Corporate Takeover Decision Making and the Effects on Consolidation Accounting

VerifiedAdded on 2023/02/01

|11

|3501

|93

AI Summary

The report intends to obtain a critical insight of the different accounting aspects associated with acquisition of a smaller organisation, FAB Limited by JKY Limited. At the time of analysing the differences between consolidation accounting and equity accounting when an organisation acquires a smaller firm, there are different measurement and recognition principles. Moreover, the treatment of intra-group transactions undertakes significant differences in the consolidated financial statements of both organisations. Finally, it has been evaluated that the disclosure requirements requiring non-controlling interest as a separate item in the consolidated financial statements has impact on the overall consolidation process.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate Takeover Decision Making and the Effects on Consolidation Accounting

Student Name:

Student Number:

Session Number:

Corporate Takeover Decision Making and the Effects on Consolidation Accounting

Student Name:

Student Number:

Session Number:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary:

The report intends to obtain a critical insight of the different accounting aspects

associated with acquisition of a smaller organisation, FAB Limited by JKY Limited. At

the time of analysing the differences between consolidation accounting and equity

accounting when an organisation acquires a smaller firm, there are different

measurement and recognition principles. Moreover, the treatment of intra-group

transactions undertakes significant differences in the consolidated financial

statements of both organisations. Finally, it has been evaluated that the disclosure

requirements requiring non-controlling interest as a separate item in the consolidated

financial statements has impact on the overall consolidation process.

Executive Summary:

The report intends to obtain a critical insight of the different accounting aspects

associated with acquisition of a smaller organisation, FAB Limited by JKY Limited. At

the time of analysing the differences between consolidation accounting and equity

accounting when an organisation acquires a smaller firm, there are different

measurement and recognition principles. Moreover, the treatment of intra-group

transactions undertakes significant differences in the consolidated financial

statements of both organisations. Finally, it has been evaluated that the disclosure

requirements requiring non-controlling interest as a separate item in the consolidated

financial statements has impact on the overall consolidation process.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction:..................................................................................................................3

Part A Response:..........................................................................................................3

Part B Response:..........................................................................................................5

Part C Response:.........................................................................................................6

Conclusion:...................................................................................................................8

Reference List:..............................................................................................................9

Table of Contents

Introduction:..................................................................................................................3

Part A Response:..........................................................................................................3

Part B Response:..........................................................................................................5

Part C Response:.........................................................................................................6

Conclusion:...................................................................................................................8

Reference List:..............................................................................................................9

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction:

The objective of the report is to obtain a critical insight of the different

accounting aspects associated with acquisition of a smaller organisation, FAB

Limited by JKY Limited. The first section of the paper would provide a distinction

between the major methodological differences in consolidation accounting and equity

accounting with appropriate examples. The second section would highlight the key

principles of intra-group transactions and their treatment by using worked examples.

Finally, the report would shed light on the impact of the disclosures associated with

the non-controlling interests in the form of a separate item in the process of

consolidation.

Part A Response:

From the provided case study, it has been identified that in order to take over

FAB Limited, the management of JKY Limited is in a dilemma regarding the selection

of the acquisition strategy. The consolidation method and the equity method are two

kinds of accounting methods utilised when two organisations are portions of a joint

venture (Atanasov and Black 2016). The selection of using any one method depends

on the way the income statement and the balance sheet statement of the

organisation report the partnerships. This clearly implies that these two accounting

methods have significant differences in methodology, which are elaborated as

follows:

Consolidation method of accounting:

According to this method of accounting, assets and liabilities of a joint venture

are recorded on the balance sheet statement of an organisation in proportion of the

percentage of involvement the organisation maintains in the venture (Balakrishnan,

Watts and Zuo 2016). At the time of computing assets and liabilities, the organisation

would list all its expenses and income from the acquisition and they are included on

the income statement and the balance sheet statement. According to “Paragraph

B86 of AASB 10”, the consolidated financial statements are combined like items of

equity, assets, liabilities, cash flows, income and expenses of the parent organisation

with those of its subsidiaries (Aasb.gov.au 2019). In addition, the method offsets or

eliminates the carrying value of the investment of the parent in each subsidiary and

the portion of equity held by the subsidiaries of the parent organisation. Furthermore,

the consolidated accounting method makes elimination adjustment with the objective

to offset intercompany transactions in order to avoid double counting of values at the

consolidated level.

