Corporate and Financial Accounting

VerifiedAdded on 2023/04/03

|9

|2562

|446

AI Summary

The report discusses the consolidation method in accounting for mergers, intragroup sales, and non-controlling interest disclosure in the consolidated financial statement.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: Corporate and Financial Accounting

Corporate and Financial Accounting

Name of the Student

Name of the University

Author Note

Corporate and Financial Accounting

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

Corporate and Financial Accounting

Executive Summary

The report has been based on the consolidation as it shows how the company

should use the method of accounting for the merger so that it can able to do the

proper accounting transaction. It also explains about the intragroup sale and how it

has been recorded the unrealized profit in the company. Lastly, it shows the non-

controlling interest and how it should do the disclosure in the consolidated financial

statement of the company

Corporate and Financial Accounting

Executive Summary

The report has been based on the consolidation as it shows how the company

should use the method of accounting for the merger so that it can able to do the

proper accounting transaction. It also explains about the intragroup sale and how it

has been recorded the unrealized profit in the company. Lastly, it shows the non-

controlling interest and how it should do the disclosure in the consolidated financial

statement of the company

2

Corporate and Financial Accounting

Table of Contents

Introduction...................................................................................................................3

Part A:...........................................................................................................................3

Part B............................................................................................................................5

Part C............................................................................................................................6

Conclusion....................................................................................................................7

Reference.....................................................................................................................9

Corporate and Financial Accounting

Table of Contents

Introduction...................................................................................................................3

Part A:...........................................................................................................................3

Part B............................................................................................................................5

Part C............................................................................................................................6

Conclusion....................................................................................................................7

Reference.....................................................................................................................9

