HA2032 Corporate and Financial Accounting Report 2022

VerifiedAdded on 2022/09/29

|15

|4085

|21

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HA2032

Corporate and Financial Accounting

1

Corporate and Financial Accounting

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract

This report aim to review the sources of finances used Wesfarmers and Woolworth

during the last three years and make comparison on use of these sources by each company. It has

been evaluated that both the selected companies make use of equity as well as debt sources of

finance depending upon the requirement and to manage the capital funds needed. This report will

also evaluate classification of entities on the basis on small proprietary company, large

proprietary company and entities that are regarded as reporting entities.

2

This report aim to review the sources of finances used Wesfarmers and Woolworth

during the last three years and make comparison on use of these sources by each company. It has

been evaluated that both the selected companies make use of equity as well as debt sources of

finance depending upon the requirement and to manage the capital funds needed. This report will

also evaluate classification of entities on the basis on small proprietary company, large

proprietary company and entities that are regarded as reporting entities.

2

Contents

Abstract............................................................................................................................................2

Introduction......................................................................................................................................4

Part A: Use of different sources of finance for raising the funds....................................................4

A (i): Items recorded under owner’s equity section of both the selected companies with

detailed explanation of each of the item......................................................................................4

A (ii): Movement in each item of owner’s equity mentioned above during the period of three

years.............................................................................................................................................5

A (iii): Items of liabilities sections recorded by each of the selected company and

understanding of each item..........................................................................................................8

A. (IV): Movement in each of items recorded under each of items for both the selected

companies with reason.................................................................................................................9

A. (V): Advantages and disadvantages of each of sources of finance used by the selected

companies...................................................................................................................................10

Part B: Critical examination of the concepts of small proprietary company, large proprietary

company and reporting entity........................................................................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

3

Abstract............................................................................................................................................2

Introduction......................................................................................................................................4

Part A: Use of different sources of finance for raising the funds....................................................4

A (i): Items recorded under owner’s equity section of both the selected companies with

detailed explanation of each of the item......................................................................................4

A (ii): Movement in each item of owner’s equity mentioned above during the period of three

years.............................................................................................................................................5

A (iii): Items of liabilities sections recorded by each of the selected company and

understanding of each item..........................................................................................................8

A. (IV): Movement in each of items recorded under each of items for both the selected

companies with reason.................................................................................................................9

A. (V): Advantages and disadvantages of each of sources of finance used by the selected

companies...................................................................................................................................10

Part B: Critical examination of the concepts of small proprietary company, large proprietary

company and reporting entity........................................................................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

3

Introduction

The purpose of this report is to evaluate the different sources of funds used by company

to make available funds to finance the assets. In addition to this, report will evaluate purpose of

classification of entities for reporting purposes. Sources of funds has been classified into two

board categories, they are internal sources of finance and external sources of finance. Internal

sources of finance are generated internally and there is no need to pay any additional charge or

dividend to make available such funds. Retained earnings are only source fund that can be

internally generated. Newly established organization cannot make use of retained earnings due to

non availability of profits during start up phase. On the other hand, external sources can be

obtained from various sources such as banks, financial institutions, and issue of ordinary shares,

preferences shares, bonds, debentures, venture capital, and many other sources. External sources

of funds can be classified as equity sources and debt sources depending upon the charge each

source bear with them. Examples of equity sources are ordinary capital, preference capital, and

retained earnings. On other hand, examples of debt sources of finance includes borrowing from

banks, debentures, venture capital, loans from financial institutions, and many more.

Two ASX companies selected to understand the use of sources of funds are Wesfarmers

and Woolworth. Annual reports of year 2016, 2017 and 2018 have been extracted for both

companies from their respective websites.

Part A: Use of different sources of finance for raising the funds

A (i): Items recorded under owner’s equity section of both the selected companies with

detailed explanation of each of the item

Owner’s equity refers to source of funds contributed by the owner’s of company ie

shareholders of such company. This source of funds is prominent and does not bear any fixed

charge. As discussed earlier, some of important items of owner’s equity are ordinary capital,

retained earnings and reserves.

Owner’s equity items presented in balance sheet of Wesfarmers Group:

Issued capital

Retained Earnings

Reserves

(Wesfarmers: Annual Report, 2017 and Wesfarmers: Annual Report, 2018)

Owner’s equity items presented in balance sheet of Woolworth Group

Contributed Equity

Reserves

4

The purpose of this report is to evaluate the different sources of funds used by company

to make available funds to finance the assets. In addition to this, report will evaluate purpose of

classification of entities for reporting purposes. Sources of funds has been classified into two

board categories, they are internal sources of finance and external sources of finance. Internal

sources of finance are generated internally and there is no need to pay any additional charge or

dividend to make available such funds. Retained earnings are only source fund that can be

internally generated. Newly established organization cannot make use of retained earnings due to

non availability of profits during start up phase. On the other hand, external sources can be

obtained from various sources such as banks, financial institutions, and issue of ordinary shares,

preferences shares, bonds, debentures, venture capital, and many other sources. External sources

of funds can be classified as equity sources and debt sources depending upon the charge each

source bear with them. Examples of equity sources are ordinary capital, preference capital, and

retained earnings. On other hand, examples of debt sources of finance includes borrowing from

banks, debentures, venture capital, loans from financial institutions, and many more.

Two ASX companies selected to understand the use of sources of funds are Wesfarmers

and Woolworth. Annual reports of year 2016, 2017 and 2018 have been extracted for both

companies from their respective websites.

Part A: Use of different sources of finance for raising the funds

A (i): Items recorded under owner’s equity section of both the selected companies with

detailed explanation of each of the item

Owner’s equity refers to source of funds contributed by the owner’s of company ie

shareholders of such company. This source of funds is prominent and does not bear any fixed

charge. As discussed earlier, some of important items of owner’s equity are ordinary capital,

retained earnings and reserves.

Owner’s equity items presented in balance sheet of Wesfarmers Group:

Issued capital

Retained Earnings

Reserves

(Wesfarmers: Annual Report, 2017 and Wesfarmers: Annual Report, 2018)

Owner’s equity items presented in balance sheet of Woolworth Group

Contributed Equity

Reserves

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Retained Earnings

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

Explanation of each of owner’s equity items

Issued Capital/Contributed equity: Issued capital is also referred as ordinary share

capital as it contributed shareholder’s of the company. Listed companies have authority

to issue their shares in market and subscribed by common people. In financial tem issued

capital refers to amount received on number of shares issued and allocated to

shareholders of the company. It is part of authorized capital that has been allowed to be

issued in market to raise the funds. According to the requirement of raising the funds,

company makes issue of ordinary shares and allocates shares to shareholders. These

shares can either be issue at premium, par or discount depending upon the market

position of the company.

Retained Earnings: Retained earnings is part of profit left after meeting all the expenses

during each period. It can be regarded as earnings left after paying the dividend to

shareholders. Value of retained earnings depends upon the profit margin and dividend

policies of respective company. Retained earnings are regarded as free funds as they are

not entitled to be used for specific purpose.

