Corporate and Financial Accounting: Takeover and Consolidation Report

VerifiedAdded on 2023/04/04

|11

|2780

|214

Report

AI Summary

This report delves into the core concepts of corporate and financial accounting, primarily focusing on business combinations and the application of equity and consolidation accounting methods. The report provides a clear distinction between asset acquisition and business combination, outlining the procedures and considerations required under AASB 3. It illustrates equity accounting, emphasizing significant influence and the treatment of investments in associates. The report further elucidates consolidation accounting, highlighting the parent-subsidiary relationship and the preparation of consolidated financial statements. It presents the differences between equity and consolidation accounting, and addresses the treatment of intra-group transactions, including profit allocation in upstream sales, and the principles relating to non-controlling interest (NCI) and disclosure requirements. Finally, the report discusses issues encountered in the consolidation process, particularly concerning the transition from equity to consolidation accounting, providing a thorough understanding of corporate accounting principles.

Running Head: Corporate and Financial Accounting

Corporate and Financial Accounting

Corporate and Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

Contents

Executive Summary.......................................................................................................................................2

Introduction.....................................................................................................................................................2

Equity Accounting and Consolidation Accounting.....................................................................................2

Equity Accounting......................................................................................................................................3

Consolidation Accounting.........................................................................................................................4

Difference between Equity Accounting and Consolidation Accounting..............................................5

Treatment of Intra-group Transactions and Profit Allocation...................................................................5

Disclosure requirements of Non-controlling Interest.................................................................................7

Issues in the Consolidation Process...........................................................................................................7

Conclusion......................................................................................................................................................9

References...................................................................................................................................................10

1

Contents

Executive Summary.......................................................................................................................................2

Introduction.....................................................................................................................................................2

Equity Accounting and Consolidation Accounting.....................................................................................2

Equity Accounting......................................................................................................................................3

Consolidation Accounting.........................................................................................................................4

Difference between Equity Accounting and Consolidation Accounting..............................................5

Treatment of Intra-group Transactions and Profit Allocation...................................................................5

Disclosure requirements of Non-controlling Interest.................................................................................7

Issues in the Consolidation Process...........................................................................................................7

Conclusion......................................................................................................................................................9

References...................................................................................................................................................10

1

Corporate and Financial Accounting

Executive Summary

This report is prepared to seek clarity between the business combination and simple asset

acquisition. The report also outlines the two important acquisition methods which include

equity accounting and consolidation accounting. These methods are properly explained by

applying both the methods in two companies namely JKY Ltd and FAB ltd. Apart from this,

the reader will know how intra-group transactions are treated and how the profit is

allocated in such cases. Then significant principles relating to Non-controlling interest

(NCI) and disclosure requirements of NCI are studied. At the end, the main issues which

arise out of the consolidation process are discussed.

Introduction

For every company, the preparing and presenting the financial statements is a vital portion

which could never be ignored. The listed companies have to prepare their financial

statements according to the accounting standards. However, the practice of maintaining

and preparing financial statements become easy for the companies which do not hold any

subsidiary company or holds even a certain amount of share in another company. For the

companies who hold a substantial interest in other companies are required to meet certain

guidelines at the time of preparing and reporting their financial performance through the

financial statements. Such companies have to opt for making consolidated financial

statements wherein the accounting method is little different than that of simple accounting.

Equity Accounting and Consolidation Accounting

Before moving ahead with any transaction or event, JKY Ltd is required to confirm whether

the plan of acquiring FAB ltd satisfies the condition of being a business combination as per

AASB 3: Business Combination. As per AASB 3, when assets and liabilities acquired and

assumed respectively actually forms the business then only such transaction or event is

considered as a business combination, otherwise if a firm simply acquires the asset then it

is considered as an asset acquisition. For a proper business acquisition, JKY Ltd needs to

identify themselves as an acquirer and then a specific acquiring date of the acquiree

2

Executive Summary

This report is prepared to seek clarity between the business combination and simple asset

acquisition. The report also outlines the two important acquisition methods which include

equity accounting and consolidation accounting. These methods are properly explained by

applying both the methods in two companies namely JKY Ltd and FAB ltd. Apart from this,

the reader will know how intra-group transactions are treated and how the profit is

allocated in such cases. Then significant principles relating to Non-controlling interest

(NCI) and disclosure requirements of NCI are studied. At the end, the main issues which

arise out of the consolidation process are discussed.

Introduction

For every company, the preparing and presenting the financial statements is a vital portion

which could never be ignored. The listed companies have to prepare their financial

statements according to the accounting standards. However, the practice of maintaining

and preparing financial statements become easy for the companies which do not hold any

subsidiary company or holds even a certain amount of share in another company. For the

companies who hold a substantial interest in other companies are required to meet certain

guidelines at the time of preparing and reporting their financial performance through the

financial statements. Such companies have to opt for making consolidated financial

statements wherein the accounting method is little different than that of simple accounting.

Equity Accounting and Consolidation Accounting

Before moving ahead with any transaction or event, JKY Ltd is required to confirm whether

the plan of acquiring FAB ltd satisfies the condition of being a business combination as per

AASB 3: Business Combination. As per AASB 3, when assets and liabilities acquired and

assumed respectively actually forms the business then only such transaction or event is

considered as a business combination, otherwise if a firm simply acquires the asset then it

is considered as an asset acquisition. For a proper business acquisition, JKY Ltd needs to

identify themselves as an acquirer and then a specific acquiring date of the acquiree

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting

needs to be determined by the JKY Ltd (acquirer). On the date of acquisition all the assets,

liabilities and other non-controlling interest in the acquiree (FABLtd.) are need to be

recognised however, goodwill is not required to be recognised. At last goodwill or gain

earned from the bargain purchase must be recognised. Goodwill amount is recognised

when the sum of consideration transferred, the amount relating to acquiree’s non-

controlling interest and the business combination realized in phases exceed the

recognised amount on the acquisition date of the acquired identifiable assets and liabilities

assumed and vice-versa in case of bargain purchase (AASB 3, 2015).

