Balance sheet of ASX listed entities AMP Ltd and Bapcor Ltd

VerifiedAdded on 2022/10/17

|14

|3635

|165

AI Summary

Introduction 4 Part A 4 (i) Owner’s equity and explanation of equity items 4 (ii) Movement of the items reported under owner’s equity 4 (iii) Liabilities and explanation of items reported under equity 5 (iv) Movement of the items reported under owner’s equity 6 (v) Advantages and disadvantages of sources of the funds used by the entities 7 Part B 10 Conclusion 11 Reference 12 Introduction AMP limited is the wealth management entity included under service financial service provider sector.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and financial accounting

Name of the student

Name of the university

Student ID

Author note

Corporate and financial accounting

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE AND FINANCIAL ACCOUNTING

Abstract

The report will highlight the items included in the balance sheet of 2 ASX listed entities AMP

Ltd and Bapcor Ltd. It will focus on the equity items as well as liability items reported by the

entity and the reasons behind the changes in the reported value of those items over the 3

years period covering the year 2016, 2017 and 2018. In the next section of the report, source

of finance used by the entities and their advantages and disadvantages will be reported. In

addition the report will highlight the details of the small proprietary company, large proprietary

company and reporting entity.

Abstract

The report will highlight the items included in the balance sheet of 2 ASX listed entities AMP

Ltd and Bapcor Ltd. It will focus on the equity items as well as liability items reported by the

entity and the reasons behind the changes in the reported value of those items over the 3

years period covering the year 2016, 2017 and 2018. In the next section of the report, source

of finance used by the entities and their advantages and disadvantages will be reported. In

addition the report will highlight the details of the small proprietary company, large proprietary

company and reporting entity.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction.................................................................................................................................4

Part A..........................................................................................................................................4

(i) Owner’s equity and explanation of equity items............................................................4

(ii) Movement of the items reported under owner’s equity.................................................4

(iii) Liabilities and explanation of items reported under equity............................................5

(iv) Movement of the items reported under owner’s equity.................................................6

(v) Advantages and disadvantages of sources of the funds used by the entities..............7

Part B........................................................................................................................................10

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

Table of Contents

Introduction.................................................................................................................................4

Part A..........................................................................................................................................4

(i) Owner’s equity and explanation of equity items............................................................4

(ii) Movement of the items reported under owner’s equity.................................................4

(iii) Liabilities and explanation of items reported under equity............................................5

(iv) Movement of the items reported under owner’s equity.................................................6

(v) Advantages and disadvantages of sources of the funds used by the entities..............7

Part B........................................................................................................................................10

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

3CORPORATE AND FINANCIAL ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE AND FINANCIAL ACCOUNTING

Introduction

AMP limited is the wealth management entity included under service financial service

provider sector. Operating segment of the entity includes Australian wealth management that

offers services related to financial services, superannuation linked to unit, platform

administration, managed products related to investment and retirement income. The entity

was formed with simple but bold idea and believed that it may help to empower people for

achieving futures they always wanted (loans, retirement and hub 2019). On the other hand,

Bapcor Limited that was known as Burson Group Limited formerly, provides aftermarket parts

for automotive, servicing of motor vehicles, accessories, automotive services and equipment.

It generates revenues from selling and distributing these products and services and operates

the business in New Zealand, Thailand and Australia. It has retail, trade and specialist

wholesale segments (Bapcor.com.au 2019)

Part A

(i) Owner’s equity and explanation of equity items

Owner’s equity is the ownership of the owner in business. In other words, it represents

the assets owned by owner of the business. It further represents the amount that is invested

by the owner in the business reduced by the amount taken out from the business as the

withdrawal.

AMP Limited – owner’s equity section of the entity includes the following –

Contributed equity – contributed equity that is also known as paid-in-capital is amount

of cash as well as other assets that is contributed by the shareholder in exchange of

the stock. To be more specific, this represents the amount paid by the shareholders in

exchange of their ownership in the entity (Bernstein et al. 2016).

Reserves –generally, the particular reserves are kept aside for fulfilling specific

purpose and are not utilised for any other purposes. Reserves are maintained for

strengthening the entity’s financial position, purchasing fixed asset, clearing credits and

debts and future investments.

Retained earnings – retained earnings are the business profits that is reserved in the

business for the purpose of re-investment and are not distributed to the shareholders

by any means (Goldstein, Jiang and Ng 2017)

Non-controlling interest –this is the minority interest that is the ownership status where

the entity owns lower than 50% of the outstanding shares and does not have any

control on decisions.

Bapcor Limited – owner’s equity section of the entity includes the following –

Issued capital – it is the amount raised through issuing shares to the shareholders by

the entity. To be more specific, shares held or held subsequently by shareholders is

known as the issued capital (Ang et al. 2018).

Reserves – as explained for AMP Limited

Retained earnings –as explained for AMP Limited

Non-controlling interest - as explained for AMP Limited

Introduction

AMP limited is the wealth management entity included under service financial service

provider sector. Operating segment of the entity includes Australian wealth management that

offers services related to financial services, superannuation linked to unit, platform

administration, managed products related to investment and retirement income. The entity

was formed with simple but bold idea and believed that it may help to empower people for

achieving futures they always wanted (loans, retirement and hub 2019). On the other hand,

Bapcor Limited that was known as Burson Group Limited formerly, provides aftermarket parts

for automotive, servicing of motor vehicles, accessories, automotive services and equipment.

It generates revenues from selling and distributing these products and services and operates

the business in New Zealand, Thailand and Australia. It has retail, trade and specialist

wholesale segments (Bapcor.com.au 2019)

Part A

(i) Owner’s equity and explanation of equity items

Owner’s equity is the ownership of the owner in business. In other words, it represents

the assets owned by owner of the business. It further represents the amount that is invested

by the owner in the business reduced by the amount taken out from the business as the

withdrawal.