Reserves: It is also referred as part of retained earnings but they are set aside for some

specific purpose unlike in case of retained earnings. Reserves are regarded as part of

profit set aside to pay the liabilities expected to arise in future.

A (ii): Movement in each item of owner’s equity mentioned above during the period of

three years

Movement in items of owner’s equity can be reviewed from the statement of changes in

equity presented as part of financial statement in annual reports of each company.

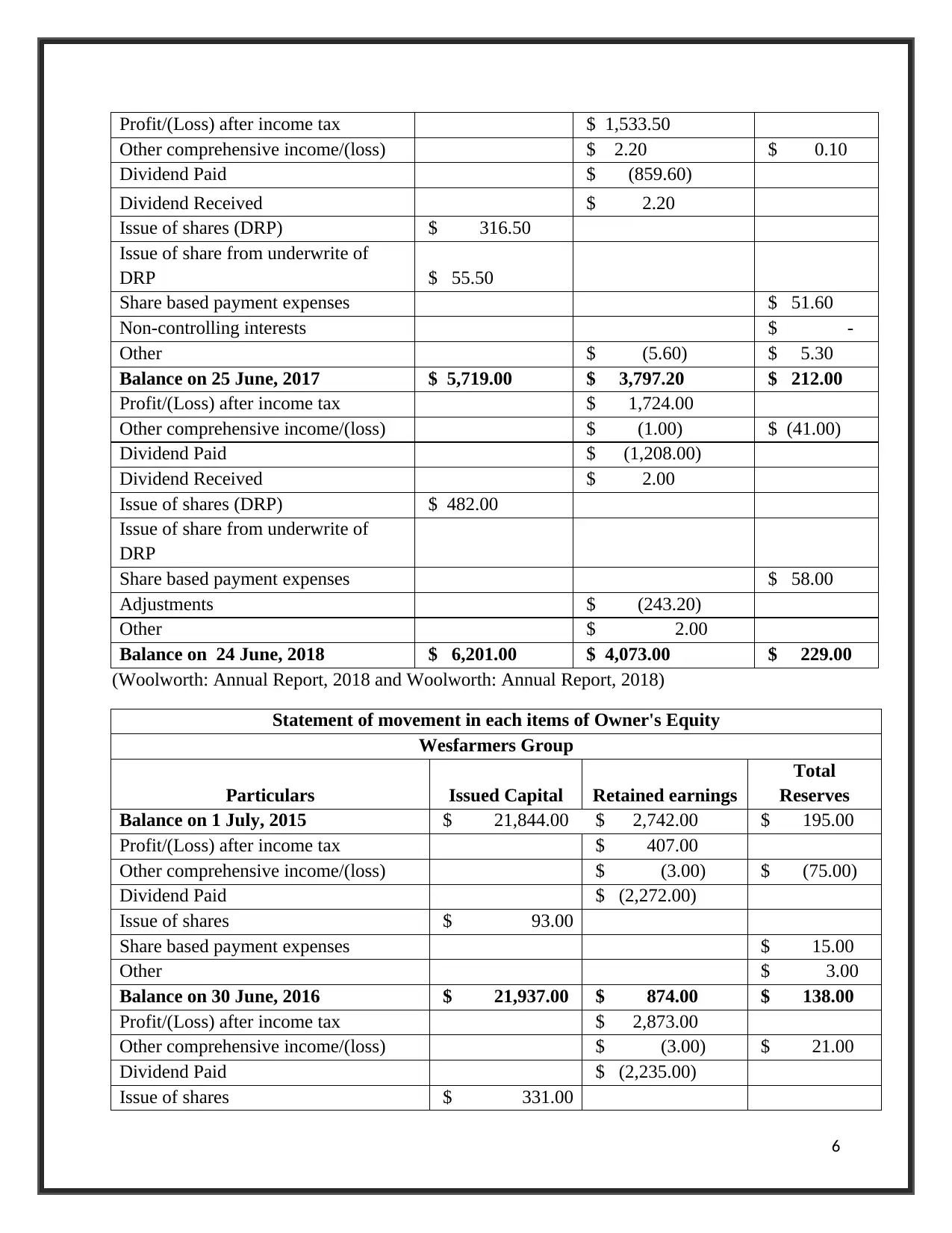

Statement of movement in each items of Owner's Equity

Woolworth Group

Particulars

Contributed

Equity Retained earnings Reserves

Balance on 26 June, 2015 $ 5,064.90 $ 5,830.10 $ 95.10

Profit/(Loss) after income tax $ (1,234.80)

Other comprehensive income/(loss) $ (3.90) $ 192.50

Dividend Paid $ (1,471.20)

Dividend Received $ 4.30

Issue of shares (DRP) $ 282.10

Share based payment expenses $ 20.80

Non-controlling interests $ (153.40)

Balance on 26 June, 2016 $ 5,347.00 $ 3,124.50 $ 155.00

5

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

Explanation of each of owner’s equity items

Issued Capital/Contributed equity: Issued capital is also referred as ordinary share

capital as it contributed shareholder’s of the company. Listed companies have authority

to issue their shares in market and subscribed by common people. In financial tem issued

capital refers to amount received on number of shares issued and allocated to

shareholders of the company. It is part of authorized capital that has been allowed to be

issued in market to raise the funds. According to the requirement of raising the funds,

company makes issue of ordinary shares and allocates shares to shareholders. These

shares can either be issue at premium, par or discount depending upon the market

position of the company.

Retained Earnings: Retained earnings is part of profit left after meeting all the expenses

during each period. It can be regarded as earnings left after paying the dividend to

shareholders. Value of retained earnings depends upon the profit margin and dividend

policies of respective company. Retained earnings are regarded as free funds as they are

not entitled to be used for specific purpose.

Reserves: It is also referred as part of retained earnings but they are set aside for some

specific purpose unlike in case of retained earnings. Reserves are regarded as part of

profit set aside to pay the liabilities expected to arise in future.

A (ii): Movement in each item of owner’s equity mentioned above during the period of

three years

Movement in items of owner’s equity can be reviewed from the statement of changes in

equity presented as part of financial statement in annual reports of each company.

Statement of movement in each items of Owner's Equity

Woolworth Group

Particulars

Contributed

Equity Retained earnings Reserves

Balance on 26 June, 2015 $ 5,064.90 $ 5,830.10 $ 95.10

Profit/(Loss) after income tax $ (1,234.80)

Other comprehensive income/(loss) $ (3.90) $ 192.50

Dividend Paid $ (1,471.20)

Dividend Received $ 4.30

Issue of shares (DRP) $ 282.10

Share based payment expenses $ 20.80

Non-controlling interests $ (153.40)

Balance on 26 June, 2016 $ 5,347.00 $ 3,124.50 $ 155.00

5

Profit/(Loss) after income tax $ 1,533.50

Other comprehensive income/(loss) $ 2.20 $ 0.10

Dividend Paid $ (859.60)

Dividend Received $ 2.20

Issue of shares (DRP) $ 316.50

Issue of share from underwrite of

DRP $ 55.50

Share based payment expenses $ 51.60

Non-controlling interests $ -

Other $ (5.60) $ 5.30

Balance on 25 June, 2017 $ 5,719.00 $ 3,797.20 $ 212.00

Profit/(Loss) after income tax $ 1,724.00

Other comprehensive income/(loss) $ (1.00) $ (41.00)