3

Corporate and Financial Accounting

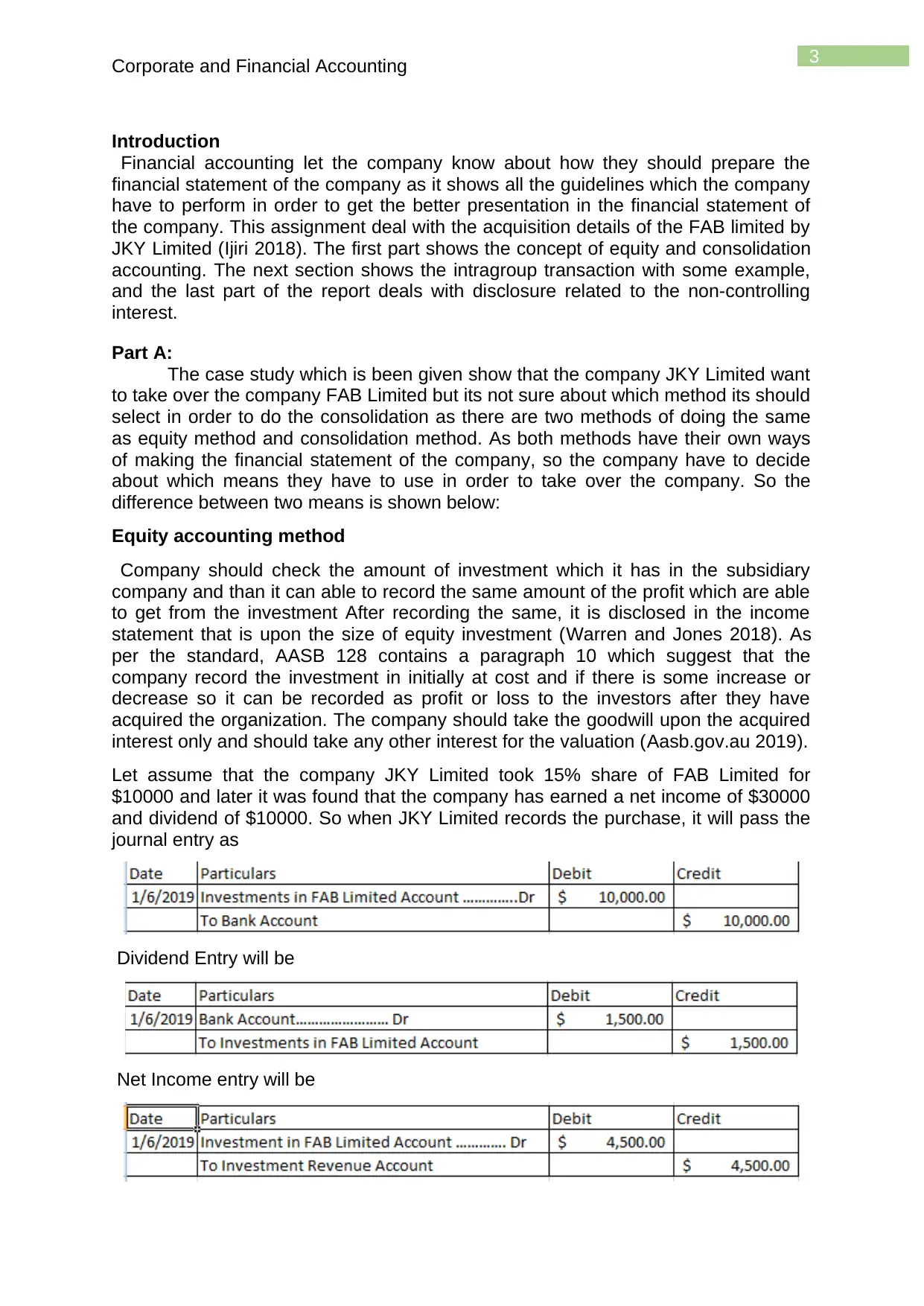

Introduction

Financial accounting let the company know about how they should prepare the

financial statement of the company as it shows all the guidelines which the company

have to perform in order to get the better presentation in the financial statement of

the company. This assignment deal with the acquisition details of the FAB limited by

JKY Limited (Ijiri 2018). The first part shows the concept of equity and consolidation

accounting. The next section shows the intragroup transaction with some example,

and the last part of the report deals with disclosure related to the non-controlling

interest.

Part A:

The case study which is been given show that the company JKY Limited want

to take over the company FAB Limited but its not sure about which method its should

select in order to do the consolidation as there are two methods of doing the same

as equity method and consolidation method. As both methods have their own ways

of making the financial statement of the company, so the company have to decide

about which means they have to use in order to take over the company. So the

difference between two means is shown below:

Equity accounting method

Company should check the amount of investment which it has in the subsidiary

company and than it can able to record the same amount of the profit which are able

to get from the investment After recording the same, it is disclosed in the income

statement that is upon the size of equity investment (Warren and Jones 2018). As

per the standard, AASB 128 contains a paragraph 10 which suggest that the

company record the investment in initially at cost and if there is some increase or

decrease so it can be recorded as profit or loss to the investors after they have

acquired the organization. The company should take the goodwill upon the acquired

interest only and should take any other interest for the valuation (Aasb.gov.au 2019).

Let assume that the company JKY Limited took 15% share of FAB Limited for

$10000 and later it was found that the company has earned a net income of $30000

and dividend of $10000. So when JKY Limited records the purchase, it will pass the

journal entry as

Dividend Entry will be

Net Income entry will be

Corporate and Financial Accounting

Introduction

Financial accounting let the company know about how they should prepare the

financial statement of the company as it shows all the guidelines which the company

have to perform in order to get the better presentation in the financial statement of

the company. This assignment deal with the acquisition details of the FAB limited by

JKY Limited (Ijiri 2018). The first part shows the concept of equity and consolidation

accounting. The next section shows the intragroup transaction with some example,

and the last part of the report deals with disclosure related to the non-controlling

interest.

Part A:

The case study which is been given show that the company JKY Limited want

to take over the company FAB Limited but its not sure about which method its should

select in order to do the consolidation as there are two methods of doing the same

as equity method and consolidation method. As both methods have their own ways

of making the financial statement of the company, so the company have to decide

about which means they have to use in order to take over the company. So the

difference between two means is shown below:

Equity accounting method

Company should check the amount of investment which it has in the subsidiary

company and than it can able to record the same amount of the profit which are able

to get from the investment After recording the same, it is disclosed in the income

statement that is upon the size of equity investment (Warren and Jones 2018). As

per the standard, AASB 128 contains a paragraph 10 which suggest that the

company record the investment in initially at cost and if there is some increase or

decrease so it can be recorded as profit or loss to the investors after they have

acquired the organization. The company should take the goodwill upon the acquired

interest only and should take any other interest for the valuation (Aasb.gov.au 2019).