AMP Limited – owner’s equity section of the entity includes the following –

Contributed equity – contributed equity that is also known as paid-in-capital is amount

of cash as well as other assets that is contributed by the shareholder in exchange of

the stock. To be more specific, this represents the amount paid by the shareholders in

exchange of their ownership in the entity (Bernstein et al. 2016).

Reserves –generally, the particular reserves are kept aside for fulfilling specific

purpose and are not utilised for any other purposes. Reserves are maintained for

strengthening the entity’s financial position, purchasing fixed asset, clearing credits and

debts and future investments.

Retained earnings – retained earnings are the business profits that is reserved in the

business for the purpose of re-investment and are not distributed to the shareholders

by any means (Goldstein, Jiang and Ng 2017)

Non-controlling interest –this is the minority interest that is the ownership status where

the entity owns lower than 50% of the outstanding shares and does not have any

control on decisions.

Bapcor Limited – owner’s equity section of the entity includes the following –

Issued capital – it is the amount raised through issuing shares to the shareholders by

the entity. To be more specific, shares held or held subsequently by shareholders is

known as the issued capital (Ang et al. 2018).

Reserves – as explained for AMP Limited

Retained earnings –as explained for AMP Limited

Non-controlling interest - as explained for AMP Limited

5CORPORATE AND FINANCIAL ACCOUNTING

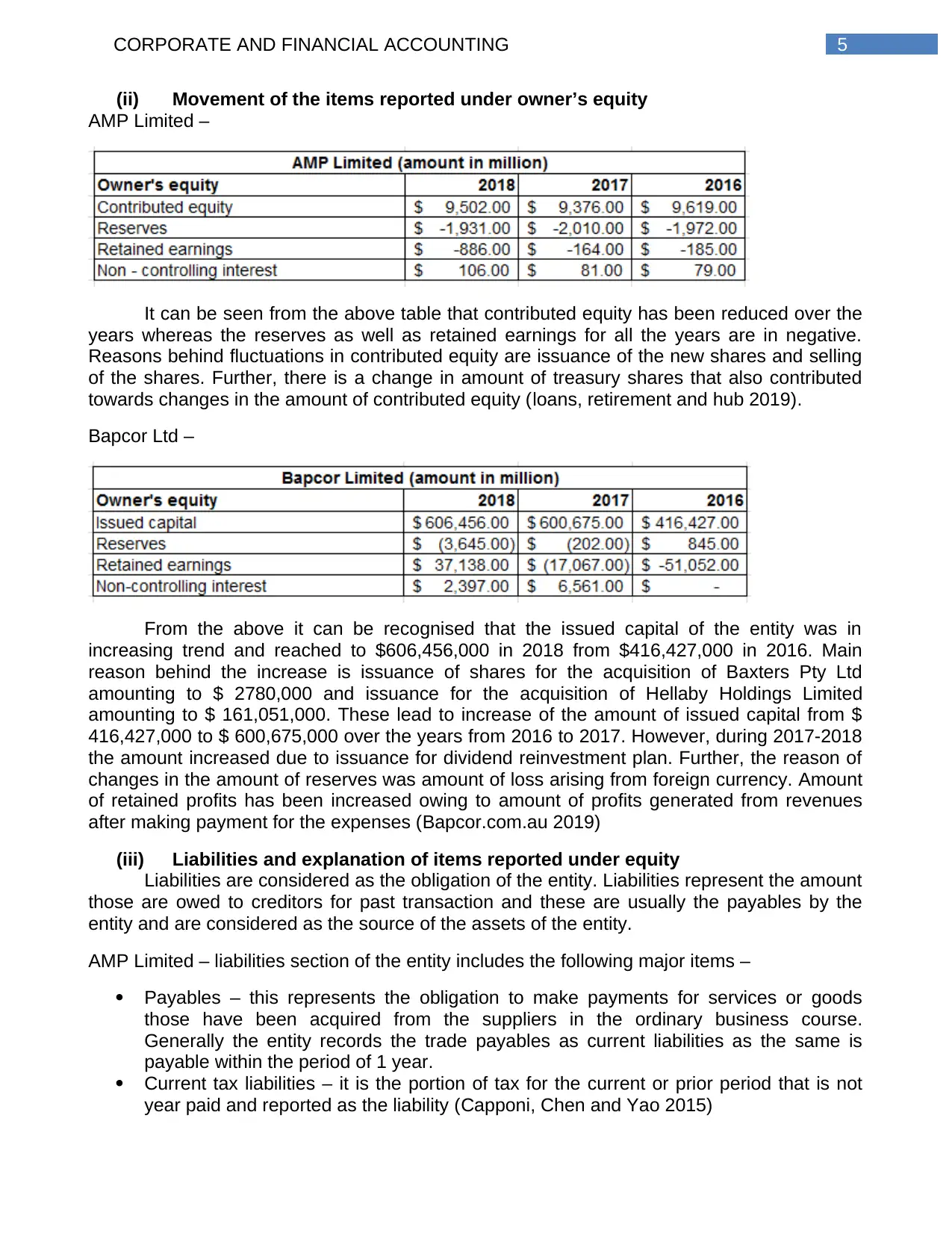

(ii) Movement of the items reported under owner’s equity

AMP Limited –

It can be seen from the above table that contributed equity has been reduced over the

years whereas the reserves as well as retained earnings for all the years are in negative.

Reasons behind fluctuations in contributed equity are issuance of the new shares and selling

of the shares. Further, there is a change in amount of treasury shares that also contributed

towards changes in the amount of contributed equity (loans, retirement and hub 2019).

