Corporate Accounting Report: Analysis of Grain Corp Ltd Financials

VerifiedAdded on 2020/10/05

|11

|3063

|426

Report

AI Summary

This report presents a detailed analysis of the financial statements of Grain Corp Ltd, an ASX-listed agribusiness company. The analysis covers the cash flow statement, examining receipts, payments, and net cash flows from operating, investing, and financing activities over three years (2015-2017). It highlights trends in cash flow, including changes in borrowings, dividends, and investments. The report also explores the other comprehensive income statement, discussing items not reclassified and those reclassified to the profit and loss account, including the impact of taxes and exchange differences. Furthermore, the report delves into the accounting for corporate income tax, including the firm's tax expense, effective tax rate, and deferred tax assets/liabilities, providing insights into Grain Corp Ltd's financial performance and tax obligations.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

CASH FLOW STATEMENT..........................................................................................................1

1. Discuss items of cash flow statement of company in past years........................................1

2. Analysing cash flows of previous years.............................................................................3

OTHER COMPREHENSIVE INCOME STATEMENT................................................................4

3. Discuss items of other comprehensive income statement..................................................4

4. Understanding of each item in the statement.....................................................................5

5. Items not recorded in income statement.............................................................................6

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................6

6. Firm's tax expense..............................................................................................................6

7. Is figure same as company tax rate times of firm's accounting income.............................6

8. Commenting on deferred tax assets/liabilities....................................................................7

9. Providing current tax assets or income tax payable reported by firm................................7

10. Is income tax paid same as income tax expense...............................................................7

11. Treatment of tax of firm...................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

CASH FLOW STATEMENT..........................................................................................................1

1. Discuss items of cash flow statement of company in past years........................................1

2. Analysing cash flows of previous years.............................................................................3

OTHER COMPREHENSIVE INCOME STATEMENT................................................................4

3. Discuss items of other comprehensive income statement..................................................4

4. Understanding of each item in the statement.....................................................................5

5. Items not recorded in income statement.............................................................................6

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................6

6. Firm's tax expense..............................................................................................................6

7. Is figure same as company tax rate times of firm's accounting income.............................6

8. Commenting on deferred tax assets/liabilities....................................................................7

9. Providing current tax assets or income tax payable reported by firm................................7

10. Is income tax paid same as income tax expense...............................................................7

11. Treatment of tax of firm...................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Financial statements are important documents of company in analysing information in

effective way. Present report deals with analysing financial statements of ASX listed company

named as Grain Corp Ltd engaged in agribusiness. Financials are effectively assessed and items

of the same are discussed quite effectually. Evaluation of firm's tax expense and all relevant

items are explained.

CASH FLOW STATEMENT

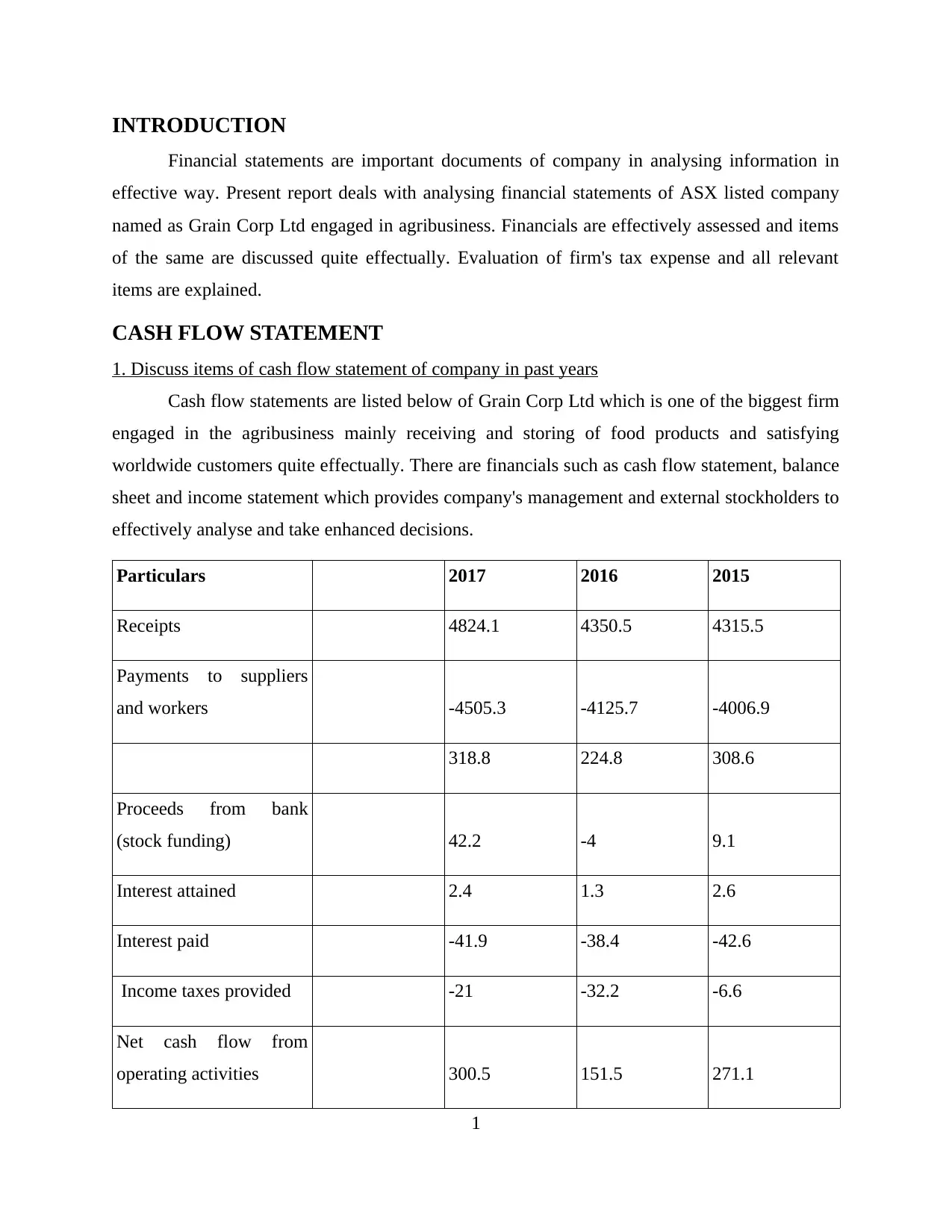

1. Discuss items of cash flow statement of company in past years

Cash flow statements are listed below of Grain Corp Ltd which is one of the biggest firm

engaged in the agribusiness mainly receiving and storing of food products and satisfying

worldwide customers quite effectually. There are financials such as cash flow statement, balance

sheet and income statement which provides company's management and external stockholders to

effectively analyse and take enhanced decisions.