“Paragraph B88 of AASB 10” sets out the measurement requirements of the

different line items of the financial statements, in which income and expenses of the

subsidiary are based on asset and liability amounts realised in the consolidated

financial statements at the date of acquisition. Thus, these items are measured at

fair values at the date of acquisition. “Paragraph 32 of AASB 3” lays out a particular

criterion in terms of goodwill recognition. The acquirer has to recognise goodwill at

the acquisition date as the higher of the two below:

a. The aggregate of:-

Introduction:

The objective of the report is to obtain a critical insight of the different

accounting aspects associated with acquisition of a smaller organisation, FAB

Limited by JKY Limited. The first section of the paper would provide a distinction

between the major methodological differences in consolidation accounting and equity

accounting with appropriate examples. The second section would highlight the key

principles of intra-group transactions and their treatment by using worked examples.

Finally, the report would shed light on the impact of the disclosures associated with

the non-controlling interests in the form of a separate item in the process of

consolidation.

Part A Response:

From the provided case study, it has been identified that in order to take over

FAB Limited, the management of JKY Limited is in a dilemma regarding the selection

of the acquisition strategy. The consolidation method and the equity method are two

kinds of accounting methods utilised when two organisations are portions of a joint

venture (Atanasov and Black 2016). The selection of using any one method depends

on the way the income statement and the balance sheet statement of the

organisation report the partnerships. This clearly implies that these two accounting

methods have significant differences in methodology, which are elaborated as

follows:

Consolidation method of accounting:

According to this method of accounting, assets and liabilities of a joint venture

are recorded on the balance sheet statement of an organisation in proportion of the

percentage of involvement the organisation maintains in the venture (Balakrishnan,

Watts and Zuo 2016). At the time of computing assets and liabilities, the organisation

would list all its expenses and income from the acquisition and they are included on

the income statement and the balance sheet statement. According to “Paragraph

B86 of AASB 10”, the consolidated financial statements are combined like items of

equity, assets, liabilities, cash flows, income and expenses of the parent organisation

with those of its subsidiaries (Aasb.gov.au 2019). In addition, the method offsets or

eliminates the carrying value of the investment of the parent in each subsidiary and

the portion of equity held by the subsidiaries of the parent organisation. Furthermore,

the consolidated accounting method makes elimination adjustment with the objective

to offset intercompany transactions in order to avoid double counting of values at the

consolidated level.

“Paragraph B88 of AASB 10” sets out the measurement requirements of the

different line items of the financial statements, in which income and expenses of the

subsidiary are based on asset and liability amounts realised in the consolidated

financial statements at the date of acquisition. Thus, these items are measured at

fair values at the date of acquisition. “Paragraph 32 of AASB 3” lays out a particular

criterion in terms of goodwill recognition. The acquirer has to recognise goodwill at

the acquisition date as the higher of the two below:

a. The aggregate of:-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE AND FINANCIAL ACCOUNTING

The transfer of consideration gauged in accordance with AASB 3 requiring fair

value at the acquisition date

The non-controlling interest value in the acquiree gauged according to the

standard

In a business combination accomplished in stages, the fair value of the equity

interest held in the past in the acquiree by the acquirer at the fair value of the

acquisition date

b. The net of the identifiable asset amounts acquired and the assumed liabilities

gauged in compliance with the standard (Aasb.gov.au 2019)