Bapcor Ltd –

From the above it can be recognised that the issued capital of the entity was in

increasing trend and reached to $606,456,000 in 2018 from $416,427,000 in 2016. Main

reason behind the increase is issuance of shares for the acquisition of Baxters Pty Ltd

amounting to $ 2780,000 and issuance for the acquisition of Hellaby Holdings Limited

amounting to $ 161,051,000. These lead to increase of the amount of issued capital from $

416,427,000 to $ 600,675,000 over the years from 2016 to 2017. However, during 2017-2018

the amount increased due to issuance for dividend reinvestment plan. Further, the reason of

changes in the amount of reserves was amount of loss arising from foreign currency. Amount

of retained profits has been increased owing to amount of profits generated from revenues

after making payment for the expenses (Bapcor.com.au 2019)

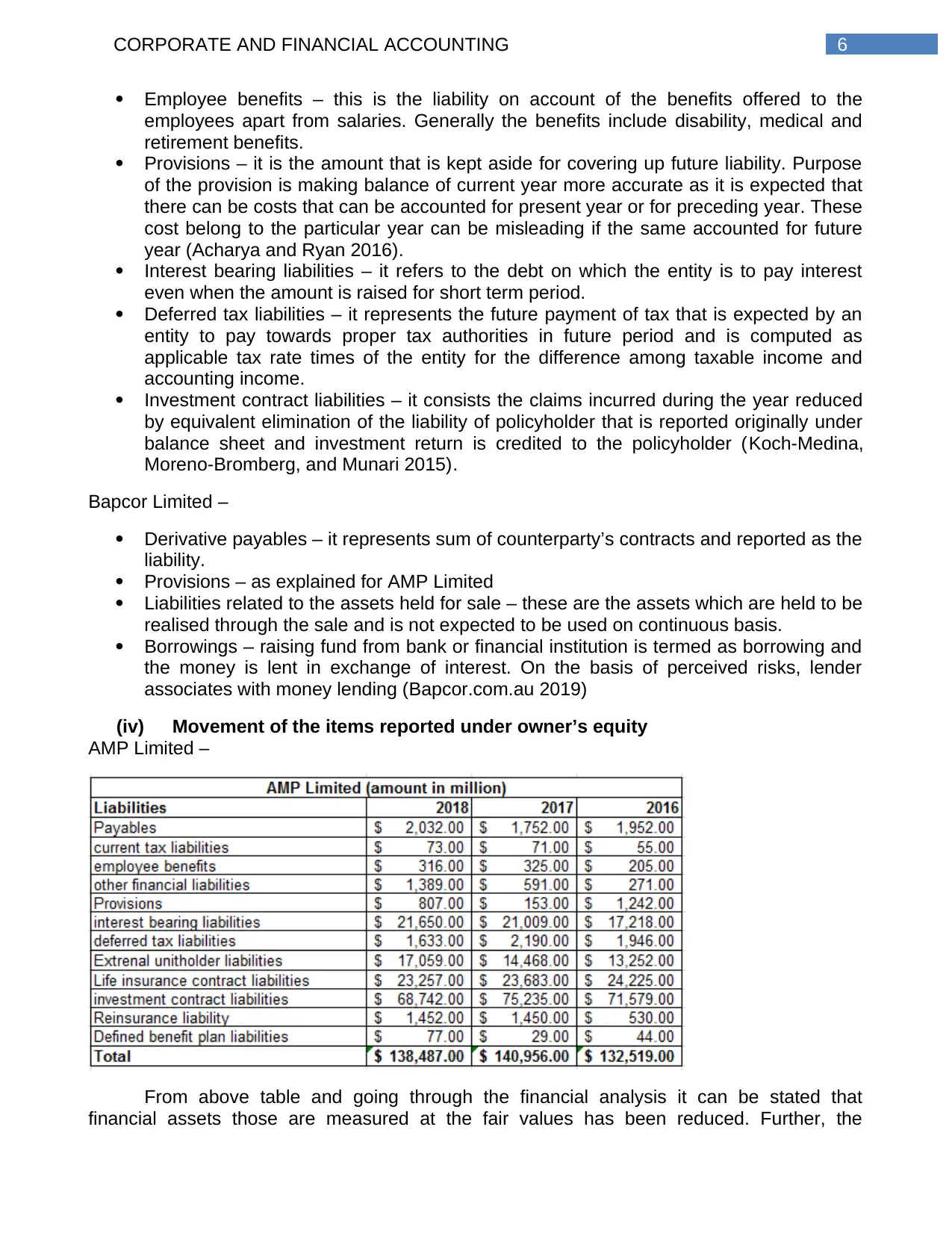

(iii) Liabilities and explanation of items reported under equity

Liabilities are considered as the obligation of the entity. Liabilities represent the amount

those are owed to creditors for past transaction and these are usually the payables by the

entity and are considered as the source of the assets of the entity.

AMP Limited – liabilities section of the entity includes the following major items –

Payables – this represents the obligation to make payments for services or goods

those have been acquired from the suppliers in the ordinary business course.

Generally the entity records the trade payables as current liabilities as the same is

payable within the period of 1 year.

Current tax liabilities – it is the portion of tax for the current or prior period that is not

year paid and reported as the liability (Capponi, Chen and Yao 2015)

(ii) Movement of the items reported under owner’s equity

AMP Limited –

It can be seen from the above table that contributed equity has been reduced over the

years whereas the reserves as well as retained earnings for all the years are in negative.

Reasons behind fluctuations in contributed equity are issuance of the new shares and selling

of the shares. Further, there is a change in amount of treasury shares that also contributed

towards changes in the amount of contributed equity (loans, retirement and hub 2019).