Dividend Paid $ (1,208.00)

Dividend Received $ 2.00

Issue of shares (DRP) $ 482.00

Issue of share from underwrite of

DRP

Share based payment expenses $ 58.00

Adjustments $ (243.20)

Other $ 2.00

Balance on 24 June, 2018 $ 6,201.00 $ 4,073.00 $ 229.00

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

Statement of movement in each items of Owner's Equity

Wesfarmers Group

Particulars Issued Capital Retained earnings

Total

Reserves

Balance on 1 July, 2015 $ 21,844.00 $ 2,742.00 $ 195.00

Profit/(Loss) after income tax $ 407.00

Other comprehensive income/(loss) $ (3.00) $ (75.00)

Dividend Paid $ (2,272.00)

Issue of shares $ 93.00

Share based payment expenses $ 15.00

Other $ 3.00

Balance on 30 June, 2016 $ 21,937.00 $ 874.00 $ 138.00

Profit/(Loss) after income tax $ 2,873.00

Other comprehensive income/(loss) $ (3.00) $ 21.00

Dividend Paid $ (2,235.00)

Issue of shares $ 331.00

6

Other comprehensive income/(loss) $ 2.20 $ 0.10

Dividend Paid $ (859.60)

Dividend Received $ 2.20

Issue of shares (DRP) $ 316.50

Issue of share from underwrite of

DRP $ 55.50

Share based payment expenses $ 51.60

Non-controlling interests $ -

Other $ (5.60) $ 5.30

Balance on 25 June, 2017 $ 5,719.00 $ 3,797.20 $ 212.00

Profit/(Loss) after income tax $ 1,724.00

Other comprehensive income/(loss) $ (1.00) $ (41.00)

Dividend Paid $ (1,208.00)

Dividend Received $ 2.00

Issue of shares (DRP) $ 482.00

Issue of share from underwrite of

DRP

Share based payment expenses $ 58.00

Adjustments $ (243.20)

Other $ 2.00

Balance on 24 June, 2018 $ 6,201.00 $ 4,073.00 $ 229.00

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

Statement of movement in each items of Owner's Equity

Wesfarmers Group

Particulars Issued Capital Retained earnings

Total

Reserves

Balance on 1 July, 2015 $ 21,844.00 $ 2,742.00 $ 195.00

Profit/(Loss) after income tax $ 407.00

Other comprehensive income/(loss) $ (3.00) $ (75.00)

Dividend Paid $ (2,272.00)

Issue of shares $ 93.00

Share based payment expenses $ 15.00

Other $ 3.00

Balance on 30 June, 2016 $ 21,937.00 $ 874.00 $ 138.00

Profit/(Loss) after income tax $ 2,873.00

Other comprehensive income/(loss) $ (3.00) $ 21.00

Dividend Paid $ (2,235.00)

Issue of shares $ 331.00

6

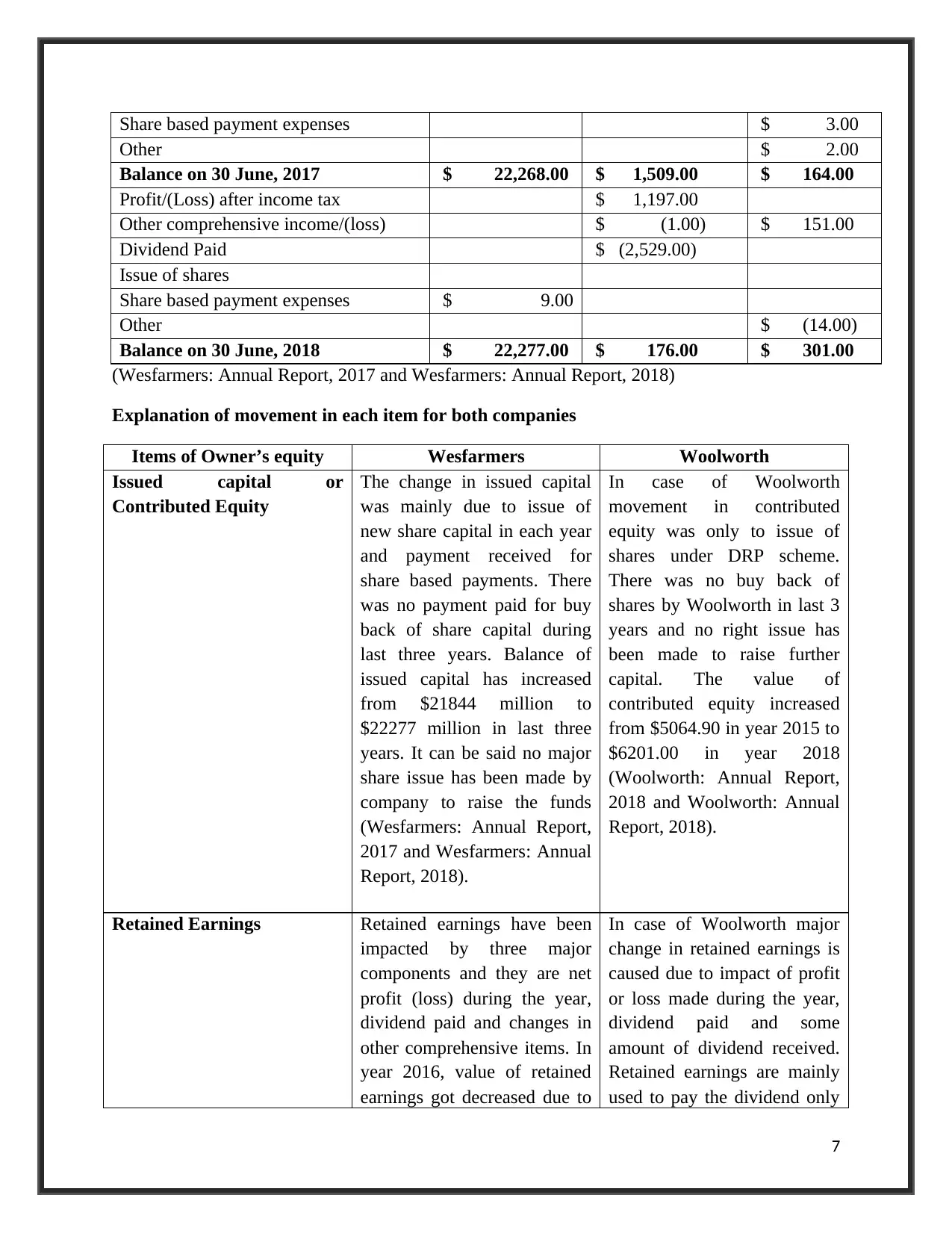

Share based payment expenses $ 3.00

Other $ 2.00

Balance on 30 June, 2017 $ 22,268.00 $ 1,509.00 $ 164.00

Profit/(Loss) after income tax $ 1,197.00

Other comprehensive income/(loss) $ (1.00) $ 151.00

Dividend Paid $ (2,529.00)

Issue of shares

Share based payment expenses $ 9.00

Other $ (14.00)

Balance on 30 June, 2018 $ 22,277.00 $ 176.00 $ 301.00

(Wesfarmers: Annual Report, 2017 and Wesfarmers: Annual Report, 2018)

Explanation of movement in each item for both companies

Items of Owner’s equity Wesfarmers Woolworth

Issued capital or

Contributed Equity

The change in issued capital

was mainly due to issue of

new share capital in each year

and payment received for

share based payments. There

was no payment paid for buy

back of share capital during

last three years. Balance of

issued capital has increased

from $21844 million to

$22277 million in last three

years. It can be said no major

share issue has been made by

company to raise the funds

(Wesfarmers: Annual Report,

2017 and Wesfarmers: Annual

Report, 2018).

