Sourcing Funds

Added on 2022-10-17

21 Pages3548 Words244 Views

Running head: REPORT 1

Corporate and Financial accounting

Student details:

9/24/2019

Corporate and Financial accounting

Student details:

9/24/2019

REPORT 2

Abstract

It is required by the companies to raise the capital funds or external funds, for expanding the

businesses in new marketplaces or places, for investing in research as well as development, or

for fending off competition. Sourcing money can be made for the various reasons. The

conventional fields of the requirement can be for capital asset gaining - new machineries or a

creation of a new buildings and depots. Production of new products may be extremely costly as

well as here again capital can be needed. Usually, this development is funded internally, where

the capital for acquirement of machineries can come from external resources. In recent as well as

age of tight liquidity, various entities have searched the short term capital in a manner of

overdrafts and loans for rendering the cash flow cushion. The rate of interest may differ from

company to company and also as per the purposes. The following parts discuss significance and

drawback of the sources of funds, concept of large and small proprietary companies and concept

of reporting entity.

Abstract

It is required by the companies to raise the capital funds or external funds, for expanding the

businesses in new marketplaces or places, for investing in research as well as development, or

for fending off competition. Sourcing money can be made for the various reasons. The

conventional fields of the requirement can be for capital asset gaining - new machineries or a

creation of a new buildings and depots. Production of new products may be extremely costly as

well as here again capital can be needed. Usually, this development is funded internally, where

the capital for acquirement of machineries can come from external resources. In recent as well as

age of tight liquidity, various entities have searched the short term capital in a manner of

overdrafts and loans for rendering the cash flow cushion. The rate of interest may differ from

company to company and also as per the purposes. The following parts discuss significance and

drawback of the sources of funds, concept of large and small proprietary companies and concept

of reporting entity.

REPORT 3

Contents

Introduction......................................................................................................................................4

Part-A...............................................................................................................................................4

Items recorded under owner’s equity section..............................................................................4

Movement over three years period in each item recorded under equity section..........................4

Items recorded under liabilities section.......................................................................................9

Movement over three years period in items recorded under liabilities section.........................10

Advantages and disadvantages of sources of fund.....................................................................13

Part-B.............................................................................................................................................14

Concepts of small proprietary company, large proprietary company and reporting entity.......14

Implications of three types of companies in relation to compliance and reporting requirements

....................................................................................................................................................15

Conclusion.....................................................................................................................................15

References......................................................................................................................................17

Contents

Introduction......................................................................................................................................4

Part-A...............................................................................................................................................4

Items recorded under owner’s equity section..............................................................................4

Movement over three years period in each item recorded under equity section..........................4

Items recorded under liabilities section.......................................................................................9

Movement over three years period in items recorded under liabilities section.........................10

Advantages and disadvantages of sources of fund.....................................................................13

Part-B.............................................................................................................................................14

Concepts of small proprietary company, large proprietary company and reporting entity.......14

Implications of three types of companies in relation to compliance and reporting requirements

....................................................................................................................................................15

Conclusion.....................................................................................................................................15

References......................................................................................................................................17

REPORT 4

Introduction

When the corporations aim to utilize the profits from business functions to fund like projects, this

is regularly more favorable for companies to look for external investors as well as lenders. In

spite of the differences amongst numerous organizations everywhere in the world across

numerous industries, there are some sources of fund accessible to entities. The sources of

funds for the business are debt, equity, debenture, term-loan, letter of credit, retained earnings,

working capital loan, as well as venture-funds and others (cremers, et. al, 2016). All sources of

funds can be useful in different conditions. They are categorized as per the period, and

regulation, ownership along with the generation’s sources. In the following parts, different

sources of fund used by Commonwealth Bank and ANZ bank is discussed and critically

examined. The first also recognizes the movement over the three periods in the sources of funds

used by Commonwealth Bank and ANZ bank. The second part also states the concept of small

proprietary company, large proprietary company and reporting entity, and implications of them

in relation to compliance as well reporting requirements.