Let assume that the company JKY Limited took 15% share of FAB Limited for

$10000 and later it was found that the company has earned a net income of $30000

and dividend of $10000. So when JKY Limited records the purchase, it will pass the

journal entry as

Dividend Entry will be

Net Income entry will be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

Corporate and Financial Accounting

Consolidation Method of Accounting

As per this method the company should record the proportion of the interest in the

joint venture as the percentage it help should only be recorded. The company has to

show all the expenses and income which they have been displayed in the financial

statement as to when the time of valuation of the asset and liabilities have come in

the balance sheet. As per AASB 10 contain a paragraph B86 which state that the

company consolidation statement is a combination of all the items of the parent

company with its subsidiary companies as it includes things like an asset, liability,

equity and many other activities. It even able to minimize the risk of double

accounting as it does not take into consideration about the intercompany transaction,

so it helps the company to keep accounts as simple they can keep.

As per the AASB 10 which have a paragraph B88 which contain details about

the measurement of the requirement which is to do in the set of different lines items

of the company financial statement which is been related to the income and

expenses of the subsidiary company that are directly related to the asset and

liabilities so the amounts which is been realised in the statement of consolidation at

the time of the acquisition. As per the AASB 3, it contains a paragraph 32 which

state about how the company is able to recognize the goodwill in the financial

statement and to recognize it have to select higher of the same and should record it

after it able to get the value of it

The example is that let take JKY Ltd have invested $60 million for the start-up so it

will show it as

So it invested in FAB Limited sum of $50million so entry will be

In the books of FAB Limited

Part B

As the company wants to prepare the consolidated accounts so to do that, it has to

eliminate all the operation which happen in between the two entity, and it has to

remove the also part of the equity which the parent organization holds in the body

(Paterson et al ., 2018). As per the AASB 127, it contains a paragraph which says

that the company has to eliminate the intra-group balances and also all the income

and expense related to the same. The intra-group can be classified as:

The transaction which are done between the parent company and the subsidiary

company it can be anything such as some payments in between the two or some

amount of sale transfer.

Corporate and Financial Accounting

Consolidation Method of Accounting

As per this method the company should record the proportion of the interest in the

joint venture as the percentage it help should only be recorded. The company has to

show all the expenses and income which they have been displayed in the financial

statement as to when the time of valuation of the asset and liabilities have come in

the balance sheet. As per AASB 10 contain a paragraph B86 which state that the

company consolidation statement is a combination of all the items of the parent

company with its subsidiary companies as it includes things like an asset, liability,

equity and many other activities. It even able to minimize the risk of double

accounting as it does not take into consideration about the intercompany transaction,

so it helps the company to keep accounts as simple they can keep.

As per the AASB 10 which have a paragraph B88 which contain details about

the measurement of the requirement which is to do in the set of different lines items

of the company financial statement which is been related to the income and

expenses of the subsidiary company that are directly related to the asset and

liabilities so the amounts which is been realised in the statement of consolidation at

the time of the acquisition. As per the AASB 3, it contains a paragraph 32 which

state about how the company is able to recognize the goodwill in the financial

statement and to recognize it have to select higher of the same and should record it

after it able to get the value of it

The example is that let take JKY Ltd have invested $60 million for the start-up so it

will show it as

So it invested in FAB Limited sum of $50million so entry will be

In the books of FAB Limited

Part B

As the company wants to prepare the consolidated accounts so to do that, it has to

eliminate all the operation which happen in between the two entity, and it has to

remove the also part of the equity which the parent organization holds in the body

(Paterson et al ., 2018). As per the AASB 127, it contains a paragraph which says

that the company has to eliminate the intra-group balances and also all the income

and expense related to the same. The intra-group can be classified as:

The transaction which are done between the parent company and the subsidiary

company it can be anything such as some payments in between the two or some

amount of sale transfer.

5

Corporate and Financial Accounting

As per the adjustment related to the consolidation of the intra-group transaction

eliminate all the deal by doing the reversal of the transaction of accounting, which

has been done by the company.

As per the case study, it can be seen that the company JKY Limited want to

make the purchase of inventory from its one of the owned subsidiary company.

As the company is concerned, it cannot record the revenue as it can be only able

to do after the sale has been made to the external parties. So if there is some

unrealized profit so it should be removed from the consolidated accounts, the

unrealized gain is the profit which should be taken in the inventory form the gain

at the end of the year. As per the AASB 127, it contains a paragraph 25 which

say about the if the company is able to have some amount of profit or losses

which arise from the intra-group transaction so it should be recorded in the

financial statement as a non-current asset and the part of the inventory is totally

eliminated.