Bapcor Ltd –

From the above it can be recognised that the issued capital of the entity was in

increasing trend and reached to $606,456,000 in 2018 from $416,427,000 in 2016. Main

reason behind the increase is issuance of shares for the acquisition of Baxters Pty Ltd

amounting to $ 2780,000 and issuance for the acquisition of Hellaby Holdings Limited

amounting to $ 161,051,000. These lead to increase of the amount of issued capital from $

416,427,000 to $ 600,675,000 over the years from 2016 to 2017. However, during 2017-2018

the amount increased due to issuance for dividend reinvestment plan. Further, the reason of

changes in the amount of reserves was amount of loss arising from foreign currency. Amount

of retained profits has been increased owing to amount of profits generated from revenues

after making payment for the expenses (Bapcor.com.au 2019)

(iii) Liabilities and explanation of items reported under equity

Liabilities are considered as the obligation of the entity. Liabilities represent the amount

those are owed to creditors for past transaction and these are usually the payables by the

entity and are considered as the source of the assets of the entity.

AMP Limited – liabilities section of the entity includes the following major items –

Payables – this represents the obligation to make payments for services or goods

those have been acquired from the suppliers in the ordinary business course.

Generally the entity records the trade payables as current liabilities as the same is

payable within the period of 1 year.

Current tax liabilities – it is the portion of tax for the current or prior period that is not

year paid and reported as the liability (Capponi, Chen and Yao 2015)

6CORPORATE AND FINANCIAL ACCOUNTING

Employee benefits – this is the liability on account of the benefits offered to the

employees apart from salaries. Generally the benefits include disability, medical and

retirement benefits.

Provisions – it is the amount that is kept aside for covering up future liability. Purpose

of the provision is making balance of current year more accurate as it is expected that

there can be costs that can be accounted for present year or for preceding year. These

cost belong to the particular year can be misleading if the same accounted for future

year (Acharya and Ryan 2016).

Interest bearing liabilities – it refers to the debt on which the entity is to pay interest

even when the amount is raised for short term period.

Deferred tax liabilities – it represents the future payment of tax that is expected by an

entity to pay towards proper tax authorities in future period and is computed as

applicable tax rate times of the entity for the difference among taxable income and

accounting income.

Investment contract liabilities – it consists the claims incurred during the year reduced

by equivalent elimination of the liability of policyholder that is reported originally under

balance sheet and investment return is credited to the policyholder (Koch-Medina,

Moreno-Bromberg, and Munari 2015).

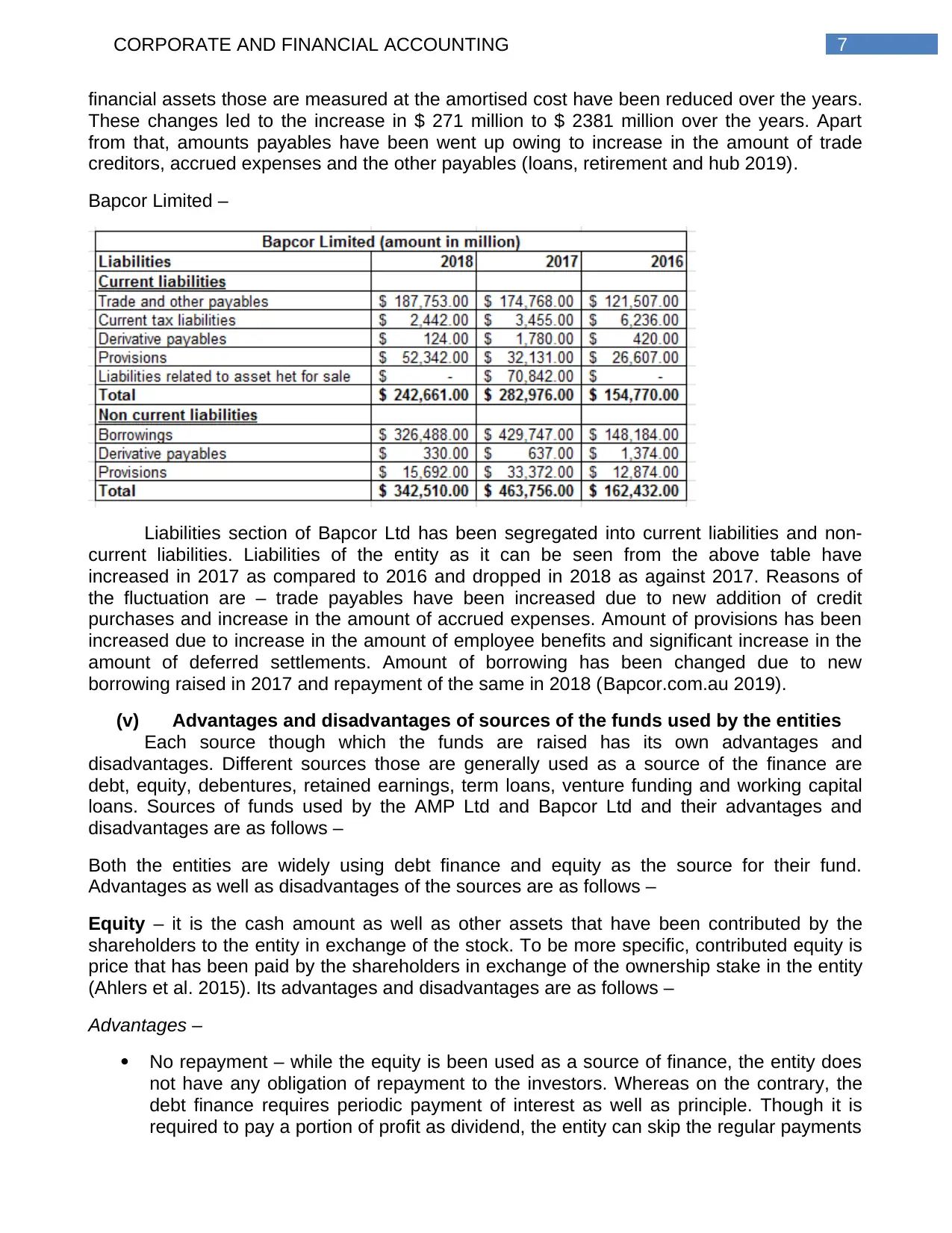

Bapcor Limited –

Derivative payables – it represents sum of counterparty’s contracts and reported as the

liability.