There are usually two preferably methods of accounting:

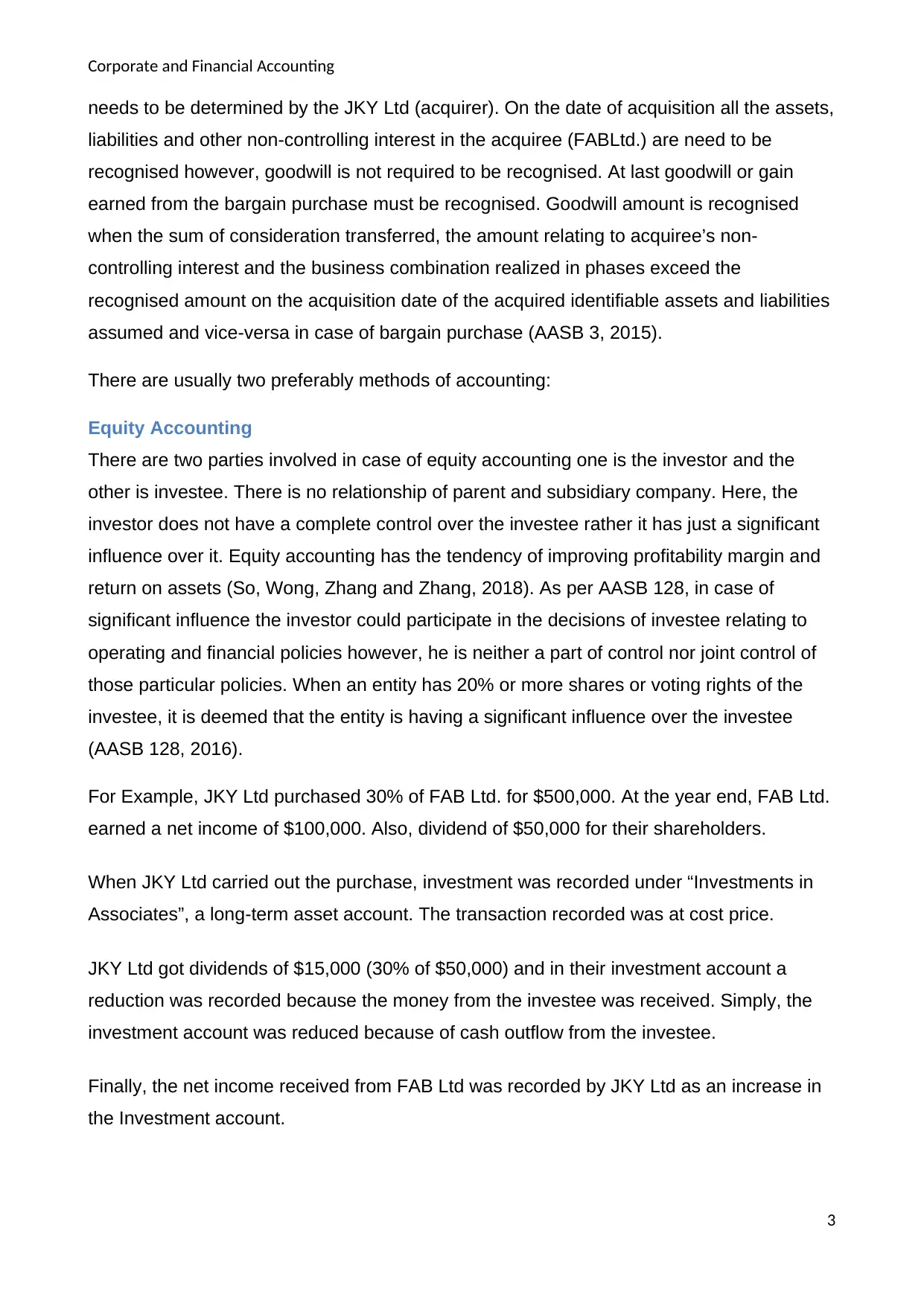

Equity Accounting

There are two parties involved in case of equity accounting one is the investor and the

other is investee. There is no relationship of parent and subsidiary company. Here, the

investor does not have a complete control over the investee rather it has just a significant

influence over it. Equity accounting has the tendency of improving profitability margin and

return on assets (So, Wong, Zhang and Zhang, 2018). As per AASB 128, in case of

significant influence the investor could participate in the decisions of investee relating to

operating and financial policies however, he is neither a part of control nor joint control of

those particular policies. When an entity has 20% or more shares or voting rights of the

investee, it is deemed that the entity is having a significant influence over the investee

(AASB 128, 2016).

For Example, JKY Ltd purchased 30% of FAB Ltd. for $500,000. At the year end, FAB Ltd.

earned a net income of $100,000. Also, dividend of $50,000 for their shareholders.

When JKY Ltd carried out the purchase, investment was recorded under “Investments in

Associates”, a long-term asset account. The transaction recorded was at cost price.

JKY Ltd got dividends of $15,000 (30% of $50,000) and in their investment account a

reduction was recorded because the money from the investee was received. Simply, the

investment account was reduced because of cash outflow from the investee.

Finally, the net income received from FAB Ltd was recorded by JKY Ltd as an increase in

the Investment account.

3

needs to be determined by the JKY Ltd (acquirer). On the date of acquisition all the assets,

liabilities and other non-controlling interest in the acquiree (FABLtd.) are need to be

recognised however, goodwill is not required to be recognised. At last goodwill or gain

earned from the bargain purchase must be recognised. Goodwill amount is recognised

when the sum of consideration transferred, the amount relating to acquiree’s non-

controlling interest and the business combination realized in phases exceed the

recognised amount on the acquisition date of the acquired identifiable assets and liabilities

assumed and vice-versa in case of bargain purchase (AASB 3, 2015).