Part-A

Items recorded under owner’s equity section

The owner's equity or shareholder’s equity is described as a proportion of total value of the

assets of corporation, which may be claimed by the owners such as partner sole proprietor. The

owner's or shareholder’s equity is considered (along with liability) as the business asset’s source.

Introduction

When the corporations aim to utilize the profits from business functions to fund like projects, this

is regularly more favorable for companies to look for external investors as well as lenders. In

spite of the differences amongst numerous organizations everywhere in the world across

numerous industries, there are some sources of fund accessible to entities. The sources of

funds for the business are debt, equity, debenture, term-loan, letter of credit, retained earnings,

working capital loan, as well as venture-funds and others (cremers, et. al, 2016). All sources of

funds can be useful in different conditions. They are categorized as per the period, and

regulation, ownership along with the generation’s sources. In the following parts, different

sources of fund used by Commonwealth Bank and ANZ bank is discussed and critically

examined. The first also recognizes the movement over the three periods in the sources of funds

used by Commonwealth Bank and ANZ bank. The second part also states the concept of small

proprietary company, large proprietary company and reporting entity, and implications of them

in relation to compliance as well reporting requirements.

Part-A

Items recorded under owner’s equity section

The owner's equity or shareholder’s equity is described as a proportion of total value of the

assets of corporation, which may be claimed by the owners such as partner sole proprietor. The

owner's or shareholder’s equity is considered (along with liability) as the business asset’s source.

REPORT 5

The major elements of the shareholder’s equity (owner’s equity) cover the retained earnings,

outstanding shares, treasury stock as well as additional paid up capital (Carini, 2018).