Provisions – as explained for AMP Limited

Liabilities related to the assets held for sale – these are the assets which are held to be

realised through the sale and is not expected to be used on continuous basis.

Borrowings – raising fund from bank or financial institution is termed as borrowing and

the money is lent in exchange of interest. On the basis of perceived risks, lender

associates with money lending (Bapcor.com.au 2019)

(iv) Movement of the items reported under owner’s equity

AMP Limited –

From above table and going through the financial analysis it can be stated that

financial assets those are measured at the fair values has been reduced. Further, the

Employee benefits – this is the liability on account of the benefits offered to the

employees apart from salaries. Generally the benefits include disability, medical and

retirement benefits.

Provisions – it is the amount that is kept aside for covering up future liability. Purpose

of the provision is making balance of current year more accurate as it is expected that

there can be costs that can be accounted for present year or for preceding year. These

cost belong to the particular year can be misleading if the same accounted for future

year (Acharya and Ryan 2016).

Interest bearing liabilities – it refers to the debt on which the entity is to pay interest

even when the amount is raised for short term period.

Deferred tax liabilities – it represents the future payment of tax that is expected by an

entity to pay towards proper tax authorities in future period and is computed as

applicable tax rate times of the entity for the difference among taxable income and

accounting income.

Investment contract liabilities – it consists the claims incurred during the year reduced

by equivalent elimination of the liability of policyholder that is reported originally under

balance sheet and investment return is credited to the policyholder (Koch-Medina,

Moreno-Bromberg, and Munari 2015).

Bapcor Limited –

Derivative payables – it represents sum of counterparty’s contracts and reported as the

liability.

Provisions – as explained for AMP Limited

Liabilities related to the assets held for sale – these are the assets which are held to be

realised through the sale and is not expected to be used on continuous basis.

Borrowings – raising fund from bank or financial institution is termed as borrowing and

the money is lent in exchange of interest. On the basis of perceived risks, lender

associates with money lending (Bapcor.com.au 2019)

(iv) Movement of the items reported under owner’s equity

AMP Limited –

From above table and going through the financial analysis it can be stated that

financial assets those are measured at the fair values has been reduced. Further, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

financial assets those are measured at the amortised cost have been reduced over the years.

These changes led to the increase in $ 271 million to $ 2381 million over the years. Apart

from that, amounts payables have been went up owing to increase in the amount of trade

creditors, accrued expenses and the other payables (loans, retirement and hub 2019).

Bapcor Limited –

Liabilities section of Bapcor Ltd has been segregated into current liabilities and non-

current liabilities. Liabilities of the entity as it can be seen from the above table have

increased in 2017 as compared to 2016 and dropped in 2018 as against 2017. Reasons of

the fluctuation are – trade payables have been increased due to new addition of credit

purchases and increase in the amount of accrued expenses. Amount of provisions has been

increased due to increase in the amount of employee benefits and significant increase in the

amount of deferred settlements. Amount of borrowing has been changed due to new

borrowing raised in 2017 and repayment of the same in 2018 (Bapcor.com.au 2019).

(v) Advantages and disadvantages of sources of the funds used by the entities

Each source though which the funds are raised has its own advantages and

disadvantages. Different sources those are generally used as a source of the finance are

debt, equity, debentures, retained earnings, term loans, venture funding and working capital

loans. Sources of funds used by the AMP Ltd and Bapcor Ltd and their advantages and

disadvantages are as follows –

Both the entities are widely using debt finance and equity as the source for their fund.

Advantages as well as disadvantages of the sources are as follows –

Equity – it is the cash amount as well as other assets that have been contributed by the

shareholders to the entity in exchange of the stock. To be more specific, contributed equity is

price that has been paid by the shareholders in exchange of the ownership stake in the entity

(Ahlers et al. 2015). Its advantages and disadvantages are as follows –

Advantages –

No repayment – while the equity is been used as a source of finance, the entity does

not have any obligation of repayment to the investors. Whereas on the contrary, the

debt finance requires periodic payment of interest as well as principle. Though it is

required to pay a portion of profit as dividend, the entity can skip the regular payments

financial assets those are measured at the amortised cost have been reduced over the years.

These changes led to the increase in $ 271 million to $ 2381 million over the years. Apart

from that, amounts payables have been went up owing to increase in the amount of trade

creditors, accrued expenses and the other payables (loans, retirement and hub 2019).

Bapcor Limited –

Liabilities section of Bapcor Ltd has been segregated into current liabilities and non-

current liabilities. Liabilities of the entity as it can be seen from the above table have

increased in 2017 as compared to 2016 and dropped in 2018 as against 2017. Reasons of

the fluctuation are – trade payables have been increased due to new addition of credit

purchases and increase in the amount of accrued expenses. Amount of provisions has been

increased due to increase in the amount of employee benefits and significant increase in the

amount of deferred settlements. Amount of borrowing has been changed due to new

borrowing raised in 2017 and repayment of the same in 2018 (Bapcor.com.au 2019).

(v) Advantages and disadvantages of sources of the funds used by the entities

Each source though which the funds are raised has its own advantages and

disadvantages. Different sources those are generally used as a source of the finance are

debt, equity, debentures, retained earnings, term loans, venture funding and working capital

loans. Sources of funds used by the AMP Ltd and Bapcor Ltd and their advantages and

disadvantages are as follows –

Both the entities are widely using debt finance and equity as the source for their fund.