As per the case study, it can be seen that the subsidiary has sold some

inventory to JKY Limited, and it is considered as that it should have a mark-up

portion included in the stock. It can be said as the external sale has been made

so it should be fine as a group transaction point. As the company have not done

the deal to the external customer so does not able to earn profit, but as the

subsidiary has sold them to JXY Limited, so it was recorded as an unrealized

profit, so it directly affects the overall group profit, and it will show a high amount

of profit which is not really happening in the company. As per assumption is

made that the company have purchased the inventory from subsidiary as

$15000, at it is kept at the end of the year. Next assumption which can be made

is the subsidiary keeps 25% of the margin and so is able to earn a profit on

inventory as $3000 (25/125 * $15000). So as per the group profit is consider the

overvalued amount in profit is $3000, so the adjust the amount is should pass this

entry as:

Consolidated Profit Account Dr $3000

To Consolidated Inventory Account $3000

The sales of the non-controlling interest to the group which has been done by

the subsidiary than it should eliminate the unrealized profit of the same. So this

transaction led to make the question about the gain which should be reported in

the non-controlling interest. The approaches can be different; one method can be

that it should assign a share of un-recognized profit to the non-controlling

interest. So, as a result, it directly removed all the profit which is generated by the

selling entity. The different method which can be used by the company is that it

should not record any portion of the unrecognized profit in the non-controlling

interest and as a result of it, the figure related to non-controlling interest should

be included in the reserves and share capital which is in regards of the subsidiary

company (Jefrey 2018).

Part C

Separate items effects upon NCI Disclosures

Corporate and Financial Accounting

As per the adjustment related to the consolidation of the intra-group transaction

eliminate all the deal by doing the reversal of the transaction of accounting, which

has been done by the company.

As per the case study, it can be seen that the company JKY Limited want to

make the purchase of inventory from its one of the owned subsidiary company.

As the company is concerned, it cannot record the revenue as it can be only able

to do after the sale has been made to the external parties. So if there is some

unrealized profit so it should be removed from the consolidated accounts, the

unrealized gain is the profit which should be taken in the inventory form the gain

at the end of the year. As per the AASB 127, it contains a paragraph 25 which

say about the if the company is able to have some amount of profit or losses

which arise from the intra-group transaction so it should be recorded in the

financial statement as a non-current asset and the part of the inventory is totally

eliminated.

As per the case study, it can be seen that the subsidiary has sold some

inventory to JKY Limited, and it is considered as that it should have a mark-up

portion included in the stock. It can be said as the external sale has been made

so it should be fine as a group transaction point. As the company have not done

the deal to the external customer so does not able to earn profit, but as the

subsidiary has sold them to JXY Limited, so it was recorded as an unrealized

profit, so it directly affects the overall group profit, and it will show a high amount

of profit which is not really happening in the company. As per assumption is

made that the company have purchased the inventory from subsidiary as

$15000, at it is kept at the end of the year. Next assumption which can be made

is the subsidiary keeps 25% of the margin and so is able to earn a profit on

inventory as $3000 (25/125 * $15000). So as per the group profit is consider the

overvalued amount in profit is $3000, so the adjust the amount is should pass this

entry as:

Consolidated Profit Account Dr $3000

To Consolidated Inventory Account $3000

The sales of the non-controlling interest to the group which has been done by

the subsidiary than it should eliminate the unrealized profit of the same. So this

transaction led to make the question about the gain which should be reported in

the non-controlling interest. The approaches can be different; one method can be

that it should assign a share of un-recognized profit to the non-controlling

interest. So, as a result, it directly removed all the profit which is generated by the

selling entity. The different method which can be used by the company is that it

should not record any portion of the unrecognized profit in the non-controlling

interest and as a result of it, the figure related to non-controlling interest should

be included in the reserves and share capital which is in regards of the subsidiary

company (Jefrey 2018).

Part C

Separate items effects upon NCI Disclosures

6

Corporate and Financial Accounting

In the standard of AASB 127 in the paragraph 27 states that it should state

about the consolidated financial statement so that the company should do the

presentation separately in regards of the noncontrolling asset which have been

related to the interest that the company gets from the equity of the parent company.

