Corporate and Financial Accounting: Takeover Decision & Consolidation

VerifiedAdded on 2023/03/23

|12

|3555

|38

Report

AI Summary

This report provides an understanding of accounting aspects related to the acquisition of FAB Limited by JKY Limited. It assesses how accounting treatments, especially concerning non-controlling interests and consolidation accounting, vary across accounting standards. The report elaborates on the methodological differences between equity accounting and consolidation accounting, focusing on recognition principles and measurement bases. It also examines the treatment of intra-group transactions in consolidated financial statements, highlighting significant variations. Furthermore, the report evaluates the impact of disclosure requirements for non-controlling interests as a distinct item in consolidated financial reports, affecting the overall consolidation process. Desklib is a platform where you can find past papers and solved assignments for students.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

sCorporate Takeover Decision Making and the Effects on Consolidation Accounting

Student Name:

Student Number:

Session Number:

sCorporate Takeover Decision Making and the Effects on Consolidation Accounting

Student Name:

Student Number:

Session Number:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary:

The report is prepared with the intent for obtaining an understanding of the various

aspects of accounting related to the acquisition of a smaller firm, which is FAB Limited

and the organisation to acquire it would be JKY Limited. It has been assessed that the

accounting treatments change considerably, particularly those associated with non-

controlling interest as well as consolidation accounting pertaining to the different

standards of accounting. When the differences between the methods of equity

accounting and consolidation accounting are evaluated in case of acquisition of a small

organisation by the parent, the principles of recognition and bases of measurement vary

from organisation to organisation. In addition, the intra-group transactions have

significant variations in terms of treatment in the consolidated financial statements of

both the firms. Finally, it has been assessed that the disclosure requirements needing

non-controlling interests in the form of a distinct item in the consolidated financial

reports has considerable effect on the entire process of consolidation.

Executive Summary:

The report is prepared with the intent for obtaining an understanding of the various

aspects of accounting related to the acquisition of a smaller firm, which is FAB Limited

and the organisation to acquire it would be JKY Limited. It has been assessed that the

accounting treatments change considerably, particularly those associated with non-

controlling interest as well as consolidation accounting pertaining to the different

standards of accounting. When the differences between the methods of equity

accounting and consolidation accounting are evaluated in case of acquisition of a small

organisation by the parent, the principles of recognition and bases of measurement vary

from organisation to organisation. In addition, the intra-group transactions have

significant variations in terms of treatment in the consolidated financial statements of

both the firms. Finally, it has been assessed that the disclosure requirements needing

non-controlling interests in the form of a distinct item in the consolidated financial

reports has considerable effect on the entire process of consolidation.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction:.......................................................................................................................3

Part A Response:...............................................................................................................3

Part B Response:...............................................................................................................5

Part C Response:..............................................................................................................7

Conclusion:........................................................................................................................8

References:......................................................................................................................10

Table of Contents

Introduction:.......................................................................................................................3

Part A Response:...............................................................................................................3

Part B Response:...............................................................................................................5

Part C Response:..............................................................................................................7

Conclusion:........................................................................................................................8

References:......................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction:

The main reason of preparing is to gain an insight of the number of accounting

aspects related to the acquisition of a smaller firm, which is FAB Limited and the

organisation to acquire it would be JKY Limited. The initial segment would elaborate the

segregation between the significant methodological differences in equity accounting and

consolidation accounting with suitable examples. The next segment would emphasise

on the doctrines of intra-group transactions along with their treatment through solved

illustrations. Finally, the paper would deal with the effect of disclosures related to non-

controlling interests as a different item in the consolidation process.

Part A Response:

Based on the provided case, it could be observed that for acquiring FAB Limited,

the management of JKY Limited is unsure regarding the selection of the strategy of

acquisition. The equity method and the consolidation method are two types of

accounting methods, which are used when two companies are parts of any joint venture

(Aletkin2014). In order to choose any one method, it relies on the techniques the

income statement and the balance sheet statement of the firm discloses the

partnerships. Thus, these methods are deemed to have significant methodological

differences and they are discussed briefly as follows:

Consolidation accounting method:

This method states that the balance sheet statement is used for recording assets

and liabilities arising from a joint venture as part of the percentage of engagement

maintained by the organisation in the venture (Atanasov and Black 2016). At the time of

calculating assets and liabilities, all expenses and income need to be listed by the firm

from acquisition and they are incorporated in the income statement as well as the

balance sheet statement. “Paragraph B86 of AASB 110” states that the consolidated

financial statements contain combined items like income, expenses, assets, liabilities,

equity and cash flows of the parent firm and its related subsidiaries (Aasb.gov.au 2019).

Moreover, it is involved in offsetting or eradicating the carrying amounts of the

investment of the main company in all subsidiaries and the part of equity that the

subsidiaries hold in the parent firm. Along with this, the method conducts elimination

adjustment for offsetting the inter-firm transactions so that there is double counting of

values at the level of consolidation.

As mentioned in “Paragraph B88 of AASB 10”, the different line items of the

measurement requirements of the financial reports are shown where income and

expenses of the subsidiaries depend on the amounts of liabilities and assets recognised

in the consolidated accounting statements at the period they are acquired. Hence, fair

values are used for gauging these items at the acquisition date. On the other hand,

“Paragraph 32 of AASB 3” requires a specific criterion for recognition of goodwill. It is

necessary for the acquirer to realise goodwill at the date of acquisition as the greater of

the two as follows:

i. The average of:

Introduction:

The main reason of preparing is to gain an insight of the number of accounting

aspects related to the acquisition of a smaller firm, which is FAB Limited and the

organisation to acquire it would be JKY Limited. The initial segment would elaborate the

segregation between the significant methodological differences in equity accounting and

consolidation accounting with suitable examples. The next segment would emphasise

on the doctrines of intra-group transactions along with their treatment through solved

illustrations. Finally, the paper would deal with the effect of disclosures related to non-

controlling interests as a different item in the consolidation process.