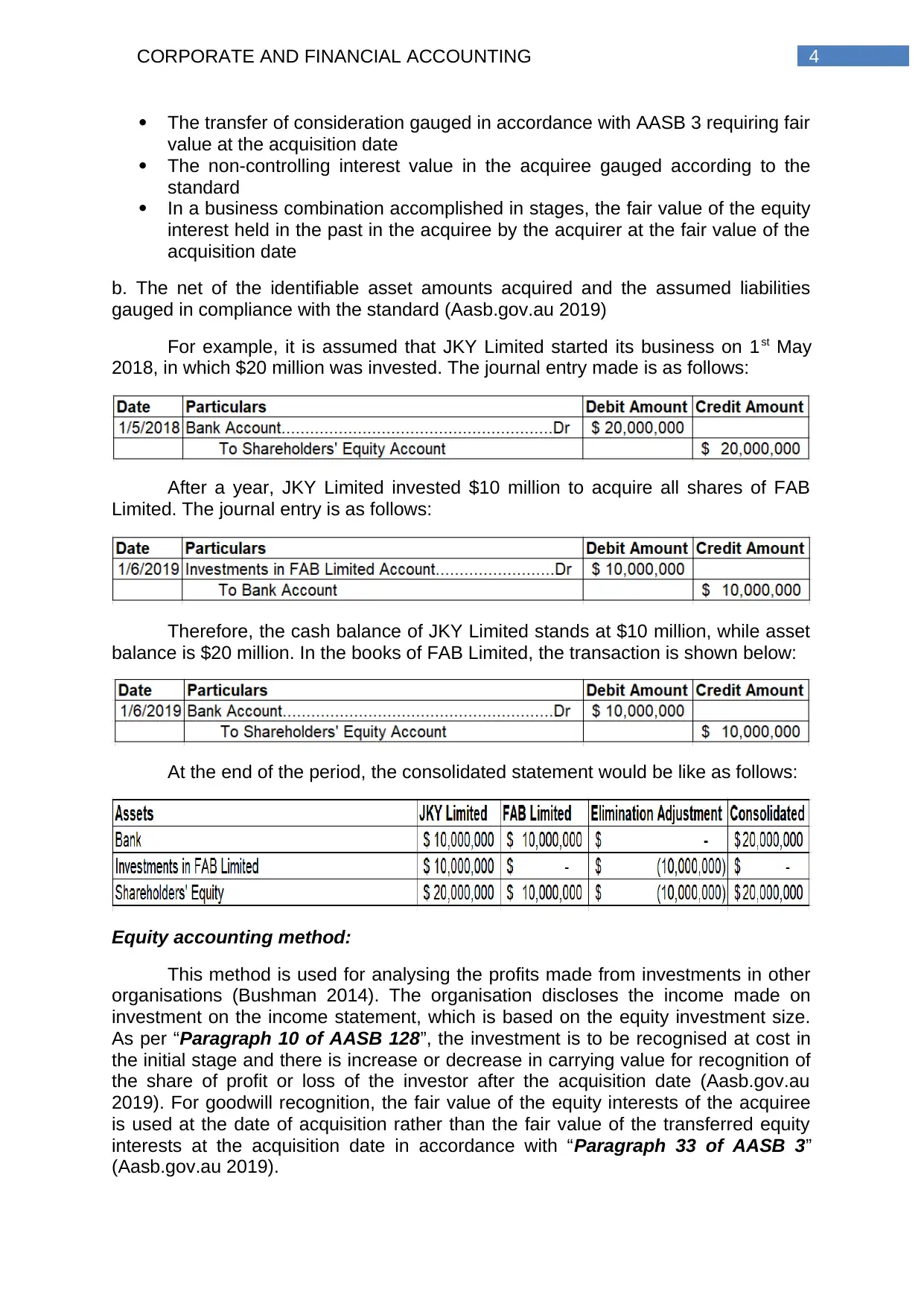

For example, it is assumed that JKY Limited started its business on 1st May

2018, in which $20 million was invested. The journal entry made is as follows:

After a year, JKY Limited invested $10 million to acquire all shares of FAB

Limited. The journal entry is as follows:

Therefore, the cash balance of JKY Limited stands at $10 million, while asset

balance is $20 million. In the books of FAB Limited, the transaction is shown below:

At the end of the period, the consolidated statement would be like as follows:

Equity accounting method:

This method is used for analysing the profits made from investments in other

organisations (Bushman 2014). The organisation discloses the income made on

investment on the income statement, which is based on the equity investment size.

As per “Paragraph 10 of AASB 128”, the investment is to be recognised at cost in

the initial stage and there is increase or decrease in carrying value for recognition of

the share of profit or loss of the investor after the acquisition date (Aasb.gov.au

2019). For goodwill recognition, the fair value of the equity interests of the acquiree

is used at the date of acquisition rather than the fair value of the transferred equity

interests at the acquisition date in accordance with “Paragraph 33 of AASB 3”

(Aasb.gov.au 2019).

The transfer of consideration gauged in accordance with AASB 3 requiring fair

value at the acquisition date

The non-controlling interest value in the acquiree gauged according to the

standard

In a business combination accomplished in stages, the fair value of the equity

interest held in the past in the acquiree by the acquirer at the fair value of the

acquisition date

b. The net of the identifiable asset amounts acquired and the assumed liabilities

gauged in compliance with the standard (Aasb.gov.au 2019)

For example, it is assumed that JKY Limited started its business on 1st May

2018, in which $20 million was invested. The journal entry made is as follows:

After a year, JKY Limited invested $10 million to acquire all shares of FAB

Limited. The journal entry is as follows:

Therefore, the cash balance of JKY Limited stands at $10 million, while asset

balance is $20 million. In the books of FAB Limited, the transaction is shown below:

At the end of the period, the consolidated statement would be like as follows:

Equity accounting method:

This method is used for analysing the profits made from investments in other

organisations (Bushman 2014). The organisation discloses the income made on

investment on the income statement, which is based on the equity investment size.

As per “Paragraph 10 of AASB 128”, the investment is to be recognised at cost in

the initial stage and there is increase or decrease in carrying value for recognition of

the share of profit or loss of the investor after the acquisition date (Aasb.gov.au

2019). For goodwill recognition, the fair value of the equity interests of the acquiree

is used at the date of acquisition rather than the fair value of the transferred equity

interests at the acquisition date in accordance with “Paragraph 33 of AASB 3”

(Aasb.gov.au 2019).