Particulars 2017 2016 2015

Receipts 4824.1 4350.5 4315.5

Payments to suppliers

and workers -4505.3 -4125.7 -4006.9

318.8 224.8 308.6

Proceeds from bank

(stock funding) 42.2 -4 9.1

Interest attained 2.4 1.3 2.6

Interest paid -41.9 -38.4 -42.6

Income taxes provided -21 -32.2 -6.6

Net cash flow from

operating activities 300.5 151.5 271.1

1

Financial statements are important documents of company in analysing information in

effective way. Present report deals with analysing financial statements of ASX listed company

named as Grain Corp Ltd engaged in agribusiness. Financials are effectively assessed and items

of the same are discussed quite effectually. Evaluation of firm's tax expense and all relevant

items are explained.

CASH FLOW STATEMENT

1. Discuss items of cash flow statement of company in past years

Cash flow statements are listed below of Grain Corp Ltd which is one of the biggest firm

engaged in the agribusiness mainly receiving and storing of food products and satisfying

worldwide customers quite effectually. There are financials such as cash flow statement, balance

sheet and income statement which provides company's management and external stockholders to

effectively analyse and take enhanced decisions.

Particulars 2017 2016 2015

Receipts 4824.1 4350.5 4315.5

Payments to suppliers

and workers -4505.3 -4125.7 -4006.9

318.8 224.8 308.6

Proceeds from bank

(stock funding) 42.2 -4 9.1

Interest attained 2.4 1.3 2.6

Interest paid -41.9 -38.4 -42.6

Income taxes provided -21 -32.2 -6.6

Net cash flow from

operating activities 300.5 151.5 271.1

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