Part A Response:

Based on the provided case, it could be observed that for acquiring FAB Limited,

the management of JKY Limited is unsure regarding the selection of the strategy of

acquisition. The equity method and the consolidation method are two types of

accounting methods, which are used when two companies are parts of any joint venture

(Aletkin2014). In order to choose any one method, it relies on the techniques the

income statement and the balance sheet statement of the firm discloses the

partnerships. Thus, these methods are deemed to have significant methodological

differences and they are discussed briefly as follows:

Consolidation accounting method:

This method states that the balance sheet statement is used for recording assets

and liabilities arising from a joint venture as part of the percentage of engagement

maintained by the organisation in the venture (Atanasov and Black 2016). At the time of

calculating assets and liabilities, all expenses and income need to be listed by the firm

from acquisition and they are incorporated in the income statement as well as the

balance sheet statement. “Paragraph B86 of AASB 110” states that the consolidated

financial statements contain combined items like income, expenses, assets, liabilities,

equity and cash flows of the parent firm and its related subsidiaries (Aasb.gov.au 2019).

Moreover, it is involved in offsetting or eradicating the carrying amounts of the

investment of the main company in all subsidiaries and the part of equity that the

subsidiaries hold in the parent firm. Along with this, the method conducts elimination

adjustment for offsetting the inter-firm transactions so that there is double counting of

values at the level of consolidation.

As mentioned in “Paragraph B88 of AASB 10”, the different line items of the

measurement requirements of the financial reports are shown where income and

expenses of the subsidiaries depend on the amounts of liabilities and assets recognised

in the consolidated accounting statements at the period they are acquired. Hence, fair

values are used for gauging these items at the acquisition date. On the other hand,

“Paragraph 32 of AASB 3” requires a specific criterion for recognition of goodwill. It is

necessary for the acquirer to realise goodwill at the date of acquisition as the greater of

the two as follows:

i. The average of:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

The consideration transfer measured in compliance with AASB 3 needing fair

value at the time the same has been obtained

The amount related to the acquiree’s non-controlling interest gauged as per the

guideline

In case of business combination achieved in phases, the fair value of equity

interest held previously in the acquireee on the part of the acquirer at the fair

value of the date it is acquired

ii. The net of the amounts related to identifiable amounts acquired along with the

projected liabilities in accordance with the standard (Aasb.gov.au 2019)

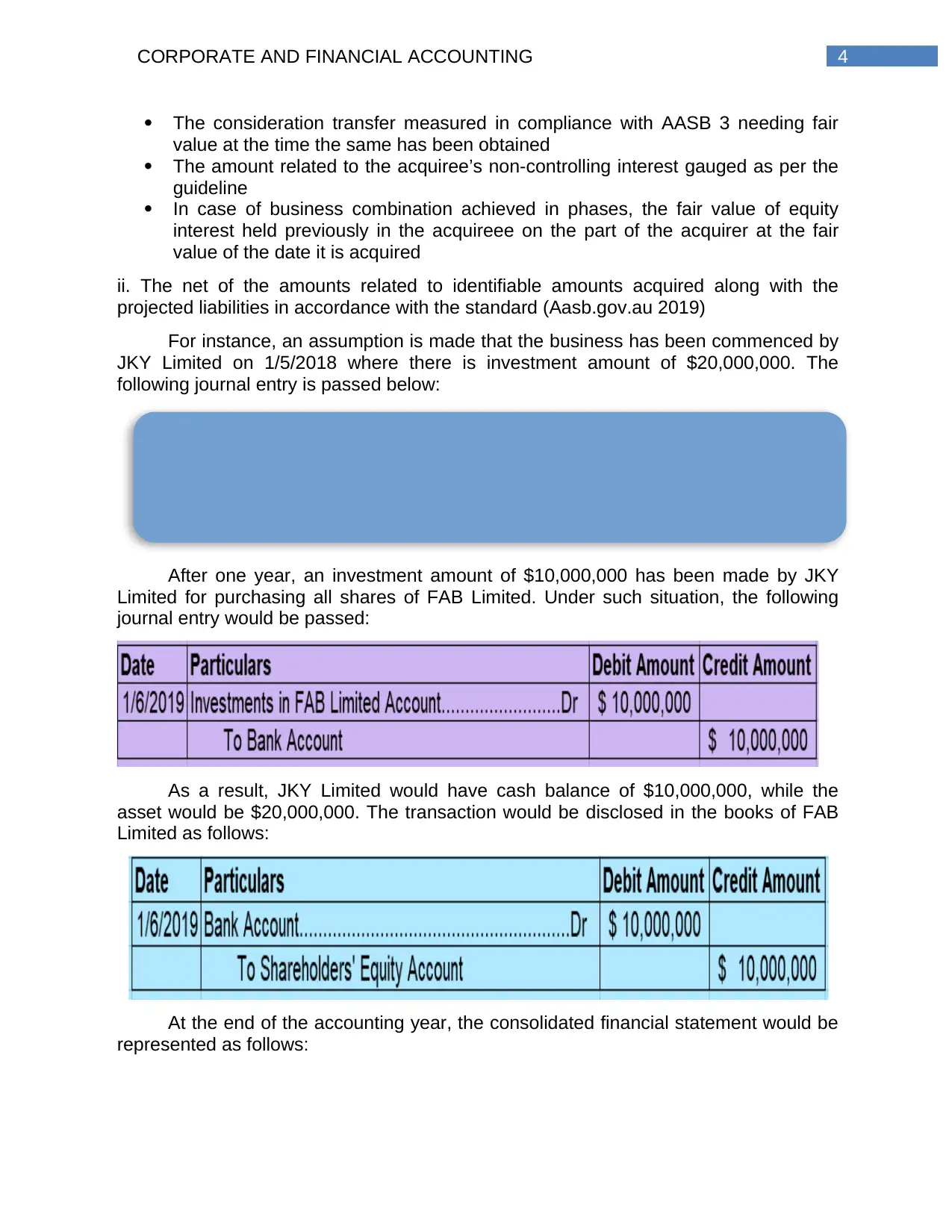

For instance, an assumption is made that the business has been commenced by

JKY Limited on 1/5/2018 where there is investment amount of $20,000,000. The

following journal entry is passed below:

After one year, an investment amount of $10,000,000 has been made by JKY

Limited for purchasing all shares of FAB Limited. Under such situation, the following

journal entry would be passed:

As a result, JKY Limited would have cash balance of $10,000,000, while the

asset would be $20,000,000. The transaction would be disclosed in the books of FAB

Limited as follows:

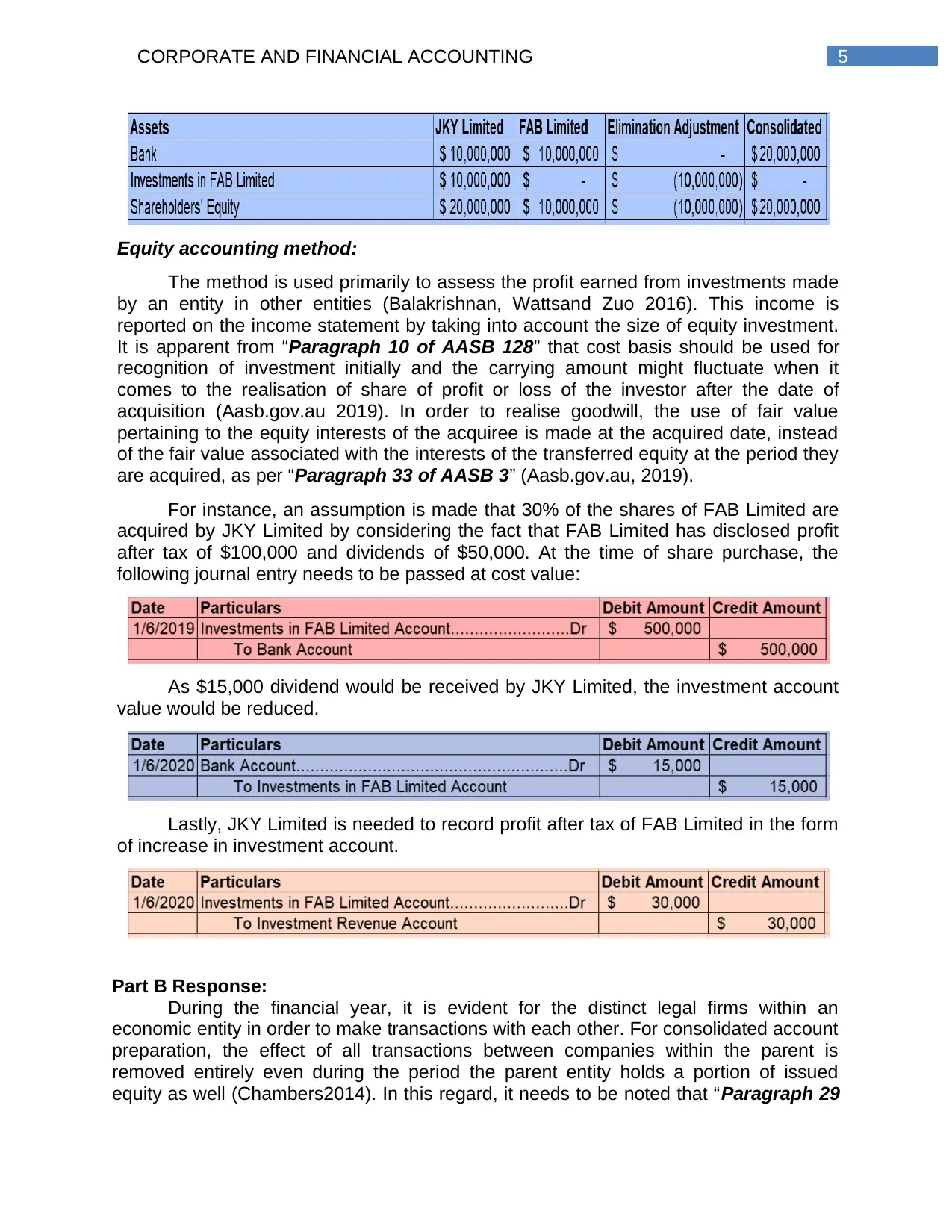

At the end of the accounting year, the consolidated financial statement would be

represented as follows:

The consideration transfer measured in compliance with AASB 3 needing fair

value at the time the same has been obtained

The amount related to the acquiree’s non-controlling interest gauged as per the

guideline

In case of business combination achieved in phases, the fair value of equity

interest held previously in the acquireee on the part of the acquirer at the fair

value of the date it is acquired

ii. The net of the amounts related to identifiable amounts acquired along with the

projected liabilities in accordance with the standard (Aasb.gov.au 2019)

For instance, an assumption is made that the business has been commenced by

JKY Limited on 1/5/2018 where there is investment amount of $20,000,000. The

following journal entry is passed below:

After one year, an investment amount of $10,000,000 has been made by JKY

Limited for purchasing all shares of FAB Limited. Under such situation, the following

journal entry would be passed:

As a result, JKY Limited would have cash balance of $10,000,000, while the

asset would be $20,000,000. The transaction would be disclosed in the books of FAB

Limited as follows:

At the end of the accounting year, the consolidated financial statement would be

represented as follows:

5CORPORATE AND FINANCIAL ACCOUNTING

Equity accounting method:

The method is used primarily to assess the profit earned from investments made

by an entity in other entities (Balakrishnan, Wattsand Zuo 2016). This income is

reported on the income statement by taking into account the size of equity investment.

It is apparent from “Paragraph 10 of AASB 128” that cost basis should be used for

recognition of investment initially and the carrying amount might fluctuate when it

comes to the realisation of share of profit or loss of the investor after the date of

acquisition (Aasb.gov.au 2019). In order to realise goodwill, the use of fair value

pertaining to the equity interests of the acquiree is made at the acquired date, instead

of the fair value associated with the interests of the transferred equity at the period they

are acquired, as per “Paragraph 33 of AASB 3” (Aasb.gov.au, 2019).