Non-controlling interest cannot be included to the parent firm as it is the equity

related to the subsidiary. So this standard was beneficial in regards to the

development of the accounting and the reporting associated with the non-controlling

interest in regards to the financial statement of the company. There is a separate

reporting in regards of the non-controlling interest in the consolidation process, and

also it should record the change which is reconciled in considerations of the

shareholder's equity which has been in the parent company and as per even the

non-controlling interest. As per the ASA 101, the paragraphs contain state that it

should able to recognize the amount. This compliance of the better presentation is

being done so that it can able to give the proper amount of understanding to the

stakeholder as well to the person who owns their claims in the group of the

company.

The variation which is related to the ownership interest of the parent company is

termed as an equity transaction. It also is seen that it is not able to take place when

the parent company loses its control over the subsidiary company. So if the interest

is changed in the portion of the equity that change represents the adjustments upon

the carrying values of the controlling and non-controlling interest, as the transaction

is being done, then it should consider the correction about the fair value and non-

controlling interest should directly recognize and should be recorded in the

shareholders to the parent organization.

Changes in order to ensure the accurate representation of the consolidated

financial statement:

AS per the standard of AASB 101 state, there should be some change in the

description of the consolidated financial statements. It states that all the transaction

which are happening in the subsidiary and the parent company should be

appropriately adjusted and also it says that the preparation of the statement should

not be done in the same reporting time. It too so that the investment which the

company has done in the subsidiary it should be eliminated and even the equity

portion which the subsidiary company holds in the parent company should also be

eliminated.

The amount of the asset which is done as impairment in the associated should be

recognized as the intragroup losses. So it should eliminate all the transaction related

to the intragroup such as income, expense, and other transaction in the company

(Aasb.gov.au 2019). The consolidation should record all the transaction of the parent

as well as the subsidiary company as items such as balance sheet, and also other

activities. It should also take into consideration AASB 1112 while doing the

consolidation. The group should use proper accounting policy and which is used in

all the company and it should also show about the different adjustment which should

be done by the company in regards of the statement so that it can help the user to

get proper details of the same (Braam and Peeters 2018).

The company should have to record the overall income in regards to the non-

controlling interest and the parent owners; it should be done even there is some

Corporate and Financial Accounting

In the standard of AASB 127 in the paragraph 27 states that it should state

about the consolidated financial statement so that the company should do the

presentation separately in regards of the noncontrolling asset which have been

related to the interest that the company gets from the equity of the parent company.

Non-controlling interest cannot be included to the parent firm as it is the equity

related to the subsidiary. So this standard was beneficial in regards to the

development of the accounting and the reporting associated with the non-controlling

interest in regards to the financial statement of the company. There is a separate

reporting in regards of the non-controlling interest in the consolidation process, and

also it should record the change which is reconciled in considerations of the

shareholder's equity which has been in the parent company and as per even the

non-controlling interest. As per the ASA 101, the paragraphs contain state that it

should able to recognize the amount. This compliance of the better presentation is

being done so that it can able to give the proper amount of understanding to the

stakeholder as well to the person who owns their claims in the group of the

company.

The variation which is related to the ownership interest of the parent company is

termed as an equity transaction. It also is seen that it is not able to take place when

the parent company loses its control over the subsidiary company. So if the interest

is changed in the portion of the equity that change represents the adjustments upon

the carrying values of the controlling and non-controlling interest, as the transaction

is being done, then it should consider the correction about the fair value and non-

controlling interest should directly recognize and should be recorded in the

shareholders to the parent organization.

Changes in order to ensure the accurate representation of the consolidated

financial statement:

AS per the standard of AASB 101 state, there should be some change in the

description of the consolidated financial statements. It states that all the transaction

which are happening in the subsidiary and the parent company should be

appropriately adjusted and also it says that the preparation of the statement should

not be done in the same reporting time. It too so that the investment which the

company has done in the subsidiary it should be eliminated and even the equity

portion which the subsidiary company holds in the parent company should also be

eliminated.

The amount of the asset which is done as impairment in the associated should be

recognized as the intragroup losses. So it should eliminate all the transaction related

to the intragroup such as income, expense, and other transaction in the company

(Aasb.gov.au 2019). The consolidation should record all the transaction of the parent

as well as the subsidiary company as items such as balance sheet, and also other

activities. It should also take into consideration AASB 1112 while doing the

consolidation. The group should use proper accounting policy and which is used in

all the company and it should also show about the different adjustment which should

be done by the company in regards of the statement so that it can help the user to

get proper details of the same (Braam and Peeters 2018).