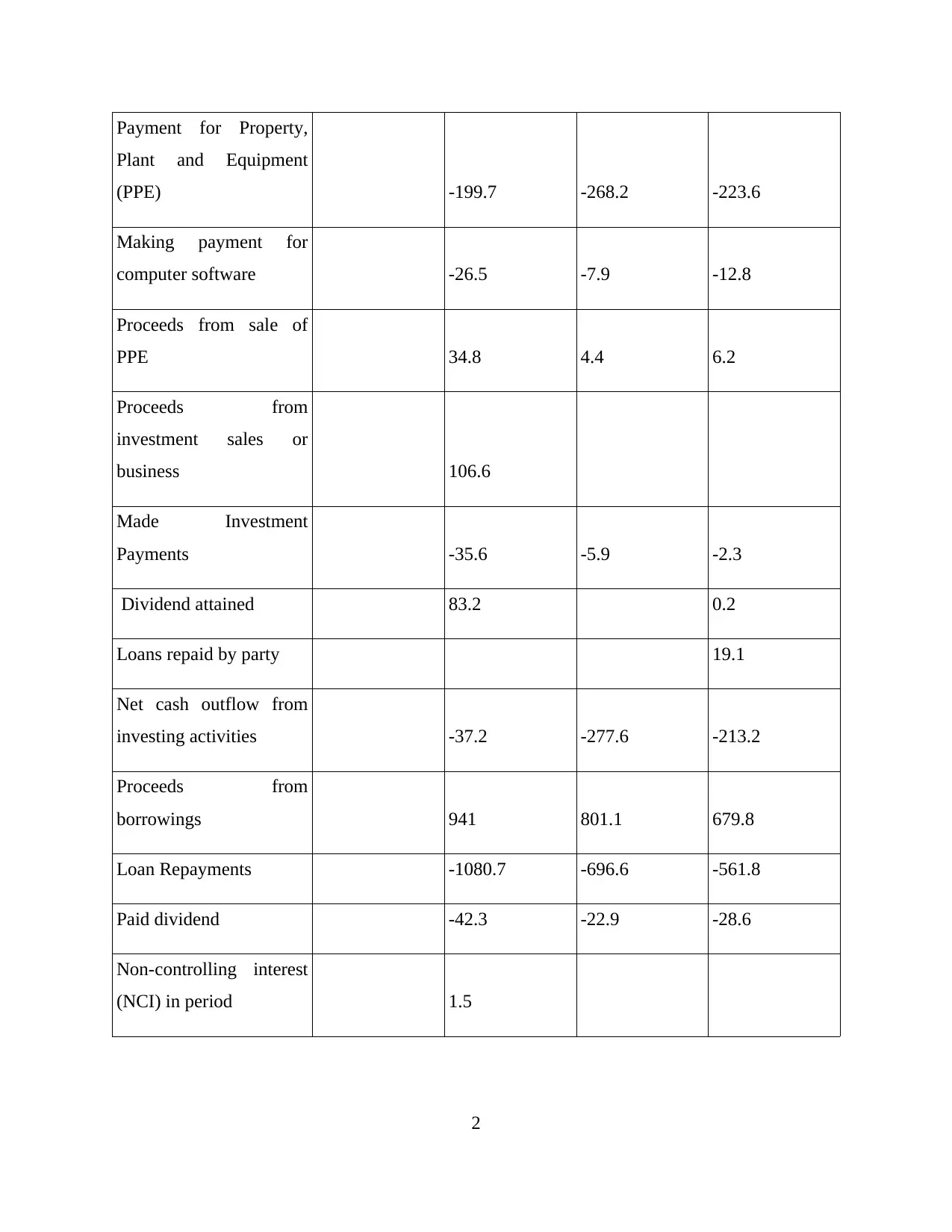

Payment for Property,

Plant and Equipment

(PPE) -199.7 -268.2 -223.6

Making payment for

computer software -26.5 -7.9 -12.8

Proceeds from sale of

PPE 34.8 4.4 6.2

Proceeds from

investment sales or

business 106.6

Made Investment

Payments -35.6 -5.9 -2.3

Dividend attained 83.2 0.2

Loans repaid by party 19.1

Net cash outflow from

investing activities -37.2 -277.6 -213.2

Proceeds from

borrowings 941 801.1 679.8

Loan Repayments -1080.7 -696.6 -561.8

Paid dividend -42.3 -22.9 -28.6

Non-controlling interest

(NCI) in period 1.5

2

Plant and Equipment

(PPE) -199.7 -268.2 -223.6

Making payment for

computer software -26.5 -7.9 -12.8

Proceeds from sale of

PPE 34.8 4.4 6.2

Proceeds from

investment sales or

business 106.6

Made Investment

Payments -35.6 -5.9 -2.3

Dividend attained 83.2 0.2

Loans repaid by party 19.1

Net cash outflow from

investing activities -37.2 -277.6 -213.2

Proceeds from

borrowings 941 801.1 679.8

Loan Repayments -1080.7 -696.6 -561.8

Paid dividend -42.3 -22.9 -28.6

Non-controlling interest

(NCI) in period 1.5

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

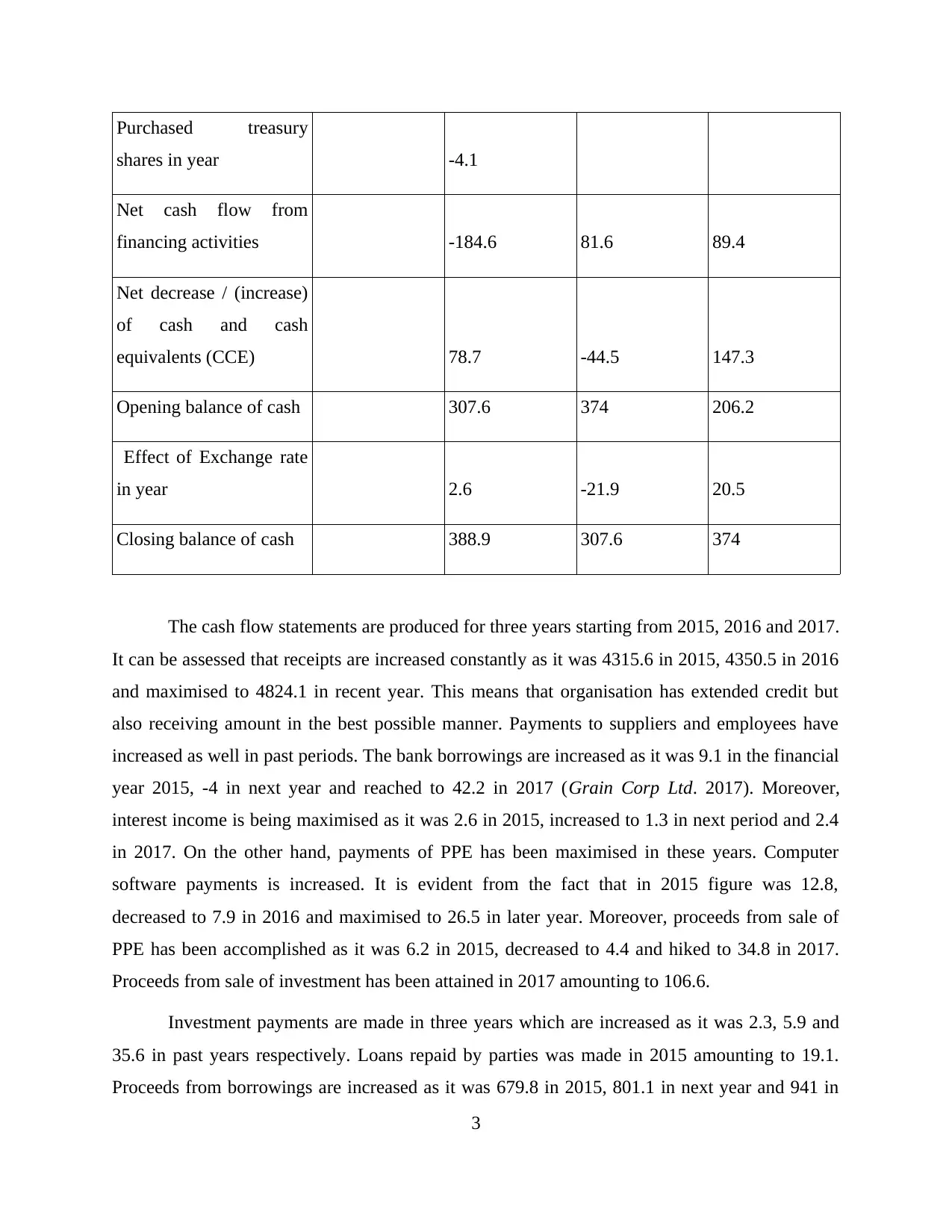

Purchased treasury

shares in year -4.1

Net cash flow from

financing activities -184.6 81.6 89.4

Net decrease / (increase)

of cash and cash

equivalents (CCE) 78.7 -44.5 147.3

Opening balance of cash 307.6 374 206.2

Effect of Exchange rate

in year 2.6 -21.9 20.5

Closing balance of cash 388.9 307.6 374

The cash flow statements are produced for three years starting from 2015, 2016 and 2017.