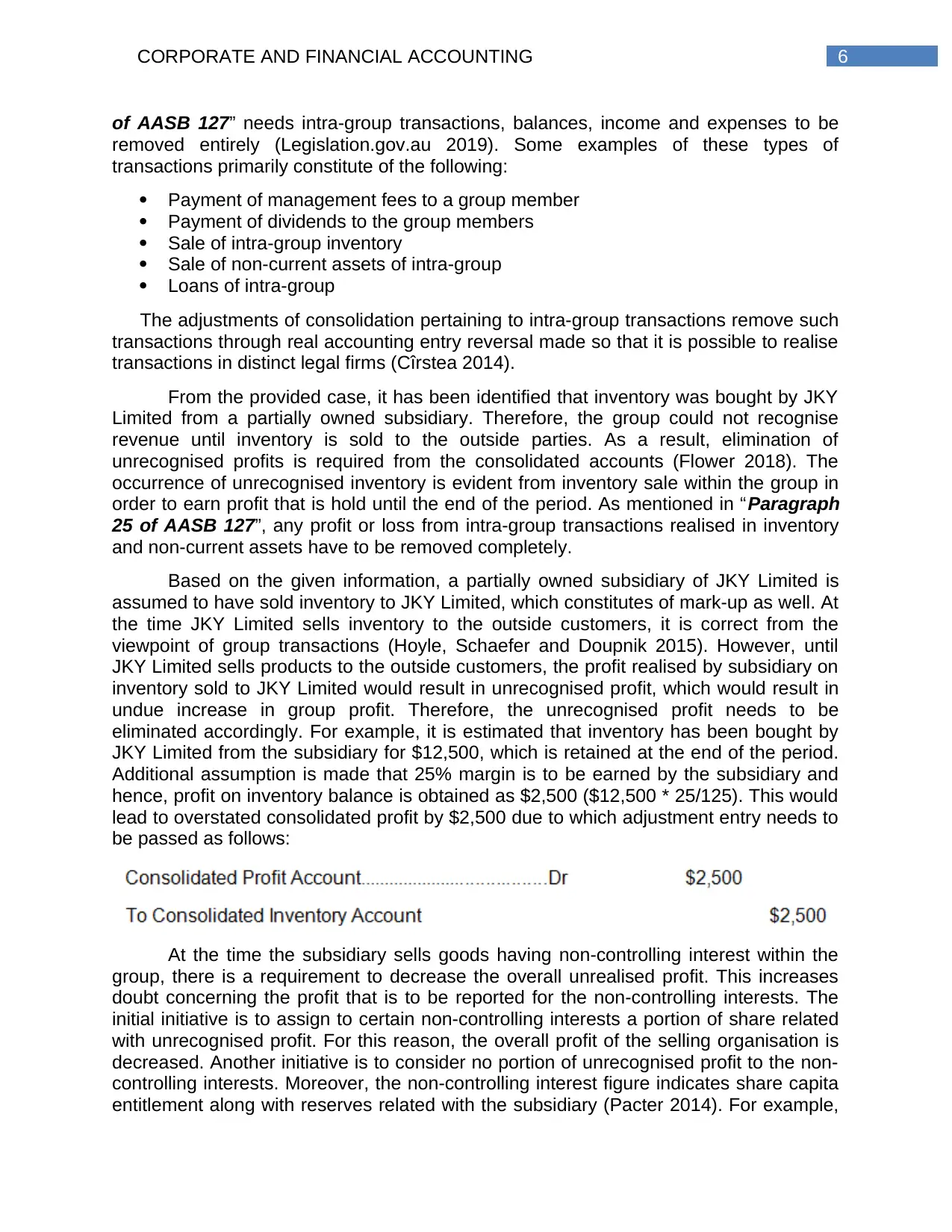

For instance, an assumption is made that 30% of the shares of FAB Limited are

acquired by JKY Limited by considering the fact that FAB Limited has disclosed profit

after tax of $100,000 and dividends of $50,000. At the time of share purchase, the

following journal entry needs to be passed at cost value:

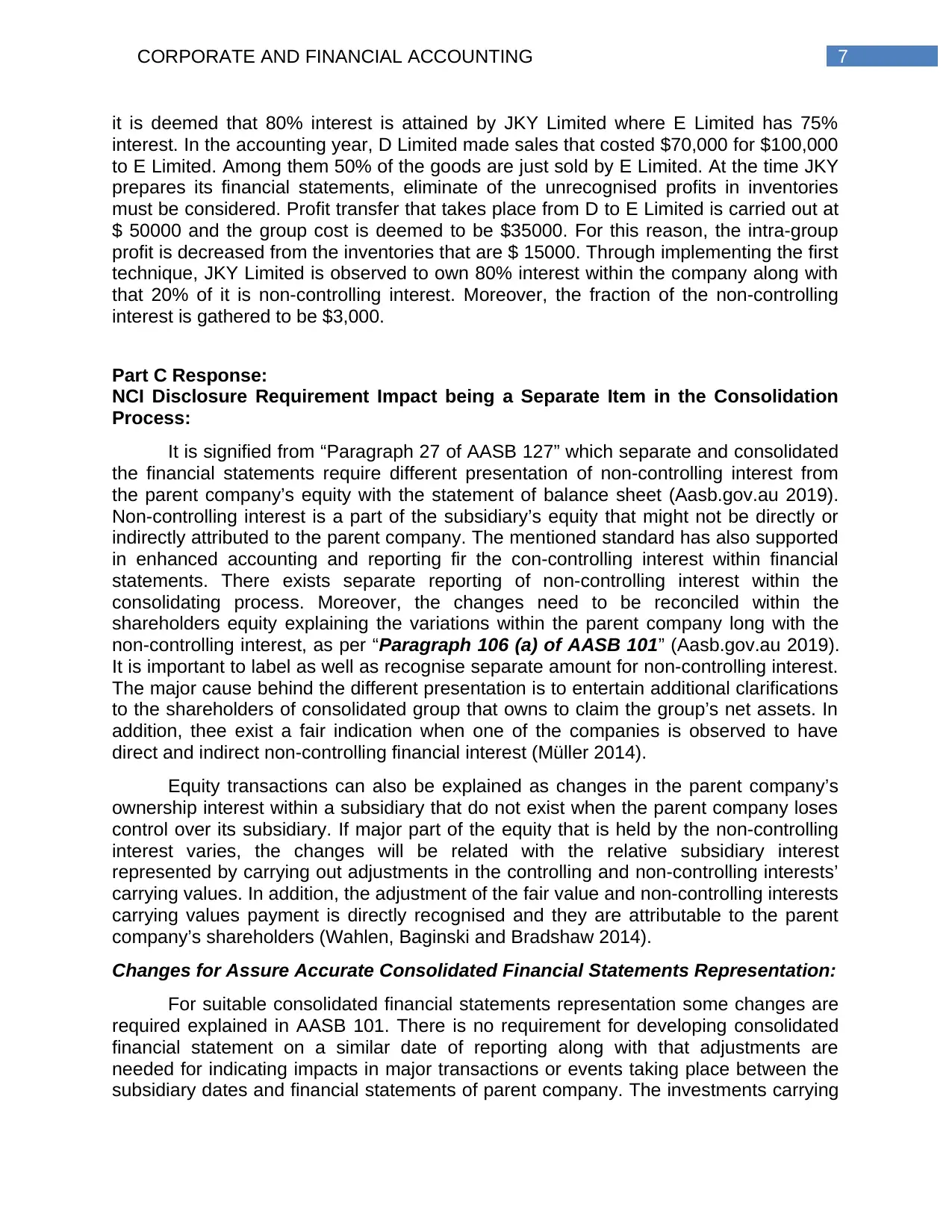

As $15,000 dividend would be received by JKY Limited, the investment account

value would be reduced.

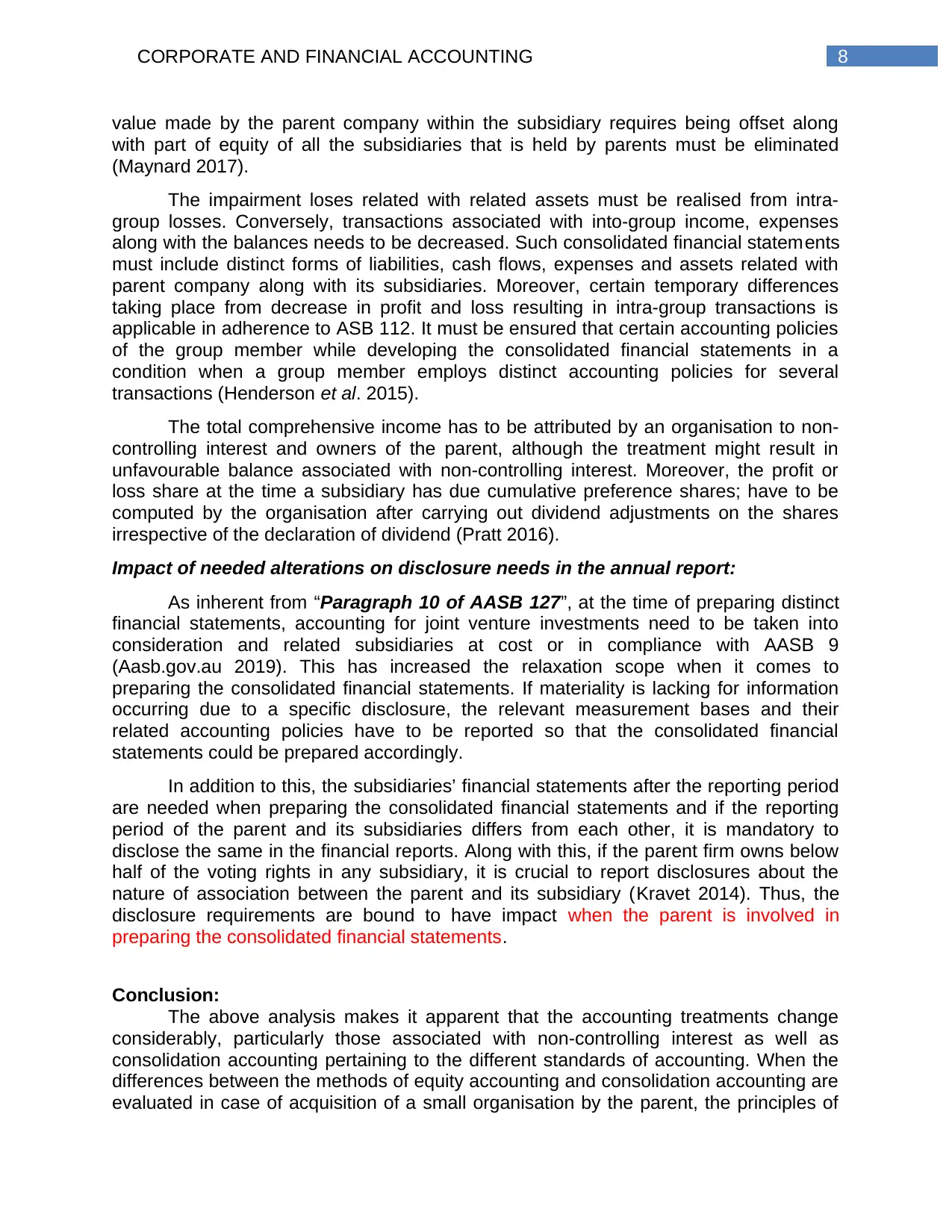

Lastly, JKY Limited is needed to record profit after tax of FAB Limited in the form

of increase in investment account.

Part B Response:

During the financial year, it is evident for the distinct legal firms within an

economic entity in order to make transactions with each other. For consolidated account

preparation, the effect of all transactions between companies within the parent is

removed entirely even during the period the parent entity holds a portion of issued

equity as well (Chambers2014). In this regard, it needs to be noted that “Paragraph 29

Equity accounting method:

The method is used primarily to assess the profit earned from investments made

by an entity in other entities (Balakrishnan, Wattsand Zuo 2016). This income is

reported on the income statement by taking into account the size of equity investment.

It is apparent from “Paragraph 10 of AASB 128” that cost basis should be used for

recognition of investment initially and the carrying amount might fluctuate when it

comes to the realisation of share of profit or loss of the investor after the date of

acquisition (Aasb.gov.au 2019). In order to realise goodwill, the use of fair value

pertaining to the equity interests of the acquiree is made at the acquired date, instead

of the fair value associated with the interests of the transferred equity at the period they

are acquired, as per “Paragraph 33 of AASB 3” (Aasb.gov.au, 2019).