5CORPORATE AND FINANCIAL ACCOUNTING

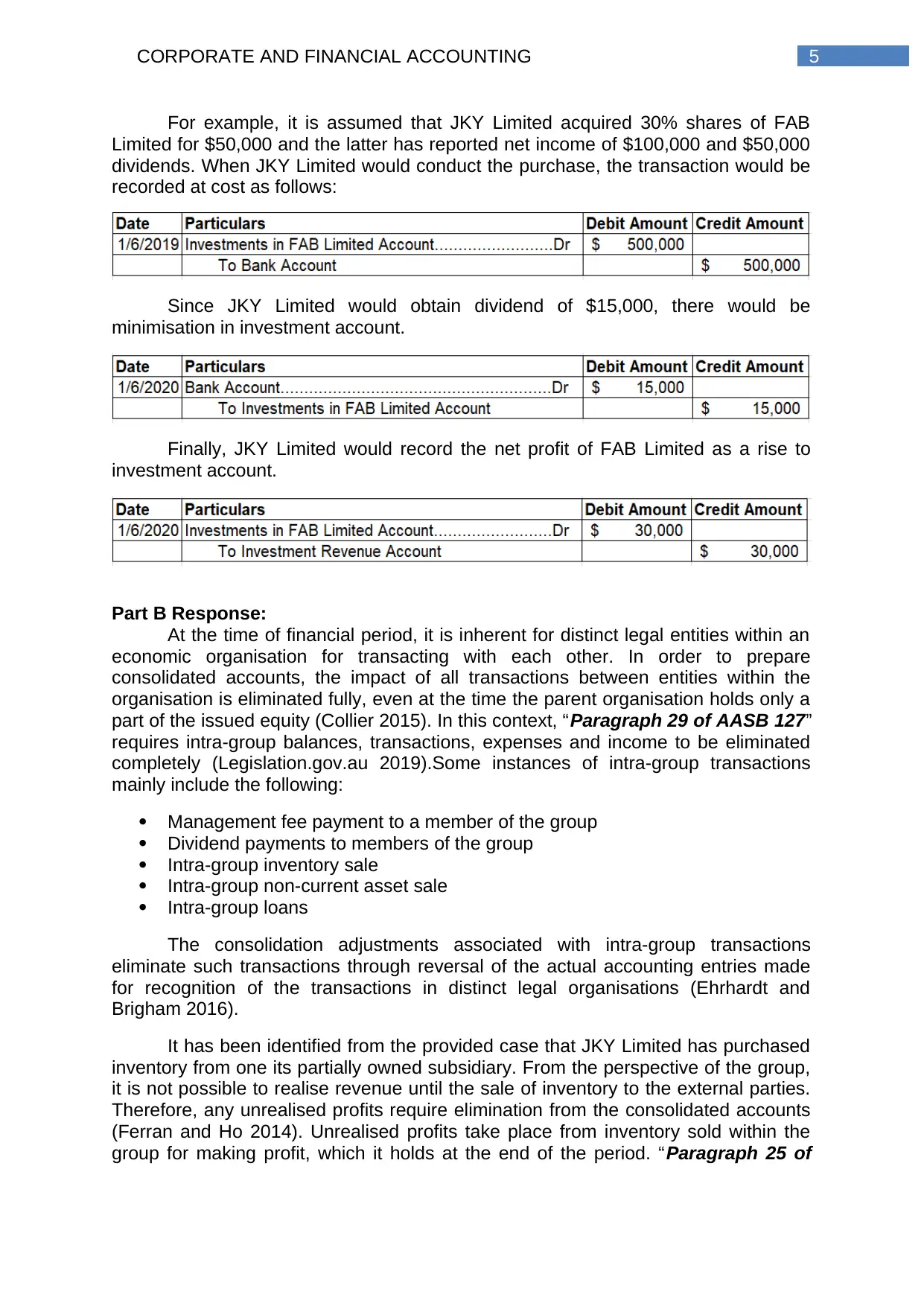

For example, it is assumed that JKY Limited acquired 30% shares of FAB

Limited for $50,000 and the latter has reported net income of $100,000 and $50,000

dividends. When JKY Limited would conduct the purchase, the transaction would be

recorded at cost as follows:

Since JKY Limited would obtain dividend of $15,000, there would be

minimisation in investment account.

Finally, JKY Limited would record the net profit of FAB Limited as a rise to

investment account.

Part B Response:

At the time of financial period, it is inherent for distinct legal entities within an

economic organisation for transacting with each other. In order to prepare

consolidated accounts, the impact of all transactions between entities within the

organisation is eliminated fully, even at the time the parent organisation holds only a

part of the issued equity (Collier 2015). In this context, “Paragraph 29 of AASB 127”

requires intra-group balances, transactions, expenses and income to be eliminated

completely (Legislation.gov.au 2019).Some instances of intra-group transactions

mainly include the following:

Management fee payment to a member of the group

Dividend payments to members of the group

Intra-group inventory sale

Intra-group non-current asset sale

Intra-group loans

The consolidation adjustments associated with intra-group transactions

eliminate such transactions through reversal of the actual accounting entries made

for recognition of the transactions in distinct legal organisations (Ehrhardt and

Brigham 2016).