Advantages as well as disadvantages of the sources are as follows –

Equity – it is the cash amount as well as other assets that have been contributed by the

shareholders to the entity in exchange of the stock. To be more specific, contributed equity is

price that has been paid by the shareholders in exchange of the ownership stake in the entity

(Ahlers et al. 2015). Its advantages and disadvantages are as follows –

Advantages –

No repayment – while the equity is been used as a source of finance, the entity does

not have any obligation of repayment to the investors. Whereas on the contrary, the

debt finance requires periodic payment of interest as well as principle. Though it is

required to pay a portion of profit as dividend, the entity can skip the regular payments

8CORPORATE AND FINANCIAL ACCOUNTING

as in the case of debt finance. This assists the entity to use that money for any other

purpose (Nassr and Wehinger 2016)

Lower level of risk – generally the entity with higher level of equity and lower level of

debt is considered to be lower leveraged. In case the business suffers setback and is

not able to make payments for interest, creditors may force it to liquidate. However, in

case of equity the investors do not have any such right and they must wait for the

business to earn profit in order to get returns.

Bringing equity partners – while money is the definite advantage of funding through

new equity, partners with who works are carried out has vested interest for the

success of the entity. If partners are well experienced and have good influence and

connections, it will make difference among thriving or struggling business. Apart from

that engagement of good partners can eliminate the disadvantages associated with

debt finance (Schwienbacher, Baker and Welter 2015).

Disadvantages –

Dilution of ownership – one of the major disadvantages of equity finance is loss of

ownership of the entity as with more shareholders ownership of existing shareholders

is diluted.

Higher cost – though the equity finance does not require any interest payment, its

overall cost is higher than the debt capital. Further, the stockholder feel that they shall

shoulder higher risk from their aspect as compared to the creditors as they are in the

bottom line for getting payment in case the entity liquidates. Hence, they are provided

more stock with lower price to compensate the risk (Hasan, Hossain and Habib 2015).

Debt capital or borrowing – it signifies the money raised by the entity through issuing

debentures, selling bonds and borrowing from banks or financial institutions. In exchange of

the money lent, the lender receives promise for getting repayment of the amount along with

interest.

Advantages –

Ownership – borrowing fund from the bank or financial institution is simplest way of

raising fund. Unlike the equity issue, debt finance does not offer any ownership on the

entity and hence the ownership of existing shareholders remains same.

Tax deductions – major advantage of debt finance is the interest paid on the

borrowings are deductible under tax unlike the equity finance where the dividend

payment is not deductible under tax.

Option of lower interest – with good credit rating score, the entity can raise money at

lower rate of interest (Khmel and Zhao 2016).

Disadvantages –

Long-term commitment – borrowing bring long term commitment as compared to

investment made by the investment. In case of equity finance the investors are

required to make payment only after the business earns profit. However, in case of

debt finance payment for interest and repayments of principle amount has to be made

on periodic basis irrespective of whether the entity has surplus earnings or not.

Credit ratings – generally the entity with higher level of debt and lower level of equity is

considered to be higher leveraged and it has direct impact on its credit rating. The

as in the case of debt finance. This assists the entity to use that money for any other

purpose (Nassr and Wehinger 2016)

Lower level of risk – generally the entity with higher level of equity and lower level of

debt is considered to be lower leveraged. In case the business suffers setback and is

not able to make payments for interest, creditors may force it to liquidate. However, in

case of equity the investors do not have any such right and they must wait for the

business to earn profit in order to get returns.

Bringing equity partners – while money is the definite advantage of funding through

new equity, partners with who works are carried out has vested interest for the

success of the entity. If partners are well experienced and have good influence and

connections, it will make difference among thriving or struggling business. Apart from

that engagement of good partners can eliminate the disadvantages associated with

debt finance (Schwienbacher, Baker and Welter 2015).

Disadvantages –

Dilution of ownership – one of the major disadvantages of equity finance is loss of

ownership of the entity as with more shareholders ownership of existing shareholders

is diluted.

Higher cost – though the equity finance does not require any interest payment, its

overall cost is higher than the debt capital. Further, the stockholder feel that they shall

shoulder higher risk from their aspect as compared to the creditors as they are in the

bottom line for getting payment in case the entity liquidates. Hence, they are provided

more stock with lower price to compensate the risk (Hasan, Hossain and Habib 2015).

Debt capital or borrowing – it signifies the money raised by the entity through issuing

debentures, selling bonds and borrowing from banks or financial institutions. In exchange of

the money lent, the lender receives promise for getting repayment of the amount along with

interest.

Advantages –

Ownership – borrowing fund from the bank or financial institution is simplest way of

raising fund. Unlike the equity issue, debt finance does not offer any ownership on the

entity and hence the ownership of existing shareholders remains same.

Tax deductions – major advantage of debt finance is the interest paid on the

borrowings are deductible under tax unlike the equity finance where the dividend

payment is not deductible under tax.

Option of lower interest – with good credit rating score, the entity can raise money at

lower rate of interest (Khmel and Zhao 2016).

Disadvantages –

Long-term commitment – borrowing bring long term commitment as compared to

investment made by the investment. In case of equity finance the investors are

required to make payment only after the business earns profit. However, in case of

debt finance payment for interest and repayments of principle amount has to be made

on periodic basis irrespective of whether the entity has surplus earnings or not.

Credit ratings – generally the entity with higher level of debt and lower level of equity is

considered to be higher leveraged and it has direct impact on its credit rating. The

9CORPORATE AND FINANCIAL ACCOUNTING

entity with bad credit rating face issues while applies for funding through borrowing

(Barakat 2014).

entity with bad credit rating face issues while applies for funding through borrowing

(Barakat 2014).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE AND FINANCIAL ACCOUNTING

Part B

Small proprietary company – any proprietary concern will be considered as the small

proprietary company for any financial year if the entity fulfils at least 2 of below mentioned

criteria –

Consolidated gross revenue from operation for the concerned financial year for the

entity along with the entities controlled by it is below $ 10 million.