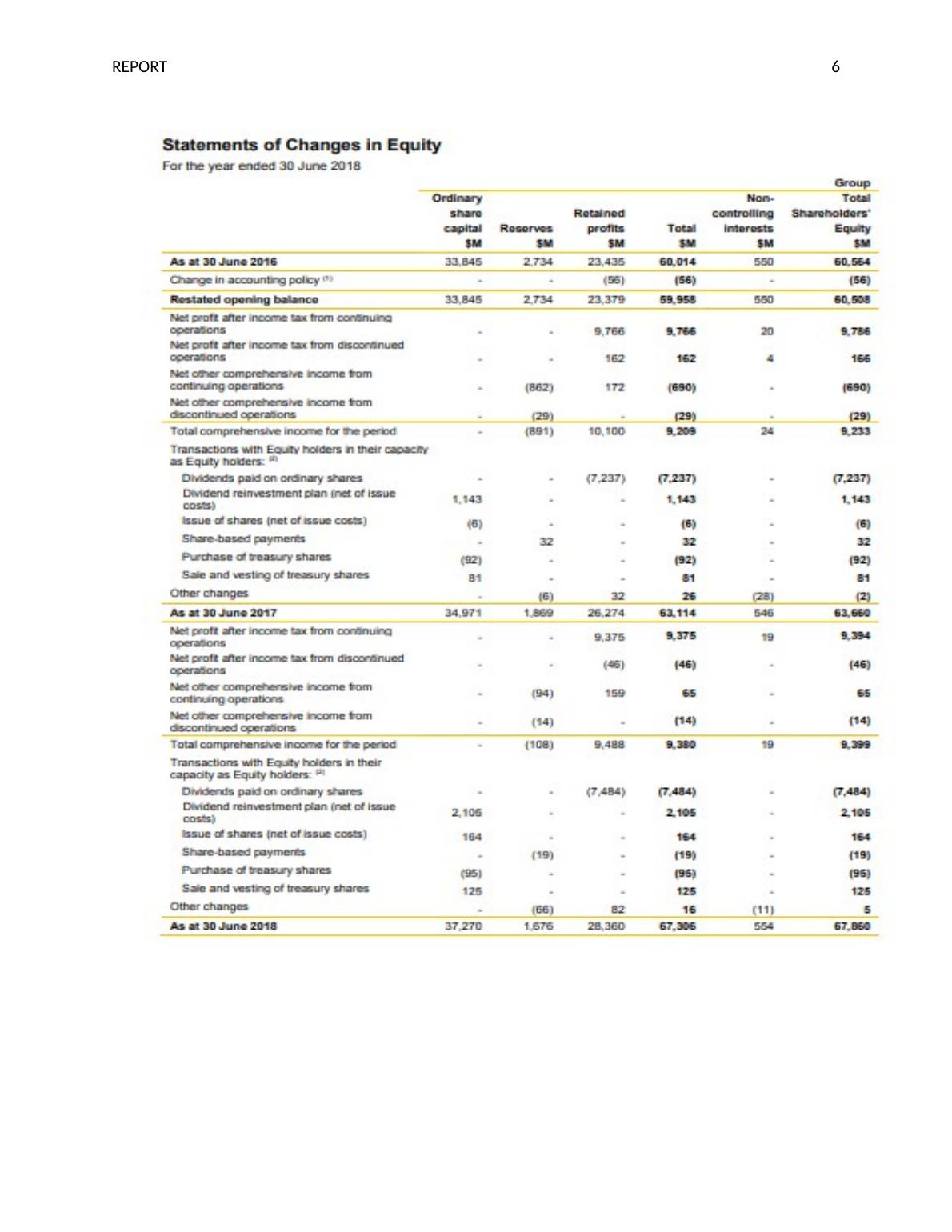

From the annual report of ANZ Bank, it is analyzed that there are some items are recorded under

owner’s equity. These items are ordinary share capital, reserves as well as retained earnings. It is

stated that Shares capital and reserve distributed to stakeholders of an organization, and non-

controlling interest are also recorded under the Owner’s equity or shareholder’s equity.

Furthermore, when Commonwealth Bank’s annual report is analyzed, this is found that items

recorded under the owner or owner’s equity are reserves, retained profits along with ordinary

share-capital. In addition, non-controlling interest as well as shareholders’ Equity distributed to

Equity holders is also covered under owner’s equity (Suryanta, 2016).

Movement over three years period in each item recorded under equity section

The main accounts, which affect the owner's equity, include revenue, expense, gain as well as the

loss. The owner's equity would enhance in case of having gains as well as revenues. The owner's

equity reduces in case of incurring losses as well as expenditures (Allashel, 2015). In a case,

when the liabilities become higher than the assets, the company would have the negative owner's

equity. The movement over three years in items recorded under equity is explained below-

Commonwealth Bank-

The major elements of the shareholder’s equity (owner’s equity) cover the retained earnings,

outstanding shares, treasury stock as well as additional paid up capital (Carini, 2018).

From the annual report of ANZ Bank, it is analyzed that there are some items are recorded under

owner’s equity. These items are ordinary share capital, reserves as well as retained earnings. It is

stated that Shares capital and reserve distributed to stakeholders of an organization, and non-

controlling interest are also recorded under the Owner’s equity or shareholder’s equity.

Furthermore, when Commonwealth Bank’s annual report is analyzed, this is found that items

recorded under the owner or owner’s equity are reserves, retained profits along with ordinary

share-capital. In addition, non-controlling interest as well as shareholders’ Equity distributed to

Equity holders is also covered under owner’s equity (Suryanta, 2016).

Movement over three years period in each item recorded under equity section

The main accounts, which affect the owner's equity, include revenue, expense, gain as well as the

loss. The owner's equity would enhance in case of having gains as well as revenues. The owner's

equity reduces in case of incurring losses as well as expenditures (Allashel, 2015). In a case,

when the liabilities become higher than the assets, the company would have the negative owner's

equity. The movement over three years in items recorded under equity is explained below-

Commonwealth Bank-

REPORT 6

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

HA2032 Corporate and Financial Accounting Report 2022lg...

|15

|4085

|21

Corporate & Financial Accounting Assignmentlg...

|15

|3652

|35

Corporate Accounting Report 2022lg...

|16

|2922

|16

Corporate Accounting Report 2022lg...

|15

|2851

|12

Equity and Liabilities Analysis of Commonwealth Bank and Bank of Queenslandlg...

|10

|2402

|181

Corporate and Financial Accounting 2022 Reportlg...

|17

|3557

|9