There are usually two preferably methods of accounting:

Equity Accounting

There are two parties involved in case of equity accounting one is the investor and the

other is investee. There is no relationship of parent and subsidiary company. Here, the

investor does not have a complete control over the investee rather it has just a significant

influence over it. Equity accounting has the tendency of improving profitability margin and

return on assets (So, Wong, Zhang and Zhang, 2018). As per AASB 128, in case of

significant influence the investor could participate in the decisions of investee relating to

operating and financial policies however, he is neither a part of control nor joint control of

those particular policies. When an entity has 20% or more shares or voting rights of the

investee, it is deemed that the entity is having a significant influence over the investee

(AASB 128, 2016).

For Example, JKY Ltd purchased 30% of FAB Ltd. for $500,000. At the year end, FAB Ltd.

earned a net income of $100,000. Also, dividend of $50,000 for their shareholders.

When JKY Ltd carried out the purchase, investment was recorded under “Investments in

Associates”, a long-term asset account. The transaction recorded was at cost price.

JKY Ltd got dividends of $15,000 (30% of $50,000) and in their investment account a

reduction was recorded because the money from the investee was received. Simply, the

investment account was reduced because of cash outflow from the investee.

Finally, the net income received from FAB Ltd was recorded by JKY Ltd as an increase in

the Investment account.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

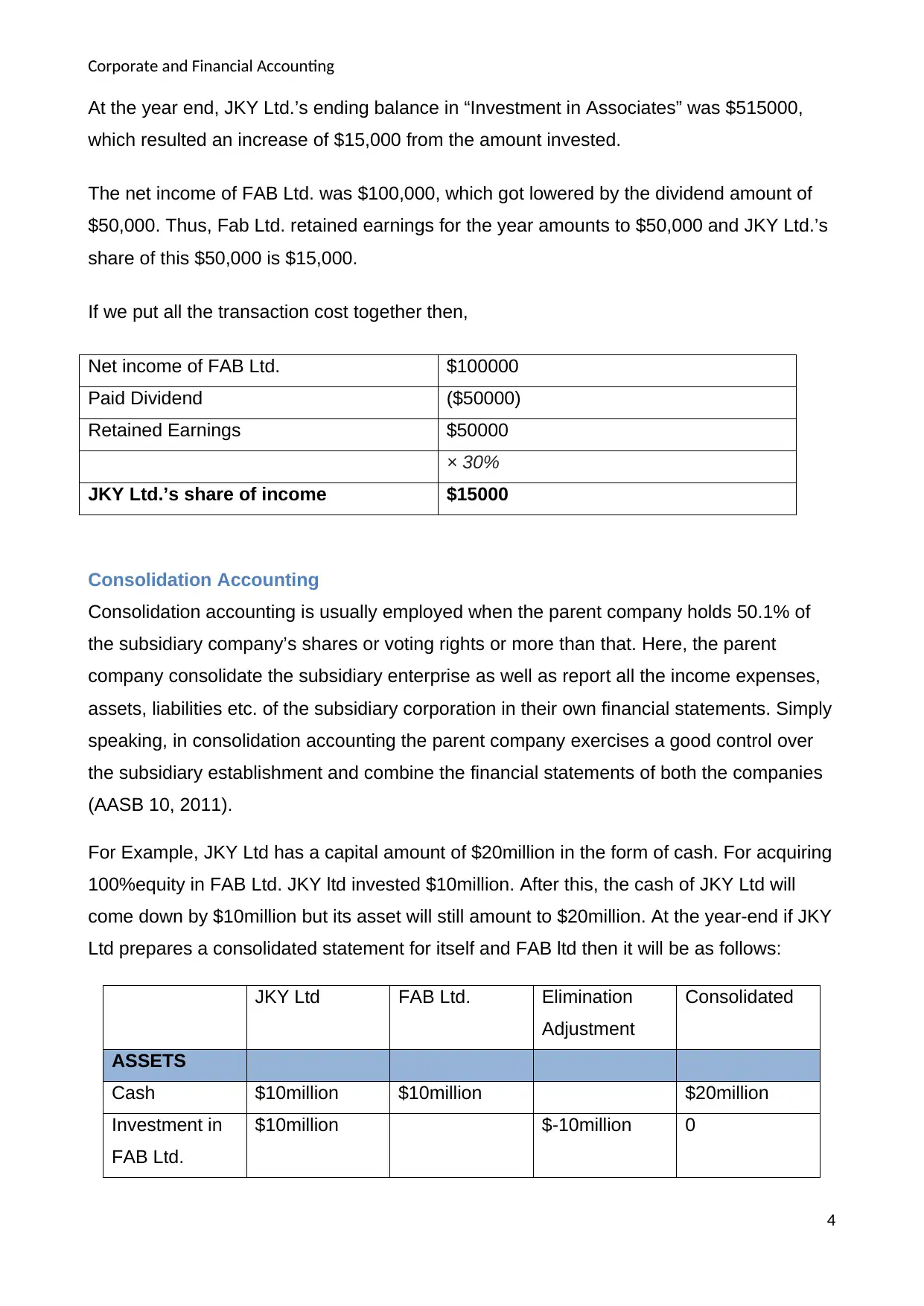

At the year end, JKY Ltd.’s ending balance in “Investment in Associates” was $515000,

which resulted an increase of $15,000 from the amount invested.

The net income of FAB Ltd. was $100,000, which got lowered by the dividend amount of

$50,000. Thus, Fab Ltd. retained earnings for the year amounts to $50,000 and JKY Ltd.’s

share of this $50,000 is $15,000.