Amount of the consolidated gross assets at the closing of concerned financial year for

the entity along with the entities controlled by it is below $ 5 million.

At the closing of concerned financial year the entity along with the entities controlled by

it has less than 50 employees (Asic.gov.au 2019).

Reporting requirements – Small proprietary entity does not have any obligations for financial

reporting or accounting except below –

It has been directed to prepare the same as per sec 294 that is ASIC direction or as

per section 209 that is shareholder direction.

The entity is controlled by any foreign entity that is the subsidiary of the entity is registered

outside the jurisdiction of Australia and is not consolidated into the accounts those are lodged

with the ASIC by the foreign registered entity (Asic.gov.au 2019)

Large proprietary company – any proprietary concern will be considered as the large

proprietary entity for any financial year if the entity satisfies at least 2 of below mentioned

criteria –

Consolidated gross revenue from operation for the concerned financial year for the

entity along with the entities controlled by it is below $ 10 million.

Amount of the gross consolidated assets at the closing of concerned financial year for

the entity along with the entities controlled by it is below $ 5 million.

At the closing of concerned financial year the entity along with the entities controlled by

it has less than 50 employees (Asic.gov.au 2019).

Reporting requirements – Large entities shall prepare their financial report in accordance with

the requirement of Corporation Act 2001, Chapter 2M. Further, it must appoint auditors to

audit the financial reports unless it meets the requirements of ASIC Corporation (audit relief)

Instruments 2016/784. Further, the financial statements shall be filed with ASIC along with

sending to the members of the entity within 4 months of the financial year closing (Asic.gov.au

2019).

Reporting entity – it is the entity where it is rational for expecting that users are there who

are dependent on the GPFR (general purpose financial report) for gaining understanding of

financial performance as well as financial position and taking decisions on the basis of the

financial information and other associated information incorporated in the financial report. The

users here can be members, shareholders, creditors, employees, potential investors and

lenders.

Part B

Small proprietary company – any proprietary concern will be considered as the small

proprietary company for any financial year if the entity fulfils at least 2 of below mentioned

criteria –

Consolidated gross revenue from operation for the concerned financial year for the

entity along with the entities controlled by it is below $ 10 million.

Amount of the consolidated gross assets at the closing of concerned financial year for

the entity along with the entities controlled by it is below $ 5 million.

At the closing of concerned financial year the entity along with the entities controlled by

it has less than 50 employees (Asic.gov.au 2019).

Reporting requirements – Small proprietary entity does not have any obligations for financial

reporting or accounting except below –

It has been directed to prepare the same as per sec 294 that is ASIC direction or as

per section 209 that is shareholder direction.

The entity is controlled by any foreign entity that is the subsidiary of the entity is registered

outside the jurisdiction of Australia and is not consolidated into the accounts those are lodged

with the ASIC by the foreign registered entity (Asic.gov.au 2019)

Large proprietary company – any proprietary concern will be considered as the large

proprietary entity for any financial year if the entity satisfies at least 2 of below mentioned

criteria –

Consolidated gross revenue from operation for the concerned financial year for the

entity along with the entities controlled by it is below $ 10 million.

Amount of the gross consolidated assets at the closing of concerned financial year for

the entity along with the entities controlled by it is below $ 5 million.

At the closing of concerned financial year the entity along with the entities controlled by

it has less than 50 employees (Asic.gov.au 2019).

Reporting requirements – Large entities shall prepare their financial report in accordance with

the requirement of Corporation Act 2001, Chapter 2M. Further, it must appoint auditors to

audit the financial reports unless it meets the requirements of ASIC Corporation (audit relief)

Instruments 2016/784. Further, the financial statements shall be filed with ASIC along with

sending to the members of the entity within 4 months of the financial year closing (Asic.gov.au

2019).

Reporting entity – it is the entity where it is rational for expecting that users are there who

are dependent on the GPFR (general purpose financial report) for gaining understanding of

financial performance as well as financial position and taking decisions on the basis of the

financial information and other associated information incorporated in the financial report. The

users here can be members, shareholders, creditors, employees, potential investors and

lenders.

11CORPORATE AND FINANCIAL ACCOUNTING

Reporting requirement – these entities are required to prepare the GPFR as per the

requirement of statement of accounting standards and accounting concepts (Asic.gov.au

2019).

Conclusion

From above it is concluded that AMP limited that is included in the financial service

industry and Bapcor Ltd that is included in the retail industry, both are using debt capital and

equity capital as the major source of finance. Further, the equity section mainly includes share

capital, reserves and retained earnings whereas the liability section majorly includes items

like payables, tax payable, provisions and derivative payable.

Reporting requirement – these entities are required to prepare the GPFR as per the

requirement of statement of accounting standards and accounting concepts (Asic.gov.au

2019).

Conclusion

From above it is concluded that AMP limited that is included in the financial service

industry and Bapcor Ltd that is included in the retail industry, both are using debt capital and

equity capital as the major source of finance. Further, the equity section mainly includes share

capital, reserves and retained earnings whereas the liability section majorly includes items

like payables, tax payable, provisions and derivative payable.

12CORPORATE AND FINANCIAL ACCOUNTING

Reference

Acharya, V.V. and Ryan, S.G., 2016. Banks’ financial reporting and financial system

stability. Journal of Accounting Research, 54(2), pp.277-340.

Ahlers, G.K., Cumming, D., Günther, C. and Schweizer, D., 2015. Signaling in equity

crowdfunding. Entrepreneurship theory and practice, 39(4), pp.955-980.

Ang, A., Chen, B., Goetzmann, W.N. and Phalippou, L., 2018. Estimating private equity

returns from limited partner cash flows. The Journal of Finance, 73(4), pp.1751-1783.