It has been identified from the provided case that JKY Limited has purchased

inventory from one its partially owned subsidiary. From the perspective of the group,

it is not possible to realise revenue until the sale of inventory to the external parties.

Therefore, any unrealised profits require elimination from the consolidated accounts

(Ferran and Ho 2014). Unrealised profits take place from inventory sold within the

group for making profit, which it holds at the end of the period. “Paragraph 25 of

For example, it is assumed that JKY Limited acquired 30% shares of FAB

Limited for $50,000 and the latter has reported net income of $100,000 and $50,000

dividends. When JKY Limited would conduct the purchase, the transaction would be

recorded at cost as follows:

Since JKY Limited would obtain dividend of $15,000, there would be

minimisation in investment account.

Finally, JKY Limited would record the net profit of FAB Limited as a rise to

investment account.

Part B Response:

At the time of financial period, it is inherent for distinct legal entities within an

economic organisation for transacting with each other. In order to prepare

consolidated accounts, the impact of all transactions between entities within the

organisation is eliminated fully, even at the time the parent organisation holds only a

part of the issued equity (Collier 2015). In this context, “Paragraph 29 of AASB 127”

requires intra-group balances, transactions, expenses and income to be eliminated

completely (Legislation.gov.au 2019).Some instances of intra-group transactions

mainly include the following:

Management fee payment to a member of the group

Dividend payments to members of the group

Intra-group inventory sale

Intra-group non-current asset sale

Intra-group loans

The consolidation adjustments associated with intra-group transactions

eliminate such transactions through reversal of the actual accounting entries made

for recognition of the transactions in distinct legal organisations (Ehrhardt and

Brigham 2016).

It has been identified from the provided case that JKY Limited has purchased

inventory from one its partially owned subsidiary. From the perspective of the group,

it is not possible to realise revenue until the sale of inventory to the external parties.

Therefore, any unrealised profits require elimination from the consolidated accounts

(Ferran and Ho 2014). Unrealised profits take place from inventory sold within the

group for making profit, which it holds at the end of the period. “Paragraph 25 of

6CORPORATE AND FINANCIAL ACCOUNTING

AASB 127” states the profits or losses arising from intra-group transactions

recognised in assets like non-current assets and inventory are eliminated fully.

In the provided case, the partially owned subsidiary has sold inventory to JKY

Limited and it is assumed that the sale includes a mark-up, When JKY Limited sells

the same to the external customers, it is accurate in terms of group transaction point

(Henderson et al. 2015). However, until the goods are sold to the external customers

by JKY Limited, the profit that the subsidiary has realised on inventory sold to JKY

Limited would lead to unrealised profit and therefore, the group profit would be

boosted unduly. This mandates the elimination of unrealised profit. For instance, it is

assumed that JKY Limited has purchased inventory from its subsidiary at $12,500,

which is kept at the end of the year. Further assumption is made that the subsidiary

earns 25% margin and thus, it earned a profit on inventory balance of $2,500

(25/125 x $12,500). Therefore, from the group viewpoint, there is overstatement of

consolidated profit by $2,500, for which the following adjustment entry is needed:

Consolidated Profit Account......................................Dr $2,500

To Consolidated Inventory Account $2,500

When the subsidiary sells the goods with non-controlling interest to the group,

there is need to eradicate the entire unrealised profit (Hillier et al. 2014). This raises

the question regarding the profit to be reported for non-controlling interests. The first

approach is to assign to the non-controlling interests the proportionate share of

unrecognised profit. Thus, the entire profit in the selling entity is eliminated. Another

approach is to assign no portion of unrecognised profit to non-controlling interests

and the figure for non-controlling interests depicts entitlement to share capital and

reserves associated with the subsidiary (Hoyle, Schaefer and Doupnik 2015).

For instance, it is assumed that JKY Limited has 80% interest in D Limited

and 75% interest in E Limited. In an accounting year, D Limited sells goods costing

$70,000 for $100,000 to E Limited; out of which E Limited sells only 50% of the

goods. When JKY Limited would prepare its consolidated financial statements, the

unrecognised profit in inventories has to be eliminated. The transfer of profit from D

Limited to E Limited is made at $50,000 and the group cost would be $35,000.

Therefore, the intra-group profit to be removed from inventories is $15,000. By

applying the first method, since JKY Limited owns 80% interest in JKY Limited and

20% is non-controlling interest, the proportion of non-controlling interest would be

$3,000 ($15,000 x 20%).