The company should have to record the overall income in regards to the non-

controlling interest and the parent owners; it should be done even there is some

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Corporate and Financial Accounting

harmful effects f the same in the non-controlling interest. If the company have some

preference share so it should make the adjustment of the dividend and as the

preferences share are cumulative in nature.

Changes in disclosure in the annual report:

As per the AASB 127, it contains a paragraph 10 which state that when the

company has to prepare the separated financials statement that in should the show

the investment in the joint venture as in cost. The company should able to disclose

all the related information in the consolidated financial statement of the company as

it should what is the estimation of the company is done and also about the

accounting policy is associated with the same (Aasb.gov.au 2019). It should also

disclose the nature of the transaction related to the subsidiary so that it can be able

to know all the details of the consolidation.

If the company is having different accounting date as both the parent and subsidiary

company have different reporting date so the proper disclosure is made in regards of

the same so that the user can able to understand the reason of the various reporting

date (Aasb.gov.au 2019), it is also be done that if the company is not having more

than 50% share than proper disclosure is to be done so that the company

shareholder can able to know the reason and able to take a necessary decision

about the same.

Conclusion

On the final note, it can be said that the consolidation can be done by the two

methods equity and consolidation method. The report concludes about the Company

JXY Limited as it wants to acquire the FAB Limited so which purpose is to be used

by the company. It also shows the intra purchase in the group of the company and

how it should be treated in the account. Lastly, it reveals about the consolidation

which is done as the non-controlling interest as to how it should be treated and how

it can affect the disclosure of the consolidated financial statement.

Corporate and Financial Accounting

harmful effects f the same in the non-controlling interest. If the company have some

preference share so it should make the adjustment of the dividend and as the

preferences share are cumulative in nature.

Changes in disclosure in the annual report:

As per the AASB 127, it contains a paragraph 10 which state that when the

company has to prepare the separated financials statement that in should the show

the investment in the joint venture as in cost. The company should able to disclose

all the related information in the consolidated financial statement of the company as

it should what is the estimation of the company is done and also about the

accounting policy is associated with the same (Aasb.gov.au 2019). It should also

disclose the nature of the transaction related to the subsidiary so that it can be able

to know all the details of the consolidation.

If the company is having different accounting date as both the parent and subsidiary

company have different reporting date so the proper disclosure is made in regards of

the same so that the user can able to understand the reason of the various reporting

date (Aasb.gov.au 2019), it is also be done that if the company is not having more

than 50% share than proper disclosure is to be done so that the company

shareholder can able to know the reason and able to take a necessary decision

about the same.

Conclusion

On the final note, it can be said that the consolidation can be done by the two

methods equity and consolidation method. The report concludes about the Company

JXY Limited as it wants to acquire the FAB Limited so which purpose is to be used

by the company. It also shows the intra purchase in the group of the company and

how it should be treated in the account. Lastly, it reveals about the consolidation

which is done as the non-controlling interest as to how it should be treated and how

it can affect the disclosure of the consolidated financial statement.

8

Corporate and Financial Accounting

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 28

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

28 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 28

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 28 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed

28 May 2019].

Braam, G. and Peeters, R., 2018. Corporate sustainability performance and

assurance on sustainability reports: Diffusion of accounting practices in the realm of

sustainable development. Corporate Social Responsibility and Environmental

Management, 25(2), pp.164-181.

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A

Review. Accounting, Economics, and Law: A Convivium, 8(1).

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in

accounting. Emerald Publishing Limited.

Paterson, A., Yonekura, A., Jackson, W. and Jubb, D. eds., 2018. Contemporary

Issues in Social Accounting. Goodfellow Publishers Limited.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Corporate and Financial Accounting

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 28

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

28 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 28

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 28 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed

28 May 2019].

Braam, G. and Peeters, R., 2018. Corporate sustainability performance and

assurance on sustainability reports: Diffusion of accounting practices in the realm of

sustainable development. Corporate Social Responsibility and Environmental

Management, 25(2), pp.164-181.

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A

Review. Accounting, Economics, and Law: A Convivium, 8(1).

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in

accounting. Emerald Publishing Limited.

Paterson, A., Yonekura, A., Jackson, W. and Jubb, D. eds., 2018. Contemporary

Issues in Social Accounting. Goodfellow Publishers Limited.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.