment for PPE,

the company has been experiencing an overall cash crunch pertaining to the investing activities

in the FY 2017 (Needles, Powers and Susan V. Crosson 2014).

Other comprehensive income statement:

Requirement (iii):

The financial statement analysis of “Telstra corporations Ltd” have been conducive in

identifying the other comprehensive income with inclusion of items such as “Foreign currency

translation reserve, Cash flow hedging reserve and Foreign currency basis spread reserve” (Bay,

Catasús and Johed 2014).

Requirement (iv):

Some of the main consideration of the information evaluated by the company is based on

the reserve for foreign currency translation associated to conversion of outcomes related to

foreign subsidiaries. These subsidiaries are often considered as the of “parent firm to the

reporting currency”. The important consideration for maintenance of cash flow hedging reserve

is beneficial for the company and interpretation of exposure to radiation is in cash flow of asset

or liability pertaining to the changes in risk areas like “rate of interest on debt instrument

associated to floating rate”. In addition to this, the IT expense is considered to be incurred on

part of the PBT earned by Telstra (Financial Reporting Council 2014).

9CORPORATE ACCOUNTING

Requirement (v):

The description of net income has been considered with the study of comprehensive

income. The main reason for the inclusion of other comprehensive income statement is related to

provide a more complete overview of the items of operation which we are not generally included

as a part of the income statement of the company. Telstra corporations have provided a more

diversified disclosure on the net profit which was marked shown in an elaborated manner in the

income statement (Garrett, Hoitash and Prawitt 2014).

Accounting for corporate income tax:

Requirement (vi):

The important obligation for tax expense have been led by the factors related to “state

government proceedings, federal and municipal activities”. With particular reference to Telstra,

the total amount of IT expense is valued at “$ 1773 in 2017 in contrast to $ 1768 in 2016”.

Requirement (vii):

It can be also depicted that the organization has earned PBIT which is amounted to $

5600 in 2016 and $ 5647 in 2017. Moreover, this particular amount is inherent with “tax rate of

30% on PBIT”.

Requirement (viii):

A significant review of the DTA performed by Telstra corporations Ltd during the end of

reporting period shows that the carrying amount of such assets are recognised only that extent

where the sufficient taxable profit is utilised in favour of the company. Furthermore, Telstra has

offset income tax levied by the taxation authority based on the DTL and DTA (Heakal 2017).

Requirement (v):

The description of net income has been considered with the study of comprehensive

income. The main reason for the inclusion of other comprehensive income statement is related to

provide a more complete overview of the items of operation which we are not generally included

as a part of the income statement of the company. Telstra corporations have provided a more

diversified disclosure on the net profit which was marked shown in an elaborated manner in the

income statement (Garrett, Hoitash and Prawitt 2014).

Accounting for corporate income tax:

Requirement (vi):

The important obligation for tax expense have been led by the factors related to “state

government proceedings, federal and municipal activities”. With particular reference to Telstra,

the total amount of IT expense is valued at “$ 1773 in 2017 in contrast to $ 1768 in 2016”.

Requirement (vii):

It can be also depicted that the organization has earned PBIT which is amounted to $

5600 in 2016 and $ 5647 in 2017. Moreover, this particular amount is inherent with “tax rate of

30% on PBIT”.

Requirement (viii):

A significant review of the DTA performed by Telstra corporations Ltd during the end of

reporting period shows that the carrying amount of such assets are recognised only that extent

where the sufficient taxable profit is utilised in favour of the company. Furthermore, Telstra has

offset income tax levied by the taxation authority based on the DTL and DTA (Heakal 2017).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE ACCOUNTING

Requirement (ix):

The important depictions of the assertions for the franking credits are taken into account

with the main results of IT payable which is amounted to $ 146m in 2017 and $ 158m in 2016.

Moreover, the overall amount of IT payable in 2017, 2016 and 2015 was seen to be increasing in

nature. The total amount of IT payable in the “subsequent year was observed to be $ 161m in

2017 and $ 176m in 2016” (Bay, Catasús and Johed 2014).

Requirement (x):

The critical disclosure is associated to the income tax expense have been taken into

account with “current tax expense, Deferred tax resulting from the origination and reversal of

temporary differences”. Along with this the company has included the major disclosures of

income tax with the “Under provision of tax in prior years”. Furthermore, “Notional income tax

expense calculated at the Australian tax rate of 30%” have been considered with a total amount

of “$ 1694 in 2017 and $ 2294 in 2016” (Edwards, Schwab and Shevlin 2016).

Requirement (ix):

The important depictions of the assertions for the franking credits are taken into account

with the main results of IT payable which is amounted to $ 146m in 2017 and $ 158m in 2016.

Moreover, the overall amount of IT payable in 2017, 2016 and 2015 was seen to be increasing in

nature. The total amount of IT payable in the “subsequent year was observed to be $ 161m in

2017 and $ 176m in 2016” (Bay, Catasús and Johed 2014).