In case of Woolworth

movement in contributed

equity was only to issue of

shares under DRP scheme.

There was no buy back of

shares by Woolworth in last 3

years and no right issue has

been made to raise further

capital. The value of

contributed equity increased

from $5064.90 in year 2015 to

$6201.00 in year 2018

(Woolworth: Annual Report,

2018 and Woolworth: Annual

Report, 2018).

Retained Earnings Retained earnings have been

impacted by three major

components and they are net

profit (loss) during the year,

dividend paid and changes in

other comprehensive items. In

year 2016, value of retained

earnings got decreased due to

In case of Woolworth major

change in retained earnings is

caused due to impact of profit

or loss made during the year,

dividend paid and some

amount of dividend received.

Retained earnings are mainly

used to pay the dividend only

7

Other $ 2.00

Balance on 30 June, 2017 $ 22,268.00 $ 1,509.00 $ 164.00

Profit/(Loss) after income tax $ 1,197.00

Other comprehensive income/(loss) $ (1.00) $ 151.00

Dividend Paid $ (2,529.00)

Issue of shares

Share based payment expenses $ 9.00

Other $ (14.00)

Balance on 30 June, 2018 $ 22,277.00 $ 176.00 $ 301.00

(Wesfarmers: Annual Report, 2017 and Wesfarmers: Annual Report, 2018)

Explanation of movement in each item for both companies

Items of Owner’s equity Wesfarmers Woolworth

Issued capital or

Contributed Equity

The change in issued capital

was mainly due to issue of

new share capital in each year

and payment received for

share based payments. There

was no payment paid for buy

back of share capital during

last three years. Balance of

issued capital has increased

from $21844 million to

$22277 million in last three

years. It can be said no major

share issue has been made by

company to raise the funds

(Wesfarmers: Annual Report,

2017 and Wesfarmers: Annual

Report, 2018).

In case of Woolworth

movement in contributed

equity was only to issue of

shares under DRP scheme.

There was no buy back of

shares by Woolworth in last 3

years and no right issue has

been made to raise further

capital. The value of

contributed equity increased

from $5064.90 in year 2015 to

$6201.00 in year 2018

(Woolworth: Annual Report,

2018 and Woolworth: Annual

Report, 2018).

Retained Earnings Retained earnings have been

impacted by three major

components and they are net

profit (loss) during the year,

dividend paid and changes in

other comprehensive items. In

year 2016, value of retained

earnings got decreased due to

In case of Woolworth major

change in retained earnings is

caused due to impact of profit

or loss made during the year,

dividend paid and some

amount of dividend received.

Retained earnings are mainly

used to pay the dividend only

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

lower net profit and higher

dividend paid during the year.

and there is no plan of

company to make use of

retained earnings in any other

payments.

Reserves Reserves are impacted only

due to the change in other

comprehensive income items,

share based payments. They

are specific in nature and used

only for payment of selected

liabilities.

The change in balance of

reserves is due to change in

values of other comprehensive

income items, non controlling

interest and share based

payments. All this reserve is

set aside to meet the

requirement of some specific

requirement that arises every

year (Gibson, 2011).

A (iii): Items of liabilities sections recorded by each of the selected company and

understanding of each item

In this section only those liabilities items have been considered are being used as sources

of funds. Items such as derivatives, trade payable, income tax payable and other items have been

ignored as they are part of working capital and completely depend on how company manages its

working capital.

Following items have been reported by Wesfarmers in liabilities section

Interest bearing loans and borrowings

1. Bank Loans

2. Capital market debt

Provisions

(Wesfarmers: Annual Report, 2017 and Wesfarmers: Annual Report, 2018)

Following items have been used by Woolworth as debt capital and shown under liabilities

section:

Borrowings

1. Bank loans

2. Securities

3. Finance leases

4. Notes payable

Provisions

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

8

dividend paid during the year.

and there is no plan of

company to make use of

retained earnings in any other

payments.

Reserves Reserves are impacted only

due to the change in other

comprehensive income items,

share based payments. They

are specific in nature and used

only for payment of selected

liabilities.

The change in balance of

reserves is due to change in

values of other comprehensive

income items, non controlling

interest and share based

payments. All this reserve is

set aside to meet the

requirement of some specific

requirement that arises every

year (Gibson, 2011).

A (iii): Items of liabilities sections recorded by each of the selected company and

understanding of each item

In this section only those liabilities items have been considered are being used as sources

of funds. Items such as derivatives, trade payable, income tax payable and other items have been

ignored as they are part of working capital and completely depend on how company manages its

working capital.

Following items have been reported by Wesfarmers in liabilities section

Interest bearing loans and borrowings

1. Bank Loans

2. Capital market debt

Provisions

(Wesfarmers: Annual Report, 2017 and Wesfarmers: Annual Report, 2018)

Following items have been used by Woolworth as debt capital and shown under liabilities

section:

Borrowings

1. Bank loans

2. Securities

3. Finance leases

4. Notes payable

Provisions

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

8

Explanation of each of items shown under liabilities

Bank loan: The amount of funds taken from financial institutions, banks or from any

lender that requires company to pay fixed charge (Interest expenses). Bank loans is

comparatively easy to use for raising funds as compared to equity funds but there is need

to bear interest expenses on amount of capital raised. This expense is fixed charge on

company and it has to paid whether there is profit or not during the respective year.

Capital market debt/Securities: Capital market represents instruments used to raise

funds through issuing them in open market. Examples of capital market debts are bonds,

debentures, leases, bills of exchange, etc. Financial instruments that are being brought

and sold in capital market are represented as capital market instruments and instruments

that create the financial obligation on entities are regarded as capital market debt.

Financial leases: It is type of financial instrument that requires lessee to pay defined

amount on each interval. Liabilities of finance lease are offset from the amount of right to

use assets shown in asset section of balance sheet. Entities make an arrangement of lease

to take over the required assets as there is no requirement to pay complete upfront cash at

the same times. Instead all such payments are deferred to series of lease payments

represented in form of liabilities (Baker and Powell, 2010).