It can be assessed that receipts are increased constantly as it was 4315.6 in 2015, 4350.5 in 2016

and maximised to 4824.1 in recent year. This means that organisation has extended credit but

also receiving amount in the best possible manner. Payments to suppliers and employees have

increased as well in past periods. The bank borrowings are increased as it was 9.1 in the financial

year 2015, -4 in next year and reached to 42.2 in 2017 (Grain Corp Ltd. 2017). Moreover,

interest income is being maximised as it was 2.6 in 2015, increased to 1.3 in next period and 2.4

in 2017. On the other hand, payments of PPE has been maximised in these years. Computer

software payments is increased. It is evident from the fact that in 2015 figure was 12.8,

decreased to 7.9 in 2016 and maximised to 26.5 in later year. Moreover, proceeds from sale of

PPE has been accomplished as it was 6.2 in 2015, decreased to 4.4 and hiked to 34.8 in 2017.

Proceeds from sale of investment has been attained in 2017 amounting to 106.6.

Investment payments are made in three years which are increased as it was 2.3, 5.9 and

35.6 in past years respectively. Loans repaid by parties was made in 2015 amounting to 19.1.

Proceeds from borrowings are increased as it was 679.8 in 2015, 801.1 in next year and 941 in

3

shares in year -4.1

Net cash flow from

financing activities -184.6 81.6 89.4

Net decrease / (increase)

of cash and cash

equivalents (CCE) 78.7 -44.5 147.3

Opening balance of cash 307.6 374 206.2

Effect of Exchange rate

in year 2.6 -21.9 20.5

Closing balance of cash 388.9 307.6 374

The cash flow statements are produced for three years starting from 2015, 2016 and 2017.

It can be assessed that receipts are increased constantly as it was 4315.6 in 2015, 4350.5 in 2016

and maximised to 4824.1 in recent year. This means that organisation has extended credit but

also receiving amount in the best possible manner. Payments to suppliers and employees have

increased as well in past periods. The bank borrowings are increased as it was 9.1 in the financial

year 2015, -4 in next year and reached to 42.2 in 2017 (Grain Corp Ltd. 2017). Moreover,

interest income is being maximised as it was 2.6 in 2015, increased to 1.3 in next period and 2.4

in 2017. On the other hand, payments of PPE has been maximised in these years. Computer

software payments is increased. It is evident from the fact that in 2015 figure was 12.8,

decreased to 7.9 in 2016 and maximised to 26.5 in later year. Moreover, proceeds from sale of

PPE has been accomplished as it was 6.2 in 2015, decreased to 4.4 and hiked to 34.8 in 2017.

Proceeds from sale of investment has been attained in 2017 amounting to 106.6.

Investment payments are made in three years which are increased as it was 2.3, 5.9 and

35.6 in past years respectively. Loans repaid by parties was made in 2015 amounting to 19.1.

Proceeds from borrowings are increased as it was 679.8 in 2015, 801.1 in next year and 941 in

3

2017. Loans are repaid by Grain Corp Ltd as figure has been hiked in 2017 to 1080.7 while it

was 561.8 in 2015. Dividends are paid by company to shareholders as it was 28.6 in 2015, 22.9 I

later year and increased to 42.3 in the latest financial year. Non-controlling Interest is 1.5 in

2017. Treasury shares are purchased amounting to 4.1 in 2017. Thus, ending cash balance of

organisation is more than opening balance in 2017 which shows position is enhanced from past

years (García-Meca, López-Iturriaga and Tejerina-Gaite, 2017).

2. Analysing cash flows of previous years

It can be analysed from the cash flow statements that cash position of company is overall

good. Cash is properly used in various operational activities quite effectually. It is clarified by

the operating activities that it was 271.1 in 2015. However, it was decreased to 151.5 in 2016 and

again hiked to 300.5 in recent year. On the other hand, investing activities are also favourable as

cash is being generated in the past years by selling of investments and fixed assets in the best

possible manner. It is evident from the fact that in 2015, figure was 213.2 and increased to 277.6

while again reduced to 37.2 in 2017. On the other side, cash flows from financing activities were

89.4 in 2015, decreased to 81.6 in 2016. While, -184.6 of outflow is attained as cash has been

utilised in paying bank borrowings and dividends. However, it can be assessed that overall cash

position is good as closing balance of cash is favourable (Agrawal and Cooper, 2017).