If we put all the transaction cost together then,

Net income of FAB Ltd. $100000

Paid Dividend ($50000)

Retained Earnings $50000

× 30%

JKY Ltd.’s share of income $15000

Consolidation Accounting

Consolidation accounting is usually employed when the parent company holds 50.1% of

the subsidiary company’s shares or voting rights or more than that. Here, the parent

company consolidate the subsidiary enterprise as well as report all the income expenses,

assets, liabilities etc. of the subsidiary corporation in their own financial statements. Simply

speaking, in consolidation accounting the parent company exercises a good control over

the subsidiary establishment and combine the financial statements of both the companies

(AASB 10, 2011).

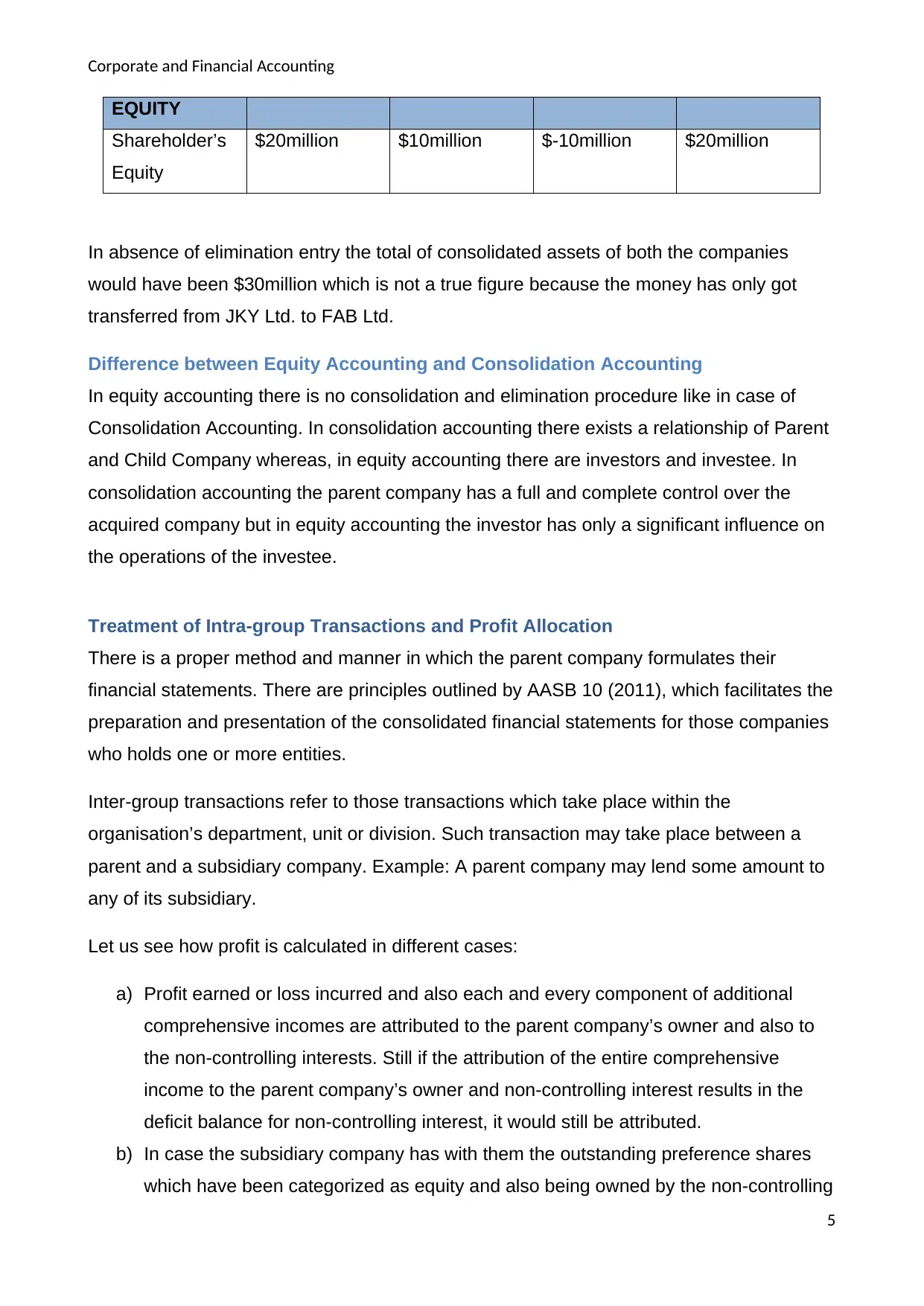

For Example, JKY Ltd has a capital amount of $20million in the form of cash. For acquiring

100%equity in FAB Ltd. JKY ltd invested $10million. After this, the cash of JKY Ltd will

come down by $10million but its asset will still amount to $20million. At the year-end if JKY

Ltd prepares a consolidated statement for itself and FAB ltd then it will be as follows:

JKY Ltd FAB Ltd. Elimination

Adjustment

Consolidated

ASSETS

Cash $10million $10million $20million

Investment in

FAB Ltd.

$10million $-10million 0

4

At the year end, JKY Ltd.’s ending balance in “Investment in Associates” was $515000,

which resulted an increase of $15,000 from the amount invested.

The net income of FAB Ltd. was $100,000, which got lowered by the dividend amount of

$50,000. Thus, Fab Ltd. retained earnings for the year amounts to $50,000 and JKY Ltd.’s

share of this $50,000 is $15,000.

If we put all the transaction cost together then,

Net income of FAB Ltd. $100000

Paid Dividend ($50000)

Retained Earnings $50000

× 30%

JKY Ltd.’s share of income $15000

Consolidation Accounting

Consolidation accounting is usually employed when the parent company holds 50.1% of

the subsidiary company’s shares or voting rights or more than that. Here, the parent

company consolidate the subsidiary enterprise as well as report all the income expenses,

assets, liabilities etc. of the subsidiary corporation in their own financial statements. Simply

speaking, in consolidation accounting the parent company exercises a good control over

the subsidiary establishment and combine the financial statements of both the companies

(AASB 10, 2011).