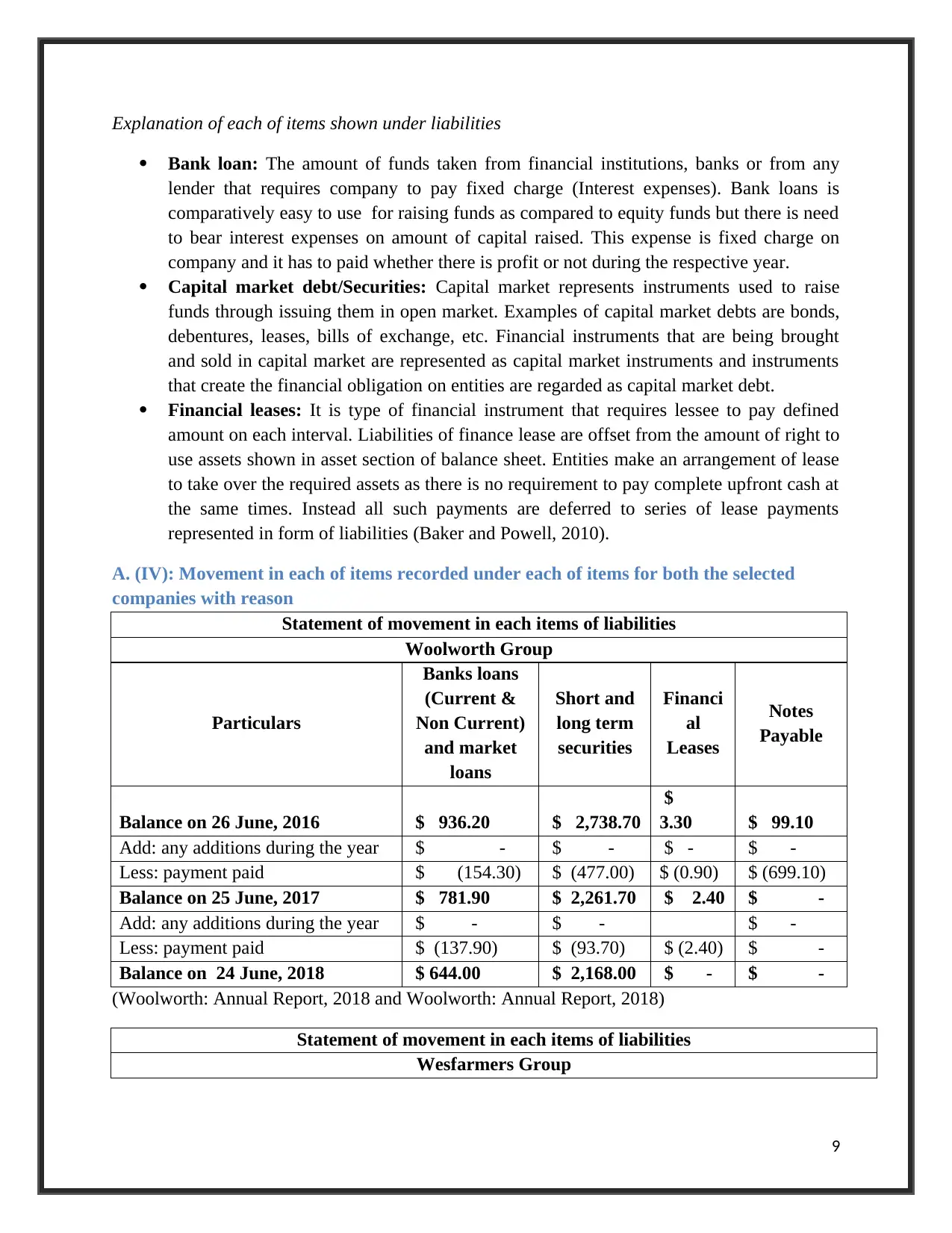

A. (IV): Movement in each of items recorded under each of items for both the selected

companies with reason

Statement of movement in each items of liabilities

Woolworth Group

Particulars

Banks loans

(Current &

Non Current)

and market

loans

Short and

long term

securities

Financi

al

Leases

Notes

Payable

Balance on 26 June, 2016 $ 936.20 $ 2,738.70

$

3.30 $ 99.10

Add: any additions during the year $ - $ - $ - $ -

Less: payment paid $ (154.30) $ (477.00) $ (0.90) $ (699.10)