Asic.gov.au. 2019. Are you a large or small proprietary company | ASIC - Australian

Securities and Investments Commission . [online] Available at: https://asic.gov.au/regulatory-

resources/financial-reporting-and-audit/preparers-of-financial-reports/are-you-a-large-or-

small-proprietary-company/ [Accessed 25 Sep. 2019].

Asic.gov.au. 2019. Lodgement of financial reports | ASIC - Australian Securities and

Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/lodgement-of-financial-reports/ [Accessed 25 Sep. 2019].

Bapcor.com.au. 2019. Bapcor - Aftermarket Auto Parts, Accessories, Service. [online]

Available at: https://www.bapcor.com.au/ [Accessed 25 Sep. 2019].

Barakat, A., 2014. The impact of financial structure, financial leverage and profitability on

industrial companies shares value (applied study on a sample of Saudi industrial

companies). Research Journal of Finance and Accounting, 5(1), pp.55-66.

Bernstein, S., Lerner, J., Sorensen, M. and Strömberg, P., 2016. Private equity and industry

performance. Management Science, 63(4), pp.1198-1213.

Capponi, A., Chen, P.C. and Yao, D.D., 2015. Liability concentration and systemic losses in

financial networks. Operations Research, 64(5), pp.1121-1134.

Goldstein, I., Jiang, H. and Ng, D.T., 2017. Investor flows and fragility in corporate bond

funds. Journal of Financial Economics, 126(3), pp.592-613.

Hasan, M.M., Hossain, M. and Habib, A., 2015. Corporate life cycle and cost of equity

capital. Journal of Contemporary Accounting & Economics, 11(1), pp.46-60.

Khmel, V. and Zhao, S., 2016. Arrangement of financing for highway infrastructure projects

under the conditions of Public–Private Partnership. IAtSS Research, 39(2), pp.138-145.

Koch-Medina, P., Moreno-Bromberg, S. and Munari, C., 2015. Capital adequacy tests and

limited liability of financial institutions. Journal of Banking & Finance, 51, pp.93-102.

loans, H., retirement, S. and hub, F. 2019. AMP Personal Banking - Accounts, Super, Home

Loans & Insurance | AMP. [online] Amp.com.au. Available at: https://www.amp.com.au/

[Accessed 25 Sep. 2019].

Nassr, I.K. and Wehinger, G., 2016. Opportunities and limitations of public equity markets for

SMEs. OECD Journal: Financial Market Trends, 2015(1), pp.49-84.

Reference

Acharya, V.V. and Ryan, S.G., 2016. Banks’ financial reporting and financial system

stability. Journal of Accounting Research, 54(2), pp.277-340.

Ahlers, G.K., Cumming, D., Günther, C. and Schweizer, D., 2015. Signaling in equity

crowdfunding. Entrepreneurship theory and practice, 39(4), pp.955-980.

Ang, A., Chen, B., Goetzmann, W.N. and Phalippou, L., 2018. Estimating private equity

returns from limited partner cash flows. The Journal of Finance, 73(4), pp.1751-1783.

Asic.gov.au. 2019. Are you a large or small proprietary company | ASIC - Australian

Securities and Investments Commission . [online] Available at: https://asic.gov.au/regulatory-

resources/financial-reporting-and-audit/preparers-of-financial-reports/are-you-a-large-or-

small-proprietary-company/ [Accessed 25 Sep. 2019].

Asic.gov.au. 2019. Lodgement of financial reports | ASIC - Australian Securities and

Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/lodgement-of-financial-reports/ [Accessed 25 Sep. 2019].

Bapcor.com.au. 2019. Bapcor - Aftermarket Auto Parts, Accessories, Service. [online]

Available at: https://www.bapcor.com.au/ [Accessed 25 Sep. 2019].

Barakat, A., 2014. The impact of financial structure, financial leverage and profitability on

industrial companies shares value (applied study on a sample of Saudi industrial

companies). Research Journal of Finance and Accounting, 5(1), pp.55-66.

Bernstein, S., Lerner, J., Sorensen, M. and Strömberg, P., 2016. Private equity and industry

performance. Management Science, 63(4), pp.1198-1213.

Capponi, A., Chen, P.C. and Yao, D.D., 2015. Liability concentration and systemic losses in

financial networks. Operations Research, 64(5), pp.1121-1134.

Goldstein, I., Jiang, H. and Ng, D.T., 2017. Investor flows and fragility in corporate bond

funds. Journal of Financial Economics, 126(3), pp.592-613.

Hasan, M.M., Hossain, M. and Habib, A., 2015. Corporate life cycle and cost of equity

capital. Journal of Contemporary Accounting & Economics, 11(1), pp.46-60.

Khmel, V. and Zhao, S., 2016. Arrangement of financing for highway infrastructure projects

under the conditions of Public–Private Partnership. IAtSS Research, 39(2), pp.138-145.

Koch-Medina, P., Moreno-Bromberg, S. and Munari, C., 2015. Capital adequacy tests and

limited liability of financial institutions. Journal of Banking & Finance, 51, pp.93-102.

loans, H., retirement, S. and hub, F. 2019. AMP Personal Banking - Accounts, Super, Home

Loans & Insurance | AMP. [online] Amp.com.au. Available at: https://www.amp.com.au/

[Accessed 25 Sep. 2019].

Nassr, I.K. and Wehinger, G., 2016. Opportunities and limitations of public equity markets for

SMEs. OECD Journal: Financial Market Trends, 2015(1), pp.49-84.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CORPORATE AND FINANCIAL ACCOUNTING

Schwienbacher, A., Baker, T. and Welter, F., 2015. Financing the business. The Routledge

companion to entrepreneurship, pp.193-206.

Schwienbacher, A., Baker, T. and Welter, F., 2015. Financing the business. The Routledge

companion to entrepreneurship, pp.193-206.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.