For Example, JKY Ltd has a capital amount of $20million in the form of cash. For acquiring

100%equity in FAB Ltd. JKY ltd invested $10million. After this, the cash of JKY Ltd will

come down by $10million but its asset will still amount to $20million. At the year-end if JKY

Ltd prepares a consolidated statement for itself and FAB ltd then it will be as follows:

JKY Ltd FAB Ltd. Elimination

Adjustment

Consolidated

ASSETS

Cash $10million $10million $20million

Investment in

FAB Ltd.

$10million $-10million 0

4

Corporate and Financial Accounting

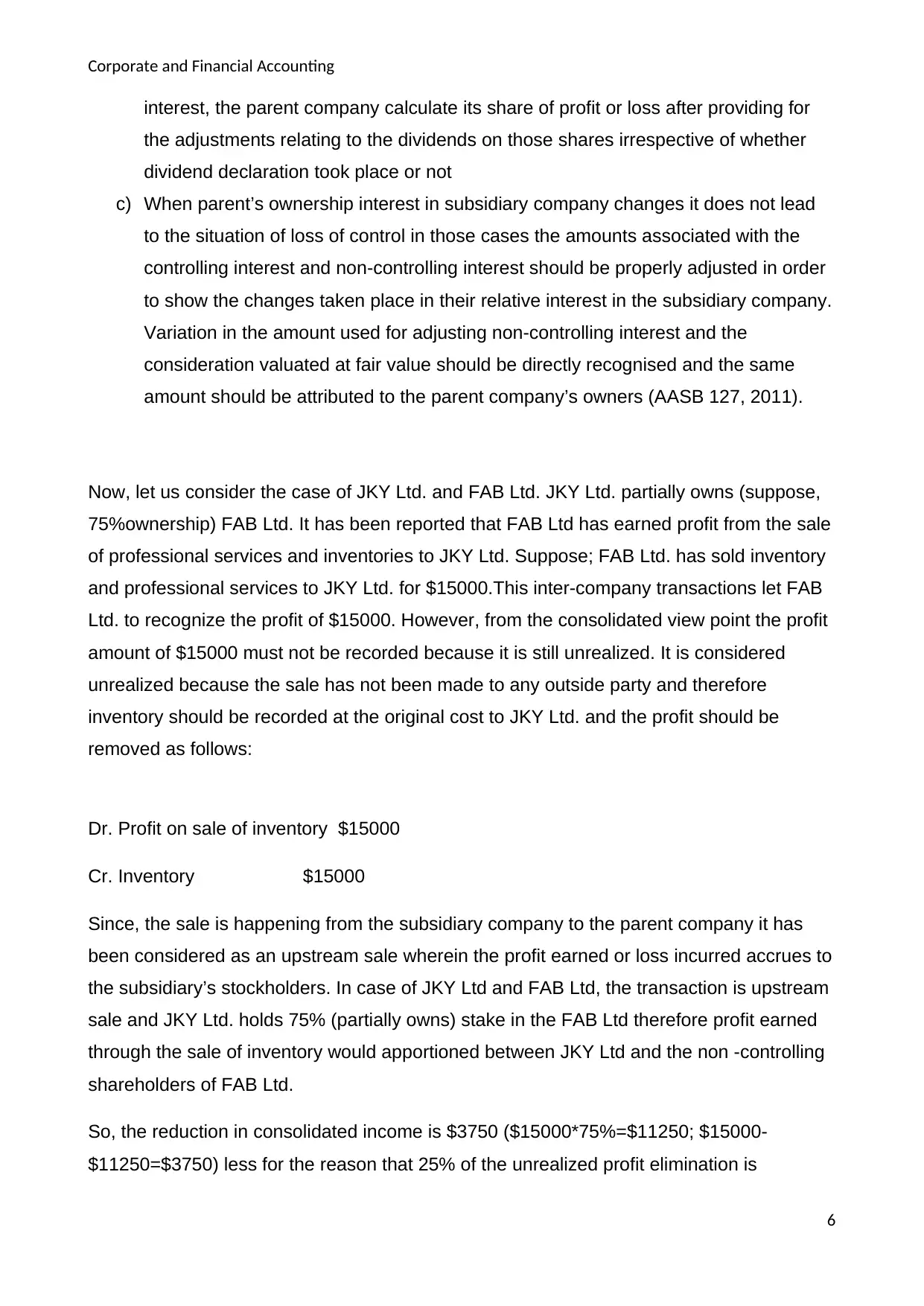

EQUITY

Shareholder’s

Equity

$20million $10million $-10million $20million

In absence of elimination entry the total of consolidated assets of both the companies

would have been $30million which is not a true figure because the money has only got

transferred from JKY Ltd. to FAB Ltd.

Difference between Equity Accounting and Consolidation Accounting

In equity accounting there is no consolidation and elimination procedure like in case of

Consolidation Accounting. In consolidation accounting there exists a relationship of Parent

and Child Company whereas, in equity accounting there are investors and investee. In

consolidation accounting the parent company has a full and complete control over the

acquired company but in equity accounting the investor has only a significant influence on

the operations of the investee.

Treatment of Intra-group Transactions and Profit Allocation

There is a proper method and manner in which the parent company formulates their

financial statements. There are principles outlined by AASB 10 (2011), which facilitates the

preparation and presentation of the consolidated financial statements for those companies

who holds one or more entities.

Inter-group transactions refer to those transactions which take place within the

organisation’s department, unit or division. Such transaction may take place between a

parent and a subsidiary company. Example: A parent company may lend some amount to

any of its subsidiary.