Balance on 25 June, 2017 $ 781.90 $ 2,261.70 $ 2.40 $ -

Add: any additions during the year $ - $ - $ -

Less: payment paid $ (137.90) $ (93.70) $ (2.40) $ -

Balance on 24 June, 2018 $ 644.00 $ 2,168.00 $ - $ -

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

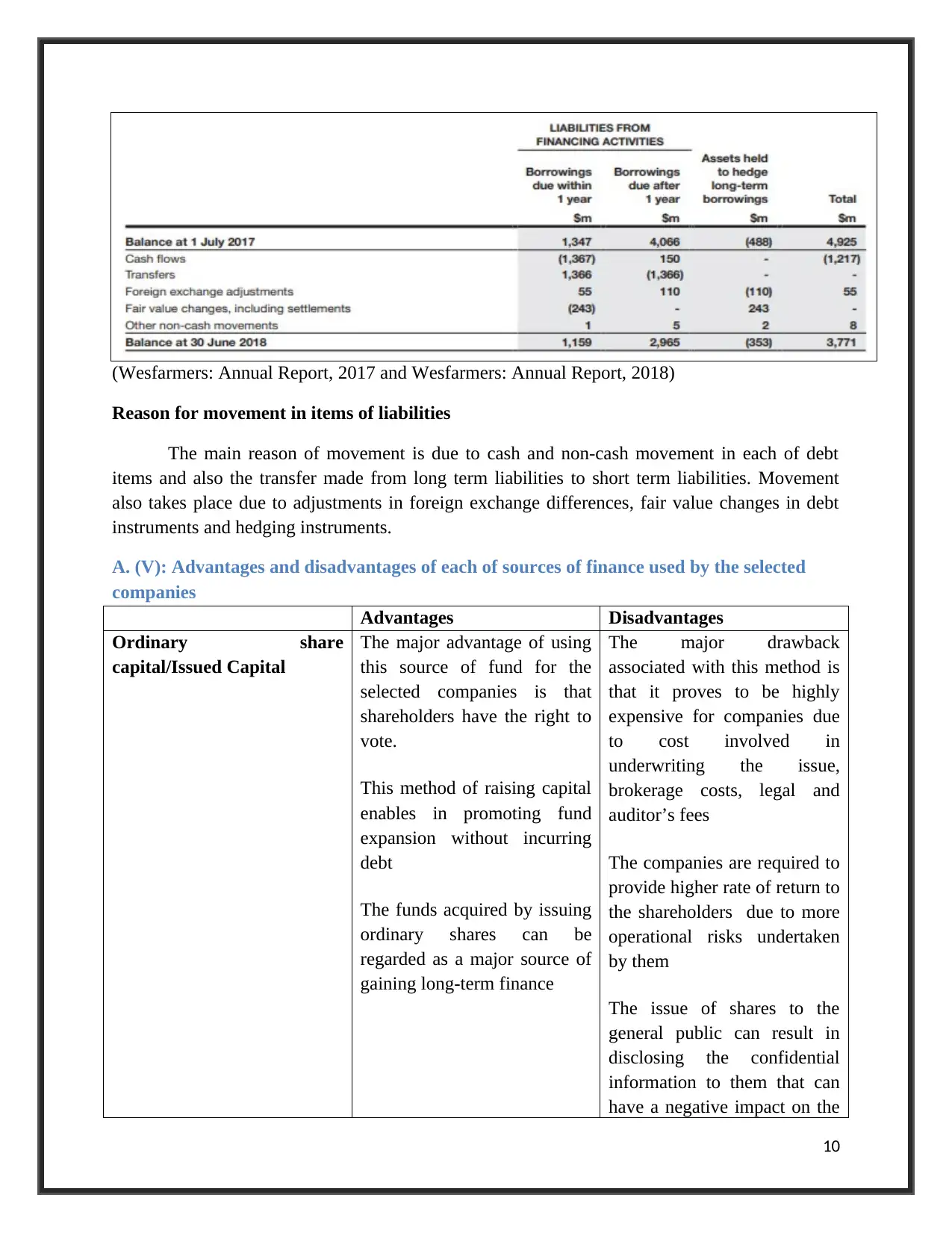

Statement of movement in each items of liabilities

Wesfarmers Group

9

Bank loan: The amount of funds taken from financial institutions, banks or from any

lender that requires company to pay fixed charge (Interest expenses). Bank loans is

comparatively easy to use for raising funds as compared to equity funds but there is need

to bear interest expenses on amount of capital raised. This expense is fixed charge on

company and it has to paid whether there is profit or not during the respective year.

Capital market debt/Securities: Capital market represents instruments used to raise

funds through issuing them in open market. Examples of capital market debts are bonds,

debentures, leases, bills of exchange, etc. Financial instruments that are being brought

and sold in capital market are represented as capital market instruments and instruments

that create the financial obligation on entities are regarded as capital market debt.

Financial leases: It is type of financial instrument that requires lessee to pay defined

amount on each interval. Liabilities of finance lease are offset from the amount of right to

use assets shown in asset section of balance sheet. Entities make an arrangement of lease

to take over the required assets as there is no requirement to pay complete upfront cash at

the same times. Instead all such payments are deferred to series of lease payments

represented in form of liabilities (Baker and Powell, 2010).

A. (IV): Movement in each of items recorded under each of items for both the selected

companies with reason

Statement of movement in each items of liabilities

Woolworth Group

Particulars

Banks loans

(Current &

Non Current)

and market

loans

Short and

long term

securities

Financi

al

Leases

Notes

Payable

Balance on 26 June, 2016 $ 936.20 $ 2,738.70

$

3.30 $ 99.10

Add: any additions during the year $ - $ - $ - $ -

Less: payment paid $ (154.30) $ (477.00) $ (0.90) $ (699.10)

Balance on 25 June, 2017 $ 781.90 $ 2,261.70 $ 2.40 $ -

Add: any additions during the year $ - $ - $ -

Less: payment paid $ (137.90) $ (93.70) $ (2.40) $ -

Balance on 24 June, 2018 $ 644.00 $ 2,168.00 $ - $ -

(Woolworth: Annual Report, 2018 and Woolworth: Annual Report, 2018)

Statement of movement in each items of liabilities

Wesfarmers Group

9

(Wesfarmers: Annual Report, 2017 and Wesfarmers: Annual Report, 2018)

Reason for movement in items of liabilities

The main reason of movement is due to cash and non-cash movement in each of debt

items and also the transfer made from long term liabilities to short term liabilities. Movement

also takes place due to adjustments in foreign exchange differences, fair value changes in debt

instruments and hedging instruments.

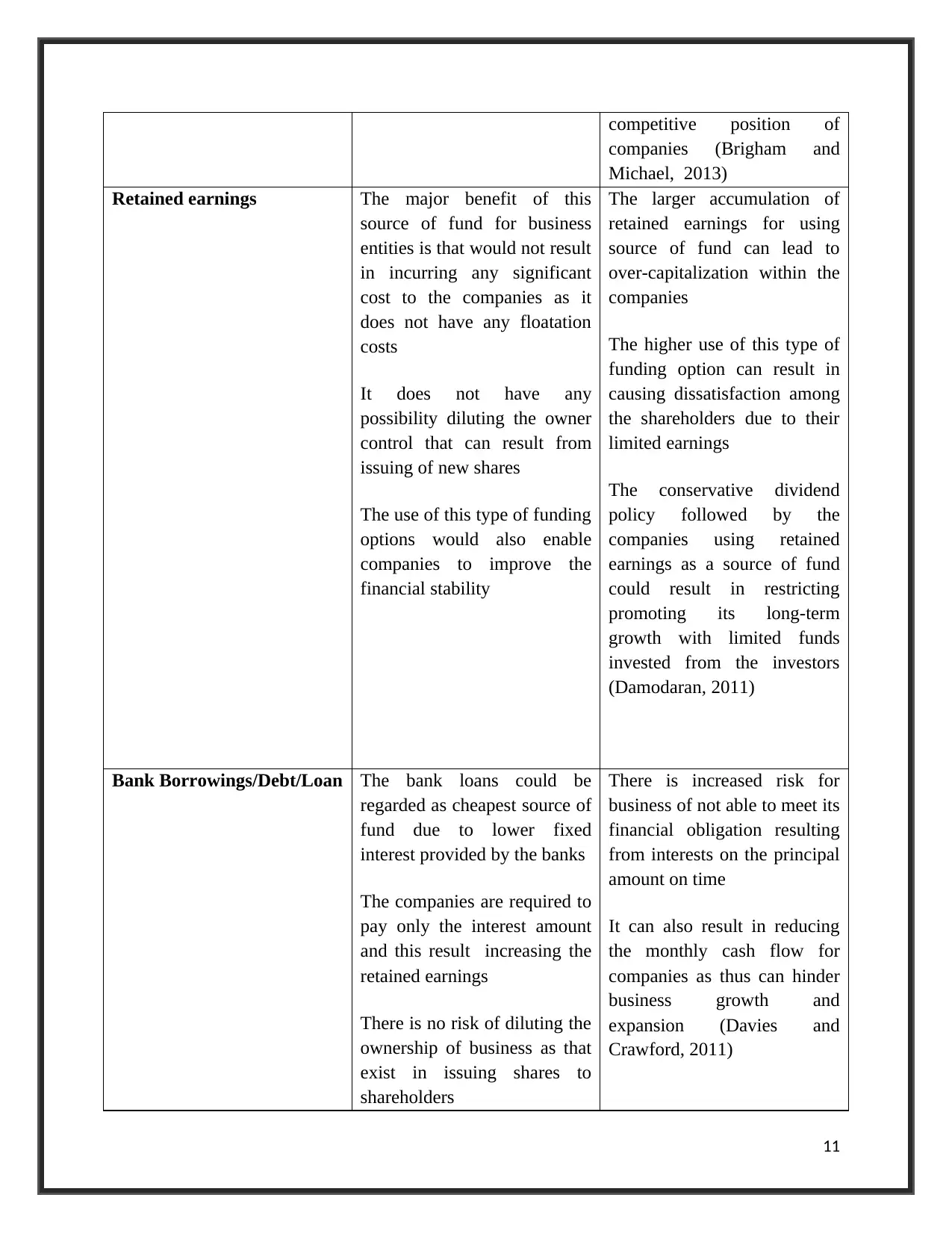

A. (V): Advantages and disadvantages of each of sources of finance used by the selected

companies

Advantages Disadvantages

Ordinary share

capital/Issued Capital

The major advantage of using

this source of fund for the

selected companies is that

shareholders have the right to

vote.