For instance, an assumption is made that 30% of the shares of FAB Limited are

acquired by JKY Limited by considering the fact that FAB Limited has disclosed profit

after tax of $100,000 and dividends of $50,000. At the time of share purchase, the

following journal entry needs to be passed at cost value:

As $15,000 dividend would be received by JKY Limited, the investment account

value would be reduced.

Lastly, JKY Limited is needed to record profit after tax of FAB Limited in the form

of increase in investment account.

Part B Response:

During the financial year, it is evident for the distinct legal firms within an

economic entity in order to make transactions with each other. For consolidated account

preparation, the effect of all transactions between companies within the parent is

removed entirely even during the period the parent entity holds a portion of issued

equity as well (Chambers2014). In this regard, it needs to be noted that “Paragraph 29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

of AASB 127” needs intra-group transactions, balances, income and expenses to be

removed entirely (Legislation.gov.au 2019). Some examples of these types of

transactions primarily constitute of the following:

Payment of management fees to a group member

Payment of dividends to the group members

Sale of intra-group inventory

Sale of non-current assets of intra-group

Loans of intra-group

The adjustments of consolidation pertaining to intra-group transactions remove such

transactions through real accounting entry reversal made so that it is possible to realise

transactions in distinct legal firms (Cîrstea 2014).

From the provided case, it has been identified that inventory was bought by JKY

Limited from a partially owned subsidiary. Therefore, the group could not recognise

revenue until inventory is sold to the outside parties. As a result, elimination of

unrecognised profits is required from the consolidated accounts (Flower 2018). The

occurrence of unrecognised inventory is evident from inventory sale within the group in

order to earn profit that is hold until the end of the period. As mentioned in “Paragraph

25 of AASB 127”, any profit or loss from intra-group transactions realised in inventory

and non-current assets have to be removed completely.

Based on the given information, a partially owned subsidiary of JKY Limited is

assumed to have sold inventory to JKY Limited, which constitutes of mark-up as well. At

the time JKY Limited sells inventory to the outside customers, it is correct from the

viewpoint of group transactions (Hoyle, Schaefer and Doupnik 2015). However, until

JKY Limited sells products to the outside customers, the profit realised by subsidiary on

inventory sold to JKY Limited would result in unrecognised profit, which would result in

undue increase in group profit. Therefore, the unrecognised profit needs to be

eliminated accordingly. For example, it is estimated that inventory has been bought by

JKY Limited from the subsidiary for $12,500, which is retained at the end of the period.

Additional assumption is made that 25% margin is to be earned by the subsidiary and

hence, profit on inventory balance is obtained as $2,500 ($12,500 * 25/125). This would

lead to overstated consolidated profit by $2,500 due to which adjustment entry needs to

be passed as follows:

At the time the subsidiary sells goods having non-controlling interest within the

group, there is a requirement to decrease the overall unrealised profit. This increases

doubt concerning the profit that is to be reported for the non-controlling interests. The

initial initiative is to assign to certain non-controlling interests a portion of share related

with unrecognised profit. For this reason, the overall profit of the selling organisation is

decreased. Another initiative is to consider no portion of unrecognised profit to the non-

controlling interests. Moreover, the non-controlling interest figure indicates share capita

entitlement along with reserves related with the subsidiary (Pacter 2014). For example,

of AASB 127” needs intra-group transactions, balances, income and expenses to be

removed entirely (Legislation.gov.au 2019). Some examples of these types of

transactions primarily constitute of the following:

Payment of management fees to a group member

Payment of dividends to the group members

Sale of intra-group inventory

Sale of non-current assets of intra-group

Loans of intra-group

The adjustments of consolidation pertaining to intra-group transactions remove such

transactions through real accounting entry reversal made so that it is possible to realise

transactions in distinct legal firms (Cîrstea 2014).

From the provided case, it has been identified that inventory was bought by JKY

Limited from a partially owned subsidiary. Therefore, the group could not recognise

revenue until inventory is sold to the outside parties. As a result, elimination of

unrecognised profits is required from the consolidated accounts (Flower 2018). The

occurrence of unrecognised inventory is evident from inventory sale within the group in

order to earn profit that is hold until the end of the period. As mentioned in “Paragraph

25 of AASB 127”, any profit or loss from intra-group transactions realised in inventory

and non-current assets have to be removed completely.

Based on the given information, a partially owned subsidiary of JKY Limited is

assumed to have sold inventory to JKY Limited, which constitutes of mark-up as well. At

the time JKY Limited sells inventory to the outside customers, it is correct from the

viewpoint of group transactions (Hoyle, Schaefer and Doupnik 2015). However, until

JKY Limited sells products to the outside customers, the profit realised by subsidiary on

inventory sold to JKY Limited would result in unrecognised profit, which would result in

undue increase in group profit. Therefore, the unrecognised profit needs to be

eliminated accordingly. For example, it is estimated that inventory has been bought by

JKY Limited from the subsidiary for $12,500, which is retained at the end of the period.

Additional assumption is made that 25% margin is to be earned by the subsidiary and

hence, profit on inventory balance is obtained as $2,500 ($12,500 * 25/125). This would

lead to overstated consolidated profit by $2,500 due to which adjustment entry needs to

be passed as follows:

At the time the subsidiary sells goods having non-controlling interest within the

group, there is a requirement to decrease the overall unrealised profit. This increases

doubt concerning the profit that is to be reported for the non-controlling interests. The

initial initiative is to assign to certain non-controlling interests a portion of share related

with unrecognised profit. For this reason, the overall profit of the selling organisation is

decreased. Another initiative is to consider no portion of unrecognised profit to the non-

controlling interests. Moreover, the non-controlling interest figure indicates share capita

entitlement along with reserves related with the subsidiary (Pacter 2014). For example,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

it is deemed that 80% interest is attained by JKY Limited where E Limited has 75%

interest. In the accounting year, D Limited made sales that costed $70,000 for $100,000

to E Limited. Among them 50% of the goods are just sold by E Limited. At the time JKY

prepares its financial statements, eliminate of the unrecognised profits in inventories

must be considered. Profit transfer that takes place from D to E Limited is carried out at

$ 50000 and the group cost is deemed to be $35000. For this reason, the intra-group

profit is decreased from the inventories that are $ 15000. Through implementing the first

technique, JKY Limited is observed to own 80% interest within the company along with

that 20% of it is non-controlling interest. Moreover, the fraction of the non-controlling

interest is gathered to be $3,000.