Part C Response:

Effects of NCI disclosure requirement as a separate item in the process of

consolidation:

It is evident from “Paragraph 27 of AASB 127” that separate and

consolidated financial statements need separate presentation of non-controlling

interest from the equity of the parent company in the balance sheet statement

(Aasb.gov.au 2019). Non-controlling interest is the part of equity in subsidiary, which

could not be attributed directly or indirectly to the parent firm. The above standard

has assisted in improved accounting and reporting for non-controlling interest in the

financial statements. At the time there is separate reporting of non-controlling

AASB 127” states the profits or losses arising from intra-group transactions

recognised in assets like non-current assets and inventory are eliminated fully.

In the provided case, the partially owned subsidiary has sold inventory to JKY

Limited and it is assumed that the sale includes a mark-up, When JKY Limited sells

the same to the external customers, it is accurate in terms of group transaction point

(Henderson et al. 2015). However, until the goods are sold to the external customers

by JKY Limited, the profit that the subsidiary has realised on inventory sold to JKY

Limited would lead to unrealised profit and therefore, the group profit would be

boosted unduly. This mandates the elimination of unrealised profit. For instance, it is

assumed that JKY Limited has purchased inventory from its subsidiary at $12,500,

which is kept at the end of the year. Further assumption is made that the subsidiary

earns 25% margin and thus, it earned a profit on inventory balance of $2,500

(25/125 x $12,500). Therefore, from the group viewpoint, there is overstatement of

consolidated profit by $2,500, for which the following adjustment entry is needed:

Consolidated Profit Account......................................Dr $2,500

To Consolidated Inventory Account $2,500

When the subsidiary sells the goods with non-controlling interest to the group,

there is need to eradicate the entire unrealised profit (Hillier et al. 2014). This raises

the question regarding the profit to be reported for non-controlling interests. The first

approach is to assign to the non-controlling interests the proportionate share of

unrecognised profit. Thus, the entire profit in the selling entity is eliminated. Another

approach is to assign no portion of unrecognised profit to non-controlling interests

and the figure for non-controlling interests depicts entitlement to share capital and

reserves associated with the subsidiary (Hoyle, Schaefer and Doupnik 2015).

For instance, it is assumed that JKY Limited has 80% interest in D Limited

and 75% interest in E Limited. In an accounting year, D Limited sells goods costing

$70,000 for $100,000 to E Limited; out of which E Limited sells only 50% of the

goods. When JKY Limited would prepare its consolidated financial statements, the

unrecognised profit in inventories has to be eliminated. The transfer of profit from D

Limited to E Limited is made at $50,000 and the group cost would be $35,000.

Therefore, the intra-group profit to be removed from inventories is $15,000. By

applying the first method, since JKY Limited owns 80% interest in JKY Limited and

20% is non-controlling interest, the proportion of non-controlling interest would be

$3,000 ($15,000 x 20%).

Part C Response:

Effects of NCI disclosure requirement as a separate item in the process of

consolidation:

It is evident from “Paragraph 27 of AASB 127” that separate and

consolidated financial statements need separate presentation of non-controlling

interest from the equity of the parent company in the balance sheet statement

(Aasb.gov.au 2019). Non-controlling interest is the part of equity in subsidiary, which

could not be attributed directly or indirectly to the parent firm. The above standard

has assisted in improved accounting and reporting for non-controlling interest in the

financial statements. At the time there is separate reporting of non-controlling

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

interest in the consolidation process, the changes have to be reconciled in the

shareholders’ equity outlining the alterations in parent firm and non-controlling

interest respectively, as per “Paragraph 106 (a) of AASB 101” (Aasb.gov.au 2019).

It is necessary to label and identify the separate non-controlling interest amount

clearly. The main reason behind such separate presentation is to ensure additional

clarifications to the shareholders of the consolidated group owing to their claim on

the net assets of the group (Mitchell et al. 2015). Moreover, there is fair depiction

when one of the organisations has direct or indirect non-controlling financial interest.

Equity transactions could be described as the variations in ownership interest

of parent firm in a subsidiary, which does not take place when the parent firm loses

control over the subsidiary. If the portion of equity that the non-controlling interest

holds changes, the variation in the relative subsidiary interest is represented by

conducting adjustments in the carrying values of controlling and non-controlling

interests. Along with this, the adjustment of non-controlling interest and fair value of

consideration payment is to be recognised directly and they are attributable to the

shareholders of the parent organisation.

Changes needed to ensure the accurate representation of the consolidated

financial statements:

For accurate representation of the consolidated financial statements, certain

changes are required mentioned in AASB 101. There is no need of preparing the

consolidated financial statements at the same date of reporting and adjustments are

required for depicting the effects on main transactions or events occurring between

the dates of the subsidiary and the parent financial statements. The carrying value of

investment made by the parent in the subsidiary needs to be offset and the part of

equity of each subsidiary that the parent holds needs to be eradicated (Nobes 2014).