Requirement (x):

The critical disclosure is associated to the income tax expense have been taken into

account with “current tax expense, Deferred tax resulting from the origination and reversal of

temporary differences”. Along with this the company has included the major disclosures of

income tax with the “Under provision of tax in prior years”. Furthermore, “Notional income tax

expense calculated at the Australian tax rate of 30%” have been considered with a total amount

of “$ 1694 in 2017 and $ 2294 in 2016” (Edwards, Schwab and Shevlin 2016).

11CORPORATE ACCOUNTING

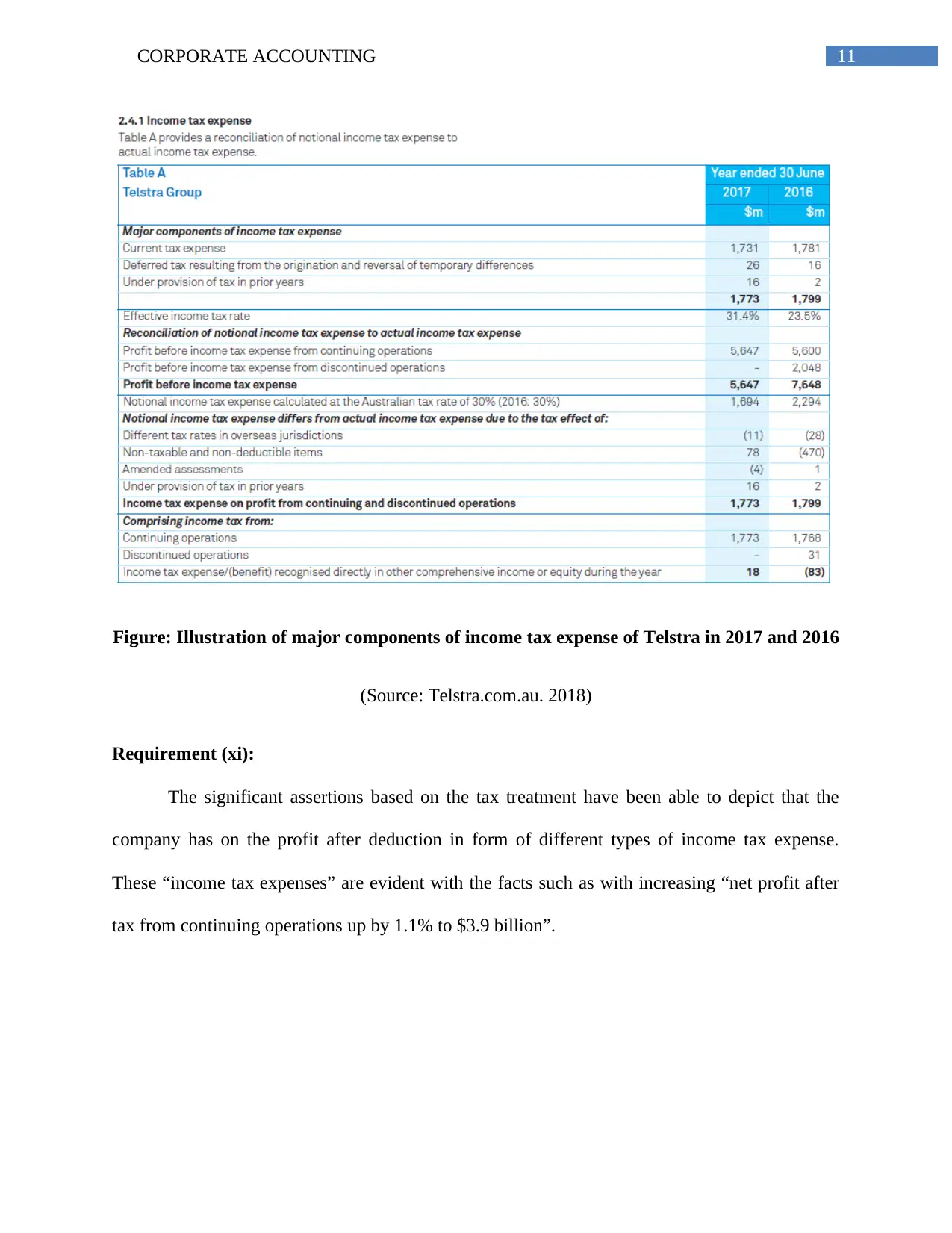

Figure: Illustration of major components of income tax expense of Telstra in 2017 and 2016

(Source: Telstra.com.au. 2018)

Requirement (xi):

The significant assertions based on the tax treatment have been able to depict that the

company has on the profit after deduction in form of different types of income tax expense.

These “income tax expenses” are evident with the facts such as with increasing “net profit after

tax from continuing operations up by 1.1% to $3.9 billion”.

Figure: Illustration of major components of income tax expense of Telstra in 2017 and 2016

(Source: Telstra.com.au. 2018)

Requirement (xi):

The significant assertions based on the tax treatment have been able to depict that the

company has on the profit after deduction in form of different types of income tax expense.