Part C Response:

NCI Disclosure Requirement Impact being a Separate Item in the Consolidation

Process:

It is signified from “Paragraph 27 of AASB 127” which separate and consolidated

the financial statements require different presentation of non-controlling interest from

the parent company’s equity with the statement of balance sheet (Aasb.gov.au 2019).

Non-controlling interest is a part of the subsidiary’s equity that might not be directly or

indirectly attributed to the parent company. The mentioned standard has also supported

in enhanced accounting and reporting fir the con-controlling interest within financial

statements. There exists separate reporting of non-controlling interest within the

consolidating process. Moreover, the changes need to be reconciled within the

shareholders equity explaining the variations within the parent company long with the

non-controlling interest, as per “Paragraph 106 (a) of AASB 101” (Aasb.gov.au 2019).

It is important to label as well as recognise separate amount for non-controlling interest.

The major cause behind the different presentation is to entertain additional clarifications

to the shareholders of consolidated group that owns to claim the group’s net assets. In

addition, thee exist a fair indication when one of the companies is observed to have

direct and indirect non-controlling financial interest (Müller 2014).

Equity transactions can also be explained as changes in the parent company’s

ownership interest within a subsidiary that do not exist when the parent company loses

control over its subsidiary. If major part of the equity that is held by the non-controlling

interest varies, the changes will be related with the relative subsidiary interest

represented by carrying out adjustments in the controlling and non-controlling interests’

carrying values. In addition, the adjustment of the fair value and non-controlling interests

carrying values payment is directly recognised and they are attributable to the parent

company’s shareholders (Wahlen, Baginski and Bradshaw 2014).

Changes for Assure Accurate Consolidated Financial Statements Representation:

For suitable consolidated financial statements representation some changes are

required explained in AASB 101. There is no requirement for developing consolidated

financial statement on a similar date of reporting along with that adjustments are

needed for indicating impacts in major transactions or events taking place between the

subsidiary dates and financial statements of parent company. The investments carrying

it is deemed that 80% interest is attained by JKY Limited where E Limited has 75%

interest. In the accounting year, D Limited made sales that costed $70,000 for $100,000

to E Limited. Among them 50% of the goods are just sold by E Limited. At the time JKY

prepares its financial statements, eliminate of the unrecognised profits in inventories

must be considered. Profit transfer that takes place from D to E Limited is carried out at

$ 50000 and the group cost is deemed to be $35000. For this reason, the intra-group

profit is decreased from the inventories that are $ 15000. Through implementing the first

technique, JKY Limited is observed to own 80% interest within the company along with

that 20% of it is non-controlling interest. Moreover, the fraction of the non-controlling

interest is gathered to be $3,000.

Part C Response:

NCI Disclosure Requirement Impact being a Separate Item in the Consolidation

Process:

It is signified from “Paragraph 27 of AASB 127” which separate and consolidated

the financial statements require different presentation of non-controlling interest from

the parent company’s equity with the statement of balance sheet (Aasb.gov.au 2019).

Non-controlling interest is a part of the subsidiary’s equity that might not be directly or

indirectly attributed to the parent company. The mentioned standard has also supported

in enhanced accounting and reporting fir the con-controlling interest within financial

statements. There exists separate reporting of non-controlling interest within the

consolidating process. Moreover, the changes need to be reconciled within the

shareholders equity explaining the variations within the parent company long with the

non-controlling interest, as per “Paragraph 106 (a) of AASB 101” (Aasb.gov.au 2019).

It is important to label as well as recognise separate amount for non-controlling interest.

The major cause behind the different presentation is to entertain additional clarifications

to the shareholders of consolidated group that owns to claim the group’s net assets. In

addition, thee exist a fair indication when one of the companies is observed to have

direct and indirect non-controlling financial interest (Müller 2014).

Equity transactions can also be explained as changes in the parent company’s

ownership interest within a subsidiary that do not exist when the parent company loses

control over its subsidiary. If major part of the equity that is held by the non-controlling

interest varies, the changes will be related with the relative subsidiary interest

represented by carrying out adjustments in the controlling and non-controlling interests’

carrying values. In addition, the adjustment of the fair value and non-controlling interests

carrying values payment is directly recognised and they are attributable to the parent

company’s shareholders (Wahlen, Baginski and Bradshaw 2014).

Changes for Assure Accurate Consolidated Financial Statements Representation:

For suitable consolidated financial statements representation some changes are

required explained in AASB 101. There is no requirement for developing consolidated

financial statement on a similar date of reporting along with that adjustments are

needed for indicating impacts in major transactions or events taking place between the

subsidiary dates and financial statements of parent company. The investments carrying

8CORPORATE AND FINANCIAL ACCOUNTING

value made by the parent company within the subsidiary requires being offset along

with part of equity of all the subsidiaries that is held by parents must be eliminated

(Maynard 2017).

The impairment loses related with related assets must be realised from intra-

group losses. Conversely, transactions associated with into-group income, expenses

along with the balances needs to be decreased. Such consolidated financial statements

must include distinct forms of liabilities, cash flows, expenses and assets related with

parent company along with its subsidiaries. Moreover, certain temporary differences

taking place from decrease in profit and loss resulting in intra-group transactions is

applicable in adherence to ASB 112. It must be ensured that certain accounting policies

of the group member while developing the consolidated financial statements in a

condition when a group member employs distinct accounting policies for several

transactions (Henderson et al. 2015).

The total comprehensive income has to be attributed by an organisation to non-

controlling interest and owners of the parent, although the treatment might result in

unfavourable balance associated with non-controlling interest. Moreover, the profit or

loss share at the time a subsidiary has due cumulative preference shares; have to be

computed by the organisation after carrying out dividend adjustments on the shares

irrespective of the declaration of dividend (Pratt 2016).