The impairment losses of the associated assets have to be realised, which

could be identified from intra-group losses. Moreover, the transactions related to

intra-group income, expenses and balances have to be eliminated. These

consolidated financial statements need to combine different items of cash flows,

liabilities, assets and expenses of both the parent organisation and its subsidiaries.

Furthermore, the temporary differences taking place from elimination of profit and

loss leading to intra-group transactions is applicable in compliance with AASB 112. It

needs to be assured that the accounting policies of the group have to be uniform by

making suitable adjustments to the financial statements of the group member at the

time of developing the consolidated financial statements in situations when a

member of the group utilises different accounting policies for certain transactions

(Vernimmen et al. 2014).

The organisation is needed to attribute the overall comprehensive income to

the parent owners and the non-controlling interest, even if the treatment has the

consequence of having adverse balance related to non-controlling interest. In

addition, the share of profit or loss when any subsidiary has outstanding cumulative

preference shares, it needs to be calculated by the organisation after conducting

adjustments for dividends on those shares regardless of dividend declaration.

Effects of the required changes on the disclosure requirements in the annual

report:

interest in the consolidation process, the changes have to be reconciled in the

shareholders’ equity outlining the alterations in parent firm and non-controlling

interest respectively, as per “Paragraph 106 (a) of AASB 101” (Aasb.gov.au 2019).

It is necessary to label and identify the separate non-controlling interest amount

clearly. The main reason behind such separate presentation is to ensure additional

clarifications to the shareholders of the consolidated group owing to their claim on

the net assets of the group (Mitchell et al. 2015). Moreover, there is fair depiction

when one of the organisations has direct or indirect non-controlling financial interest.

Equity transactions could be described as the variations in ownership interest

of parent firm in a subsidiary, which does not take place when the parent firm loses

control over the subsidiary. If the portion of equity that the non-controlling interest

holds changes, the variation in the relative subsidiary interest is represented by

conducting adjustments in the carrying values of controlling and non-controlling

interests. Along with this, the adjustment of non-controlling interest and fair value of

consideration payment is to be recognised directly and they are attributable to the

shareholders of the parent organisation.

Changes needed to ensure the accurate representation of the consolidated

financial statements:

For accurate representation of the consolidated financial statements, certain

changes are required mentioned in AASB 101. There is no need of preparing the

consolidated financial statements at the same date of reporting and adjustments are

required for depicting the effects on main transactions or events occurring between

the dates of the subsidiary and the parent financial statements. The carrying value of

investment made by the parent in the subsidiary needs to be offset and the part of

equity of each subsidiary that the parent holds needs to be eradicated (Nobes 2014).

The impairment losses of the associated assets have to be realised, which

could be identified from intra-group losses. Moreover, the transactions related to

intra-group income, expenses and balances have to be eliminated. These

consolidated financial statements need to combine different items of cash flows,

liabilities, assets and expenses of both the parent organisation and its subsidiaries.

Furthermore, the temporary differences taking place from elimination of profit and

loss leading to intra-group transactions is applicable in compliance with AASB 112. It

needs to be assured that the accounting policies of the group have to be uniform by

making suitable adjustments to the financial statements of the group member at the

time of developing the consolidated financial statements in situations when a

member of the group utilises different accounting policies for certain transactions

(Vernimmen et al. 2014).

The organisation is needed to attribute the overall comprehensive income to

the parent owners and the non-controlling interest, even if the treatment has the

consequence of having adverse balance related to non-controlling interest. In

addition, the share of profit or loss when any subsidiary has outstanding cumulative

preference shares, it needs to be calculated by the organisation after conducting

adjustments for dividends on those shares regardless of dividend declaration.

Effects of the required changes on the disclosure requirements in the annual

report:

8CORPORATE AND FINANCIAL ACCOUNTING

According to “Paragraph 10 of AASB 127”, when an organisation prepares

separate financial statements, it needs to account for investments made in joint

ventures, associated and subsidiaries either at cost or as per AASB 9 (Aasb.gov.au

2019). Thus, there has been relaxation in the preparation of the consolidated

financial statements. In case; the information arising from any disclosure lacks

materiality, it is necessary to disclose the pertinent accounting policies along with the

measurement bases used to prepare the consolidated financial statements.

Therefore, the consolidated financial statements have to be developed by disclosing

the nature and degree of any important limitations arising from the need of

regulations on the ability of the subsidiary in transferring to the parent either through

repayment of loans, advances and dividends in cash.