These “income tax expenses” are evident with the facts such as with increasing “net profit after

tax from continuing operations up by 1.1% to $3.9 billion”.

12CORPORATE ACCOUNTING

References

Accounting Management (2015) Debt to equity ratio - explanation, formula, example and

interpretation | Accounting for Management, Financial Statement Analysis.

Bay, C., Catasús, B. and Johed, G. (2014) ‘Situating financial literacy’, Critical Perspectives on

Accounting, 25(1), pp. 36–45. doi: 10.1016/j.cpa.2012.11.011.

Biscarri, J. G. (2014) ‘FINANCIAL ACCOUNTING’, in Current topics in accounting, pp. 1–9.

doi: 10.1016/B978-0-12-397920-9.09994-7.

Cao, M., Chychyla, R. and Stewart, T. (2015) ‘Big data analytics in financial statement audits’,

Accounting Horizons, 29(2), pp. 423–429. doi: 10.2308/acch-51068.

Edwards, A., Schwab, C. and Shevlin, T. (2016) ‘Financial constraints and cash tax savings’, in

Accounting Review, pp. 859–881. doi: 10.2308/accr-51282.

Financial Reporting Council (2014) ‘The UK corporate governance code’, Financial Reporting

Council, (September), pp. 1–36. doi: Retrieved from Financial Reporting Council.

Francis, J. R., Pinnuck, M. L. and Watanabe, O. (2014) ‘Auditor style and financial statement

comparability’, Accounting Review, 89(2), pp. 605–633. doi: 10.2308/accr-50642.

Garrett, J., Hoitash, R. and Prawitt, D. F. (2014) ‘Trust and financial reporting quality’, Journal

of Accounting Research, 52(5), pp. 1087–1125. doi: 10.1111/1475-679X.12063.

Heakal, R. (2017) ‘What is a cash flow statement?’, Investopedia, pp. 1–16. Available at:

https://www.investopedia.com/articles/04/033104.asp%0Ahttp://www.investopedia.com/

articles/04/033104.asp.

References

Accounting Management (2015) Debt to equity ratio - explanation, formula, example and

interpretation | Accounting for Management, Financial Statement Analysis.

Bay, C., Catasús, B. and Johed, G. (2014) ‘Situating financial literacy’, Critical Perspectives on

Accounting, 25(1), pp. 36–45. doi: 10.1016/j.cpa.2012.11.011.

Biscarri, J. G. (2014) ‘FINANCIAL ACCOUNTING’, in Current topics in accounting, pp. 1–9.

doi: 10.1016/B978-0-12-397920-9.09994-7.

Cao, M., Chychyla, R. and Stewart, T. (2015) ‘Big data analytics in financial statement audits’,

Accounting Horizons, 29(2), pp. 423–429. doi: 10.2308/acch-51068.

Edwards, A., Schwab, C. and Shevlin, T. (2016) ‘Financial constraints and cash tax savings’, in

Accounting Review, pp. 859–881. doi: 10.2308/accr-51282.

Financial Reporting Council (2014) ‘The UK corporate governance code’, Financial Reporting

Council, (September), pp. 1–36. doi: Retrieved from Financial Reporting Council.

Francis, J. R., Pinnuck, M. L. and Watanabe, O. (2014) ‘Auditor style and financial statement

comparability’, Accounting Review, 89(2), pp. 605–633. doi: 10.2308/accr-50642.

Garrett, J., Hoitash, R. and Prawitt, D. F. (2014) ‘Trust and financial reporting quality’, Journal

of Accounting Research, 52(5), pp. 1087–1125. doi: 10.1111/1475-679X.12063.

Heakal, R. (2017) ‘What is a cash flow statement?’, Investopedia, pp. 1–16. Available at:

https://www.investopedia.com/articles/04/033104.asp%0Ahttp://www.investopedia.com/

articles/04/033104.asp.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CORPORATE ACCOUNTING

Karpoff, J. M., Koester, A., Lee, D. S. and Martin, G. S. (2017) ‘Proxies and databases in

financial misconduct research’, Accounting Review, 92(6), pp. 129–163. doi: 10.2308/accr-

51766.

Needles, B. E., Powers, M. and Susan V. Crosson (2014) Principles of Accounting, Financial

Accounting. doi: 10.1037/h0092877.

Telstra.com.au. (2018). Telstra - Our company. [online] Available at:

https://www.telstra.com.au/aboutus/our-company [Accessed 21 May 2018].

Karpoff, J. M., Koester, A., Lee, D. S. and Martin, G. S. (2017) ‘Proxies and databases in

financial misconduct research’, Accounting Review, 92(6), pp. 129–163. doi: 10.2308/accr-

51766.

Needles, B. E., Powers, M. and Susan V. Crosson (2014) Principles of Accounting, Financial

Accounting. doi: 10.1037/h0092877.

Telstra.com.au. (2018). Telstra - Our company. [online] Available at:

https://www.telstra.com.au/aboutus/our-company [Accessed 21 May 2018].

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.