OTHER COMPREHENSIVE INCOME STATEMENT

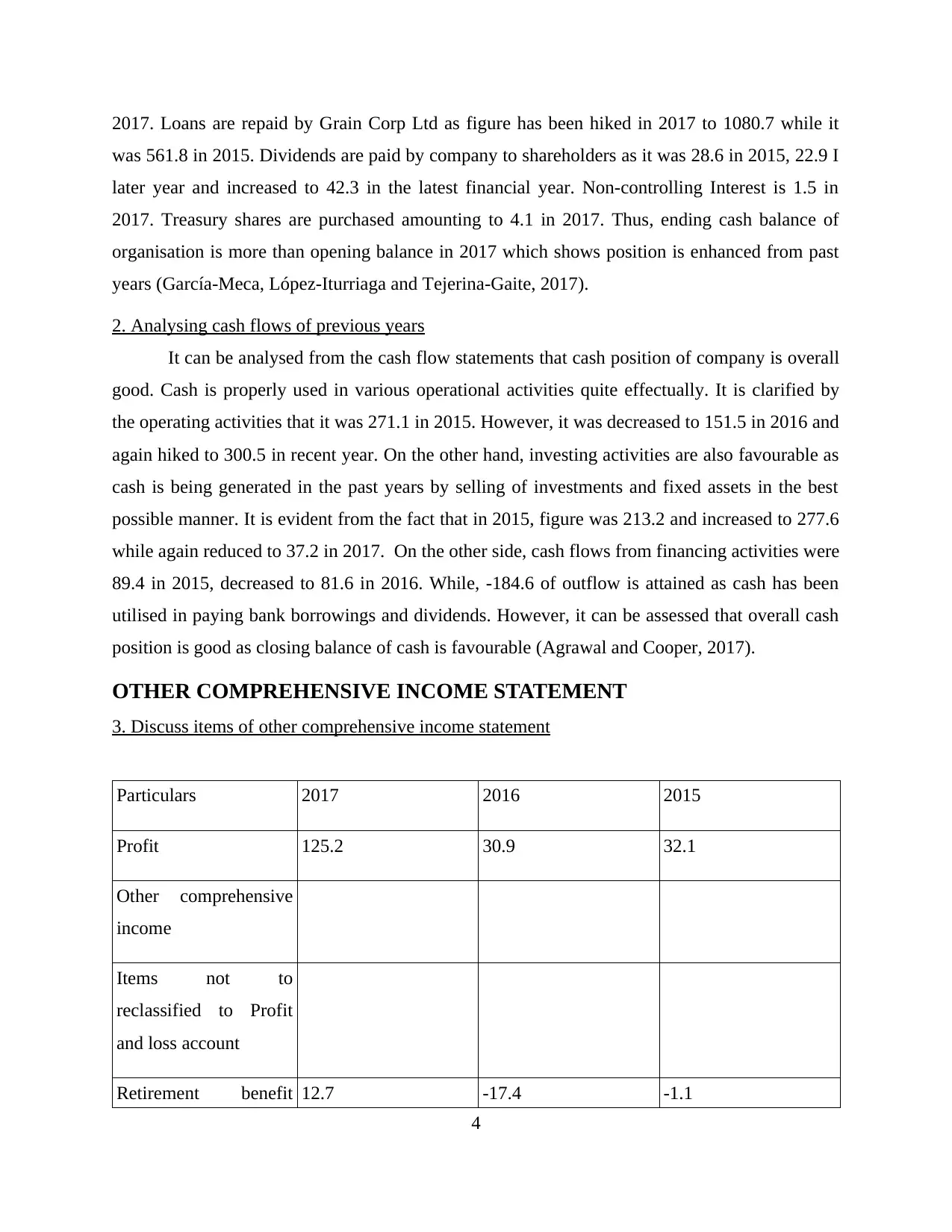

3. Discuss items of other comprehensive income statement

Particulars 2017 2016 2015

Profit 125.2 30.9 32.1

Other comprehensive

income

Items not to

reclassified to Profit

and loss account

Retirement benefit 12.7 -17.4 -1.1

4

was 561.8 in 2015. Dividends are paid by company to shareholders as it was 28.6 in 2015, 22.9 I

later year and increased to 42.3 in the latest financial year. Non-controlling Interest is 1.5 in

2017. Treasury shares are purchased amounting to 4.1 in 2017. Thus, ending cash balance of

organisation is more than opening balance in 2017 which shows position is enhanced from past

years (García-Meca, López-Iturriaga and Tejerina-Gaite, 2017).

2. Analysing cash flows of previous years

It can be analysed from the cash flow statements that cash position of company is overall

good. Cash is properly used in various operational activities quite effectually. It is clarified by

the operating activities that it was 271.1 in 2015. However, it was decreased to 151.5 in 2016 and

again hiked to 300.5 in recent year. On the other hand, investing activities are also favourable as

cash is being generated in the past years by selling of investments and fixed assets in the best

possible manner. It is evident from the fact that in 2015, figure was 213.2 and increased to 277.6

while again reduced to 37.2 in 2017. On the other side, cash flows from financing activities were

89.4 in 2015, decreased to 81.6 in 2016. While, -184.6 of outflow is attained as cash has been

utilised in paying bank borrowings and dividends. However, it can be assessed that overall cash

position is good as closing balance of cash is favourable (Agrawal and Cooper, 2017).