This method of raising capital

enables in promoting fund

expansion without incurring

debt

The funds acquired by issuing

ordinary shares can be

regarded as a major source of

gaining long-term finance

The major drawback

associated with this method is

that it proves to be highly

expensive for companies due

to cost involved in

underwriting the issue,

brokerage costs, legal and

auditor’s fees

The companies are required to

provide higher rate of return to

the shareholders due to more

operational risks undertaken

by them

The issue of shares to the

general public can result in

disclosing the confidential

information to them that can

have a negative impact on the

10

Reason for movement in items of liabilities

The main reason of movement is due to cash and non-cash movement in each of debt

items and also the transfer made from long term liabilities to short term liabilities. Movement

also takes place due to adjustments in foreign exchange differences, fair value changes in debt

instruments and hedging instruments.

A. (V): Advantages and disadvantages of each of sources of finance used by the selected

companies

Advantages Disadvantages

Ordinary share

capital/Issued Capital

The major advantage of using

this source of fund for the

selected companies is that

shareholders have the right to

vote.

This method of raising capital

enables in promoting fund

expansion without incurring

debt

The funds acquired by issuing

ordinary shares can be

regarded as a major source of

gaining long-term finance

The major drawback

associated with this method is

that it proves to be highly

expensive for companies due

to cost involved in

underwriting the issue,

brokerage costs, legal and

auditor’s fees

The companies are required to

provide higher rate of return to

the shareholders due to more

operational risks undertaken

by them

The issue of shares to the

general public can result in

disclosing the confidential

information to them that can

have a negative impact on the

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

competitive position of

companies (Brigham and

Michael, 2013)

Retained earnings The major benefit of this

source of fund for business

entities is that would not result

in incurring any significant

cost to the companies as it

does not have any floatation

costs

It does not have any

possibility diluting the owner

control that can result from

issuing of new shares

The use of this type of funding

options would also enable

companies to improve the

financial stability

The larger accumulation of

retained earnings for using

source of fund can lead to

over-capitalization within the

companies

The higher use of this type of

funding option can result in

causing dissatisfaction among

the shareholders due to their

limited earnings

The conservative dividend

policy followed by the

companies using retained

earnings as a source of fund

could result in restricting

promoting its long-term

growth with limited funds

invested from the investors

(Damodaran, 2011)

Bank Borrowings/Debt/Loan The bank loans could be

regarded as cheapest source of

fund due to lower fixed

interest provided by the banks

The companies are required to

pay only the interest amount

and this result increasing the

retained earnings

There is no risk of diluting the

ownership of business as that

exist in issuing shares to

shareholders

There is increased risk for

business of not able to meet its

financial obligation resulting

from interests on the principal

amount on time

It can also result in reducing

the monthly cash flow for

companies as thus can hinder

business growth and

expansion (Davies and

Crawford, 2011)

11

companies (Brigham and

Michael, 2013)

Retained earnings The major benefit of this

source of fund for business

entities is that would not result

in incurring any significant

cost to the companies as it

does not have any floatation

costs

It does not have any

possibility diluting the owner

control that can result from

issuing of new shares

The use of this type of funding

options would also enable

companies to improve the

financial stability

The larger accumulation of

retained earnings for using

source of fund can lead to

over-capitalization within the

companies

The higher use of this type of

funding option can result in

causing dissatisfaction among

the shareholders due to their

limited earnings

The conservative dividend

policy followed by the

companies using retained

earnings as a source of fund

could result in restricting

promoting its long-term

growth with limited funds

invested from the investors

(Damodaran, 2011)

Bank Borrowings/Debt/Loan The bank loans could be

regarded as cheapest source of

fund due to lower fixed

interest provided by the banks

The companies are required to

pay only the interest amount

and this result increasing the

retained earnings

There is no risk of diluting the

ownership of business as that

exist in issuing shares to

shareholders

There is increased risk for

business of not able to meet its

financial obligation resulting

from interests on the principal

amount on time

It can also result in reducing

the monthly cash flow for

companies as thus can hinder

business growth and

expansion (Davies and

Crawford, 2011)

11

Capital market

debt/Securities

It allows the companies to

invest both in time and money

as compared to issuing new

shares

It proves to be a quick source

of finance as compared to the

venture capital markets

It enables the companies to

select their own investors

having similar objectives

This can reduce the potential

of companies to raise funds

with the issue of new shares

that can have a negative effect

on the value of business

The companies are using only

limited number of potential

investors and this restrict the

inflow of larger amount of

fund within the companies

(Krantz, 2016)

Part B: Critical examination of the concepts of small proprietary company, large

proprietary company and reporting entity

Proprietary Company can be regarded as a form of privately held company within

Australia which means that its shares are not offered for general public. This means that the

major distinction that exist between a proprietary and public company is that proprietary

company’s shares are available only few shareholders whereas public companies shares are

available to the general public for trading. The proprietary companies are classified as either

small or large on the basis of following criteria:

Small Proprietary Company: The small property companies need to be met following criteria:

The consolidated revenue at the end of a financial year for the companies and its entities

under control to be less than $25 million as before 30 June, 2019 and less than $50

million after 1 July, 2019

The overall value of consolidated gross assets at the end of a financial year should be less

than $12.5 million till 30 June, 2019 and $25 million on and after 1 July, 2019.

The companies and its controlled entities need to have less than 50 full-time employees till

30 June, 2019 and less than 100 employees after 1 July, 2019 (Dagwell, Wines and Lambert,

2009)

Also, this type of proprietary company is not requires to develop and disclose their financial

reports as corporation act until it has been controlled by a foreign company. As per the

Corporations Act, small proprietary companies controlled by a foreign entity are required to

develop and lodge its financial reports with ASIC (Australian Securities Investment

Commission). In addition to this, if five per cent or large number of shareholders request for

developing and disclosure of financial reports then such proprietary companies are required to

develop a financial report as per the relevant accounting standards (Deloitte, 2019).

12

debt/Securities

It allows the companies to

invest both in time and money

as compared to issuing new

shares

It proves to be a quick source

of finance as compared to the

venture capital markets

It enables the companies to

select their own investors

having similar objectives

This can reduce the potential

of companies to raise funds

with the issue of new shares

that can have a negative effect

on the value of business

The companies are using only

limited number of potential

investors and this restrict the

inflow of larger amount of

fund within the companies

(Krantz, 2016)

Part B: Critical examination of the concepts of small proprietary company, large

proprietary company and reporting entity

Proprietary Company can be regarded as a form of privately held company within

Australia which means that its shares are not offered for general public. This means that the

major distinction that exist between a proprietary and public company is that proprietary

company’s shares are available only few shareholders whereas public companies shares are

available to the general public for trading. The proprietary companies are classified as either

small or large on the basis of following criteria:

Small Proprietary Company: The small property companies need to be met following criteria:

The consolidated revenue at the end of a financial year for the companies and its entities

under control to be less than $25 million as before 30 June, 2019 and less than $50

million after 1 July, 2019

The overall value of consolidated gross assets at the end of a financial year should be less

than $12.5 million till 30 June, 2019 and $25 million on and after 1 July, 2019.