Let us see how profit is calculated in different cases:

a) Profit earned or loss incurred and also each and every component of additional

comprehensive incomes are attributed to the parent company’s owner and also to

the non-controlling interests. Still if the attribution of the entire comprehensive

income to the parent company’s owner and non-controlling interest results in the

deficit balance for non-controlling interest, it would still be attributed.

b) In case the subsidiary company has with them the outstanding preference shares

which have been categorized as equity and also being owned by the non-controlling

5

EQUITY

Shareholder’s

Equity

$20million $10million $-10million $20million

In absence of elimination entry the total of consolidated assets of both the companies

would have been $30million which is not a true figure because the money has only got

transferred from JKY Ltd. to FAB Ltd.

Difference between Equity Accounting and Consolidation Accounting

In equity accounting there is no consolidation and elimination procedure like in case of

Consolidation Accounting. In consolidation accounting there exists a relationship of Parent

and Child Company whereas, in equity accounting there are investors and investee. In

consolidation accounting the parent company has a full and complete control over the

acquired company but in equity accounting the investor has only a significant influence on

the operations of the investee.

Treatment of Intra-group Transactions and Profit Allocation

There is a proper method and manner in which the parent company formulates their

financial statements. There are principles outlined by AASB 10 (2011), which facilitates the

preparation and presentation of the consolidated financial statements for those companies

who holds one or more entities.

Inter-group transactions refer to those transactions which take place within the

organisation’s department, unit or division. Such transaction may take place between a

parent and a subsidiary company. Example: A parent company may lend some amount to

any of its subsidiary.

Let us see how profit is calculated in different cases:

a) Profit earned or loss incurred and also each and every component of additional

comprehensive incomes are attributed to the parent company’s owner and also to

the non-controlling interests. Still if the attribution of the entire comprehensive

income to the parent company’s owner and non-controlling interest results in the

deficit balance for non-controlling interest, it would still be attributed.

b) In case the subsidiary company has with them the outstanding preference shares

which have been categorized as equity and also being owned by the non-controlling

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting

interest, the parent company calculate its share of profit or loss after providing for

the adjustments relating to the dividends on those shares irrespective of whether

dividend declaration took place or not

c) When parent’s ownership interest in subsidiary company changes it does not lead

to the situation of loss of control in those cases the amounts associated with the

controlling interest and non-controlling interest should be properly adjusted in order

to show the changes taken place in their relative interest in the subsidiary company.

Variation in the amount used for adjusting non-controlling interest and the

consideration valuated at fair value should be directly recognised and the same

amount should be attributed to the parent company’s owners (AASB 127, 2011).

Now, let us consider the case of JKY Ltd. and FAB Ltd. JKY Ltd. partially owns (suppose,

75%ownership) FAB Ltd. It has been reported that FAB Ltd has earned profit from the sale

of professional services and inventories to JKY Ltd. Suppose; FAB Ltd. has sold inventory

and professional services to JKY Ltd. for $15000.This inter-company transactions let FAB

Ltd. to recognize the profit of $15000. However, from the consolidated view point the profit

amount of $15000 must not be recorded because it is still unrealized. It is considered

unrealized because the sale has not been made to any outside party and therefore

inventory should be recorded at the original cost to JKY Ltd. and the profit should be

removed as follows:

Dr. Profit on sale of inventory $15000

Cr. Inventory $15000

Since, the sale is happening from the subsidiary company to the parent company it has

been considered as an upstream sale wherein the profit earned or loss incurred accrues to

the subsidiary’s stockholders. In case of JKY Ltd and FAB Ltd, the transaction is upstream

sale and JKY Ltd. holds 75% (partially owns) stake in the FAB Ltd therefore profit earned

through the sale of inventory would apportioned between JKY Ltd and the non -controlling

shareholders of FAB Ltd.

So, the reduction in consolidated income is $3750 ($15000*75%=$11250; $15000-

$11250=$3750) less for the reason that 25% of the unrealized profit elimination is

6

interest, the parent company calculate its share of profit or loss after providing for

the adjustments relating to the dividends on those shares irrespective of whether

dividend declaration took place or not

c) When parent’s ownership interest in subsidiary company changes it does not lead

to the situation of loss of control in those cases the amounts associated with the

controlling interest and non-controlling interest should be properly adjusted in order

to show the changes taken place in their relative interest in the subsidiary company.

Variation in the amount used for adjusting non-controlling interest and the

consideration valuated at fair value should be directly recognised and the same

amount should be attributed to the parent company’s owners (AASB 127, 2011).

Now, let us consider the case of JKY Ltd. and FAB Ltd. JKY Ltd. partially owns (suppose,

75%ownership) FAB Ltd. It has been reported that FAB Ltd has earned profit from the sale

of professional services and inventories to JKY Ltd. Suppose; FAB Ltd. has sold inventory

and professional services to JKY Ltd. for $15000.This inter-company transactions let FAB

Ltd. to recognize the profit of $15000. However, from the consolidated view point the profit

amount of $15000 must not be recorded because it is still unrealized. It is considered

unrealized because the sale has not been made to any outside party and therefore

inventory should be recorded at the original cost to JKY Ltd. and the profit should be

removed as follows:

Dr. Profit on sale of inventory $15000

Cr. Inventory $15000

Since, the sale is happening from the subsidiary company to the parent company it has

been considered as an upstream sale wherein the profit earned or loss incurred accrues to

the subsidiary’s stockholders. In case of JKY Ltd and FAB Ltd, the transaction is upstream

sale and JKY Ltd. holds 75% (partially owns) stake in the FAB Ltd therefore profit earned

through the sale of inventory would apportioned between JKY Ltd and the non -controlling

shareholders of FAB Ltd.

So, the reduction in consolidated income is $3750 ($15000*75%=$11250; $15000-

$11250=$3750) less for the reason that 25% of the unrealized profit elimination is

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

subtracted from the non-controlling interest instead of deducting the full amount from the

controlling interest.

Disclosure requirements of Non-controlling Interest

As per AASB 101:

1. The financial statement of position shall include the line items that should include the

amount of many items along with the amount associated with Non-controlling interest

presented under the head equity.