OTHER COMPREHENSIVE INCOME STATEMENT

3. Discuss items of other comprehensive income statement

Particulars 2017 2016 2015

Profit 125.2 30.9 32.1

Other comprehensive

income

Items not to

reclassified to Profit

and loss account

Retirement benefit 12.7 -17.4 -1.1

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

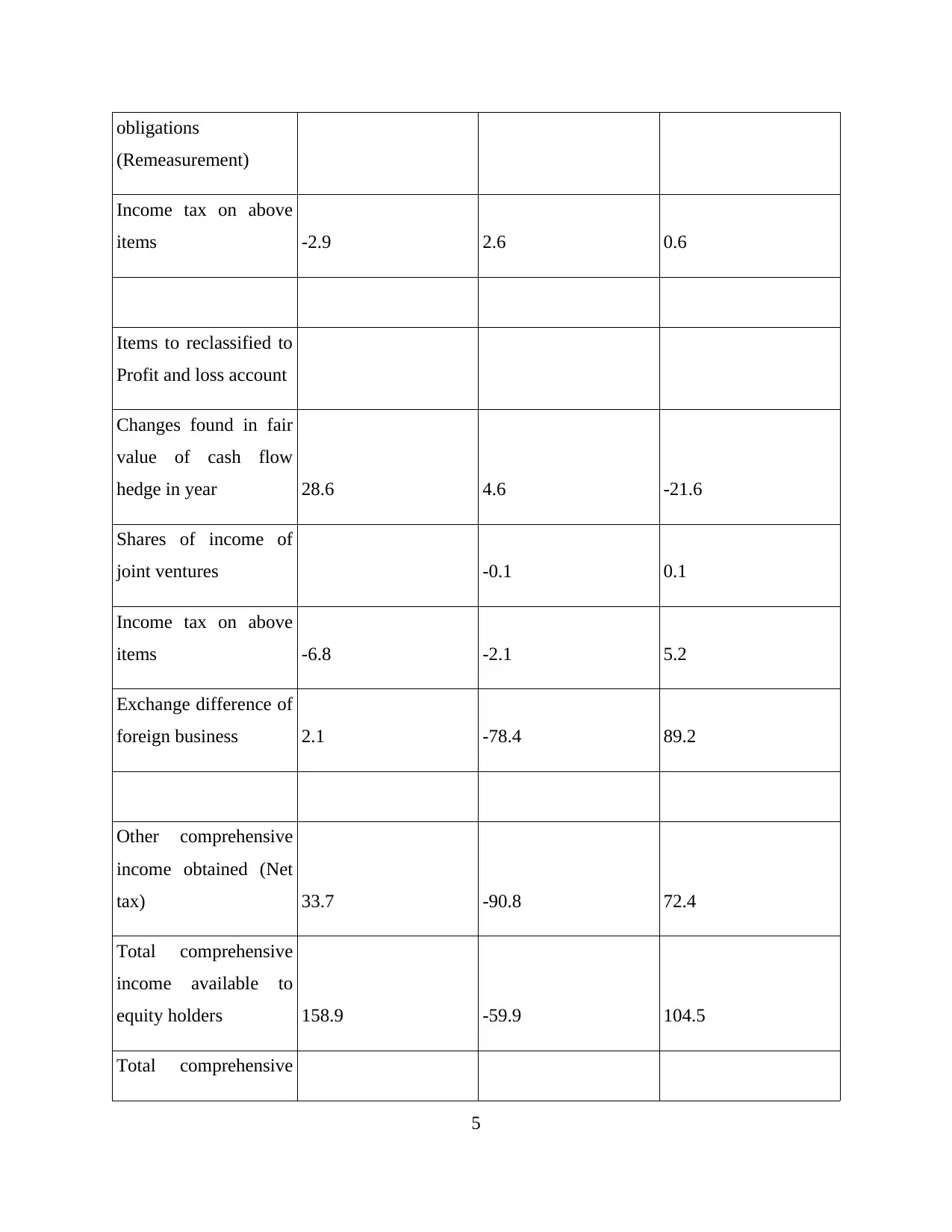

obligations

(Remeasurement)

Income tax on above

items -2.9 2.6 0.6

Items to reclassified to

Profit and loss account

Changes found in fair

value of cash flow

hedge in year 28.6 4.6 -21.6

Shares of income of

joint ventures -0.1 0.1

Income tax on above

items -6.8 -2.1 5.2

Exchange difference of

foreign business 2.1 -78.4 89.2

Other comprehensive

income obtained (Net

tax) 33.7 -90.8 72.4

Total comprehensive

income available to

equity holders 158.9 -59.9 104.5

Total comprehensive

5

(Remeasurement)

Income tax on above

items -2.9 2.6 0.6

Items to reclassified to

Profit and loss account

Changes found in fair

value of cash flow

hedge in year 28.6 4.6 -21.6

Shares of income of

joint ventures -0.1 0.1

Income tax on above

items -6.8 -2.1 5.2

Exchange difference of

foreign business 2.1 -78.4 89.2

Other comprehensive

income obtained (Net

tax) 33.7 -90.8 72.4

Total comprehensive

income available to

equity holders 158.9 -59.9 104.5

Total comprehensive

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

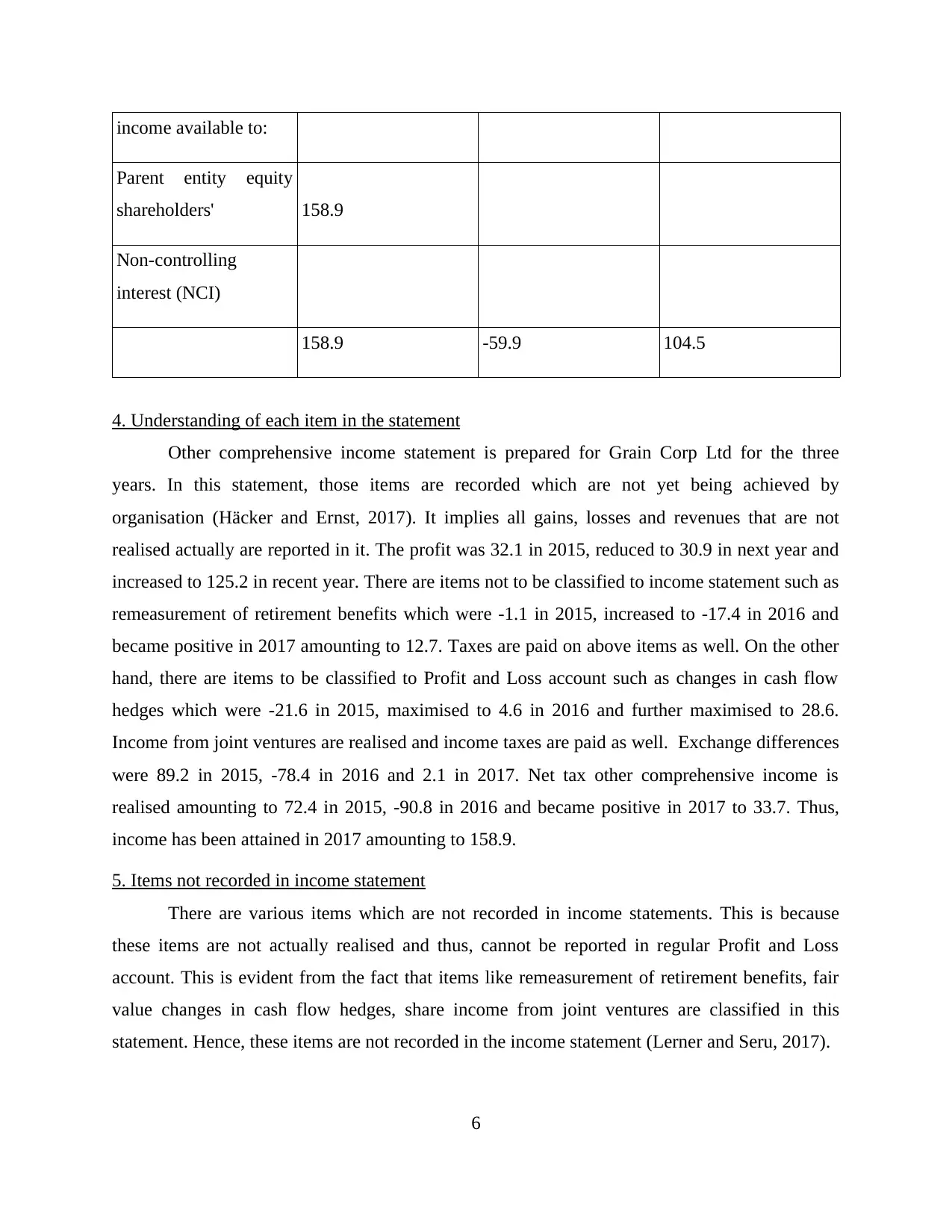

income available to:

Parent entity equity

shareholders' 158.9

Non-controlling

interest (NCI)

158.9 -59.9 104.5

4. Understanding of each item in the statement

Other comprehensive income statement is prepared for Grain Corp Ltd for the three

years. In this statement, those items are recorded which are not yet being achieved by

organisation (Häcker and Ernst, 2017). It implies all gains, losses and revenues that are not

realised actually are reported in it. The profit was 32.1 in 2015, reduced to 30.9 in next year and

increased to 125.2 in recent year. There are items not to be classified to income statement such as

remeasurement of retirement benefits which were -1.1 in 2015, increased to -17.4 in 2016 and

became positive in 2017 amounting to 12.7. Taxes are paid on above items as well. On the other

hand, there are items to be classified to Profit and Loss account such as changes in cash flow

hedges which were -21.6 in 2015, maximised to 4.6 in 2016 and further maximised to 28.6.

Income from joint ventures are realised and income taxes are paid as well. Exchange differences

were 89.2 in 2015, -78.4 in 2016 and 2.1 in 2017. Net tax other comprehensive income is

realised amounting to 72.4 in 2015, -90.8 in 2016 and became positive in 2017 to 33.7. Thus,

income has been attained in 2017 amounting to 158.9.

5. Items not recorded in income statement

There are various items which are not recorded in income statements. This is because

these items are not actually realised and thus, cannot be reported in regular Profit and Loss

account. This is evident from the fact that items like remeasurement of retirement benefits, fair

value changes in cash flow hedges, share income from joint ventures are classified in this

statement. Hence, these items are not recorded in the income statement (Lerner and Seru, 2017).

6

Parent entity equity

shareholders' 158.9

Non-controlling

interest (NCI)

158.9 -59.9 104.5

4. Understanding of each item in the statement

Other comprehensive income statement is prepared for Grain Corp Ltd for the three

years. In this statement, those items are recorded which are not yet being achieved by

organisation (Häcker and Ernst, 2017). It implies all gains, losses and revenues that are not

realised actually are reported in it. The profit was 32.1 in 2015, reduced to 30.9 in next year and

increased to 125.2 in recent year. There are items not to be classified to income statement such as

remeasurement of retirement benefits which were -1.1 in 2015, increased to -17.4 in 2016 and

became positive in 2017 amounting to 12.7. Taxes are paid on above items as well. On the other

hand, there are items to be classified to Profit and Loss account such as changes in cash flow

hedges which were -21.6 in 2015, maximised to 4.6 in 2016 and further maximised to 28.6.

Income from joint ventures are realised and income taxes are paid as well. Exchange differences

were 89.2 in 2015, -78.4 in 2016 and 2.1 in 2017. Net tax other comprehensive income is

realised amounting to 72.4 in 2015, -90.8 in 2016 and became positive in 2017 to 33.7. Thus,

income has been attained in 2017 amounting to 158.9.

5. Items not recorded in income statement

There are various items which are not recorded in income statements. This is because

these items are not actually realised and thus, cannot be reported in regular Profit and Loss

account. This is evident from the fact that items like remeasurement of retirement benefits, fair

value changes in cash flow hedges, share income from joint ventures are classified in this

statement. Hence, these items are not recorded in the income statement (Lerner and Seru, 2017).

6

ACCOUNTING FOR CORPORATE INCOME TAX

6. Firm's tax expense

The tax expenditure is required to be ascertain as it brings liability on the side of

company to pay taxes to the government in a particular year. The current year tax expense of

Grain Corp Ltd is 59.5. The amount has been segregated and includes prior periods provision

amounting to -0.9, deferred tax of 50.8 and current tax amounting to 9.6. On the other hand, from

this tax expense, effective income tax can be calculated by implementing formula. It can be

accomplished by dividing tax expense by EBIT (Earnings Before Interest and Taxes) and thus,

32.2 % is attained. Hence, this amount of tax is reported as current liability because it needs to be

paid in current year.

7. Is figure same as company tax rate times of firm's accounting income

It can be said that accounting income is generated from the normal business operations as

estimation of performances are done (Liu, Li, Zeng and An, 2017). In relation to this, gains and

losses which are actually realised are only accounted for. It is clarified that unrealised losses or

gains are not taken. Income tax expenditure of Grain Corp Ltd is 59.5 and effective tax rate

amounts to 32.2 %. Thus, it can be said that tax expense figure is same as tax rate of accounting

income of organisation.

8. Commenting on deferred tax assets/liabilities

Deferred tax assets are favourable for the organisation as it helps to reduce income tax

liability in the future. This figure is attained when company has overpaid taxes to the government

or advance payment is being made. It can be analysed from balance sheet of Grain Corp Ltd that

in 2017 deferred tax assets were 37. However, it was 63.8 in 2016 and increased to 71.2 in 2016.

Thus, it can be said that figure is reduced in 2017 and taxable income is required to be fully paid

and only 37 may be reduced from the same. Deferred tax liability is opposite of deferred tax

asset as when differences are observed in future and current tax amount, obligation to pay in the

future arises (Harris, Kinkela, Arnold and Liu 2017). The amount was 78 in 2015, increased to

80.6 in 2017 and liability is increased to pay tax.

9. Providing current tax assets or income tax payable reported by firm

Financials such as balance sheet is scrutinised and figures of current tax assets are found

out in the same. It can be assessed that amount of 1.1 is recorded in 2015, maximised to 2.5 in

7

6. Firm's tax expense

The tax expenditure is required to be ascertain as it brings liability on the side of

company to pay taxes to the government in a particular year. The current year tax expense of

Grain Corp Ltd is 59.5. The amount has been segregated and includes prior periods provision

amounting to -0.9, deferred tax of 50.8 and current tax amounting to 9.6. On the other hand, from

this tax expense, effective income tax can be calculated by implementing formula. It can be

accomplished by dividing tax expense by EBIT (Earnings Before Interest and Taxes) and thus,

32.2 % is attained. Hence, this amount of tax is reported as current liability because it needs to be

paid in current year.