The companies and its controlled entities need to have less than 50 full-time employees till

30 June, 2019 and less than 100 employees after 1 July, 2019 (Dagwell, Wines and Lambert,

2009)

Also, this type of proprietary company is not requires to develop and disclose their financial

reports as corporation act until it has been controlled by a foreign company. As per the

Corporations Act, small proprietary companies controlled by a foreign entity are required to

develop and lodge its financial reports with ASIC (Australian Securities Investment

Commission). In addition to this, if five per cent or large number of shareholders request for

developing and disclosure of financial reports then such proprietary companies are required to

develop a financial report as per the relevant accounting standards (Deloitte, 2019).

12

Large Proprietary Company: It should meet the following criteria as provided by the ASIC:

The consolidated revenue for the financial year should be more than $25 million till 30

June, 2019 and more than $50 million after 1 July, 2019

The overall value of consolidated gross assets at the end of a financial year should be

more than $12.5 million till 30 June, 2019 and more than $25 million after 1 July, 2019

The companies and its controlled entities need to have more than 50 full-time employees

till 30 June, 2019 and more than 100 employees after 1 July, 2019

This type of proprietary companies is required to develop and lodge their financial reports for

each financial year as per ASIC (ASIC, 2019).

Reporting Entity Concept

The AASB standard has defined a reporting entity as an economic entity that is

recognized on the basis of existence of its users of general purpose financial reports that would

assist in them in making relevant decisions about allocating scarce resources. The concept of

reporting entity includes a publicly listed corporation, a borrowing corporation and company

which is subsidiary of a foreign company and its securities are listed to be quite on stock market

or are traded within stock market. However, the concept is not only limited to these types of

business corporations. As directed by the AASB, the reporting entities are required to develop

and present their genial purpose financial statements according to the statement of accounting

concepts and relevant accounting standards (Statement of Accounting Concepts, 2017).

Conclusion

It has been concluded from the overall analysis of sources of funds used by both the

selected companies that it is necessary to make the balance of both equity and debt capital in

order to reduce the dependencies on single source of funds. It has been also observed that both

companies has not used preference capital to raise the funds and instead has expanded their

dependencies on securities and capital market debts.

13

The consolidated revenue for the financial year should be more than $25 million till 30

June, 2019 and more than $50 million after 1 July, 2019

The overall value of consolidated gross assets at the end of a financial year should be

more than $12.5 million till 30 June, 2019 and more than $25 million after 1 July, 2019

The companies and its controlled entities need to have more than 50 full-time employees

till 30 June, 2019 and more than 100 employees after 1 July, 2019

This type of proprietary companies is required to develop and lodge their financial reports for

each financial year as per ASIC (ASIC, 2019).

Reporting Entity Concept

The AASB standard has defined a reporting entity as an economic entity that is

recognized on the basis of existence of its users of general purpose financial reports that would

assist in them in making relevant decisions about allocating scarce resources. The concept of

reporting entity includes a publicly listed corporation, a borrowing corporation and company

which is subsidiary of a foreign company and its securities are listed to be quite on stock market

or are traded within stock market. However, the concept is not only limited to these types of

business corporations. As directed by the AASB, the reporting entities are required to develop

and present their genial purpose financial statements according to the statement of accounting

concepts and relevant accounting standards (Statement of Accounting Concepts, 2017).

Conclusion

It has been concluded from the overall analysis of sources of funds used by both the

selected companies that it is necessary to make the balance of both equity and debt capital in

order to reduce the dependencies on single source of funds. It has been also observed that both

companies has not used preference capital to raise the funds and instead has expanded their

dependencies on securities and capital market debts.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

ASIC. 2019. [Online]. Available at: https://asic.gov.au/regulatory-resources/financial-reporting-

and-audit/preparers-of-financial-reports/are-you-a-large-or-small-proprietary-company/

[Accessed on: 5 October 2019].

Baker, K. and Powell, G. 2010. Understanding Financial Management: A Practical Guide.

USA: John Wiley & Sons.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Dagwell, R., Wines, G. and Lambert, C. 2009. Corporate Accounting in Australia. Australia:

UNSW Press.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Deloitte. 2019. Clarity in financial reporting. [Online]. Available at:

https://www2.deloitte.com/content/dam/Deloitte/au/Documents/audit/deloitte-au-audit-clarity-

changes-proprietary-company-thresholds-may-2019-310519.pdf [Accessed on: 5 October 2019].

Gibson, C. 2011. Financial Reporting and Analysis: Using Financial Accounting Information.

Australia: Cengage Learning.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Statement of Accounting Concepts. 2017. Definition of the Reporting Entity. [Online]. Available

at: https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed on: 5

October 2019].

Wesfarmers: Annual Report. 2017. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed on: 5 October, 2019].

Wesfarmers: Annual Report. 2017. [Online]. Available at:

https://www.woolworthsgroup.com.au/icms_docs/188795_annual-report-2017.pdf[Accessed on:

5 October, 2019].

Wesfarmers: Annual Report. 2018. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn=0 [Accessed on: 5 October, 2019].

14

ASIC. 2019. [Online]. Available at: https://asic.gov.au/regulatory-resources/financial-reporting-

and-audit/preparers-of-financial-reports/are-you-a-large-or-small-proprietary-company/

[Accessed on: 5 October 2019].

Baker, K. and Powell, G. 2010. Understanding Financial Management: A Practical Guide.

USA: John Wiley & Sons.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Dagwell, R., Wines, G. and Lambert, C. 2009. Corporate Accounting in Australia. Australia:

UNSW Press.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Deloitte. 2019. Clarity in financial reporting. [Online]. Available at:

https://www2.deloitte.com/content/dam/Deloitte/au/Documents/audit/deloitte-au-audit-clarity-

changes-proprietary-company-thresholds-may-2019-310519.pdf [Accessed on: 5 October 2019].

Gibson, C. 2011. Financial Reporting and Analysis: Using Financial Accounting Information.

Australia: Cengage Learning.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Statement of Accounting Concepts. 2017. Definition of the Reporting Entity. [Online]. Available

at: https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed on: 5

October 2019].

Wesfarmers: Annual Report. 2017. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed on: 5 October, 2019].

Wesfarmers: Annual Report. 2017. [Online]. Available at:

https://www.woolworthsgroup.com.au/icms_docs/188795_annual-report-2017.pdf[Accessed on:

5 October, 2019].

Wesfarmers: Annual Report. 2018. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn=0 [Accessed on: 5 October, 2019].

14

Woolworth: Annual Report. 2018. [Online]. Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf[Accessed on:

5 October, 2019].

15

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf[Accessed on:

5 October, 2019].

15

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.