Along with this, at the time of developing the consolidated financial

statements, the financial statements of the subsidiaries at the end of the reporting

year are required and in case; the reporting date of the parent organisation and its

subsidiaries does not match with each other, relevant disclosures need to be made

regarding the same. Furthermore, if the parent organisation owns less than 50% of

voting rights in a subsidiary, be it direct or indirect, disclosures are necessary to be

made regarding the nature of relationship inherent between the parent organisation

and the subsidiary (Warren and Jones 2018). Hence, it could be stated there is

impact of disclosure requirements at the time of preparing the consolidated financial

statements.

Conclusion:

Based on the above analysis, it could be stated that there are considerable

alterations in accounting treatment of non-controlling interest and consolidation

accounting in relation to various accounting standards. At the time of analysing the

differences between consolidation accounting and equity accounting when an

organisation acquires a smaller firm, there are different measurement and

recognition principles. Moreover, the treatment of intra-group transactions

undertakes significant differences in the consolidated financial statements of both

organisations. Finally, it has been evaluated that the disclosure requirements

requiring non-controlling interest as a separate item in the consolidated financial

statements has impact on the overall consolidation process.

According to “Paragraph 10 of AASB 127”, when an organisation prepares

separate financial statements, it needs to account for investments made in joint

ventures, associated and subsidiaries either at cost or as per AASB 9 (Aasb.gov.au

2019). Thus, there has been relaxation in the preparation of the consolidated

financial statements. In case; the information arising from any disclosure lacks

materiality, it is necessary to disclose the pertinent accounting policies along with the

measurement bases used to prepare the consolidated financial statements.

Therefore, the consolidated financial statements have to be developed by disclosing

the nature and degree of any important limitations arising from the need of

regulations on the ability of the subsidiary in transferring to the parent either through

repayment of loans, advances and dividends in cash.

Along with this, at the time of developing the consolidated financial

statements, the financial statements of the subsidiaries at the end of the reporting

year are required and in case; the reporting date of the parent organisation and its

subsidiaries does not match with each other, relevant disclosures need to be made

regarding the same. Furthermore, if the parent organisation owns less than 50% of

voting rights in a subsidiary, be it direct or indirect, disclosures are necessary to be

made regarding the nature of relationship inherent between the parent organisation

and the subsidiary (Warren and Jones 2018). Hence, it could be stated there is

impact of disclosure requirements at the time of preparing the consolidated financial

statements.

Conclusion:

Based on the above analysis, it could be stated that there are considerable

alterations in accounting treatment of non-controlling interest and consolidation

accounting in relation to various accounting standards. At the time of analysing the

differences between consolidation accounting and equity accounting when an

organisation acquires a smaller firm, there are different measurement and

recognition principles. Moreover, the treatment of intra-group transactions

undertakes significant differences in the consolidated financial statements of both

organisations. Finally, it has been evaluated that the disclosure requirements

requiring non-controlling interest as a separate item in the consolidated financial

statements has impact on the overall consolidation process.

9CORPORATE AND FINANCIAL ACCOUNTING

Reference List:

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism

on corporate investment during the global financial crisis. Journal of Business

Finance & Accounting, 43(5-6), pp.513-542.

Bushman, R.M., 2014. Thoughts on financial accounting and the banking

industry. Journal of Accounting and Economics, 58(2-3), pp.384-395.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach.

Cengage learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals

of corporate finance (No. 2nd Eu). McGraw Hill.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting,

Binder Ready Version. John Wiley & Sons.

Reference List:

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism

on corporate investment during the global financial crisis. Journal of Business

Finance & Accounting, 43(5-6), pp.513-542.

Bushman, R.M., 2014. Thoughts on financial accounting and the banking

industry. Journal of Accounting and Economics, 58(2-3), pp.384-395.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach.

Cengage learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals

of corporate finance (No. 2nd Eu). McGraw Hill.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting,

Binder Ready Version. John Wiley & Sons.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE AND FINANCIAL ACCOUNTING

Legislation.gov.au., 2019. AASB 127 - Consolidated and Separate Financial

Statements - July 2004. [online] Available at:

https://www.legislation.gov.au/Details/F2009C01112 [Accessed 4 May 2019].

Mitchell, R.K., Van Buren III, H.J., Greenwood, M. and Freeman, R.E., 2015.

Stakeholder inclusion and accounting for stakeholders. Journal of Management

Studies, 52(7), pp.851-877.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Legislation.gov.au., 2019. AASB 127 - Consolidated and Separate Financial

Statements - July 2004. [online] Available at:

https://www.legislation.gov.au/Details/F2009C01112 [Accessed 4 May 2019].

Mitchell, R.K., Van Buren III, H.J., Greenwood, M. and Freeman, R.E., 2015.

Stakeholder inclusion and accounting for stakeholders. Journal of Management

Studies, 52(7), pp.851-877.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.