2. In the financial statement a company shall present profit earned or loss incurred

attributable to the NCI and Parent company’s owner. It should also mention the

comprehensive income eligible to get attributed to NCI and parent company’s owner

(AASB 201, 2015).

The following steps are involved at the time of preparing consolidated financial statements:

d) The carrying sum of investment made by the parent company in each of its’

subsidiary entity and equity part of each subsidiary of parent company are removed

or eliminated.

e) Identification of non-controlling interest in the subsidiaries’ profit and loss for the

period of reporting

f) Parent company’s ownership interest in the net assets of the subsidiary company

are identified distinctly from the non-controlling interest in the same net assets of

the consolidated subsidiary

g) Non- controlling interest should be shown separately in the consolidated financial

statements under the head equity however separated from the equity of the

proprietors of the parent company

Issues in the Consolidation Process

1. Acquisition from non-control to control: It happens when a change happens in the

control and ownership during the year and at the year-end parent company holds

the subsidiary. Simply, it is about shifting from equity accounting to consolidation or

acquisition accounting.

7

subtracted from the non-controlling interest instead of deducting the full amount from the

controlling interest.

Disclosure requirements of Non-controlling Interest

As per AASB 101:

1. The financial statement of position shall include the line items that should include the

amount of many items along with the amount associated with Non-controlling interest

presented under the head equity.

2. In the financial statement a company shall present profit earned or loss incurred

attributable to the NCI and Parent company’s owner. It should also mention the

comprehensive income eligible to get attributed to NCI and parent company’s owner

(AASB 201, 2015).

The following steps are involved at the time of preparing consolidated financial statements:

d) The carrying sum of investment made by the parent company in each of its’

subsidiary entity and equity part of each subsidiary of parent company are removed

or eliminated.

e) Identification of non-controlling interest in the subsidiaries’ profit and loss for the

period of reporting

f) Parent company’s ownership interest in the net assets of the subsidiary company

are identified distinctly from the non-controlling interest in the same net assets of

the consolidated subsidiary

g) Non- controlling interest should be shown separately in the consolidated financial

statements under the head equity however separated from the equity of the

proprietors of the parent company

Issues in the Consolidation Process

1. Acquisition from non-control to control: It happens when a change happens in the

control and ownership during the year and at the year-end parent company holds

the subsidiary. Simply, it is about shifting from equity accounting to consolidation or

acquisition accounting.

7

Corporate and Financial Accounting

Example: Assume, JKY Ltd goes for equity accounting and holds 30% share in FAB

Ltd. during the year and then at the year-end converts to consolidation accounting and

as a result holds 80%share in the FAB ltd.

In consolidated income statement non-controlling interest would be introduced. From

the year start till the date of consolidation taking place at the end of the year will be

accounted for FAB Ltd. as per equity accounting. At this step the profit earned by FAB

ltd. will be pro-rated and then the group share is taken. JKY Ltd will consider profit after

tax earned after the acquisition date. However, intra-group transactions will be

eliminated completely. Non-controlling interest will be introduced with an aim of post-

acquisition element. The original profit or loss will be determined after disposing JKY

Ltd.’s original share of 30% and remeasuring to fair value.

In consolidated statement of financial position when JKY Ltd. owns 80% share in FAB

Ltd., goodwill of JKY Ltd. would be calculated and on the basis of 20%holding non-

controlling interest would be calculated at the end of the year.

2. Acquisition from control to control: It happens when there is an increase in the

control and ownership during the year and at the year-end. Here, the parent firm

owns a greater share of the net assets of subsidiary company.

Example: JKY ltd. now holds 80% share whereas it originally held 60% share in

FAB Ltd.

In consolidated income statement non-controlling interest would come down. Before

acquisition also JKY Ltd. was consolidating line by line to Profit after tax and will still

move in the same way. For the Non-controlling interest, profit would be prorated in

order to show the decrease in the holding of non-controlling interest. There would

be no profit or loss associated with the disposal.

In consolidated statement of financial position when JKY Ltd. holds 80% share in

FAB Ltd. The net assets would be consolidated line by line as it was carried out

when JKY Ltd. had 60% holding. There would not be any changes in goodwill. Now

the transfer would take place between Non-Controlling Interest and equity as a

result the share of NCI would be only 20% of net assets.

8

Example: Assume, JKY Ltd goes for equity accounting and holds 30% share in FAB

Ltd. during the year and then at the year-end converts to consolidation accounting and

as a result holds 80%share in the FAB ltd.

In consolidated income statement non-controlling interest would be introduced. From

the year start till the date of consolidation taking place at the end of the year will be

accounted for FAB Ltd. as per equity accounting. At this step the profit earned by FAB

ltd. will be pro-rated and then the group share is taken. JKY Ltd will consider profit after

tax earned after the acquisition date. However, intra-group transactions will be

eliminated completely. Non-controlling interest will be introduced with an aim of post-

acquisition element. The original profit or loss will be determined after disposing JKY

Ltd.’s original share of 30% and remeasuring to fair value.

In consolidated statement of financial position when JKY Ltd. owns 80% share in FAB

Ltd., goodwill of JKY Ltd. would be calculated and on the basis of 20%holding non-

controlling interest would be calculated at the end of the year.

2. Acquisition from control to control: It happens when there is an increase in the

control and ownership during the year and at the year-end. Here, the parent firm

owns a greater share of the net assets of subsidiary company.

Example: JKY ltd. now holds 80% share whereas it originally held 60% share in

FAB Ltd.

In consolidated income statement non-controlling interest would come down. Before

acquisition also JKY Ltd. was consolidating line by line to Profit after tax and will still

move in the same way. For the Non-controlling interest, profit would be prorated in

order to show the decrease in the holding of non-controlling interest. There would

be no profit or loss associated with the disposal.