7. Is figure same as company tax rate times of firm's accounting income

It can be said that accounting income is generated from the normal business operations as

estimation of performances are done (Liu, Li, Zeng and An, 2017). In relation to this, gains and

losses which are actually realised are only accounted for. It is clarified that unrealised losses or

gains are not taken. Income tax expenditure of Grain Corp Ltd is 59.5 and effective tax rate

amounts to 32.2 %. Thus, it can be said that tax expense figure is same as tax rate of accounting

income of organisation.

8. Commenting on deferred tax assets/liabilities

Deferred tax assets are favourable for the organisation as it helps to reduce income tax

liability in the future. This figure is attained when company has overpaid taxes to the government

or advance payment is being made. It can be analysed from balance sheet of Grain Corp Ltd that

in 2017 deferred tax assets were 37. However, it was 63.8 in 2016 and increased to 71.2 in 2016.

Thus, it can be said that figure is reduced in 2017 and taxable income is required to be fully paid

and only 37 may be reduced from the same. Deferred tax liability is opposite of deferred tax

asset as when differences are observed in future and current tax amount, obligation to pay in the

future arises (Harris, Kinkela, Arnold and Liu 2017). The amount was 78 in 2015, increased to

80.6 in 2017 and liability is increased to pay tax.

9. Providing current tax assets or income tax payable reported by firm

Financials such as balance sheet is scrutinised and figures of current tax assets are found

out in the same. It can be assessed that amount of 1.1 is recorded in 2015, maximised to 2.5 in

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2016 and 16 in the financial year 2017. The taxable income and accounting income are not same.

Moreover, it is analysed that income tax liability will be increased in the future as current tax

assets are maximised.

10. Is income tax paid same as income tax expense

The income tax expense reported in the income statement is not same as income tax paid

listed in the cash flow statements. The main reason behind difference is that accounting rules and

regulations in relation to the financial reporting is way distinguished when tax computation is

done and as such, figures attained are different from each other. Final amount of tax can be

accomplished which must be paid on profits will be different from actual tax bills. It can be

assessed from financial statements that income tax expense is 59.5 reported in income statement.

On the other hand, income tax paid by Grain Corp Ltd in 2017 is 21 which is distinguished from

one another and thus, these are not same (Tahat, Omran and Dunne, 2017).

11. Treatment of tax of firm

The treatment of tax is differently treated by companies as per accounting rules and

policies adopted by it. It can be analysed that Grain Corp Ltd has followed different tax

computation for latest financial year. The method of depreciation chosen by organisation is

straight line and as such, fixed assets are depreciated accordingly. The income tax is regarded as

current liability as it has to be paid in current year. The treatment is made by applying 30 % tax

rate as per the rates applicable by Australian government. Deferred tax computation is not made

on items such as identification of assets and liabilities, goodwill having no impact on income of

firm (Warren and Jones, 2018). Moreover, consolidated tax group has been headed by having

agreement in tax and thus, overall treatment of tax is interesting to understand.

CONCLUSION

Hereby it can be concluded that financial statements are effectively utilised by the parties

to take enhanced decisions. External users of accounting information and management of

organisation are benefited by scrutinising financials. Thus, they are able to take better decisions

quite effectually.

8

Moreover, it is analysed that income tax liability will be increased in the future as current tax

assets are maximised.

10. Is income tax paid same as income tax expense

The income tax expense reported in the income statement is not same as income tax paid

listed in the cash flow statements. The main reason behind difference is that accounting rules and

regulations in relation to the financial reporting is way distinguished when tax computation is

done and as such, figures attained are different from each other. Final amount of tax can be

accomplished which must be paid on profits will be different from actual tax bills. It can be

assessed from financial statements that income tax expense is 59.5 reported in income statement.

On the other hand, income tax paid by Grain Corp Ltd in 2017 is 21 which is distinguished from

one another and thus, these are not same (Tahat, Omran and Dunne, 2017).

11. Treatment of tax of firm

The treatment of tax is differently treated by companies as per accounting rules and

policies adopted by it. It can be analysed that Grain Corp Ltd has followed different tax

computation for latest financial year. The method of depreciation chosen by organisation is

straight line and as such, fixed assets are depreciated accordingly. The income tax is regarded as

current liability as it has to be paid in current year. The treatment is made by applying 30 % tax

rate as per the rates applicable by Australian government. Deferred tax computation is not made

on items such as identification of assets and liabilities, goodwill having no impact on income of

firm (Warren and Jones, 2018). Moreover, consolidated tax group has been headed by having

agreement in tax and thus, overall treatment of tax is interesting to understand.

CONCLUSION

Hereby it can be concluded that financial statements are effectively utilised by the parties

to take enhanced decisions. External users of accounting information and management of

organisation are benefited by scrutinising financials. Thus, they are able to take better decisions

quite effectually.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance. 7(01). p.1650014.

García-Meca, E., López-Iturriaga, F. and Tejerina-Gaite, F., 2017. Institutional investors on

boards: Does their behavior influence corporate finance?. Journal of Business

Ethics,146(2), pp.365-382.

Häcker, J. and Ernst, D., 2017. Corporate Finance Part I. InFinancial Modeling (pp. 501-622).

Palgrave Macmillan, London.

Harris, P., Kinkela, K., Arnold, L.W. and Liu, M., 2017. Corporate Accounting Malfeasance and

Financial Reporting Restatements in the Post-Sarbanes-Oxley Era.

9

Books and Journals

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance. 7(01). p.1650014.

García-Meca, E., López-Iturriaga, F. and Tejerina-Gaite, F., 2017. Institutional investors on

boards: Does their behavior influence corporate finance?. Journal of Business

Ethics,146(2), pp.365-382.

Häcker, J. and Ernst, D., 2017. Corporate Finance Part I. InFinancial Modeling (pp. 501-622).

Palgrave Macmillan, London.

Harris, P., Kinkela, K., Arnold, L.W. and Liu, M., 2017. Corporate Accounting Malfeasance and

Financial Reporting Restatements in the Post-Sarbanes-Oxley Era.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.