Impact of needed alterations on disclosure needs in the annual report:

As inherent from “Paragraph 10 of AASB 127”, at the time of preparing distinct

financial statements, accounting for joint venture investments need to be taken into

consideration and related subsidiaries at cost or in compliance with AASB 9

(Aasb.gov.au 2019). This has increased the relaxation scope when it comes to

preparing the consolidated financial statements. If materiality is lacking for information

occurring due to a specific disclosure, the relevant measurement bases and their

related accounting policies have to be reported so that the consolidated financial

statements could be prepared accordingly.

In addition to this, the subsidiaries’ financial statements after the reporting period

are needed when preparing the consolidated financial statements and if the reporting

period of the parent and its subsidiaries differs from each other, it is mandatory to

disclose the same in the financial reports. Along with this, if the parent firm owns below

half of the voting rights in any subsidiary, it is crucial to report disclosures about the

nature of association between the parent and its subsidiary (Kravet 2014). Thus, the

disclosure requirements are bound to have impact when the parent is involved in

preparing the consolidated financial statements.

Conclusion:

The above analysis makes it apparent that the accounting treatments change

considerably, particularly those associated with non-controlling interest as well as

consolidation accounting pertaining to the different standards of accounting. When the

differences between the methods of equity accounting and consolidation accounting are

evaluated in case of acquisition of a small organisation by the parent, the principles of

value made by the parent company within the subsidiary requires being offset along

with part of equity of all the subsidiaries that is held by parents must be eliminated

(Maynard 2017).

The impairment loses related with related assets must be realised from intra-

group losses. Conversely, transactions associated with into-group income, expenses

along with the balances needs to be decreased. Such consolidated financial statements

must include distinct forms of liabilities, cash flows, expenses and assets related with

parent company along with its subsidiaries. Moreover, certain temporary differences

taking place from decrease in profit and loss resulting in intra-group transactions is

applicable in adherence to ASB 112. It must be ensured that certain accounting policies

of the group member while developing the consolidated financial statements in a

condition when a group member employs distinct accounting policies for several

transactions (Henderson et al. 2015).

The total comprehensive income has to be attributed by an organisation to non-

controlling interest and owners of the parent, although the treatment might result in

unfavourable balance associated with non-controlling interest. Moreover, the profit or

loss share at the time a subsidiary has due cumulative preference shares; have to be

computed by the organisation after carrying out dividend adjustments on the shares

irrespective of the declaration of dividend (Pratt 2016).

Impact of needed alterations on disclosure needs in the annual report:

As inherent from “Paragraph 10 of AASB 127”, at the time of preparing distinct

financial statements, accounting for joint venture investments need to be taken into

consideration and related subsidiaries at cost or in compliance with AASB 9

(Aasb.gov.au 2019). This has increased the relaxation scope when it comes to

preparing the consolidated financial statements. If materiality is lacking for information

occurring due to a specific disclosure, the relevant measurement bases and their

related accounting policies have to be reported so that the consolidated financial

statements could be prepared accordingly.

In addition to this, the subsidiaries’ financial statements after the reporting period

are needed when preparing the consolidated financial statements and if the reporting

period of the parent and its subsidiaries differs from each other, it is mandatory to

disclose the same in the financial reports. Along with this, if the parent firm owns below

half of the voting rights in any subsidiary, it is crucial to report disclosures about the

nature of association between the parent and its subsidiary (Kravet 2014). Thus, the

disclosure requirements are bound to have impact when the parent is involved in

preparing the consolidated financial statements.

Conclusion:

The above analysis makes it apparent that the accounting treatments change

considerably, particularly those associated with non-controlling interest as well as

consolidation accounting pertaining to the different standards of accounting. When the

differences between the methods of equity accounting and consolidation accounting are

evaluated in case of acquisition of a small organisation by the parent, the principles of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

recognition and bases of measurement vary from organisation to organisation. In

addition, the intra-group transactions have significant variations in terms of treatment in

the consolidated financial statements of both the firms. Finally, it has been assessed

that the disclosure requirements needing non-controlling interests in the form of a

distinct item in the consolidated financial reports has considerable effect on the entire

process of consolidation.

recognition and bases of measurement vary from organisation to organisation. In

addition, the intra-group transactions have significant variations in terms of treatment in

the consolidated financial statements of both the firms. Finally, it has been assessed

that the disclosure requirements needing non-controlling interests in the form of a

distinct item in the consolidated financial reports has considerable effect on the entire

process of consolidation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

References:

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 18 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 18

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 18

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 18 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 18

May 2019].

Aletkin, P.A., 2014. International financial reporting standards implementation into the

Russian accounting system. Mediterranean Journal of Social Sciences, 5(24), p.33

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Chambers, R.L. ed., 2014. An accounting thesaurus: 500 years of accounting. Elsevier.

Cîrstea, A., 2014. The need for public sector consolidated financial

statements. Procedia Economics and Finance, 15, pp.1289-1296.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kravet, T.D., 2014. Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2-3), pp.218-240.

Legislation.gov.au., 2019. AASB 127 - Consolidated and Separate Financial Statements

- July 2004. [online] Available at: https://www.legislation.gov.au/Details/F2009C01112

[Accessed 4 May 2019].

References:

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 18 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 18

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 18

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 18 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 18

May 2019].

Aletkin, P.A., 2014. International financial reporting standards implementation into the

Russian accounting system. Mediterranean Journal of Social Sciences, 5(24), p.33

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Chambers, R.L. ed., 2014. An accounting thesaurus: 500 years of accounting. Elsevier.

Cîrstea, A., 2014. The need for public sector consolidated financial

statements. Procedia Economics and Finance, 15, pp.1289-1296.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kravet, T.D., 2014. Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2-3), pp.218-240.

Legislation.gov.au., 2019. AASB 127 - Consolidated and Separate Financial Statements

- July 2004. [online] Available at: https://www.legislation.gov.au/Details/F2009C01112

[Accessed 4 May 2019].

11CORPORATE AND FINANCIAL ACCOUNTING

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University

Press.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Pacter, P., 2014. Global accounting standards-From Vision to reality. Professional

Accountant, 2014(1), pp.26-27.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University

Press.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Pacter, P., 2014. Global accounting standards-From Vision to reality. Professional

Accountant, 2014(1), pp.26-27.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.