In consolidated statement of financial position when JKY Ltd. holds 80% share in

FAB Ltd. The net assets would be consolidated line by line as it was carried out

when JKY Ltd. had 60% holding. There would not be any changes in goodwill. Now

the transfer would take place between Non-Controlling Interest and equity as a

result the share of NCI would be only 20% of net assets.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting

3. Disposal at the time loss of control: It happens when there is a decrease in the

ownership during the year and at the year end the parent company becomes an

associate company.

Example: Originally, JKY Ltd. held 80% shares in Fab Ltd. But now JKY Ltd. sold

out 50% shares as a result it would be left with only 30% shares in FAB Ltd. Here,

JKY Ltd. becomes associate of FAB Ltd.

In consolidated income statement the non-controlling interest would be reflected

only for the time FAB Ltd. was the subsidiary company of JKY Ltd. PAT would be

consolidated line by line till the time there was a loss of control. Till the date of

disposal the amount for NCI would be computed. After the operating profit under the

head of exceptional item, mention the amount of gain or loss happened to JKY Ltd.

In consolidated statement of financial position the net assets of JKY Ltd. and FAB

ltd. would no longer be added together as a result of loss of control. Under non-

current asset there should be an addition of line speaking about investment in the

FAB Ltd. This amount should be calculated at the fair value on the disposal date.

Both goodwill and NCI should not be mentioned anywhere (Chartered Institute of

Management Accountants, 2012).

Conclusion

At the end, we know that when the assets and liabilities acquired by any company forms a

business then only it could be considered as a business combination otherwise it would be

a simple asset acquisition. Apart from this, we now know that when a company holds 20%

or more shares in another company then it has a significant influence over it and the

relationship shared in such cases is of investor and investee. In case, the company holds

more than 50% shares then it becomes the parent company of the company in which it

holds the share. At the end we are well versed with different acquisition methods, the intra

group transactions and non-controlling interests.

9

3. Disposal at the time loss of control: It happens when there is a decrease in the

ownership during the year and at the year end the parent company becomes an

associate company.

Example: Originally, JKY Ltd. held 80% shares in Fab Ltd. But now JKY Ltd. sold

out 50% shares as a result it would be left with only 30% shares in FAB Ltd. Here,

JKY Ltd. becomes associate of FAB Ltd.

In consolidated income statement the non-controlling interest would be reflected

only for the time FAB Ltd. was the subsidiary company of JKY Ltd. PAT would be

consolidated line by line till the time there was a loss of control. Till the date of

disposal the amount for NCI would be computed. After the operating profit under the

head of exceptional item, mention the amount of gain or loss happened to JKY Ltd.

In consolidated statement of financial position the net assets of JKY Ltd. and FAB

ltd. would no longer be added together as a result of loss of control. Under non-

current asset there should be an addition of line speaking about investment in the

FAB Ltd. This amount should be calculated at the fair value on the disposal date.

Both goodwill and NCI should not be mentioned anywhere (Chartered Institute of

Management Accountants, 2012).

Conclusion

At the end, we know that when the assets and liabilities acquired by any company forms a

business then only it could be considered as a business combination otherwise it would be

a simple asset acquisition. Apart from this, we now know that when a company holds 20%

or more shares in another company then it has a significant influence over it and the

relationship shared in such cases is of investor and investee. In case, the company holds

more than 50% shares then it becomes the parent company of the company in which it

holds the share. At the end we are well versed with different acquisition methods, the intra

group transactions and non-controlling interests.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

References

AASB 3.(2015). Business Combinations. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf.

AASB 10.(2011). Consolidated Financial Statements. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf.

AASB 101.(2015). Presentation of Financial Statements. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf.

AASB 127.(2011). Consolidated and Separate Financial Statements. Available 30 May,

2019 https://www.aasb.gov.au/admin/file/content105/c9/AASB127_03-08_COMPjul11_07-

11.pdf.

AASB 128.(2016). Investments in Associates and Joint Ventures. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-15_COMPdec15_01-

18.pdf.

Chartered Institute of Management Accountants.(2012). Principles of Management

Accounting. Available 30 May, 2019 http://www.cimaglobal.com/Pages-that-we-will-need-

to-bring-back/velocity-archive/Velocity-e-magazine/Velocity-2012/Velocity-April-2012/

Principles-of-group-accounting-F2-by-Jayne-Howson/.

So, S., Wong, K.S., Zhang, F. And Zhang, X. (2018).Value Relevance of proportionate

consolidation versus the equity method: Evidence from Hong Kong. China Journal of

Accounting Research.[Online]. 11(4), p. 255-278. Available 30 May, 2019

https://www.sciencedirect.com/science/article/pii/S1755309118301321

10

References

AASB 3.(2015). Business Combinations. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf.

AASB 10.(2011). Consolidated Financial Statements. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf.

AASB 101.(2015). Presentation of Financial Statements. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf.

AASB 127.(2011). Consolidated and Separate Financial Statements. Available 30 May,

2019 https://www.aasb.gov.au/admin/file/content105/c9/AASB127_03-08_COMPjul11_07-

11.pdf.

AASB 128.(2016). Investments in Associates and Joint Ventures. Available 30 May, 2019

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-15_COMPdec15_01-

18.pdf.

Chartered Institute of Management Accountants.(2012). Principles of Management

Accounting. Available 30 May, 2019 http://www.cimaglobal.com/Pages-that-we-will-need-

to-bring-back/velocity-archive/Velocity-e-magazine/Velocity-2012/Velocity-April-2012/

Principles-of-group-accounting-F2-by-Jayne-Howson/.

So, S., Wong, K.S., Zhang, F. And Zhang, X. (2018).Value Relevance of proportionate

consolidation versus the equity method: Evidence from Hong Kong. China Journal of

Accounting Research.[Online]. 11(4), p. 255-278. Available 30 May, 2019

https://www.sciencedirect.com/science/article/pii/S1755309118301321

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.